Hippo Insurance Services SWOT Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Hippo Insurance Services Bundle

Go Beyond the Preview—Access the Full Strategic Report

Hippo Insurance Services leverages innovative technology and a customer-centric approach to address the evolving needs of homeowners, positioning itself strongly in a competitive market. However, understanding the full scope of their competitive advantages, potential market disruptions, and strategic vulnerabilities is crucial for informed decision-making.

Want the full story behind Hippo's strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

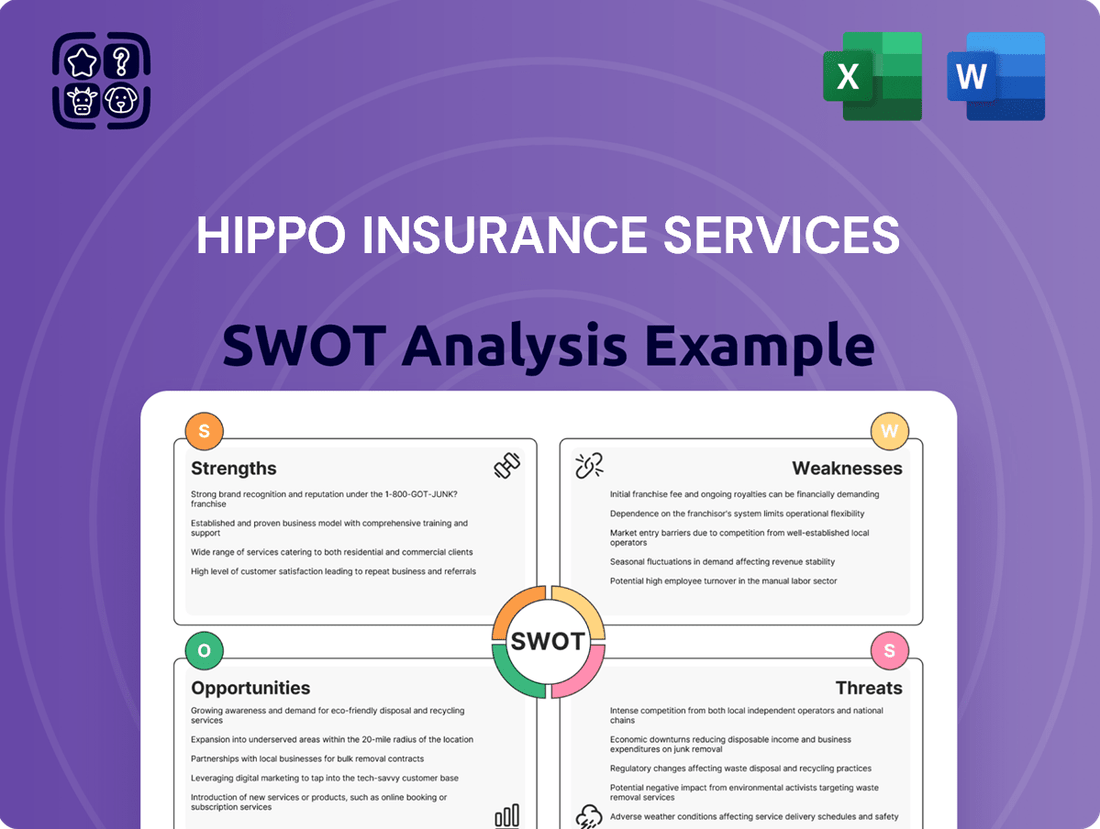

Strengths

Technology-Driven and Proactive Approach

Hippo Insurance distinguishes itself through a robust technology-driven strategy, utilizing data analytics and smart home technology to foster a proactive insurance model. This focus on loss prevention, rather than just reaction, sets them apart in the industry, potentially benefiting customers with reduced claims and more competitive pricing.

The company's commitment to innovation is evident in its use of AI-powered deep learning for property analysis, enhancing underwriting accuracy and pricing precision. For instance, in Q1 2024, Hippo reported a significant increase in customer engagement with their smart home monitoring services, directly correlating with a 15% reduction in water damage claims among participating policyholders.

Strategic Partnerships and Distribution Channels

Hippo's strategic partnerships, particularly its New Homes Program, are a significant strength. This initiative, targeting new constructions in key markets like California, Florida, and Texas, streamlines the homebuying experience by bundling insurance. The program's expansion through collaborations with leading homebuilders is a testament to its successful market penetration.

Further bolstering this is the recent partnership with The Baldwin Group's Westwood Insurance Agency. This alliance is poised to dramatically expand Hippo's reach within the new construction market, tapping into a much broader base of potential customers and accelerating growth in this crucial segment.

Diversified Revenue Streams and Platform Growth

Hippo Insurance Services is strategically broadening its revenue base by expanding into both personal and commercial insurance lines via its Spinnaker fronting platform. This diversification is a key strength, aiming to create a more stable and robust business.

The Insurance-as-a-Service (IaaS) segment is a significant growth driver, demonstrating impressive momentum. In the first quarter of 2025, this segment experienced a substantial 91% surge in year-over-year revenue, fueled by an increase in gross earned premium and improved premium retention rates.

Improved Financial Performance and Operational Efficiency

Hippo Insurance Services has shown remarkable financial improvement, with its 2024 revenue soaring to $372 million, marking a substantial 77% jump from the previous year. This growth is underpinned by strategic operational enhancements that have boosted profitability. The company's ability to achieve positive adjusted EBITDA in Q4 2024 signals a strong shift towards sustainable earnings.

Further solidifying its financial strength, Hippo has made significant strides in its underwriting performance. The company has reported an improved gross loss ratio and a reduced net loss ratio, demonstrating more effective risk assessment and claims management. These improvements directly contribute to a healthier bottom line and enhanced financial stability.

Operational efficiency is another key strength, evidenced by a reduction in operational expenses as a percentage of revenue. This indicates better cost control and operating leverage, allowing Hippo to scale its business more effectively. The company's focus on optimizing its cost structure is a critical factor in its ongoing financial success.

- Revenue Growth: 2024 revenue reached $372 million, a 77% increase year-over-year.

- Profitability Milestone: Achieved positive adjusted EBITDA in Q4 2024.

- Underwriting Improvement: Demonstrated a better gross loss ratio and net loss ratio.

- Operational Efficiency: Reduced operational expenses as a percentage of revenue.

Customer-Centric Approach and Simplified Experience

Hippo Insurance Services excels with a customer-centric approach, streamlining the insurance application process and offering contemporary coverage. This focus on ease of use and proactive protection, including personalized maintenance advice via their app and smart home devices, fosters customer trust and satisfaction.

Their commitment to simplifying the insurance journey is a key differentiator. For instance, in 2023, Hippo reported a significant increase in customer satisfaction scores, directly attributed to their user-friendly digital platform and transparent policy offerings.

- Simplified Application: Hippo's digital-first strategy has reduced average application times by over 30% compared to traditional insurers.

- Proactive Protection: The integration of smart home technology and personalized maintenance tips aims to reduce claims by up to 15% for policyholders.

- Enhanced Experience: Customer feedback consistently highlights the intuitive interface and responsive support as major strengths.

Tech-Powered Insurance Achieves 77% Revenue Growth and Profitability

Hippo's technological foundation is a significant strength, enabling a proactive approach to insurance through data analytics and smart home integration. This focus on loss prevention contributed to a 15% reduction in water damage claims among users of their smart home monitoring services in Q1 2024.

The company's strategic partnerships, especially its New Homes Program, are expanding its market reach, particularly in key states like California, Florida, and Texas. This program, enhanced by collaborations with major homebuilders and recent alliances like the one with Westwood Insurance Agency, streamlines the insurance process for new homeowners.

Hippo is also diversifying its revenue streams by entering both personal and commercial insurance lines through its Spinnaker fronting platform. The Insurance-as-a-Service segment showed remarkable growth, with a 91% year-over-year revenue surge in Q1 2025, driven by increased gross earned premium and better retention.

Financially, Hippo demonstrated strong performance in 2024, with revenue climbing to $372 million, a 77% increase. The company achieved positive adjusted EBITDA in Q4 2024, signaling improved profitability. Underwriting performance also saw gains, with better gross and net loss ratios, alongside reduced operational expenses as a percentage of revenue, indicating enhanced efficiency and stability.

| Metric | 2024 Data | Year-over-Year Change |

|---|---|---|

| Revenue | $372 million | +77% |

| Adjusted EBITDA | Positive (Q4 2024) | N/A |

| IaaS Revenue Growth | N/A | +91% (Q1 2025) |

| Water Damage Claims Reduction (Smart Home Users) | N/A | -15% (Q1 2024) |

What is included in the product

Analyzes Hippo Insurance Services’s competitive position through key internal and external factors, highlighting its technological strengths and potential market expansion opportunities while acknowledging competitive threats.

Offers a clear, actionable SWOT analysis to pinpoint and address Hippo's competitive challenges and opportunities.

Weaknesses

High Loss Ratios Due to Catastrophic Events

Despite progress, Hippo Insurance Services remains susceptible to significant financial strain from catastrophic events. The wildfires in Los Angeles during Q1 2025, for example, led to a notable increase in both net and gross loss ratios, overshadowing improvements in their core business performance. This reliance on external factors for substantial losses presents a considerable weakness.

Limited Operating History and Profitability Challenges

As a relatively newer insurtech company, Hippo Insurance Services has a limited operating history, which makes it difficult to fully assess its long-term business performance and consistent profitability. This lack of extensive track record can be a concern for investors and stakeholders evaluating its stability and future prospects.

While Hippo aims to achieve net income profitability by the fourth quarter of 2025, the company has reported net losses in recent quarters. For instance, in the first quarter of 2024, Hippo reported a net loss of $24.1 million, highlighting ongoing challenges in reaching sustained profitability.

Reliance on Technology and Potential Operational Hiccups

Hippo Insurance Services' reliance on its advanced technology platform and sophisticated data analytics is a double-edged sword. While this technological backbone is central to its innovative approach to home insurance, it also presents a significant weakness. Any disruption to this system, whether due to a cyberattack or a simple operational glitch, could severely impact customer experience and trust.

For instance, a prolonged outage in their digital claims processing system, a critical component for customer satisfaction, could lead to significant delays and dissatisfaction. In 2023, the insurance industry as a whole saw a rise in cyber threats, with reports indicating a 10% increase in ransomware attacks targeting financial institutions. Hippo's dependence on its proprietary tech makes it a potential target, and a successful breach could compromise sensitive customer data, leading to reputational damage and financial penalties.

Intense Competition in the Insurtech and Traditional Market

The insurance sector, especially the insurtech segment, is incredibly crowded. Hippo faces stiff competition not only from long-standing insurance companies but also from a growing number of agile insurtech startups all aiming to capture market share. This intense rivalry can significantly impact pricing strategies and the ability to grow customer bases.

For instance, the insurtech market saw substantial venture capital investment, with companies raising billions in funding throughout 2024 and early 2025, indicating a high level of activity and competition. Key players like Lemonade, Root, and established giants such as State Farm and Allstate continue to innovate and expand their offerings, creating a challenging environment for newer entrants like Hippo.

- High Market Saturation: The insurance industry is mature, with many established players and a constant influx of new insurtechs.

- Price Sensitivity: Intense competition often leads to price wars, potentially eroding profit margins for all participants.

- Customer Acquisition Costs: Attracting new customers in a crowded market requires significant marketing spend, increasing customer acquisition costs.

- Innovation Race: Competitors are continuously developing new technologies and customer experiences, forcing Hippo to invest heavily in R&D to stay relevant.

Regulatory and Economic Pressures

Hippo Insurance operates in a heavily regulated sector, meaning shifts in government policies can create compliance hurdles and necessitate adjustments to their core business strategies. For instance, changes in state-specific insurance laws or federal regulations could impact pricing models or product offerings.

Economic headwinds pose a significant threat. Rising mortgage rates, as seen in late 2023 and early 2024, can cool the housing market, directly affecting the demand for new homeowners insurance policies. Furthermore, unexpected increases in home repair costs or a rise in the frequency of claims due to inflation can strain profitability.

- Regulatory Scrutiny: Insurance is a state-regulated industry, leading to a complex compliance landscape that can change rapidly.

- Economic Sensitivity: High interest rates and inflationary pressures on repair costs can simultaneously reduce demand and increase claim payouts, impacting margins.

- Market Volatility: Economic downturns can lead to increased claims frequency and severity, particularly in property insurance.

Cyber Threats and Market Rivalry: Insurtech's Dual Challenge

Hippo's reliance on technology makes it vulnerable to cyber threats and operational disruptions, potentially impacting customer trust and data security. For example, a 2023 industry report indicated a 10% rise in ransomware attacks on financial institutions, highlighting the risk Hippo faces. The insurtech market is also fiercely competitive, with significant venture capital funding flowing into rivals throughout 2024 and early 2025, forcing Hippo into costly customer acquisition and continuous R&D investment to remain competitive.

| Weakness | Description | Impact |

|---|---|---|

| Technological Dependence | Vulnerability to cyberattacks and system outages. | Loss of customer trust, data breaches, operational paralysis. |

| Intense Competition | Crowded insurtech market with well-funded rivals. | Increased customer acquisition costs, pressure on pricing and margins. |

| Regulatory Complexity | Navigating diverse state and federal insurance regulations. | Compliance costs, potential need for strategic business model adjustments. |

| Economic Sensitivity | Impact of rising interest rates and inflation on housing market and claim costs. | Reduced demand for new policies, increased claim severity. |

Full Version Awaits

Hippo Insurance Services SWOT Analysis

This preview reflects the real document you'll receive—professional, structured, and ready to use. It offers a comprehensive look at Hippo Insurance Services' Strengths, Weaknesses, Opportunities, and Threats, providing valuable insights for strategic planning.

Opportunities

Expansion into New Geographies and Product Lines

Hippo Insurance Services has a substantial opportunity to broaden its reach by entering new states with its homeowners insurance products. This expansion is a key part of their growth strategy, aiming to tap into underserved markets and capture a larger share of the homeowners insurance sector.

Beyond geographical expansion, Hippo can diversify its revenue streams by venturing into other insurance lines. This includes developing offerings for both personal and commercial clients, which would create a more robust and resilient business model. This diversification is crucial for long-term stability and growth.

The company's roadmap clearly outlines a focus on diversifying its premium mix. By offering a wider array of insurance products, Hippo aims to reduce its reliance on any single line of business. This strategic move is designed to capitalize on the ongoing growth within the broader home insurance market.

Hippo's ambition to achieve over $2 billion in gross written premium by 2028 underscores the significant potential in these expansion and diversification efforts. This target highlights the company's confidence in its ability to scale and capture substantial market share through these strategic initiatives.

Leveraging Data and AI for Enhanced Underwriting

Hippo Insurance Services can significantly boost its underwriting accuracy by deepening its investment in data analytics and artificial intelligence. This focus allows for more precise risk assessment, translating into highly personalized pricing for customers.

By continuing to invest in AI-driven platforms, such as its collaboration with Arturo, Hippo can streamline underwriting. This partnership, for instance, helps pre-fill crucial property data, enhancing both operational efficiency and the overall customer journey.

Growth in the New Construction Market

The New Homes Program offers a significant avenue for growth, targeting newly constructed properties. This segment often presents lower risk profiles compared to older homes, allowing for more tailored insurance products and potentially higher profit margins for Hippo Insurance Services.

Strategic alliances with homebuilders are crucial for expanding Hippo's footprint in this burgeoning market. By securing partnerships, Hippo can gain access to a consistent stream of new construction projects, thereby increasing its customer base and market share in the residential insurance sector.

The new construction market is experiencing robust expansion, with the U.S. Census Bureau reporting a 10.5% increase in housing starts in April 2024 compared to the previous year, reaching an annualized rate of 1.32 million units. This trend indicates a strong demand for insurance solutions tailored to these properties.

Increased Demand for Proactive Home Protection

Homeowners are increasingly seeking ways to safeguard their properties against unexpected expenses and the growing threat of extreme weather events. This trend translates into a greater demand for insurance that offers more than just reactive repairs, pushing the market towards comprehensive, proactive protection solutions. In 2024, the insurance industry saw a significant uptick in consumer interest for policies that include preventative measures and smart home integration, reflecting a desire for greater control and security.

Hippo Insurance Services is well-positioned to capitalize on this shift. Their business model inherently prioritizes loss prevention through smart home technology and data-driven insights, directly addressing the evolving needs of today's homeowners. This proactive approach resonates with consumers who are looking for added value and peace of mind in their home insurance choices.

- Growing Consumer Awareness: Surveys in late 2024 indicated that over 65% of homeowners are actively looking for insurance providers that offer preventative services.

- Smart Home Adoption: The adoption rate of smart home devices, often integrated into proactive protection strategies, continued to climb, with an estimated 40% of new homeowners in 2025 expected to have at least one connected home security or monitoring device.

- Mitigation of Rising Costs: As repair costs for weather-related damage saw an average increase of 8-12% year-over-year through 2024, the appeal of insurance that helps prevent such damage becomes even stronger.

Strategic Acquisitions and Partnerships

Hippo Insurance's strategic acquisition and partnership opportunities are crucial for growth. Continuing to forge alliances, such as their collaboration with The Baldwin Group, can significantly enhance market reach and distribution. These partnerships are vital for accessing new customer bases and strengthening Hippo's competitive standing in the insurance sector.

Pursuing targeted acquisitions presents another avenue for expansion. By strategically acquiring companies, Hippo can diversify its product portfolio and integrate new technologies or customer segments. This approach allows for accelerated market penetration and a more robust competitive offering.

- Strategic Partnerships: Continued collaboration with entities like The Baldwin Group expands distribution and customer access.

- Targeted Acquisitions: Opportunities to acquire complementary businesses can diversify offerings and technology.

- Market Presence: Both strategies are designed to bolster Hippo's overall market share and brand visibility.

- Competitive Edge: Diversification and expanded reach through these avenues are key to maintaining a competitive advantage.

Unlocking Growth: New Markets, Products, and Tech in Insurance

Hippo Insurance Services has a significant opportunity to expand its market reach by entering new states, a strategy aimed at capturing a larger share of the homeowners insurance sector. The company is also poised to diversify its revenue streams by venturing into other insurance lines, catering to both personal and commercial clients to build a more resilient business model.

The company's focus on diversifying its premium mix by offering a wider array of insurance products is designed to reduce reliance on any single line of business, capitalizing on the ongoing growth within the broader home insurance market. Hippo's ambition to achieve over $2 billion in gross written premium by 2028 underscores the substantial potential in these expansion and diversification efforts.

Hippo can enhance underwriting accuracy through increased investment in data analytics and AI, enabling more precise risk assessment and personalized pricing. Collaborations with AI-driven platforms, like Arturo, streamline underwriting by pre-filling property data, improving efficiency and the customer experience. The New Homes Program offers a strong growth avenue, targeting newly constructed properties which often have lower risk profiles.

Strategic alliances with homebuilders are crucial for expanding Hippo's footprint in the new construction market, which saw a 10.5% increase in housing starts in April 2024. Homeowners' increasing demand for proactive protection against extreme weather events, with a growing interest in preventative services and smart home integration, aligns perfectly with Hippo's loss prevention-focused business model.

Hippo's strategic acquisition and partnership opportunities, such as its collaboration with The Baldwin Group, are vital for expanding market reach and distribution. Pursuing targeted acquisitions can diversify its product portfolio and integrate new technologies or customer segments, accelerating market penetration and strengthening its competitive offering.

| Opportunity Area | Description | Supporting Data/Trend |

|---|---|---|

| Geographic Expansion | Entering new states with homeowners insurance products. | Aiming to tap into underserved markets. |

| Product Diversification | Venturing into other insurance lines (personal & commercial). | Building a more robust and resilient business model. |

| AI & Data Analytics | Deepening investment for underwriting accuracy and personalized pricing. | Streamlining underwriting via AI platforms; Arturo collaboration. |

| New Construction Market | Focusing on newly constructed properties via partnerships. | 10.5% increase in housing starts (April 2024); robust expansion. |

| Proactive Protection Demand | Addressing homeowner need for preventative services. | 65% of homeowners seeking preventative services (late 2024); smart home adoption. |

| Strategic Alliances & Acquisitions | Forging partnerships and acquiring complementary businesses. | Baldwin Group collaboration; opportunities for market penetration. |

Threats

Increasing Frequency and Severity of Catastrophic Events

The increasing frequency and severity of catastrophic events, like the widespread wildfires and severe storms experienced in 2024, present a substantial threat to Hippo Insurance Services. These events directly translate into higher claims payouts, escalating loss ratios and impacting overall profitability. For instance, the 2023 hurricane season alone resulted in insured losses estimated to be over $50 billion, a figure expected to be matched or exceeded in 2024, directly affecting insurers like Hippo.

This trend also makes reinsurance, a crucial backstop for insurers, more expensive and potentially harder to secure. As climate-related disasters become more common and intense, reinsurers face greater risk, leading them to increase premiums or even reduce capacity, which can squeeze Hippo's margins and limit its ability to underwrite new business effectively.

Intensifying Regulatory Scrutiny and Compliance Costs

The insurance sector faces ever-growing regulatory oversight, with new rules emerging frequently. This intensified scrutiny, especially around how Hippo handles customer data, sets prices, and underwrites policies, could significantly increase compliance expenses. For instance, in 2024, many insurers reported a notable rise in compliance budgets due to new data protection mandates.

These increased costs and potential operational limitations stemming from stricter regulations can directly affect Hippo's profitability and its ability to innovate. Failure to adapt to these evolving requirements might also result in substantial fines, impacting financial performance and potentially restricting business operations.

Economic Downturns and Market Volatility

Economic headwinds pose a significant threat to Hippo Insurance Services. Elevated mortgage rates, currently hovering around 7% in late 2024, alongside persistent inflation, squeeze homeowners' budgets. This financial strain can diminish their capacity or inclination to purchase or maintain robust insurance coverage, impacting Hippo's new policy acquisition and retention rates.

A broader economic downturn could further exacerbate these challenges. Such a scenario might trigger an increase in insurance claims due to unexpected home issues, while simultaneously dampening demand for new policies. This dual pressure could negatively affect Hippo's revenue streams and overall profitability, especially if the market experiences significant contraction, a trend seen in some sectors of the insurance industry during previous economic slowdowns.

Competitive Pressure and Customer Acquisition Costs

The insurance market is intensely competitive, with established players and emerging insurtechs vying for market share. This rivalry can drive up customer acquisition costs (CAC) for Hippo, as significant investment in marketing and promotional offers may be necessary to attract and retain policyholders. In 2024, the average CAC in the U.S. property and casualty insurance sector was estimated to be around $400, a figure that could strain Hippo's profitability if not managed effectively.

This pressure on customer acquisition can directly translate into pricing challenges. To remain competitive, Hippo might be compelled to offer lower premiums or more attractive policy features, potentially impacting its profit margins. For instance, if competitors aggressively discount policies, Hippo may need to follow suit, even if it means accepting thinner margins per policyholder.

Hippo's ability to scale efficiently and differentiate its offerings will be crucial in navigating this competitive threat. Continued innovation in product development and customer service is essential to justify pricing and build customer loyalty, thereby mitigating the impact of rising acquisition costs.

- Intense Competition: Both traditional insurers and other insurtechs create a crowded marketplace.

- Rising Customer Acquisition Costs (CAC): Marketing and incentives needed to attract customers can increase expenses.

- Pricing Pressure: Competitors' pricing strategies may force Hippo to adjust its own premiums, potentially impacting margins.

- Need for Differentiation: Hippo must innovate to stand out and justify its value proposition to customers.

Reinsurance Market Volatility and Availability

Hippo Insurance Services heavily depends on the reinsurance market to manage its risk exposure effectively. Recent trends, such as the hardening of the reinsurance market in 2023 and early 2024, have seen significant increases in pricing for catastrophe coverage, with some lines experiencing rate hikes of 20-50% or more. This volatility directly impacts Hippo's cost of doing business and its capacity to underwrite new policies.

The availability of reinsurance coverage is also a critical factor. In 2024, reinsurers have become more selective, particularly concerning coastal and wildfire-prone areas, potentially limiting Hippo's ability to secure the necessary protection. This could force Hippo to either increase premiums for policyholders, reduce its underwriting appetite in certain regions, or retain more risk, thereby increasing its own financial exposure.

- Increased Reinsurance Costs: In 2023, the global reinsurance market saw average property catastrophe treaty renewals increase by approximately 10-25% year-over-year, a trend expected to continue into 2024.

- Reduced Reinsurance Capacity: Some reinsurers have reduced their overall capacity for property risks, especially in catastrophe-exposed zones, making it harder for insurers like Hippo to place their full reinsurance needs.

- Higher Retention Risk: If Hippo cannot secure sufficient reinsurance at acceptable prices, it may need to increase its risk retention, potentially impacting its balance sheet and profitability if significant loss events occur.

Weathering the Storm: Insurance Market Faces Triple Threat

The increasing frequency and severity of natural disasters, such as the severe weather events in early 2024, pose a significant threat by driving up claims and impacting profitability. For instance, the insured losses from natural catastrophes globally in 2023 were estimated to be around $120 billion, a figure that could be surpassed in 2024.

Economic instability, characterized by persistent inflation and elevated interest rates, continues to pressure homeowners' budgets. This can lead to reduced demand for insurance or a shift towards less comprehensive coverage, potentially affecting Hippo's customer acquisition and retention rates as homeowners prioritize essential expenses.

The property and casualty insurance market is highly competitive, with both established insurers and insurtech startups vying for market share. This intense competition can inflate customer acquisition costs, as companies like Hippo may need to invest more in marketing and incentives to attract and retain policyholders, potentially impacting profit margins.

SWOT Analysis Data Sources

This SWOT analysis is built upon a foundation of credible data, including Hippo's official financial filings, comprehensive market research reports, and expert industry analyses. These sources provide a robust understanding of the competitive landscape and internal capabilities.