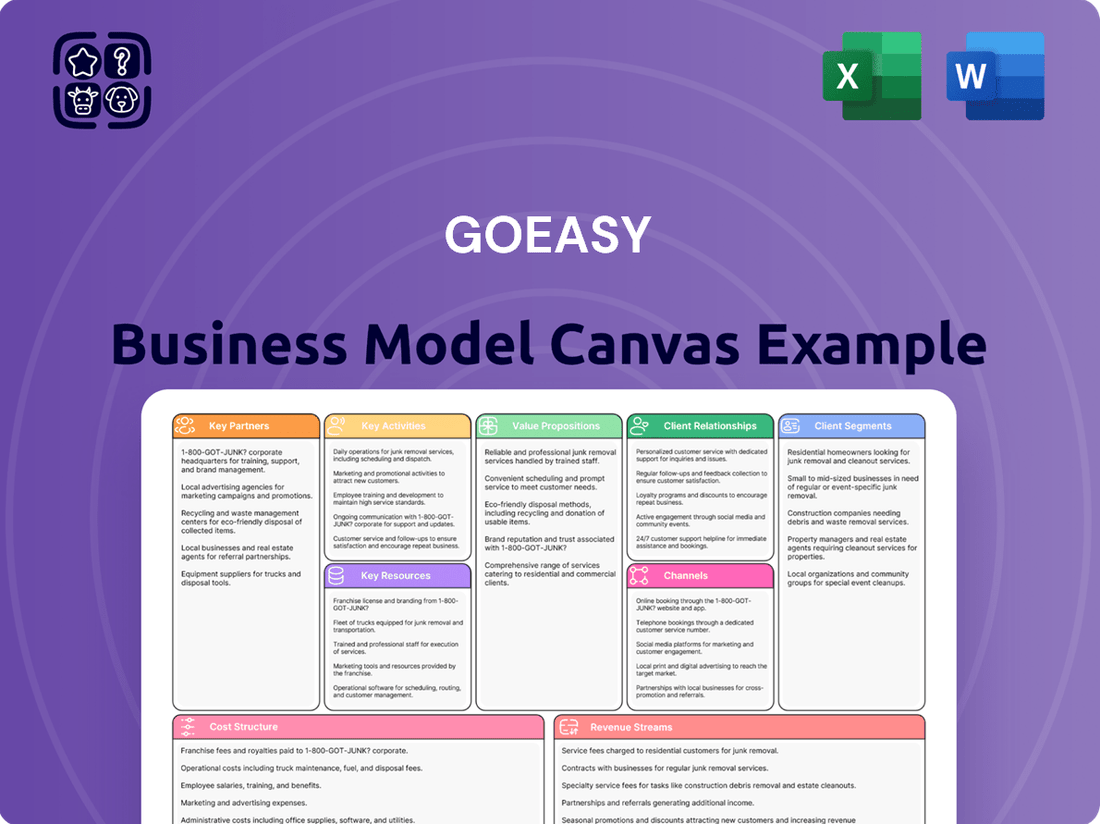

goeasy Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

goeasy

goeasy's Business Model: A Deep Dive

Unlock the strategic blueprint behind goeasy's success with our comprehensive Business Model Canvas. This in-depth analysis reveals how they effectively serve diverse customer segments and generate revenue through innovative financial solutions. Gain actionable insights into their key partnerships and value propositions.

Ready to dissect goeasy's winning formula? Our full Business Model Canvas provides a detailed, section-by-section breakdown of their operations, from customer relationships to cost structures. Download it now to benchmark your own strategies or inspire new ventures.

Partnerships

Financial Institutions

goeasy’s crucial partnerships with major financial institutions, including the Bank of Montreal and the Royal Bank of Canada, are foundational to its business model. These relationships provide essential credit facilities and diverse funding sources, enabling goeasy to maintain robust lending operations and expand its loan portfolio. For instance, in 2023, goeasy successfully renewed a significant credit facility, demonstrating the ongoing trust and support from these key banking partners.

Merchant and Dealer Networks

goeasy strategically leverages an extensive network of over 10,000 merchant and dealer partners. This vast network spans diverse industries such as retail, automotive, powersports, home improvement, and healthcare.

Through its LendCare brand, these partnerships facilitate point-of-sale financing, allowing customers to secure flexible payment options directly at the time of purchase. This strategy significantly broadens goeasy's customer base and diversifies its revenue generation.

Technology and Data Providers

goeasy’s partnerships with technology and data providers are fundamental to its sophisticated risk assessment and underwriting processes. These collaborations allow for the continuous refinement of credit scoring models, directly impacting loan approval efficiency and accuracy, particularly for the non-prime demographic.

By integrating cutting-edge data analytics and technological solutions, goeasy stays ahead in managing credit risk and adapting to evolving market conditions, including new interest rate cap regulations. For instance, in 2023, goeasy reported a loan portfolio of $2.3 billion, underscoring the scale at which these technological partnerships support their lending operations and risk management strategies.

Credit Bureaus

goeasy’s collaboration with credit bureaus, such as TransUnion, is fundamental to its customer-centric approach. These partnerships are not merely transactional; they are integral to goeasy's core mission of empowering customers to enhance their financial well-being.

By reporting payment performance to credit bureaus, goeasy provides a tangible pathway for its customers to build positive credit histories. This reporting mechanism is crucial for enabling customers to eventually qualify for prime lending rates, signifying a significant step towards long-term financial stability and improved access to credit markets.

- Credit bureau partnerships enable reporting of customer payment behavior.

- This reporting facilitates customer progression to prime lending rates.

- goeasy aims to foster long-term financial improvement for its clientele through these collaborations.

Community and Charity Organizations

goeasy actively collaborates with prominent community and charity organizations, notably its long-standing partnership with BGC Canada. This relationship highlights goeasy's dedication to corporate social responsibility, extending beyond its core business operations. These collaborations are characterized by substantial financial contributions and active community involvement, which in turn bolster goeasy's brand image and cultivate strong, positive connections within the communities it serves.

In 2024, goeasy continued its significant support for BGC Canada, contributing to programs that benefit Canadian youth. The company's commitment to social impact is a key element of its business model, fostering goodwill and reinforcing its role as a responsible corporate citizen. These partnerships are not just about financial aid; they involve hands-on engagement that resonates deeply with local communities.

- BGC Canada Partnership: goeasy's extensive support for BGC Canada provides vital resources for youth development programs across the country.

- Community Engagement: The company actively participates in local initiatives, demonstrating a commitment to the well-being of the communities where it operates.

- Brand Reputation Enhancement: These strategic alliances contribute to a positive brand perception, aligning goeasy with values of social responsibility and community support.

- Relationship Building: Partnerships foster strong, reciprocal relationships with community stakeholders, enhancing trust and mutual benefit.

Ecosystem Partnerships: Powering Growth

goeasy's ecosystem thrives on strategic alliances, particularly with financial institutions like the Bank of Montreal and Royal Bank of Canada, which provide crucial credit facilities. Its expansive network of over 10,000 merchant and dealer partners, spanning retail, automotive, and home improvement sectors, is vital for point-of-sale financing. Furthermore, collaborations with technology and data providers enhance risk assessment, while partnerships with credit bureaus like TransUnion facilitate customer credit building. The company's commitment to social responsibility is exemplified by its significant support for BGC Canada, reinforcing its community presence and brand reputation.

| Partnership Type | Key Partners | Impact on Business Model | 2023/2024 Data/Notes |

|---|---|---|---|

| Financial Institutions | Bank of Montreal, Royal Bank of Canada | Access to credit facilities and diverse funding sources, enabling lending operations. | Renewed significant credit facility in 2023. |

| Merchant & Dealer Network | 10,000+ partners (Retail, Auto, Home Improvement, etc.) | Facilitates point-of-sale financing, expanding customer base and revenue. | LendCare brand operates within this network. |

| Technology & Data Providers | Various providers | Enhances risk assessment, underwriting, and credit scoring models. | Supports efficient loan approvals and risk management. Loan portfolio was $2.3 billion in 2023. |

| Credit Bureaus | TransUnion | Enables customer credit history reporting and improvement. | Facilitates customer progression to prime lending rates. |

| Community Organizations | BGC Canada | Enhances corporate social responsibility and brand reputation. | Continued significant support in 2024 for youth programs. |

What is included in the product

A detailed Business Model Canvas for goeasy, outlining its customer segments, value propositions, and revenue streams, particularly focusing on its accessible lending and home furnishing solutions.

This model highlights goeasy's strategy of serving underserved markets through a robust network of channels and key partnerships, emphasizing its operational efficiency and competitive advantages.

goeasy's Business Model Canvas effectively addresses the pain point of financial accessibility for underserved consumers by clearly outlining its customer segments, value propositions, and channels for delivering affordable lending solutions.

Activities

Loan Origination and Underwriting

Goeasy's core activity revolves around originating and underwriting a variety of loans, primarily through its easyfinancial division. This includes unsecured personal loans, secured home equity loans, and auto loans, catering specifically to the non-prime consumer segment.

The company employs a sophisticated underwriting process, powered by proprietary technology, to accurately assess the risk associated with each applicant. This focus on advanced risk assessment is crucial for serving a market that may have less traditional credit histories.

In 2024, goeasy continued to enhance its credit models, demonstrating a commitment to adapting to evolving regulatory landscapes and maintaining robust credit performance. This ongoing refinement ensures the company's ability to manage risk effectively within its target market.

Lease-to-Own Operations

goeasy's key activities in lease-to-own operations primarily revolve around managing its easyhome division. This involves the core functions of acquiring and maintaining inventory of furniture, appliances, and electronics, alongside the crucial tasks of customer onboarding and managing lease agreements.

A significant part of these operations includes diligent payment collection from customers. In 2023, goeasy reported that its lease-to-own segment, easyhome, generated $599.2 million in revenue, highlighting the scale of these activities and the company's focus on providing accessible financing options.

Customer Relationship Management

goeasy's customer relationship management is centered on providing accessible financial solutions and fostering long-term customer loyalty. This involves proactive communication and support to help clients improve their financial standing.

A core activity is guiding customers toward better financial health, which includes offering financial education and creating opportunities for them to qualify for lower interest rates. For instance, in 2023, goeasy's loan portfolio continued to grow, demonstrating their ability to manage and expand customer relationships within their accessible lending model.

Capital Management and Funding

goeasy actively manages its capital structure, employing a mix of funding sources to fuel its expansion. This includes issuing senior unsecured notes and utilizing revolving credit facilities, ensuring robust liquidity for its growing loan book and strategic investments. For instance, in the first quarter of 2024, goeasy reported total assets of $2.5 billion, underscoring the scale of capital required to support its operations.

This proactive capital management is essential for maintaining financial stability and the capacity for future growth. It allows goeasy to pursue strategic initiatives, such as share repurchases, while also ensuring it has the necessary funds to underwrite its expanding loan portfolio. The company’s commitment to a diversified funding strategy mitigates risk and provides flexibility in a dynamic financial landscape.

- Senior Unsecured Notes: A key component of goeasy's long-term funding strategy, providing stable, long-dated capital.

- Revolving Credit Facilities: Offer flexibility and immediate access to funds for short-term liquidity needs and ongoing loan origination.

- Liquidity Management: Crucial for supporting a growing loan portfolio and operational expansion.

- Share Repurchases: Demonstrates confidence in the company's financial health and aims to enhance shareholder value.

Omnichannel Distribution Management

Omnichannel distribution management is a core activity for goeasy, ensuring customers can access its services seamlessly. This involves overseeing a network that spans over 400 physical retail locations, robust online platforms, and user-friendly mobile applications. The company also leverages a wide array of merchant partners, integrating point-of-sale financing solutions directly at the customer's purchasing point.

This integrated approach is critical for goeasy’s broad reach across Canada. It allows for efficient delivery of a diverse product and service portfolio, catering to various customer preferences and accessibility needs. For instance, in 2024, goeasy continued to expand its digital offerings, seeing a significant portion of its new customer acquisition occur through online channels, complementing its established brick-and-mortar presence.

- Managing Over 400 Physical Locations: Maintaining and optimizing the extensive physical retail footprint for customer interaction and service delivery.

- Operating Online and Mobile Platforms: Ensuring the functionality and user experience of e-commerce websites and mobile applications for sales and customer support.

- Coordinating Merchant Partner Networks: Integrating and managing relationships with a vast network of merchants to facilitate point-of-sale financing.

- Ensuring Broad Canadian Accessibility: Strategically managing distribution channels to provide widespread access to goeasy's products and services throughout Canada.

Powering Non-Prime Financial Services and Growth

Goeasy's key activities encompass originating and underwriting loans, primarily for non-prime consumers through easyfinancial, and managing its lease-to-own business, easyhome. This involves sophisticated risk assessment, inventory management for easyhome, and diligent payment collection. In 2024, goeasy continued to refine its credit models, and by Q1 2024, its total assets reached $2.5 billion, reflecting significant operational scale.

The company also focuses on customer relationship management, aiming to improve financial literacy and foster loyalty, and actively manages its capital structure through diverse funding sources like senior unsecured notes and revolving credit facilities. Furthermore, goeasy manages an omnichannel distribution network, including over 400 retail locations, online platforms, and merchant partnerships, ensuring broad Canadian accessibility.

| Key Activity | Description | 2023/2024 Data Point |

| Loan Origination & Underwriting | Serving non-prime consumers with personal, home equity, and auto loans. | Continued refinement of credit models in 2024. |

| Lease-to-Own Operations | Managing easyhome, including inventory, customer onboarding, and collections. | easyhome generated $599.2 million in revenue in 2023. |

| Customer Relationship Management | Enhancing financial literacy and building long-term customer loyalty. | Loan portfolio growth demonstrated effective customer relationship management in 2023. |

| Capital Management | Securing diverse funding sources for expansion and liquidity. | Total assets reached $2.5 billion in Q1 2024. |

| Omnichannel Distribution | Managing physical stores, online platforms, and merchant partnerships. | Over 400 physical locations and significant online customer acquisition in 2024. |

What You See Is What You Get

Business Model Canvas

The goeasy Business Model Canvas preview you are viewing is the actual, complete document you will receive upon purchase. This means you're seeing the exact structure, content, and formatting that will be yours to use, with no alterations or placeholders. You can be confident that the professional, ready-to-edit file you see now is precisely what you'll download to strategize and grow your business.

Resources

Financial Capital

goeasy's substantial financial capital is a cornerstone of its business model. This includes a robust consumer loan portfolio, which saw significant growth, and substantial cash reserves. For instance, as of the first quarter of 2024, goeasy reported total assets of $2.4 billion, with a significant portion allocated to its loan portfolio.

Access to diversified funding sources is critical. goeasy leverages unsecured debt markets and revolving credit facilities to maintain liquidity and fuel its operations. This financial flexibility allows the company to originate new loans and expand its market reach effectively.

Proprietary Underwriting Technology

goeasy leverages sophisticated proprietary underwriting technology and credit models to effectively assess risk within the non-prime lending market. This advanced system is crucial for their business, enabling them to make efficient and accurate loan approval decisions.

This technological edge allows goeasy to serve a demographic often overlooked by traditional lenders, while simultaneously managing credit risk with a high degree of precision. For instance, in the first quarter of 2024, goeasy reported a loan portfolio of $2.7 billion, demonstrating the scale at which their underwriting technology operates.

Extensive Branch Network

goeasy leverages its extensive branch network, boasting over 400 physical locations across Canada, to build customer trust and provide a tangible presence. These branches are crucial hubs for loan originations, customer service, and lease-to-own operations, supporting an omnichannel strategy.

In 2024, goeasy's physical footprint remained a cornerstone of its business, facilitating direct customer interaction and reinforcing brand accessibility. This network is instrumental in their ability to serve a broad customer base, particularly those who prefer or require in-person service for financial transactions.

Skilled Workforce and Management

goeasy's operational strength is built upon a substantial team of over 2,600 dedicated employees. This diverse workforce includes specialized financial professionals, customer service representatives focused on client engagement, and a highly experienced management cadre.

The collective expertise within this team is a cornerstone of goeasy's success. Their deep understanding of non-prime lending nuances, robust risk management practices, and effective customer relationship strategies are critical for maintaining operational efficiency and successfully implementing the company's strategic objectives.

- Skilled Workforce: Over 2,600 employees, encompassing financial experts and customer service personnel.

- Management Expertise: A seasoned management team with extensive experience in non-prime lending and risk assessment.

- Operational Drivers: The team's proficiency directly fuels operational efficiency and the execution of strategic initiatives.

- Customer Relations: Strong customer relationship management skills are key to goeasy's service delivery.

Brand Recognition and Customer Loyalty

goeasy's strong brand recognition, particularly through its easyfinancial, easyhome, and LendCare divisions, is a cornerstone of its business model. This established presence cultivates significant customer loyalty, creating a valuable intangible asset that drives repeat business and attracts new clientele by offering a trusted and familiar choice within its target market.

This brand equity is not just about name recognition; it's about the consistent delivery of services that resonate with goeasy's customer base. For instance, in 2023, goeasy reported a significant increase in its customer base, underscoring the effectiveness of its brand in attracting and retaining users. This loyalty translates directly into predictable revenue streams and a reduced cost of customer acquisition compared to competitors still building their brand presence.

- Brand Strength: goeasy operates under well-recognized brands like easyfinancial, easyhome, and LendCare, which are familiar to its core customer demographic.

- Customer Loyalty: Years of service have fostered a loyal customer base, leading to repeat business and a strong referral network.

- Market Differentiation: This established brand equity sets goeasy apart in a competitive lending and retail services landscape.

- Asset Value: The collective brand recognition and loyalty represent a substantial intangible asset, contributing to the company's overall valuation and market position.

Strategic Resources Powering Non-Prime Financial Services

goeasy's key resources are its substantial financial capital, including a robust loan portfolio and significant cash reserves, as evidenced by $2.4 billion in total assets in Q1 2024. Diversified funding sources, such as unsecured debt markets and credit facilities, ensure liquidity. Proprietary underwriting technology and credit models are crucial for efficient risk assessment, enabling the company to serve the non-prime market effectively, with a loan portfolio reaching $2.7 billion in Q1 2024.

| Resource Category | Specific Resource | Key Characteristic/Impact | Data Point (as of Q1 2024 or latest available) |

|---|---|---|---|

| Financial Capital | Loan Portfolio | Core asset, drives revenue and growth | $2.7 billion |

| Financial Capital | Cash Reserves | Ensures liquidity and operational flexibility | Part of $2.4 billion total assets |

| Funding Sources | Unsecured Debt & Credit Facilities | Provides ongoing access to capital | Not specified, but critical for operations |

| Technology | Underwriting & Credit Models | Enables precise risk assessment in non-prime market | Proprietary and sophisticated |

| Physical Infrastructure | Branch Network | Facilitates customer interaction and service delivery | Over 400 locations |

| Human Capital | Skilled Workforce | Drives operational efficiency and customer relations | Over 2,600 employees |

| Intangible Assets | Brand Recognition (easyfinancial, easyhome, LendCare) | Builds customer loyalty and market differentiation | Strong and established |

Value Propositions

Accessible Financial Solutions

goeasy offers financial solutions to Canadians who might not get approved by traditional banks. This means everyday people can access funds for things like furniture, appliances, or even unexpected expenses, filling a gap in the market.

In 2024, goeasy's accessible lending model continued to serve a broad customer base, with over 1.7 million active customers across its brands. This accessibility is key to their value proposition, providing essential financial tools to those often overlooked by mainstream lenders.

Path to Improved Credit

goeasy provides a tangible path for customers to enhance their creditworthiness. A significant 60% of their customers experience an improvement in their credit scores, demonstrating the effectiveness of their approach.

Furthermore, the company’s model is designed to foster long-term financial health, with one in three customers successfully graduating to prime interest rates within a year of engagement.

This value proposition extends beyond mere access to credit, actively working to empower individuals toward a more stable and prosperous financial future.

Diverse Product Offering

goeasy's diverse product offering is a cornerstone of its business model, providing a wide array of financial solutions. This includes unsecured and secured personal loans, auto loans, and point-of-sale financing, demonstrating a commitment to meeting varied consumer credit needs.

Further expanding its reach, goeasy also offers lease-to-own options for furniture, appliances, and electronics through its Easyhome and Leons brands. This broad selection ensures that goeasy can attract and serve a larger customer base with different purchasing power and preferences.

In 2023, goeasy reported a significant increase in its loan portfolio, reaching $2.5 billion, underscoring the success of its diversified product strategy in driving growth and customer engagement.

Convenient and Flexible Access

Customers can engage with goeasy through a variety of channels, reflecting a commitment to convenience and flexibility. This omnichannel approach includes user-friendly online platforms, dedicated mobile applications, and a robust network of over 400 physical retail locations. This extensive physical presence, combined with a broad merchant partner network, ensures that customers can access goeasy's services in a way that best suits their individual preferences and needs.

This strategy directly addresses the need for accessible financial solutions. For instance, goeasy's loan approval process is designed to be straightforward, with many customers receiving funds quickly, often the same day. This speed and ease of access are critical value propositions for individuals seeking immediate financial assistance.

The availability of over 400 physical locations across Canada provides a tangible point of contact for customers who prefer in-person interactions or require assistance beyond digital channels. This physical footprint is a significant differentiator, particularly for customers who may not be as comfortable with online-only transactions.

Furthermore, the integration with a vast merchant partner network expands the reach and accessibility of goeasy's offerings. This allows customers to utilize goeasy's services for various purchases, seamlessly integrating financial solutions into their everyday shopping experiences.

Quick and Efficient Approval Process

goeasy's quick and efficient approval process is a cornerstone of its value proposition, built upon proprietary underwriting technology. This technological edge allows for rapid loan decisions, a critical factor for customers needing immediate financial solutions.

This streamlined approach significantly reduces the time and effort applicants spend, making goeasy's financial products more accessible. For instance, in 2023, goeasy processed a substantial volume of loans, highlighting the efficiency of its systems.

- Proprietary Technology: goeasy utilizes advanced, in-house underwriting technology to assess loan applications swiftly.

- Reduced Friction: The streamlined process minimizes paperwork and waiting times for customers.

- Timely Access to Funds: This efficiency ensures that customers receive the financial assistance they need promptly.

- Market Advantage: Speed of approval differentiates goeasy from competitors, attracting a broad customer base.

Essential Financial Access & Credit Improvement for Canadians

goeasy provides essential financial accessibility to Canadians often excluded by traditional banks, offering a pathway to improved creditworthiness and financial stability. Their model not only grants access to funds for everyday needs but also actively supports customers in building better financial futures, with a notable 60% seeing credit score improvements.

A diverse product suite, including personal loans, auto loans, and point-of-sale financing, alongside lease-to-own options, caters to a wide range of consumer needs. This breadth, evidenced by a $2.5 billion loan portfolio in 2023, solidifies goeasy's position in meeting varied credit demands.

Convenience is paramount, with customers able to interact through over 400 physical locations, online platforms, and mobile apps, ensuring broad accessibility. This omnichannel approach, coupled with rapid, technology-driven approvals, provides a distinct advantage for customers seeking timely financial solutions.

goeasy's commitment to customer financial uplift is a core value, with one in three customers progressing to prime interest rates. This focus on empowerment and long-term financial health distinguishes their service beyond simple lending.

| Value Proposition | Description | Supporting Data (2023/2024) |

|---|---|---|

| Financial Accessibility | Providing credit solutions to underserved Canadians. | 1.7 million active customers in 2024. |

| Credit Improvement | Helping customers build credit history and scores. | 60% of customers experience credit score improvement. |

| Product Diversity | Offering a wide range of loan and lease-to-own products. | $2.5 billion loan portfolio in 2023. |

| Convenient Access | Multiple channels for customer interaction and service. | Over 400 physical locations across Canada. |

| Fast Approvals | Utilizing proprietary technology for quick loan decisions. | Streamlined process enabling timely access to funds. |

Customer Relationships

Personalized and Supportive Service

goeasy focuses on building trust through personalized and supportive service, a critical element for customers with non-prime credit. This approach acknowledges the unique financial challenges many face, offering tailored guidance to help them achieve their objectives.

In 2024, goeasy's commitment to customer support was evident in its operational focus. The company emphasizes understanding individual circumstances, a strategy that underpins its success in serving a diverse customer base.

Financial Education and Credit Building

goeasy's customer relationships are built on a foundation of financial education and active credit rebuilding support. This dual approach not only helps customers manage their current financial needs but also empowers them for future financial success.

By offering resources and guidance, goeasy fosters a sense of partnership, encouraging loyalty. This strategy is particularly impactful as it enables customers to improve their creditworthiness, potentially accessing prime lending rates over time.

In 2023, goeasy's focus on customer success saw significant traction, with a substantial portion of its loan portfolio originating from customers who were previously underserved by traditional lenders, demonstrating the effectiveness of their relationship-building model.

Omnichannel Engagement

goeasy maintains customer relationships through an omnichannel strategy, offering interaction via its website, mobile app, and over 400 physical locations. This wide reach ensures customers can engage through their preferred channel, enhancing accessibility and convenience.

Post-Lending Support

goeasy's post-lending support is vital for customer retention and managing risk. This includes clear communication about payment schedules and available options, which fosters trust and helps customers manage their financial obligations effectively. For instance, in 2023, goeasy reported a strong customer base, indicating the success of their relationship management strategies.

This proactive approach not only aids in timely repayments but also reinforces goeasy's commitment to its customers' financial well-being. By offering ongoing assistance, they aim to reduce delinquency rates and build long-term relationships. In the first quarter of 2024, the company continued to emphasize customer service initiatives.

Key aspects of their post-lending support include:

- Clear communication channels for payment inquiries and adjustments.

- Proactive outreach to customers facing potential payment difficulties.

- Providing educational resources on financial management.

- Offering flexible payment options when feasible.

Direct and Indirect Interaction

goeasy builds customer relationships through a dual approach: direct interactions at its branches and online platforms, and indirect engagement via its network of merchant partners offering point-of-sale financing. This strategy allows for personalized service and broad market reach.

In 2024, goeasy continued to leverage its omni-channel approach. For instance, its Easyfinancial segment saw significant growth, with over 1.7 million customers served by the end of Q3 2024, demonstrating the effectiveness of both direct digital engagement and in-person branch interactions in fostering loyalty.

- Direct Engagement: Branches and online portals provide a personal touch, facilitating trust and immediate problem resolution.

- Indirect Engagement: Merchant partnerships extend goeasy's reach, embedding financing solutions directly into the customer purchase journey.

- Brand Presence: This blend ensures goeasy remains visible and accessible, whether customers are actively seeking financial services or encountering them serendipitously.

- Customer Reach: By catering to diverse preferences for interaction, goeasy effectively serves a wider demographic, from digitally savvy individuals to those preferring face-to-face service.

Empowering Non-Prime Customers: Building Trust & Expanding Reach

goeasy cultivates lasting customer relationships through a blend of personalized support and accessible channels, aiming to empower individuals with non-prime credit. The company's commitment extends to financial education and credit rebuilding, fostering trust and long-term loyalty.

In 2024, goeasy continued to expand its customer base, serving over 1.7 million customers through its Easyfinancial segment by the third quarter. This growth underscores the effectiveness of their omni-channel strategy, which includes over 400 physical locations and robust digital platforms.

goeasy's customer relationship strategy emphasizes proactive post-lending support, including clear communication and flexible payment options, which helps manage risk and enhance customer retention. This approach is crucial for building confidence among customers navigating financial challenges.

| Metric | 2023 | Q3 2024 |

|---|---|---|

| Total Customers (Easyfinancial) | ~1.5 million | >1.7 million |

| Physical Locations | ~400 | ~400+ |

| Customer Retention Focus | High | High |

Channels

Physical Branch Network

goeasy's physical branch network, encompassing over 400 easyfinancial and easyhome locations across Canada, is a cornerstone of its customer engagement strategy. These branches facilitate direct customer interactions, streamline loan application processes, and allow for hands-on selection of lease-to-own products, providing a crucial tangible touchpoint.

Online and Mobile Platforms

goeasy leverages sophisticated online and mobile platforms, such as the easyfinancial and easyhome websites and apps, to offer customers convenient access to financial services. These digital touchpoints are crucial for loan applications, account management, and information retrieval, contributing significantly to new loan originations.

Point-of-Sale (POS) Financing through Merchant Partners

goeasy's LendCare brand facilitates point-of-sale financing, connecting customers with immediate loan options at approximately 11,000 merchant locations. This expansive network spans critical sectors including automotive, powersports, retail, home improvement, and healthcare, enabling seamless financing at the moment of purchase.

Direct Marketing and Advertising

goeasy leverages direct marketing and advertising to connect with its core customer base, emphasizing its accessible financial products. These efforts span digital channels, including search engine marketing and social media, alongside traditional advertising like television and radio spots. Promotional materials further detail their loan and leasing options.

In 2023, goeasy reported substantial marketing expenditures to drive customer acquisition and brand awareness. For instance, their focus on digital channels saw a significant increase in online lead generation, contributing to their overall growth. This multi-channel approach is crucial for reaching diverse customer segments.

- Digital Advertising: Targeted campaigns across search engines and social media platforms to capture individuals actively seeking financial solutions.

- Traditional Media: Utilizing television, radio, and print to build broad brand recognition and reach a wider audience.

- Promotional Materials: Developing informative brochures, flyers, and in-store displays to educate potential customers about goeasy's services.

- Customer Relationship Management (CRM): Employing CRM strategies to nurture leads and maintain ongoing communication with existing customers, encouraging repeat business and referrals.

Referral Programs

Referral programs are a key element for goeasy in acquiring new customers, particularly within the non-prime demographic. By encouraging existing, satisfied customers to refer friends and family, goeasy taps into a powerful, trust-based marketing channel.

This approach leverages word-of-mouth, which is highly effective in communities where trust is paramount. For instance, in 2023, goeasy continued to focus on customer satisfaction, a crucial precursor for successful referral initiatives. While specific referral program conversion rates aren't publicly detailed, the company's consistent growth in its loan portfolio suggests the effectiveness of its customer acquisition strategies.

- Leveraging satisfied customers for organic growth.

- Building trust through word-of-mouth marketing in the non-prime segment.

- Strategic partnerships can also drive customer acquisition via referrals.

- This channel reduces customer acquisition costs compared to traditional advertising.

Seamless Access: Physical & Digital Financial Touchpoints

goeasy's channels are a robust mix of physical and digital touchpoints. The extensive branch network offers direct customer interaction and product experience, while online and mobile platforms provide convenient access to services and facilitate loan originations. Point-of-sale financing through LendCare at numerous merchant locations ensures immediate loan availability.

Customer Segments

Non-Prime Canadian Consumers

goeasy's core customer base consists of everyday Canadians who might not qualify for traditional banking services due to non-prime credit scores. These are individuals who are employed and responsible but have limited credit history or lower scores, needing accessible financial products.

In 2024, goeasy continued to serve this demographic, which represents a significant portion of the Canadian population. For instance, a substantial percentage of Canadians have credit scores that fall outside the prime range, making goeasy's offerings particularly relevant to their financial needs.

Individuals Seeking Unsecured Loans

Individuals seeking unsecured loans represent a significant customer segment for goeasy, particularly through its easyfinancial brand. These customers often need funds for a variety of personal reasons, including consolidating existing debts, covering unexpected medical bills, or financing home improvements. In 2024, the demand for such flexible financing solutions remained robust, as many individuals sought to manage their finances more effectively.

goeasy's easyfinancial arm is specifically designed to cater to this demographic by offering accessible and straightforward unsecured personal loan products. The company's strategy focuses on providing quick approvals and manageable repayment terms, which are crucial for individuals who may not qualify for traditional bank loans. This approach allows goeasy to serve a market segment that values convenience and a less stringent application process.

Consumers Needing Secured Loans

Consumers needing secured loans, such as those for vehicles or home equity, represent a significant customer base. These individuals utilize their existing assets as collateral to access larger sums of money, often securing more favorable interest rates compared to unsecured alternatives.

In 2024, the demand for secured lending remained robust, with auto loan originations projected to reach $700 billion in the US, reflecting a continued reliance on vehicles as valuable collateral. Similarly, home equity lines of credit (HELOCs) saw a resurgence, with outstanding balances climbing, indicating homeowners leveraging their property equity for various financial needs.

Households Desiring Lease-to-Own Products

The easyhome division specifically targets households that find lease-to-own solutions ideal for acquiring furniture, appliances, and electronics. This segment often prioritizes flexibility and avoids the upfront costs and long-term commitments associated with traditional ownership or financing methods.

These customers are typically looking for accessible ways to furnish their homes, often facing credit limitations or preferring to spread payments over time. For example, in 2023, goeasy reported that its lease-to-own segment served a significant number of customers seeking these flexible arrangements, demonstrating a consistent demand for this product offering.

- Target Audience: Households seeking flexible furniture, appliance, and electronics acquisition.

- Value Proposition: Lease-to-own provides an alternative to traditional ownership and financing, emphasizing affordability and manageable payments.

- Customer Needs: Access to home goods without immediate large capital outlay or strict credit requirements.

- Market Relevance: In 2023, goeasy's lease-to-own segment continued to be a core revenue driver, reflecting sustained consumer interest in this model.

Merchant Customers for POS Financing

goeasy's merchant customers are businesses that offer larger ticket items or services and want to provide their customers with financing options at the point of sale. These merchants partner with goeasy to offer their buyers accessible credit for purchases like powersports vehicles, home renovations, or medical procedures.

This segment benefits from goeasy's financing solutions by increasing their sales conversion rates and average transaction values. By offering immediate financing, merchants can help customers overcome budget barriers, leading to more completed sales. For instance, a powersports dealer can offer financing for a new motorcycle, making a significant purchase more manageable for the buyer.

In 2024, goeasy continued to expand its merchant network, facilitating financing for a wide array of goods and services. This strategic approach allows goeasy to reach a broader customer base indirectly through its merchant partners, enhancing the overall accessibility of credit for consumers across various sectors.

- Merchant Partners: Businesses selling high-value goods or services.

- Customer Benefit: Seamless point-of-sale financing for larger purchases.

- Sales Impact: Increased conversion rates and average transaction values for merchants.

- Sector Reach: Powersports, home improvement, healthcare, and more.

Unlocking Financial Access for Everyday Canadians

goeasy's customer segments are diverse, primarily serving everyday Canadians who may not fit traditional banking criteria. This includes individuals seeking unsecured personal loans for various needs like debt consolidation or unexpected expenses, a market that remained strong in 2024.

Another key segment comprises consumers requiring secured loans, leveraging assets such as vehicles for financing. Additionally, goeasy caters to households preferring lease-to-own arrangements for furniture and appliances, avoiding large upfront costs and credit hurdles.

Finally, goeasy partners with businesses that offer financing at the point of sale, enabling their customers to purchase higher-ticket items or services, thereby boosting merchant sales and expanding goeasy's reach.

| Customer Segment | Key Characteristics | 2024 Relevance/Data Point |

|---|---|---|

| Non-Prime Individuals | Limited credit history, lower scores, employed | Significant portion of Canadian population |

| Unsecured Loan Seekers | Debt consolidation, medical bills, home improvements | Robust demand for flexible financing |

| Secured Loan Seekers | Utilize assets (vehicles, home equity) as collateral | Auto loan originations strong; HELOCs resurged |

| Lease-to-Own Consumers | Furnishing homes, preference for manageable payments | Core revenue driver, sustained consumer interest |

| Merchant Partners | Businesses offering high-value goods/services | Facilitated financing for powersports, home renovations, medical procedures |

Cost Structure

Interest Expense on Borrowed Capital

Interest expense on borrowed capital is a substantial cost for goeasy. This includes interest paid on their senior unsecured notes and revolving credit facilities, which are crucial for funding their lending operations.

For goeasy, a company that operates as a lender, the cost of acquiring these funds directly influences its bottom line. In 2023, for instance, goeasy reported interest expense of $216.2 million, a significant portion of their overall operating costs, highlighting the direct impact of interest rates on their profitability.

Credit Loss Provisions and Net Charge-Offs

Credit loss provisions and net charge-offs are significant costs for goeasy, stemming directly from its non-prime lending model. In 2024, the company's credit loss provisions were a key component of its operating expenses, reflecting the inherent risk in serving customers with less established credit histories. These provisions are carefully managed and adjusted based on evolving economic conditions and goeasy's own performance data.

Operating Expenses (Salaries, Rent, Marketing)

goeasy's operating expenses are substantial, reflecting its broad reach and operational complexity. In 2023, the company reported operating expenses of $1.4 billion, a significant portion of which goes towards compensating its workforce of over 2,600 employees across Canada.

Maintaining its extensive network of over 400 physical locations, which are crucial for its omnichannel strategy and customer accessibility, incurs considerable rent and property-related costs. These physical touchpoints are key to serving its diverse customer base effectively.

Marketing and advertising are also critical components of goeasy's cost structure. These investments are vital for brand awareness, customer acquisition, and promoting its various financial products and services to its target demographic, ensuring continued growth and market penetration.

Technology and System Development Costs

goeasy invests heavily in its proprietary underwriting technology and digital platforms. These technology and system development costs are essential for refining risk assessment and boosting operational efficiency. For instance, in 2024, the company continued to prioritize these investments to support its ongoing digital transformation initiatives.

- Proprietary Underwriting Technology: Ongoing development and refinement of algorithms for credit risk assessment.

- Digital Platforms: Investment in customer-facing websites and mobile applications for seamless user experience.

- IT Infrastructure: Upgrades to cloud computing, data analytics, and cybersecurity to ensure scalability and security.

Administrative and Regulatory Compliance Costs

goeasy incurs significant expenses in administrative functions and ensuring strict adherence to regulatory frameworks. These costs are essential for maintaining operational licenses and overall business integrity within the financial services sector.

These administrative and regulatory compliance costs include expenses for legal counsel, audit services, and systems to monitor and manage compliance with evolving financial regulations. For example, changes in consumer protection laws or lending regulations can necessitate updates to internal processes and technology, adding to the cost base.

- Administrative Expenses: Costs associated with general management, human resources, IT infrastructure, and office operations.

- Legal and Compliance Fees: Expenses for legal advice, regulatory filings, and ensuring adherence to all applicable laws and industry standards.

- Interest Rate Cap Adherence: Costs related to adjusting loan products and pricing strategies to comply with mandated interest rate limitations, which can impact profitability and operational models.

- Licensing and Permitting: Fees required to obtain and maintain business licenses and permits in all jurisdictions where goeasy operates.

Unpacking a Lender's Q1 2024 Cost Structure

Interest expense remains a primary cost driver for goeasy, reflecting its reliance on borrowed capital to fund its lending activities. In the first quarter of 2024, goeasy reported interest expense of $147.9 million, a notable increase from the previous year, underscoring the impact of higher interest rates on its cost of funds.

Credit risk management is a significant expense category, directly tied to goeasy's non-prime lending model. The company's credit loss provisions and net charge-offs are carefully monitored and adjusted, with provisions for credit losses amounting to $103.5 million in Q1 2024, reflecting the inherent risks in its customer base.

| Cost Category | Q1 2024 (Millions) | Commentary |

| Interest Expense | $147.9 | Reflects higher borrowing costs and increased debt levels. |

| Provisions for Credit Losses | $103.5 | Directly related to the non-prime lending portfolio risk. |

| Operating Expenses (excl. interest & credit losses) | $317.7 | Includes employee compensation, rent, marketing, and technology. |

Revenue Streams

Interest Income from Unsecured Loans

goeasy's primary revenue driver is the interest earned on unsecured personal loans provided by its easyfinancial division. This income stream is substantial, directly correlating with the number of loans issued and the interest rates applied to them.

In 2024, goeasy's loan portfolio continued to grow, with a significant portion of its revenue stemming from these interest charges. The company's ability to originate and service a large volume of unsecured loans underpins this critical revenue stream.

Interest Income from Secured Loans

Interest income from secured loans, such as auto and home equity loans, forms a significant revenue stream for goeasy. These loans, often carrying larger principal amounts, bolster the company's overall loan portfolio and directly contribute to its total interest earnings.

In 2024, goeasy's secured loan portfolio continued to be a cornerstone of its financial performance. The company reported substantial growth in its loan book, with interest income from these secured products playing a crucial role in its profitability.

Lease Revenue from Easyhome

The easyhome division is a key revenue generator for goeasy, primarily through lease payments for furniture, appliances, and electronics. This offers customers a flexible lease-to-own model, providing a consistent and predictable income stream for the company.

In 2023, goeasy's retail segment, which includes easyhome, saw significant performance. For instance, the company reported total revenue of $1.1 billion in 2023, with a substantial portion derived from its lending and retail operations.

Point-of-Sale (POS) Financing Fees and Interest

goeasy generates revenue through fees and interest from point-of-sale financing offered via its LendCare brand. This financing is available to consumers purchasing goods or services from goeasy's extensive network of retail, automotive, powersports, home improvement, and healthcare partners.

This revenue stream is directly tied to the volume of transactions facilitated through these partnerships. For instance, in 2023, goeasy's loan portfolio grew significantly, indicating increased utilization of its financing solutions by consumers at the point of sale.

- Point-of-Sale Financing: LendCare provides financing at the checkout for various retailers.

- Merchant Network: Revenue is driven by partnerships across diverse sectors like automotive, home improvement, and healthcare.

- Fee and Interest Income: goeasy earns from the interest charged on financed amounts and potential administrative fees.

- Transaction Volume: The success of this stream is directly linked to the number of successful financing applications processed.

Other Fees and Charges

goeasy also generates revenue through various fees and charges linked to its loan and leasing offerings. These can include administrative fees for account management or charges for late payments, all within legal and regulatory frameworks. These supplementary income sources bolster the company's overall financial performance.

For instance, in the first quarter of 2024, goeasy reported that its non-interest income, which encompasses these types of fees, played a role in its financial results. While specific figures for just these fees aren't broken out separately from all non-interest income, the company's overall strategy includes leveraging these charges to enhance profitability.

- Administrative Fees: Charges for account setup or maintenance.

- Late Payment Charges: Penalties applied when payments are not received on time.

- Other Service Fees: Potential charges for specific services related to lending or leasing products.

Revenue Streams: A Detailed Breakdown

goeasy's revenue streams are diverse, primarily driven by interest income from its lending operations, both unsecured personal loans via easyfinancial and secured loans. Additionally, its easyhome division generates consistent income through lease payments for furniture and appliances, offering a lease-to-own model.

The company also earns revenue through point-of-sale financing via LendCare, partnering with a wide range of businesses. Fees and charges related to loan and lease management further contribute to its overall financial performance.

| Revenue Stream | Primary Source | 2023 Performance Indicator |

|---|---|---|

| Unsecured Personal Loans (easyfinancial) | Interest Income | Significant contributor to overall revenue, with loan portfolio growth in 2023. |

| Secured Loans | Interest Income | Cornerstone of financial performance, with substantial loan book growth reported in 2023. |

| Lease Payments (easyhome) | Lease-to-Own Agreements | Key revenue generator, contributing to the $1.1 billion total revenue in 2023. |

| Point-of-Sale Financing (LendCare) | Interest and Fees | Driven by transaction volume across automotive, home improvement, and healthcare partners. |

| Fees and Charges | Account Management, Late Payments | Supplementary income enhancing overall financial results. |

Business Model Canvas Data Sources

The goeasy Business Model Canvas is built upon a foundation of internal financial data, customer insights gleaned from operational metrics, and extensive market research. These sources ensure each canvas block is populated with actionable and relevant information.