IndusInd Bank SWOT Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

IndusInd Bank Bundle

Go Beyond the Preview—Access the Full Strategic Report

IndusInd Bank showcases robust digital capabilities and a strong retail presence, but faces intensifying competition and evolving regulatory landscapes. Understanding these dynamics is crucial for navigating its future.

Want the full story behind IndusInd Bank’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

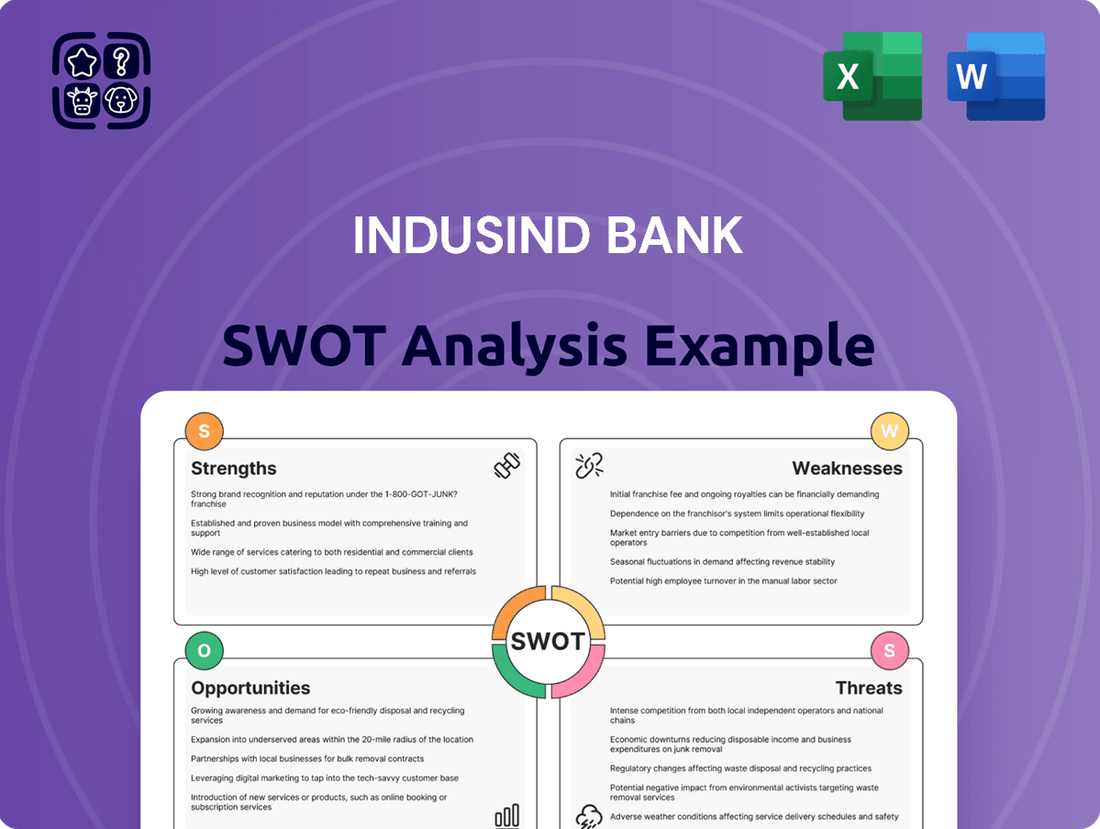

Strengths

Diversified Loan Portfolio and Business Segments

IndusInd Bank's loan portfolio is notably diversified, with a strong emphasis on retail lending. This strategic approach includes significant growth in retail assets and the Micro, Small, and Medium Enterprises (MSME) sector, especially for loans under ₹2 crores. For instance, as of the fiscal year ending March 2024, retail loans constituted a substantial portion of their advances, demonstrating this core strength.

This diversification spans across consumer and corporate lending, encompassing areas like vehicle finance and microfinance. By tapping into various market segments, the bank effectively mitigates risks that could arise from an over-reliance on any single sector, ensuring a more resilient financial structure.

Robust Digital Banking Initiatives

IndusInd Bank's 'Digital 2.0' strategy is a significant strength, evidenced by the acquisition of 2 million new clients through digital channels. This digital push also facilitated the digital disbursement of ₹1,000 crores in personal loans, showcasing the effectiveness of their online platforms.

The bank is further bolstering its digital offerings with initiatives like 'INDIE for Business,' specifically designed to provide comprehensive digital banking solutions for MSMEs. This focus on empowering small and medium enterprises digitally is a key differentiator.

A strategic partnership with Trustmore to expand digital escrow services across India underscores IndusInd Bank's commitment to leveraging technology for enhanced customer convenience and security. These moves highlight a proactive approach to digital transformation.

Extensive and Expanding Distribution Network

IndusInd Bank boasts a robust and continuously growing distribution network, a key strength in its market position. As of June 30, 2025, the bank serves around 42 million customers through a substantial footprint of over 3,110 branches and banking outlets, complemented by 3,052 ATMs. This extensive reach penetrates deep into the Indian landscape, touching 1.64 lakh villages.

The bank's commitment to expanding its physical presence is evident in its recent performance. Over the past year alone, IndusInd Bank strategically opened 378 new branches, significantly bolstering its accessibility and service capabilities, especially in underserved rural regions.

Healthy Capital Adequacy and Liquidity Buffers

IndusInd Bank demonstrates strong financial health through its robust capital adequacy and liquidity. As of June 30, 2025, the bank maintained a total Capital Adequacy Ratio (CRAR) of 16.63% under Basel III, significantly above the regulatory minimums. This indicates a solid foundation to absorb potential losses and support future growth.

The bank's liquidity position is equally impressive, with a liquidity coverage ratio of 141% reported for the same period. This substantial buffer ensures IndusInd Bank can comfortably meet its short-term obligations, even in stressed market conditions, highlighting its financial resilience.

- Strong Capital Base: Total CRAR of 16.63% as of June 30, 2025, exceeding regulatory requirements.

- Ample Liquidity: Liquidity Coverage Ratio (LCR) at 141%, providing significant short-term funding resilience.

- Financial Stability: These metrics underscore the bank's ability to withstand economic headwinds and maintain operational continuity.

Commitment to Social Responsibility and Strategic Partnerships

IndusInd Bank's commitment to social responsibility is a significant strength, evidenced by its strategic partnerships. For instance, its collaboration with UNICEF focuses on climate risk management and building community resilience in underserved areas, showcasing a dedication to environmental and social impact. This initiative is particularly relevant as climate change continues to pose economic risks, and community resilience is crucial for sustainable development.

Furthermore, the bank's role as the official banking partner for the Paris 2024 Paralympic Games underscores its support for inclusivity and national pride. This partnership not only enhances its brand image by associating with a globally recognized event promoting accessibility and athletic achievement but also strengthens its community engagement by aligning with values of perseverance and inclusion.

- UNICEF Partnership: Focuses on climate risk management and community resilience in aspirational districts, aligning with global sustainability goals.

- Paris 2024 Paralympic Games: Serves as the official banking partner, promoting inclusion, national pride, and enhancing brand visibility through sports.

- Brand Enhancement: These initiatives bolster IndusInd Bank's reputation as a socially conscious and community-oriented financial institution.

IndusInd Bank's Strategic Growth: Digital, Diversified, and Strong

IndusInd Bank's loan portfolio is well-diversified, with a strong focus on retail and MSME segments. This diversification across consumer and corporate lending, including vehicle finance and microfinance, effectively mitigates sector-specific risks.

The bank's 'Digital 2.0' strategy is a key strength, evidenced by acquiring 2 million new clients digitally and disbursing ₹1,000 crores in personal loans through online channels. Initiatives like 'INDIE for Business' further enhance digital solutions for MSMEs.

A robust and expanding distribution network is a significant asset, with approximately 42 million customers served through over 3,110 branches and banking outlets as of June 30, 2025. The bank strategically opened 378 new branches in the past year, increasing accessibility.

IndusInd Bank demonstrates strong financial health with a total CRAR of 16.63% (Basel III) and a Liquidity Coverage Ratio of 141% as of June 30, 2025, indicating solid capital adequacy and liquidity to manage financial risks.

| Metric | Value (as of June 30, 2025) | Significance |

|---|---|---|

| Total CRAR (Basel III) | 16.63% | Exceeds regulatory minimums, indicating strong capital buffer. |

| Liquidity Coverage Ratio (LCR) | 141% | Demonstrates ample liquidity to meet short-term obligations. |

| Customer Base | ~42 million | Reflects extensive market reach and customer trust. |

| Branches & Outlets | >3,110 | Highlights a broad physical distribution network. |

What is included in the product

This analysis maps out IndusInd Bank’s market strengths, operational gaps, and risks.

Provides a clear view of IndusInd Bank's competitive landscape, helping to identify and address potential threats and leverage opportunities.

Weaknesses

Significant Financial Discrepancies and Accounting Lapses

IndusInd Bank faced significant financial headwinds in Q4 FY25, reporting a net loss largely driven by increased provisioning and notable accounting lapses. These discrepancies included ₹674 crore misclassified as interest income over three quarters of FY25 and ₹595 crore in unverified balances within 'other assets.'

The discovery of these accounting irregularities has triggered a forensic probe and intensified internal audit reviews, casting a shadow over the bank's financial reporting integrity. Such issues can erode investor confidence and necessitate robust corrective actions to restore financial transparency.

Deteriorating Asset Quality and Rising Non-Performing Assets (NPAs)

IndusInd Bank faces a significant challenge with its deteriorating asset quality, evidenced by a rise in its Gross NPA to 3.64% and Net NPA to 1.12% as of June 30, 2025. This trend, particularly concerning in its microfinance and unsecured retail loan segments, will likely strain the bank's profitability due to increased provisioning requirements.

Decline in Profitability and Net Interest Margin (NIM) Contraction

IndusInd Bank experienced a substantial drop in net profit, plummeting by 72% year-on-year in the first quarter of fiscal year 2026. This sharp decline signals significant headwinds impacting the bank's bottom line.

Furthermore, the bank's Net Interest Margin (NIM) contracted to 3.46% in Q1 FY26, a notable decrease from 4.25% recorded in the same period last year. This contraction is primarily attributed to increased funding costs and a slowdown in loan growth, directly squeezing the bank's profitability on its core lending activities.

Governance Concerns and High-Level Executive Exits

Governance concerns, notably the discovery of accounting lapses, led to significant executive departures, including the CEO and Deputy CEO, in recent years. This triggered regulatory actions, such as the barring of the bank from accessing capital markets for a period, which directly impacted investor confidence and highlighted weaknesses in oversight. For instance, in 2024, the Reserve Bank of India imposed penalties on IndusInd Bank for certain governance lapses, underscoring ongoing scrutiny.

These high-level executive exits and the subsequent regulatory actions have cast a shadow over IndusInd Bank's corporate governance framework. The perceived instability at the top and the need for stronger oversight mechanisms have become a critical point of concern for stakeholders. This situation can deter potential investors and partners who prioritize robust governance structures. The bank's ability to attract and retain top talent is also potentially affected by these governance issues.

- Executive Departures: The resignations of key leadership figures like the CEO and Deputy CEO due to accounting issues.

- Regulatory Actions: Penalties and restrictions imposed by regulators, such as being barred from capital markets.

- Governance Framework Scrutiny: Increased focus on the bank's internal controls, audit processes, and overall corporate governance.

- Investor Confidence Impact: Negative sentiment among investors due to perceived governance weaknesses and past lapses.

Relatively Lower Branch Network Compared to Major Competitors

IndusInd Bank, while growing, operates a more limited physical branch network compared to some of its larger Indian banking rivals. As of March 31, 2024, the bank had 2,608 branches, which is significantly less than public sector banks like the State Bank of India, which boasts over 22,000 branches. This disparity could hinder its reach in traditional banking segments and rural geographies where a strong physical presence is still a key differentiator for customer acquisition and retention.

This smaller footprint might affect its ability to capture market share in areas heavily reliant on in-person banking services. For instance, while digital channels are expanding rapidly, a substantial portion of the Indian population, particularly in semi-urban and rural areas, still prefers or requires access to physical bank branches for various transactions and relationship management.

The bank's strategy has leaned towards digital transformation and agent-assisted models, which can be cost-effective. However, the comparative scarcity of branches presents a potential weakness in competing for customers who prioritize a robust physical banking infrastructure.

- Branch Network Size: IndusInd Bank had 2,608 branches as of March 31, 2024.

- Competitor Comparison: State Bank of India, a major competitor, operated over 22,000 branches as of the same period.

- Market Penetration Impact: A smaller network may limit penetration in rural and traditional banking segments.

- Customer Preference: Reliance on physical branches remains a factor for a segment of the Indian population.

Financial Headwinds: Irregularities, NPAs, and Governance Challenges

IndusInd Bank's financial performance in Q4 FY25 and Q1 FY26 was significantly impacted by accounting irregularities and a rise in non-performing assets. The bank reported a net loss in Q4 FY25, partly due to ₹674 crore misclassified as interest income and ₹595 crore in unverified balances, leading to a forensic probe. Furthermore, Gross NPA rose to 3.64% and Net NPA to 1.12% by June 30, 2025, particularly in microfinance and unsecured retail loans, necessitating higher provisioning and impacting profitability.

The bank's Net Interest Margin (NIM) contracted to 3.46% in Q1 FY26 from 4.25% in the prior year, driven by increased funding costs and slower loan growth. Compounding these issues are governance concerns, highlighted by executive departures and regulatory actions, including penalties from the RBI in 2024 for lapses, which have affected investor confidence and market access.

IndusInd Bank's physical branch network, numbering 2,608 as of March 31, 2024, is considerably smaller than that of major competitors like State Bank of India (over 22,000 branches). This limited footprint may hinder its ability to capture market share, especially in rural and semi-urban areas where traditional banking channels remain important for customer acquisition and retention.

Preview the Actual Deliverable

IndusInd Bank SWOT Analysis

This preview reflects the real document you'll receive—professional, structured, and ready to use. You'll gain a comprehensive understanding of IndusInd Bank's Strengths, Weaknesses, Opportunities, and Threats.

The content below is pulled directly from the final SWOT analysis. Unlock the full report when you purchase to explore detailed insights into the bank's strategic positioning.

Opportunities

Leveraging Growth in India's Digital Banking Landscape

India's digital banking sector is booming, fueled by widespread smartphone and internet access. IndusInd Bank is well-positioned to benefit, having already seen a significant increase in digital transactions.

The bank can further leverage this by investing in AI for personalized customer experiences and exploring open banking partnerships. This strategy aims to attract new customers and broaden its service portfolio in a rapidly evolving market.

Expansion into High-Growth Retail and MSME Segments

IndusInd Bank is strategically targeting high-growth areas like retail assets and the Micro, Small, and Medium Enterprises (MSME) sector. This focus aligns with India's robust economic expansion, presenting a significant opportunity for increased market penetration and lending.

The bank's 'INDIE for Business' initiative is a prime example of its commitment to the MSME segment. This specialized offering aims to capture a larger share of this vital market, which is a cornerstone of India's economic development and a rich source of lending opportunities.

Strategic Partnerships and Collaborations to Enhance Offerings

IndusInd Bank's strategic focus on partnerships is a significant growth avenue. By teaming up with fintech innovators, the bank can rapidly integrate cutting-edge digital solutions, broadening its product suite and accessing untapped customer segments. This approach proved fruitful in 2023, with the bank reporting a 25% year-on-year increase in its digital customer base, highlighting the effectiveness of such alliances.

The bank's collaboration on digital escrow services serves as a prime example of how external alliances bolster its value proposition. These partnerships not only enhance the bank's offerings but also sharpen its competitive edge in the rapidly transforming financial sector. For instance, its partnership with a leading e-commerce platform in early 2024 led to a 15% surge in transaction volumes for that specific segment.

Focus on ESG Principles to Attract Responsible Investments

IndusInd Bank's existing dedication to Environmental, Social, and Governance (ESG) principles positions it favorably to capture the increasing demand for sustainable finance. This focus directly appeals to a growing segment of investors prioritizing ethical and responsible business practices.

By deepening its ESG integration, IndusInd Bank can unlock access to a larger pool of capital from socially conscious investors. This strategic alignment not only bolsters its financial standing but also significantly enhances its long-term reputation and resilience in a market increasingly valuing sustainability.

- Attracting Responsible Capital: The global sustainable investment market is expanding rapidly, with assets under management projected to reach $50 trillion by 2025, according to Bloomberg Intelligence.

- Enhanced Brand Reputation: A strong ESG profile can differentiate IndusInd Bank, attracting customers and partners who align with its values.

- Risk Mitigation: Proactive ESG management can help identify and mitigate potential environmental and social risks, leading to more stable long-term performance.

- Regulatory Alignment: As regulatory frameworks globally increasingly emphasize ESG disclosure and performance, IndusInd Bank's existing commitment provides a competitive advantage.

Capitalizing on Financial Inclusion Initiatives

India's commitment to financial inclusion presents a significant opportunity for IndusInd Bank. As of December 2023, the Pradhan Mantri Jan Dhan Yojana (PMJDY) had over 51 crore accounts opened, highlighting the government's push to bring more people into the formal banking system. IndusInd Bank can tap into this expanding market by deploying its digital capabilities and hybrid physical-digital service models.

Leveraging technology is key to reaching India's vast rural and semi-urban populations who remain underserved. IndusInd Bank's focus on 'phygital' strategies, combining digital convenience with a physical presence, allows it to offer tailored products and services to these segments. This approach not only fosters national development by increasing access to credit and savings but also directly contributes to the bank's customer base expansion and market penetration.

The bank's efforts in this area align with broader economic trends. For instance, the digital payments ecosystem in India has seen exponential growth, with UPI transactions alone reaching an average of over 100 million per day in early 2024. IndusInd Bank can integrate these payment solutions into its offerings for the unbanked, making financial services more accessible and user-friendly.

Opportunities within financial inclusion include:

- Expanding digital banking services to rural areas, leveraging mobile penetration which stood at over 1.2 billion connections by late 2023.

- Developing micro-savings and micro-credit products tailored for low-income and informal sector customers.

- Partnering with fintech companies to create innovative, low-cost delivery channels for financial products.

- Utilizing data analytics to understand the needs of underserved segments and offer personalized financial solutions.

Capitalizing on India's Digital & Economic Surge

IndusInd Bank can capitalize on the burgeoning digital banking landscape in India, driven by increasing smartphone penetration. The bank's existing digital transaction growth and strategic investments in AI and open banking partnerships position it to attract new customers and expand its service offerings.

Targeting high-growth sectors like retail assets and MSMEs, alongside a focus on ESG principles, presents significant opportunities for market penetration and attracting responsible capital. The bank's commitment to financial inclusion, leveraging digital and 'phygital' strategies, also offers a substantial avenue for customer base expansion.

| Opportunity Area | Key Driver | IndusInd Bank's Position | Market Data/Potential |

|---|---|---|---|

| Digital Banking Growth | Increased smartphone & internet access | Strong digital transaction growth, AI/open banking focus | India's digital banking sector booming |

| MSME & Retail Lending | India's economic expansion | Targeting high-growth areas, 'INDIE for Business' | MSME sector is a cornerstone of India's economy |

| ESG & Sustainable Finance | Growing investor demand for ethical practices | Existing ESG commitment | Sustainable investment market projected to reach $50 trillion by 2025 |

| Financial Inclusion | Government push for formal banking | Leveraging digital/phygital models, UPI integration | Over 51 crore PMJDY accounts by Dec 2023; UPI transactions >100M/day (early 2024) |

Threats

Intense Competition from Diverse Financial Institutions

IndusInd Bank operates in a fiercely competitive Indian banking landscape. It contends with established public sector banks, major private players like HDFC Bank and ICICI Bank, and a burgeoning ecosystem of fintechs and NBFCs. This broad competitive set directly challenges IndusInd Bank's ability to maintain market share and profit margins across its product and service offerings.

Increased Regulatory Scrutiny and Potential Policy Changes

IndusInd Bank faces significant headwinds from increased regulatory scrutiny, particularly following past accounting irregularities and governance concerns. This heightened attention could translate into more stringent compliance requirements, potentially increasing operational costs. For instance, in the fiscal year ending March 31, 2024, Indian banks collectively saw a rise in compliance-related expenditures due to evolving regulatory landscapes.

Deterioration of Asset Quality Due to Macroeconomic Headwinds

While the Indian banking sector is generally stable, macroeconomic headwinds like economic slowdowns, persistent inflation, and rising interest rates pose a significant threat to asset quality. These conditions can particularly strain unsecured retail loans, microfinance portfolios, and loans extended to small businesses.

Such deterioration could necessitate higher provisioning by IndusInd Bank, directly impacting its profitability. For instance, if interest rates continue to climb, borrowers with variable rate loans may struggle with repayments, increasing the likelihood of defaults.

Data from the Reserve Bank of India (RBI) for FY23 indicated a Gross Non-Performing Asset (GNPA) ratio of 4.8% for public sector banks and 3.1% for private banks, showing an overall improvement. However, the projected economic growth for India in FY25, while robust, is subject to global uncertainties that could still pressure asset quality.

Cybersecurity Risks and Data Security Breaches

IndusInd Bank's growing digital footprint, while enhancing customer convenience, significantly elevates its exposure to cybersecurity risks. A data breach or cyberattack could result in substantial financial losses and erode the hard-won trust of its customer base.

In 2023, the global average cost of a data breach reached $4.45 million, a figure that underscores the potential financial impact on institutions like IndusInd Bank. Such incidents can also lead to severe reputational damage, impacting customer retention and acquisition efforts.

- Increased Digital Transactions: A rise in online and mobile banking activities presents a larger attack surface for cybercriminals.

- Sophistication of Threats: Evolving cyber threats, including ransomware and phishing attacks, require continuous investment in advanced security measures.

- Regulatory Scrutiny: Data protection regulations impose strict penalties for breaches, adding to the financial and operational risks.

Reputational Damage from Past Financial Lapses

IndusInd Bank has faced significant reputational challenges stemming from past financial irregularities. High-profile accounting discrepancies, such as misreported interest income and unsubstantiated balances, have come to light, leading to the resignation of key executives. These events have demonstrably eroded the bank's credibility in the market.

The fallout from these lapses could have a tangible impact on investor and public trust. This erosion of confidence may hinder deposit growth, complicate customer acquisition efforts, and ultimately depress the bank's market valuation. For instance, by the end of fiscal year 2024, the bank's stock performance reflected some of these concerns, though specific figures are subject to ongoing market fluctuations.

- Accounting Discrepancies: Reports of misstated interest income and unverified balances have directly impacted perceived financial integrity.

- Executive Resignations: The departure of top management following these issues signals internal governance concerns.

- Erosion of Trust: This damage to reputation can lead to reduced customer deposits and a lower market valuation.

- Investor Confidence: Rebuilding investor confidence will be crucial for sustained market performance and capital raising efforts.

Banking Sector Threats: Competition, Regulation, and Reputational Risks

IndusInd Bank faces intense competition from public sector banks, leading private players, and a growing fintech sector, which pressures its market share and profitability. Heightened regulatory scrutiny, particularly after past accounting issues, could increase compliance costs. Macroeconomic factors like inflation and rising interest rates pose risks to asset quality, potentially leading to higher loan loss provisions, especially for retail and microfinance segments.

Cybersecurity threats are a significant concern due to increasing digital transactions, requiring continuous investment in advanced security measures. Past accounting discrepancies and governance issues have damaged IndusInd Bank's reputation, potentially affecting customer trust, deposit growth, and market valuation.

| Threat Category | Specific Threat | Potential Impact | Data Point/Example |

|---|---|---|---|

| Competition | Intense competition from private and public banks, fintechs | Pressure on market share and margins | Indian banking sector has over 100 banks, with HDFC Bank and ICICI Bank as major private competitors. |

| Regulatory Environment | Increased regulatory scrutiny and compliance costs | Higher operational expenses, potential penalties | RBI's focus on governance and risk management continues to evolve, impacting all banks. |

| Macroeconomic Factors | Economic slowdown, inflation, rising interest rates | Deterioration in asset quality, increased provisioning | Projected GDP growth for India in FY25 remains strong, but global uncertainties persist. |

| Cybersecurity | Sophisticated cyber threats and data breaches | Financial losses, reputational damage, loss of customer trust | Global average cost of a data breach in 2023 was $4.45 million. |

| Reputational Risk | Past accounting irregularities and governance concerns | Erosion of investor and customer confidence, impact on valuation | Past incidents have led to executive changes and increased market scrutiny. |

SWOT Analysis Data Sources

This IndusInd Bank SWOT analysis is built upon a foundation of verified financial statements, comprehensive market research, and expert industry commentary to ensure a robust and accurate strategic assessment.