IndusInd Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

IndusInd Bank

From Overview to Strategy Blueprint

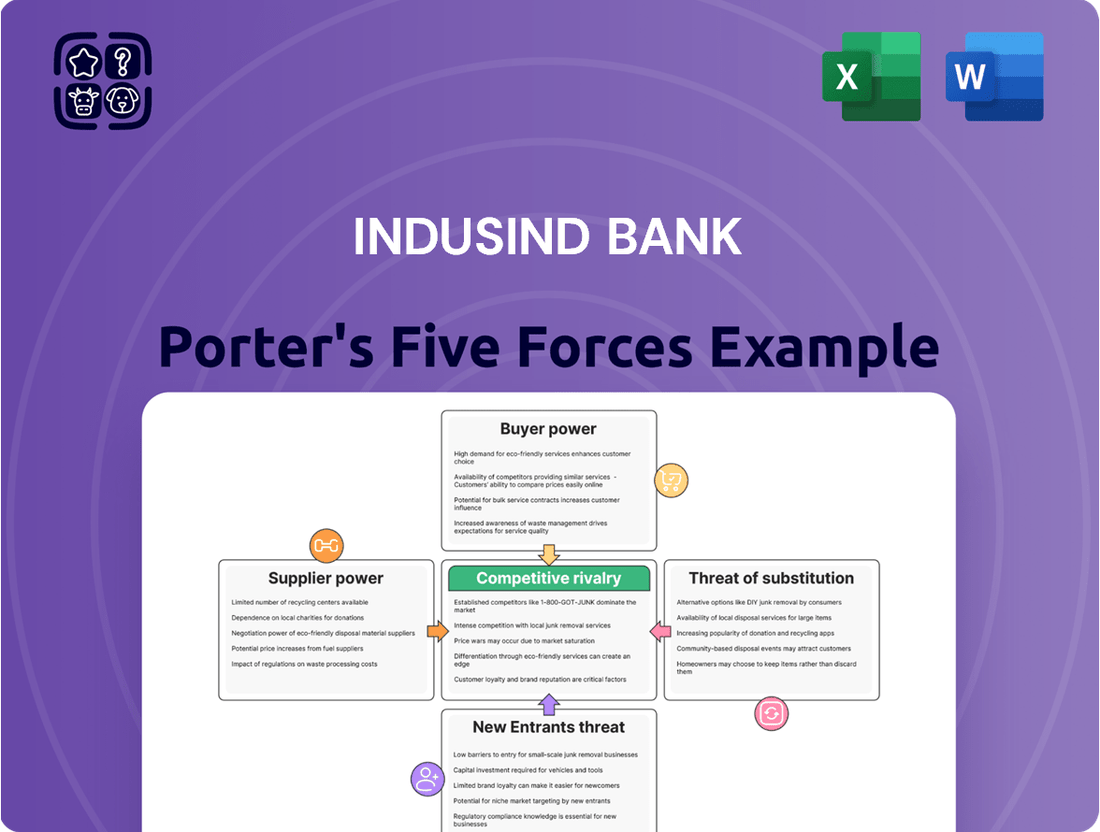

IndusInd Bank navigates a competitive landscape shaped by moderate buyer power and intense rivalry among established players. Understanding the threat of substitutes and the bargaining power of suppliers is crucial for its strategic positioning. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore IndusInd Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Depositor Power

Depositors, particularly those with substantial funds or actively seeking higher yields, exert considerable bargaining power over IndusInd Bank. The bank's cost of deposits saw an uptick in FY24, a clear signal that it must offer competitive interest rates to attract and retain essential funding in a dynamic financial landscape. This means depositors can often negotiate better terms, influencing the bank's profitability.

Furthermore, the Reserve Bank of India's (RBI) adjustments to the definition of bulk deposits could reshape how banks vie for larger customer accounts. This regulatory shift might intensify competition for significant deposit volumes, potentially granting these larger depositors even more leverage in securing favorable interest rates from institutions like IndusInd Bank.

Technology and Software Providers

IndusInd Bank's increasing reliance on digital transformation, AI, and cybersecurity solutions significantly boosts the bargaining power of technology and software providers. The bank's strategic focus on these areas means it depends heavily on these external partners for critical innovation and operational efficiency.

In 2024, the global IT spending by financial services is projected to reach over $300 billion, highlighting the substantial market for these tech suppliers. Furthermore, the growing demand for sophisticated RegTech solutions to navigate complex regulatory landscapes further empowers these providers, as they offer essential tools for compliance.

Human Capital and Specialized Talent

The banking, financial services, and insurance (BFSI) sector, including institutions like IndusInd Bank, faces a significant challenge in securing specialized talent. Areas like artificial intelligence, advanced data analytics, and stringent regulatory compliance require professionals with unique skill sets.

This scarcity of highly skilled individuals grants them considerable bargaining power. For instance, in 2024, the demand for AI and machine learning specialists in finance outstripped supply by an estimated 20%, leading to increased salary expectations and competitive recruitment packages for banks.

Consequently, IndusInd Bank, like its peers, must invest heavily in retention strategies and competitive compensation to attract and keep these in-demand professionals. The upward pressure on wages for these roles directly impacts operational costs and profitability.

Interbank and Wholesale Funding Markets

The interbank and wholesale funding markets act as significant suppliers for IndusInd Bank. While the bank saw a reduction in its overall borrowings in FY24, its reliance on these markets for liquidity means supplier power remains a consideration. Accessing these crucial funding sources at competitive rates is directly tied to IndusInd Bank's perceived financial stability and the prevailing market liquidity conditions.

IndusInd Bank's ability to manage its supplier power in these markets hinges on maintaining a strong liability structure. This involves attracting and retaining diverse funding sources beyond just deposits.

- Interbank Market Access: The cost of borrowing from other banks is influenced by their willingness to lend and the rates they demand, reflecting their own liquidity and risk appetite.

- Wholesale Funding Costs: Rates on certificates of deposit, commercial paper, and other wholesale instruments are set by market participants, with IndusInd Bank's creditworthiness being a key determinant.

- Liquidity Management: A robust liability franchise, including a stable deposit base and diversified wholesale funding, reduces dependence on any single supplier and enhances bargaining power.

- FY24 Borrowings: While specific figures for interbank and wholesale funding are part of the bank's overall borrowings, the trend indicates a strategic management of its funding mix.

Credit Rating Agencies

Credit rating agencies wield considerable power over banks like IndusInd Bank by acting as gatekeepers of crucial financial information. Their assessments directly influence a bank's cost of capital and its overall market perception. For instance, in early 2024, Moody's and India Ratings revised their outlook for IndusInd Bank to negative, citing concerns regarding internal controls and management succession. This action underscores the significant impact these agencies have on investor confidence and, consequently, on the bank's ability to secure funding at favorable rates.

The bargaining power of credit rating agencies stems from several factors:

- Information Asymmetry: Agencies possess specialized analytical capabilities and access to data that individual investors may lack, creating an information imbalance.

- Mandatory Requirements: Certain financial regulations and investment mandates require issuers to obtain credit ratings, creating a demand for their services.

- Reputational Capital: Established agencies have built significant trust and credibility over time, making their opinions highly influential.

- Limited Number of Major Players: The industry is dominated by a few large rating agencies, reducing the choices available to banks and increasing their leverage.

Suppliers' Leverage: Driving Bank Costs and Strategy

The bargaining power of suppliers for IndusInd Bank is multifaceted, encompassing depositors, technology providers, specialized talent, funding markets, and credit rating agencies. Each group can influence the bank's costs and operational flexibility.

Depositors, especially those with large sums, can negotiate better rates, as evidenced by the uptick in the bank's cost of deposits in FY24. Similarly, the increasing reliance on digital solutions empowers technology and software providers, with global IT spending in financial services projected to exceed $300 billion in 2024.

The scarcity of skilled professionals in areas like AI and data analytics, with demand outstripping supply by an estimated 20% for AI specialists in finance in 2024, grants them significant leverage, driving up recruitment costs.

The bank's access to interbank and wholesale funding markets also means these markets act as suppliers whose rates are influenced by IndusInd Bank's financial health and market liquidity.

Credit rating agencies, like Moody's and India Ratings which revised their outlook to negative for IndusInd Bank in early 2024, hold substantial power due to information asymmetry and regulatory requirements, directly impacting the bank's cost of capital.

What is included in the product

This Porter's Five Forces analysis for IndusInd Bank dissects the competitive landscape, examining threats from new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry within the banking sector.

Easily identify and mitigate competitive threats with a visual breakdown of Porter's Five Forces, enabling proactive strategic adjustments for IndusInd Bank.

Customers Bargaining Power

Low Switching Costs for Basic Services

For fundamental banking needs like savings accounts, individual customers face minimal hurdles when switching providers, granting them significant leverage. The increasing availability of digital banking platforms and streamlined account opening procedures further ease this transition.

This low barrier to entry means banks, including IndusInd Bank, must consistently innovate and improve their service quality and product portfolios to retain their customer base. In 2023, the average customer acquisition cost for retail banking in India was estimated to be around 3-5% of the customer's lifetime value, highlighting the expense associated with attracting new clients in a competitive landscape.

Diverse Clientele with Varying Power

IndusInd Bank caters to a broad customer base, encompassing individuals, corporations, and government bodies. This diversity means the bank must manage varying levels of customer influence.

Major corporate and institutional clients often wield significant bargaining power. Their substantial transaction volumes allow them to negotiate more favorable pricing and customized services, a common dynamic in the banking sector where large accounts are highly sought after.

While individual retail customers may have limited power on their own, their collective actions and preferences can shape market trends and product demand. For instance, shifts in retail savings patterns or loan demand can influence the bank's strategic focus.

Digital Empowerment and Accessibility

Digital banking platforms and mobile apps are significantly shifting power towards customers. With increased convenience and access, individuals can now effortlessly compare services and pricing across various financial institutions. IndusInd Bank's INDIE app, for instance, caters to this demand for digital solutions, but simultaneously enhances customers' ability to switch providers if better options emerge.

Access to Diverse Financial Products

Customers today enjoy a vast selection of financial products and services, from loans and credit cards to diverse investment options, all readily available from numerous providers. This abundance of choice significantly amplifies their bargaining power, as they can easily switch to or select offerings that provide the best value and meet their specific requirements in a highly competitive landscape.

IndusInd Bank, recognizing this dynamic, strives to meet customer demand by offering a comprehensive suite of products designed to cater to varied financial needs. For instance, as of early 2024, the Indian banking sector saw continued growth in digital lending, with platforms offering competitive rates and flexible terms, directly impacting customer expectations for service and pricing from all banks, including IndusInd.

- Increased Customer Choice: The proliferation of fintech companies and digital banking platforms has expanded the financial product universe, giving consumers more avenues to explore beyond traditional banks.

- Price Sensitivity: With easy comparison tools and readily available information on interest rates and fees across different institutions, customers are more sensitive to pricing and are likely to seek out the most cost-effective solutions.

- Demand for Value-Added Services: Beyond basic transactions, customers increasingly expect personalized financial advice, seamless digital experiences, and integrated services, which puts pressure on banks to innovate and differentiate their offerings.

Information Availability and Price Sensitivity

Customers today are much more informed. With the internet, they can easily check interest rates, fees, and how good the service is at various banks. This means they're more likely to shop around for the best deal.

This increased information availability directly impacts IndusInd Bank. For instance, in early 2024, the average savings account interest rate offered by major Indian banks hovered around 3-4%, but some digital-only banks were offering up to 5-6%. This puts pressure on traditional banks like IndusInd to offer competitive rates to retain customers.

- Informed Customers: Access to online comparison tools and financial news empowers customers to make more discerning choices.

- Price Sensitivity: Customers are increasingly comparing not just rates but also the overall value proposition, including digital services and customer support.

- Competitive Pressure: Banks must actively manage their pricing and service offerings to remain attractive in a transparent market.

Customer Power Reshapes Banking Landscape

The bargaining power of customers for IndusInd Bank is significant, driven by increased choice and information availability. Customers can easily compare interest rates, fees, and digital services across numerous financial institutions, pushing banks to offer competitive pricing and enhanced value propositions. For example, as of early 2024, the digital banking landscape in India saw innovative players offering attractive rates, putting pressure on traditional banks like IndusInd to match these offerings to retain their customer base.

| Factor | Impact on IndusInd Bank | Customer Action Example |

|---|---|---|

| Increased Digital Access | Lowers switching costs, enhances customer comparison capabilities. | Switching to a competitor for a better mobile banking experience or lower transaction fees. |

| Information Transparency | Customers are more aware of market rates and competitor offerings. | Negotiating for better loan rates or choosing a savings account with a higher interest yield. |

| Product Proliferation | Customers have a wider array of financial products to choose from. | Opting for specialized fintech solutions for investments or payments instead of traditional banking services. |

Same Document Delivered

IndusInd Bank Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. Our IndusInd Bank Porter's Five Forces Analysis details the competitive landscape, including the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the banking sector. This comprehensive report is ready for your immediate use.

Rivalry Among Competitors

Presence of Numerous and Diverse Players

The Indian banking landscape is incredibly crowded, with a mix of public sector giants, nimble private players, international banks, and specialized small finance banks all vying for customers. This fragmentation fuels a fierce competitive environment where every institution is constantly looking for an edge.

IndusInd Bank itself is a significant player, ranking as the 7th largest private sector bank in India. This means it's directly up against many well-established and resource-rich competitors who have a long history of serving the market and a deep understanding of customer needs.

The sheer volume of competitors forces banks like IndusInd to adopt aggressive strategies, whether through innovative product offerings, competitive pricing, or enhanced customer service. For instance, as of March 2024, the Indian banking sector had over 120 scheduled commercial banks, highlighting the intense rivalry.

Rapid Digitalization and Innovation Race

The banking sector is embroiled in a fierce innovation race, driven by significant investments in digital transformation, artificial intelligence, and data analytics. This intense competition compels banks to continuously enhance their offerings and operational capabilities to stay ahead.

IndusInd Bank's proactive approach, exemplified by its Digital 2.0 strategy and the launch of initiatives like INDIE for Business, directly addresses this competitive pressure. These efforts are designed to elevate customer experience and streamline internal operations, crucial for maintaining market relevance.

In 2024, the digital banking segment saw substantial growth, with many banks reporting double-digit increases in digital transactions. For instance, a significant portion of new customer acquisitions for leading banks are now happening through digital channels, underscoring the importance of these investments.

Regulatory Environment and Compliance Burden

The Reserve Bank of India's (RBI) stringent regulatory framework, covering capital adequacy, asset quality, and lending practices, significantly shapes competition among banks like IndusInd. Compliance with these evolving norms, including recent measures on unsecured retail credit, presents a substantial cost and a critical factor in a bank's ability to compete effectively.

Focus on Retail and MSME Segments

The banking sector is witnessing heightened competition, particularly within the retail lending, affordable housing, and MSME segments. This intensified focus by numerous financial institutions on these high-growth areas directly fuels aggressive rivalry, influencing pricing strategies and the distribution of market share.

IndusInd Bank is actively participating in this competitive landscape, leveraging its strong foundation in microfinance. The bank's strategic objective includes the digital empowerment of MSMEs, a key growth driver for the Indian economy.

- Retail Lending Growth: The Indian retail lending market is projected to grow significantly, with banks actively vying for customers in this segment.

- MSME Digitalization Push: IndusInd Bank's digital initiatives for MSMEs aim to capture a larger share of this rapidly expanding market.

- Intensified Competition: The concentration of multiple banks on similar customer bases and product offerings naturally escalates competitive pressures.

Pricing Pressure and Net Interest Margins

Intense competition in the Indian banking sector exerts significant pricing pressure on both deposits and loans, directly impacting net interest margins (NIMs). This dynamic forces banks to constantly re-evaluate their pricing strategies to remain competitive while safeguarding profitability.

IndusInd Bank, like its peers, navigates this challenging landscape. For the fiscal year ending March 31, 2024 (FY24), the bank’s net interest margin stood at 4.10%, a slight decrease from 4.21% in FY23. This contraction reflects the dual impact of increased funding costs and competitive pressures on lending rates.

- Competitive Pricing: Banks face pressure to offer attractive deposit rates to attract and retain customers, while also needing to price loans competitively to win market share.

- Rising Cost of Funds: Higher interest rates in the economy generally increase the cost for banks to borrow money, which can erode NIMs if not passed on effectively.

- Margin Management: IndusInd Bank’s FY24 NIM of 4.10% indicates a balancing act between maintaining growth ambitions and managing profitability amidst these pressures.

Indian Banking: Competition, Digital Drive, and Margin Pressure

The Indian banking sector is highly competitive, featuring over 120 scheduled commercial banks as of March 2024, including public sector banks, private players, and foreign institutions. This dense market forces institutions like IndusInd Bank to innovate aggressively, particularly in digital services and customer acquisition, to maintain market share.

IndusInd Bank, as the 7th largest private sector bank, faces intense rivalry from well-established competitors. The drive for digital transformation and AI adoption is a key battleground, with many banks reporting double-digit growth in digital transactions in 2024, pushing for enhanced customer experience and operational efficiency.

This competitive pressure directly impacts pricing, leading to tighter net interest margins (NIMs). IndusInd Bank’s NIM was 4.10% for FY24, down from 4.21% in FY23, reflecting increased funding costs and the need for competitive lending rates to attract and retain customers in high-growth segments like retail lending and MSME financing.

| Metric | IndusInd Bank (FY24) | Industry Trend |

| Number of Scheduled Commercial Banks | N/A (part of over 120) | High Fragmentation |

| Net Interest Margin (NIM) | 4.10% | Under Pressure (slight decline) |

| Digital Transaction Growth | Significant | Double-digit growth reported by peers |

SSubstitutes Threaten

Fintech Companies and Digital Payment Platforms

Fintech companies, with their innovative digital payment platforms and agile services in lending and wealth management, present a significant threat of substitutes for traditional banks like IndusInd. The widespread adoption of platforms such as Unified Payments Interface (UPI) in India, which facilitated over 13.4 billion transactions in the first half of 2024 alone, offers a convenient and often lower-cost alternative to cash and conventional bank transfers.

Non-Banking Financial Companies (NBFCs)

Non-Banking Financial Companies (NBFCs) present a significant threat of substitution for IndusInd Bank, particularly in specialized lending areas such as vehicle finance, microfinance, and personal loans. Their agile operational structures often allow them to provide quicker and more customized financial solutions compared to traditional banks, drawing in a segment of the customer base. By the end of the fiscal year 2023-24, the NBFC sector in India had grown substantially, with total assets managed by NBFCs reaching approximately INR 40 lakh crore, indicating their considerable market presence and competitive reach.

Emergence of Digital-Only Banks and Neo-banks

The emergence of digital-only banks and neo-banks presents a significant threat of substitutes for traditional banking services. These agile, tech-focused players, operating without the overhead of physical branches, are capturing market share by offering streamlined, often lower-cost, digital experiences. For instance, by mid-2024, several neo-banks reported substantial year-over-year growth in customer acquisition, with some reaching millions of active users, indicating a clear preference among a growing segment of the population for entirely digital banking solutions.

Direct Capital Markets and Investment Platforms

Investors increasingly bypass traditional bank intermediation for investment services, opting for direct access to capital markets. Online brokerage firms and wealth management platforms provide a wide array of investment products, often with lower fees, presenting a significant substitute for services offered by banks like IndusInd Bank. For instance, the growth of robo-advisors and direct-to-consumer investment platforms has democratized access to financial markets.

The threat from substitutes is amplified by the accessibility and cost-effectiveness of alternative investment channels. In 2024, the global digital wealth management market is projected to continue its robust expansion, with many platforms offering commission-free trading on certain assets. This trend directly challenges traditional banking models that rely on fees and commissions for investment advisory and execution services.

- Direct Market Access: Online platforms allow investors to directly purchase stocks, bonds, and other securities, bypassing bank-managed funds or advisory services.

- Cost Efficiency: Many substitute platforms offer lower transaction fees and management costs compared to traditional bank investment products.

- Product Diversification: Alternative platforms often provide a broader range of investment options, including niche markets and alternative assets, that may not be readily available through a single bank.

- Technological Advancement: User-friendly interfaces, advanced analytics, and personalized recommendations offered by fintech substitutes enhance the investor experience.

Embedded Finance Solutions

Embedded finance solutions present a significant threat of substitutes for traditional banking services. By integrating financial functionalities directly into non-financial platforms, these solutions offer customers convenience and context, potentially bypassing direct engagement with banks. For instance, a customer purchasing goods on an e-commerce site might opt for a buy-now-pay-later option directly integrated into the checkout process, rather than applying for a credit card from a bank.

This trend is rapidly gaining traction. By the end of 2023, the global embedded finance market was projected to reach approximately $2.5 trillion, with expectations of further substantial growth. This indicates a clear shift in consumer behavior, where financial transactions are becoming an ancillary part of other digital experiences.

- Convenience: Embedded finance offers financial services at the point of need, reducing friction for consumers.

- Contextual Relevance: Financial products are offered within the user's current activity, making them more appealing.

- Market Growth: The embedded finance market is experiencing exponential growth, demonstrating its increasing adoption.

- Customer Loyalty: Non-financial platforms offering seamless embedded finance can foster greater customer loyalty.

Digital Disruptors Challenge Traditional Banking

The threat of substitutes for IndusInd Bank is substantial, stemming from a diverse range of financial service providers and technological innovations. These substitutes often offer greater convenience, lower costs, or more specialized services, directly challenging traditional banking models. The increasing digital savviness of consumers and the rapid evolution of fintech are key drivers behind this intensifying competitive landscape.

Fintech companies, particularly those offering digital payments and lending, are significant substitutes. The Unified Payments Interface (UPI) in India, for example, processed over 13.4 billion transactions in the first half of 2024, showcasing a clear shift towards digital alternatives. Similarly, Non-Banking Financial Companies (NBFCs) are capturing market share in specialized lending, with their sector managing approximately INR 40 lakh crore in assets by March 2024.

Digital-only banks and embedded finance solutions also pose a considerable threat. Neo-banks are rapidly acquiring customers, with some reaching millions of active users by mid-2024. Embedded finance, projected to reach $2.5 trillion globally by the end of 2023, integrates financial services into non-financial platforms, offering seamless user experiences that bypass traditional banking channels.

| Substitute Type | Key Offerings | 2024 Market Indicator/Trend |

| Fintech Payment Platforms | Digital payments, money transfers | UPI transactions exceeded 13.4 billion (H1 2024) |

| Non-Banking Financial Companies (NBFCs) | Specialized lending (vehicle, personal) | NBFC assets managed approx. INR 40 lakh crore (FY 2023-24) |

| Neo-banks/Digital Banks | Online account opening, digital services | Rapid customer acquisition, some reaching millions of users (mid-2024) |

| Embedded Finance | Point-of-sale lending, integrated payments | Global market projected to reach $2.5 trillion (end of 2023) |

Entrants Threaten

High Regulatory Barriers and Capital Requirements

The Indian banking sector, overseen by the Reserve Bank of India (RBI), presents substantial hurdles for new players. Stringent licensing processes, significant capital infusion mandates, and a complex web of compliance regulations effectively act as gatekeepers, making it incredibly difficult for aspiring entities to launch full-scale banking operations.

These high entry barriers are a critical factor in limiting the threat of new entrants. For instance, as of 2024, the minimum paid-up voting equity capital requirement for a new universal bank in India is INR 500 crore, a substantial sum that deters many smaller or less capitalized firms. This capital requirement, coupled with ongoing operational and regulatory compliance costs, significantly raises the ante for any potential competitor.

Established Brand Loyalty and Customer Trust

Established brand loyalty and customer trust represent a significant barrier for new entrants aiming to compete with incumbents like IndusInd Bank. IndusInd Bank, like other major players, has spent years building strong brand recognition and fostering deep customer relationships. In 2023, IndusInd Bank reported a customer base exceeding 35 million, demonstrating the scale of established trust it commands. Newcomers must overcome the inertia of existing customer loyalty and the inherent trust placed in well-known financial institutions.

Digital Transformation Lowering Entry Barriers for Fintech

The digital revolution significantly reduces barriers for new players in financial services. Fintech startups can bypass the extensive physical infrastructure and regulatory hurdles faced by traditional banks, allowing them to enter specific market segments more easily. For instance, companies offering digital wallets or peer-to-peer lending platforms can operate with a fraction of the capital required for a full-service bank.

Government Initiatives and Financial Inclusion

Government initiatives focused on financial inclusion and the creation of digital public infrastructure (DPI) can lower barriers to entry for new financial service providers. These frameworks, like India Stack, simplify customer onboarding and transaction processing, making it easier for specialized fintechs to target specific market segments.

For instance, the Pradhan Mantri Jan Dhan Yojana (PMJDY) has significantly expanded access to banking services, with over 51 crore accounts opened as of May 2024. This widespread digital footprint, coupled with the Unified Payments Interface (UPI) enabling over 13 billion transactions in the first four months of 2024, provides a ready-made ecosystem for new entrants to build innovative financial products and services, potentially siphoning off customer bases from established banks like IndusInd.

- DPI Facilitates New Entrants: Digital public infrastructure streamlines customer acquisition and service delivery, reducing the need for extensive physical branch networks.

- Financial Inclusion Drives Market Growth: Government programs expand the addressable market, attracting new players eager to serve previously unbanked or underbanked populations.

- UPI's Transaction Volume: The sheer volume of UPI transactions in early 2024 demonstrates the public's adoption of digital payments, a key enabler for new fintechs.

- PMJDY Account Numbers: The substantial number of PMJDY accounts indicates a large, digitally-enabled customer base accessible to new market participants.

Potential Entry of Large Technology Companies

Large technology companies, often referred to as "Big Tech," represent a significant threat of new entrants into the financial services landscape. Their extensive user bases, coupled with vast amounts of data and robust digital infrastructure, provide a powerful springboard for entering and disrupting traditional banking and financial services. For instance, by mid-2024, companies like Apple, Google, and Amazon have already made inroads into payments and lending, demonstrating their potential to rapidly capture market share.

These tech giants can leverage their existing platforms and deep customer relationships to offer integrated financial products seamlessly. This allows them to bypass many of the traditional barriers to entry that financial institutions face. Their ability to innovate quickly and adapt to changing consumer preferences further amplifies this threat. For example, the continued expansion of digital wallets and embedded finance solutions by these companies in 2024 highlights their strategic focus on capturing a larger slice of the financial services pie.

The threat is particularly pronounced in areas like digital payments, personal loans, and wealth management. Their capacity to offer user-friendly interfaces and personalized experiences, often at lower costs due to their scale and technological prowess, makes them formidable competitors. As of early 2024, the growth in fintech adoption, often driven by these tech players, indicates a clear shift in consumer behavior towards digital-first financial solutions.

- Big Tech's User Base Advantage: Companies like Apple and Google boast billions of active users, providing an immediate customer pool for financial services.

- Data Monetization Potential: Access to extensive user data allows for sophisticated credit scoring and personalized financial product offerings.

- Digital Infrastructure Strength: Existing cloud computing and payment processing capabilities reduce the need for significant new infrastructure investment.

- Innovation Speed: Tech companies are known for rapid product development and iteration, enabling them to quickly respond to market demands.

Digital Disruption: New Entrants Challenge Banking's Old Guard

While traditional banking faces high capital and regulatory hurdles, the threat of new entrants is amplified by digital public infrastructure and fintech innovation. Government initiatives like PMJDY have onboarded over 51 crore accounts by May 2024, and UPI facilitated over 13 billion transactions in the first four months of 2024, creating a fertile ground for specialized digital financial services to emerge and attract customers from established banks.

Big Tech companies pose a significant threat due to their vast user bases, data capabilities, and digital infrastructure. Companies like Apple and Google are already expanding into payments and lending, leveraging their existing platforms to offer integrated financial products seamlessly, potentially disrupting traditional banking models.

| Factor | Impact on New Entrants | Example for IndusInd Bank Context |

|---|---|---|

| Regulatory Hurdles | High (Licensing, Capital) | Minimum INR 500 crore capital for new universal banks in India (2024). |

| Customer Loyalty | Significant Barrier | IndusInd Bank's 35+ million customer base (2023) signifies strong established trust. |

| Digital Public Infrastructure (DPI) | Lowers Barriers | PMJDY accounts (51 crore+ by May 2024) and UPI transactions (13 billion+ Jan-Apr 2024) enable new fintechs. |

| Big Tech Presence | High Threat | Tech giants' user bases and data offer rapid market entry in payments and lending. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for IndusInd Bank is built upon a foundation of diverse and credible data sources. We leverage annual reports, investor presentations, and official company disclosures to understand internal strategies and financial health.

Furthermore, we incorporate insights from reputable financial news outlets, industry-specific publications, and market research reports to gauge external competitive pressures and industry trends.