ICICI Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

ICICI Bank

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

ICICI Bank operates within a dynamic financial landscape shaped by intense competition, evolving customer expectations, and regulatory shifts. Understanding the interplay of these forces is crucial for strategic advantage.

This preview only scratches the surface of ICICI Bank's competitive environment. Unlock the full Porter's Five Forces Analysis to explore ICICI Bank’s strategic advantages, market pressures, and detailed competitive dynamics.

Suppliers Bargaining Power

Depositor Base as a Key Supplier

ICICI Bank's significant depositor base, which stood at ₹12.81 lakh crore in 2024, represents a critical supplier relationship. This substantial pool of funds gives depositors leverage, particularly in a market where banks compete fiercely for capital. The bank's ability to attract and retain these deposits directly influences its funding costs and overall liquidity management.

Limited Number of Technology Providers

ICICI Bank's dependence on a select few technology providers for its crucial banking systems and digital platforms significantly bolsters supplier bargaining power. Companies like Infosys, TCS, Wipro, and Oracle, which are major players in the IT services sector, hold considerable sway due to their specialized expertise and market concentration.

This limited pool of capable vendors means ICICI Bank has fewer alternatives when negotiating contracts or seeking new solutions, allowing these suppliers to dictate terms and pricing more effectively. The sheer scale of the global fintech market, projected to exceed $150 billion in 2024, underscores the substantial value and demand placed on these technology providers.

High Switching Costs for Core Systems

Migrating from one core banking system to another is a significant undertaking for a bank like ICICI Bank, involving substantial complexity and expense. These high switching costs inherently bolster the leverage of current technology providers.

The financial burden associated with such a transition is considerable, with estimates placing the cost of migrating core banking technology providers between ₹75-100 crore. This figure encompasses critical elements like system migration, the intricate process of data transfer, and comprehensive staff training to ensure operational continuity.

Reliance on Skilled Human Capital

The growing need for specialized skills in areas like digital banking, data analytics, and cybersecurity is giving skilled employees considerable leverage. This intense competition for talent can drive up labor expenses and create recruitment and retention hurdles for institutions such as ICICI Bank.

This reliance on specialized human capital significantly impacts the bargaining power of suppliers, as the availability and cost of these critical skills become a key factor. For ICICI Bank, securing and retaining top talent in these high-demand fields is paramount to maintaining its competitive edge and operational efficiency.

- Digital Banking Expertise: Demand for professionals skilled in developing and managing digital platforms is soaring.

- Data Analytics Professionals: The ability to interpret vast amounts of data is crucial for strategic decision-making.

- Cybersecurity Specialists: Protecting sensitive financial data is a top priority, increasing the value of these experts.

- Salary Benchmarks: In 2024, the average salary for data scientists in India was approximately ₹12 lakhs per annum, illustrating the high cost of specialized talent.

Regulatory Influence on Supplier Power

The Reserve Bank of India's (RBI) regulatory framework profoundly shapes the banking landscape, impacting everything from funding costs to lending rates. These regulations, designed to ensure financial stability, can indirectly cap the bargaining power of depositors, who are essentially suppliers of capital to banks like ICICI Bank. For instance, while depositors might seek higher interest rates, RBI's monetary policy directives and capital adequacy norms can constrain a bank's ability to offer significantly elevated rates.

In 2024, the RBI continued to manage liquidity and interest rates through various policy tools. For example, the repo rate, a key benchmark, remained a significant factor influencing the cost of funds for banks. Changes in these rates, driven by the RBI's assessment of inflation and economic growth, directly affect the interest banks can offer to depositors, thereby modulating the suppliers' bargaining power.

- RBI's Monetary Policy: The repo rate, a key indicator of the cost of borrowing for banks, influences the interest rates offered to depositors.

- Liquidity Management: RBI's actions to manage liquidity in the banking system can impact the availability and cost of funds, affecting supplier power.

- Capital Adequacy Norms: Regulations on capital requirements can influence a bank's risk appetite and its ability to attract deposits at competitive rates.

- Financial Stability Mandate: The RBI's overarching goal of financial stability allows it to intervene and set parameters that can limit extreme bargaining by any single group of suppliers.

Unpacking a Bank's Supplier Bargaining Power in 2024

ICICI Bank's bargaining power with suppliers is influenced by several factors, including its substantial depositor base, which reached ₹12.81 lakh crore in 2024, giving depositors some leverage. However, the Reserve Bank of India's (RBI) regulatory framework, including its management of liquidity and interest rates via tools like the repo rate, plays a significant role in moderating this power by influencing the rates banks can offer.

| Supplier Group | Bargaining Power Factor | Impact on ICICI Bank (2024) |

|---|---|---|

| Depositors | Size of depositor base (₹12.81 lakh crore in 2024) | Moderate to High leverage, especially in competitive capital markets. |

| Technology Providers | Specialized expertise, market concentration, high switching costs (₹75-100 crore migration cost) | High leverage due to limited alternatives and complexity of system changes. |

| Skilled Employees | Demand for digital banking, data analytics, cybersecurity skills (e.g., ₹12 lakh avg. data scientist salary) | Moderate to High leverage, driving up labor costs and retention challenges. |

| Regulators (RBI) | Monetary policy, liquidity management, capital adequacy norms | Indirectly limits supplier power by setting parameters for funding costs and rates. |

What is included in the product

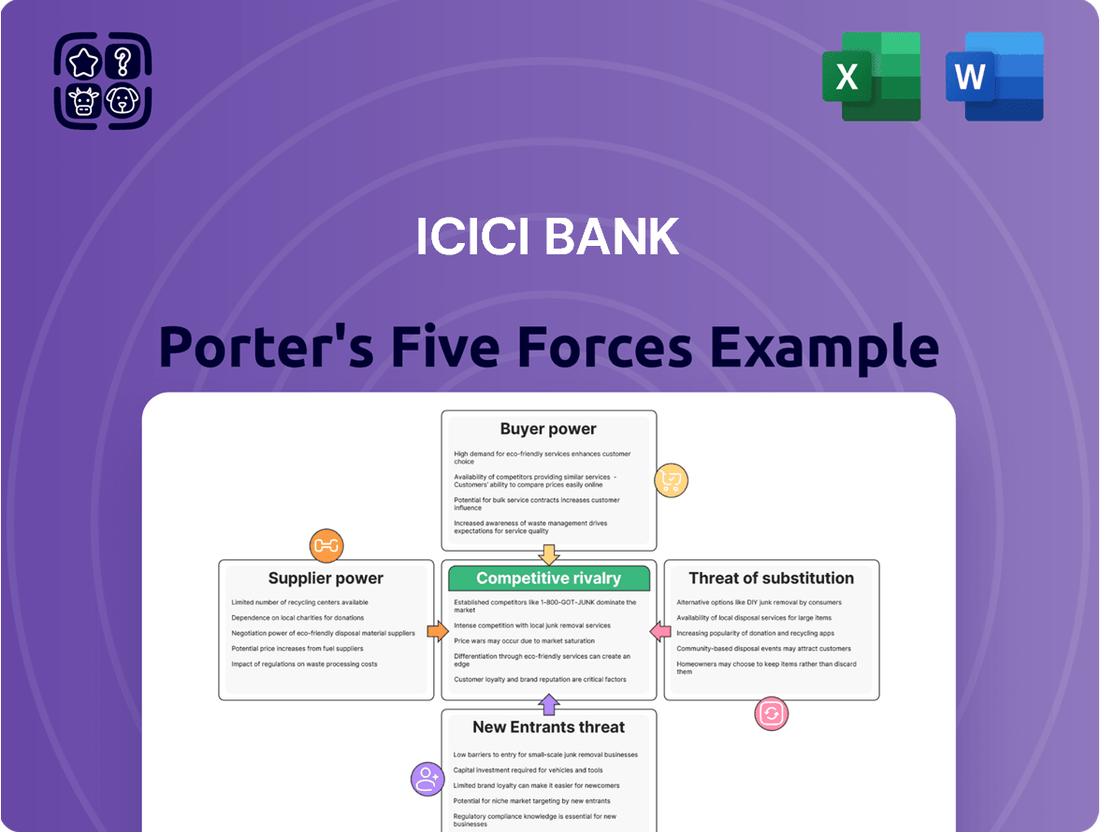

This analysis delves into the competitive forces impacting ICICI Bank, examining the intensity of rivalry, the bargaining power of customers and suppliers, and the threat of new entrants and substitutes.

Instantly identify and address competitive threats by visualizing the intensity of each of Porter's Five Forces for ICICI Bank, allowing for proactive strategy adjustments.

Customers Bargaining Power

Low Switching Costs for Basic Services

Customers can easily switch between banks for fundamental services, a trend amplified by streamlined digital onboarding. This low friction environment compels ICICI Bank to consistently deliver attractive pricing and enhanced customer experiences to secure loyalty.

The ease of changing providers means ICICI Bank needs to remain competitive on rates and service quality. Data from 2024 suggests retail banking churn rates hover between 10% and 15%, highlighting the dynamic nature of customer retention.

Numerous Banking Options Available

The Indian banking landscape is incredibly diverse, featuring a vast number of public, private, foreign, and cooperative banks. This fragmentation means customers have a wealth of options when choosing a bank. For instance, as of March 2024, India had over 12,000 cooperative banks, alongside hundreds of public and private sector banks, all competing for market share.

This abundance of choice significantly enhances the bargaining power of customers. They can easily switch banks if they find better rates, services, or digital offerings elsewhere. This forces ICICI Bank to continuously innovate and offer compelling value propositions to retain its customer base.

The intense competition compels ICICI Bank to focus on differentiating its services and maintaining competitive pricing. In 2023, the Net Interest Margins for major private banks in India hovered around 3.5-4.0%, indicating the pressure to offer attractive deposit rates and competitive loan pricing.

Increased Digital Empowerment

Customers are more empowered than ever due to the widespread adoption of digital banking and readily available market information online. This allows them to easily compare products, services, and interest rates from various financial institutions, thereby strengthening their bargaining position.

ICICI Bank's own data highlights this shift, with 94.2% of its total transactions occurring digitally as of recent reports. This high digital engagement signifies customers’ ability to quickly access and evaluate offerings, increasing their power to negotiate better terms.

Rising Expectations for Personalized Services

Customers today expect banking services tailored precisely to their needs, a shift fueled by sophisticated AI and data analytics. ICICI Bank needs to harness these technologies to provide customized loan rates, personalized investment guidance, and smooth digital interactions to keep pace with these evolving demands. This strong customer desire for personalization directly shapes how products are created and services are delivered.

This increased expectation for bespoke financial solutions means customers can exert more pressure on banks like ICICI. For instance, in 2024, reports indicated a significant rise in customer churn in the digital banking sector when personalization efforts were perceived as lacking, with some studies suggesting up to a 15% increase in switching rates due to poor digital experience. This highlights the direct impact of personalization on customer loyalty and bargaining power.

- Hyper-personalization: Customers demand financial products and advice that are uniquely suited to their individual circumstances and goals.

- Data-driven insights: The ability of banks to leverage AI and data analytics to understand and anticipate customer needs is crucial.

- Digital experience: Seamless and intuitive digital platforms are now a baseline expectation, not a differentiator.

- Customer retention: Failure to meet these personalization expectations can lead to increased customer attrition, giving customers more leverage.

Impact of Loyalty Programs and Rewards

Loyalty programs, while designed to keep customers engaged, face a significant challenge from the ease with which customers can switch banks and the sheer number of financial service providers available. This high degree of substitutability, coupled with a growing customer preference for personalized benefits like cashback and digital rewards, can dilute the impact of traditional loyalty schemes.

Banks and fintech companies are actively using these reward systems to incentivize credit card usage and digital transactions. For instance, in 2023, the global loyalty management market was valued at approximately USD 3.5 billion, indicating a strong investment in customer retention strategies, though the actual effectiveness in mitigating customer bargaining power remains a point of contention due to low switching costs.

- Customer Preference: Growing demand for personalized rewards, cashback, and digital incentives.

- Low Switching Costs: Customers can easily move between financial institutions.

- Competitive Landscape: Numerous alternatives available from traditional banks and fintechs.

- Loyalty Program Effectiveness: Programs aim to reward usage but may be undermined by easy switching.

Customer Power: ICICI Bank's Key Competitive Challenge

The bargaining power of customers with ICICI Bank is substantial, driven by the ease of switching and the vast array of banking options available in India. Customers can readily compare interest rates, fees, and digital services across numerous public, private, and cooperative banks, as well as fintech providers. This competitive environment necessitates that ICICI Bank consistently offers superior value, competitive pricing, and personalized experiences to retain its clientele.

| Factor | Impact on ICICI Bank | Supporting Data (as of early 2024) |

|---|---|---|

| Ease of Switching | High customer mobility pressures pricing and service quality. | Retail banking churn rates estimated between 10-15%. |

| Availability of Alternatives | Intensifies competition, forcing differentiation. | Over 12,000 cooperative banks in India, plus numerous public and private sector banks. |

| Digital Adoption | Enables quick comparison and access to better offers. | ICICI Bank reports 94.2% of transactions are digital. |

| Demand for Personalization | Requires tailored products and services to prevent attrition. | Reports suggest up to 15% increase in switching due to lack of personalization. |

Same Document Delivered

ICICI Bank Porter's Five Forces Analysis

This preview displays the complete ICICI Bank Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape. The document you see here is the exact, professionally formatted report you will receive instantly upon purchase, ensuring you get precisely what you need for your strategic planning. This comprehensive analysis delves into the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the banking sector.

Rivalry Among Competitors

Intense Competition from Numerous Players

ICICI Bank operates within a fiercely competitive Indian banking landscape. The sector is populated by a vast array of public sector banks, private sector institutions, foreign banks, and cooperative banks, all vying for the same pool of customers. This crowded market naturally escalates the rivalry.

This intense competition means banks are in a perpetual battle for market share and profitability. For instance, as of March 31, 2024, the Indian banking sector comprised 12 public sector banks, 21 private sector banks, and 43 foreign banks, all actively competing for customer deposits and loans.

Aggressive Market Strategies and Innovation

Banks, including ICICI Bank, actively employ aggressive market strategies. This often involves dynamic adjustments to interest rates on loans and deposits, a crucial tactic for customer acquisition and retention in the competitive banking sector.

Innovation is a constant theme, especially in digital banking. ICICI Bank, for instance, has focused on enhancing its digital platforms and launching novel financial products. This includes features like instant loan approvals and highly personalized banking experiences, directly responding to the intense competition.

In 2023, ICICI Bank reported a 30% year-on-year growth in its retail loan portfolio, underscoring the effectiveness of its customer-centric strategies and product innovation in attracting and serving a wider customer base.

Pressure on Profitability and Margins

The intense competition in India's banking landscape significantly pressures profitability and net interest margins. Banks frequently adjust lending and deposit rates, directly affecting their net interest income. ICICI Bank's net interest margin stood at around 4.5% in 2024, reflecting this challenging environment.

Digital Transformation Driving Rivalry

The banking sector is experiencing heightened competition, largely fueled by rapid digital transformation and the emergence of agile fintech companies. This digital wave compels traditional banks like ICICI to significantly invest in their technological infrastructure and customer-facing digital platforms to maintain relevance and attract customers.

Banks are aggressively enhancing their digital capabilities and customer experience to gain a competitive edge. This includes developing user-friendly mobile apps, seamless online banking services, and innovative digital payment solutions.

- Digital Transaction Growth: Digital transactions in India saw a substantial increase of 25% in 2024, underscoring the critical role of digital proficiency in the current competitive landscape.

- Fintech Disruption: The rise of fintech startups offering specialized, often more convenient, digital financial services presents a direct challenge to established banks.

- Investment in Technology: Banks are channeling significant capital into AI, cloud computing, and data analytics to improve operational efficiency and personalize customer offerings.

- Customer Experience Focus: A superior digital customer experience is becoming a key differentiator, with banks striving for intuitive interfaces and responsive support.

Undifferentiated Products and Services

Many banking services, including savings accounts, current accounts, and personal loans, are largely indistinguishable across institutions. Competitors frequently and rapidly copy successful innovations and technological features, such as mobile banking apps and digital payment solutions. This makes it difficult for banks like ICICI Bank to establish a unique selling proposition based on product features alone.

This lack of differentiation compels banks to compete intensely on factors like interest rates, fees, and customer service quality. For instance, in 2024, the average savings account interest rate offered by major Indian banks hovered around 3% to 4%, creating a price-sensitive environment. The ease with which new digital services are replicated means that any competitive edge gained through technology is often short-lived, intensifying the rivalry.

- Product Homogeneity: Core banking products and services offered by ICICI Bank and its rivals often lack significant differentiation.

- Rapid Imitation: Successful technological advancements and product launches are quickly adopted by competitors, diminishing their unique value.

- Price and Service Competition: The absence of distinct offerings forces competition to focus on price (interest rates, fees) and service efficiency.

- Intensified Rivalry: Continuous copying of services and technology fuels a high level of competition within the Indian banking sector.

India's Banking Battle: Digital Drives Intense Rivalry

Competitive rivalry within India's banking sector is exceptionally high, driven by a large number of players including public, private, and foreign banks, alongside emerging fintech firms. This intense competition forces banks like ICICI Bank to constantly innovate and adjust pricing strategies, impacting profitability.

The rapid digital transformation further fuels this rivalry, with banks investing heavily in technology to enhance customer experience and offer seamless digital services. However, the inherent homogeneity of core banking products means that differentiation is often short-lived, leading to a focus on price and service quality.

| Metric | ICICI Bank (2024) | Indian Banking Sector (2024) |

|---|---|---|

| Net Interest Margin | ~4.5% | Varies, but generally under pressure due to competition |

| Digital Transaction Growth | Significant contributor to overall growth | ~25% increase in digital transactions |

| Retail Loan Portfolio Growth | 30% year-on-year (2023) | Strong growth across the sector |

SSubstitutes Threaten

Rise of Fintech Companies

Fintech companies are a major threat of substitutes for traditional banks like ICICI Bank. They offer specialized financial services, often with greater efficiency and user-friendliness, bypassing conventional banking. These agile firms are innovating in payments, lending, and wealth management, directly challenging established players.

The rapid growth of fintech is evident in global revenue projections, which are expected to reach $325 billion by 2025. This expansion highlights their increasing ability to attract customers seeking modern, technology-driven financial solutions, thereby posing a significant competitive pressure.

Digital Payment Platforms and Wallets

The proliferation of digital payment platforms, exemplified by India's Unified Payments Interface (UPI), presents a significant threat of substitutes to traditional banking services. UPI's remarkable growth, with over 6.5 billion transactions recorded in a recent quarter, underscores its increasing dominance in everyday financial exchanges. This shift diminishes customer loyalty to established banking channels for routine payments.

Growth of Non-Banking Financial Companies (NBFCs)

The growth of Non-Banking Financial Companies (NBFCs) presents a significant threat of substitutes for traditional banks like ICICI Bank. NBFCs, offering a wide array of financial products from loans and wealth management to insurance, directly compete with bank services. For instance, in 2023, the Indian NBFC sector saw its assets under management grow by approximately 10-12%, indicating a substantial increase in their market presence and customer reach.

These specialized financial entities often provide more tailored solutions and can operate with greater agility, leading to quicker loan approvals or more personalized investment advice. This agility allows them to capture market share by appealing to customers seeking alternatives to conventional banking channels. The increasing accessibility and diverse offerings from NBFCs mean customers have more choices, intensifying competitive pressure on established banks.

Emergence of Embedded Finance

The rise of embedded finance poses a significant threat of substitution for traditional banking services. This model integrates financial products directly into non-financial platforms, such as e-commerce sites or ride-sharing apps, allowing customers to access services like loans or payments at the point of need. For instance, a customer buying a product online might be offered point-of-sale financing directly on the retailer's website, bypassing the need to visit a bank's portal.

This integration fundamentally alters customer behavior and expectations, making traditional banking channels less relevant. By offering convenience and contextual relevance, embedded finance solutions can attract customers away from incumbent banks. For example, many neobanks and fintech companies are partnering with businesses to offer banking-like services, potentially capturing market share from established players like ICICI Bank.

The competitive landscape is shifting as non-financial companies become de facto financial service providers. This trend is projected to grow substantially; reports indicate that embedded finance transactions could reach trillions of dollars globally in the coming years. Specifically, the buy now, pay later (BNPL) segment, a prime example of embedded finance, saw significant growth in 2023 and is expected to continue its upward trajectory.

- Embedded finance allows financial services within non-financial platforms.

- Customers gain access to credit or insurance at their point of need.

- This blurs industry lines, creating new competitive pressures.

- The global embedded finance market is projected for significant growth, with BNPL as a key driver.

Shift to Alternative Investment Avenues

Indian households are increasingly channeling their savings into alternative investment avenues like mutual funds and direct equity. This trend, driven by the pursuit of higher returns, directly competes with traditional bank deposits. For instance, mutual fund assets under management (AUM) in India surged by over 30% in FY2024, reaching approximately INR 54.5 trillion by March 2024, showcasing a significant diversion of funds.

This shift poses a threat of substitution for ICICI Bank, as it can reduce the inflow of low-cost retail deposits, which are a crucial funding source for banks. As more investors opt for market-linked instruments, banks may face increased competition for capital, potentially impacting their net interest margins and overall liquidity.

- Growing popularity of mutual funds: Mutual fund AUM in India crossed INR 54.5 trillion by March 2024, indicating a strong preference for these instruments.

- Direct equity market growth: The number of demat accounts in India crossed the 150 million mark by early 2024, reflecting increased retail participation in the stock market.

- Impact on bank deposits: This migration of savings from bank deposits to alternative investments can constrain a bank's ability to fund its lending activities.

- Search for higher yields: Investors are actively seeking instruments that offer returns potentially higher than those typically available through savings accounts or fixed deposits.

Financial Services Face Digital Disruption and Emerging Competitors

The proliferation of digital payment platforms, such as India's UPI, offers a direct substitute for traditional banking payment services. UPI's rapid adoption, with over 6.5 billion transactions in a recent quarter, highlights its convenience and widespread use for everyday financial exchanges, potentially reducing reliance on bank-specific payment channels.

Fintech companies continue to innovate, offering specialized services in lending, wealth management, and payments that bypass conventional banking infrastructure. Global fintech revenue is projected to reach $325 billion by 2025, underscoring their growing appeal and ability to attract customers seeking modern, efficient financial solutions.

Non-Banking Financial Companies (NBFCs) are increasingly offering a broad spectrum of financial products, directly competing with ICICI Bank's services. The Indian NBFC sector's assets under management grew by roughly 10-12% in 2023, demonstrating their expanding market presence and customer reach.

Embedded finance, where financial services are integrated into non-financial platforms like e-commerce sites, presents a significant substitution threat. This model offers convenience at the point of need, potentially diverting customers from traditional banking interactions. The buy now, pay later (BNPL) segment, a key aspect of embedded finance, saw substantial growth in 2023.

| Substitute Type | Key Characteristics | Market Trend/Data Point | Impact on ICICI Bank |

| Digital Payment Platforms (e.g., UPI) | Convenience, speed, wide adoption | 6.5 billion+ transactions in a recent quarter | Reduced transaction fees, diminished loyalty for basic payments |

| Fintech Companies | Specialized services, agility, user-friendliness | Global revenue projected to reach $325 billion by 2025 | Competition for customer acquisition and retention, pressure on margins |

| NBFCs | Diverse financial products, tailored solutions | 10-12% AUM growth in India (2023) | Competition for lending and deposit base, potential disintermediation |

| Embedded Finance (e.g., BNPL) | Contextual relevance, seamless integration | Significant growth in BNPL segment in 2023 | Loss of direct customer interaction, potential erosion of core banking services |

Entrants Threaten

High Regulatory Barriers for Traditional Banks

The Indian banking sector presents a formidable challenge for new entrants due to the stringent regulatory framework established by the Reserve Bank of India (RBI). Obtaining a banking license is an arduous process, requiring substantial capital and adherence to strict operational guidelines. For instance, in 2023, the RBI continued to emphasize robust capital adequacy ratios, with many established banks comfortably exceeding the Basel III requirements, a benchmark that new players must meet from day one.

These high regulatory barriers, including extensive compliance obligations and rigorous capital requirements, significantly deter potential new traditional banks from entering the market. The RBI's deliberate approach prioritizes the stability of the financial system and the safeguarding of customer deposits, effectively limiting the ease of market entry for aspiring banks.

Need for Significant Capital Investment

Establishing a new bank, like ICICI Bank, demands a massive initial capital outlay. This includes setting up physical branches, investing in robust IT infrastructure, and crucially, building a reputation of trust and reliability, which can take years and significant financial commitment. For instance, as of early 2024, regulatory capital requirements for new banks in many major economies remain substantial, often running into hundreds of millions of dollars, effectively deterring many aspiring entrants.

This high barrier to entry means that the threat of new competitors emerging to challenge established players like ICICI Bank is relatively low. Existing banks already possess the necessary infrastructure, economies of scale, and a loyal customer base, giving them a significant advantage over any newcomer who would have to start from scratch. ICICI Bank's extensive network of over 6,000 branches and a digital presence reaching millions across India in 2024 underscores this entrenched advantage.

Established Brand Loyalty and Trust

Established brand loyalty and trust represent a significant hurdle for new entrants aiming to compete with established players like ICICI Bank. For instance, in 2024, customer retention rates in the Indian banking sector remained high, with many consumers preferring to stick with banks they have long trusted for their financial needs.

Overcoming this deeply ingrained customer confidence, built through years of reliable service and consistent brand messaging, is a formidable task. New banks must invest heavily in marketing and customer acquisition to even begin chipping away at this loyalty, a costly endeavor that can deter potential entrants.

Fintech Startups as Digital Entrants

The threat of new entrants for ICICI Bank is significantly shaped by the burgeoning fintech sector. Unlike the capital-intensive and heavily regulated path to becoming a traditional bank, fintech startups can emerge with focused digital offerings, bypassing many legacy barriers.

These agile players often leverage India's robust digital public infrastructure, such as the Unified Payments Interface (UPI), to rapidly acquire customers and market share in specific financial service areas. This digital-first approach allows them to operate with lower overheads and offer competitive, often niche, solutions.

India's high fintech adoption rate, standing at 87% as of recent data, underscores the significant opportunity for these new entrants. This widespread acceptance means consumers are readily embracing digital financial tools, creating a fertile ground for startups to challenge established players like ICICI Bank by offering specialized and convenient services.

- Fintechs bypass traditional banking entry barriers.

- Leverage digital infrastructure like UPI for rapid growth.

- India's 87% fintech adoption rate fuels new entrants.

- Niche digital services pose a competitive threat.

Potential for NBFCs to Convert to Banks

The possibility of large Non-Banking Financial Companies (NBFCs) converting into full-service banks presents a significant threat of new entrants for established banks like ICICI Bank. Discussions around this policy shift are ongoing, indicating a potential, albeit regulated, pathway for new and substantial players to enter the banking sector.

While the Reserve Bank of India (RBI) Governor has voiced concerns about potential conflicts of interest arising from corporate entities obtaining banking licenses, this regulatory evolution could fundamentally alter the competitive landscape. Such a conversion would allow well-capitalized NBFCs with existing customer bases and operational expertise to leverage these strengths within a full banking framework.

- Regulatory Evolution: Ongoing discussions about NBFCs converting to banks signal a potential shift in market entry barriers.

- RBI Concerns: The RBI Governor has highlighted inherent conflicts of interest for corporates seeking banking licenses, suggesting a cautious approach to new entrants.

- Competitive Impact: Successful conversions could introduce formidable new competitors with established market presence and financial muscle.

- Market Dynamics: This potential policy change could significantly reshape the competitive forces within the Indian banking sector.

Navigating New Entrants: Fintech, NBFCs, and Regulatory Shifts

The threat of new entrants for ICICI Bank is somewhat mitigated by high regulatory hurdles and substantial capital requirements for traditional banks. However, the rapidly evolving fintech landscape presents a more dynamic challenge. India's strong digital infrastructure and high fintech adoption rates, reaching 87% in 2024, empower agile new players to offer specialized digital services, bypassing many legacy entry barriers.

Furthermore, ongoing policy discussions regarding Non-Banking Financial Companies (NBFCs) converting into full-service banks could introduce well-capitalized entities with existing customer bases, potentially altering the competitive dynamics. While the RBI remains cautious about corporate conflicts of interest, this regulatory evolution could lead to new, formidable competitors.

| Factor | Impact on New Entrants | Relevance to ICICI Bank |

|---|---|---|

| Regulatory Capital Requirements | High barrier for traditional banks | Limits new traditional bank entrants |

| Fintech Agility | Bypasses legacy barriers, leverages digital infrastructure | Direct competitive threat in niche services |

| NBFC Conversion Potential | Pathway for well-capitalized entities | Potential for new, strong competitors |

| Customer Trust & Loyalty | Difficult for new entrants to replicate | Existing advantage for ICICI Bank |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for ICICI Bank is built upon a foundation of reliable data, including the bank's annual reports, investor presentations, and filings with regulatory bodies like SEBI. We also incorporate insights from reputable financial news outlets, industry research reports from firms like CRISIL and Fitch, and macroeconomic data from sources such as the Reserve Bank of India.