Fuyao Glass Industry Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Fuyao Glass Industry Group Bundle

A Must-Have Tool for Decision-Makers

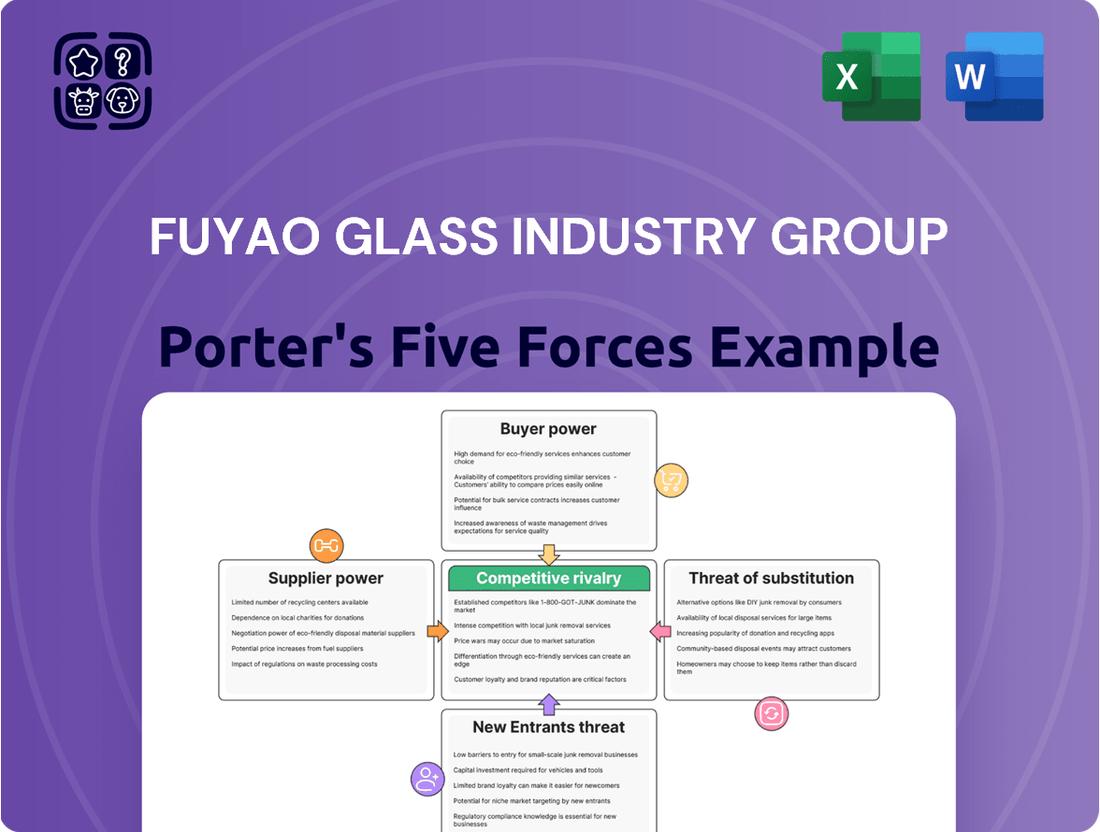

Fuyao Glass Industry Group navigates an industry characterized by moderate buyer power, as automotive manufacturers seek cost-effective, high-quality glass. The threat of new entrants is somewhat limited by significant capital requirements and established relationships, yet emerging players can still disrupt the market. The intensity of rivalry is high, with several global competitors vying for market share, pushing for innovation and efficiency.

The bargaining power of suppliers, particularly for raw materials like silica and soda ash, presents a moderate challenge, as fluctuations in these inputs can impact production costs. Furthermore, the threat of substitutes, while not immediate in the automotive sector, looms with the potential for advanced materials to replace traditional glass in the long term.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fuyao Glass Industry Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Concentration and Uniqueness of Inputs

Fuyao Glass Industry Group depends on essential inputs such as float glass, polyvinyl butyral (PVB) interlayer, and specific chemicals for its diverse product lines. The influence these suppliers wield is directly tied to their market concentration and the distinctiveness of their products. As demand for laminated glass grows, the importance of specialized interlayers, often sourced from a limited number of providers, intensifies, thereby enhancing supplier leverage.

Switching Costs for Fuyao

Switching costs for Fuyao can significantly impact the bargaining power of its suppliers. If a supplier provides highly specialized materials or proprietary technology crucial for Fuyao's advanced products, like components for smart glass or advanced driver-assistance systems (ADAS) windshields, switching becomes costly. For instance, in 2024, integrating new materials for ADAS features often requires extensive R&D and recalibration of manufacturing processes, potentially adding millions in upfront investment for Fuyao.

The expense and time involved in establishing new supplier relationships and retooling production lines to meet different material specifications present a substantial barrier. This process can delay product launches and disrupt supply chains, directly benefiting suppliers who have already invested in meeting Fuyao's stringent requirements. Fuyao's reliance on these specialized inputs means suppliers can leverage this dependency to negotiate more favorable terms, thus increasing their bargaining power.

Threat of Forward Integration by Suppliers

The threat of suppliers integrating forward into automotive glass manufacturing, like Fuyao Glass Industry Group, is typically low. This is primarily because entering this sector demands substantial capital, highly specialized technology, and existing relationships with Original Equipment Manufacturers (OEMs), which are difficult for raw material suppliers to replicate. For example, setting up an automotive glass production line can easily cost hundreds of millions of dollars, a significant barrier for most raw material providers.

Importance of Fuyao to its Suppliers

Fuyao Glass, as a dominant force in the automotive glass sector, wields considerable influence over its suppliers. Its substantial procurement volumes mean that many raw material providers rely heavily on Fuyao's business. This dependence grants Fuyao a degree of bargaining power, particularly when dealing with suppliers of more standardized or less specialized inputs. For instance, in 2023, Fuyao's revenue reached approximately $3.4 billion USD, underscoring its massive purchasing capacity. Suppliers are incentivized to offer competitive pricing and favorable terms to secure and maintain such a significant client relationship.

The bargaining power Fuyao holds is further amplified by the nature of its supply chain. While some specialized chemicals or advanced materials might come from fewer sources, many core inputs are more widely available. This allows Fuyao to switch suppliers or negotiate aggressively if prices become unfavorable. The company's scale means that even a slight price reduction on key materials can translate into substantial cost savings. This dynamic ensures that suppliers must remain competitive to retain Fuyao's patronage.

Consider these points regarding Fuyao's supplier relationships:

- Significant Customer: Fuyao's global market share makes it a critical revenue source for many of its raw material suppliers.

- Volume Leverage: The sheer quantity of materials Fuyao purchases allows it to negotiate better prices and terms.

- Supplier Dependence: For many smaller or less diversified suppliers, Fuyao represents a disproportionately large percentage of their sales.

- Market Conditions: The availability and concentration of suppliers for specific raw materials directly impact Fuyao's bargaining strength.

Impact of Raw Material Price Fluctuations

Fluctuations in raw material prices, particularly for float glass and aluminum, can significantly affect Fuyao Glass Industry Group's profitability. For instance, global commodity prices saw notable volatility in 2024, with energy and transportation costs also contributing to supply chain pressures. While Fuyao's considerable purchasing volume provides some leverage against suppliers, sustained increases in the cost of critical inputs like silica sand and specialized chemicals could still squeeze its profit margins.

The bargaining power of suppliers for Fuyao is influenced by several factors:

- Concentration of Suppliers: If there are few suppliers for key raw materials, their collective bargaining power increases.

- Uniqueness of Input: Highly specialized or proprietary materials give suppliers more leverage.

- Switching Costs: High costs associated with changing suppliers can empower existing ones.

- Threat of Forward Integration: Suppliers who could potentially enter Fuyao's business might wield more power.

Supplier Leverage: Balancing Volume with Specialized Input Power

The bargaining power of Fuyao Glass Industry Group's suppliers is moderate. While Fuyao's substantial purchasing volume, evidenced by its $3.4 billion USD revenue in 2023, grants it significant leverage, the uniqueness and concentration of certain input suppliers can elevate their influence.

For specialized materials critical to advanced products, such as those for ADAS windshields, suppliers can command stronger terms due to high switching costs for Fuyao. For example, integrating new materials in 2024 often requires significant R&D and production recalibration, making supplier dependence a real factor.

Conversely, for more commoditized inputs like basic chemicals, Fuyao's scale allows for aggressive price negotiation and supplier diversification, thus limiting supplier power in those segments.

| Factor | Impact on Supplier Bargaining Power | Example for Fuyao Glass |

|---|---|---|

| Fuyao's Purchasing Volume | Reduces Supplier Power | $3.4 billion USD revenue (2023) indicates strong negotiation leverage. |

| Supplier Concentration (Specialized Inputs) | Increases Supplier Power | Limited providers of proprietary interlayers for smart glass. |

| Switching Costs (New Technology Integration) | Increases Supplier Power | High R&D and recalibration costs for ADAS windshield materials (2024). |

| Availability of Alternative Suppliers (Commoditized Inputs) | Reduces Supplier Power | Numerous suppliers for basic chemicals and float glass. |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Fuyao Glass Industry Group's position in the global automotive glass market.

Understand competitive intensity with a visual representation of how Fuyao Glass navigates buyer power and supplier leverage, clarifying strategic positioning.

Customers Bargaining Power

Customer Concentration and OEM Dominance

Fuyao Glass Industry Group faces significant bargaining power from its primary customers: major global automobile manufacturers, or OEMs. These include prestigious brands like Bentley, Mercedes-Benz, BMW, Audi, General Motors, and Toyota. This concentration means that a few key buyers hold considerable sway in pricing and contract negotiations.

The OEM segment dominated the automotive glass market in 2024, representing a substantial 78.50% of its revenue. This high market share for OEMs underscores their purchasing power and influence over suppliers like Fuyao.

While Fuyao's customer base is concentrated, its top five customers represented only 17.75% of its revenue in 2024. This suggests that while customer concentration is a factor, the company has managed to avoid an over-reliance on any single client, mitigating some of the extreme bargaining power risks.

Customer Switching Costs

Customer switching costs for automotive original equipment manufacturers (OEMs) are substantial. These costs arise from rigorous qualification processes, lengthy supply contracts, and the intricate technical integration needed for components like automotive glass.

Once Fuyao Glass Industry Group successfully integrates its products into an OEM's vehicle design and manufacturing workflow, the effort and expense for an OEM to switch to a new supplier become considerable. This includes significant re-engineering, extensive testing, and potential disruptions to production lines, creating a degree of customer loyalty for Fuyao.

For instance, the automotive industry often involves multi-year supply agreements, and the lead time for qualifying a new glass supplier can extend to 18-24 months, encompassing design validation and production trials. This lengthy integration process acts as a significant barrier to switching, thereby increasing Fuyao's bargaining power.

Price Sensitivity of Customers

Automotive original equipment manufacturers (OEMs) are acutely aware of price, given the intense competition within their own industry. This means they are always on the lookout for ways to cut costs, and this pressure trickles down to their suppliers. For Fuyao Glass, this translates into a significant bargaining power for its automotive clients. In 2024, the automotive sector continued to navigate supply chain complexities and fluctuating consumer demand, amplifying the need for cost control among OEMs.

Threat of Backward Integration by Customers

The threat of automotive original equipment manufacturers (OEMs) integrating backward into glass manufacturing for Fuyao Glass Industry Group is considerably low. This is largely due to the substantial capital outlay and highly specialized technical expertise needed to produce automotive-grade glass efficiently and at scale. In 2024, the automotive glass market demands advanced manufacturing processes, including sophisticated tempering, laminating, and coating technologies, which are core competencies of established players like Fuyao.

OEMs generally concentrate on vehicle design, assembly, and marketing, preferring to outsource specialized components to expert suppliers. This allows them to avoid the massive investments and operational complexities associated with glass production. For instance, the cost of setting up a state-of-the-art automotive glass manufacturing facility can run into hundreds of millions of dollars, a significant barrier for OEMs not specializing in this area. Fuyao Glass, as a dedicated automotive glass supplier, benefits from established economies of scale and optimized production lines.

- High Capital Investment: Establishing automotive glass production requires significant upfront investment in specialized machinery, R&D, and facilities, deterring OEMs.

- Technical Expertise: Automotive glass manufacturing involves complex processes like chemical tempering and advanced coating, requiring specialized knowledge Fuyao Glass possesses.

- Economies of Scale: Fuyao Glass, as a leading global supplier, achieves production efficiencies and cost advantages that are difficult for individual OEMs to replicate.

- Focus on Core Competencies: OEMs prioritize their core business of vehicle assembly, relying on specialist suppliers for component innovation and quality.

Demand for Advanced Glass Solutions

The automotive industry's growing appetite for sophisticated glass technologies, including lightweight materials, energy-saving features, and smart glass integrated with Advanced Driver-Assistance Systems (ADAS), directly impacts the bargaining power of customers. This escalating demand for high-value, technologically advanced components can actually bolster the position of innovative suppliers like Fuyao Glass, particularly if they are at the forefront of these developments.

Fuyao's ability to meet these evolving customer needs is crucial. For instance, the automotive sector's push towards electric vehicles (EVs) necessitates lighter glass to improve range, and the integration of ADAS requires specialized glass for sensor visibility. Companies that can deliver these cutting-edge solutions gain leverage.

- Demand for ADAS-compatible glass: As ADAS features become standard, automakers require glass that seamlessly integrates cameras and sensors without signal interference.

- Lightweighting trend: The drive for fuel efficiency and EV range extension pushes demand for thinner, lighter, yet equally strong automotive glass solutions.

- Smart glass adoption: Features like electrochromic dimming and heads-up display (HUD) integration are increasingly sought after, requiring specialized glass manufacturing capabilities.

Customer Bargaining Power Dominates Automotive Glass

The bargaining power of customers for Fuyao Glass is considerable, primarily driven by the concentration of major automotive manufacturers as its key buyers. These OEMs, including giants like Toyota and General Motors, represent a significant portion of the automotive glass market, giving them considerable leverage in price negotiations and contract terms. While Fuyao has managed to diversify its client base, with its top five customers accounting for a manageable 17.75% of revenue in 2024, the inherent power of these large buyers remains a critical factor. The high switching costs for OEMs, due to extensive integration and qualification processes, do offer some mitigation, but the constant pressure for cost reduction from these customers is a persistent challenge.

| Customer Type | Market Share (2024) | Fuyao's Revenue Share (Top 5 Customers, 2024) | Key Bargaining Factors |

| Automotive OEMs | 78.50% | 17.75% | Price sensitivity, potential for backward integration (though low), supplier switching costs (high, but negotiation power remains) |

What You See Is What You Get

Fuyao Glass Industry Group Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The analysis details Fuyao Glass Industry Group's competitive landscape, evaluating the intensity of rivalry among existing competitors, the bargaining power of suppliers, the threat of new entrants, the bargaining power of buyers, and the threat of substitute products. This comprehensive assessment equips you with a clear understanding of the external forces shaping Fuyao Glass's strategic position and future prospects.

Rivalry Among Competitors

Number and Size of Competitors

The global automotive glass market is a crowded arena with several significant international companies vying for market share. Fuyao Glass Industry Group finds itself in direct competition with established giants such as AGC Inc., Saint-Gobain Sekurit, and Pilkington, which is part of the NSG Group. Another formidable competitor is Xinyi Glass.

Fuyao Glass, however, holds a distinct advantage as the world's largest manufacturer of automotive glass. This scale provides significant leverage in terms of production capacity and cost efficiency, allowing them to compete aggressively on price and volume.

Industry Growth Rate

The automotive glass market is on a solid growth trajectory, with projections indicating it will reach USD 29.21 billion by 2030. This upward trend, reflecting a compound annual growth rate of 5.5% from 2025 to 2030, suggests a market with ample room for expansion. Such healthy growth can act as a buffer against intense competitive rivalry, as opportunities are more readily available for all industry participants.

Several key factors are fueling this expansion. Increased global vehicle production is a primary driver, creating a larger demand base for automotive glass. Furthermore, tightening safety regulations worldwide necessitate the use of more advanced and robust glass solutions, contributing to market value. The burgeoning electric vehicle (EV) segment also plays a significant role, often requiring specialized glass for features like panoramic roofs and improved aerodynamics, further diversifying demand and potentially easing direct competition.

Product Differentiation and Innovation

Competitive rivalry in the automotive glass sector is intensifying, with companies like Fuyao Glass Industry Group increasingly differentiating themselves through product innovation. The focus is shifting towards advanced features such as smart glass technology, which offers dynamic tinting capabilities, and the integration of lightweight materials to improve fuel efficiency. This push for higher-value-added products is a key battleground for market share.

Fuyao's strategic investments in research and development are critical in this environment. By developing specialized products like intelligent panoramic sunroof glass, which can incorporate advanced functionalities, and windshields designed for Advanced Driver-Assistance Systems (ADAS), Fuyao aims to secure a competitive edge. These innovations directly address evolving automotive trends and consumer demands for more sophisticated vehicle features.

High Fixed Costs and Exit Barriers

The automotive glass manufacturing sector, where Fuyao Glass Industry Group operates, is characterized by substantial fixed costs. This is primarily due to the immense capital required for float glass production lines and sophisticated processing equipment. For instance, a modern float glass plant can easily cost hundreds of millions of dollars to build and equip.

These high fixed costs create significant barriers to entry and exit for companies in the industry. When demand softens, firms with high fixed costs are compelled to operate at lower capacity, often leading to intense price competition as they try to cover their overhead. Fuyao Glass, being a major player, must navigate this dynamic where underutilization can severely impact profitability.

The substantial investment in manufacturing facilities means that exiting the market is not a simple decision. Companies face considerable losses if they try to sell off specialized, capital-intensive assets. This situation can trap firms in the industry, even when market conditions are unfavorable, further intensifying rivalry among existing players.

Consider these points regarding high fixed costs and exit barriers:

- Capital Intensity: The automotive glass industry demands massive upfront investment in plant, property, and equipment, making it a capital-intensive business.

- Price Pressure: High fixed costs can force manufacturers to compete aggressively on price to maintain production volume and cover expenses.

- Exit Barriers: The specialized nature of assets and the scale of investment make it difficult and costly for companies to leave the market, thereby increasing competitive intensity.

- Operational Leverage: Once operational, the variable costs are relatively lower than fixed costs, meaning that sales volume significantly impacts profitability, driving a desire for high utilization rates.

Global Presence and Strategic Partnerships

Fuyao Glass Industry Group's global presence is a significant factor in competitive rivalry. With production bases and R&D centers spanning North America, Europe, and Asia, Fuyao effectively serves major automotive original equipment manufacturers (OEMs) across the globe. This extensive network allows for localized production and faster response times, crucial in the fast-paced automotive supply chain.

Strategic partnerships and acquisitions further bolster Fuyao's competitive standing. For instance, their investment in a US float glass plant enhances supply chain control and expands market reach within a key automotive manufacturing region. Such moves are vital for maintaining market share against competitors who also operate on a global scale.

- Global Production Footprint: Fuyao operates manufacturing facilities and R&D centers in key automotive markets worldwide, enabling efficient service to global OEMs.

- Strategic Investments: Acquisitions and investments, such as the US float glass plant, are employed to strengthen supply chain integration and deepen market penetration.

- OEM Relationships: Strong, long-term relationships with major automotive manufacturers are cultivated through reliable supply and advanced technological capabilities.

- Competitive Landscape: Fuyao competes with other large, globally integrated glass manufacturers who also possess extensive production networks and strategic alliances.

Automotive Glass: Intense Rivalry, Growth, and Innovation

Competitive rivalry within the automotive glass sector is intense, featuring global players like AGC, Saint-Gobain, and Pilkington. Fuyao Glass, as the world's largest automotive glass manufacturer, leverages its scale for cost efficiency and volume, though differentiation through advanced features like smart glass and ADAS-compatible windshields is crucial. The market's growth, projected to reach USD 29.21 billion by 2030, offers opportunities but also fuels competition among established and emerging manufacturers.

SSubstitutes Threaten

Alternative Materials for Automotive Glazing

The threat of substitutes for automotive glazing is a significant consideration for Fuyao Glass. Alternative materials like polycarbonate and reinforced polymers are emerging as viable options, driven by their lighter weight and superior impact resistance. These characteristics are particularly attractive for the automotive industry, especially with the growing focus on electric vehicles where every kilogram saved contributes to improved range and fuel efficiency.

These advanced polymers offer potential advantages in safety and performance. For instance, polycarbonate glazing can be up to 50% lighter than traditional glass, directly impacting a vehicle's energy consumption. The automotive sector's ongoing pursuit of lightweighting strategies to meet stringent emissions standards and enhance the performance of EVs means these substitute materials will continue to be a relevant threat.

Performance and Cost of Substitutes

While alternatives like polycarbonate offer advantages in weight and impact resistance, traditional glass, particularly laminated variants, continues to hold a strong market position. This is largely due to its superior optical clarity and a more favorable cost structure for Original Equipment Manufacturers (OEMs). For instance, automotive windshields, a key market for Fuyao Glass, still overwhelmingly utilize glass, with advancements in laminated glass technology enhancing safety and durability without significantly increasing costs compared to plastics.

Technological Advancements in Substitutes

Advancements in polymer science are making glass alternatives more appealing, offering improved optical clarity and thermal stability. These materials also boast enhanced recyclability, a growing concern for many industries. For example, by 2024, the global market for advanced polymers used in automotive glazing was projected to reach billions, signaling a significant shift.

The increasing integration of smart functionalities, such as embedded sensors or displays, into these polymer substitutes could broaden their application scope significantly. This technological leap could allow them to perform functions far beyond what traditional glass can offer, posing a direct competitive threat to glass manufacturers like Fuyao Glass.

Customer Acceptance and Regulatory Hurdles

Customer acceptance of alternatives to traditional automotive glass for critical visibility components remains low. This is primarily due to stringent safety regulations and ingrained consumer expectations regarding durability and optical clarity. For instance, while advanced polymers are explored, their widespread adoption for windshields faces significant hurdles in meeting current crash test standards and maintaining long-term performance against scratching and UV degradation. In 2024, the automotive industry continues to prioritize glass for its proven track record in safety and performance, making the threat of substitutes in this core area relatively weak.

Regulatory frameworks are a key determinant in the adoption of alternative materials for vehicle glazing. Agencies like the National Highway Traffic Safety Administration (NHTSA) in the U.S. and similar bodies globally set rigorous standards for windshields, impact resistance, and optical properties. These regulations often favor materials with a long history of proven safety, like glass, creating a barrier for newer technologies. The slow pace of regulatory approval for novel materials means that Fuyao Glass Industry Group, as a major supplier of automotive glass, faces limited immediate threat from substitutes in the primary glazing market.

- Limited Consumer Acceptance: Consumers still largely prefer glass for windshields due to perceived safety and optical quality.

- Regulatory Barriers: Safety standards set by bodies like NHTSA favor established materials like glass.

- Durability Concerns: Alternatives like polymers face challenges meeting long-term durability and scratch resistance requirements.

- Slow Adoption of New Materials: The pace of regulatory approval for novel glazing materials is gradual, limiting immediate substitute threats.

Niche Applications for Substitutes

Substitutes for automotive glass are more likely to emerge and gain acceptance in niche applications initially. Think about areas like interior decorative panels, sunroofs, or even specific, non-critical windows where the performance demands are less stringent than for a windshield or side window. These segments could be testing grounds for alternative materials.

For instance, while automotive glass is the undisputed leader for windshields and sidelites due to safety and visibility requirements, materials like advanced polymers or composites might find early adoption in less critical areas. By 2024, the global automotive glass market was valued at approximately $20 billion, with windshields and sidelites representing the largest share. However, innovation in lighter, more impact-resistant plastics continues, potentially impacting lower-demand applications first.

- Niche Market Entry: Substitutes often target specialized applications before challenging core markets.

- Material Innovation: Advanced polymers and composites are being developed with properties that could suit less critical automotive glazing.

- Market Segmentation: Interior panels and sunroofs are identified as potential initial entry points for substitute materials.

- Performance Thresholds: Safety and visibility requirements for windshields currently maintain glass's dominance in those areas.

Automotive Glass: Unyielding Dominance in a Changing Landscape

While advanced polymers offer lighter weight and enhanced impact resistance, traditional automotive glass, particularly laminated variants, maintains a strong market position due to its superior optical clarity and cost-effectiveness. The automotive industry's continued preference for glass in critical areas like windshields, driven by stringent safety regulations and consumer expectations for durability, limits the immediate threat from substitutes. In 2024, the automotive glass market was valued at roughly $20 billion, underscoring glass's dominance, though innovation in plastics continues for less critical applications.

| Substitute Material | Key Advantages | Current Limitations for Core Glazing | Potential Applications |

|---|---|---|---|

| Polycarbonate/Polymers | Lighter weight, higher impact resistance | Optical clarity, scratch resistance, UV degradation, regulatory approval | Sunroofs, interior panels, potentially side windows |

| Advanced Composites | High strength-to-weight ratio | Cost, manufacturing complexity, long-term durability data | Specialty vehicles, non-critical glazing elements |

Entrants Threaten

High Capital Investment and Economies of Scale

The automotive glass sector demands significant upfront capital. Building state-of-the-art float glass manufacturing plants and sophisticated processing facilities can easily run into hundreds of millions of dollars, presenting a formidable hurdle for newcomers.

To be competitive, any new entrant must rapidly achieve massive economies of scale. Fuyao Glass, for instance, leverages its extensive production capacity to drive down per-unit costs, a feat difficult for smaller, less established operations to replicate.

For example, major automotive glass manufacturers often invest over $300 million in new production lines. This high capital requirement effectively deters many potential competitors from entering the market.

Established Relationships with OEMs

Fuyao Glass Industry Group and its competitors benefit from decades-long, deeply ingrained relationships with major automotive original equipment manufacturers (OEMs). These aren't casual partnerships; they represent intricate supply chain integrations, collaborative product development phases, and rigorous supplier qualification procedures that new entrants find exceedingly difficult to penetrate.

For instance, securing a contract with a major automaker typically involves years of testing, validation, and demonstration of consistent quality and reliability. This established trust and proven track record act as a significant barrier, effectively deterring potential new players from entering the automotive glass market segment served by these incumbents.

Intense R&D and Technological Complexity

The automotive glass sector demands significant upfront investment in research and development, particularly for advanced features like smart glass and Advanced Driver-Assistance Systems (ADAS) compatibility. Newcomers must possess substantial R&D capabilities to compete with established firms like Fuyao Glass, which actively invests in these areas to meet evolving automotive needs.

Regulatory and Safety Standards

The automotive sector operates under stringent global safety and quality regulations for glass. New entrants must navigate and meet these demanding standards, which often involve extensive testing, meticulous certification processes, and specialized manufacturing capabilities. For instance, in 2024, compliance with evolving automotive safety standards like those mandated by UNECE WP.29 continues to be a critical barrier.

These regulatory hurdles significantly increase the initial investment and time-to-market for potential competitors. Fuyao Glass, with its established history of meeting and exceeding these requirements, benefits from this high entry cost. The company’s long-standing relationships with certification bodies and deep understanding of compliance protocols provide a substantial competitive advantage.

- Global Automotive Safety Standards: Compliance with regulations such as FMVSS (USA), ECE (Europe), and CCC (China) is mandatory.

- Testing and Certification Costs: New entrants face millions of dollars in expenses for product testing and obtaining necessary certifications.

- Manufacturing Expertise: Producing automotive glass that meets specific impact, optical, and durability standards requires advanced technology and skilled labor.

- R&D Investment: Continuous investment in research and development is needed to keep pace with evolving safety features like advanced driver-assistance systems (ADAS) integration.

Brand Recognition and Customer Loyalty

Established players like Fuyao Glass Industry Group benefit significantly from strong brand recognition and a well-earned reputation for quality and reliability within the automotive manufacturing sector. This established trust is a formidable barrier; new entrants would face the daunting task of replicating this level of brand loyalty, a process that is both time-consuming and capital-intensive.

Fuyao's long-standing relationships with major automakers, built over years of consistent performance and product delivery, create a significant hurdle. For instance, in 2023, Fuyao Glass reported revenues of approximately $4.05 billion, underscoring its substantial market presence and the scale of investment required to challenge such an entrenched position. Developing comparable brand equity and customer loyalty would likely demand years of sustained effort and substantial marketing expenditure, making the threat of new entrants comparatively low in this regard.

- Brand Trust: Fuyao's established reputation for quality makes it difficult for new companies to gain the confidence of automotive OEMs.

- Customer Loyalty: Long-term relationships with key automotive manufacturers create switching costs and reduce the appeal of new suppliers.

- Investment Requirement: Building comparable brand recognition and loyalty requires significant and sustained financial investment.

- Market Penetration: Fuyao's market share, which stood at approximately 27% of the global automotive glass market in recent years, highlights the difficulty new players face in gaining traction.

Automotive Glass: A Fortress of Entry Barriers

The automotive glass sector presents substantial barriers to entry, primarily due to the immense capital required for manufacturing facilities and advanced research. Fuyao Glass, like its competitors, benefits from established, deep-rooted relationships with original equipment manufacturers (OEMs), which involve years of rigorous testing and validation. Furthermore, navigating stringent global safety and quality regulations, such as those mandated by UNECE WP.29 in 2024, demands significant investment and expertise, making it difficult for new players to gain a foothold.

| Barrier | Description | Impact on New Entrants |

|---|---|---|

| Capital Requirements | Building state-of-the-art float glass plants costs hundreds of millions of dollars. | High upfront investment deters many potential competitors. |

| Economies of Scale | Reaching massive production volumes is crucial for cost competitiveness. | New entrants struggle to match incumbent cost structures. |

| OEM Relationships | Years of trust and integration are needed to secure supply contracts. | Penetrating established supply chains is extremely challenging. |

| R&D and Technology | Investment in advanced features like ADAS integration is essential. | Newcomers need substantial R&D capabilities to compete. |

| Regulatory Compliance | Meeting global safety and quality standards involves extensive testing and certification. | Navigating complex regulations increases time-to-market and costs. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Fuyao Glass Industry Group leverages data from their official annual reports, investor relations disclosures, and industry-specific market research reports. We also consult macroeconomic indicators and global trade association publications to understand the broader competitive landscape.