Fedbank Financial Services Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Fedbank Financial Services

A Must-Have Tool for Decision-Makers

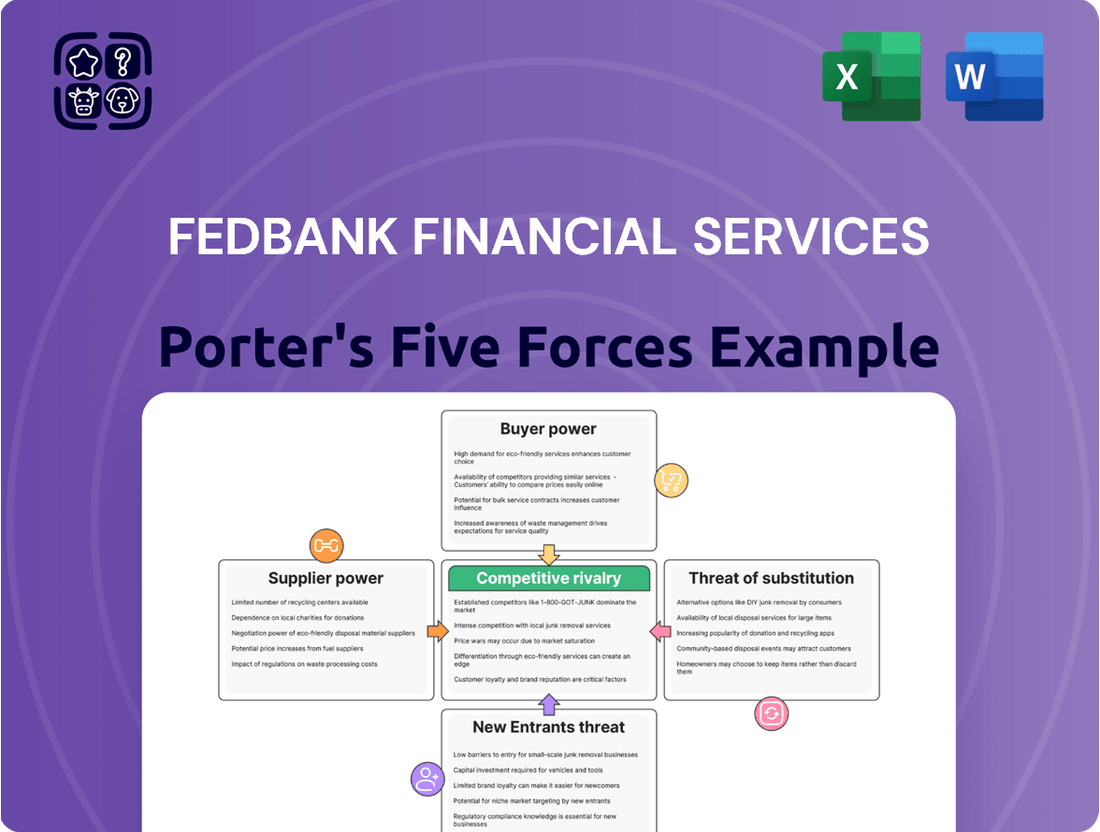

Fedbank Financial Services operates within a dynamic financial services landscape, where understanding the five key competitive forces is crucial for strategic success. Our analysis delves into the intense rivalry among existing players, the significant bargaining power of customers, and the ever-present threat of new entrants disrupting the market.

The full Porter's Five Forces Analysis reveals the strength and intensity of each market force affecting Fedbank Financial Services, complete with visuals and summaries for fast, clear interpretation. Unlock key insights into Fedbank Financial Services’s industry forces—from buyer power to substitute threats—and use this knowledge to inform strategy or investment decisions.

Suppliers Bargaining Power

Funding Sources

Fedbank Financial Services, operating as a Non-Banking Financial Company (NBFC), sources its capital primarily from external avenues. These include commercial banks, other financial institutions, and the broader debt markets.

The leverage Fedbank holds over these funding sources is directly tied to the prevailing liquidity conditions within the financial ecosystem and its own creditworthiness. For instance, a higher credit rating typically translates to lower borrowing costs, diminishing the suppliers' bargaining power.

In 2024, the Reserve Bank of India's monetary policy stance, including repo rate adjustments, significantly impacted the cost of funds for NBFCs. For example, if the repo rate increased, the cost of borrowing for Fedbank would likely rise, potentially increasing the bargaining power of its bank lenders.

Technology Providers

Technology providers, particularly those offering specialized core banking software, loan origination systems, and advanced data analytics platforms, can exert significant bargaining power over financial institutions like Fedbank Financial Services. This power stems from the complexity and criticality of their offerings, often requiring deep integration and specialized expertise. For instance, a vendor with a proprietary, highly efficient loan origination system that significantly reduces processing time might command higher prices due to its unique value proposition. The difficulty in switching providers, due to data migration challenges and retraining costs, further solidifies their position.

However, this supplier power is not absolute. The financial services sector benefits from a growing ecosystem of technology vendors, including those offering open-source solutions and more standardized platforms. This increased competition and the availability of alternatives can serve to temper the bargaining leverage of individual technology suppliers. For example, the rise of cloud-based, modular banking solutions allows Fedbank Financial Services to potentially mix and match components from different providers, reducing reliance on any single vendor. In 2024, the global FinTech market was valued at approximately $1.2 trillion, indicating a broad and competitive landscape for technology providers.

Human Capital

Skilled employees, especially those with expertise in financial services, risk management, and emerging digital technologies, represent a critical component of human capital for companies like Fedbank Financial Services. The intense competition for this talent within India's rapidly growing financial sector significantly amplifies the bargaining power of these skilled individuals, as their specialized knowledge is in high demand.

Rating Agencies

Credit rating agencies hold significant sway over Fedbank Financial Services by influencing its cost of capital. A strong rating from agencies like Moody's, S&P, or Fitch can drastically lower borrowing expenses, effectively giving these agencies indirect bargaining power over Fedbank's funding strategies.

For instance, in the first half of 2024, Fedbank maintained a BBB+ rating from one major agency, which typically translates to lower interest rates compared to companies with lower credit profiles. This favorable rating is crucial for Fedbank's ability to access debt markets efficiently.

- Influence on Funding Costs: A higher credit rating directly reduces the interest Fedbank pays on its debt, impacting overall profitability.

- Market Perception: Ratings shape investor confidence, affecting the ease with which Fedbank can raise capital.

- Cost of Capital Advantage: In 2024, companies with investment-grade ratings often saw borrowing costs several percentage points lower than their sub-investment-grade counterparts.

Regulatory and Compliance Services

Fedbank Financial Services relies on legal firms, auditors, and compliance consultants to navigate India's intricate regulatory landscape. These professionals offer specialized knowledge critical for adherence to laws and financial reporting standards.

The non-negotiable nature of compliance requirements, coupled with the need for expert guidance, grants these service providers a moderate level of bargaining power. For instance, in 2023, the cost of statutory audit fees for financial institutions in India saw an average increase of 8-10% due to evolving auditing standards and increased compliance demands.

The bargaining power of these suppliers is influenced by several factors:

- Expertise and Specialization: The deep understanding of complex financial regulations and legal frameworks possessed by these firms is a key driver of their power.

- Switching Costs: The effort and time involved in onboarding new legal or audit firms, including knowledge transfer and due diligence, can make switching costly for Fedbank.

- Availability of Alternatives: While there are multiple firms, the availability of those with proven track records and specific expertise in financial services might be limited, concentrating power.

Navigating Supplier Power in Financial Services

Fedbank Financial Services faces moderate bargaining power from its capital suppliers, primarily banks and debt markets. This power is influenced by liquidity conditions and Fedbank's creditworthiness. In 2024, the Reserve Bank of India's monetary policy, such as repo rate changes, directly affected borrowing costs and thus supplier leverage.

Technology providers, particularly for core banking and loan origination, hold significant power due to the critical and complex nature of their solutions. Switching costs and the specialized expertise required further solidify their position. However, a growing FinTech market, valued at approximately $1.2 trillion globally in 2024, offers increasing alternatives and can mitigate this power.

Skilled employees, especially in digital finance and risk management, command strong bargaining power due to high demand and intense competition for talent in India's financial sector.

Credit rating agencies wield indirect power by influencing Fedbank's cost of capital. A strong rating, like Fedbank's BBB+ in early 2024, lowers borrowing expenses and enhances market perception.

Legal, audit, and compliance firms possess moderate power due to the non-negotiable nature of regulatory adherence and the specialized expertise required. The increasing complexity of auditing standards led to an average 8-10% rise in statutory audit fees for financial institutions in India during 2023.

| Supplier Type | Bargaining Power Level | Key Factors Influencing Power | 2024 Impact/Data Point |

|---|---|---|---|

| Capital Suppliers (Banks, Debt Markets) | Moderate | Liquidity, Creditworthiness, Monetary Policy | RBI's repo rate adjustments influenced borrowing costs. |

| Technology Providers | High | Specialized Solutions, Integration Complexity, Switching Costs | Global FinTech market valued at ~$1.2 trillion. |

| Skilled Employees | High | Talent Scarcity, Demand for Expertise | Intense competition for financial and digital skills. |

| Credit Rating Agencies | Indirectly High | Influence on Cost of Capital, Market Perception | BBB+ rating in early 2024 facilitated access to debt markets. |

| Legal, Audit, Compliance Firms | Moderate | Regulatory Complexity, Specialized Knowledge, Switching Costs | Audit fees rose 8-10% in 2023 due to compliance demands. |

What is included in the product

This analysis dissects the competitive forces impacting Fedbank Financial Services, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Fedbank Financial Services' Porter's Five Forces analysis provides a clear, one-sheet summary of all competitive forces, perfect for quick strategic decision-making and identifying key pain points.

Easily visualize and customize pressure levels for each force based on new data or evolving market trends, offering a dynamic and responsive approach to competitive analysis.

Customers Bargaining Power

Customer Segment Characteristics

Fedbank Financial Services largely caters to emerging middle and lower-middle-income families and businesses. This customer base is typically quite sensitive to pricing and has a significant need for readily available credit, which can give them a degree of bargaining power.

While individual customers in this segment might have limited collateral, their sheer numbers and collective demand for financial products can translate into a noticeable influence on pricing and service terms. For instance, a significant portion of India's population falls into these income brackets, representing a substantial market share for financial institutions.

Availability of Alternatives

Fedbank Financial Services operates in a market where customers have numerous alternatives. This includes not only public and private sector banks but also a growing number of Non-Banking Financial Companies (NBFCs) and innovative fintech lenders, all vying for the same customer base. For instance, in 2024, the Indian digital lending market was projected to reach over $150 billion, indicating a highly competitive environment with many players offering similar financial products.

The sheer availability of these diverse options significantly enhances the bargaining power of customers. They can readily compare interest rates, processing fees, loan tenures, and customer service quality across various providers. This ease of comparison empowers them to seek out and switch to lenders offering more favorable terms, putting pressure on Fedbank Financial Services to remain competitive.

Switching Costs

Switching costs play a significant role in the bargaining power of customers for Fedbank Financial Services. For larger financial products like home loans or loans against property, customers often face substantial switching costs. These can include the need to re-submit extensive documentation, pay new processing fees, and incur valuation charges, making it less attractive to move to a competitor.

However, for smaller or more transactional loan products, such as gold loans or short-term business loans, the barriers to switching are considerably lower. In these segments, customers can often move between lenders with minimal hassle and expense, thereby increasing their bargaining power and ability to seek out better terms or rates.

Information Access

Customers today have unprecedented access to information, significantly boosting their bargaining power. Digital literacy is on the rise globally, with an estimated 5.3 billion internet users in 2023, many of whom utilize online comparison tools. This means individuals and businesses can easily research and compare interest rates, fees, and product features from various financial institutions like Fedbank Financial Services. This transparency directly challenges information asymmetry, a traditional advantage for lenders.

The ease with which customers can now gather data means they are far more aware of market alternatives. For instance, a significant portion of consumers, estimated to be over 70% in developed markets, actively research financial products online before making a decision. This informed stance empowers them to negotiate better terms or switch to competitors offering more favorable conditions, thereby increasing their leverage over financial service providers.

- Increased Online Comparison: Platforms allow for side-by-side analysis of loan products, deposit rates, and investment options.

- Reduced Information Asymmetry: Customers are no longer reliant solely on the information provided by a single financial institution.

- Price Sensitivity: Greater awareness of pricing structures makes customers more sensitive to higher fees or less competitive interest rates.

- Demand for Transparency: Customers expect clear and easily accessible information regarding all aspects of financial products.

Product Homogeneity

Fedbank Financial Services operates in a market where several of its products, particularly gold loans, exhibit a high degree of homogeneity. This means that for many customers, the core offering is similar across different providers. Differentiation in this segment often boils down to competitive interest rates, the speed of loan processing, and the quality of customer service experienced during the transaction.

This product similarity directly impacts the bargaining power of customers. When financial products are largely interchangeable, customers become more price-sensitive. They can readily compare offerings from various institutions, putting pressure on Fedbank to maintain competitive pricing to attract and retain business. For instance, in the unsecured lending space, where Fedbank also operates, the average interest rate for personal loans in India hovered around 10-15% in early 2024, highlighting the competitive landscape driven by product similarity.

- Product Homogeneity: Many Fedbank products, especially gold loans, are similar across competitors.

- Price Sensitivity: High homogeneity makes customers more focused on interest rates and fees.

- Competitive Landscape: Differentiation relies heavily on service speed and customer experience.

- Market Pressure: Customers can easily switch providers, increasing price competition.

Customer Bargaining Power: A Force in Lending

Fedbank Financial Services faces considerable bargaining power from its customer base, largely due to the price sensitivity of its target market and the increasing availability of alternatives. The sheer volume of customers in the emerging middle and lower-middle-income segments, coupled with a high demand for credit, gives them collective leverage. This is amplified by the growing digital lending market in India, which in 2024 was projected to exceed $150 billion, indicating a highly competitive environment where customers can easily compare and switch providers based on favorable terms.

Switching costs are a key factor; while higher for products like home loans, they are minimal for transactional services such as gold loans. This ease of switching, combined with enhanced customer access to information through online comparison tools—with over 5.3 billion internet users globally in 2023—empowers customers to seek better rates and terms. The homogeneity of certain products, like gold loans, further intensifies this pressure, making price and service speed crucial differentiators for Fedbank.

| Factor | Impact on Fedbank | Customer Leverage |

|---|---|---|

| Customer Price Sensitivity | Requires competitive pricing strategies. | High, due to sensitivity of target income groups. |

| Availability of Alternatives | Increases competition and customer retention challenges. | High, due to numerous banks and NBFCs. |

| Switching Costs (Low for some products) | Reduces customer loyalty for transactional loans. | High for products with low switching barriers. |

| Information Accessibility | Demands greater transparency and competitive offers. | High, via online comparison tools and digital literacy. |

| Product Homogeneity (e.g., Gold Loans) | Drives competition based on price and service speed. | High, as products are easily substitutable. |

Same Document Delivered

Fedbank Financial Services Porter's Five Forces Analysis

The document you see is your deliverable. It’s ready for immediate use—no customization or setup required. This comprehensive Porter's Five Forces analysis for Fedbank Financial Services meticulously details the competitive landscape, evaluating the threat of new entrants, the bargaining power of buyers, the bargaining power of suppliers, the threat of substitute products or services, and the intensity of rivalry among existing competitors.

Rivalry Among Competitors

Number and Diversity of Competitors

The Indian financial services landscape, especially in non-banking financial companies (NBFCs) and lending, is incredibly crowded. Think of it as a bustling marketplace with public and private banks, a vast array of NBFCs both big and small, and a growing number of innovative fintech companies all vying for customers.

This sheer volume and variety of players create a fiercely competitive environment. For instance, as of March 2024, India had over 1,600 Non-Banking Financial Companies registered with the Reserve Bank of India, alongside hundreds of scheduled commercial banks, all actively competing for market share.

Market Growth Rate

The Indian credit market, particularly for segments like MSMEs and individuals seeking affordable financing, is experiencing strong demand. However, this growth environment is intensely competitive, with numerous financial institutions vying for customers. This high saturation means that expansion for one player often directly impacts another, fostering an aggressive landscape where market share gains are hard-won.

This dynamic fuels strategies focused on aggressive pricing and product innovation to attract and retain customers. For instance, in 2024, the Non-Banking Financial Company (NBFC) sector in India saw a significant increase in loan disbursals, reflecting this robust demand but also the intense competition to secure that business.

Product Differentiation

Product differentiation in secured lending, such as gold and home loans, is a tough battleground for Fedbank Financial Services. Competitors frequently go head-to-head on pricing, speed of processing, customer experience, and the sheer number of branches they operate. This intense rivalry means many players are chasing the same customer base with very similar offerings.

Exit Barriers

Fedbank Financial Services, like many Non-Banking Financial Companies (NBFCs), faces substantial exit barriers that can keep it competing even when profitability is low. The significant capital already sunk into establishing and maintaining extensive branch networks and sophisticated technology infrastructure represents a major commitment. These are not easily recouped, making a swift exit financially unviable.

Furthermore, the intricate web of financial regulations in India adds another layer of complexity. Navigating these rules for winding down operations or divesting assets can be a lengthy and costly process, further discouraging premature exits. This regulatory environment essentially locks in players, ensuring continued competition.

- High Capital Investments: NBFCs like Fedbank Financial Services invest heavily in physical branches and IT systems, creating sunk costs that are difficult to recover.

- Regulatory Hurdles: The complex and evolving regulatory landscape for financial services in India can make exiting the market a slow and expensive undertaking.

- Compelled Competition: These barriers often force companies to remain active and compete, even in less profitable market conditions, to avoid substantial losses on exit.

Strategic Objectives of Competitors

Competitors in the financial services sector often pursue distinct strategic aims. For instance, some might prioritize aggressive market share growth, even at the expense of short-term profitability. Others may focus on maximizing profitability within their existing customer base or specializing in high-margin niche markets.

This divergence in objectives fuels unpredictable competitive dynamics. For example, a competitor aiming for rapid expansion might engage in aggressive pricing strategies, intensifying rivalry in specific product segments like personal loans or wealth management services.

In 2024, the Indian financial services landscape saw varied approaches. Several fintech players, for example, focused on user acquisition and market penetration, often offering competitive rates. Meanwhile, established banks and non-banking financial companies (NBFCs) like Fedbank Financial Services often balanced growth with a strong emphasis on asset quality and profitability.

- Market Share Expansion: Competitors may invest heavily in marketing and product development to gain a larger slice of the market.

- Profitability Focus: Some players prioritize improving net interest margins and operational efficiency to boost profits.

- Niche Specialization: Certain firms concentrate on specific customer segments or financial products, aiming for deep expertise and customer loyalty.

- Geographic Penetration: Expansion into underserved regions or specific urban centers can be a key strategic objective.

India's Financial Battleground: Navigating Intense Market Rivalry

The competitive rivalry for Fedbank Financial Services is intense due to the sheer number of players in India's financial services sector, including banks, numerous NBFCs, and fintech firms. This crowded market means many institutions are actively pursuing the same customer base with similar products, driving competition on factors like pricing and service speed.

The Indian financial services market, particularly for lending, is characterized by high saturation, with over 1,600 NBFCs and hundreds of banks operating as of March 2024. This environment fosters aggressive strategies as firms battle for market share, making customer acquisition and retention a constant challenge.

Fedbank Financial Services faces significant exit barriers, such as substantial investments in branch networks and technology, alongside regulatory complexities, which compel continued competition. This means firms often remain active even when profitability is challenged, contributing to sustained rivalry.

Competitors exhibit diverse strategic aims, from aggressive market share expansion to niche specialization and profitability focus. For example, in 2024, fintechs prioritized user acquisition with competitive rates, while established players like Fedbank balanced growth with asset quality, creating varied competitive pressures.

| Competitor Type | Key Strategies Observed (2024) | Impact on Rivalry |

|---|---|---|

| Public Sector Banks | Aggressive deposit rates, expanding digital services | Intensified competition on pricing and convenience |

| Private Sector Banks | Product innovation, customer experience focus | Drives differentiation and customer acquisition efforts |

| Large NBFCs | Market share growth, leveraging digital channels | Direct competition for lending segments |

| Fintech Companies | Rapid user acquisition, competitive loan pricing | Disruptive force, particularly in unsecured lending |

SSubstitutes Threaten

Informal Lending Channels

For Fedbank Financial Services' target customers, informal lending channels, such as friends, family, or local moneylenders, represent a significant threat of substitutes. These informal options can be particularly attractive for smaller, immediate credit needs where the borrower might find the application process for formal institutions cumbersome. For instance, in many emerging markets, a substantial portion of credit is still extended through informal networks, highlighting their prevalence.

The primary appeal of these substitutes lies in their speed and accessibility. Unlike traditional financial institutions that require extensive documentation and credit checks, informal lenders often operate with minimal paperwork and faster disbursement times. This ease of access can be a compelling factor, even if the interest rates charged by informal lenders are typically much higher than those offered by Fedbank.

Personal Savings and Self-Funding

Customers often opt to tap into their personal savings or sell off other assets rather than seeking a loan, especially for modest financial needs. This self-funding approach acts as a direct alternative to borrowing from institutions like Fedbank Financial Services.

For instance, in 2023, a significant portion of consumer spending on durable goods was financed through savings, with reports indicating that over 40% of major purchases were made without taking on new debt, highlighting the strength of this substitute.

Government Welfare Schemes and Subsidies

Government welfare schemes and subsidies present a significant threat of substitutes for Fedbank Financial Services. These initiatives, often focused on financial inclusion or supporting small enterprises, can offer alternative funding avenues. For instance, the Pradhan Mantri Mudra Yojana (PMMY) disbursed over ₹4.05 lakh crore to 12.5 crore beneficiaries by March 2024, directly competing with traditional lending by institutions like Fedbank for micro and small businesses.

Peer-to-Peer (P2P) Lending Platforms

Peer-to-peer (P2P) lending platforms present a growing threat of substitutes for Fedbank Financial Services, particularly for unsecured personal loans and small business financing. These digital platforms connect borrowers directly with individual investors, often offering faster approval times and potentially lower interest rates than traditional banks.

While P2P lending for secured loans is still developing, its appeal to a tech-savvy demographic seeking convenient credit solutions is undeniable. For instance, by the end of 2023, the global P2P lending market was estimated to be valued at over $100 billion, with projections indicating continued expansion. This digital alternative can siphon off customers who might otherwise seek financing from established institutions like Fedbank.

- Digital Convenience: P2P platforms offer a streamlined, online application process, appealing to borrowers who prioritize speed and ease of use.

- Niche Market Appeal: They cater to individuals and small businesses often underserved by traditional banks, providing a viable alternative for credit.

- Market Growth: The P2P lending sector is experiencing significant growth, indicating a rising acceptance and utilization of these substitute services.

Microfinance Institutions (MFIs)

Microfinance Institutions (MFIs) pose a significant threat of substitution, particularly for the lower middle-income segment. They offer small loans, often utilizing group lending and streamlined application processes, which can directly compete with the small business and personal loan offerings from Non-Banking Financial Companies (NBFCs) like Fedbank Financial Services. In 2023, the Indian microfinance sector disbursed over INR 1.5 lakh crore, highlighting its substantial market presence and reach.

The accessibility and tailored nature of MFI products, even if typically unsecured, make them an attractive alternative for individuals and small businesses seeking capital that might be unavailable or too complex to obtain from traditional lenders. This competitive pressure means NBFCs must continually refine their product offerings and customer service to retain market share.

- MFI loan disbursement in India reached approximately INR 1.55 lakh crore in FY 2023-24.

- Group lending models common in MFIs reduce perceived risk and operational costs.

- MFIs often cater to unbanked or underbanked populations, expanding the overall credit market.

Exploring Lending Alternatives: Savings, Schemes, P2P, MFIs

Informal lending, personal savings, and government schemes represent significant substitutes for Fedbank Financial Services, particularly for smaller credit needs and specific demographic segments. These alternatives often offer greater speed and accessibility, even if at a higher cost or with different eligibility criteria. For example, the Pradhan Mantri Mudra Yojana (PMMY) disbursed over ₹4.05 lakh crore by March 2024, directly impacting the micro-enterprise lending space.

Peer-to-peer (P2P) lending platforms and microfinance institutions (MFIs) are also emerging as strong substitutes, especially for unsecured personal and small business loans. P2P lending, valued globally at over $100 billion by the end of 2023, provides a digital-first alternative, while MFIs, which disbursed over INR 1.5 lakh crore in India in 2023, cater to the unbanked and underbanked with tailored products.

| Substitute Type | Key Characteristics | Impact on Fedbank | Relevant Data (Approximate) |

| Informal Lending | Speed, Accessibility, High Cost | Siphons off immediate, small credit needs | Prevalent in emerging markets for a significant portion of credit |

| Personal Savings | Self-funding, No Debt | Reduces demand for loans for purchases | Over 40% of major purchases financed by savings in 2023 |

| Govt. Schemes (e.g., PMMY) | Subsidized/Targeted Funding | Direct competition for specific segments | ₹4.05 lakh crore disbursed by PMMY by March 2024 |

| P2P Lending | Digital, Faster Approval, Niche Appeal | Attracts tech-savvy borrowers | Global market over $100 billion by end of 2023 |

| Microfinance Institutions (MFIs) | Small Loans, Tailored Products, Group Lending | Competes for lower-middle income segment | INR 1.55 lakh crore disbursed in India in FY 2023-24 |

Entrants Threaten

Regulatory Hurdles and Licensing

The Reserve Bank of India (RBI) maintains rigorous licensing procedures and capital adequacy standards for new Non-Banking Financial Company (NBFC) entrants, particularly in the secured lending space. These regulatory requirements act as a substantial deterrent, making it challenging for new entities to enter the market easily.

Capital Requirements

Establishing a strong lending business, particularly one with a physical branch network and a focus on secured loans, demands significant capital. Fedbank Financial Services, for instance, would need substantial funds to set up its infrastructure and operational capacity.

This high initial capital requirement acts as a considerable hurdle for any new company looking to enter the financial services sector, making it difficult for them to compete effectively from the outset.

Brand Recognition and Trust

In the financial services sector, brand recognition and trust are incredibly important. For new companies trying to enter the market, establishing this credibility against established players like Fedbank, which has a long history and a strong reputation, is a major hurdle. It takes significant time and resources to build that same level of customer confidence.

Distribution Network and Reach

Fedbank Financial Services leverages a robust branch-led distribution network, a significant barrier for potential new entrants. Establishing a comparable physical presence across diverse geographies requires substantial capital investment and time, making it difficult for newcomers to compete effectively on reach.

The sheer scale of Fedbank's established network, which includes numerous branches, presents a formidable challenge. For instance, as of December 31, 2023, Fedbank operated 580 branches. Replicating this extensive footprint would necessitate a massive outlay in real estate, staffing, and operational setup, a hurdle that many aspiring financial service providers may find insurmountable.

- Significant Capital Outlay: New entrants face the challenge of investing heavily in physical infrastructure to match Fedbank's reach.

- Time-Intensive Network Building: Developing a widespread distribution network akin to Fedbank's takes years, creating a time lag advantage for the incumbent.

- Geographic Diversification Costs: Expanding into multiple regions amplifies the cost and complexity for new players aiming for broad market penetration.

Access to Funding and Cost of Funds

New entrants into the non-banking financial company (NBFC) sector, like Fedbank Financial Services, often face significant hurdles in securing capital. Established players typically benefit from lower borrowing costs due to their long-standing relationships with banks and a proven history of financial stability. For instance, in early 2024, major banks were offering wholesale funding to well-established NBFCs at rates that were noticeably lower than what newer entities could access, reflecting the perceived risk differential.

This disparity in funding costs directly impacts a new entrant's ability to compete. If a new NBFC must pay a higher interest rate on its borrowings, its operational expenses increase, potentially making its loan products less attractive or its profit margins thinner. This can be a substantial barrier, as seen when comparing the average cost of funds for a startup NBFC versus a seasoned one, where the difference can be several percentage points, significantly affecting their pricing power and market penetration capabilities.

The threat of new entrants is thus mitigated by the difficulty in achieving cost parity for funding. Established NBFCs have built robust treasury functions and diversified funding sources, giving them an advantage. For example, by mid-2024, the Reserve Bank of India's regulatory framework continued to emphasize capital adequacy and liquidity, further reinforcing the importance of a strong financial foundation, which new entrants may take time to build, thereby increasing their initial funding costs.

- Funding Access Disparity: New NBFCs often find it harder to secure loans at favorable rates compared to established firms with strong banking ties and a track record.

- Cost of Funds Impact: Higher borrowing costs for new entrants can lead to less competitive product pricing and reduced profitability, hindering market entry.

- Competitive Disadvantage: In early 2024, wholesale funding rates for established NBFCs were notably lower than those available to new entities, creating an immediate competitive gap.

- Regulatory Reinforcement: RBI regulations in 2024 on capital and liquidity requirements favor entities with established financial strength, indirectly increasing the funding cost barrier for newcomers.

Financial Services: Entry Barriers Keep New Competitors Out

The threat of new entrants for Fedbank Financial Services is considerably low due to substantial barriers to entry. High capital requirements for licensing and operations, coupled with the need for extensive branch networks and established brand trust, make it difficult for newcomers to compete. Furthermore, access to favorable funding rates, a key competitive advantage for established players like Fedbank, remains a significant hurdle for new entities.

| Barrier | Description | Impact on New Entrants |

| Regulatory Hurdles | Rigorous licensing and capital adequacy standards by RBI. | Increases initial investment and time to market. |

| Capital Intensity | Significant funds needed for infrastructure, branches, and operations. | High upfront investment required, limiting the pool of potential entrants. |

| Brand & Trust | Established reputation and customer confidence built over time. | New entrants struggle to gain credibility against incumbents. |

| Distribution Network | Extensive branch presence (e.g., Fedbank's 580 branches as of Dec 2023). | Replicating this reach requires massive investment and time. |

| Funding Costs | Established players access lower wholesale funding rates. | New entrants face higher borrowing costs, impacting pricing and profitability. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Fedbank Financial Services is built upon a foundation of diverse and credible data. We leverage information from Fedbank's official annual reports and investor relations materials, alongside industry-specific publications and reports from reputable financial data providers.