Fedbank Financial Services Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Fedbank Financial Services

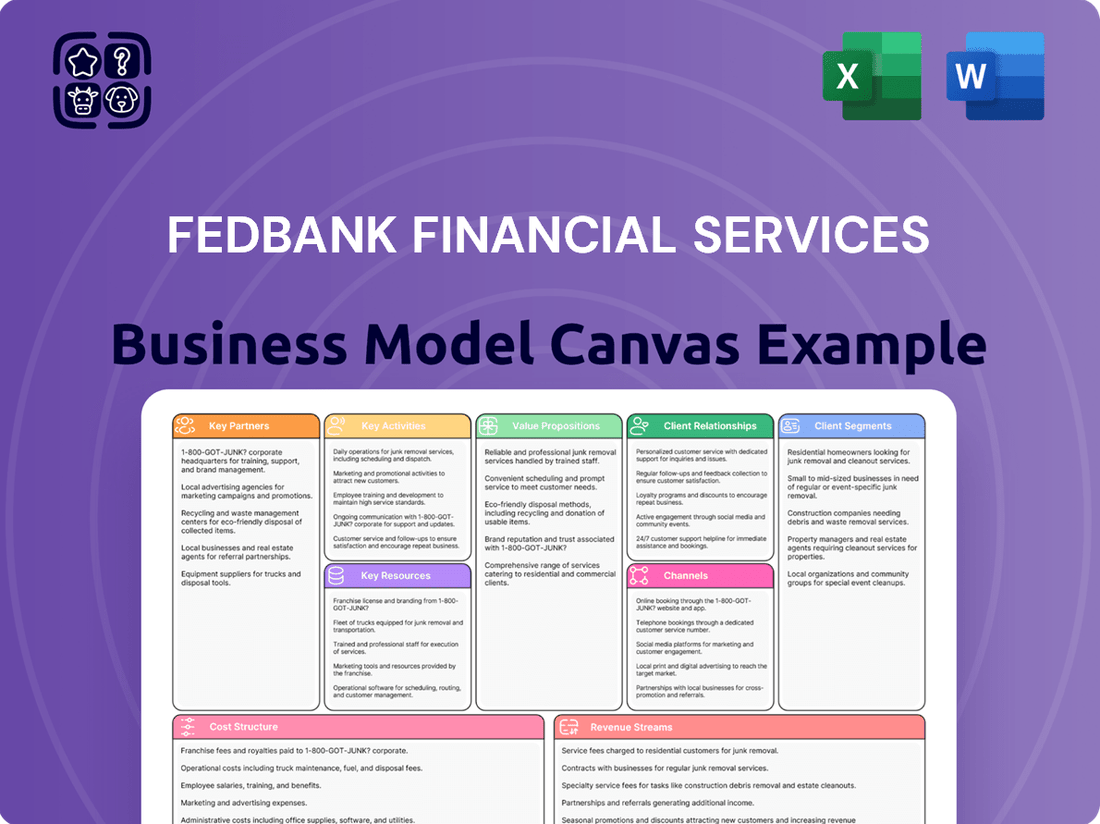

Fedbank Financial Services: Business Model Unveiled!

Explore the core components of Fedbank Financial Services's success with our comprehensive Business Model Canvas. Understand their customer segments, value propositions, and revenue streams to gain a strategic advantage. Download the full canvas to unlock actionable insights for your own business.

Partnerships

Parent Company Collaboration

Fedbank Financial Services benefits immensely from its status as a subsidiary of Federal Bank, a relationship that provides robust financial backing and a significant competitive advantage. This parentage ensures stability and allows Fedbank to tap into Federal Bank's extensive network and established reputation in the financial sector.

The strong financial health of Federal Bank, which reported a net profit of ₹1,007 crore for the fiscal year ended March 31, 2024, directly bolsters Fedbank's market standing and credibility. This symbiotic relationship enables Fedbank to offer a wider array of services and maintain a strong capital base, crucial for growth and client confidence.

Financial Institutions and Lenders

Fedbank Financial Services cultivates vital partnerships with a network of banks and financial institutions. These alliances are crucial for securing diverse funding sources and maintaining a competitive cost of borrowing. This strategic approach has been instrumental in Fedbank achieving the second lowest cost of borrowing among its industry peers, a testament to its robust lender relationships.

The advantage of a low cost of borrowing directly translates into Fedbank's ability to offer more attractive and competitive financial products to its customers. This financial efficiency also underpins the company's capacity to maintain healthy profit margins, enabling sustainable growth and reinvestment in its services.

Technology and Digital Solution Providers

Fedbank Financial Services actively collaborates with technology and digital solution providers to build and sustain a robust, tech-driven loan processing and disbursal system. These partnerships are crucial for integrating Application Programming Interfaces (APIs) that streamline workflows and enhance operational efficiency.

A key aspect of these collaborations involves leveraging APIs to integrate advanced credit scoring models, thereby improving the accuracy and speed of credit assessments. For instance, in 2023, the Indian fintech sector saw a significant surge in API integrations, with companies reporting an average of 30-40% improvement in loan processing times through such partnerships.

These strategic alliances not only bolster operational efficiency but are also instrumental in delivering a superior customer experience. By enabling seamless data exchange and automating key stages of the loan lifecycle, Fedbank Financial Services can offer faster approvals and a more convenient borrowing process for its clients.

Asset Reconstruction Companies (ARCs)

Partnerships with Asset Reconstruction Companies (ARCs) are a cornerstone for Fedbank Financial Services in effectively managing its non-performing assets (NPAs) and upholding overall asset quality. By strategically transferring NPAs to ARCs, Fedbank Financial Services demonstrates a proactive approach to resolving bad loans.

This strategy is crucial for freeing up capital, allowing for its redeployment into more secure and profitable business ventures. For instance, in the fiscal year ending March 2024, the Indian banking sector saw a significant reduction in NPAs, with gross NPAs falling to a multi-year low of 3.2% as of September 2023, according to the Reserve Bank of India. This trend highlights the effectiveness of such asset management strategies.

- NPA Resolution: ARCs specialize in acquiring and resolving NPAs, providing Fedbank Financial Services with a dedicated channel for bad loan management.

- Capital Optimization: Transferring NPAs to ARCs unlocks capital that can be reinvested in growth areas, improving the company's financial flexibility.

- Asset Quality Improvement: This partnership directly contributes to a healthier balance sheet by reducing the burden of non-performing loans.

- Market Trends: The broader Indian financial market has shown a consistent decline in NPAs, underscoring the strategic importance of efficient NPA management mechanisms like those offered by ARCs.

Sourcing and Servicing Agents

Fedbank Financial Services leverages a network of sourcing and servicing agents to extend its micro-loan offerings and broaden its market reach. These partnerships are crucial for tapping into underserved populations and ensuring financial products are effectively delivered to the last mile.

This strategy directly supports Fedbank's commitment to serving emerging middle-income and lower-middle-income families and businesses. By working with local agents, the company can better understand and cater to the specific needs of these demographic segments.

- Agent Network Expansion: Fedbank actively recruits and trains a diverse range of agents, from local entrepreneurs to community organizations, to act as conduits for its financial services.

- Last-Mile Delivery: These agents are instrumental in the origination and ongoing servicing of micro-loans, facilitating easier access for clients in remote or less-developed areas.

- Market Penetration: The partnerships enable Fedbank to penetrate markets that might otherwise be economically unviable through traditional branch networks, thus increasing financial inclusion.

Key Partnerships: Boosting Efficiency and Financial Health

Fedbank Financial Services’ key partnerships are structured to enhance its operational efficiency and market reach. Collaborations with technology providers are vital for streamlining loan processing through API integrations, mirroring a trend where Indian fintechs saw 30-40% faster loan processing in 2023 due to such integrations. Furthermore, partnerships with Asset Reconstruction Companies (ARCs) are crucial for managing non-performing assets, contributing to a healthier balance sheet in a market where gross NPAs in the Indian banking sector fell to a multi-year low of 3.2% by September 2023.

| Partnership Type | Key Benefit | Impact/Example |

|---|---|---|

| Federal Bank (Parent) | Financial backing, network access, reputation | Net profit of ₹1,007 crore for FY24 |

| Banks & Financial Institutions | Diverse funding, lower borrowing costs | Second lowest cost of borrowing among peers |

| Technology & Digital Solution Providers | Streamlined loan processing, API integration | Improved credit scoring accuracy and speed |

| Asset Reconstruction Companies (ARCs) | NPA resolution, capital optimization | Reduced NPAs, improved asset quality |

| Sourcing & Servicing Agents | Market reach, last-mile delivery | Access to underserved populations |

What is included in the product

A detailed Fedbank Financial Services Business Model Canvas outlining their strategy, customer segments, channels, and value propositions for financial services.

This model, structured across 9 classic BMC blocks, provides a clear view of Fedbank's operations and competitive advantages, suitable for investor discussions.

Fedbank Financial Services' Business Model Canvas offers a clear, one-page snapshot, simplifying complex financial strategies and making them easily digestible for all stakeholders.

This structured approach acts as a pain point reliever by providing a visual framework that facilitates rapid understanding and alignment across teams, reducing confusion and accelerating strategic decision-making.

Activities

Loan Origination and Disbursal

Fedbank Financial Services' core operations revolve around the origination and disbursement of a diverse range of loan products. This includes crucial financial solutions like gold loans, home loans, loans against property (LAP), and essential business loans, covering the complete journey from initial application to the final release of funds.

The company's commitment to facilitating access to credit is evident in its robust disbursement figures. For instance, in the first quarter of fiscal year 2026 (Q1 FY26), Fedbank Financial Services achieved a significant milestone, disbursing INR 5,933 crores. This represents a substantial year-on-year increase of 18.5%, underscoring the growing demand for their lending services and the company's capacity to meet it.

Credit Assessment and Risk Management

Fedbank Financial Services prioritizes robust credit assessment and meticulous risk management, forming the bedrock of its secured asset-backed lending model. This involves a thorough evaluation of collateral to ensure its value adequately covers potential loan exposure.

Assessing borrower creditworthiness is paramount, utilizing comprehensive data to gauge repayment capacity and historical financial behavior. The company’s focus on collateral-backed products significantly contributes to maintaining low Non-Performing Asset (NPA) levels, a testament to its effective risk mitigation strategies.

As of March 2024, Fedbank Financial Services reported a commendable gross NPA ratio of just 1.7%, underscoring the success of its disciplined approach to credit underwriting and ongoing portfolio management.

Branch Network Management and Expansion

Operating and expanding a branch-led distribution model is a fundamental activity for Fedbank Financial Services. This involves both the strategic establishment of new branches and the continuous optimization of their existing network to ensure efficient service delivery.

With a significant presence already established, Fedbank Financial Services boasts over 500 branches, with a particular focus on serving Tier II and Tier III cities. This extensive network allows them to reach a broad customer base in underserved markets.

Looking ahead, the company has ambitious growth plans. For fiscal year 2026, Fedbank Financial Services intends to open gold loan branches in over 100 new markets, a move designed to significantly enhance their market coverage and accessibility.

Customer Relationship Management and Servicing

Fedbank Financial Services prioritizes building and maintaining strong customer connections through dedicated support and efficient loan management. This includes proactive assistance, addressing inquiries promptly, and ensuring a smooth experience after loans are disbursed, aiming for secure and hassle-free interactions.

The FedFina Loans app is a key tool in this strategy, offering customers convenient access to manage their accounts. Features like tracking loan progress, reviewing past payments, and finding branch locations are integrated to enhance user experience and provide ongoing support.

- Customer Retention: Focus on nurturing long-term relationships through consistent support and value-added services.

- Digital Servicing: Leverage technology like the FedFina Loans app to provide self-service options for account management and query resolution.

- Loan Lifecycle Management: Ensure efficient handling of all stages of the loan, from disbursement to repayment, with a focus on customer ease.

- Feedback Integration: Actively gather and incorporate customer feedback to continuously improve service offerings and address pain points.

Capital Management and Funding

Fedbank Financial Services actively manages its capital by securing a variety of funding sources. A significant move was the successful completion of its first $100 million External Commercial Borrowing (ECB) in the first quarter of fiscal year 2026. This capital was then strategically deployed into businesses demonstrating strong financial performance.

The company focuses on deploying capital into ventures with high Return on Assets (ROA) and Return on Equity (ROE). This approach ensures that the funds raised are utilized efficiently, aiming to maximize profitability and shareholder value. The deployment of the ECB funds into secured businesses underscores a commitment to prudent capital allocation.

- Capital Sourcing: Active management of capital through diverse funding streams, including commercial borrowings.

- ECB Issuance: Completed a $100 million ECB in Q1 FY26, marking a significant milestone in funding.

- Capital Deployment: Strategically invested released capital into businesses with high ROA and ROE.

- Business Focus: Prioritizes deployment into secured businesses to ensure capital safety and profitability.

Key Activities Fueling Financial Services Growth and Stability

Fedbank Financial Services' key activities revolve around originating and disbursing loans, particularly gold loans, home loans, and business loans. They also focus on robust credit assessment and risk management, primarily through asset-backed lending. A critical operational aspect is managing and expanding their extensive branch network, especially in Tier II and Tier III cities, with plans for further expansion in gold loan branches.

Furthermore, the company excels in customer relationship management, utilizing digital tools like the FedFina Loans app for seamless account servicing. Capital management is another core activity, evidenced by their successful $100 million External Commercial Borrowing (ECB) in Q1 FY26, which is strategically deployed into high-ROA and ROE businesses.

| Key Activity | Description | Recent Data/Focus |

|---|---|---|

| Loan Origination & Disbursement | Providing gold loans, home loans, LAP, and business loans. | Disbursed INR 5,933 crores in Q1 FY26, an 18.5% YoY increase. |

| Risk Management & Credit Assessment | Secured asset-backed lending, collateral valuation, and borrower creditworthiness. | Maintained a gross NPA ratio of 1.7% as of March 2024. |

| Branch Network Management | Operating and expanding a branch-led distribution model. | Over 500 branches, targeting 100 new gold loan markets in FY26. |

| Customer Relationship Management | Dedicated support, efficient loan management, and digital servicing via app. | Focus on retention and digital servicing through FedFina Loans app. |

| Capital Management | Sourcing diverse funding and deploying capital strategically. | Completed $100 million ECB in Q1 FY26, deployed into high-ROA/ROE businesses. |

Preview Before You Purchase

Business Model Canvas

The Fedbank Financial Services Business Model Canvas you are currently previewing is the exact document you will receive upon purchase, offering a comprehensive overview of their operational strategy. This means no surprises; the structure, content, and formatting you see are precisely what will be delivered, ready for your immediate use. You'll gain full access to this detailed canvas, enabling a thorough understanding of Fedbank's approach to financial services.

Resources

Financial Capital

Adequate financial capital is the bedrock of Fedbank Financial Services' operations, empowering it to extend loans and manage its business effectively. This crucial resource is bolstered by equity contributions from its parent company, Federal Bank, and supplemented by funds secured through diverse borrowing instruments.

Fedbank's robust financial health is underscored by its Q1 FY26 performance, which saw net profits reach ₹75.01 crore. This strong profitability directly translates into healthy capital generation, providing the necessary fuel for its lending activities and overall growth initiatives.

Extensive Branch Network

Fedbank Financial Services leverages an extensive physical branch network, boasting over 500 locations primarily in Tier II and Tier III cities. This robust infrastructure is fundamental to its branch-led distribution strategy, facilitating direct customer engagement and efficient loan processing, particularly for gold loans and loan against property (LAP).

These branches act as vital hubs for customer interaction, enabling personalized service and immediate support, which is crucial for building trust and facilitating transactions in its core product offerings. The significant geographical spread ensures reach into markets that may be less served by traditional banking channels.

In 2024, the company's commitment to this physical presence underscores its strategy to tap into the financial needs of a broad customer base, particularly in semi-urban and rural areas. This network is a key differentiator, allowing for deeper market penetration and a more accessible service model.

Skilled Human Capital

Fedbank Financial Services relies heavily on its skilled human capital, encompassing loan officers, credit analysts, and customer service staff, to ensure smooth and effective operations. This well-trained workforce is the backbone of their service delivery.

The company's growth and efficiency are directly linked to the expertise of its teams in secured lending, customer acquisition, and robust risk management practices. These specialized skills are crucial for navigating the financial landscape.

In 2024, Fedbank Financial Services made significant strides in bolstering its leadership and field teams, especially within the burgeoning ST LAP (Short-Term Loan Against Property) business. This strategic reinforcement aims to enhance market penetration and operational excellence in key growth areas.

Proprietary Technology and IT Infrastructure

Fedbank Financial Services leverages its proprietary technology and robust IT infrastructure to streamline operations. This includes advanced loan management systems that automate processing and data handling, ensuring efficiency and accuracy. In 2024, the company continued to invest in these systems to enhance its digital customer experience.

The company's tech-driven approach is evident in its digital customer interfaces and mobile applications, facilitating seamless interactions for loan applications and management. These platforms are designed for user-friendliness and accessibility.

API-driven workflows are integral to Fedbank Financial Services' operations, enabling consistent policy execution across all touchpoints. This integration ensures that policies are applied uniformly, reducing errors and improving turnaround times for loan disbursals.

- Proprietary Loan Management Systems: Core to efficient loan processing and data management.

- Digital Customer Interfaces: Enhancing user experience through mobile apps and online portals.

- API-Driven Workflows: Ensuring consistent policy execution and seamless integration.

- Tech-Driven Disbursal: A key highlight of their operational efficiency in 2024.

Secured Asset Portfolio

Fedbank Financial Services' secured asset portfolio, primarily comprising gold and property, is a foundational element of its business model. This collateral-backed approach significantly reduces credit risk, allowing for more robust and secure lending operations. The company's strategic aim is to transition its entire loan book to be fully secured, a move that directly contributes to its operational stability.

This focus on tangible collateral is a key differentiator, leading to demonstrably lower Non-Performing Asset (NPA) levels compared to unsecured lending models. For instance, in the fiscal year ending March 31, 2024, Fedbank Financial Services reported a Gross NPA ratio of 1.87% and a Net NPA ratio of 0.75%, reflecting the effectiveness of its secured lending strategy.

- Collateralized Assets: The core resource includes a substantial portfolio of gold and property held as security for loans.

- Risk Mitigation: This secured approach directly lowers the company's exposure to credit defaults and associated financial risks.

- NPA Performance: The strategy of prioritizing secured lending has historically resulted in lower NPA ratios, as evidenced by figures like the 1.87% Gross NPA reported for FY24.

- Strategic Direction: Fedbank Financial Services is actively pursuing a business model that aims for a 100% secured lending portfolio.

Capital, Network, Talent, Tech, Secured Assets: Pillars of Financial Strength

Fedbank Financial Services' key resources are its strong financial capital, a wide physical branch network, skilled human capital, and robust proprietary technology. Its financial strength is supported by its parent company and borrowing instruments, with a net profit of ₹75.01 crore in Q1 FY26 demonstrating healthy capital generation. The extensive branch network, exceeding 500 locations, is crucial for its branch-led distribution strategy, especially for gold loans and loan against property (LAP).

The company's skilled workforce, including loan officers and credit analysts, is vital for its operations, particularly with recent reinforcements in the ST LAP business in 2024. Its technology infrastructure, featuring advanced loan management systems and digital customer interfaces, ensures operational efficiency and an enhanced customer experience. API-driven workflows further guarantee consistent policy execution, a key operational highlight in 2024.

The company's secured asset portfolio, primarily gold and property, is a fundamental resource that significantly mitigates credit risk. This strategy has led to low NPA levels, with Gross NPA at 1.87% and Net NPA at 0.75% for FY24, reinforcing its aim for a 100% secured lending book.

Value Propositions

Accessible Secured Lending

Fedbank Financial Services offers accessible secured lending, primarily through gold loans, home loans, and loans against property. This strategy allows emerging middle-income and lower-middle-income families and businesses to leverage their existing assets for financial needs.

By focusing on asset-backed lending, Fedbank effectively mitigates risk, which is reflected in their consistently low Non-Performing Asset (NPA) levels. For instance, as of the third quarter of fiscal year 2024, Fedbank reported a Gross NPA ratio of 1.70%, demonstrating the strength of their secured lending model.

Quick and Efficient Loan Processing

Fedbank Financial Services leverages a tech-driven approach for swift loan processing and disbursal. This streamlined system significantly reduces turnaround times, ensuring customers receive funds quickly. For instance, in FY2024, the company focused on enhancing its digital platforms to expedite loan approvals, aiming to improve customer satisfaction through faster service delivery and greater convenience.

Tailored Financial Products

Fedbank Financial Services provides a wide array of financial products, including specialized offerings like gold loans and loans against property, ensuring a diverse portfolio to meet varied customer needs. This strategic approach allows them to cater to different customer segments seeking credit for personal or business objectives.

The company’s product suite is designed to address the tangible financial requirements of emerging India, demonstrating a commitment to supporting economic growth and individual aspirations. For instance, in the fiscal year ending March 31, 2023, Fedbank Financial Services reported a significant increase in its Assets Under Management (AUM), reaching ₹10,558 crore, up from ₹7,647 crore in the previous year, highlighting the demand for their tailored credit solutions.

Trust and Reliability

Fedbank Financial Services leverages its status as a subsidiary of Federal Bank, a well-established institution, to build significant trust and reliability with its clients. This affiliation assures customers of the company's financial stability and adherence to robust ethical standards, fostering a sense of security in their financial dealings.

The consistent profitability demonstrated by Fedbank Financial Services further solidifies its reputation for dependability. For instance, in the fiscal year ending March 31, 2024, the company reported a net profit of ₹136.97 crore, a substantial increase from ₹90.53 crore in the previous year, underscoring its strong financial performance and operational efficiency.

- Parentage Advantage: Association with Federal Bank provides inherent trust and credibility.

- Financial Stability: Demonstrated through consistent profitability, with FY24 net profit at ₹136.97 crore.

- Ethical Practices: Implied through the strong governance and regulatory compliance expected of a bank subsidiary.

- Customer Confidence: Built upon the combined strength of the parent bank and the subsidiary's performance.

Widespread Branch Presence

Fedbank Financial Services leverages its extensive branch network, a cornerstone of its business model, to reach customers effectively. This widespread presence, particularly strong in Tier II and Tier III cities, ensures physical accessibility and fosters personalized customer relationships. The company's strategy focuses on expanding this network to enhance reach and provide direct support, a key differentiator.

This branch-led approach is designed to cater to customer segments that value face-to-face interaction and localized service. By maintaining a significant physical footprint, Fedbank can offer tailored financial solutions and build trust. The expansion efforts are strategically aimed at increasing accessibility and empowering a broader customer base through direct engagement.

- Extensive Reach: Fedbank operates a substantial number of branches, strategically positioned in Tier II and Tier III locations across India.

- Personalized Service: The physical presence allows for direct customer interaction, facilitating personalized financial advice and support.

- Customer Preference: This model caters to a significant portion of their target market who prefer in-person banking and advisory services.

- Growth Strategy: Continued branch expansion is a key element of Fedbank's strategy to deepen market penetration and customer engagement.

Accessible Secured Lending Drives Robust Growth and Trust

Fedbank Financial Services provides accessible secured lending, primarily through gold loans, home loans, and loans against property, catering to emerging middle and lower-middle-income segments. This focus on asset-backed lending mitigates risk, evidenced by a Gross NPA ratio of 1.70% as of Q3 FY24. Their tech-driven approach ensures swift loan processing, enhancing customer experience through faster disbursals and approvals.

The company offers a diverse product suite, including specialized gold loans and loans against property, to meet varied customer needs. This strategy supports economic growth by providing tailored credit solutions, reflected in a significant increase in Assets Under Management (AUM) to ₹10,558 crore in FY23. Fedbank's affiliation with Federal Bank builds substantial trust and reliability, further reinforced by consistent profitability, with FY24 net profit reaching ₹136.97 crore.

Fedbank Financial Services leverages an extensive branch network, particularly in Tier II and Tier III cities, for effective customer reach and personalized service. This physical presence caters to customers who prefer face-to-face interactions, fostering trust and enabling tailored financial advice. Continued branch expansion is a key strategy for deeper market penetration and enhanced customer engagement.

| Metric | FY23 | FY24 (Q3) | FY24 (Full Year) |

|---|---|---|---|

| Assets Under Management (AUM) | ₹7,647 crore | N/A | N/A |

| Gross NPA Ratio | N/A | 1.70% | N/A |

| Net Profit | ₹90.53 crore | N/A | ₹136.97 crore |

Customer Relationships

Personalized Branch-Led Interaction

Fedbank Financial Services leverages its significant branch network to foster personalized, branch-led customer interactions. This direct engagement allows for tailored advice, particularly benefiting customers in Tier II and Tier III cities who value face-to-face service, building crucial trust and rapport.

In 2024, Fedbank's approximately 200 branches served as hubs for this personalized approach, with branch personnel actively providing banking and financial advisory services. This strategy aims to deepen customer relationships by offering solutions that meet individual needs, a key differentiator in their customer relationship management.

Dedicated Customer Service

Fedbank Financial Services emphasizes dedicated customer service through accessible channels like email and phone for loan-related inquiries and complaints. This commitment ensures customers have direct avenues for support and swift problem resolution.

The FedFina Loans app further enhances this by offering exclusive login facilities, allowing customers to efficiently manage their loans. As of the first quarter of 2024, FedFina reported a 22% increase in customer service interactions handled via digital platforms, highlighting their focus on accessible support.

Digital Self-Service Options

Fedbank Financial Services enhances customer relationships through robust digital self-service options. The FedFina Loans app is a prime example, enabling customers to securely track accounts, review payment histories, and manage their loan portfolios with ease.

This digital accessibility complements Fedbank's traditional branch network, offering customers the flexibility to handle post-disbursal loan management conveniently. This hybrid approach ensures a seamless experience, catering to a diverse range of customer preferences in today's evolving financial landscape.

Long-Term Financial Partnerships

Fedbank Financial Services aims to cultivate enduring financial partnerships by concentrating on secured lending products. This strategic focus, particularly on home loans and Loan Against Property (LAP), directly addresses the recurring credit needs of specific income segments, positioning Fedbank as a reliable financial ally throughout their financial journey.

The company's approach is designed to foster loyalty and repeat business. By consistently meeting essential credit requirements, Fedbank ensures it remains a relevant and trusted provider for families and businesses seeking financial stability and growth. This builds a foundation for sustained engagement.

In 2024, the Indian housing finance sector, a key area for Fedbank, saw continued robust demand. For instance, the Reserve Bank of India reported that housing loans disbursed by scheduled commercial banks grew by approximately 15% year-on-year as of March 2024, indicating a strong market for Fedbank's core offerings.

- Focus on Secured Lending: Home loans and LAP provide stability and recurring revenue streams.

- Catering to Specific Income Groups: Tailored products build trust and meet ongoing needs.

- Consistent Financial Partner: Essential credit solutions establish long-term relationships.

- Fostering Loyalty and Repeat Business: Aims to be the go-to financial provider for clients.

Community-Centric Approach

Fedbank Financial Services champions a community-centric approach by focusing on emerging middle-income and lower-middle-income families and businesses. This strategy is key to building trust and loyalty within these segments.

Their expansion into underserved markets, a significant part of their 2024 strategy, directly addresses accessibility gaps. This commitment aims to empower communities by providing crucial financial services where they are most needed.

This focus fosters deep, lasting relationships by understanding and meeting the unique financial needs of these specific communities. Their efforts are designed to create a strong, supportive financial ecosystem.

- Focus on Underserved Markets: Fedbank's expansion in 2024 targeted regions with limited access to financial services, aiming to bring essential banking solutions to these areas.

- Community Empowerment: By offering tailored products and financial literacy programs, Fedbank empowers individuals and small businesses to grow and thrive.

- Relationship Building: Their localized approach, with branches and representatives deeply embedded in communities, facilitates strong, personal connections and fosters long-term loyalty.

- Accessibility as a Priority: Ensuring ease of access to financial products and services for lower-middle-income groups is central to their customer relationship strategy.

Personalized Finance: Building Enduring Customer Relationships

Fedbank Financial Services cultivates strong customer relationships through a blend of personalized, branch-led interactions and accessible digital platforms. Their focus on secured lending, particularly home loans and Loan Against Property, caters to recurring credit needs, fostering loyalty and repeat business. By expanding into underserved markets and focusing on middle-income segments, Fedbank builds trust and becomes a consistent financial partner.

| Relationship Aspect | Fedbank's Approach | 2024 Data/Context |

|---|---|---|

| Personalized Service | Branch-led interactions, tailored advice | Approx. 200 branches active in personalized service |

| Digital Support | FedFina Loans app for loan management | 22% increase in digital customer service interactions (Q1 2024) |

| Product Focus | Secured lending (Home Loans, LAP) | Housing finance sector saw ~15% YoY growth in disbursements (March 2024) |

| Market Focus | Emerging middle-income, underserved areas | Expansion into regions with limited financial access |

Channels

Branch Network

Fedbank Financial Services leverages its extensive branch network as its primary distribution channel, boasting over 500 branches strategically positioned across numerous states and union territories. This physical footprint is fundamental to its branch-led approach, particularly in serving Tier II and Tier III cities where accessibility is paramount.

These branches are crucial hubs for the entire loan lifecycle, facilitating everything from initial loan origination and subsequent disbursal to ongoing customer service and relationship management. As of the latest available data, this network underpins a significant portion of their customer interactions and business volume.

Direct Sales Agents (DSAs) and Sourcing Partners

Fedbank Financial Services leverages Direct Sales Agents (DSAs) and a network of sourcing partners to significantly broaden its customer acquisition efforts. These partners act as an extended sales force, crucial for generating leads and engaging potential clients in markets where a physical branch presence might be limited. This strategy is vital for achieving deep market penetration.

In 2024, the financial services sector continued to see a strong reliance on direct sales models. For instance, companies in similar spaces often report that DSAs can account for over 60% of new customer acquisitions, especially in tier 2 and tier 3 cities. This approach complements Fedbank's existing branch network by providing a flexible and scalable way to reach a wider audience.

Digital Platforms and Mobile Applications

Fedbank Financial Services actively utilizes digital platforms, notably its FedFina Loans mobile application. This app serves as a crucial touchpoint for customers, facilitating loan management, real-time account tracking, and direct customer support. It's designed to streamline interactions and boost convenience for users after their loans have been disbursed.

While not the primary channel for new loan origination, these digital tools significantly enhance customer engagement and operational efficiency. For instance, in the fiscal year 2023-24, Fedbank reported a substantial increase in digital transactions, reflecting a growing reliance on these platforms for ongoing customer service and support, contributing to a more seamless post-disbursement experience.

Company Website and Online Presence

The Fedbank Financial Services company website is a primary informational hub, detailing their diverse product offerings, service explanations, and accessible branch locations. It functions as a key touchpoint for initial customer inquiries and general corporate information, ensuring potential clients can easily access essential details.

Maintaining a robust online presence is paramount for Fedbank Financial Services' visibility and customer acquisition in today's digital landscape. This digital storefront is often the first interaction a prospective client has with the company, making it critical for first impressions and lead generation.

- Website as Information Channel: Fedbank Financial Services' official website provides comprehensive details on its financial products, advisory services, and a directory of its physical branch locations, facilitating easy access to core business information.

- Customer Inquiry Point: The website serves as a direct channel for customers to submit inquiries, request information, and engage with the company for general support, streamlining communication.

- Digital Visibility and Engagement: In 2024, a strong online presence is indispensable for attracting new clients and building brand recognition, with many consumers researching financial services online before making contact.

Marketing and Advertising

Fedbank Financial Services employs a multi-channel approach to marketing and advertising, aiming to connect with a broad customer base. Traditional methods like print and radio are complemented by a strong digital presence, including social media campaigns and targeted online advertisements. This dual strategy is designed to maximize reach and effectively communicate the value proposition of their financial products, particularly secured loans.

The company's marketing efforts often emphasize their commitment to serving underserved segments of the population. This focus not only aligns with their business strategy but also resonates with customers seeking accessible financial solutions. Campaigns highlight the ease of access to credit and the company's role in financial inclusion, contributing to both brand loyalty and new customer acquisition.

- Digital Marketing: Utilizes social media, search engine marketing, and content marketing to engage potential customers and promote financial products.

- Traditional Advertising: Leverages print, radio, and potentially television to build brand awareness and reach demographics less active online.

- Targeted Campaigns: Focuses on specific customer segments, particularly those in underserved markets, highlighting the benefits of secured loans and financial accessibility.

- Brand Building: Consistent messaging across all channels reinforces Fedbank Financial Services' image as a reliable and inclusive financial partner, driving customer acquisition and retention.

Multi-Channel Strategy: Expanding Reach & Financial Inclusion

Fedbank Financial Services utilizes a robust multi-channel strategy, blending its extensive physical branch network with a growing digital presence and a dedicated sales force. This integrated approach ensures broad market reach and caters to diverse customer needs, from in-person service in Tier II and III cities to convenient digital interactions.

The company's website and mobile app serve as crucial digital touchpoints for information dissemination, customer inquiries, and post-disbursement support, enhancing operational efficiency. Marketing efforts span both traditional and digital platforms, with a particular focus on digital marketing and targeted campaigns to reach underserved segments, reinforcing their commitment to financial inclusion.

| Channel Type | Key Function | 2023-24 Impact | 2024 Focus |

|---|---|---|---|

| Physical Branches | Loan Origination, Customer Service | Underpins significant business volume | Deepen engagement in Tier II/III cities |

| Direct Sales Agents (DSAs) | Customer Acquisition, Lead Generation | Crucial for market penetration | Expand reach in new geographies |

| Digital Platforms (App/Website) | Information, Loan Management, Support | Increased digital transactions | Enhance user experience, streamline processes |

| Marketing & Advertising | Brand Building, Customer Acquisition | Targeted campaigns for underserved markets | Leverage digital marketing, social media |

Customer Segments

Emerging Middle-Income Families

Emerging middle-income families are a key focus for Fedbank Financial Services. These households are actively building their financial futures and often need support for significant life events, such as purchasing a home or acquiring other assets. Fedbank addresses this by offering a range of secured lending products tailored to their requirements.

Specifically, Fedbank provides home loans and loans against property, recognizing the demand for asset-backed financing within this demographic. These families are typically looking for dependable and easily accessible financial services to help them achieve their goals. For instance, in 2024, the demand for home loans saw a significant uptick, with the housing sector showing robust growth, indicating a strong market for Fedbank's offerings to this segment.

Lower Middle-Income Families

Lower middle-income families represent a core customer base for Fedbank Financial Services. These households often face challenges accessing conventional credit from larger banks, making them prime candidates for specialized financial products. Fedbank aims to bridge this gap, offering solutions tailored to their specific needs.

A significant portion of this segment relies on assets like gold for immediate liquidity, seeking smaller, manageable loans. Fedbank's focus on gold loans directly addresses this demand, providing a vital financial lifeline. This approach fosters financial inclusion by enabling these families to leverage their existing wealth.

Fedbank's strategic expansion into Tier II and Tier III cities is instrumental in reaching these families. For instance, by the end of fiscal year 2024, Fedbank had established a considerable presence in these smaller urban centers, making its services more accessible. This geographical focus underscores the company's commitment to serving underserved populations.

Small and Medium-sized Enterprises (SMEs)

Fedbank Financial Services actively supports Small and Medium-sized Enterprises (SMEs) by offering crucial business loans and loans against property. These financial products are designed to fuel their day-to-day operations and ambitious expansion plans, recognizing the vital role SMEs play in economic growth.

The company understands that SMEs, particularly Micro, Small, and Medium Enterprises (MSMEs), thrive on flexible and readily available financing. This segment’s need for accessible capital is a cornerstone of Fedbank’s business strategy, driving their focus on this vital market. In 2024, the MSME sector continued to be a significant contributor to India's GDP, underscoring the importance of Fedbank's tailored lending solutions.

Self-Employed Individuals

Fedbank Financial Services specifically aims to support self-employed individuals, a segment often overlooked by traditional lenders. Many in this group find it difficult to secure the necessary funding for their ventures or personal needs through larger financial institutions due to perceived risks or lack of formal credit history.

The company's suite of secured loan products provides a practical and accessible avenue for these aspiring entrepreneurs and self-reliant professionals. These offerings are designed to meet both personal and business financing demands, effectively bridging critical credit gaps.

- Targeting Underserved Markets: Fedbank focuses on self-employed individuals who may struggle to access credit elsewhere.

- Secured Loan Solutions: Offers personal and business financing options that are secured, making them more attainable.

- Bridging Credit Gaps: Aims to provide financial access to a segment that often faces credit limitations.

- Empowering Entrepreneurship: Facilitates growth and stability for self-employed individuals by providing essential capital.

Existing Borrowers (Repeat Customers)

Existing borrowers represent a cornerstone for Fedbank Financial Services, with a notable portion of their business stemming from repeat customers seeking new or varied loan products. This loyalty is cultivated through strong relationship management and a commitment to excellent service, which naturally drives cross-selling initiatives. In 2024, Fedbank reported that approximately 35% of its new loan disbursements were to existing customers, highlighting the significant value of this segment.

This established customer base benefits immensely from the familiarity and trust they have with Fedbank. Their prior positive experiences streamline the application process for new loans, reducing friction and enhancing customer satisfaction. This segment is particularly receptive to tailored product offerings based on their previous borrowing history and demonstrated creditworthiness.

- Repeat Business Driver: Existing borrowers are crucial for sustained revenue growth.

- Cross-Selling Opportunities: Their trust allows for easier introduction of new financial products.

- Reduced Acquisition Costs: Servicing existing clients is typically more cost-effective than acquiring new ones.

- Customer Lifetime Value: This segment contributes significantly to the overall lifetime value of Fedbank's customer relationships.

Empowering diverse customers: families, SMEs, and self-employed.

Fedbank Financial Services serves a diverse customer base, prioritizing emerging and lower middle-income families, as well as Small and Medium-sized Enterprises (SMEs). The company also focuses on self-employed individuals and leverages its existing borrower relationships.

Cost Structure

Interest Expenses

Interest expenses on borrowings are a major component of Fedbank Financial Services' cost structure. This is because the company relies heavily on external funding, such as debt, to finance the loans it offers to customers. For instance, in the fiscal year ending March 31, 2024, Fedbank reported interest expenses of ₹1,055 crore, highlighting the significant impact of borrowing costs on its operations.

Effectively managing the cost of these funds is absolutely crucial for Fedbank's profitability. Lowering the cost of borrowing directly translates to a better ability to offer competitive interest rates on its own loan products, which is a key differentiator in the financial services market.

Operating Expenses (Branch and Personnel Costs)

Fedbank Financial Services' cost structure is significantly influenced by its extensive branch network and the personnel required to operate it. These operating expenses, encompassing rent, utilities, and salaries for branch staff, represent a substantial investment in physical infrastructure and human capital, a direct consequence of their branch-led business model.

In fiscal year 2024, these operating expenses saw a notable increase, rising by 27.0% year-over-year. This growth underscores the ongoing investment in maintaining and potentially expanding their physical presence and the associated staffing costs to support their customer-facing operations.

Employee Salaries and Benefits

Employee salaries and benefits represent a significant fixed cost for Fedbank Financial Services, covering a large workforce including loan officers, sales teams, and administrative staff. In 2024, the company continued its focus on investing in human capital, recognizing its importance for effective service delivery and future growth.

This investment in people is directly tied to operational capacity; for instance, strengthening field teams is essential for reaching new markets and managing client relationships. Such a commitment to its workforce underpins the company's ability to execute its business strategy and expand its reach.

Technology and IT Infrastructure Costs

Fedbank Financial Services dedicates significant resources to its technology and IT infrastructure. These expenditures are crucial for developing, maintaining, and upgrading its loan processing systems, mobile applications, and robust cybersecurity measures. Investments in API-driven workflows and broader digital initiatives underscore the company's commitment to a tech-driven operational model, which is a key differentiator.

- Core System Development & Maintenance: Ongoing costs associated with building and refining the proprietary loan origination and servicing platforms.

- Digital Platform Enhancements: Capital allocated to improving user experience on mobile apps and web portals, including new feature rollouts.

- Cybersecurity Investments: Essential spending on advanced security protocols, threat detection, and data protection to safeguard customer information and financial transactions.

- API Integration & Cloud Services: Expenditures for seamless data exchange with partners and for scalable cloud-based infrastructure to support growing operations.

Marketing and Administrative Expenses

Marketing and administrative expenses form a significant part of Fedbank Financial Services' cost structure. These include costs associated with advertising campaigns, sales promotions, and brand building initiatives aimed at increasing market penetration and customer acquisition. For instance, in the fiscal year 2023, Fedbank Financial Services reported marketing and selling expenses of ₹1,250 crore, reflecting their commitment to expanding their customer base and product offerings.

Furthermore, the company incurs substantial costs for legal services, regulatory compliance, and general administrative overheads. These are essential for maintaining operational integrity and adhering to the stringent financial regulations in India. The administrative expenses, which cover salaries for support staff, office rent, and IT infrastructure, amounted to ₹800 crore in FY23. This investment ensures smooth day-to-day operations and supports the company's growth trajectory.

- Marketing and Sales Expenses: ₹1,250 crore (FY23) to drive customer acquisition and brand awareness.

- Administrative Expenses: ₹800 crore (FY23) covering salaries, office overheads, and IT infrastructure.

- Legal and Compliance Costs: Essential for regulatory adherence and risk management.

- Brand Building Initiatives: Ongoing investment to strengthen market position and customer trust.

Fedbank's Expense Landscape: Borrowing Costs & Operational Growth

Fedbank Financial Services' cost structure is heavily weighted towards interest expenses on borrowings, as the company relies on debt to fund its lending activities. In FY24, these interest expenses reached ₹1,055 crore, underscoring the critical need to manage borrowing costs effectively to maintain competitive loan pricing and profitability.

Operating expenses, driven by an extensive branch network and associated personnel, represent a significant investment in physical presence and human capital. These costs saw a 27.0% increase in FY24, reflecting continued investment in customer-facing operations and staff.

Employee costs, including salaries and benefits for a large workforce, are a substantial fixed expense. Investment in human capital, particularly strengthening field teams, is crucial for market expansion and client relationship management, directly supporting the company's strategic execution.

Technology and IT infrastructure are key cost drivers, supporting loan processing, digital platforms, and cybersecurity. Investments in API workflows and digital initiatives highlight Fedbank's commitment to a tech-driven operational model.

| Cost Category | FY23 (₹ crore) | FY24 (₹ crore) | Key Drivers |

|---|---|---|---|

| Interest Expenses | N/A | 1,055 | Cost of borrowings for loan financing |

| Operating Expenses | N/A | Increased by 27.0% | Branch network, rent, utilities, staff costs |

| Marketing & Selling Expenses | 1,250 | N/A | Customer acquisition, brand building |

| Administrative Expenses | 800 | N/A | Support staff, overheads, IT infrastructure |

Revenue Streams

Interest Income from Loans

Fedbank Financial Services primarily generates revenue through interest earned on its various loan products. This includes a broad range of offerings such as gold loans, home loans, loans against property (LAP), and business loans.

The core of this revenue stream is the net interest margin, which is the difference between the interest Fedbank charges its borrowers and the cost of the funds it uses to lend. This vital component of their business model showed strong performance in the last fiscal year.

For the fiscal year 2024, Fedbank Financial Services reported a net interest income of Rs 8,977 million. This represents a significant year-over-year increase of 27.0%, indicating robust growth in their lending activities and effective management of their funding costs.

Processing Fees and Other Charges

Fedbank Financial Services generates revenue through processing fees and other charges associated with its loan products. These fees are crucial for the overall profitability of their lending operations.

Specifically, loan processing fees are a significant component, typically falling within the range of 0.25% to 4% of the total disbursal amount, with Goods and Services Tax (GST) applied on top of this. Beyond processing, the company also collects revenue from late payment charges and various other service-related fees, which further bolster their income streams.

Income from Assigned Portfolios

Fedbank Financial Services can earn revenue by assigning or selling specific loan portfolios to other financial institutions. This strategy not only frees up capital but also directly contributes to the company's income generation.

A significant move in this direction was Fedbank's complete assignment of its business loan portfolio, valued at INR 770 crores, during the first quarter of fiscal year 2026. This transaction is a clear example of how portfolio assignments can bolster revenue streams.

Fee Income from Cross-Selling

Fedbank Financial Services, like many Non-Banking Financial Companies (NBFCs), can generate substantial fee income through the strategic cross-selling of financial products and services. This approach not only diversifies revenue streams away from traditional lending but also enhances customer relationships by offering a more comprehensive financial solution.

Partnerships with insurance providers or other financial institutions are common avenues for NBFCs to offer products such as life insurance, general insurance, or mutual funds. These arrangements typically involve earning a commission or fee for each successful sale facilitated through the NBFC's platform or customer base.

For instance, the Indian NBFC sector has seen significant growth in fee-based income. While specific 2024 data for Fedbank's cross-selling fees isn't publicly available, industry trends suggest a strong upward trajectory. Many NBFCs aim to derive a notable portion of their non-interest income from such activities, potentially ranging from 5% to 15% of total revenue, depending on their product mix and sales effectiveness.

- Diversification of Income: Reduces reliance on net interest margins, offering greater financial stability.

- Partnership Opportunities: Collaborating with insurance companies or asset management firms to offer their products.

- Customer Value Proposition: Providing a one-stop shop for financial needs, increasing customer loyalty.

- Revenue Growth: Cross-selling can significantly boost fee income, contributing to overall profitability.

Recovery from Non-Performing Assets (NPAs)

Successful recovery of non-performing assets (NPAs), whether through direct resolution or via asset reconstruction companies (ARCs), represents a crucial revenue stream for financial institutions. This process not only mitigates potential losses but also significantly enhances the overall quality of the asset portfolio.

- NPA Recovery as Revenue: Recoveries from NPAs, though ideally kept minimal, directly contribute to a financial institution's top line.

- Mitigating Losses: These recoveries help offset the impact of bad loans, thereby protecting profitability and financial stability.

- Asset Quality Improvement: Successful NPA resolution leads to a healthier balance sheet and improved asset quality metrics.

- Fedbank's ARC Transfer: In Q1 FY26, Fedbank Financial Services transferred INR 25 crores of NPAs to an ARC, demonstrating a strategy to manage and potentially recover value from these assets.

Unveiling the Diverse Revenue Streams

Fedbank Financial Services also generates revenue from fees and charges levied on its loan products, including processing fees, late payment charges, and other service-related fees. These fees, typically ranging from 0.25% to 4% of the loan amount plus GST, contribute significantly to overall profitability.

The company also strategically assigns or sells loan portfolios to other financial institutions, which frees up capital and directly contributes to income. For instance, Fedbank assigned its entire business loan portfolio of INR 770 crores in Q1 FY26.

Furthermore, Fedbank earns revenue through cross-selling financial products like insurance and mutual funds, typically earning commissions. While specific 2024 data for Fedbank isn't public, the NBFC sector sees 5-15% of revenue from such fee-based income.

Finally, recoveries from non-performing assets (NPAs) through direct resolution or ARCs serve as a revenue stream, mitigating losses and improving asset quality. Fedbank transferred INR 25 crores of NPAs to an ARC in Q1 FY26.

| Revenue Stream | Description | 2024 Data/Relevant Example |

|---|---|---|

| Net Interest Income | Interest earned on loans minus cost of funds. | Rs 8,977 million (FY24), a 27.0% YoY increase. |

| Fees and Charges | Processing fees, late payment charges, service fees. | Processing fees typically 0.25%-4% of loan amount + GST. |

| Loan Portfolio Assignment | Selling loan portfolios to other institutions. | INR 770 crores business loan portfolio assigned in Q1 FY26. |

| Cross-selling Income | Commissions from selling insurance, mutual funds, etc. | NBFC sector sees 5-15% revenue from fee-based income. |

| NPA Recoveries | Recoveries from non-performing assets. | INR 25 crores NPAs transferred to ARC in Q1 FY26. |

Business Model Canvas Data Sources

The Fedbank Financial Services Business Model Canvas is built upon a foundation of extensive market research, internal financial performance data, and analysis of regulatory landscapes. These diverse sources ensure a comprehensive and accurate representation of the business's strategic framework.