Eris Lifesciences SWOT Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Eris Lifesciences

Dive Deeper Into the Company’s Strategic Blueprint

Eris Lifesciences, a prominent player in the Indian pharmaceutical market, demonstrates robust strengths in its specialized product portfolio and strong brand equity, particularly in the chronic therapy areas. However, it faces potential threats from increasing competition and evolving regulatory landscapes.

Want the full story behind Eris Lifesciences’ strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

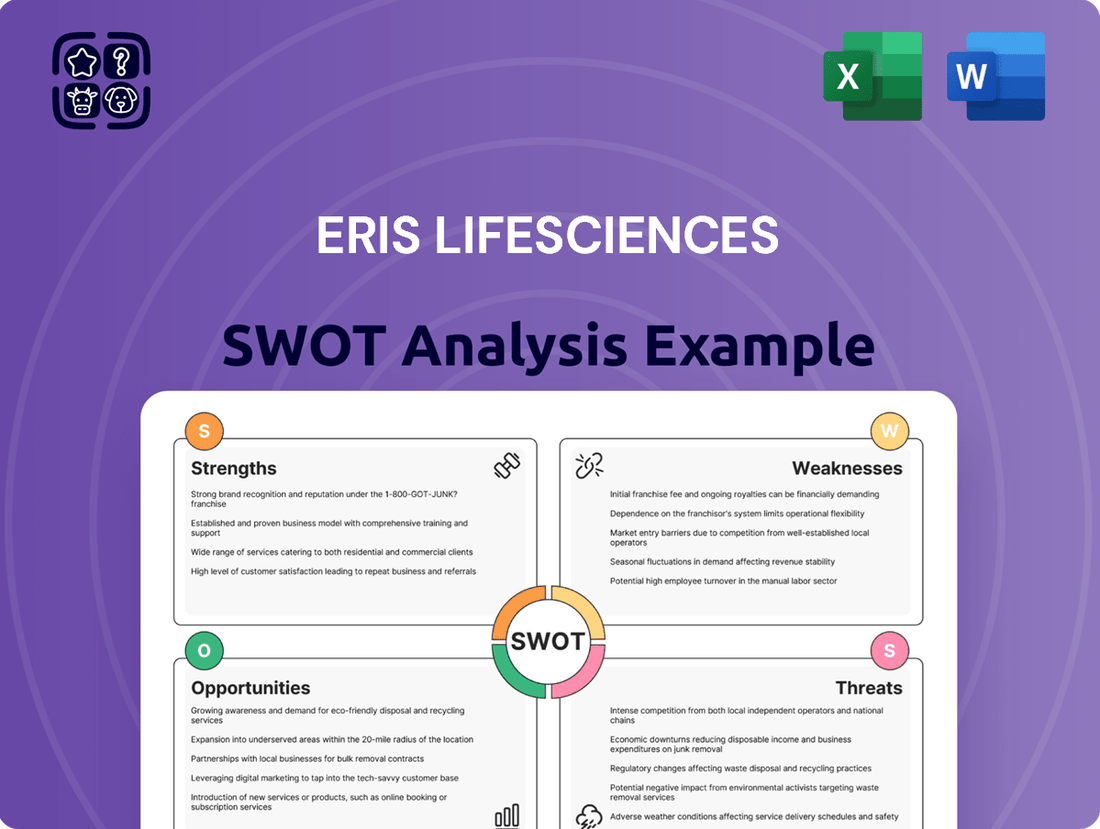

Strengths

Strong Focus on Chronic and Lifestyle-Related Therapies

Eris Lifesciences' core strength lies in its dedicated focus on chronic and lifestyle-related therapies, a strategic alignment with India's increasing burden of such conditions. This specialization enables them to hone their marketing efforts and product development for a substantial and growing patient demographic.

Their robust performance in key chronic segments, including cardiac, anti-diabetic, and neurology/central nervous system (CNS) therapies, underscores this advantageous positioning. For instance, in the fiscal year 2023-24, Eris Lifesciences reported significant growth in its chronic business, contributing over 70% of its total revenue, with cardiac and anti-diabetic segments showing particular resilience.

Robust Financial Performance and Growth

Eris Lifesciences has showcased impressive financial momentum. For the fourth quarter of fiscal year 2024-2025, the company reported a notable surge in revenue, continuing this trend for the entirety of FY2025. This robust top-line growth was complemented by a substantial increase in net profit during the same Q4 period.

Strategic Acquisitions and Portfolio Expansion

Eris Lifesciences has demonstrated a strong growth strategy through targeted acquisitions. A notable example is its February 2024 acquisition of a 51% stake in Swiss Parenterals, a move that bolstered its presence in the injectables market.

Further strengthening its portfolio, Eris acquired the India branded formulation business of Biocon Biologics in March 2024. This strategic move allowed Eris to expand into crucial therapeutic areas, including oncology and critical care.

These acquisitions have significantly broadened Eris Lifesciences' market reach and product offerings. The company has solidified its position as a leader, particularly in the rapidly growing insulin segment, by integrating these new capabilities.

Established Presence in the Indian Pharmaceutical Market

Eris Lifesciences holds a significant position as a leading player in India's domestic branded formulations market. Its recognition as one of the youngest companies to achieve a top 20 ranking within the Indian Pharmaceutical Market (IPM) underscores its rapid growth and market penetration.

This established presence translates into tangible benefits, including robust distribution networks and strong brand recall among healthcare professionals and patients. For instance, as of Q4 FY24, Eris Lifesciences reported a revenue of INR 1,444 crore for the fiscal year, demonstrating its substantial operational scale.

- Market Leadership: A prominent position in the branded formulations segment.

- Youthful Growth: Among the youngest top 20 players in the IPM, indicating agility and rapid expansion.

- Brand Equity: Strong brand recognition built through consistent performance and market engagement.

- Distribution Strength: Well-established networks facilitating product reach across India.

Patient-Centric Initiatives and Manufacturing Capabilities

Eris Lifesciences distinguishes itself through robust patient-centric initiatives (PCI), offering a comprehensive platform of healthcare solutions designed to enhance patient outcomes and adherence. This focus directly addresses the evolving needs of the healthcare landscape, fostering stronger patient relationships and potentially leading to improved long-term market share.

The company's strategic manufacturing facility located in Guwahati, Assam, is a significant strength, providing a stable and controlled production base. This facility underpins the consistent quality and reliable supply of its diverse product portfolio, a critical factor in the competitive pharmaceutical market. For instance, in the fiscal year 2023, Eris Lifesciences reported a revenue of INR 1,270 crore, showcasing the scale of its operations and the demand for its products.

- Patient-Centric Initiatives: Eris Lifesciences' PCI platform provides integrated healthcare solutions, aiming to improve patient well-being and treatment effectiveness.

- Manufacturing Prowess: The Guwahati manufacturing plant ensures supply chain resilience and stringent quality control for Eris's wide array of pharmaceutical products.

- Operational Scale: With revenues reaching INR 1,270 crore in FY23, the company demonstrates significant operational capacity and market penetration.

Indian Pharma's Ascent: Chronic Care Focus & Strategic Acquisitions

Eris Lifesciences' strategic focus on chronic and lifestyle-related therapies, particularly in cardiac, anti-diabetic, and CNS segments, positions it well within India's growing healthcare needs. Its rapid ascent to become one of the youngest top 20 players in the Indian Pharmaceutical Market (IPM) highlights its agility and market penetration.

The company's robust financial performance, evidenced by significant revenue and profit growth in FY2025, underscores its operational strength. Furthermore, strategic acquisitions, such as the stakes in Swiss Parenterals and the Biocon Biologics formulation business in early 2024, have substantially expanded its product portfolio and market reach, especially in injectables, oncology, and critical care.

Eris Lifesciences boasts strong brand equity and well-established distribution networks, facilitating deep market penetration. Its patient-centric initiatives (PCI) further enhance patient engagement and treatment adherence, creating a competitive advantage. The company's manufacturing facility in Guwahati also ensures supply chain stability and product quality.

| Key Financial & Market Data (FY2024-2025) | ||

| Total Revenue (FY2024-2025) | INR 1,444 crore (Q4 FY24 figure for context, full FY25 data expected) | |

| Chronic Business Contribution | Over 70% of total revenue | |

| Acquisition: Swiss Parenterals | February 2024 (51% stake) | |

| Acquisition: Biocon Biologics Business | March 2024 |

What is included in the product

Delivers a strategic overview of Eris Lifesciences’s internal and external business factors, highlighting its strengths in chronic disease management and opportunities in the growing Indian pharmaceutical market, while also addressing potential weaknesses in product diversification and threats from intense competition.

Offers a clear, actionable SWOT analysis for Eris Lifesciences, simplifying complex market dynamics to pinpoint pain points and strategic opportunities.

Weaknesses

Increased Debt and Interest Costs

Eris Lifesciences' financial position shows a notable increase in current liabilities and long-term debt as of FY2024. This rise in borrowing directly translates to higher interest expenses, as evidenced by the substantial increase in interest costs observed in Q1 FY2025.

The growing debt burden poses a potential risk of liquidity strain for the company. Furthermore, increased financial leverage can negatively impact overall profitability and long-term financial stability, making the company more vulnerable to economic downturns.

Fluctuating Profit Margins and Net Profit

Eris Lifesciences has experienced fluctuating profit margins, with a notable dip in net income and profit margin in FY2025 compared to FY2024. This variability, particularly a decrease in the net profit margin from 15.2% in FY2024 to 13.8% in FY2025, raises concerns about the company's ability to consistently translate revenue growth into stable profitability.

Such inconsistencies can stem from challenges in managing operational costs or implementing effective pricing strategies. This might impact investor sentiment, as a predictable and steady profit stream is often a key indicator of a company's financial health and future potential.

Slowing Debtor Turnover Ratio

Eris Lifesciences has experienced a slowdown in its debtor turnover, with the ratio hitting a five-half-yearly period low as of June 2024. This suggests that the company is taking longer to collect payments from its customers.

This declining debtors turnover ratio, falling to its lowest point in the last five half-yearly periods by June 2024, points to potential inefficiencies in managing its accounts receivable. Such a trend can strain working capital and negatively affect the company's overall cash flow generation.

Dependence on Domestic Branded Formulations

Eris Lifesciences' significant reliance on its domestic branded formulations business, which constituted around 90% of its revenue in recent periods, presents a notable weakness. This concentration, while beneficial in a stable market, exposes the company to potential risks stemming from shifts in domestic market dynamics or unforeseen regulatory alterations impacting the branded generics sector.

The company's revenue streams are heavily anchored in this segment, making it vulnerable to any adverse developments. For instance, a slowdown in the Indian pharmaceutical market or stricter pricing controls on branded generics could disproportionately affect Eris's overall financial performance.

- Revenue Concentration: Approximately 90% of Eris Lifesciences' revenue is derived from its domestic branded formulations.

- Market Sensitivity: High dependence on the Indian branded generics market makes the company susceptible to sector-specific downturns.

- Regulatory Risk: Potential changes in Indian pharmaceutical regulations could negatively impact the profitability of its core business.

Underperformance in Specific Market Segments

Eris Lifesciences has faced challenges with underperformance in certain market segments. For instance, in May 2023, the company saw a sales decline, falling below the market average during that specific period. This indicates that while their core chronic therapy business is robust, other areas of their product portfolio may not be keeping pace with market growth.

This underperformance suggests potential weaknesses in Eris Lifesciences' strategy for specific therapeutic areas or product lines. While the company has demonstrated market-beating growth in some of its key chronic therapies, these isolated instances of lagging performance highlight a need for closer examination of their market penetration and competitive positioning in less successful segments.

- May 2023 Sales Dip: Eris Lifesciences' sales declined in May 2023, underperforming the market average for that month.

- Segment-Specific Struggles: The company's growth in certain market segments has been weaker compared to its overall performance.

- Competitive Pressure: This underperformance points to potential competitive challenges in specific therapeutic areas or product categories.

Financial Headwinds: Debt, Margins, and Concentration Risks

Eris Lifesciences' substantial debt, with current liabilities and long-term debt increasing in FY2024, leads to higher interest expenses, as seen in Q1 FY2025. This leverage heightens liquidity risks and can hinder long-term financial stability.

The company's profit margins have shown volatility, with a decline in net profit margin from 15.2% in FY2024 to 13.8% in FY2025, indicating potential issues with cost management or pricing strategies that could affect investor confidence.

A weakening debtor turnover ratio, reaching a five-half-yearly low by June 2024, suggests slower collection of payments, which can strain working capital and cash flow.

Eris Lifesciences' heavy reliance on its domestic branded formulations, accounting for about 90% of revenue, makes it vulnerable to market shifts and regulatory changes within the Indian pharmaceutical sector.

| Metric | FY2024 | FY2025 | Trend |

|---|---|---|---|

| Net Profit Margin | 15.2% | 13.8% | Decreasing |

| Debtor Turnover Ratio (Half-Yearly) | N/A | 5-period Low (June 2024) | Decreasing |

| Domestic Branded Formulations Revenue % | ~90% | ~90% | Stable (High Concentration) |

What You See Is What You Get

Eris Lifesciences SWOT Analysis

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version, providing a comprehensive look at Eris Lifesciences' Strengths, Weaknesses, Opportunities, and Threats.

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. It details Eris Lifesciences' internal capabilities and external market factors, offering actionable insights.

You’re viewing a live preview of the actual SWOT analysis file. The complete version becomes available after checkout, allowing you to fully leverage the strategic information presented for Eris Lifesciences.

Opportunities

Growing Indian Pharmaceutical Market

The Indian pharmaceutical market is experiencing robust growth, with projections indicating it will reach approximately $130 billion by 2030, up from around $50 billion in 2022. This expansion is fueled by a rising middle class, increasing healthcare awareness, and government programs like Ayushman Bharat, which aims to provide health insurance to a large segment of the population.

Eris Lifesciences is well-positioned to capitalize on this trend, especially with its focus on chronic care and branded generics. The company’s established presence in Tier II and Tier III cities, which are seeing significant healthcare infrastructure development, offers a prime opportunity for market penetration and increased sales volumes.

Expansion into Injectables and Biosimilars

Eris Lifesciences' strategic acquisitions have successfully paved its way into the burgeoning injectables market, bolstering its footprint in crucial therapeutic areas like insulin, oncology, and critical care. This move aligns perfectly with the robust growth trajectory of the Indian injectables market, which is a significant opportunity for expansion.

Furthermore, the company is well-positioned to capitalize on the substantial potential within the global biosimilars market. As key patents expire, Eris can leverage its capabilities to offer high-value, cost-effective alternatives, driving significant growth and market share in this rapidly evolving sector.

Leveraging Acquisitions for Synergies and New Product Launches

Eris Lifesciences can capitalize on its recent acquisitions, such as Biocon Biologics and Swiss Parenterals, to unlock substantial synergies. These integrations present a clear path for margin expansion, particularly through the insourcing of manufacturing processes. This strategic move is expected to enhance profitability and operational efficiency.

Furthermore, the acquisition of Swiss Parenterals provides Eris Lifesciences with access to an impressive product pipeline exceeding 230 molecules. This robust pipeline offers a significant opportunity for the launch of new products, which can fuel future revenue growth and bolster the company's market share in key therapeutic areas.

Increasing Prevalence of Lifestyle-Related Disorders

The increasing prevalence of lifestyle-related disorders in India is a significant driver for the pharmaceutical sector. Conditions like diabetes, cardiovascular diseases, and obesity are on the rise, creating a sustained demand for chronic and acute therapies. Eris Lifesciences, with its strategic focus on these very therapeutic areas, is well-positioned to benefit from this demographic shift.

The company's commitment to developing and marketing products that address these prevalent health issues allows it to tap into a growing market. For instance, the diabetes care segment, a key area for Eris, saw a substantial market size in India, estimated to be around $2.5 billion in 2023 and projected to grow further. This growth is directly linked to the increasing number of people diagnosed with diabetes, a classic lifestyle-related disorder.

- Rising Health Concerns: Lifestyle disorders such as diabetes, hypertension, and obesity are becoming more common across India.

- Therapeutic Demand: This trend directly translates into increased demand for chronic and acute medications to manage these conditions.

- Eris's Strategic Fit: Eris Lifesciences' core business, focusing on cardiovascular and anti-diabetic therapies, aligns perfectly with this market opportunity.

- Market Growth: The Indian cardiovascular drugs market alone was valued at approximately $4.2 billion in 2023 and is expected to expand, reflecting the growing health challenges.

Digital Transformation and R&D Enhancement

The Indian pharmaceutical industry's embrace of digital transformation, including AI, presents a significant opportunity for Eris Lifesciences. These technologies are crucial for boosting R&D efficiency and speeding up the journey from discovery to market. By integrating these advancements, Eris can refine its drug development pipelines and enhance overall operational effectiveness, potentially leading to cost savings and a stronger market position.

Eris Lifesciences can capitalize on the trend of digital adoption within the Indian pharma sector. For instance, the sector saw increased investment in digital health solutions and AI-driven research in 2024. This strategic move allows Eris to streamline its R&D, improve manufacturing processes, and gain a competitive advantage through innovation and efficiency.

- Leveraging AI for Drug Discovery: AI platforms can analyze vast datasets to identify potential drug candidates more rapidly, reducing R&D timelines.

- Digitalizing Clinical Trials: Implementing digital tools for data collection and patient monitoring in clinical trials can improve accuracy and reduce logistical overhead.

- Enhancing Supply Chain Visibility: Digital solutions can provide real-time tracking and management of the pharmaceutical supply chain, minimizing stockouts and wastage.

- Personalized Medicine Development: AI and data analytics can facilitate the development of personalized treatment plans, catering to specific patient needs and improving outcomes.

Driving Growth in India's Chronic Care & Pharma Market

Eris Lifesciences is poised to benefit from the increasing prevalence of lifestyle diseases in India, such as diabetes and cardiovascular conditions. The company's focus on chronic care therapies directly addresses this growing market need, with the diabetes care segment alone valued at approximately $2.5 billion in 2023.

Strategic acquisitions, like those of Biocon Biologics and Swiss Parenterals, offer significant opportunities for synergy and margin expansion, particularly through manufacturing insourcing. The Swiss Parenterals acquisition alone provides access to a pipeline of over 230 molecules, fueling future product launches.

The company can leverage the expanding Indian pharmaceutical market, projected to reach $130 billion by 2030, by strengthening its presence in Tier II and Tier III cities. Furthermore, its entry into the injectables market and potential in global biosimilars represent substantial avenues for growth.

Digital transformation, including the adoption of AI in R&D and clinical trials, presents an opportunity for Eris to enhance efficiency and accelerate drug development. The Indian pharma sector's increased investment in digital solutions in 2024 supports this strategic advantage.

Threats

Intense Competition in the Indian Pharmaceutical Market

The Indian pharmaceutical market is a crowded space, with a vast number of domestic companies and global giants vying for market share. This fierce competition often translates into significant pricing pressures, making it challenging for companies like Eris Lifesciences to maintain healthy profit margins. For instance, by the end of fiscal year 2023, the Indian pharmaceutical market was estimated to be worth around $42 billion, showcasing the scale of competition.

This intense rivalry can also lead to a dilution of market share, as new products and aggressive marketing campaigns from competitors constantly challenge established players. Eris Lifesciences, like others in the sector, faces the continuous need to invest heavily in marketing and sales to retain and grow its customer base, which can strain its financial resources and impact overall growth trajectories.

Regulatory Challenges and Compliance Changes

The pharmaceutical sector faces significant regulatory hurdles, and Eris Lifesciences is no exception. Evolving compliance requirements, such as those anticipated from the European Medicines Agency (EMA) in 2025, can necessitate substantial investments in adapting processes and documentation, potentially impacting profitability.

Furthermore, potential policy shifts, including ongoing discussions regarding pharmaceutical tariffs, could introduce new cost pressures and operational complexities. For instance, a hypothetical 5% tariff on imported active pharmaceutical ingredients (APIs) could add millions in annual costs if Eris Lifesciences relies heavily on such imports.

Rising Interest Expenses and Debt Burden

Eris Lifesciences faces a growing threat from rising interest expenses and an increasing debt burden. As interest rates climb, the cost of servicing its existing debt will naturally go up, putting pressure on profitability.

The company's debt-to-equity ratio, which stood at approximately 0.26 as of March 31, 2024, indicates a moderate level of leverage. However, any further increase in borrowing, coupled with a sustained high-interest rate environment, could significantly strain its financial resources, potentially limiting its capacity for crucial investments in research and development or strategic acquisitions.

Supply Chain Disruptions and Input Cost Volatility

Eris Lifesciences faces significant risks from supply chain disruptions and fluctuating input costs, common challenges in the pharmaceutical sector. These issues can directly impact manufacturing timelines and increase operational expenses. For instance, the global pharmaceutical industry has experienced raw material shortages and price hikes, particularly for active pharmaceutical ingredients (APIs) and excipients, driven by geopolitical events and increased demand. This volatility can squeeze profit margins and affect product affordability.

The company's reliance on a global network for sourcing key materials exposes it to potential bottlenecks. For example, disruptions in countries like China, a major supplier of APIs, can have a ripple effect. In 2023, reports indicated continued supply chain pressures for certain drug components, leading to price increases for some finished products. This environment necessitates robust inventory management and strategic supplier diversification for Eris Lifesciences to mitigate these threats.

- Global Supply Chain Vulnerability: Pharmaceutical manufacturing relies heavily on international sourcing for APIs and intermediates, making it susceptible to geopolitical instability, trade disputes, and logistical challenges.

- Input Cost Volatility: Fluctuations in the cost of raw materials, energy, and transportation directly impact manufacturing expenses, potentially reducing profit margins if not effectively managed.

- Impact on Product Availability and Pricing: Disruptions can lead to production delays, stockouts, and increased costs, which may force Eris Lifesciences to adjust product pricing or face reduced market share due to availability issues.

- Regulatory Hurdles in Sourcing: Changes in import/export regulations or quality standards for raw materials from different countries can add complexity and cost to the procurement process.

Product Patent Expiries and Generic Competition

While Eris Lifesciences operates in the branded generics space, the broader pharmaceutical industry is susceptible to patent expiries of innovator drugs. This phenomenon directly fuels the influx of generic competitors, often leading to significant price erosion for previously high-margin products. For instance, the 2024 and 2025 periods are seeing continued patent cliffs for several blockbuster drugs across various therapeutic areas, intensifying this competitive pressure.

This evolving market dynamic necessitates a proactive approach for companies like Eris. The constant threat of increased generic competition, even for branded generics, means that maintaining market share and profitability requires continuous investment in research and development, strategic product lifecycle management, and agile market adaptation to stay ahead of commoditization.

The impact of patent expiries can be substantial. For example, a drug losing patent protection in 2024 could see its market share rapidly decline as lower-priced generics enter, potentially reducing overall market value by over 80% within a year of generic entry.

Key considerations stemming from this threat include:

- Increased price pressure: Generic entry typically drives down prices, impacting revenue streams even for established branded generics.

- Need for portfolio diversification: Relying heavily on a few products vulnerable to patent expiry increases risk.

- Innovation imperative: Continuous development of new molecules or improved formulations is crucial to offset potential revenue losses.

Indian Pharma: Intense Competition, Rising Costs, Debt & Supply Woes

Intense competition within the Indian pharmaceutical market, valued at approximately $42 billion by fiscal year 2023, exerts significant pricing pressure on companies like Eris Lifesciences, potentially impacting profit margins.

Evolving regulatory landscapes, such as anticipated changes from the EMA in 2025, necessitate substantial compliance investments, adding to operational costs and potentially affecting profitability.

The company faces threats from rising interest expenses and an increasing debt burden; its debt-to-equity ratio was around 0.26 as of March 31, 2024, highlighting the need for careful financial management amidst potential interest rate hikes.

Supply chain disruptions and volatile input costs, exemplified by raw material shortages and price hikes in 2023, pose a significant risk to manufacturing timelines and operational expenses.

SWOT Analysis Data Sources

This SWOT analysis for Eris Lifesciences is built upon a foundation of robust data, including the company's official financial statements, comprehensive market research reports, and insights from industry experts, ensuring a well-rounded and accurate assessment.