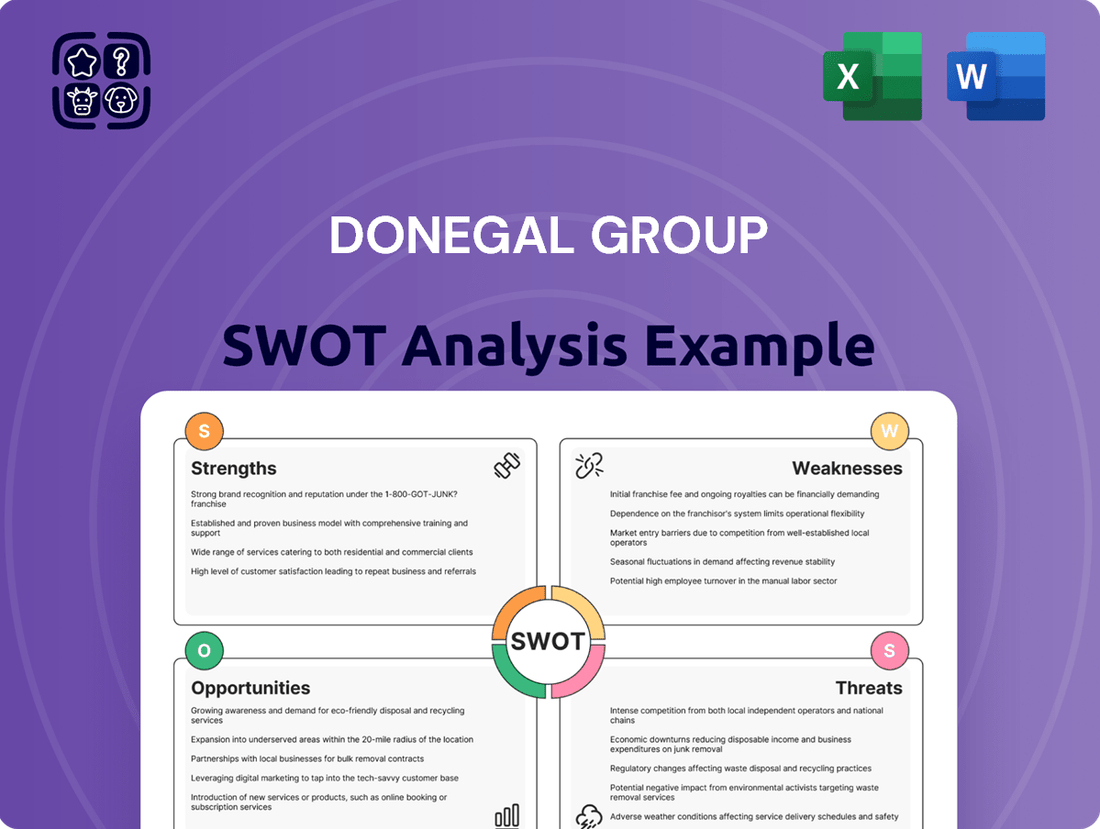

Donegal Group SWOT Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Donegal Group

Elevate Your Analysis with the Complete SWOT Report

The Donegal Group demonstrates notable strengths in its established regional presence and diversified product offerings, providing a solid foundation for its operations. However, understanding the nuances of its competitive landscape and potential regulatory shifts is crucial for navigating its opportunities and threats effectively. Its financial stability and customer loyalty are key assets, but market saturation and evolving consumer preferences present challenges that require strategic adaptation. This overview merely scratches the surface of Donegal Group's strategic positioning.

Want the full story behind Donegal Group's strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Strong Financial Performance and Underwriting Profitability

Donegal Group Inc. showcased remarkable financial strength in early 2025, achieving a net income of $25.2 million for the first quarter. This represents a significant leap of 323.2% compared to the same period in 2024, highlighting robust operational efficiency and strategic execution.

A key driver of this impressive performance was the company's improved combined ratio, which fell to 91.6% in Q1 2025 from 102.4% in Q1 2024. This substantial reduction signals enhanced underwriting profitability, meaning the company is earning more from its insurance policies than it pays out in claims and expenses.

The strategic focus on profit improvement plans, including implementing necessary rate adjustments and divesting from underperforming business lines, has clearly paid dividends. These actions have bolstered the company's financial health and positioned it for sustained growth by focusing on more profitable segments.

Robust Balance Sheet and Credit Rating

Donegal Group boasts a robust balance sheet, underscored by its risk-adjusted capitalization reaching the strongest tier as indicated by Best's Capital Adequacy Ratio (BCAR). This financial strength is further validated by AM Best's affirmation of an A (Excellent) Financial Strength Rating and 'a' (Excellent) Long-Term Issuer Credit Ratings for its insurance entities, all carrying a stable outlook as of mid-2024. Such ratings reflect not only the company's financial stability but also its commitment to a conservative investment strategy, providing a solid foundation for its operations.

The company's financial resilience is significantly enhanced by a sound liquidity position, ensuring it can meet its obligations even in challenging market conditions. Furthermore, Donegal Group employs a comprehensive reinsurance program, which effectively mitigates potential losses and diversifies risk. This strategic approach to financial management, including its strong capital base and prudent risk management practices, positions Donegal Group favorably for sustained performance and growth.

Diversified Product Portfolio and Geographic Reach

Donegal Group's strength lies in its broad product offerings, encompassing personal lines like auto and homeowners insurance, alongside crucial commercial coverages such as business liability. This diversification across various insurance types creates multiple revenue streams, making the company less vulnerable to downturns in any single market segment.

The company's operational footprint is equally robust, spanning 21 states across the Mid-Atlantic, Midwestern, New England, Southern, and Southwestern regions. This wide geographic reach is a significant advantage, as it spreads risk. For instance, a severe weather event or economic slowdown in one area is less likely to cripple the entire business, thanks to the stability provided by operations in other, unaffected regions.

Effective Independent Agency Distribution Channel

Donegal Group's reliance on an independent agency distribution channel, comprising roughly 2,100 agencies, is a significant strength. This broad network facilitates deep market penetration, allowing the company to reach a diverse customer base across various geographic regions. The local presence and expertise of these independent agents foster strong relationships with policyholders, enhancing customer loyalty and retention. This client-centric approach, inherent in the independent agency model, allows for adaptable service and tailored insurance solutions.

The extensive network also provides Donegal Group with valuable market insights and allows for agile responses to local market dynamics. In 2024, the company continued to leverage this channel to drive growth, with independent agencies playing a crucial role in policy sales and renewals. This distribution strategy allows Donegal to benefit from the entrepreneurial spirit and established client relationships of its agency partners.

Key advantages of this distribution model include:

- Extensive Market Reach: Approximately 2,100 independent agencies provide broad geographic coverage.

- Local Expertise and Relationships: Agents possess deep understanding of local markets and strong ties with policyholders.

- Client-Centric Approach: Independent agents offer adaptable service and personalized insurance solutions.

- Cost-Effectiveness: Reduces the need for a large direct sales force, potentially lowering distribution costs.

Strategic Focus on Commercial Lines Growth

Donegal Group is strategically prioritizing expansion within its commercial lines segment, a key strength that underpins its growth trajectory. This focus is not at the expense of its personal lines business, which remains a stable and profitable foundation.

The company's disciplined approach to premium growth in commercial lines is evident in its Q1 2025 performance. Net premiums written in this sector saw a healthy increase of 3.3%.

This growth is further supported by strong customer retention and successful implementation of renewal premium increases, demonstrating Donegal Group's ability to attract and maintain valuable commercial clients.

- Strategic Emphasis: Donegal Group is actively pursuing growth opportunities in commercial insurance lines.

- Financial Performance (Q1 2025): Commercial lines net premiums written grew by 3.3%.

- Key Drivers: The growth is attributed to effective customer retention and successful renewal premium adjustments.

- Disciplined Approach: This targeted premium expansion reflects a well-managed and focused strategy.

Donegal Group's Q1 2025 Net Income Soars 323.2%

Donegal Group's financial performance in early 2025 was exceptionally strong, with Q1 net income reaching $25.2 million, a 323.2% increase year-over-year. This surge was driven by a significant improvement in its combined ratio, which dropped to 91.6% in Q1 2025 from 102.4% in Q1 2024, indicating enhanced underwriting profitability.

The company maintains a robust balance sheet, evidenced by its strong risk-adjusted capitalization and AM Best's affirmation of an A (Excellent) Financial Strength Rating for its insurance entities as of mid-2024, with a stable outlook. This financial stability is further bolstered by sound liquidity and a comprehensive reinsurance program, effectively managing risk and ensuring operational resilience.

Donegal Group's diversified product portfolio, covering personal lines like auto and homeowners, alongside commercial coverages such as business liability, creates multiple revenue streams and reduces vulnerability to sector-specific downturns. This broad offering, combined with a wide geographic footprint across 21 states, spreads risk effectively and contributes to overall stability.

The company's extensive network of approximately 2,100 independent agencies is a major strength, facilitating deep market penetration and fostering strong customer relationships through local expertise and personalized service. This distribution model supports cost-effectiveness and provides valuable market insights, allowing Donegal to respond agilely to local market dynamics.

| Metric | Q1 2024 | Q1 2025 | Change |

|---|---|---|---|

| Net Income | $5.96 million | $25.2 million | +323.2% |

| Combined Ratio | 102.4% | 91.6% | -10.8 pp |

| Commercial Lines Net Premiums Written | N/A | +3.3% | N/A |

What is included in the product

Analyzes Donegal Group’s competitive position through key internal and external factors, highlighting its strengths in regional markets and opportunities for digital expansion while acknowledging potential threats from increased competition and regulatory changes.

Offers a clear, actionable framework for understanding Donegal Group's competitive landscape, easing the burden of complex strategic planning.

Weaknesses

Decline in Personal Lines Net Premiums Written

Despite Donegal Group’s overall premium growth, a significant weakness emerged in its personal lines segment. In the first quarter of 2025, net premiums written for personal lines saw a notable decrease of 9.9% when compared to the same period in 2024. This downturn, attributed to reduced new business volume and deliberate attrition, suggests potential difficulties in winning over new personal lines customers or keeping current ones engaged in today's highly competitive insurance landscape.

Potential Geographic Concentration Risk

Donegal Group's geographic concentration, primarily in the Mid-Atlantic, Midwestern, New England, Southern, and Southwestern US, presents a notable weakness. This focus means that localized risks, particularly those related to severe weather events, can disproportionately affect the company's financial performance. For instance, a significant hurricane in the Southeast or a major blizzard in the Northeast could lead to substantial claims that heavily impact underwriting results, as seen in historical trends where weather-related losses have negatively influenced profitability.

Reliance on Independent Agency Model's Evolution

Donegal Group's reliance on the independent agency model, while a core strength, also poses potential weaknesses. As these agencies navigate the rapidly changing insurance landscape, they face significant pressure to adopt new technologies and meet evolving customer demands. For instance, in 2024, many independent agencies are still grappling with digital transformation, with some reporting that less than 60% have fully integrated advanced customer relationship management (CRM) systems, potentially creating operational bottlenecks.

Operational inefficiencies within some independent agencies, such as outdated legacy systems and manual data processing, can directly impact Donegal Group's distribution effectiveness. This can lead to slower response times and a less seamless digital experience for policyholders, which is increasingly critical in the modern market. Studies from late 2024 indicate that over 40% of consumers expect immediate digital interactions, a benchmark that agencies slow to modernize may struggle to meet.

Modest Stock Price Performance and Analyst Consensus

Donegal Group's stock has experienced modest performance, with a 5-year annualized return of 4.46% as of July 2025. This figure lags behind broader market averages, indicating a less impressive growth trajectory compared to many competitors.

The current analyst consensus for Donegal Group is a 'Hold' rating. Furthermore, the consensus price target stands at $18. This suggests that Wall Street analysts do not foresee substantial immediate gains in the stock's value.

- Modest 5-Year Annualized Return: 4.46% as of July 2025.

- Below Market Average: Performance trails overall market returns.

- Analyst Consensus: Currently rated as 'Hold'.

- Price Target: Consensus stands at $18, indicating limited expected upside.

Elevated Underwriting Leverage and Investment Volatility

While Donegal Group boasts a solid balance sheet, a key weakness identified by AM Best is its elevated underwriting leverage. This suggests a higher reliance on premium income relative to its capital base, which can amplify risk. For instance, in Q1 2025, the company reported net investment losses of $15.5 million, a stark contrast to the $20.1 million in net investment gains seen in the same period of 2024. This swing highlights the inherent volatility in their investment portfolio, directly impacting the predictability of their overall financial performance and potentially straining profitability during market downturns.

This investment volatility can create challenges in managing earnings. The shift from gains to losses in the investment segment means that the company cannot consistently rely on this income stream to offset underwriting results. This makes financial planning more complex, as unexpected investment downturns, like the one observed in early 2025, can significantly affect the bottom line. The underwriting leverage, combined with this investment income variability, creates a dual pressure point for Donegal Group's financial stability.

Performance Challenges and Underwriting Risks Emerge

Donegal Group's personal lines segment exhibited a significant weakness in early 2025, with net premiums written declining by 9.9% year-over-year. This contraction, driven by lower new business and intentional customer attrition, points to potential challenges in customer acquisition and retention within a competitive market. This performance trend suggests that strategies to attract and retain personal lines policyholders may require re-evaluation.

The company's geographic concentration in specific US regions poses a risk, making it susceptible to localized catastrophic events. Severe weather, such as hurricanes or blizzards in its core operating areas, could lead to substantial claims that disproportionately impact financial results. This concentration amplifies the potential for volatility in underwriting performance, especially when weather-related losses are a significant factor.

Donegal Group's reliance on the independent agency distribution model, while a strength, also presents a weakness if these agencies lag in technological adoption. Agencies struggling with digital transformation, such as incomplete CRM integration, could create operational inefficiencies. These bottlenecks can slow down service delivery and impact the customer experience, a critical factor in today's digital-first environment.

Operational inefficiencies within some independent agencies, including outdated systems and manual processes, can hinder Donegal's distribution effectiveness. This can result in slower customer service and a less seamless digital interaction, which is increasingly important as consumers expect immediate digital engagement. Over 40% of consumers in late 2024 expected immediate digital interactions, a benchmark that agencies slow to modernize may not meet.

Donegal Group's stock performance has been modest, with a 5-year annualized return of 4.46% as of July 2025, trailing market averages. This limited growth trajectory is reflected in the current analyst consensus of a 'Hold' rating and a consensus price target of $18, indicating a lack of anticipated significant near-term appreciation.

| Metric | Value (as of July 2025) | Comparison |

| 5-Year Annualized Return | 4.46% | Below Market Average |

| Analyst Consensus | Hold | Neutral Outlook |

| Consensus Price Target | $18 | Limited Upside Expected |

Donegal Group faces a weakness in its elevated underwriting leverage, as noted by AM Best, indicating a higher dependence on premiums relative to its capital. This amplifies risk, especially considering the net investment losses of $15.5 million in Q1 2025, a reversal from $20.1 million in gains the prior year. This volatility in investment income hinders the predictability of financial performance and can strain profitability during market downturns.

Preview Before You Purchase

Donegal Group SWOT Analysis

This preview reflects the real document you'll receive—professional, structured, and ready to use. The Donegal Group SWOT analysis you see here is the identical, complete report you'll download after purchase. We believe in transparency, so what you preview is precisely what you get. This detailed analysis covers strengths, weaknesses, opportunities, and threats specific to the Donegal Group.

Opportunities

Leveraging Technology for Operational Modernization

Donegal Group can capitalize on the insurance industry's digital shift by integrating advanced technologies like AI and automation. This aligns with their strategy to modernize operations, offering a clear path to boosting efficiency and cutting costs. For instance, adopting AI in claims processing can speed up resolution times, a key factor in customer satisfaction.

The company has an opportunity to leverage technology to streamline underwriting processes, making them faster and more accurate. By investing in these digital tools, Donegal Group can reduce manual work, minimize errors, and gain a competitive edge. This modernization directly supports their goal of enhancing overall operational performance and customer service.

Expansion into Emerging Niche Markets and Product Bundling

Donegal Group has a significant opportunity to expand into emerging niche markets driven by evolving customer needs. Younger generations, in particular, are seeking personalized, flexible, and usage-based insurance options. For instance, the increasing prevalence of remote work has fueled a demand for specialized home-based business insurance, a segment Donegal can actively pursue.

By developing tailored niche products, Donegal can better serve these shifting preferences. This strategic move allows the company to address unmet needs and capture new market share. Offering bundled policies can also foster deeper client relationships, increasing customer loyalty and lifetime value.

Targeting emerging segments like cyber liability or pet insurance presents a clear growth avenue. Data from 2024 indicates a substantial increase in cyber insurance claims, highlighting the market's potential. Similarly, the pet insurance market has shown consistent growth, with industry experts projecting continued expansion through 2025.

Strategic Acquisitions and Partnerships in a Consolidating Market

The insurance industry's M&A activity in 2024 and 2025 is seeing significant consolidation, with a keen interest in insurtech firms to drive modernization. Donegal Group, backed by its solid financial standing and an A.M. Best rating, is well-positioned to leverage this trend. The company has a proven track record of growth through strategic acquisitions, which presents a clear opportunity to enhance its technological capabilities, broaden its market reach, and explore new geographical territories.

Capitalizing on Favorable P&C Market Conditions

The U.S. property and casualty (P&C) insurance market is poised for robust growth, with S&P Global projecting net premium growth between 8% and 9% for 2025 and 2026. This expansion is driven by insurers implementing measured rate hikes to counter rising claims costs, a trend that significantly benefits companies like Donegal Group. Its demonstrated improvement in underwriting performance throughout 2024 and into the first quarter of 2025 directly positions it to capitalize on these favorable market dynamics, especially in property insurance segments where rate adjustments are more pronounced.

Donegal Group is well-positioned to leverage the hardening P&C market. The anticipated outperformance of P&C market growth over GDP in 2025 and 2026 presents a significant tailwind. Specifically, the 8%-9% net premium growth forecast by S&P Global highlights an environment where companies with strong underwriting discipline can thrive.

- Strong Market Growth: The U.S. P&C insurance market is expected to grow faster than the overall GDP in 2025-2026.

- Premium Growth Forecast: S&P Global anticipates 8%-9% net premium growth, driven by insurers’ necessary rate increases.

- Donegal's Positioning: Improved underwriting results in 2024 and Q1 2025 enhance Donegal Group's ability to benefit from these trends.

- Property Line Advantage: The company is particularly set to gain from increasing rates in property insurance lines.

Enhancing Agent Support and Digital Tools for Independent Network

The independent agency model is undergoing a significant transformation, necessitating that agents acquire new proficiencies and leverage advanced digital resources to effectively connect with policyholders. Donegal Group has a clear opportunity to bolster its distribution channels by equipping its independent agency network with improved digital tools, comprehensive training programs, and robust support systems.

This strategic enhancement will empower agents to cater to contemporary consumer expectations for intuitive digital interactions, thereby enabling them to maintain a competitive edge against direct insurers and agile insurtech companies. For instance, in 2024, a significant portion of insurance consumers, estimated at over 70%, expressed a preference for digital self-service options, highlighting the critical need for such investments. By facilitating this digital evolution, Donegal Group can foster stronger relationships with its agency partners and, by extension, with the end customer.

- Digital Tool Investment: Allocating resources to develop or acquire user-friendly digital platforms for quoting, policy management, and customer service.

- Agent Training Programs: Implementing specialized training modules focused on digital literacy, CRM usage, and virtual client engagement techniques.

- Support Infrastructure: Establishing dedicated support teams to assist agents with digital tool integration and troubleshooting.

- Competitive Advantage: Enabling agents to offer seamless digital experiences that rival those provided by direct-to-consumer models.

Unlocking Insurance Growth: Niche, M&A, and Digital Strategies

Donegal Group can leverage the increasing demand for specialized insurance products in niche markets. The company's ability to develop tailored offerings, such as cyber liability or pet insurance, aligns with evolving consumer needs and presents a significant growth opportunity. Data from 2024 shows a surge in cyber insurance claims, indicating strong market potential, while the pet insurance sector continues its steady expansion through 2025.

The ongoing consolidation within the insurance sector, particularly the acquisition of insurtech firms, offers Donegal Group a strategic path for growth. With its solid financial footing and strong ratings, the company is well-positioned to engage in mergers and acquisitions to enhance its technological capabilities and expand its market presence. This strategy has proven effective for Donegal in the past, bolstering its competitive standing.

Donegal Group is strategically positioned to benefit from the hardening U.S. property and casualty (P&C) insurance market. S&P Global projects robust net premium growth of 8%-9% for 2025 and 2026, driven by necessary rate increases. Donegal's improved underwriting performance in 2024 and Q1 2025 allows it to capitalize on this favorable environment, especially in property lines where rate adjustments are more pronounced.

The company can enhance its distribution network by equipping its independent agents with advanced digital tools and training. This initiative will enable agents to meet customer preferences for digital self-service, a trend strongly supported by over 70% of consumers in 2024 preferring digital interactions. Such investments strengthen agency relationships and improve customer engagement.

Threats

Intense Competition from Larger Carriers and Insurtechs

Donegal Group faces significant pressure from larger national insurers who benefit from substantial capital reserves and established brand recognition, allowing for aggressive pricing strategies and broader market reach. For instance, major players often possess the financial muscle to invest heavily in advanced analytics and digital platforms, creating seamless customer experiences that are difficult for smaller carriers to replicate.

The rise of insurtech companies presents another formidable challenge, as these agile firms are disrupting traditional insurance models with technology-driven solutions, often focusing on niche markets or offering highly personalized products. These competitors can rapidly adapt to changing consumer demands, utilizing data analytics to improve underwriting accuracy and streamline claims processing, potentially eroding market share from established players like Donegal Group.

Larger competitors' economies of scale translate into lower operating costs per policy, enabling them to offer more competitive premiums and invest more in customer acquisition and retention efforts. This can create a pricing disadvantage for Donegal Group, impacting its ability to attract and maintain policyholders in a price-sensitive market.

Increasing Frequency and Severity of Catastrophic Events

The escalating frequency and intensity of climate-related natural disasters, including wildfires, hurricanes, and floods, present a significant hurdle for property insurers like Donegal Group. These events are not just isolated incidents; they represent a growing trend that directly impacts underwriting and claims.

While Donegal Group maintains a robust reinsurance strategy, the sheer scale of losses from increasingly severe catastrophes can still strain its financial capacity and test its existing catastrophe budgets. This can lead to an uptick in claims expenses and introduce greater volatility into the company's underwriting performance, affecting profitability.

For instance, the insured losses from natural catastrophes in the United States alone were estimated to be in the tens of billions of dollars in 2023, underscoring the financial pressure such events exert. This trend is projected to continue, making risk management and capital allocation crucial for insurers navigating this evolving landscape.

Inflationary Pressures and Rising Claims Costs

Ongoing inflationary pressures, coupled with persistent supply chain disruptions and labor shortages, are significantly inflating the costs associated with repairing and replacing vehicles and property. This trend directly contributes to underwriting losses across the property and casualty (P&C) insurance sector. For instance, in 2024, the U.S. Bureau of Labor Statistics reported that the Consumer Price Index for motor vehicle maintenance and parts increased by 9.5% year-over-year, impacting insurers' repair expenses.

Furthermore, social inflation, a phenomenon characterized by increasingly large jury verdicts and escalating litigation expenses, is severely exacerbating claims severity, particularly in casualty and liability lines of business. This dynamic directly erodes profitability for insurers like Donegal Group. Data from the U.S. Chamber Institute for Legal Reform indicated that the average jury award in U.S. tort litigation has seen a substantial uptick, placing further strain on insurance reserves and underwriting results.

Regulatory Changes and Compliance Burden

Donegal Group, like all insurers, faces the persistent threat of regulatory changes. For instance, as of early 2024, states continue to refine data privacy laws and cybersecurity mandates, adding layers of complexity to operations. Navigating these evolving requirements across its multiple operating states, including Pennsylvania and New York, demands significant investment in compliance infrastructure and personnel.

The burden of compliance can directly impact profitability by increasing operational costs. Donegal Group’s ability to adapt quickly to new regulations, such as potential changes in capital requirements or consumer protection rules, is crucial for maintaining its financial health and market position. Failure to comply can result in substantial fines and reputational damage.

Key areas of regulatory focus impacting Donegal Group include:

- Data Security and Privacy: Adherence to state-specific data breach notification laws and evolving privacy regulations.

- Capital Adequacy: Meeting varying state solvency requirements and risk-based capital standards.

- Market Conduct: Ensuring fair practices in underwriting, claims handling, and policyholder communications.

- Environmental, Social, and Governance (ESG): Growing pressure to incorporate ESG principles into business practices and reporting.

Evolving Customer Expectations and Digital Disruption

Modern consumers increasingly expect instant, digital-first interactions, demanding 24/7 access to information and support. This shift puts pressure on Donegal Group and its agency partners to keep pace with technological advancements.

Failure to continuously adapt and integrate advanced digital capabilities could lead to a loss of market relevance and customer loyalty. Competitors who are more agile in adopting new technologies may capture a larger share of the market.

For instance, customer satisfaction scores in the insurance industry are heavily influenced by digital engagement channels. A recent survey indicated that over 70% of consumers prefer digital self-service options for routine insurance tasks.

- Digital Expectations: Consumers desire seamless, fast, and digital-first experiences.

- 24/7 Access: Instant information and round-the-clock customer service are paramount.

- Competitive Landscape: Technologically advanced competitors pose a significant threat to market share.

- Customer Loyalty: Adapting to evolving expectations is crucial for retaining customer loyalty.

Insurance Industry Confronts Competition, Escalating Costs, and Climate Disasters

Donegal Group faces intense competition from larger national insurers with greater financial resources and brand recognition, enabling them to offer more competitive pricing and invest in advanced digital platforms. The rapid growth of insurtech companies, leveraging technology for personalized products and streamlined operations, also poses a significant threat by potentially eroding market share. Furthermore, escalating costs due to inflation, supply chain issues, and social inflation, particularly in claims severity, directly impact profitability. The increasing frequency and severity of climate-related natural disasters also strain financial capacity and introduce volatility, as evidenced by billions in insured losses in 2023.

| Threat Category | Specific Challenge | Impact on Donegal Group | Example/Data Point (2023-2024) |

|---|---|---|---|

| Competitive Landscape | Larger Insurers' Scale & Resources | Pricing disadvantage, difficulty matching digital investments | National insurers' ability to absorb higher marketing costs. |

| Market Disruption | Insurtech Innovation | Erosion of market share, pressure to adopt new technologies | Agile insurtechs offering niche, data-driven products. |

| Economic Factors | Inflation & Supply Chain Issues | Increased claims costs (repair/replacement) | CPI for motor vehicle maintenance & parts up 9.5% (U.S. BLS, 2024). |

| Economic Factors | Social Inflation | Exacerbated claims severity, higher litigation expenses | Rising average jury awards in U.S. tort litigation. |

| Environmental Factors | Climate-Related Disasters | Strain on financial capacity, increased claims volatility | Tens of billions in insured losses from U.S. natural catastrophes (2023). |

| Regulatory Environment | Evolving Compliance Demands | Increased operational costs, risk of fines/reputational damage | New data privacy and cybersecurity mandates impacting compliance spending. |

| Customer Expectations | Digital-First Demands | Risk of losing market relevance and customer loyalty | Over 70% of consumers prefer digital self-service (industry survey). |

SWOT Analysis Data Sources

This SWOT analysis is built using a comprehensive array of data, including Donegal Group's official financial statements, up-to-date market research reports, and insights from industry experts and analysts.