Christie Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Christie Group

Go Beyond the Preview—Access the Full Strategic Report

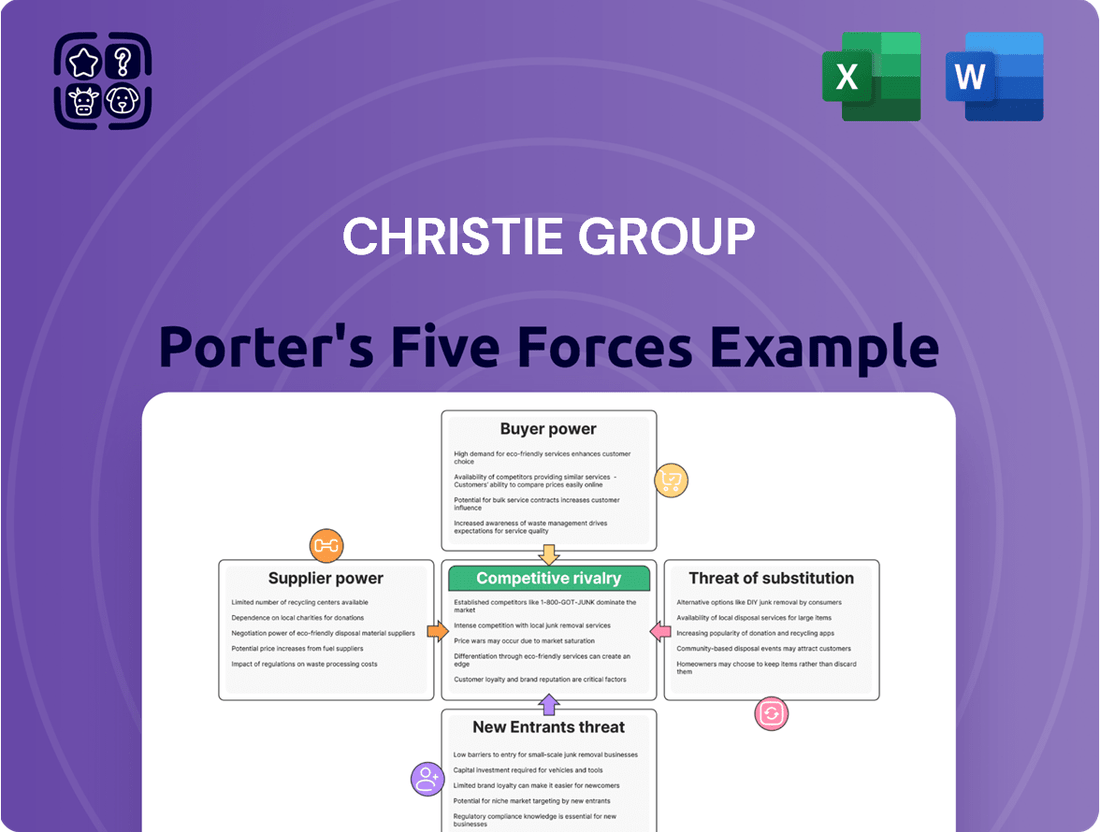

Christie Group operates within a dynamic market, facing pressures from rivals, potential new entrants, and the bargaining power of both buyers and suppliers. Understanding these forces is crucial for navigating its competitive landscape.

The complete report reveals the real forces shaping Christie Group’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Specialized Talent

Christie Group's reliance on specialized talent in areas like hospitality and healthcare valuation, agency, and consultancy means that professionals with unique industry knowledge hold considerable sway. The limited availability of these highly skilled individuals, particularly those with established client relationships, can significantly enhance their bargaining power.

Proprietary Software and Systems

Christie Group's reliance on proprietary software and systems from third-party vendors can significantly impact supplier bargaining power. If these suppliers provide highly specialized or integrated solutions, such as core accounting platforms or critical operational software, Christie Group faces substantial switching costs. These costs can include data migration, system re-integration, and employee retraining, effectively locking Christie Group into existing relationships.

Data and Market Intelligence Providers

The bargaining power of suppliers for data and market intelligence providers, crucial for Christie Group's valuation and consultancy, is significant. Companies like Bloomberg and Refinitiv, which offer extensive financial data, can command high prices due to the proprietary nature and comprehensiveness of their information. In 2023, the global market for financial data and analytics was valued at approximately $30 billion, indicating the substantial revenue streams these suppliers generate and their leverage.

Regulatory and Compliance Expertise

Christie Group's reliance on specialized regulatory and compliance expertise, particularly within sectors like healthcare and financial services, grants significant bargaining power to external consultants possessing niche knowledge. The critical nature of adhering to stringent regulations, with substantial penalties for non-compliance, amplifies this power. For instance, in 2024, the financial services sector alone faced an estimated $2.5 trillion in regulatory costs globally, highlighting the immense value of compliance proficiency.

The scarcity of highly specialized legal and compliance professionals capable of navigating complex frameworks in these sectors means fewer providers can offer these essential services. This limited supply, coupled with high demand driven by evolving regulatory landscapes, allows these consultants to command premium fees. For example, a 2024 survey indicated that demand for cybersecurity and data privacy compliance experts in the financial sector outstripped supply by over 30%.

- High Demand for Niche Expertise: Sectors like healthcare and financial services require specialized regulatory knowledge, creating a strong demand for consultants with this proficiency.

- Risk of Non-Compliance: The potential for severe financial penalties and reputational damage due to regulatory breaches empowers consultants who can ensure adherence.

- Limited Supply of Specialists: The availability of consultants with deep, sector-specific compliance experience is often constrained, increasing their bargaining leverage.

- Escalating Regulatory Costs: With global regulatory costs in finance reaching trillions annually, the value proposition of effective compliance guidance is substantial.

Financial Lenders and Insurers

The bargaining power of financial lenders and insurers is a crucial element in Christie Group's operations. While Christie offers its own finance and insurance services, it still relies on external institutions for its own funding and for facilitating client transactions. In 2024, with interest rates remaining a key consideration, the terms offered by these external providers can significantly impact Christie's cost of capital and its ability to structure competitive deals for clients.

When external financial institutions have significant leverage, perhaps due to a concentrated market or limited lending capacity, they can impose stricter terms. This could translate to higher interest rates or more stringent collateral requirements, directly affecting Christie Group's profitability and the attractiveness of its client solutions. For instance, if a major bank tightens lending criteria in mid-2024, Christie might face higher costs when seeking credit lines for its own expansion or when arranging finance for its clients.

- Limited External Options: In scenarios where the number of available lenders or insurers is scarce, their ability to dictate terms increases.

- Market Conditions: During periods of economic uncertainty or tight credit markets, lenders and insurers often gain more bargaining power.

- Christie's Reliance: Christie Group's need for external funding or client financing arrangements makes it susceptible to these terms.

- Impact on Client Offerings: The cost and availability of external finance directly influence the competitiveness of Christie's own financial product offerings.

Niche Suppliers Wield Significant Power

Christie Group's dependence on specialized talent, proprietary software, and essential data providers grants significant leverage to its suppliers. The scarcity of niche expertise, particularly in regulated sectors like healthcare and finance, allows these providers to command premium pricing. For example, in 2024, the demand for cybersecurity compliance experts in finance exceeded supply by over 30%, underscoring the power of these specialized suppliers.

The bargaining power of suppliers is amplified by Christie Group's substantial switching costs for critical systems and the high value of comprehensive market intelligence. Providers like Bloomberg, whose financial data market was valued at approximately $30 billion in 2023, leverage the proprietary nature of their information. Furthermore, the escalating global regulatory costs, estimated at $2.5 trillion for the financial services sector in 2024, highlight the critical need for and therefore the power of compliance expertise suppliers.

| Supplier Type | Key Factor | Impact on Christie Group | 2023/2024 Data Point |

|---|---|---|---|

| Specialized Talent | Scarcity of niche skills | Higher recruitment and retention costs | 30%+ supply/demand gap for compliance experts |

| Software Vendors | High switching costs | Limited flexibility, potential for price increases | Proprietary systems lock-in |

| Data Providers | Proprietary & comprehensive data | Significant expenditure on essential intelligence | $30 billion global financial data market |

| Compliance Consultants | Critical regulatory knowledge | Premium fees due to risk of non-compliance | $2.5 trillion global financial regulatory costs |

What is included in the product

This analysis dissects the competitive forces impacting Christie Group, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the presence of substitutes.

Quickly identify and address competitive threats with a pre-built, customizable Porter's Five Forces template.

Customers Bargaining Power

Fragmented Customer Base

Christie Group's customer base is quite varied, encompassing everyone from individual business owners to substantial corporate organizations across different industries. This wide spread means that no single customer usually represents a large chunk of the company's income, which naturally weakens the bargaining power of any one client.

While the overall fragmentation dilutes individual customer leverage, it's important to note that larger corporate clients may still possess more significant bargaining power due to their scale and potential impact on Christie Group's revenue streams. For instance, in 2023, Christie Group reported that its largest customer accounted for less than 5% of its total revenue, underscoring the general lack of concentration.

High Switching Costs for Integrated Services

For clients deeply embedded with Christie Group's integrated services, like their combined inventory management and valuation offerings, the cost and effort involved in switching to a competitor can be substantial. This integration, especially with their proprietary software and data systems, creates significant barriers to exit.

Migrating extensive client data, retraining personnel on entirely new platforms, and re-establishing workflows can represent a considerable investment of both time and capital. For instance, the average cost for businesses to switch cloud-based ERP systems can range from $10,000 to $250,000 or more, depending on complexity, making such a move a significant decision. This inherent stickiness in Christie Group's service ecosystem effectively dampens the bargaining power of their customers.

Importance of Reputation and Track Record

Christie Group's enduring legacy, originating in 1896, coupled with its proven performance in niche sectors, significantly bolsters its appeal to clients. This history demonstrates a consistent ability to deliver value and expertise, which is a powerful differentiator.

Clients in specialized fields, particularly those involved in substantial deals such as business acquisitions or intricate property appraisals, often prioritize dependability and specialized knowledge over minor cost variations. This focus on quality and proven results inherently diminishes their inclination to negotiate aggressively on price or seek alternative providers, thereby limiting their bargaining power.

Availability of Alternative Service Providers

The bargaining power of Christie Group's customers is influenced by the availability of alternative service providers. While Christie Group specializes in areas like business brokerage and professional practice sales, clients can explore smaller, niche consultancies or independent brokers who might offer more focused or potentially lower-cost solutions for specific needs. This competitive landscape, even with specialized services, means customers have options, which can translate into leverage during negotiations.

For instance, in the business brokerage market, the number of active brokers can vary significantly by region and industry sector. In 2024, reports indicated a robust market for business sales, with a growing number of independent brokers and online platforms facilitating transactions, potentially increasing customer options. This means a business owner looking to sell their practice might compare Christie Group's offerings against several other specialized intermediaries, impacting their ability to negotiate fees or terms.

Customers also possess the option of developing in-house capabilities for certain tasks that Christie Group might provide. For example, larger organizations could choose to handle internal due diligence or market analysis themselves rather than outsourcing. This internal capacity, even if not a perfect substitute for Christie Group's expertise, serves as a benchmark and a potential negotiation point for clients seeking external services.

- Alternative Providers: Customers can choose from niche consultancies, independent brokers, or even manage services internally.

- Negotiation Leverage: The presence of alternatives empowers customers to negotiate pricing and service agreements with Christie Group.

- Market Dynamics (2024): A strong market for business sales in 2024 saw an increase in independent brokers and online platforms, expanding customer choices.

- In-house Capabilities: Larger clients may opt for internal management of services, creating a comparative baseline for outsourced solutions.

Economic Conditions Impacting Client Budgets

The economic health of sectors like hospitality, leisure, healthcare, and retail significantly shapes client budgets for professional services. During economic downturns, businesses in these areas often cut back on non-essential spending, directly impacting demand for services. For instance, a slowdown in the hospitality sector might lead hotels to reduce their expenditure on consulting or IT upgrades.

When economic conditions are tough, clients gain leverage. They are more likely to negotiate lower fees for professional services or postpone projects altogether, thereby increasing their bargaining power. This pressure can force service providers to become more competitive on pricing.

- Hospitality Sector Performance: In 2024, the UK hospitality sector experienced a mixed performance, with some segments showing resilience while others faced significant cost pressures. For example, rising energy costs and labor shortages continued to impact profitability, potentially leading businesses to scrutinize service provider fees more closely.

- Retail Spending Trends: Consumer spending in the UK retail sector in early 2024 indicated cautious optimism but also highlighted a sensitivity to economic factors like inflation. This cautious spending environment translates to businesses in retail being more budget-conscious when engaging external professional services.

- Leisure Industry Outlook: The leisure industry, while often resilient, can also be affected by discretionary income. Economic uncertainty in 2024 meant that some leisure operators might have scaled back on investments in new services or operational improvements, thus increasing their negotiating stance with service providers.

- Healthcare Sector Budgets: Public and private healthcare providers in 2024 continued to operate under significant financial constraints. This often leads to a more stringent approach to budgeting for external consultancy or technology services, amplifying the bargaining power of these clients.

Clients Hold Moderate Power Amidst Market Alternatives

Christie Group's customers exhibit moderate bargaining power, primarily due to the availability of alternative providers and their ability to develop in-house capabilities. While Christie Group offers specialized services, smaller niche consultancies and independent brokers provide viable alternatives, especially in 2024's robust business sales market which saw increased competition from online platforms. This competitive landscape allows clients to negotiate terms more effectively.

| Factor | Impact on Bargaining Power | 2024 Context |

|---|---|---|

| Alternative Providers | Increases bargaining power | Growing number of niche brokers and online platforms |

| In-house Capabilities | Increases bargaining power | Larger organizations can perform some services internally |

| Switching Costs | Decreases bargaining power | High for integrated proprietary systems |

| Customer Concentration | Decreases bargaining power | Largest customer accounted for <5% of revenue in 2023 |

Preview the Actual Deliverable

Christie Group Porter's Five Forces Analysis

The preview you see is the exact Christie Group Porter's Five Forces Analysis you will receive immediately after purchase, offering a comprehensive examination of industry competitive forces. This document is fully formatted and ready for your immediate use, providing actionable insights into the competitive landscape. You're looking at the actual, professionally written analysis, ensuring no surprises or placeholder content.

Rivalry Among Competitors

Diverse Range of Competitors

Christie Group encounters a broad spectrum of competitors, ranging from general business brokers to niche consultancies focusing on specific industries. This includes large accounting firms with dedicated advisory divisions and even technology firms providing software that overlaps with Christie's offerings.

This multifaceted competitive environment means rivalry is particularly intense. Different types of firms often target distinct market segments, but their combined presence creates pressure across Christie Group's business lines. For instance, in the hospitality sector, specialized brokers compete directly, while in broader business sales, larger advisory firms may also vie for mandates.

Market Fragmentation and Niche Specialization

While Christie Group focuses on specific sectors like licensed property and professional services, the markets they operate in can be quite fragmented. This means there are numerous smaller, regional competitors who possess intimate local knowledge, often leading to intense competition for particular deals, especially those that are less complex.

For instance, in the UK, the market for business broking and advisory services, which Christie Group is part of, includes a significant number of independent firms. In 2024, it's estimated that there are over 500 active business brokers in the UK, many of whom operate on a regional basis and can offer highly competitive terms for smaller or more localized transactions, directly challenging Christie Group's market share in those segments.

Reputation and Brand Strength

Christie Group's extensive history and deeply ingrained brand name provide a formidable competitive edge, fostering trust and recognition among clients. This established reputation is a key differentiator in a crowded market.

However, the competitive landscape is intensified by other firms that have cultivated strong reputations within specific niche sectors or possess significant regional brand loyalty. These competitors leverage their own established client relationships and local market understanding to challenge Christie Group's market share.

Service Differentiation and Innovation

Competitive rivalry in the professional services sector, including for Christie Group, is significantly fueled by service differentiation and ongoing innovation. Companies vie for market share by offering unique value propositions, whether that's through deeper market intelligence, cutting-edge technology, or a more holistic suite of services. Christie Group's strategic integration of professional and financial services with proprietary software solutions serves as a prime example of such differentiation.

Competitors are not standing still; they are actively investing in innovation to capture market share. For instance, many firms are developing AI-powered analytics tools to provide clients with more predictive insights, a move that could challenge Christie Group's current technological edge. The ability to consistently introduce novel services or enhance existing ones remains a critical factor in maintaining a competitive advantage.

- Service Differentiation: Christie Group differentiates by combining professional advice with financial services and software, a model that appeals to clients seeking integrated solutions.

- Innovation as a Driver: Competitors are actively innovating, particularly in areas like AI-driven analytics and digital client portals, to enhance their service offerings and attract new business.

- Market Insight: Superior market insight, often gained through proprietary data analysis and research, is a key differentiator that allows firms to offer more targeted and effective advice.

- Technological Advancement: The adoption and development of innovative technology solutions, such as advanced data visualization or predictive modeling tools, are crucial for staying ahead in a competitive landscape.

Economic Sensitivity of Target Sectors

The hospitality, leisure, healthcare, and retail sectors, key areas for Christie Group, are notably sensitive to economic cycles. When the economy slows, consumer spending in these areas typically decreases, leading to reduced transaction volumes.

This economic sensitivity directly impacts competitive rivalry. As the overall market shrinks, businesses within these sectors often intensify their efforts to capture a larger share of the remaining demand. This can manifest as price wars or increased marketing spend, putting pressure on fees and profit margins for service providers like Christie Group.

- Economic Downturns: In 2024, global economic growth projections have moderated, with many developed economies facing slower expansion, impacting discretionary spending in leisure and hospitality.

- Reduced Transaction Volumes: A decline in consumer confidence and disposable income directly translates to fewer property transactions or business sales within Christie Group's target sectors.

- Fee Pressure: With fewer deals available, firms like Christie Group may face increased competition for mandates, potentially leading to downward pressure on commission rates and fees.

- Sectoral Impact: For instance, a slowdown in retail sales can reduce the number of businesses looking to sell or lease premises, directly affecting the volume of brokerage activity.

Market Dynamics: Facing Diverse Competitors and Economic Shifts

Christie Group faces intense rivalry from a diverse range of competitors, including specialized brokers, large advisory firms, and technology companies. This competition is amplified by the fragmented nature of many of Christie Group's target markets, where numerous smaller, regional players offer localized expertise and competitive pricing.

The drive for market share is fueled by service differentiation and continuous innovation, with firms actively developing advanced analytics and digital solutions. For example, the UK business broking market alone saw over 500 active brokers in 2024, many of whom compete aggressively on price for smaller transactions.

Economic downturns, particularly in sectors like hospitality and retail, exacerbate competitive pressures by reducing transaction volumes and leading to increased competition for remaining deals. This often results in downward pressure on fees and profit margins for service providers.

| Competitor Type | Key Differentiators | Impact on Christie Group |

|---|---|---|

| Specialized Brokers | Niche market expertise, local knowledge | Direct competition for specific deals, potential for price undercutting |

| Large Advisory Firms | Broader service offering, established brand reputation | Competition for larger mandates, potential to leverage cross-selling opportunities |

| Technology Firms | Software solutions, data analytics | Threat of disintermediation, need for technological integration |

| Regional Competitors | Local relationships, cost-effectiveness | Pressure on smaller transactions, erosion of market share in specific geographies |

SSubstitutes Threaten

In-house Capabilities

For substantial clients, building internal departments for valuation, agency, or inventory oversight presents a direct alternative to engaging Christie Group. This strategy, though demanding considerable upfront capital, becomes a practical consideration for enterprises with consistent, large-volume requirements, especially for recurring operational tasks.

Generalist Business Consultancies

Clients might choose generalist business consultancies or broader real estate advisory firms, even if these lack Christie Group's specialized focus. These alternatives can present a more budget-friendly choice for simpler advisory needs.

For instance, in 2024, the global management consulting market was valued at approximately $300 billion, with a significant portion catering to general business needs. This indicates a substantial pool of competitors offering a wide range of services, potentially at lower price points for clients not requiring niche expertise.

Online Platforms and DIY Tools

The proliferation of online platforms and do-it-yourself (DIY) valuation tools presents a significant threat of substitutes for Christie Group. These digital solutions, especially those catering to smaller businesses or straightforward transactions, can offer a more budget-friendly and readily available alternative to traditional brokerage services. For instance, as of early 2024, numerous online business marketplaces and valuation software providers have seen substantial user growth, indicating a growing comfort level with self-service options.

While these platforms may not replicate the nuanced expertise and established networks that Christie Group provides, their accessibility and lower price point are compelling. Many of these DIY tools leverage automated valuation models and broad market data, making them attractive for businesses with simpler asset structures or those prioritizing cost-effectiveness over bespoke advisory. The increasing sophistication of these online offerings means they can increasingly handle a wider range of business types, thereby broadening their substitutive impact.

Direct Sales or Acquisitions

Clients may consider direct sales or acquisitions, bypassing intermediaries like Christie & Co, especially if they possess strong existing networks or aim to reduce brokerage costs. This approach, however, often introduces significant risks and operational complexities. For instance, in 2024, the average time to sell a business directly without professional representation was estimated to be 30% longer than with a broker, with a reported 15% higher chance of a deal falling through due to valuation miscalculations or legal oversights.

The threat of substitutes in business sales, particularly through direct channels, is influenced by several factors:

- Reduced Transaction Costs: Businesses might attempt DIY sales to avoid agency commissions, which can range from 5% to 10% of the sale price for many mid-market transactions.

- Control Over the Process: Some owners prefer to manage the sale directly to maintain control over negotiations and buyer interactions.

- Market Volatility: In rapidly appreciating markets, some sellers may feel confident enough to market and sell their businesses independently, believing they can achieve optimal terms.

- Availability of Online Platforms: The rise of business-for-sale listing websites and digital marketplaces offers alternative avenues for direct promotion, though these often lack the specialized advisory services provided by established brokers.

Alternative Financing Channels

Clients looking for financing might bypass intermediaries like Christie Finance by directly approaching traditional banks or exploring private equity and venture capital firms. This direct access to capital markets offers an alternative route to securing funds.

The increasing availability and accessibility of diverse funding sources, such as crowdfunding platforms and peer-to-peer lending, reduce the necessity for specialized finance brokers. For instance, in 2024, the global alternative lending market was projected to reach over $2 trillion, showcasing a significant shift in financing avenues.

- Direct Bank Lending: Businesses can directly apply for loans from banks, potentially securing better terms without a broker's commission.

- Private Equity & Venture Capital: Companies can pitch directly to PE and VC firms, bypassing the need for a broker to facilitate introductions or negotiations.

- Crowdfunding & P2P Lending: Online platforms allow direct engagement with investors or lenders, offering alternative financing channels that bypass traditional brokerage services.

Internal, Generalist, Digital: Your Service Substitutes

Clients may opt for internal teams to handle valuation, agency, or inventory management, especially those with consistent, high-volume needs. This internal approach, while capital intensive, offers direct control over recurring operational tasks, bypassing the need for external specialists like Christie Group.

Generalist consulting firms and broader real estate advisors represent another substitute, offering a wider service array at potentially lower costs for less specialized client requirements. The global management consulting market, valued at approximately $300 billion in 2024, highlights the breadth of these generalist competitors.

Online platforms and DIY valuation tools are increasingly accessible substitutes. These digital solutions, popular for smaller businesses or simpler transactions, offer cost-effectiveness and immediate availability, though they may lack Christie Group's nuanced expertise and established networks.

| Substitute Type | Key Characteristics | 2024 Market Context/Data |

| Internal Departments | Direct control, capital intensive, suitable for high-volume needs | N/A (client-specific decision) |

| Generalist Consultants | Broader services, potentially lower cost for simple needs | Global Management Consulting Market: ~$300 billion |

| Online/DIY Tools | Cost-effective, accessible, may lack specialized expertise | Growing user adoption in online marketplaces and valuation software |

Entrants Threaten

High Barriers to Entry in Specialized Sectors

Entering specialized professional business services, particularly in sectors like healthcare and hospitality, presents substantial hurdles for newcomers. Success demands deep industry expertise, navigating complex regulatory landscapes, and cultivating a robust network of established relationships, all of which act as significant barriers.

Reputation and Trust as Entry Barriers

Christie Group's decades-long history has cultivated a robust reputation and deep-seated trust among its clientele, acting as a significant deterrent to newcomers. This established credibility is not easily replicated, requiring substantial time and financial resources for any potential entrant to build a comparable level of assurance with customers.

Capital Requirements for Comprehensive Services

The capital needed to offer a complete range of services, such as valuation, brokerage, financing, and specialized software, acts as a significant barrier. Christie Group's investment in its global network of offices, skilled personnel, and advanced technological platforms represents a considerable upfront cost. For instance, establishing a presence in key markets and developing proprietary software solutions can easily run into millions of dollars, deterring many smaller or less capitalized potential competitors.

Regulatory and Licensing Hurdles

Operating within financial services, such as Christie Finance and Christie Insurance, and specific consultancy sectors necessitates adherence to a stringent web of regulations and licensing. These requirements significantly increase the capital investment and operational complexity for any new entity aiming to enter these markets.

For instance, in the UK, financial advice firms must be authorized by the Financial Conduct Authority (FCA), a process that involves demonstrating robust compliance frameworks and adequate financial resources. As of 2024, the FCA's authorization process can take several months, and firms are subject to ongoing reporting and capital adequacy rules, effectively raising the barrier to entry.

These regulatory and licensing barriers serve as a substantial deterrent to potential new entrants.

- FCA Authorization: New financial services firms require FCA approval, a lengthy and resource-intensive process.

- Capital Requirements: Firms must meet minimum capital adequacy standards, which can be substantial.

- Compliance Costs: Ongoing adherence to regulations incurs significant operational expenses for training, systems, and reporting.

- Licensing Fees: Obtaining and maintaining necessary licenses often involves recurring fees.

Talent Acquisition and Retention

The threat of new entrants in the context of talent acquisition and retention for Christie Group is significant. Attracting and keeping experienced professionals with specialized sector knowledge is paramount. New competitors would find it difficult to recruit such talent, as established companies like Christie Group typically boast strong employee loyalty and well-developed talent acquisition strategies.

For instance, in 2024, the average tenure for employees in the professional services sector, where Christie Group operates, remained robust, indicating a challenge for newcomers to poach experienced staff. Companies with a strong employer brand and competitive compensation packages, like Christie Group, often have an advantage in securing top-tier talent.

- Talent Scarcity: Key sectors often face a shortage of highly skilled professionals, making recruitment a competitive battleground.

- High Onboarding Costs: New entrants must invest heavily in training and development to bring new hires up to speed, a cost already absorbed by established firms.

- Retention as a Barrier: Christie Group's success in retaining its workforce means fewer experienced individuals are available for new companies to hire.

Moderate Threat: High Barriers Deter New Market Entrants

The threat of new entrants for Christie Group is moderate, primarily due to high capital requirements and established brand loyalty. While specialized knowledge is crucial, the significant investment needed for a comprehensive service offering, including technology and global networks, deters many potential competitors. Regulatory hurdles in financial services further solidify this barrier, demanding substantial compliance infrastructure and capital.

| Barrier Type | Description | Impact on New Entrants | Example Data (2024) |

|---|---|---|---|

| Capital Requirements | Investment in global offices, skilled personnel, and advanced technology platforms. | High; discourages less capitalized entrants. | Establishing a full-service presence can cost millions. |

| Brand Loyalty & Reputation | Christie Group's decades of experience build trust and credibility. | High; difficult for newcomers to replicate. | Long client relationships are hard to break. |

| Regulatory Compliance | Adherence to stringent financial services regulations (e.g., FCA authorization). | High; increases complexity and cost. | FCA authorization can take months and requires significant resources. |

| Talent Acquisition | Attracting and retaining experienced professionals with specialized sector knowledge. | Moderate; established firms have an advantage. | Average employee tenure in professional services remains robust, indicating retention challenges for newcomers. |

Porter's Five Forces Analysis Data Sources

Our Christie Group Porter's Five Forces analysis is built upon a robust foundation of data, incorporating insights from industry-specific market research reports, financial statements of key players, and publicly available business intelligence platforms.