Butterfield Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Butterfield

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

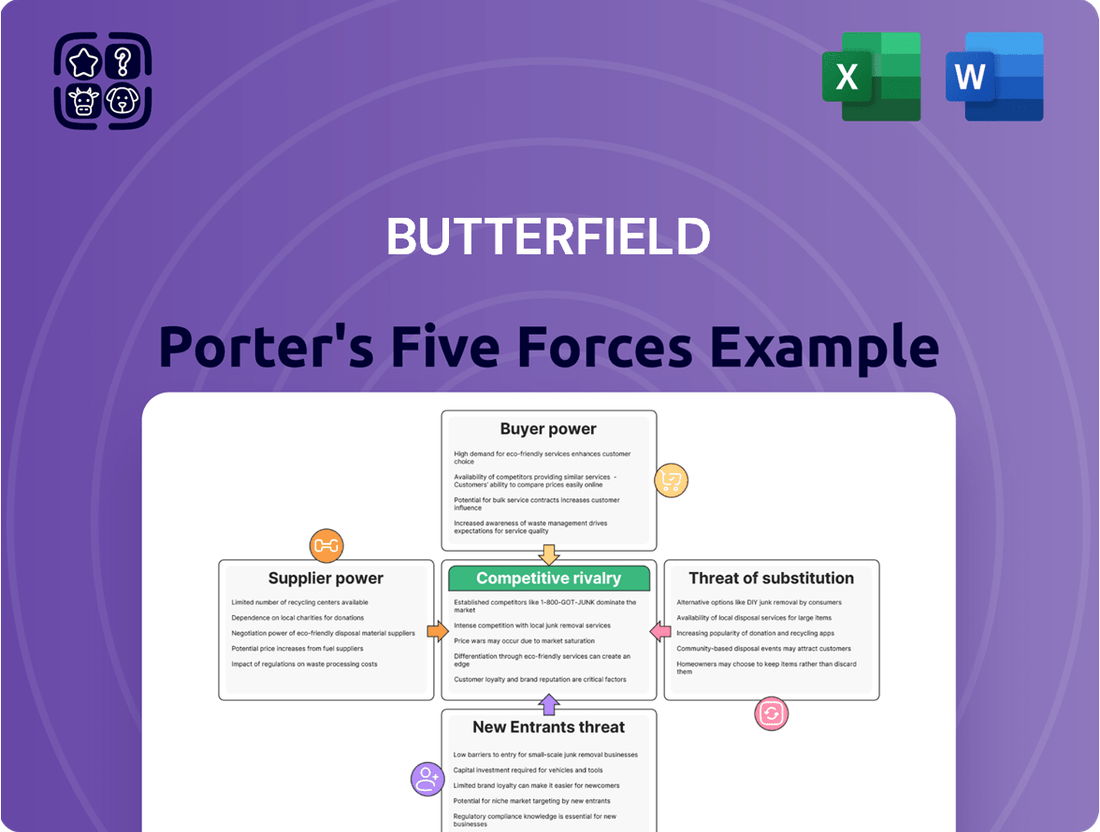

Butterfield's competitive landscape is shaped by five key forces: the bargaining power of buyers, the threat of new entrants, the threat of substitute products or services, the bargaining power of suppliers, and the intensity of rivalry among existing competitors. Understanding these dynamics is crucial for strategic decision-making.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Butterfield’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Technology Providers

Technology providers hold considerable sway in the banking and wealth management industry. The sector's growing dependence on advanced software, hardware, and robust cybersecurity means specialized firms, especially those with cutting-edge fintech or core banking systems, can exert significant influence. This power stems from the substantial costs and operational disruptions associated with switching providers, coupled with the essential nature of these technological services.

Butterfield's strategic investments in technology, aimed at improving client experience, highlight this reliance. For instance, in 2024, many financial institutions are allocating substantial budgets to digital transformation initiatives, with reports indicating a global fintech market projected to reach over $33 trillion by 2030, underscoring the critical role and leverage of these technology suppliers.

Skilled Labor and Talent

The financial services sector, particularly in international hubs, relies heavily on specialized talent in areas like banking, wealth management, compliance, and information technology. A constrained supply of these highly qualified individuals, especially within specialized offshore markets, can significantly amplify the leverage held by employees.

Butterfield's strategic initiatives, such as the expansion of its Halifax service center and ongoing investments in technological advancements, are likely designed to improve labor cost efficiency and broaden access to essential talent pools. For instance, as of early 2024, the demand for cybersecurity professionals within financial institutions saw a notable increase, with some reports indicating a 40% rise in job postings for these roles compared to the previous year, highlighting the competitive landscape for skilled IT personnel.

Providers of Capital (Depositors)

While individual depositors typically hold little sway, substantial institutional or high-net-worth clients can collectively impact interest rates or negotiate terms due to the significant volume of their deposits. Butterfield's strategic growth in its deposit base, notably in Bermuda and the Channel Islands during 2024, with total deposits reaching $13.1 billion by the end of Q1 2024, serves to dilute this potential power by lessening dependence on a concentrated few.

Regulatory Bodies

Regulatory bodies act as significant indirect suppliers for banks like Butterfield. For instance, the Bermuda Monetary Authority (BMA) sets the operational rules and capital needs, directly influencing costs and profitability. Butterfield's adherence to frameworks such as Basel III is crucial for its compliance and financial health.

Butterfield's robust regulatory capital ratios, a key indicator of its ability to meet these demands, demonstrate its strong position. As of the first quarter of 2024, Butterfield reported a Common Equity Tier 1 (CET1) ratio of 15.3%, comfortably exceeding regulatory minimums.

- BMA Regulations: Dictate operational framework and capital requirements.

- Basel III Compliance: Impacts operations and profitability.

- Capital Ratios: Butterfield's CET1 ratio stood at 15.3% in Q1 2024, showing strong compliance.

Interbank Market and Financial Institutions

Butterfield, much like its peers, depends on the interbank market for essential liquidity and funding. It also engages with other financial institutions for critical services such as correspondent banking and syndicated loans. The ease of access and the cost of this capital are directly tied to overall market conditions and Butterfield's own financial standing, which grants these suppliers a moderate degree of bargaining power.

In late 2024, a notable factor contributing to Butterfield's positive financial performance was the reduction in its funding costs. This suggests that the suppliers in the interbank and broader financial institution markets were offering capital at more favorable terms during that period.

- Interbank Market Reliance: Banks like Butterfield need the interbank market for daily liquidity and access to funds.

- Supplier Influence: The cost and availability of capital from financial institutions are influenced by market factors and Butterfield's credit rating, giving these suppliers moderate power.

- Impact of Lower Funding Costs: For Butterfield, lower funding costs in late 2024 were a direct contributor to its improved financial results.

Unpacking Supplier Power in Finance

Suppliers in the financial sector, particularly those providing essential technology or specialized talent, can wield significant bargaining power. This leverage is amplified by the high switching costs and the critical nature of their services, as seen in the increasing demand for cybersecurity professionals in 2024.

Butterfield’s reliance on technology providers is evident in its digital transformation efforts, while its strategic hiring and service center expansions aim to secure vital talent pools, mitigating potential supplier power.

Institutional depositors and regulatory bodies also represent forms of supplier power. While large depositors can negotiate terms, Butterfield's diversified deposit growth in 2024 aims to reduce this concentration risk.

Regulatory bodies like the Bermuda Monetary Authority set operational standards, impacting costs, and Butterfield's strong capital ratios, such as a 15.3% CET1 ratio in Q1 2024, demonstrate its compliance and resilience.

| Supplier Type | Example | Impact on Butterfield | 2024 Data Point |

|---|---|---|---|

| Technology Providers | Core Banking Software | High switching costs, operational dependence | Fintech market projected over $33 trillion by 2030 |

| Labor Market | Skilled IT Professionals | Talent scarcity, wage inflation | 40% rise in cybersecurity job postings (early 2024) |

| Depositors | Large Institutional Clients | Potential to negotiate rates | Total deposits reached $13.1 billion (Q1 2024) |

| Regulators | BMA | Imposes capital and operational requirements | CET1 ratio of 15.3% (Q1 2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Butterfield's specific industry and strategic positioning.

Effortlessly identify and address competitive threats with a dynamic, visual representation of all five forces.

Customers Bargaining Power

High-Net-Worth and Institutional Clients

Butterfield's client base includes high-net-worth individuals and large institutions, entities that typically wield considerable bargaining power. These clients often manage substantial financial assets, meaning their business represents a significant revenue stream for Butterfield. For instance, in 2024, the global wealth management market continued to see strong inflows, with high-net-worth individuals accounting for a substantial portion of this growth, underscoring their financial clout.

The ability of these sophisticated clients to easily switch providers, coupled with their specific and often complex needs, amplifies their bargaining leverage. They can readily seek out competitors offering more attractive terms or better-tailored services. Butterfield's strategy to counter this involves cultivating deep, personal relationships and offering integrated solutions designed to foster loyalty and address these demanding requirements.

Retail and Small Business Clients

Individual and small business clients, though numerous, typically possess limited individual bargaining power. This is largely due to their smaller transaction volumes and the potential complexities and costs involved in switching their primary banking services. For instance, the effort to move accounts, re-establish direct deposits, and update payment information can deter frequent changes.

However, the collective actions of these numerous clients can wield considerable influence. Their aggregated decisions directly impact a bank's deposit base and the overall demand for loans. Butterfield's robust deposit growth, reaching $15.2 billion by the end of 2024, underscores the significant impact of client trust and engagement on the institution's financial standing.

Availability of Alternatives

The availability of numerous full-service banks and wealth management firms in Butterfield's key markets significantly enhances customer bargaining power. For instance, in 2024, the global wealth management market was valued at approximately $22.6 trillion, indicating a highly competitive landscape where clients have ample alternatives to consider.

This abundance of choice, further amplified by the rise of fintech solutions offering specialized services, allows customers to easily compare offerings. They can readily seek out institutions providing more favorable interest rates, reduced transaction fees, or highly customized financial solutions, putting pressure on Butterfield to remain competitive.

Butterfield's strategy of maintaining a diversified presence across multiple international financial centers is a direct response to this competitive pressure. By offering a broad spectrum of services in various locations, Butterfield aims to solidify client relationships and retain its customer base despite the increasing ease with which clients can switch providers.

Switching Costs

For many everyday banking needs, like checking accounts or basic savings, customers can indeed switch providers with relative ease. However, when you look at more specialized financial services, such as intricate wealth management, estate planning, or deep corporate banking relationships, the picture changes significantly. The effort, time, and potential disruption involved in moving these complex services can be quite substantial, creating a higher barrier to switching.

Butterfield, recognizing this, actively works to deepen its client relationships and offer integrated financial solutions. This strategy is designed to make it less appealing and more inconvenient for clients to move their business elsewhere, effectively raising the implicit costs of switching. For instance, a client with a comprehensive suite of services, from personal banking to trust administration and investment management, would face considerable complexity in untangling and transferring these interconnected elements.

The bargaining power of customers is thus influenced by these switching costs. While low for simple transactions, it diminishes considerably for clients deeply embedded in Butterfield’s more sophisticated offerings. This is a key factor in how Butterfield can maintain its customer base and pricing power.

- Low Switching Costs for Basic Services: Customers can readily move simple accounts like checking or savings between financial institutions.

- High Switching Costs for Complex Services: Wealth management, trust services, and corporate banking involve significant effort, time, and potential disruption to transfer.

- Butterfield's Strategy: The bank focuses on building long-term relationships and offering integrated solutions to increase implicit switching costs for clients.

- Impact on Bargaining Power: High switching costs for complex services reduce the bargaining power of those specific customer segments.

Information Asymmetry

Information asymmetry, or the lack of equal knowledge between buyers and sellers, significantly impacts customer bargaining power. In today's digital landscape, customers have unprecedented access to information about financial products, services, and pricing comparisons. This heightened transparency directly reduces information asymmetry.

With readily available data, customers are empowered to make more informed decisions, compare offerings across different institutions, and identify the best value. This knowledge allows them to negotiate more effectively for better terms, potentially leading to lower fees or more favorable interest rates, thus increasing their bargaining leverage.

For instance, in 2024, online financial comparison sites saw a significant surge in user engagement, with platforms like NerdWallet and Bankrate reporting millions of monthly visitors actively researching banking, investment, and loan products. This trend underscores the growing customer reliance on accessible information to drive down costs and improve service terms.

- Increased Information Access: Customers in 2024 can easily compare interest rates, fees, and service features across numerous financial institutions online.

- Reduced Information Asymmetry: This ease of access levels the playing field, diminishing the advantage previously held by institutions with proprietary information.

- Enhanced Negotiation Power: Informed customers are better equipped to negotiate for more favorable terms, directly impacting profitability for financial service providers.

- Customer Expectations: Financial institutions must adapt to these informed customers by offering competitive pricing and transparent services to retain business.

Customer Power: Shaping Financial Services Profitability

The bargaining power of customers is a critical factor in the financial services industry, directly influencing profitability and competitive strategy. For Butterfield, this power varies significantly across its client segments, driven by factors like switching costs, available alternatives, and access to information.

High-net-worth individuals and institutions, representing substantial revenue for Butterfield, often possess considerable bargaining power due to the scale of their assets and their ability to easily compare services. In 2024, the global wealth management market, valued at approximately $22.6 trillion, highlighted a competitive landscape where clients have ample choices. This allows them to negotiate for better terms, thereby increasing their leverage.

| Customer Segment | Bargaining Power Factors | Butterfield's Response |

|---|---|---|

| High-Net-Worth Individuals & Institutions | Large asset base, easy access to alternatives, sophisticated needs. | Deep relationship building, integrated solutions, personalized service. |

| Retail & Small Business Clients | Lower individual transaction volume, higher collective impact. | Focus on customer experience, digital convenience, competitive deposit rates. |

Preview the Actual Deliverable

Butterfield Porter's Five Forces Analysis

This preview showcases the complete Butterfield Porter's Five Forces Analysis, offering a detailed examination of competitive forces within the industry. The document you see here is the exact, professionally formatted file you will receive immediately upon purchase, ensuring no discrepancies or missing information. You can confidently proceed with your purchase, knowing you'll gain instant access to this comprehensive strategic tool.

Rivalry Among Competitors

Number and Diversity of Competitors

Butterfield operates in a landscape populated by a diverse array of competitors. In international financial centers, it contends with established full-service banks offering a broad spectrum of financial products, alongside specialized wealth managers focusing on high-net-worth individuals. Niche financial service providers also carve out segments of the market, offering tailored solutions.

The competitive intensity is evident in markets like Bermuda, where Butterfield is headquartered. The presence of other licensed banks in Bermuda signifies a concentrated, yet highly competitive, banking environment. This means Butterfield must constantly innovate and differentiate its offerings to maintain its market position.

Industry Growth Rate

The banking and wealth management sector in established financial hubs typically exhibits mature growth. This means companies like Butterfield often focus on capturing market share from rivals rather than benefiting from a rapidly expanding market. This dynamic naturally fuels intense competition as firms vie for the same pool of clients.

Butterfield's strategic outlook for 2025 includes a focus on sustainable growth, with potential acquisitions being a key avenue for expansion. For instance, in 2024, the global financial services industry saw continued consolidation, with M&A activity remaining a significant driver of growth for many established players seeking to enhance their market position and service offerings.

Product and Service Differentiation

Butterfield differentiates itself by offering a comprehensive suite of integrated financial services. This includes retail and corporate banking, treasury services, and wealth management, designed to serve a broad spectrum of clients.

The company's commitment to bespoke solutions, deep local market knowledge, and a strong emphasis on personal client relationships are key differentiators. These elements help Butterfield stand out in a competitive landscape.

For instance, in 2024, Butterfield reported a Return on Equity of 11.5%, reflecting its ability to leverage its differentiated offerings to generate shareholder value amidst intense competition.

High Exit Barriers

The financial services sector, including institutions like Butterfield, faces substantial exit barriers. These stem from significant investments in specialized infrastructure, stringent regulatory requirements, and the considerable reputational damage that can occur when winding down operations. These factors often mean that firms must persevere through downturns, intensifying competition.

Butterfield's strong capital position, for instance, with its Common Equity Tier 1 (CET1) ratio consistently exceeding regulatory minimums, demonstrates a commitment to long-term operational stability. As of the first quarter of 2024, Butterfield reported a CET1 ratio of 14.3%, well above the typical 7% requirement, highlighting its resilience and ability to absorb potential shocks without immediate exit considerations.

- Significant Fixed Assets: Financial institutions often possess extensive physical branches, data centers, and technology platforms that are costly to divest or repurpose.

- Regulatory Hurdles: Complying with complex banking regulations and obtaining approvals for closure or sale adds significant time and expense, discouraging swift exits.

- Reputational Risk: A disorderly exit can severely damage a firm's reputation, impacting customer trust and future business prospects, making a managed, long-term presence more attractive.

- Specialized Workforce: The highly skilled and specialized nature of financial services employees makes redeployment or retraining difficult, adding to exit costs.

Geographic Diversification

Butterfield's geographic diversification significantly dilutes competitive rivalry. By operating in key international financial centers such as Bermuda, Cayman Islands, Guernsey, Jersey, Bahamas, Singapore, Switzerland, and the UK, the bank spreads its revenue sources and client base. This global footprint allows Butterfield to tap into varied market conditions and competitive environments, reducing the impact of intense competition in any single location.

This strategic dispersion means that even if rivalry intensifies in one region, Butterfield can rely on its performance in other markets. For example, in 2024, Butterfield reported a robust performance across its international segments, with its Channel Islands operations showing particular strength, helping to offset pressures in other areas.

- Global Presence: Butterfield operates in eight key financial centers, including Bermuda, Cayman Islands, Guernsey, Jersey, Bahamas, Singapore, Switzerland, and the UK.

- Revenue Diversification: This international presence diversifies revenue streams, reducing reliance on any single market.

- Market Condition Leverage: The bank can capitalize on favorable market conditions in different regions, mitigating localized competitive pressures.

- Client Base Expansion: A wider geographic reach broadens the client base, making the bank less vulnerable to the loss of clients in one specific market.

Navigating Financial Rivalry Through Global Diversification

Competitive rivalry within the financial services sector, where Butterfield operates, is notably high due to the presence of numerous established banks and specialized wealth managers. This intensity is particularly pronounced in mature markets like Bermuda, driving a need for continuous innovation and client differentiation. High exit barriers, stemming from significant investments and regulatory complexities, compel firms to remain competitive even during market downturns.

Butterfield's strategy of geographic diversification across key international financial centers helps to mitigate the impact of intense rivalry in any single market. By spreading its operations and revenue streams across locations like the Channel Islands, Singapore, and Switzerland, the bank can leverage varied market conditions. For instance, in 2024, its robust performance in the Channel Islands provided a buffer against pressures experienced elsewhere, showcasing the benefits of this dispersed model.

SSubstitutes Threaten

Fintech and Digital Banking Solutions

The burgeoning fintech and digital banking sector presents a potent threat of substitutes for traditional financial institutions like Butterfield. These digital-first players offer streamlined, often more affordable services, ranging from online payment gateways to app-based banking and robo-advisory platforms, directly challenging established models. For instance, the global digital banking market was valued at approximately USD 21.5 billion in 2023 and is projected for substantial growth, highlighting the increasing consumer adoption of these alternatives.

Direct Investment Platforms

For wealth management clients, the rise of direct investment platforms presents a significant threat of substitution. Sophisticated investors can now bypass traditional full-service wealth managers like Butterfield Porter by utilizing online brokerage accounts or self-directed platforms to invest directly in financial markets. This offers them greater control over their portfolios and often comes with lower fees.

This trend empowers investors who prefer to manage their own assets, directly substituting the advisory and management services offered by firms like Butterfield. For instance, the assets under management on major self-directed investing platforms have seen substantial growth, with many reporting trillions of dollars in client assets by early 2024.

While this direct access poses a challenge, Butterfield Porter's diversified fee income structure, which includes asset management, advisory fees, and other financial services, helps to mitigate the potential impact of clients opting for self-directed investments. This diversification provides a cushion against a complete reliance on traditional wealth management fees.

Cryptocurrencies and Digital Assets

The rise of cryptocurrencies and digital assets presents a growing threat of substitutes for traditional financial services. These digital currencies offer alternative avenues for international transactions, asset storage, and wealth movement, potentially bypassing conventional banking channels. Global fintech investment in digital assets saw a significant uptick in early 2025, with projections indicating continued expansion in this sector.

Alternative Lending and Funding Sources

The threat of substitutes for traditional banking services is growing as alternative lending and funding sources become more prevalent. Businesses and individuals are increasingly exploring options like crowdfunding, peer-to-peer lending platforms, and private equity to secure financing, thereby reducing their dependence on conventional corporate and retail banking. This shift is evident in market trends, with Butterfield's loan portfolio experiencing a decrease in 2024, although it showed stability in the first quarter of 2025.

These alternative avenues offer flexibility and sometimes faster access to capital, posing a direct challenge to established financial institutions. For instance, the global alternative lending market was valued at approximately $1.2 trillion in 2023 and is projected to grow significantly in the coming years, indicating a substantial shift in financing preferences.

- Rising popularity of fintech lending platforms: These platforms often provide streamlined application processes and quicker approvals compared to traditional banks.

- Growth in crowdfunding and P2P lending: These methods democratize access to capital for a wider range of borrowers and investors.

- Increased access to private equity and venture capital: For businesses, these sources offer substantial funding, bypassing traditional debt markets.

- Impact on Butterfield's loan portfolio: A decrease in loan volume in 2024 highlights the competitive pressure from these substitute funding sources.

In-house Financial Management

Large corporations and high-net-worth families increasingly opt for in-house financial management, driven by the desire for greater control and the availability of specialized internal expertise. This trend is amplified by the growing complexity of financial markets, where dedicated teams can offer tailored strategies. For instance, many multinational corporations now employ sophisticated treasury departments that handle everything from cash management to complex hedging strategies, bypassing external providers.

This internal capability directly challenges external financial institutions like Butterfield. When entities can effectively manage their own portfolios and financial operations, their reliance on third-party banks or wealth managers diminishes. This can lead to a reduction in fee-based revenue for financial service providers.

Butterfield's strategic response involves offering integrated financial solutions that provide a distinct advantage over what clients can achieve independently. This includes access to proprietary research, advanced technological platforms, and specialized advisory services that might be cost-prohibitive or impractical for in-house teams to replicate. For example, in 2024, the global wealth management market saw assets under management reach an estimated $100 trillion, yet a significant portion of this is managed by large institutions with substantial internal resources.

- Scale and Expertise: Large entities can justify the significant investment in internal financial talent and technology.

- Control and Customization: In-house management allows for direct oversight and bespoke financial strategies.

- Cost Efficiency: For very large portfolios, the cost of in-house management can be lower than outsourcing.

- Risk Mitigation: Direct control can sometimes be perceived as a better way to manage specific risks.

Accessible Alternatives Reshaping Traditional Financial Services

The increasing availability of alternative investment vehicles, such as exchange-traded funds (ETFs) and direct real estate investments, poses a significant threat of substitution for traditional managed funds and advisory services. These options often provide lower fees and greater transparency, appealing to a broad range of investors. The global ETF market alone saw assets under management exceed $10 trillion by early 2024, demonstrating a clear shift towards these accessible alternatives.

| Substitute Product/Service | Key Features | Impact on Traditional Services | Example Data (2024) |

| Fintech & Digital Banking | Streamlined, often lower-cost digital services | Challenges traditional banking models, reduces reliance on physical branches. | Global digital banking market projected to grow significantly, with user adoption rising. |

| Direct Investment Platforms | Self-directed investing, lower fees, greater control | Substitutes wealth management advisory services for sophisticated investors. | Trillions in assets managed on major self-directed platforms by early 2024. |

| Cryptocurrencies & Digital Assets | Alternative for transactions, asset storage, wealth movement | Bypasses conventional banking channels for specific financial needs. | Significant uptick in fintech investment in digital assets in early 2025. |

| Alternative Lending (P2P, Crowdfunding) | Flexible, faster access to capital | Reduces dependence on traditional corporate and retail banking loans. | Global alternative lending market valued at ~$1.2 trillion in 2023, with strong growth forecasts. |

| In-house Financial Management | Greater control, specialized internal expertise | Diminishes reliance on third-party financial institutions for large entities. | Many multinational corporations employ sophisticated in-house treasury departments. |

| ETFs & Direct Real Estate | Lower fees, greater transparency, accessibility | Offers alternatives to traditional managed funds and advisory services. | Global ETF AUM exceeded $10 trillion by early 2024. |

Entrants Threaten

High Regulatory Barriers

The banking sector, particularly in established financial hubs like Bermuda where Butterfield operates, faces substantial hurdles for new players due to extensive regulation. These include rigorous licensing processes and demanding capital adequacy rules, such as those outlined by Basel III, which necessitate significant upfront investment and ongoing compliance. For instance, Bermuda's 2025 banking regulations underscore the complexity and cost associated with entering this market, effectively deterring many potential competitors.

Substantial Capital Requirements

Establishing a full-service bank and wealth management operation, like Butterfield, demands enormous capital. This includes significant investment in physical infrastructure, cutting-edge technology, and meeting stringent regulatory compliance standards. Maintaining adequate liquidity is also a critical and capital-intensive requirement.

These substantial upfront costs act as a significant deterrent, effectively raising the barrier to entry for many aspiring new competitors looking to enter the financial services sector.

For instance, Butterfield's strong capital adequacy ratios, such as a Common Equity Tier 1 ratio consistently above 15% in recent reporting periods (e.g., Q1 2024), underscore the sheer scale of capital required to operate effectively and competitively in this industry.

Economies of Scale and Scope

Established players like Butterfield benefit from significant economies of scale, meaning they can produce goods or services at a lower per-unit cost due to their large operational size. For instance, in 2024, Butterfield's operational efficiency, driven by its substantial asset base and streamlined processes, allowed it to maintain lower overheads compared to emerging competitors. This scale also extends to technology investments and risk management capabilities, which are prohibitively expensive for newcomers.

Furthermore, Butterfield leverages economies of scope by offering a diverse portfolio of integrated financial services, from banking to wealth management. This breadth of offerings creates a more compelling value proposition for customers and generates cross-selling opportunities. New entrants typically find it challenging to replicate this comprehensive service ecosystem rapidly, forcing them to compete on a narrower, less profitable front.

Brand Loyalty and Reputation

Butterfield's enduring legacy, dating back to its founding in 1858, has cultivated a robust brand loyalty and a sterling reputation, especially within the offshore banking sphere. This deep-seated trust is a significant barrier for newcomers attempting to establish a foothold, as replicating such credibility in financial services requires substantial time and investment.

The financial industry, by its very nature, demands a high degree of confidence from its clientele. Butterfield's long history and consistent performance have solidified its standing, making it difficult for new entrants to quickly erode this established trust and capture market share. For instance, as of the first quarter of 2024, Butterfield reported total assets of approximately $14.9 billion, underscoring its substantial and stable presence.

- Established Trust: Butterfield's founding in 1858 signifies over 160 years of operational history, building a deeply ingrained sense of reliability.

- Reputational Capital: A strong, stable reputation, particularly in specialized areas like offshore banking, acts as a significant deterrent to new competitors.

- Customer Loyalty: The lengthy process of cultivating trust in financial services means that existing customer loyalty to established brands like Butterfield is a formidable barrier.

Access to Distribution Channels and Client Relationships

New entrants into the financial services sector often struggle to replicate the established distribution channels and deep-seated client relationships that incumbents like Butterfield Porter possess. Building an extensive branch network or a robust digital platform requires substantial capital investment, and even then, attracting and retaining clients is a formidable task.

Butterfield's long-standing commitment to a relationship-based business model, focusing on personalized service and trust, creates a significant barrier. This emphasis means new players must not only offer competitive products but also invest heavily in cultivating similar levels of client loyalty and confidence.

For instance, as of the first quarter of 2024, Butterfield reported a strong client retention rate, underscoring the stickiness of its established relationships. New entrants would need to demonstrate a compelling value proposition to overcome Butterfield's existing market penetration and client goodwill.

- Established Networks: Butterfield benefits from a well-developed network of physical branches and digital platforms, offering convenience and accessibility that new entrants find difficult to match.

- Client Loyalty: The bank's focus on long-term client relationships, built on trust and personalized service, creates a loyal customer base that is less susceptible to switching.

- Brand Reputation: A strong brand reputation, cultivated over years of reliable service, acts as a significant deterrent for new entrants attempting to gain market share.

Banking's High Walls: Why New Entrants Face Formidable Barriers

The threat of new entrants into the banking sector, particularly for a firm like Butterfield, is considerably low due to immense capital requirements and stringent regulatory oversight. For example, Bermuda's 2025 banking regulations, alongside global standards like Basel III, demand substantial upfront investment in licensing, infrastructure, and compliance, making it prohibitively expensive for newcomers. Butterfield's own strong capital position, with a Common Equity Tier 1 ratio consistently above 15% as of Q1 2024, illustrates the scale of financial muscle needed to compete effectively.

Established players like Butterfield also benefit from significant economies of scale and scope, offering a diverse range of integrated financial services that are difficult for new entrants to replicate quickly or cost-effectively. This operational efficiency and broad service offering, coupled with over 160 years of brand building since its 1858 founding, fosters deep customer loyalty and trust, presenting a formidable barrier to market entry. As of Q1 2024, Butterfield reported total assets of approximately $14.9 billion, highlighting its substantial and stable market presence.

| Factor | Description | Impact on New Entrants |

| Capital Requirements | High upfront investment for licensing, infrastructure, and regulatory compliance. | Very High Barrier |

| Regulatory Hurdles | Complex licensing processes and ongoing compliance with standards like Basel III. | Very High Barrier |

| Economies of Scale & Scope | Lower per-unit costs due to large operations and integrated service offerings. | High Barrier |

| Brand Reputation & Trust | Long history (since 1858) builds customer loyalty and confidence. | High Barrier |

| Established Client Relationships | Focus on personalized service creates sticky customer relationships. | High Barrier |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a foundation of robust data, including industry-specific market research reports, financial statements from key players, and publicly available company filings. We also incorporate economic indicators and expert commentary from reputable trade publications to ensure a comprehensive understanding of the competitive landscape.