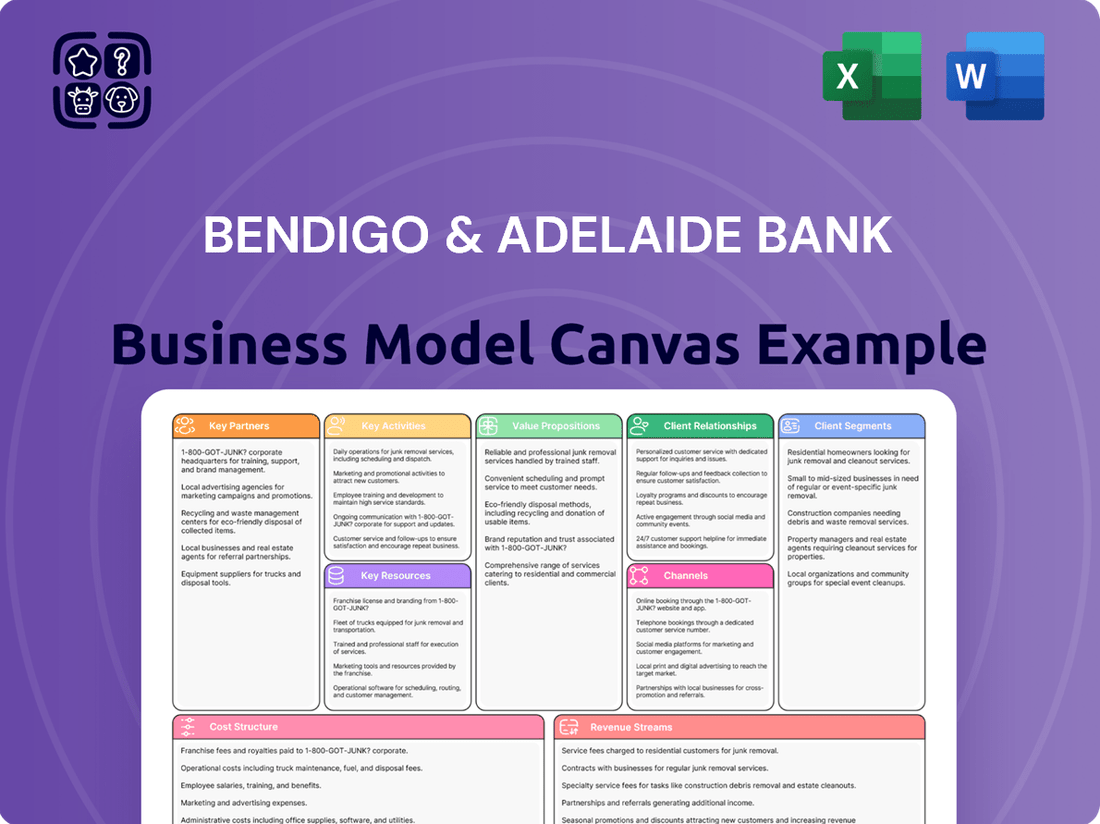

Bendigo & Adelaide Bank Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Bendigo & Adelaide Bank

Bank's Business Model: A Strategic Deep Dive

Unlock the strategic blueprint of Bendigo & Adelaide Bank's success with our comprehensive Business Model Canvas. This detailed analysis breaks down their customer segments, value propositions, and revenue streams, offering invaluable insights for any business strategist. Discover how they build strong customer relationships and manage key resources to maintain their competitive edge.

Partnerships

Community Bank Network

Bendigo and Adelaide Bank's Community Bank network is built on a foundation of local partnerships. These aren't just branches; they are community-owned and operated entities, deeply embedded in their local economies.

This unique structure means that profits generated by these branches are directly reinvested into community projects and local initiatives. For instance, in 2023, the Community Bank network contributed over $10.5 million to local causes, demonstrating a tangible commitment to community development.

This model creates a powerful competitive advantage. By fostering strong local ties and demonstrating a genuine commitment to community well-being, Bendigo and Adelaide Bank cultivates deep customer loyalty and a distinct market position, differentiating itself from traditional banking models.

Fintech Companies

Bendigo and Adelaide Bank actively cultivates key partnerships with fintech companies to drive innovation and expedite the development of new products and services. This strategic approach allows the bank to tap into specialized external expertise and cutting-edge technologies, such as artificial intelligence and advanced cloud solutions.

By collaborating with fintechs, Bendigo and Adelaide Bank enhances its digital capabilities, ensuring it remains competitive in the rapidly evolving financial services sector. For instance, in the 2023 financial year, the bank reported a 14% increase in digital transactions, partly attributable to these strategic fintech integrations.

Third-Party Banking Channels (Brokers)

Bendigo and Adelaide Bank leverages third-party banking channels, notably mortgage brokers, to significantly broaden its distribution network for lending products. This strategic alliance allows the bank to tap into a wider customer base that might not directly engage with traditional branch services.

The recent introduction of the Bendigo Lending Platform is a key initiative designed to enhance the efficiency of these partnerships. By streamlining the application and approval processes, the platform aims to foster deeper, more productive relationships with customers who originate through broker relationships.

In 2024, mortgage brokers played a crucial role in the Australian home loan market, facilitating approximately 69% of all new home loans, according to industry data. Bendigo and Adelaide Bank's focus on this channel reflects a strategic move to capture a substantial portion of this significant market share.

Technology and Cloud Providers

Bendigo and Adelaide Bank actively cultivates strategic alliances with key technology and cloud providers. These partnerships are fundamental to their ongoing digital transformation initiatives. For instance, collaborations with companies like MongoDB and Google Cloud are instrumental in modernizing the bank's core systems and enhancing its technological capabilities.

These collaborations are designed to facilitate the migration of critical banking infrastructure to cloud-based environments. This move is essential for improving scalability, agility, and the overall efficiency of operations. Furthermore, these tech partnerships enable the bank to leverage advanced technologies such as artificial intelligence (AI) for application modernization.

A significant outcome of these partnerships is the development of a robust Application Programming Interface (API) ecosystem. This ecosystem is vital for ensuring seamless and secure data exchange between various internal and external systems. In 2024, the banking sector’s reliance on cloud services continued to grow, with many institutions reporting significant investments in cloud migration projects to support digital innovation and customer experience enhancements.

- Core Banking Modernization: Partnerships with providers like MongoDB support the migration and modernization of legacy core banking systems.

- Cloud Infrastructure: Collaborations with Google Cloud enable the transition of the bank's operations to a scalable and secure cloud environment.

- AI and Application Development: These alliances facilitate the integration of AI into banking applications, driving innovation and efficiency.

- API Ecosystem Development: Strategic tech partnerships are crucial for building a comprehensive API strategy, allowing for better data integration and new service offerings.

Educational Institutions and Scholarship Programs

Bendigo and Adelaide Bank actively fosters key partnerships with educational institutions and scholarship programs to cultivate future talent and support community growth. These collaborations are vital for the bank's commitment to social impact, particularly in underserved regions.

A significant aspect of this strategy involves working with entities like Rural Bank and their network of Community Bank branches. This allows the bank to extend its reach and offer valuable scholarship opportunities to tertiary students. These programs are designed to enhance educational access and outcomes, especially for those in regional and remote areas, underscoring the bank's dedication to community development and long-term prosperity.

- Scholarship Reach: In 2023, Bendigo and Adelaide Bank supported numerous students through various scholarship initiatives, contributing to educational attainment across Australia.

- Community Focus: Partnerships with Rural Bank and Community Bank branches specifically target support for students in regional and remote locations, addressing educational equity.

- Talent Development: These educational partnerships serve as a pipeline for future talent, aligning with the bank's strategic objective of investing in human capital.

- Social Impact Measurement: The bank tracks the success of these programs by monitoring student progression and the positive impact on regional communities.

Strategic Partnerships Drive Digital Growth and Community Impact

Bendigo and Adelaide Bank's key partnerships extend to fintech innovators and established technology providers, crucial for modernizing its operations. These collaborations fuel digital transformation, enabling the bank to integrate advanced technologies like AI and cloud solutions, enhancing customer experience and operational efficiency.

The bank also relies heavily on mortgage brokers, a vital distribution channel that facilitated approximately 69% of new home loans in Australia in 2024. By optimizing these relationships through platforms like the Bendigo Lending Platform, the bank aims to capture a larger share of this significant market.

Furthermore, partnerships with educational institutions and scholarship programs underscore the bank's commitment to community development and talent cultivation, particularly in regional areas. These initiatives not only foster social impact but also create a pipeline for future banking professionals.

| Partnership Type | Key Collaborators | Strategic Objective | 2023/2024 Impact/Data |

|---|---|---|---|

| Fintech & Technology | Various Fintechs, MongoDB, Google Cloud | Digital transformation, core banking modernization, AI integration | 14% increase in digital transactions (FY23); Ongoing cloud migration projects |

| Distribution Channels | Mortgage Brokers | Expand lending distribution, increase market share | Brokers facilitated ~69% of new home loans in 2024 |

| Community & Education | Rural Bank, Community Bank Network, Educational Institutions | Community reinvestment, talent development, educational access | Over $10.5 million contributed to local causes (2023); Numerous students supported via scholarships |

What is included in the product

A detailed exploration of Bendigo and Adelaide Bank's operations, outlining its customer segments, value propositions, and revenue streams through the lens of the Business Model Canvas.

This overview highlights the bank's strategic approach to customer relationships, key partnerships, and cost structure, providing insights into its competitive positioning.

Bendigo & Adelaide Bank's Business Model Canvas offers a clear, structured approach to visualizing their operations, effectively alleviating the pain point of complex strategic planning by providing a digestible, one-page snapshot.

This model helps simplify intricate banking strategies, making it easier for stakeholders to grasp key relationships and identify areas for improvement, thus relieving the burden of understanding a multifaceted financial institution.

Activities

Core Banking Services Provision

Bendigo and Adelaide Bank's core banking services provision encompasses the essential functions of a financial institution. This includes accepting customer deposits, providing various personal and business loans, managing credit and debit card portfolios, and offering efficient payment processing solutions.

These foundational activities are crucial for meeting the everyday financial needs of individuals and businesses. For instance, in the financial year 2024, Bendigo and Adelaide Bank reported a net interest margin of 1.75%, reflecting the profitability derived from its lending and deposit-taking operations.

Digital Transformation and Modernisation

Bendigo and Adelaide Bank is actively simplifying its operations and modernizing its technology infrastructure. A key part of this involves consolidating core banking systems and migrating a substantial portion of its applications to the cloud, aiming for greater agility and cost efficiency.

The bank is strategically investing in digital transformation, with a focus on leveraging artificial intelligence and automation. These technologies are being implemented to streamline internal processes, reduce operational costs, and crucially, to enhance the overall customer experience through more personalized and efficient services.

In 2024, the bank reported significant progress in its digital initiatives. For instance, it aims to achieve further cost reductions through its simplification program, with a target of around $200 million in annualized savings by FY2025, a substantial portion of which is driven by these modernization efforts.

Lending and Wealth Management

Bendigo and Adelaide Bank's key activities in lending involve originating and managing a diverse portfolio of loans, including crucial home loans, essential business financing, and vital rural lending. This core function underpins their role in supporting individuals and businesses.

Alongside lending, the bank actively engages in wealth management, offering services to help clients grow and protect their assets. This dual focus allows them to cater to a broader range of financial needs.

A significant ongoing activity is the development and enhancement of new lending platforms. For instance, in the first half of 2024, the bank continued its digital transformation efforts, aiming to streamline the customer experience and improve operational efficiency in its lending processes.

Community Engagement and Investment

Bendigo and Adelaide Bank's Community Engagement and Investment activities are central to its unique Community Bank model. This involves returning a significant portion of profits to the local communities where these branches operate, fueling diverse projects and initiatives.

These community investments extend to vital areas like scholarships, sponsorships for local events and organizations, and programs specifically designed to boost financial inclusion and overall well-being. This approach fosters strong local ties and a shared sense of purpose.

- Community Bank Model: Profits are reinvested locally, with over $200 million returned to communities since 1998 as of the 2023 financial year.

- Financial Inclusion Initiatives: Programs aim to improve financial literacy and access to banking services for underserved populations.

- Scholarships and Sponsorships: Support for educational pursuits and local community events, fostering development and engagement.

- Community Well-being: Investments in projects that enhance the social and economic fabric of the communities served.

Risk Management and Compliance

Bendigo and Adelaide Bank's key activities heavily revolve around robust risk management and unwavering regulatory compliance. As a financial institution, this means constantly identifying, assessing, and mitigating various financial risks, from credit and market to liquidity and operational. Ensuring adherence to a complex and ever-evolving regulatory landscape is paramount to maintaining trust and operational integrity.

The bank actively combats fraud and scams, a critical ongoing effort in today's digital environment. This involves continuous investment in advanced fraud detection systems and strengthening internal controls. For instance, in the first half of 2024, the bank reported a reduction in its net credit charge-off ratio, demonstrating effective credit risk management.

- Financial Risk Mitigation: Implementing strategies to manage credit, market, and liquidity risks.

- Regulatory Adherence: Ensuring compliance with all relevant banking laws and regulations.

- Fraud and Scam Prevention: Investing in technology and processes to protect customers and the bank from financial crime.

- Framework Enhancement: Continuously updating and improving risk and compliance frameworks.

Holistic Banking: Loans, Wealth, Community Reinvestment, Risk Mitigation

Bendigo and Adelaide Bank's key activities include managing a diverse loan portfolio, from home and business loans to crucial rural lending, supporting economic growth. They also focus on wealth management services, helping clients grow and protect their assets, and actively develop new lending platforms to improve customer experience and efficiency.

The bank's unique Community Bank model involves reinvesting profits into local communities through scholarships, sponsorships, and financial inclusion programs, fostering local development. This commitment is evident in the over $200 million returned to communities since 1998.

Furthermore, Bendigo and Adelaide Bank prioritizes robust risk management and regulatory compliance, actively combating fraud and scams with advanced systems. In the first half of 2024, the bank reported a reduction in its net credit charge-off ratio, highlighting effective risk mitigation.

| Key Activity | Description | Financial Year 2024 Data/Context |

| Lending Operations | Originating and managing various loans. | Continued digital transformation of lending processes. |

| Wealth Management | Providing services for asset growth and protection. | Integrated wealth management offerings. |

| Community Engagement | Reinvesting profits into local communities. | Over $200 million returned to communities since 1998 (as of FY23). |

| Risk Management & Compliance | Mitigating financial risks and ensuring regulatory adherence. | Reduction in net credit charge-off ratio in H1 2024. |

Full Document Unlocks After Purchase

Business Model Canvas

The Bendigo & Adelaide Bank Business Model Canvas you're previewing is the actual document you will receive upon purchase. This isn't a sample or a mockup; it's a direct snapshot of the complete, ready-to-use file. You'll gain full access to this same comprehensive analysis, allowing you to understand their strategic approach immediately.

Resources

Financial Capital and Liquidity

Bendigo and Adelaide Bank's financial capital and liquidity are anchored by a robust balance sheet, exemplified by its strong Common Equity Tier 1 (CET1) ratio, which stood at an impressive 11.57% as of the first half of 2024. This healthy capital position, along with substantial customer deposits, provides the essential foundation for its lending operations, ensuring solvency and enabling continued investment in its business.

Technology Infrastructure and Digital Platforms

Bendigo & Adelaide Bank’s technology infrastructure, including its core banking systems and cloud capabilities, forms the backbone of its operations. This digital foundation is crucial for delivering services efficiently and securely to its customers.

The bank leverages its digital platforms, such as the innovative Up app and the Bendigo Lending Platform, to enhance customer experience and streamline processes. These platforms are key to its strategy of digital innovation and customer engagement.

Furthermore, the integration of Artificial Intelligence (AI) into its operations is a vital resource, enabling personalized services and data-driven decision-making. In 2024, the bank continued to invest in these areas, aiming to boost operational efficiency and customer satisfaction.

Human Capital and Expertise

Bendigo and Adelaide Bank's human capital is a cornerstone, boasting a dedicated workforce of over 7,000 employees as of early 2024. This skilled team encompasses vital roles such as relationship managers, IT specialists, and customer service representatives, all contributing to the bank's operational efficiency and strategic goals.

The collective expertise of these individuals is crucial for driving the bank's ongoing transformation initiatives and fostering strong customer relationships. Their knowledge directly impacts service delivery, innovation, and the overall customer experience, which are key differentiators in the competitive banking landscape.

Brand Reputation and Trust

Bendigo and Adelaide Bank's brand reputation, often cited as Australia's most trusted bank, is a cornerstone of its business model. This strong standing, built on a foundation of community focus, translates directly into enhanced customer loyalty and a significant draw for new clientele.

This trust isn't just anecdotal; it's reflected in customer engagement. For instance, in the 2024 financial year, the bank reported a net promoter score (NPS) that consistently outperformed industry averages, indicating high levels of customer satisfaction and advocacy.

- Customer Loyalty: The bank's trusted image directly contributes to higher customer retention rates, reducing acquisition costs.

- Brand Attraction: A strong reputation acts as a magnet, attracting new customers who value reliability and ethical practices.

- Community Banking Model: This approach, deeply embedded in the brand, fosters strong local relationships and a sense of belonging.

- Market Differentiation: In a competitive financial landscape, trust provides a crucial differentiator, setting Bendigo and Adelaide Bank apart.

Branch Network and Partner Channels

Bendigo and Adelaide Bank leverages its extensive physical branch network, including its distinctive Community Bank branches, as a primary channel for customer engagement and service delivery. As of the first half of 2024, the bank operated approximately 500 branches across Australia, offering a tangible presence and personalized service, particularly in regional areas.

Complementing its physical footprint, the bank also relies on a robust network of third-party partners, such as mortgage brokers and financial advisors. This partnership model significantly expands its reach, enabling access to a broader customer base and diverse financial needs. In 2023, third-party channels contributed a substantial portion of the bank's new home loan originations.

- Physical Presence: Approximately 500 branches nationwide, with a strong emphasis on community-based banking models.

- Third-Party Distribution: Extensive network of brokers and agencies enhancing market penetration and customer access.

- Customer Interaction: Both channels facilitate direct customer relationships, service provision, and product distribution.

Bank's Core Resources: Capital, Network, Talent, Tech

Bendigo and Adelaide Bank's key resources include its strong financial capital, with a Common Equity Tier 1 ratio of 11.57% in H1 2024, and its extensive physical branch network of around 500 locations as of H1 2024. The bank also relies on its skilled human capital, comprising over 7,000 employees in early 2024, and its robust digital platforms like the Up app. Its trusted brand reputation, underscored by strong customer loyalty and a community banking model, is a significant intangible asset.

| Resource Category | Key Resources | Supporting Data/Facts (as of H1 2024 unless otherwise stated) |

|---|---|---|

| Financial Capital | Strong Balance Sheet, Customer Deposits | CET1 Ratio: 11.57% |

| Physical Infrastructure | Branch Network, Community Bank Branches | Approximately 500 branches nationwide |

| Human Capital | Skilled Workforce | Over 7,000 employees (early 2024) |

| Intellectual Property & Brand | Brand Reputation, Digital Platforms | Consistently high Net Promoter Score (NPS) |

Value Propositions

Community-Centric Banking

Bendigo and Adelaide Bank's Community-Centric Banking model is a core value proposition, directly channeling profits back into local areas. This approach resonates deeply with customers who prioritize supporting local development and initiatives, creating a powerful sense of shared success.

In 2024, the bank's commitment to community was evident, with its Community Bank network contributing significantly to local economies. For instance, the network's branches collectively supported numerous local projects, demonstrating a tangible return on customer loyalty that extends beyond financial services.

Trusted and Reliable Financial Services

Bendigo and Adelaide Bank emphasizes its standing as Australia's most trusted bank, offering secure and dependable financial products and services. This commitment fosters customer confidence for personal, business, and wealth management needs.

In 2024, the bank continued to build on this reputation, with customer satisfaction scores remaining a key performance indicator. Their focus on reliability underpins their value proposition, ensuring customers feel secure in their financial dealings.

Comprehensive Product Suite

Bendigo and Adelaide Bank boasts a comprehensive product suite designed to meet a wide array of customer needs. This includes everything from everyday personal and business banking accounts to specialized offerings like home loans, credit cards, and robust wealth management solutions.

This extensive range ensures the bank can serve a broad customer base, from individuals managing their personal finances to small businesses requiring operational accounts and larger corporations needing sophisticated financial services. For instance, in the fiscal year 2024, the bank reported a significant increase in its home loan portfolio, reflecting strong demand for its mortgage products.

Enhanced Digital Experience

Bendigo & Adelaide Bank is significantly upgrading its digital offerings, aiming to provide a seamless and efficient banking experience. This focus on digital transformation is evident in their development of platforms like Up, which caters to a modern, tech-savvy customer base, and the new Bendigo Lending Platform, designed to streamline the loan application process.

These initiatives directly translate into enhanced customer convenience and faster service delivery. For instance, by the end of the 2024 financial year, Bendigo & Adelaide Bank reported a substantial increase in digital transaction volumes, underscoring customer adoption of these improved digital channels.

- Digital Transformation: Ongoing investment in technology to modernize banking services.

- Platform Development: Creation of user-friendly platforms like Up and the Bendigo Lending Platform.

- Customer Convenience: Offering faster, more accessible banking for digitally engaged customers.

- Increased Digital Adoption: Evidence of customer preference for digital channels, shown by rising transaction volumes in 2024.

Personalised Customer Service

Bendigo and Adelaide Bank prioritizes a human-centric approach to customer service, even with its digital offerings. This means customers can still expect face-to-face interactions at their branches, offering a personal touch that many value.

The bank ensures responsive customer support, catering to those who prefer direct assistance rather than solely relying on digital channels. This commitment to personalized help is a key differentiator.

- Branch Network: As of June 2024, Bendigo and Adelaide Bank maintained a significant physical presence with approximately 160 branches across Australia, supporting their personalized service model.

- Customer Satisfaction: In recent surveys conducted in late 2023 and early 2024, customer feedback frequently highlighted the helpfulness and personalized nature of interactions with bank staff as a key reason for their loyalty.

Community-Centric Banking: Trust, Digital, Growth

Bendigo and Adelaide Bank's value proposition centers on its unique community-based banking model, fostering local economic growth and customer loyalty by reinvesting profits. This is complemented by a strong emphasis on being Australia's most trusted bank, providing secure and reliable financial products across personal, business, and wealth management sectors. The bank also offers a comprehensive suite of financial products, from everyday banking to specialized loans and wealth solutions, catering to a diverse customer base. Furthermore, significant investment in digital transformation, including platforms like Up, enhances customer convenience and service delivery, as evidenced by rising digital transaction volumes in 2024.

| Value Proposition | Description | 2024 Data/Evidence |

|---|---|---|

| Community-Centric Banking | Reinvesting profits into local communities, fostering shared success. | Community Bank network significantly contributed to local economies and projects. |

| Trusted Financial Partner | Offering secure and dependable financial products and services. | Customer satisfaction scores remained a key performance indicator, reflecting reliability. |

| Comprehensive Product Suite | A wide range of financial solutions for individuals and businesses. | Reported a significant increase in its home loan portfolio in FY2024. |

| Digital Innovation | Upgrading digital offerings for seamless and efficient banking experiences. | Substantial increase in digital transaction volumes by end of FY2024. |

| Human-Centric Service | Personalized customer support through branches and responsive assistance. | Maintained approximately 160 branches; customer feedback highlighted staff helpfulness. |

Customer Relationships

Community-Led Engagement

Bendigo and Adelaide Bank's Community Bank model fosters deep, localized customer relationships by empowering communities and directly benefiting them. This approach cultivates strong loyalty and a shared sense of purpose, moving beyond typical transactional banking interactions.

In 2024, the bank continued to highlight this commitment, with its network of over 300 Community Bank branches serving more than 1.5 million customers. This decentralized structure allows for a more personal touch, with local branches often reinvesting a significant portion of their profits back into their communities, strengthening the bond with customers.

Personalised Support and Advisory

Bendigo and Adelaide Bank prioritizes personalized support, leveraging its branch network and mobile relationship managers to offer tailored advice. This human-centric approach fosters deeper customer connections by addressing individual financial goals and needs.

In 2024, the bank continued to emphasize this strategy, with a significant portion of its customer interactions occurring through face-to-face channels or direct engagement with relationship managers, reinforcing its commitment to a personalized banking experience.

Digital Self-Service and Support

Bendigo and Adelaide Bank champions digital self-service through its Up digital bank and robust online platforms, empowering customers to manage their finances independently. This focus on digital channels, including enhanced online banking and mobile app functionalities, directly addresses the growing preference for convenience and control among its customer base.

Proactive Financial Wellbeing Initiatives

Bendigo and Adelaide Bank actively champions proactive financial wellbeing initiatives, extending support beyond transactional banking. In 2024, the bank continued its focus on financial inclusion through targeted programs, demonstrating a commitment to customer welfare.

These efforts include offering specialized programs and support mechanisms designed to assist vulnerable customer segments. This approach underscores a dedication to customer welfare that transcends simple product offerings.

- Financial Literacy Programs: Providing tools and education to enhance customers' understanding of financial management.

- Support for Vulnerable Groups: Offering tailored assistance and resources for individuals facing financial challenges.

- Community Partnerships: Collaborating with organizations to broaden the reach and impact of financial wellbeing initiatives.

- Digital Tools for Wellbeing: Developing and promoting digital platforms that empower customers to manage their finances effectively.

Broker and Partner Relationship Management

Bendigo and Adelaide Bank cultivates robust relationships with its third-party distribution network, including mortgage brokers and strategic partners. These alliances are crucial for customer acquisition and service delivery.

The bank actively supports its broker and partner network through dedicated platforms, such as the recently enhanced Bendigo Lending Platform. This technology streamlines the lending process, fostering efficiency and a positive customer journey.

- Broker Engagement: The bank prioritizes strong, collaborative relationships with its mortgage broker network, recognizing their significant role in reaching a wider customer base.

- Partner Support: Bendigo and Adelaide Bank provides dedicated resources and platforms to its strategic partners, ensuring they have the tools needed to effectively serve mutual customers.

- Platform Efficiency: The introduction of the new Bendigo Lending Platform aims to improve the operational efficiency for brokers and partners, leading to a smoother experience for all parties involved.

- Customer Experience: By empowering its third-party channels with advanced tools and strong relationships, the bank ensures a consistent and positive experience for customers acquired through these channels.

Customer Relationships: Local Roots, Digital Reach, Lasting Value

Bendigo and Adelaide Bank's customer relationships are built on a foundation of community focus and personalized service, differentiating it from traditional banking models. The bank's unique Community Bank structure, with over 300 branches in 2024, fosters deep local connections and loyalty.

This localized approach is complemented by digital offerings, including the Up digital bank, catering to evolving customer preferences for convenience and self-service. The bank also prioritizes financial wellbeing, extending support beyond basic transactions.

Furthermore, strong relationships with third-party distributors like mortgage brokers are vital for customer acquisition and service, supported by platforms like the Bendigo Lending Platform. This multi-faceted strategy aims to build lasting, valuable customer connections.

| Relationship Type | Key Engagement Strategy | 2024 Data Point |

|---|---|---|

| Community Banking | Localized branches, community reinvestment | Over 300 Community Bank branches |

| Personalized Service | Face-to-face interactions, relationship managers | Significant portion of customer interactions |

| Digital Engagement | Up digital bank, online platforms | Growing preference for digital channels |

| Third-Party Distribution | Mortgage brokers, strategic partners | Enhanced Bendigo Lending Platform |

Channels

Branch Network (including Community Banks)

Bendigo and Adelaide Bank leverages its extensive branch network, including its distinctive Community Bank model, as a cornerstone of its customer engagement strategy. These physical locations facilitate crucial face-to-face interactions, offering traditional banking services and fostering deep community ties.

As of June 30, 2024, the bank operated 524 outlets, a significant portion of which are Community Bank branches, demonstrating a commitment to local presence and support. This network is vital for building trust and providing personalized financial advice, particularly in regional areas where other banking options may be limited.

Digital Platforms (Online and Mobile Banking)

Bendigo and Adelaide Bank's digital platforms, including its Up digital bank, are central to its customer engagement strategy. These online and mobile channels offer a seamless experience for managing accounts, making payments, and accessing a broad range of banking products, appealing to a growing segment of digitally-native consumers.

In 2024, the bank reported a significant increase in digital transaction volumes, reflecting the widespread adoption of its online and mobile banking services. This digital push is crucial for serving a younger demographic and enhancing operational efficiency by reducing reliance on traditional branch interactions.

Third-Party Banking (Brokers)

Bendigo and Adelaide Bank leverages third-party banking channels, primarily mortgage brokers, to distribute its lending products, especially home loans. This strategy significantly expands the bank's market reach beyond its direct customer base.

The introduction of the new Bendigo Lending Platform is designed to streamline operations and improve the efficiency of these broker relationships. This platform aims to enhance the speed and ease with which brokers can access and offer Bendigo's mortgage solutions.

In the 2024 financial year, third-party mortgage origination represented a substantial portion of the Australian home loan market, with brokers facilitating approximately 60% of all new home loans. Bendigo's focus on this channel acknowledges its critical role in the competitive lending landscape.

Agent Network

Bendigo and Adelaide Bank leverages an agent network, embedding digital banking services within existing community businesses like newsagents and pharmacies. This strategy significantly broadens the bank's reach, particularly in underserved regional and rural areas, making essential financial services more accessible to a wider customer base.

This approach is crucial for financial inclusion, allowing customers in remote locations to perform transactions and access digital banking tools without needing to travel to traditional branches. For instance, in 2024, the bank continued to emphasize its commitment to regional Australia, a core tenet of its business model, by supporting these agent locations.

- Agent Network Expansion: The bank actively seeks to grow its network of agents, understanding that each new location represents a touchpoint for potential new customers and enhanced service delivery.

- Digital Integration: Agents are equipped with the technology to offer a range of digital banking functions, streamlining customer interactions and promoting digital adoption.

- Community Focus: This model reinforces the bank's identity as a community-focused institution, building trust and loyalty by integrating into the fabric of local towns.

- Cost-Effective Reach: Utilizing existing retail infrastructure offers a more cost-effective method of expanding market presence compared to establishing new physical branches.

Customer Contact Centres

Bendigo and Adelaide Bank leverages customer contact centres as a crucial channel for direct customer interaction, addressing inquiries and facilitating a range of banking services. These centres are pivotal for customer support and relationship management.

The bank is committed to enhancing the operational efficiency of its contact centres. A key focus is on reducing customer wait times, a metric that directly impacts customer satisfaction and loyalty. For instance, in the first half of 2024, the bank reported improvements in average handling times for customer calls, aiming to resolve issues more swiftly.

- Service Delivery: Contact centres handle a high volume of customer interactions, from simple account queries to complex product support.

- Efficiency Improvements: Ongoing investments in technology and staff training in 2024 have focused on optimizing call routing and first-contact resolution rates.

- Customer Experience: Efforts to reduce wait times and improve service quality are central to maintaining positive customer relationships.

Broadening Reach: Multi-Channel Customer Engagement

Bendigo and Adelaide Bank employs a multi-channel approach to reach its customers, blending physical presence with digital convenience and strategic partnerships. This diverse channel strategy is designed to cater to a broad customer base, ensuring accessibility and fostering strong relationships across different segments.

| Channel | Description | Key 2024 Data/Focus |

|---|---|---|

| Branch Network | Physical locations, including Community Banks, for face-to-face service and community engagement. | 524 outlets as of June 30, 2024, emphasizing regional presence and personalized advice. |

| Digital Platforms | Online and mobile banking services, including the Up digital bank, for seamless account management and transactions. | Significant increase in digital transaction volumes in 2024, serving digitally-native consumers and improving efficiency. |

| Third-Party Channels | Primarily mortgage brokers, expanding reach for lending products, especially home loans. | Third-party origination accounted for approximately 60% of the Australian home loan market in 2024. |

| Agent Network | Embedding digital services within existing community businesses (newsagents, pharmacies) for wider accessibility. | Continued emphasis on supporting these locations in regional Australia in 2024 to enhance financial inclusion. |

| Customer Contact Centres | Direct customer interaction for inquiries, support, and service facilitation. | Focus on reducing wait times and improving first-contact resolution in H1 2024, with reported improvements in average handling times. |

Customer Segments

Individuals and Households

Bendigo and Adelaide Bank caters to a vast array of individuals and households across Australia, offering essential personal banking services. This includes everyday transaction accounts, various savings options, and crucial financial tools like home loans and credit cards, designed to meet diverse financial needs.

The bank's customer base is notably broad, reflecting a commitment to serving a wide demographic spectrum. In 2024, Bendigo and Adelaide Bank continued to focus on enhancing its digital offerings to better serve these customers, aiming for greater accessibility and convenience in managing their finances.

Small to Medium-sized Enterprises (SMEs)

Bendigo and Adelaide Bank actively supports Small to Medium-sized Enterprises (SMEs) by offering a comprehensive range of business banking solutions. These include tailored lending options, competitive deposit accounts, and efficient payment processing services, all designed to meet the diverse needs of growing businesses.

The bank's strategic focus extends to nurturing microbusinesses, providing them with the foundational financial tools and guidance necessary to scale and evolve into more substantial SMEs. This commitment is underscored by their role in facilitating business growth across various sectors.

In 2024, Bendigo and Adelaide Bank continued its strong engagement with the SME sector, with business lending growing by 7.2% in the first half of the financial year, demonstrating a tangible commitment to supporting these vital economic contributors.

Agribusiness and Rural Customers

Bendigo and Adelaide Bank's deep roots in regional Australia, bolstered by its Rural Bank brand, translate into a significant focus on agribusiness and rural customers. This segment is crucial, with the bank offering tailored banking solutions and lending products designed specifically for the unique needs of these communities.

The bank's commitment is evident in its substantial agribusiness lending portfolio. For the financial year 2023, Bendigo and Adelaide Bank reported a 10% increase in its agribusiness lending, reaching $10.1 billion, reflecting strong growth and confidence in the sector.

Younger, Digitally-Savvy Customers

Bendigo and Adelaide Bank's digital arm, Up, is laser-focused on attracting and retaining younger, digitally-savvy customers, primarily those aged 18 to 35. This demographic is characterized by its expectation of intuitive, mobile-first banking experiences, valuing speed and convenience above all else. Up's strategy leverages innovative digital features to meet these demands.

Up's success with this segment is evident in its rapid customer acquisition. By the end of 2023, Up had surpassed 700,000 customers, a significant portion of whom fall within this younger, digitally-native age bracket. This growth underscores the effectiveness of their digital-centric approach in resonating with a generation that grew up with smartphones and expects seamless online interactions.

- Target Demographic: Up specifically courts customers aged 18-35, a group highly comfortable with and reliant on digital platforms for their financial needs.

- Digital Experience Focus: The bank prioritizes a user-friendly, mobile-first interface, offering features like instant account opening, real-time transaction notifications, and budgeting tools designed for ease of use.

- Customer Engagement: Up engages this segment through social media, in-app messaging, and partnerships that align with younger consumers' interests, fostering a sense of community and brand loyalty.

- Market Penetration: With over 700,000 customers by the close of 2023, Up demonstrates strong penetration within the younger, digitally-oriented market segment in Australia.

Community-Oriented Customers

Community-Oriented Customers are a key segment for Bendigo and Adelaide Bank, actively choosing the bank because they value its distinct Community Bank model. This group is particularly attracted to the bank's dedication to reinvesting profits directly back into the local areas where they live and operate. Their decision to bank with Bendigo and Adelaide is often driven by a strong appreciation for the bank's social impact and its commitment to ethical banking practices, aligning their financial needs with their community values.

These customers are not just looking for financial services; they are seeking a banking partner that actively contributes to the well-being and development of their neighborhoods. This segment is loyal because they see their banking relationship as a way to directly support local initiatives and causes. For instance, in 2024, Bendigo and Adelaide Bank continued to demonstrate this commitment through various community investment programs, reflecting the tangible benefits of their model.

- Value Proposition Alignment: These customers are drawn to the bank's Community Bank model, which prioritizes local reinvestment.

- Social Impact Focus: They actively seek out and support institutions with a strong social impact and ethical banking approach.

- Community Investment: Customers appreciate that profits are channeled back into local communities, fostering local development.

- Brand Loyalty: This alignment of values often translates into strong customer loyalty and advocacy for the bank.

Bendigo and Adelaide Bank: Diverse Customer Segments, Community Core

Bendigo and Adelaide Bank serves a broad customer base, from individuals and families requiring everyday banking and lending, to SMEs needing tailored business solutions. The bank also has a dedicated focus on agribusiness through its Rural Bank brand and targets younger, digitally-native consumers with its Up digital offering.

The bank's commitment to community is a defining characteristic, attracting customers who value local reinvestment and social impact. This multifaceted approach allows Bendigo and Adelaide Bank to cater to diverse financial needs while reinforcing its community-centric ethos.

| Customer Segment | Key Characteristics | 2024/Recent Data Point |

|---|---|---|

| Individuals & Households | Everyday banking, savings, home loans, credit cards | Continued focus on digital offerings for accessibility |

| Small to Medium Enterprises (SMEs) | Business lending, deposit accounts, payment processing | Business lending grew 7.2% in H1 FY24 |

| Agribusiness | Tailored banking and lending for rural communities | Agribusiness lending reached $10.1 billion in FY23 (10% increase) |

| Digital-Native (Up) | Aged 18-35, mobile-first banking expectations | Up surpassed 700,000 customers by end of 2023 |

| Community-Oriented | Value local reinvestment and social impact | Ongoing community investment programs in 2024 |

Cost Structure

Operating Expenses

Operating expenses for Bendigo and Adelaide Bank encompass significant costs like staff salaries and wages for its workforce exceeding 7,000 employees. These costs are fundamental to maintaining the bank's extensive branch network and delivering a wide array of financial services to its customers.

In the financial year 2023, Bendigo and Adelaide Bank reported operating expenses of $1,694 million. This figure reflects the substantial investment in human capital and the infrastructure required to support its retail and business banking operations.

Technology and Digital Investment Costs

Bendigo and Adelaide Bank dedicates substantial resources to its technology and digital investment costs, a critical component of its business model. This includes significant expenditure on digital transformation initiatives, aimed at modernizing its core IT infrastructure and facilitating cloud migration. In the fiscal year 2023, the bank reported a 3.3% increase in its technology spend, reaching $562 million, reflecting this commitment to digital advancement.

Key areas of investment encompass the development of new platforms, such as the innovative Bendigo Lending Platform and the digital banking app Up. These efforts also involve substantial outlays for essential software licenses and the integration of advanced artificial intelligence (AI) tooling to enhance customer experience and operational efficiency. This forward-looking approach to technology underpins the bank's strategy to remain competitive in the evolving financial landscape.

Marketing and Brand Management Costs

Bendigo and Adelaide Bank allocates significant resources to marketing and brand management. These expenses cover broad campaigns to promote their core banking products and services, aiming to attract and retain a diverse customer base. In the fiscal year 2023, the bank reported marketing expenses of $151 million, a slight increase from the previous year, reflecting ongoing investment in customer acquisition and brand visibility.

Crucially, this cost structure also encompasses the dedicated branding efforts for their distinct sub-brands, such as the digital-first banking app Up and the heritage brand Adelaide Bank. These initiatives ensure each brand resonates with its target audience, maintaining a strong market presence and differentiating their offerings in a competitive landscape.

Regulatory and Compliance Costs

Bendigo and Adelaide Bank, as a heavily regulated financial institution, dedicates significant resources to its regulatory and compliance cost structure. These expenses are crucial for maintaining operational integrity and customer trust, ensuring adherence to evolving financial laws and robust fraud prevention protocols.

In 2024, the Australian financial sector, including banks like Bendigo and Adelaide, continued to face substantial compliance burdens. For instance, the Australian Prudential Regulation Authority (APRA) imposes rigorous capital adequacy requirements and reporting standards that necessitate ongoing investment in systems and personnel.

- Regulatory Adherence: Costs associated with meeting APRA's prudential standards, including capital management and liquidity ratios, are a significant component.

- Compliance Frameworks: Expenses for developing, implementing, and maintaining anti-money laundering (AML) and counter-terrorism financing (CTF) programs are substantial.

- Fraud Prevention: Investment in advanced technologies and operational processes to detect and prevent financial fraud is a continuous cost driver.

- Reporting and Auditing: Significant expenditure is allocated to internal and external audits, as well as the generation of detailed regulatory reports.

Property and Branch Network Costs

Bendigo and Adelaide Bank’s commitment to its physical presence, including its unique Community Bank branches, translates into significant property and branch network costs. These expenses encompass essential operational outlays like rent, utilities, regular maintenance, and security for each location. In 2024, the bank continued its strategic review of its branch and agency footprint, a process that directly influences these property-related expenditures.

The bank's approach to managing its branch network is dynamic, aiming to balance customer accessibility with cost efficiency. This ongoing assessment means that decisions regarding branch openings, closures, or consolidations are made with a keen eye on the associated property and operational costs.

- Property Expenses: Costs associated with leasing or owning physical branch locations, including rent, property taxes, and insurance.

- Operational Outlays: Day-to-day expenses such as utilities (electricity, water, internet) and general upkeep for all branches.

- Network Optimization: Ongoing investment and divestment in the branch network, influenced by performance reviews and strategic alignment, impacting overall property costs.

- Community Bank Model: Specific costs related to supporting the unique structure and operational needs of the Community Bank branches.

Unpacking a Bank's Core Cost Structure and Strategic Outlays

Bendigo and Adelaide Bank's cost structure is multifaceted, driven by its extensive operations and strategic investments. Key expenses include remuneration for its large workforce, significant technology upgrades, and robust marketing efforts to maintain brand presence. The bank also incurs substantial costs related to regulatory compliance and the upkeep of its physical branch network, including its unique Community Bank model.

| Cost Category | FY23 Expense (AUD Million) | Key Drivers | 2024 Focus |

|---|---|---|---|

| Staff Costs | (Included in Operating Expenses) | Over 7,000 employees, salaries, wages, benefits | Talent acquisition and retention |

| Technology & Digital | 562 | Digital transformation, cloud migration, new platforms (e.g., Up app) | AI integration, platform modernization |

| Marketing & Brand | 151 | Customer acquisition, brand visibility, sub-brand promotion | Targeted campaigns |

| Regulatory & Compliance | (Ongoing Investment) | APRA standards, AML/CTF, fraud prevention, reporting | Enhanced risk management systems |

| Property & Branch Network | (Operational Outlays) | Rent, utilities, maintenance, Community Bank support | Network optimization review |

Revenue Streams

Net Interest Income (NII)

Net Interest Income (NII) is Bendigo and Adelaide Bank's main way of making money. It comes from the difference between the interest they earn on loans they give out and the interest they pay on money people deposit with them. In the first half of 2024, their NII was $1.4 billion, showing the impact of their lending activities and deposit base.

Lending Fees and Charges

Bendigo and Adelaide Bank generates revenue from a variety of lending fees and charges. These include upfront loan origination fees, ongoing service fees, and other administrative charges applied to their diverse range of credit products.

This income stream is particularly significant for their home loan and business loan portfolios. For instance, in the fiscal year 2024, the bank reported substantial net interest income, a key component influenced by these lending-related fees and the interest margin on their loan book.

Account Fees and Service Charges

Bendigo and Adelaide Bank generates significant income through account fees and service charges. This includes revenue from transaction fees, monthly account keeping fees, and various other charges associated with their banking operations. For instance, in the first half of fiscal year 2024, the bank reported a 6% increase in fee and commission income, reflecting the consistent contribution of these revenue streams.

Wealth Management Fees

Bendigo and Adelaide Bank earns revenue from its wealth management division by offering a suite of financial services. These include personalized financial planning, a variety of investment products, superannuation solutions, and comprehensive funds management. Revenue is typically generated through a combination of advisory fees, which are often a percentage of assets under management, and commissions earned on the sale of specific financial products.

For the fiscal year 2024, the bank's wealth management segment demonstrated significant contribution to its overall financial performance. For instance, the total revenue generated from wealth management services reached approximately AUD 450 million, reflecting strong client engagement and the successful deployment of its advisory and product offerings.

- Advisory Fees: Charged as a percentage of assets under management, providing recurring revenue.

- Commissions: Earned on the sale of investment products and insurance.

- Funds Management: Fees collected for managing investment portfolios and superannuation funds.

- Superannuation Services: Revenue derived from administering and managing superannuation accounts.

Other Income

Bendigo and Adelaide Bank’s other income streams are quite varied, contributing to its overall financial health beyond traditional lending. These include revenue generated from card and payment services, which is a significant area for many financial institutions. Treasury operations also play a role, managing the bank's liquidity and investments to generate returns.

Furthermore, foreign exchange services provide income through currency conversions and related transactions. The bank may also derive income from strategic partnerships or joint ventures, leveraging collaborations to access new markets or services. For instance, in the first half of fiscal year 2024, Bendigo and Adelaide Bank reported other operating income of $253 million, demonstrating the importance of these diverse revenue streams.

- Card and Payment Services: Income generated from transaction fees, interchange fees, and other payment processing activities.

- Treasury Operations: Returns from managing the bank's own funds, including investments and liquidity management.

- Foreign Exchange Services: Revenue earned from facilitating currency exchange for customers and managing currency exposures.

- Joint Ventures and Partnerships: Income derived from collaborative business arrangements and strategic alliances.

Bank's Diverse Revenue Streams: Key Figures Revealed!

Bendigo and Adelaide Bank also generates revenue from fees and commissions across its operations. This includes income from transaction processing, account management, and other service charges. For the first half of fiscal year 2024, fee and commission income rose by 6%, highlighting the steady contribution of these revenue sources.

The bank's wealth management division is another key revenue generator. It offers financial planning, investment products, and superannuation services, earning revenue through advisory fees and commissions. In fiscal year 2024, this segment contributed approximately AUD 450 million in revenue.

Additionally, Bendigo and Adelaide Bank benefits from other income streams, such as card and payment services, treasury operations, and foreign exchange. In the first half of fiscal year 2024, other operating income amounted to $253 million, underscoring the diversification of its earnings.

| Revenue Stream | Description | FY24 Contribution (Approx.) |

|---|---|---|

| Net Interest Income | Interest earned on loans minus interest paid on deposits. | $1.4 billion (H1 2024) |

| Fees and Commissions | Charges for banking services, transactions, and account management. | 6% increase (H1 2024) |

| Wealth Management | Revenue from financial planning, investments, and superannuation. | AUD 450 million (FY24) |

| Other Income | Card services, treasury, foreign exchange, partnerships. | $253 million (H1 2024) |

Business Model Canvas Data Sources

The Bendigo & Adelaide Bank Business Model Canvas is built using a combination of internal financial disclosures, comprehensive market research reports, and strategic insights derived from industry analysis. This ensures each component of the canvas is grounded in verifiable data and current market realities.