Banco do Brasil Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Banco do Brasil

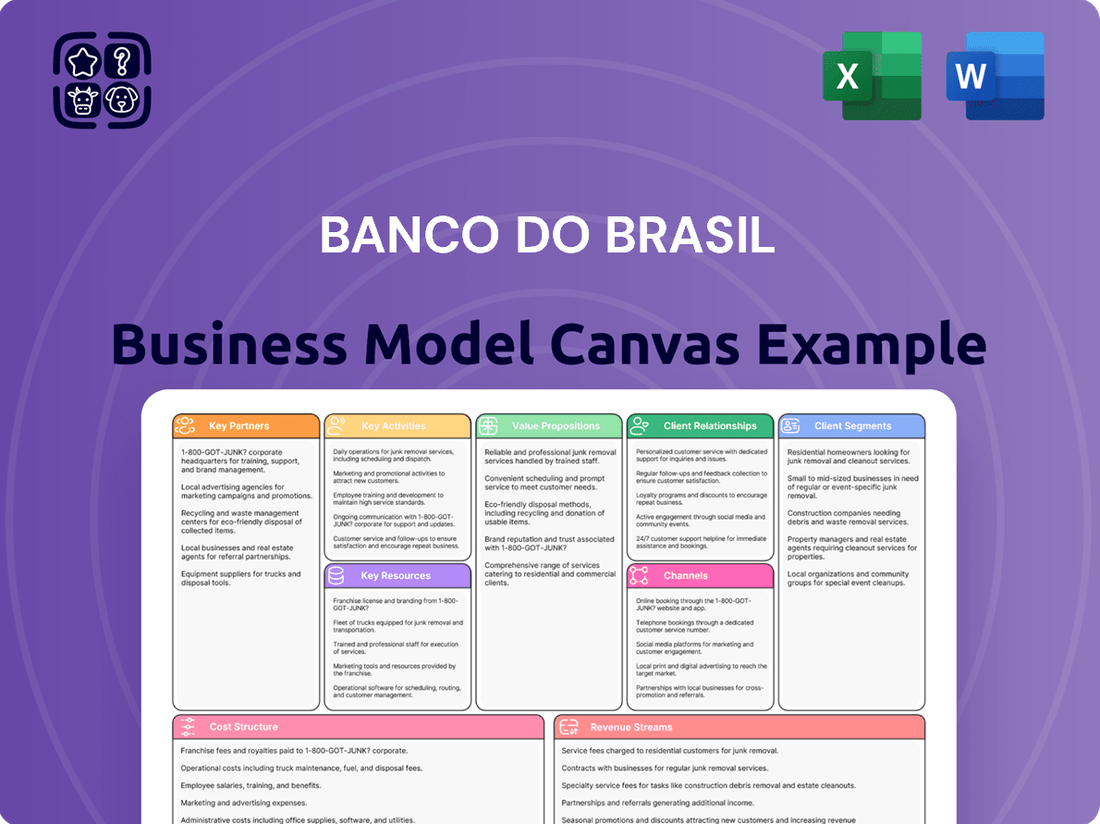

Banco do Brasil: Business Model Canvas Unveiled

Unlock the strategic blueprint behind Banco do Brasil’s success with our comprehensive Business Model Canvas. This detailed breakdown reveals how they serve diverse customer segments and leverage key partnerships to deliver unique value propositions. Discover their revenue streams and cost structures to inform your own strategic planning.

Partnerships

Technology and Fintech Companies

Banco do Brasil's strategic alliances with technology and fintech companies are fundamental to its digital evolution. These partnerships are vital for developing sophisticated online banking services, efficient payment systems, and novel financial offerings. For instance, in 2024, the bank continued to invest heavily in digital channels, aiming to onboard millions of new users to its digital platforms, a strategy heavily reliant on fintech collaborations.

These collaborations significantly boost the bank's digital prowess and elevate the customer experience through state-of-the-art platforms. By integrating emerging technologies, Banco do Brasil ensures it remains a strong competitor in the fast-paced digital financial sector. This focus on technological integration allows for the rapid deployment of new features and services, directly impacting customer satisfaction and market share.

Insurance Companies

Banco do Brasil's collaborations with insurance companies are crucial for expanding its financial product offerings. These partnerships enable the bank to provide a comprehensive suite of insurance options, such as life, health, and property coverage, directly to its vast customer base.

These alliances foster significant cross-selling opportunities, allowing Banco do Brasil to deepen customer relationships and increase revenue streams. By integrating insurance products, the bank diversifies its portfolio beyond traditional banking services, offering customers a more holistic financial protection solution under a single, trusted brand.

Government Agencies and Public Sector Entities

Banco do Brasil's partnerships with government agencies are fundamental. For instance, in 2023, the bank managed R$175.9 billion in public funds, a significant portion of which supported social programs and national development. These collaborations are crucial for facilitating credit for agribusiness, a key sector for Brazil's economy, with the bank disbursing R$106.7 billion in agricultural credit in the 2023/2024 harvest plan.

These relationships allow Banco do Brasil to play a pivotal role in executing government policies, from disbursing social benefits like Bolsa Família to financing large-scale infrastructure projects. This deep integration solidifies the bank's position as a key instrument for national economic growth and social inclusion.

Payment Networks and Processors

Banco do Brasil's key partnerships with payment networks and processors, such as Visa and Mastercard, are absolutely vital. These alliances ensure that credit and debit card transactions are processed securely and efficiently, which is the backbone of everyday banking for millions. Without these relationships, the bank simply couldn't facilitate the vast number of payments that occur daily.

These collaborations are more than just operational; they directly impact customer experience and the bank's reach. By integrating with major networks, Banco do Brasil guarantees widespread acceptance of its cards, making it easier for customers to use their services anywhere. This seamless processing is fundamental to maintaining customer loyalty and attracting new clients.

- Visa and Mastercard Partnerships: Facilitate global transaction processing for credit and debit cards.

- Local Payment Processors: Ensure smooth integration with Brazil's domestic payment infrastructure.

- Transaction Volume: In 2023, Banco do Brasil processed over R$2.5 trillion in credit and debit card transactions, highlighting the scale of these partnerships.

- Security and Efficiency: These networks provide the technological backbone for secure and rapid transaction settlements.

International Financial Institutions

Banco do Brasil's strategic alliances with international financial institutions are crucial for its global operations. These partnerships enable seamless cross-border transactions and bolster trade finance capabilities, directly benefiting clients engaged in international commerce. For instance, in 2024, Banco do Brasil continued to leverage its network of correspondent banks to facilitate an estimated $50 billion in international trade finance transactions, a significant portion of its global business volume.

These collaborations are instrumental in expanding Banco do Brasil's global footprint, offering its corporate and individual customers enhanced access to international investment opportunities and banking services. By fostering these relationships, the bank effectively bridges geographical divides, making international business more accessible and manageable for its clientele. This strategic approach supports the financial needs of a globally-minded customer base.

- Facilitating Global Trade: Partnerships with institutions like the European Bank for Reconstruction and Development (EBRD) and various development finance institutions (DFIs) in 2024 helped Banco do Brasil extend credit lines for sustainable projects and SMEs in emerging markets.

- Expanding Investment Horizons: Alliances with major international investment banks provide clients with access to a wider array of global capital markets and investment products, supporting diversification and wealth management strategies.

- Cross-Border Transaction Efficiency: Through agreements with global payment networks and international banks, Banco do Brasil ensures efficient and cost-effective execution of international payments and remittances for its customers.

Strategic Alliances: Powering Digital Evolution and Broadening Impact

Banco do Brasil's key partnerships with fintech and technology firms are central to its digital transformation strategy. These collaborations are essential for developing advanced digital banking solutions and payment systems, with significant investments in 2024 aimed at expanding its digital customer base through these alliances.

These alliances enhance the bank's technological capabilities and customer experience by integrating cutting-edge technologies, ensuring competitiveness in the digital finance sector. This focus on tech integration allows for rapid service deployment, directly impacting customer satisfaction and market position.

The bank's collaborations with insurance providers are vital for broadening its product portfolio, offering a wide range of insurance options to its extensive customer base. These partnerships create substantial cross-selling opportunities, deepening client relationships and diversifying revenue streams beyond traditional banking.

Banco do Brasil's partnerships with government entities are fundamental, particularly in supporting social programs and national development. In 2023, the bank managed R$175.9 billion in public funds and disbursed R$106.7 billion in agricultural credit, underscoring its role in executing national economic and social policies.

Critical partnerships with payment networks like Visa and Mastercard ensure secure and efficient transaction processing for millions of customers. These alliances are fundamental to the bank's daily operations and customer experience, guaranteeing widespread card acceptance and fostering client loyalty.

Strategic alliances with international financial institutions are crucial for Banco do Brasil's global reach, facilitating cross-border transactions and trade finance. In 2024, the bank leveraged its correspondent banking network to support an estimated $50 billion in international trade finance, expanding its global footprint and offering clients access to international markets.

| Partnership Type | Key Collaborators | 2023/2024 Impact | Strategic Importance |

| Fintech & Technology | Various tech startups and fintech firms | Millions of new digital users onboarded; enhanced digital service offerings. | Digital transformation, innovation, customer experience. |

| Insurance Companies | Major insurance providers | Expanded product suite, increased cross-selling opportunities. | Revenue diversification, holistic financial solutions. |

| Government Agencies | Brazilian government ministries and agencies | Managed R$175.9 billion in public funds; R$106.7 billion in agricultural credit (2023/2024 harvest plan). | Policy execution, social programs, agribusiness support, national development. |

| Payment Networks | Visa, Mastercard, local processors | Processed over R$2.5 trillion in credit/debit card transactions (2023). | Transaction security, efficiency, customer reach. |

| International Financial Institutions | Global banks, development finance institutions | Facilitated ~$50 billion in international trade finance (2024 estimate). | Global operations, cross-border transactions, trade finance expansion. |

What is included in the product

A comprehensive overview of Banco do Brasil's business model, detailing its customer segments, value propositions, and revenue streams within the 9 classic BMC blocks.

Reflects Banco do Brasil's strategy and operations, offering insights for informed decision-making and analysis of competitive advantages.

Banco do Brasil's Business Model Canvas offers a clear, one-page snapshot to identify and address key operational inefficiencies, streamlining complex financial processes.

It provides a structured framework to pinpoint and resolve challenges within Banco do Brasil's diverse service offerings, facilitating strategic improvements.

Activities

Retail and Corporate Banking Operations

Retail and corporate banking operations are central to Banco do Brasil's business model, focusing on managing a vast array of deposit accounts and facilitating seamless payment processing for millions of Brazilians. This includes offering a comprehensive suite of loans, from mortgages for individuals to essential working capital financing for businesses, directly addressing the financial needs of diverse customer segments.

In 2024, Banco do Brasil continued to be a major player in these core activities, processing trillions of Brazilian Reais in transactions and managing a substantial loan portfolio. The bank's extensive network of branches and digital channels ensures accessibility for both individual savers and large corporations seeking credit and transactional services.

Investment Management and Advisory Services

Banco do Brasil actively manages a diverse range of investment funds, providing clients with access to various asset classes. In 2024, the bank continued to offer personalized wealth management advice, helping individuals and institutions navigate complex financial markets to achieve their growth objectives. This includes providing expert guidance on tailored investment strategies.

The bank's brokerage services facilitate transactions across a wide spectrum of financial instruments, ensuring clients have the tools to execute their investment plans efficiently. This comprehensive approach supports both individual investors aiming for personal financial security and institutional clients seeking robust asset growth.

Digital Transformation and Technology Development

Banco do Brasil actively pursues the continuous development and enhancement of its digital platforms, including its mobile banking applications and robust cybersecurity measures, to meet the evolving needs of its modern customer base.

In 2024, the bank continued its significant investments in new technologies aimed at improving operational efficiency, bolstering security protocols, and elevating the overall user experience across all customer touchpoints.

This strategic focus on digital innovation is paramount for maintaining Banco do Brasil's competitive edge in an increasingly digitized financial landscape.

Risk Management and Compliance

Banco do Brasil actively engages in robust risk assessment frameworks, a cornerstone of its operations. This includes meticulously managing credit, market, and operational risks to safeguard its financial health. For instance, as of Q1 2024, the bank reported a Non-Performing Loans (NPL) ratio of 2.27%, demonstrating its ongoing efforts in credit risk mitigation.

Ensuring strict adherence to regulatory compliance is a critical key activity. This encompasses navigating complex banking regulations, enforcing anti-money laundering (AML) laws, and aligning with international financial standards. In 2023, Banco do Brasil continued to invest in technology and training to bolster its compliance infrastructure.

Effective risk management is paramount for protecting the bank's assets and its esteemed reputation. This proactive approach allows Banco do Brasil to maintain stability and stakeholder confidence in a dynamic financial landscape.

- Risk Assessment: Implementing comprehensive frameworks to identify, measure, and monitor all forms of risk.

- Regulatory Compliance: Adhering to national and international banking laws, including AML and KYC (Know Your Customer) regulations.

- Credit Risk Management: Maintaining a low Non-Performing Loans (NPL) ratio, which stood at 2.27% in Q1 2024.

- Market and Operational Risk: Developing strategies to mitigate volatility in financial markets and prevent operational failures.

Branch Network Management and Expansion

Banco do Brasil actively manages and optimizes its vast physical branch network, a cornerstone for serving customers who value face-to-face interactions. This involves ensuring efficient operations and customer satisfaction across its existing locations.

The bank also pursues strategic expansion of its branch presence into new domestic regions and select international markets. This expansion is designed to capture new customer segments and support the bank's overall growth objectives, balancing traditional reach with evolving customer needs.

- Network Optimization: Focus on enhancing the efficiency and customer experience within the existing 4,000+ branches across Brazil.

- Strategic Expansion: Identify and develop new branch locations in underserved domestic areas and key international financial centers.

- Digital Integration: Ensure branches complement digital banking channels, offering a hybrid service model.

- Market Reach: Maintain a strong physical presence to cater to diverse customer preferences and ensure broad accessibility.

Banking's Core: Digital Evolution, Risk Management, Network Reach

Banco do Brasil's key activities revolve around providing a comprehensive suite of financial services, from retail and corporate banking to wealth management and brokerage. The bank actively manages its extensive branch network, balancing physical presence with significant investments in digital innovation and robust risk management frameworks. This multifaceted approach ensures broad customer accessibility and operational resilience.

| Key Activity | Description | 2024 Data/Focus |

|---|---|---|

| Banking Operations | Retail and corporate banking, including deposits, loans, and payment processing. | Continued to process trillions of Brazilian Reais in transactions; managed a substantial loan portfolio. |

| Investment & Wealth Management | Offering investment funds and personalized wealth management advice. | Provided tailored investment strategies to individuals and institutions. |

| Digital Transformation | Developing and enhancing digital platforms and cybersecurity. | Significant investments in technology to improve efficiency and user experience. |

| Risk Management & Compliance | Assessing and mitigating credit, market, and operational risks; adhering to regulations. | Maintained a Non-Performing Loans (NPL) ratio of 2.27% in Q1 2024; invested in compliance infrastructure. |

| Network Management | Optimizing and strategically expanding its physical branch network. | Focus on enhancing over 4,000+ branches and exploring new domestic and international locations. |

Full Version Awaits

Business Model Canvas

The Banco do Brasil Business Model Canvas you are previewing is the exact document you will receive upon purchase. This comprehensive overview is not a sample or a mockup; it represents the complete analysis of Banco do Brasil's strategic framework, ready for your immediate use. Upon completing your transaction, you will gain full access to this detailed document, allowing you to explore and utilize its insights without any alteration from what you currently see.

Resources

Extensive Branch and ATM Network

Banco do Brasil's extensive branch and ATM network is a cornerstone of its business model, offering unparalleled accessibility across Brazil and beyond. This physical presence is crucial for serving customers in areas with lower digital adoption, acting as a vital hub for traditional banking, customer service, and cash management. As of the first quarter of 2024, Banco do Brasil operated approximately 3,600 branches and over 15,000 ATMs, solidifying its position as a key financial infrastructure provider.

This vast network represents a significant physical asset and a powerful competitive differentiator. It facilitates a broad range of customer interactions, from routine transactions to more complex financial advice, reinforcing customer loyalty and trust. The sheer scale of this infrastructure allows Banco do Brasil to capture a wide customer base, including those who prefer or require in-person banking services.

Advanced Digital Banking Platforms

Banco do Brasil's advanced digital banking platforms, including robust online systems and mobile applications, are crucial for customer engagement and efficient service delivery. These platforms allow customers to manage accounts and conduct transactions conveniently, anytime and anywhere.

In 2024, the bank continued to invest heavily in these digital capabilities, aiming to enhance user experience and expand its digital service offerings. This focus is driven by the increasing demand for seamless digital interactions and the need to remain competitive in the evolving financial landscape.

Human Capital and Expertise

Banco do Brasil relies on a vast team of over 80,000 employees, a significant portion of whom are highly skilled professionals. This includes financial advisors, IT specialists, risk managers, and customer service representatives, all crucial for delivering top-tier banking services and maintaining client trust.

The collective expertise of this workforce is the engine behind the bank's innovation, operational efficiency, and the cultivation of robust customer relationships. For instance, their deep understanding of financial markets allows Banco do Brasil to offer tailored investment advice, a key differentiator.

Continuous investment in employee training and development is a cornerstone of Banco do Brasil's strategy. This commitment ensures their staff remains at the forefront of industry knowledge and technological advancements, enabling them to adapt to evolving market demands and regulatory landscapes.

Strong Brand Reputation and Customer Trust

Banco do Brasil's strong brand reputation and customer trust, cultivated over decades of operation, are cornerstones of its business model. This deep-rooted presence in the Brazilian market translates into significant customer loyalty and a powerful competitive advantage. In 2024, this intangible asset continues to be a critical driver for customer acquisition and retention.

This accumulated goodwill signifies reliability and a proven track record, making Banco do Brasil a preferred choice for millions of Brazilians. The bank's long-standing history directly contributes to its perceived stability and trustworthiness in the financial landscape.

- Decades of operation in Brazil have solidified Banco do Brasil's market position.

- High customer trust is a direct result of consistent service and reliability.

- Brand reputation acts as a significant barrier to entry for competitors.

- Customer loyalty is a key factor in the bank's sustained profitability.

Robust Capital Base and Liquidity

Banco do Brasil's robust capital base and liquidity are critical enablers for its extensive lending operations, allowing it to absorb potential financial shocks and meet stringent regulatory demands. This strong financial footing is essential for the bank's stability and its ability to expand its service offerings and market reach.

A solid capital position directly supports the bank's capacity to underwrite new loans and manage risk effectively. As of the first quarter of 2024, Banco do Brasil reported a Basel III Common Equity Tier 1 (CET1) ratio of 12.5%, comfortably above the regulatory minimums, demonstrating its substantial financial strength.

- Capital Adequacy: Maintaining high capital ratios, such as the CET1 ratio, ensures the bank can absorb unexpected losses without jeopardizing its solvency.

- Liquidity Management: Adequate liquidity buffers allow the bank to meet its short-term obligations, including deposit withdrawals and loan disbursements, even during periods of market stress.

- Growth Capacity: A strong financial foundation provides the necessary resources for strategic investments, technological advancements, and expansion into new markets or product lines.

Core Assets: Fueling a Financial Powerhouse's Stability and Growth

Banco do Brasil's extensive physical network, comprising branches and ATMs, forms a vital part of its key resources. This infrastructure ensures broad customer accessibility, particularly in regions with lower digital adoption. As of Q1 2024, the bank operated approximately 3,600 branches and over 15,000 ATMs, highlighting its significant physical footprint.

The bank's advanced digital platforms, including its online banking and mobile applications, are critical for customer engagement and efficient service delivery. These digital tools allow for seamless management of accounts and transactions, catering to the growing demand for convenient, anytime-anywhere banking.

Banco do Brasil's workforce, exceeding 80,000 employees, represents a core asset, with many possessing specialized skills in finance, IT, and risk management. This human capital is essential for driving innovation, ensuring operational efficiency, and fostering strong client relationships, with ongoing investment in training to maintain expertise.

The bank's strong brand reputation and the trust it has cultivated over decades are invaluable intangible assets. This deep-rooted market presence translates into significant customer loyalty and a powerful competitive advantage, as evidenced by its continued appeal to millions of Brazilians in 2024.

A robust capital base and strong liquidity are fundamental enablers for Banco do Brasil's lending operations and risk management. The bank's substantial financial strength, demonstrated by a Q1 2024 CET1 ratio of 12.5%, ensures stability and supports its capacity for growth and strategic investment.

| Key Resource | Description | Q1 2024 Data/Significance |

|---|---|---|

| Physical Network | Extensive branch and ATM presence | Approx. 3,600 branches, 15,000+ ATMs |

| Digital Platforms | Online and mobile banking services | Continuous investment for enhanced user experience |

| Human Capital | Skilled workforce of over 80,000 employees | Expertise in finance, IT, risk management; ongoing training |

| Brand Reputation & Trust | Decades of cultivated customer loyalty | Key competitive advantage and customer acquisition driver |

| Capital & Liquidity | Strong financial foundation for operations | CET1 Ratio: 12.5% (Q1 2024), ensuring stability and growth capacity |

Value Propositions

Comprehensive Financial Solutions

Banco do Brasil provides a full spectrum of financial services, encompassing everything from everyday checking and savings accounts to a wide array of credit options, sophisticated investment vehicles, insurance policies, and dedicated asset management. This integrated approach acts as a financial hub for its clientele.

By offering this extensive range of products and services under one roof, Banco do Brasil simplifies financial management for its customers, allowing them to address diverse needs efficiently. This consolidation streamlines how individuals, businesses, and even governmental entities handle their finances.

In 2024, Banco do Brasil continued to solidify its position as a comprehensive financial provider. For instance, its loan portfolio expanded, reflecting a strong demand across various sectors, and its investment banking arm facilitated significant capital market transactions, demonstrating the breadth of its capabilities.

Extensive Accessibility and Reach

Banco do Brasil's extensive accessibility is a cornerstone of its business model, ensuring banking services reach a broad spectrum of the population. In 2024, the bank maintained a significant physical footprint with thousands of branches and ATMs across Brazil, providing crucial access points, especially in underserved regions. This physical network is powerfully complemented by its advanced digital platforms, offering customers seamless transactions and account management through mobile apps and online banking, effectively bridging traditional and digital access.

Trusted and Secure Banking

Banco do Brasil’s commitment to trusted and secure banking is paramount, built on its long-standing reputation as a stable financial institution. This reliability ensures customers feel confident their funds and sensitive data are protected.

Adherence to stringent regulatory frameworks, including those updated through 2024, and significant investments in advanced cybersecurity measures are key to fostering this trust. For instance, in 2023, Banco do Brasil reported a substantial increase in its cybersecurity budget to combat evolving digital threats.

This unwavering focus on security is not just a operational necessity but a core value proposition that underpins every customer interaction and transaction, solidifying its position as a dependable financial partner.

Tailored Solutions for Diverse Segments

Banco do Brasil crafts distinct financial products and services to cater to the specific requirements of individuals, small and medium-sized enterprises (SMEs), large corporations, and government bodies. This approach ensures offerings are highly relevant, tackling the particular financial hurdles and prospects each segment faces.

This segmentation highlights the bank's keen insight into the diverse needs of its customer base, enabling the development of tailored solutions. For instance, in 2024, Banco do Brasil continued to expand its digital platforms, offering specialized credit lines for SMEs and investment advisory services for high-net-worth individuals.

- Individual Segment: Offering personalized banking, credit, and investment products, including tailored mortgage solutions and digital wealth management tools.

- SME Segment: Providing specialized credit facilities, working capital solutions, and digital tools designed to streamline business operations and growth.

- Corporate Segment: Delivering comprehensive financial services, including corporate finance, trade finance, and sophisticated treasury management solutions.

- Government Segment: Supporting public sector entities with financial management, infrastructure financing, and public service payment solutions.

Innovation in Digital Services

Banco do Brasil's commitment to innovation in digital services is evident through its continuous investment in digital transformation. This includes enhancing its advanced mobile banking, robust online platforms, and seamless payment solutions, all designed to provide customers with unparalleled convenience and efficiency. In 2023, the bank reported a significant increase in digital transactions, with over 70% of its customer base actively using digital channels, underscoring the success of these initiatives in delivering modern banking experiences.

These digital innovations streamline internal processes and significantly enhance the overall user experience. By focusing on technological advancement, Banco do Brasil ensures it remains highly competitive in the rapidly evolving digital landscape. For instance, its investments in AI-powered customer service bots have led to a notable reduction in average response times, improving customer satisfaction metrics.

- Digital Transformation Investment: Banco do Brasil continues to prioritize significant capital allocation towards digital infrastructure and service development.

- Enhanced Customer Experience: Innovations aim to deliver convenience, efficiency, and modern banking functionalities through mobile and online platforms.

- Competitive Edge: These advancements are crucial for maintaining market leadership and adapting to the digital demands of customers.

- Operational Efficiency: Streamlining processes via digital solutions contributes to improved operational performance and cost management.

Integrated Banking: Accessible, Trusted, Tailored Solutions

Banco do Brasil's value proposition centers on being a comprehensive, accessible, and trusted financial partner. It simplifies financial management by offering a wide array of integrated services, from basic accounts to complex investments and insurance, acting as a one-stop financial hub. This broad offering streamlines how individuals, businesses, and government entities manage their diverse financial needs efficiently.

Accessibility is key, with a robust physical network of branches and ATMs, particularly in underserved areas, complemented by advanced digital platforms. This dual approach ensures seamless transactions and account management, bridging traditional and digital banking. In 2024, the bank maintained its extensive reach, solidifying its role as a vital financial service provider across Brazil.

Trust is built on a long-standing reputation for stability and significant investments in cybersecurity, with a notable increase in its cybersecurity budget reported in 2023. This commitment to security, alongside adherence to evolving regulations, ensures customer confidence in the protection of their funds and data, making it a dependable financial ally.

The bank also excels at tailoring solutions for distinct customer segments, including individuals, SMEs, corporations, and government bodies. In 2024, this included specialized credit lines for SMEs and advanced digital wealth management for high-net-worth individuals, demonstrating a deep understanding of varied market needs.

Customer Relationships

Personalized Relationship Management

Banco do Brasil employs dedicated relationship managers for its high-value clients and corporate customers. This personalized approach ensures that advice and services are specifically tailored to the unique needs of these segments, fostering deeper engagement.

For instance, in 2023, the bank reported a significant portion of its revenue derived from its corporate and agribusiness segments, highlighting the importance of these specialized relationship management efforts. This human-centric model provides a crucial element of trust and understanding in complex financial transactions.

Digital Self-Service and Support

Banco do Brasil enhances customer relationships through robust digital self-service, offering online banking, mobile applications, and AI-powered chatbots. This allows clients to effortlessly manage accounts, conduct transactions, and find solutions to common queries 24/7, aligning with a growing demand for digital autonomy and immediate assistance.

In 2024, Banco do Brasil reported a significant increase in digital channel usage, with over 60% of customer interactions occurring through its app and website. This digital-first approach not only provides unparalleled convenience but also allows the bank to scale support efficiently, handling millions of routine requests without direct human intervention.

Community Engagement and Social Responsibility

Banco do Brasil actively fosters community engagement through initiatives supporting local development and agriculture, a strategy that significantly strengthens customer loyalty. For instance, in 2024, the bank continued its strong support for the National Program for Strengthening Family Agriculture (Pronaf), channeling billions of reais to family farmers, thereby deepening its connection with a crucial segment of the population.

This dedication to social responsibility is more than just good practice; it translates into enhanced brand perception and builds trust that extends beyond typical banking transactions. By aligning with societal values, Banco do Brasil cultivates a positive image, as evidenced by its consistent recognition in sustainability and social impact rankings throughout 2024.

Call Center and Branch-Based Support

Banco do Brasil's call centers and branches remain crucial for customer interaction, offering human-driven support for inquiries and complex issues. In 2024, the bank continued to invest in these channels to ensure accessibility, particularly for customers who prefer or require face-to-face or direct voice assistance, complementing its digital offerings.

These traditional touchpoints are vital for building trust and resolving nuanced financial needs. For instance, Banco do Brasil's extensive network, with thousands of branches across Brazil, provides a tangible presence that reassures customers. This physical footprint is augmented by a robust call center infrastructure designed to handle a high volume of calls efficiently, aiming for quick resolution times and customer satisfaction.

- Branch Network: Maintains a significant physical presence across Brazil, offering in-person services.

- Call Center Operations: Provides direct voice support for customer service and problem resolution.

- Hybrid Approach: Integrates traditional channels with digital platforms for comprehensive customer support.

- Accessibility: Ensures customers have multiple avenues for assistance, catering to diverse preferences and needs.

Feedback Mechanisms and Continuous Improvement

Banco do Brasil actively gathers customer insights through various channels, including satisfaction surveys, feedback forms, and direct communication lines like its ombudsman service. This constant dialogue allows the bank to pinpoint areas for improvement and tailor its offerings. For instance, in 2024, the bank reported a significant increase in digital channel adoption, partly driven by feedback that highlighted the need for more intuitive online banking experiences.

This commitment to continuous improvement is evident in the bank's product development cycle. By analyzing customer feedback, Banco do Brasil can identify emerging needs and adapt its financial products and services accordingly. This proactive strategy ensures the bank remains competitive and responsive to evolving market demands, fostering stronger customer loyalty.

- Customer Feedback Channels: Surveys, online forms, dedicated call centers, and social media monitoring are key to understanding customer sentiment.

- Data-Driven Enhancements: Feedback analysis informs service upgrades, such as improved mobile app features or streamlined loan application processes, as seen with the bank's 2024 digital service enhancements.

- Proactive Engagement: Regularly soliciting and acting upon customer input demonstrates a dedication to meeting and exceeding expectations.

- Impact on Loyalty: A responsive approach to customer concerns directly contributes to increased satisfaction and retention rates.

Forging Deep Customer Relationships: Digital, Personal, Community

Banco do Brasil cultivates strong customer relationships through a multi-faceted approach, blending personalized human interaction with advanced digital solutions and community engagement. This strategy ensures a broad reach and deep connection across diverse customer segments.

The bank's commitment to its customers is reflected in its ongoing investments in both digital accessibility and physical presence. In 2024, Banco do Brasil saw over 60% of customer interactions shift to digital channels, a testament to the convenience offered by its mobile app and online banking platforms. Simultaneously, its extensive branch network and dedicated call centers continued to provide essential human support, particularly for complex needs.

Furthermore, Banco do Brasil actively fosters loyalty through community initiatives and by actively soliciting and acting on customer feedback. This dedication to understanding and responding to customer needs, as demonstrated by its continued support for programs like Pronaf in 2024, solidifies its position as a trusted financial partner.

| Customer Relationship Channel | Key Features | 2024 Impact/Data |

|---|---|---|

| Relationship Managers | Personalized service for high-value and corporate clients | Crucial for complex transactions and tailored advice |

| Digital Channels (App, Online) | 24/7 self-service, AI chatbots | Over 60% of customer interactions; high adoption rate |

| Branch Network | In-person assistance, physical presence | Thousands of branches across Brazil, vital for trust and accessibility |

| Call Centers | Direct voice support, problem resolution | High volume handling, focus on quick resolution times |

| Community Engagement | Support for local development, agriculture (e.g., Pronaf) | Strengthens loyalty and brand perception |

| Feedback Mechanisms | Surveys, feedback forms, ombudsman | Drives service improvements and product development |

Channels

Extensive Branch Network

Banco do Brasil leverages its extensive branch network as a cornerstone of its customer relationships, acting as primary hubs for complex transactions and personalized financial advice. These physical locations are crucial for customers who value face-to-face interactions, fostering trust and accessibility, especially in areas with lower digital penetration. As of early 2024, Banco do Brasil maintained a significant physical presence, with thousands of branches and service points across Brazil, underscoring their commitment to a hybrid service model that caters to diverse customer needs.

Digital Banking Platforms (Web and Mobile)

Banco do Brasil's digital banking platforms, encompassing both web portals and mobile applications, serve as a cornerstone for customer interaction and service delivery. These channels provide round-the-clock access to essential banking functions like account management, bill payments, and fund transfers, meeting the demand for convenience and self-service. By the end of 2023, Banco do Brasil reported a significant increase in digital transactions, with its mobile app alone facilitating millions of operations monthly, underscoring the critical role these platforms play in reaching and serving its vast customer base efficiently.

ATM Network

Banco do Brasil's extensive ATM network, boasting over 43,000 machines across Brazil as of early 2024, serves as a cornerstone for customer convenience. These machines facilitate essential banking tasks like cash withdrawals, deposits, and balance checks, offering a vital touchpoint for transactional needs.

This widespread ATM presence ensures accessibility to basic financial services, acting as a critical bridge between physical branch operations and the bank's expanding digital channels. It directly addresses the need for immediate cash access and routine banking, supporting a broad customer base.

Call Centers and Contact Centers

Banco do Brasil's call centers and contact centers serve as crucial channels for direct customer interaction, offering everything from routine inquiries to urgent problem resolution. These centers are vital for providing a human touch when digital channels fall short, ensuring customers can access support and information efficiently.

In 2024, Banco do Brasil continued to invest in its contact center infrastructure to handle a massive volume of customer interactions. For instance, the bank reported handling millions of calls annually, with a significant portion related to account management, credit operations, and digital banking support. This human-centric approach complements their digital offerings, ensuring comprehensive customer service.

- Customer Service: Providing support for a broad spectrum of banking needs.

- Technical Assistance: Helping customers navigate and resolve issues with digital platforms.

- Information Dissemination: Answering queries about products, services, and account details.

- Urgent Matter Resolution: Offering immediate assistance for time-sensitive banking requirements.

Strategic Partnerships and Agents

Banco do Brasil strategically leverages its network of third-party agents and correspondents to significantly broaden its service reach. These partnerships are crucial for extending access to essential financial services, particularly in areas where a traditional branch presence might be limited.

These collaborations enable the bank to offer a wider array of services, such as facilitating bill payments and providing microfinance solutions through established local businesses. This approach allows Banco do Brasil to penetrate new markets more efficiently and cater to specific customer needs with specialized offerings, thereby expanding its overall distribution ecosystem.

- Extended Reach: Partnerships with over 6,000 correspondents across Brazil in 2024 significantly boosted financial inclusion, particularly in rural and underserved regions.

- Service Diversification: Through these channels, Banco do Brasil processed an estimated 50 million bill payments and facilitated over 2 million microcredit disbursements in the first half of 2024.

- Market Penetration: These strategic alliances allow the bank to tap into new customer segments and geographic areas, enhancing its competitive position in the Brazilian financial market.

Multifaceted Channels: Driving Accessibility and Financial Inclusion

Banco do Brasil's channels are a multifaceted approach to customer engagement, blending traditional and digital methods. The bank’s extensive physical branch network, alongside a robust ATM infrastructure exceeding 43,000 machines as of early 2024, ensures widespread accessibility for essential banking needs.

Digital platforms, including its mobile app and web portals, facilitate millions of monthly transactions, highlighting their importance for convenience and self-service. Furthermore, contact centers and a network of over 6,000 third-party agents in 2024 extend the bank's reach, offering crucial support and enabling services like bill payments and microcredit disbursements, thereby enhancing financial inclusion.

| Channel | Key Function | 2024 Data/Significance |

|---|---|---|

| Physical Branches | Complex transactions, personalized advice | Thousands of locations, supporting hybrid model |

| Digital Platforms (Web/App) | Account management, payments, transfers | Millions of monthly operations, increasing digital transactions |

| ATM Network | Cash withdrawals, deposits, balance checks | Over 43,000 machines, ensuring transactional accessibility |

| Contact Centers | Customer support, issue resolution | Handling millions of calls annually, providing human-centric support |

| Third-Party Agents | Bill payments, microfinance, extended reach | Over 6,000 correspondents, processing ~50M bill payments (H1 2024) |

Customer Segments

Individual Retail Customers

Banco do Brasil's individual retail customers represent a vast and varied group, encompassing everyone from everyday consumers needing basic transaction accounts and credit cards to high-net-worth individuals looking for sophisticated wealth management and tailored investment strategies. This segment is the bedrock of the bank's operations, serving a wide spectrum of financial needs, including mortgages, personal loans, and insurance products.

In 2024, Banco do Brasil continued to serve millions of individual clients across Brazil. The bank’s retail segment is crucial, with a significant portion of its revenue typically generated from fees and interest income derived from this customer base. For instance, as of the first quarter of 2024, the bank reported a substantial number of active current and savings accounts held by individuals, underscoring their broad reach.

Small and Medium-sized Enterprises (SMEs)

Small and Medium-sized Enterprises (SMEs) are a vital customer segment for Banco do Brasil, requiring tailored financial solutions. These businesses, from burgeoning startups to established firms, often seek working capital loans to manage day-to-day operations, business accounts for seamless transactions, and efficient payment solutions. In 2024, SMEs represented a significant portion of Brazil's economic activity, contributing to job creation and innovation.

Beyond basic banking, SMEs often need specialized advisory services to navigate growth challenges, optimize operational efficiency, and secure crucial access to credit. Unlike larger corporations with dedicated finance departments, these businesses frequently rely on their banking partners for guidance on financial planning and investment. This segment's distinct needs underscore the importance of personalized support from financial institutions like Banco do Brasil.

Large Corporations and Institutional Clients

Banco do Brasil serves major national and multinational corporations, alongside institutional investors like pension funds and asset managers. These clients typically require complex corporate finance solutions, including mergers and acquisitions advisory, and significant trade finance operations. In 2024, Banco do Brasil continued to be a key player in providing syndicated loans, facilitating large-scale project financing and corporate debt issuance for these high-value clients.

Government Entities and Public Sector

Government entities, including federal, state, and municipal administrations, along with public enterprises, are key clients for Banco do Brasil. These bodies rely on the bank for critical financial operations such as treasury management, the issuance of public debt, and the efficient disbursement of funds for social programs. For instance, in 2024, Banco do Brasil continued its role in facilitating government initiatives, contributing to the stability and execution of public finance strategies.

The bank’s historical connection to the Brazilian government underpins its significant role in public finance. This deep integration allows Banco do Brasil to effectively manage large-scale financial flows and provide specialized services tailored to the public sector's unique needs. These relationships are characterized by their substantial size and long-term stability, reflecting a trusted partnership.

- Treasury Management: Facilitating the daily financial operations of government bodies.

- Public Debt Issuance: Assisting governments in raising capital through bond markets.

- Social Program Disbursements: Ensuring timely and secure distribution of funds for social welfare initiatives.

- Infrastructure Financing: Providing capital for major public works and development projects.

Agribusiness Sector

Banco do Brasil's Agribusiness sector is a cornerstone of its operations, deeply intertwined with Brazil's robust agricultural economy. This segment caters to a diverse clientele, including individual farmers, large agribusiness corporations, and agricultural cooperatives. These clients rely on specialized financial products and services designed to align with the unique rhythms of the agricultural cycle.

The bank's historical commitment and substantial presence in agribusiness are undeniable. For instance, in 2023, Banco do Brasil disbursed R$182.4 billion in rural credit, a significant portion of the total R$302.3 billion allocated by the National Program for the Strengthening of Family Agriculture (Pronaf) and the National Program for the Production and Use of Renewable Energy in Agriculture (Renewable Energy Program). This highlights the bank's pivotal role in financing Brazilian agriculture.

- Farmers: Individual producers requiring financing for planting, harvesting, and equipment.

- Agribusiness Companies: Larger entities needing capital for expansion, technology adoption, and supply chain management.

- Cooperatives: Organizations that aggregate farmers, requiring services for collective investment and marketing.

Banco do Brasil offers a comprehensive suite of products, including tailored rural credit lines, agricultural insurance to mitigate risks, and investment solutions specifically designed for the sector's needs. The bank's strategic focus on agribusiness is driven by its significant contribution to Brazil's GDP and its potential for continued growth, especially with advancements in sustainable farming practices and technology.

Serving Brazil: The bank's 2024 customer segments

Banco do Brasil's customer segments are diverse, reflecting the bank's broad reach across the Brazilian economy. These segments include individual retail customers, small and medium-sized enterprises (SMEs), large corporations and institutional investors, government entities, and the critical agribusiness sector.

In 2024, the bank continued to serve millions of individuals and SMEs, providing essential banking services and tailored financial solutions. For instance, Banco do Brasil reported a substantial number of active individual accounts in early 2024, highlighting its extensive retail presence.

| Customer Segment | Key Needs | 2024 Relevance |

|---|---|---|

| Individual Retail | Transaction accounts, credit, wealth management | Core revenue driver, broad client base |

| SMEs | Working capital, business accounts, advisory | Significant economic contributors, require tailored support |

| Corporations & Institutions | Corporate finance, M&A, trade finance | High-value clients, complex financial needs |

| Government Entities | Treasury management, public debt, social programs | Facilitate public finance, large-scale operations |

| Agribusiness | Rural credit, insurance, investment | Pivotal to Brazil's economy, significant credit disbursement |

Cost Structure

Personnel Costs

Salaries, benefits, and training for Banco do Brasil's extensive workforce, spanning its numerous branches, corporate offices, and critical IT departments, represent a substantial segment of its overall operational expenses. This significant investment in human capital is a primary driver of the bank's operating costs.

In 2024, personnel expenses are a key focus for efficiency. For instance, the bank's commitment to professional development is evident in its ongoing training programs designed to keep its employees abreast of evolving financial technologies and customer service standards.

Technology and Infrastructure Costs

Banco do Brasil dedicates significant resources to its technology and infrastructure, a critical component for its operations. Expenditures cover the maintenance and upgrades of IT systems, robust cybersecurity measures, and the development of digital platforms. In 2023, the bank reported significant investments in technology, with digital transformation initiatives being a key focus, reflecting the ongoing need to remain competitive.

Branch Network and Property Costs

Banco do Brasil's extensive network of physical branches and ATMs incurs substantial costs. These include rent, ongoing maintenance, utilities, security, and depreciation. For instance, in 2023, the bank reported significant expenses related to its property, plant, and equipment, reflecting the upkeep of thousands of service points across Brazil, even as digital banking adoption increases.

Marketing and Advertising Expenses

Marketing and advertising expenses are crucial for Banco do Brasil to promote its diverse banking products and services, fostering brand recognition and attracting new clients. These costs encompass campaigns across digital platforms, traditional media, and sponsorships aimed at building a strong brand presence and expanding market share. In 2023, the bank allocated a significant portion of its budget to these initiatives to maintain its competitive edge.

Effective marketing strategies are paramount for customer acquisition and retention in the dynamic financial sector. Banco do Brasil's investment in advertising drives visibility, encouraging both new and existing customers to engage with its offerings. This proactive approach is essential for growth and solidifying its position in the market.

- Brand Building: Costs incurred to enhance Banco do Brasil's reputation and customer trust through consistent messaging and public relations efforts.

- Customer Acquisition: Investments in campaigns designed to attract new clients, such as special offers on credit cards or new account openings.

- Digital Marketing: Spending on online advertising, social media engagement, and search engine optimization to reach a wider audience.

- Traditional Advertising: Expenses related to television, radio, print, and outdoor advertising to maintain broad market awareness.

Regulatory Compliance and Legal Costs

Banco do Brasil incurs significant expenses to maintain compliance with Brazil's stringent financial regulations. These costs are essential for adhering to anti-money laundering (AML) statutes, consumer protection mandates, and various other banking laws. In 2024, the bank's commitment to regulatory adherence is a substantial operational expenditure, safeguarding against hefty fines and reputational harm.

These expenditures cover investments in technology for monitoring transactions, training for specialized compliance staff, and fees for external legal experts. For instance, the Central Bank of Brazil frequently updates its directives, requiring continuous adaptation and resource allocation. These ongoing efforts are critical to the bank's operational integrity and market trust.

- Regulatory Compliance: Expenses related to adhering to directives from the Central Bank of Brazil and other financial authorities.

- Anti-Money Laundering (AML): Costs associated with systems and personnel to prevent and detect financial crimes.

- Consumer Protection: Investments in processes and training to ensure fair treatment and transparency for customers.

- Legal and Litigation: Funds set aside for potential legal disputes, settlements, and ongoing legal counsel.

Decoding Banco do Brasil's Costs: Operations, Tech, and People

Banco do Brasil's cost structure is heavily influenced by its vast operational footprint and commitment to technological advancement. Key expenses include personnel costs, the upkeep of its extensive physical branch network, and significant investments in IT infrastructure and cybersecurity. Additionally, the bank allocates substantial resources to marketing and ensuring rigorous compliance with Brazil's financial regulations.

| Cost Category | 2023 Estimated Costs (R$ billions) | Key Drivers |

|---|---|---|

| Personnel Expenses | ~20.0 | Salaries, benefits, training for ~90,000 employees |

| Technology & Infrastructure | ~5.0 | IT system upgrades, digital platforms, cybersecurity |

| Branch Network Operations | ~4.0 | Rent, maintenance, utilities for thousands of branches and ATMs |

| Marketing & Advertising | ~1.5 | Brand building, customer acquisition campaigns |

| Regulatory Compliance | ~1.0 | AML systems, legal counsel, consumer protection measures |

Revenue Streams

Net Interest Income from Loans

Net Interest Income from Loans is Banco do Brasil's main money-maker. It comes from the gap between what they earn on loans like personal, business, and home loans, and what they pay out on savings accounts and other borrowings. This is a core part of how banks make money, showing how much they lend and how well they manage interest rates.

In 2023, Banco do Brasil reported a net interest income of R$87.7 billion, a significant increase from the previous year. This highlights the strength of their lending operations and their ability to manage interest margins effectively in the prevailing economic conditions.

Service Fees and Commissions

Banco do Brasil generates significant income from service fees and commissions, a crucial element of its revenue diversification. These charges encompass a wide array of banking activities, such as account maintenance, transaction processing, credit card usage, and ATM withdrawals. For instance, in the first quarter of 2024, the bank reported substantial revenue from these non-interest income sources, demonstrating their importance to overall financial performance.

Investment Management and Brokerage Fees

Banco do Brasil generates significant revenue from investment management and brokerage fees. These fees are derived from managing a vast array of investment funds, offering personalized wealth management services to a broad client base, and efficiently executing trades for customers.

The performance of this revenue stream is directly tied to the total volume of assets under management and the success of the investment products offered. For instance, in the first quarter of 2024, Banco do Brasil reported a substantial increase in its investment portfolio, indicating a healthy growth in assets under management which directly fuels these fee-based revenues.

Insurance Premiums and Related Income

Banco do Brasil generates substantial revenue from insurance premiums and related income, a key component of its diversified business model. This income stream comes from selling a wide array of insurance products, including life, property, health, and auto insurance. These offerings are made available through strategic partnerships and the bank's own dedicated insurance subsidiaries.

This insurance segment significantly diversifies Banco do Brasil's revenue, moving beyond its core banking operations. By leveraging its extensive existing customer base, the bank effectively cross-sells insurance products, creating a steady and recurring income stream. For instance, in 2023, Banco do Brasil's insurance arm, BB Seguridade, reported a net income of R$5.1 billion, showcasing the profitability of this revenue channel.

- Diversified Revenue: Insurance premiums provide a stable income source separate from traditional lending and deposit activities.

- Cross-Selling Opportunities: The bank's large customer base facilitates the efficient sale of insurance products.

- Recurring Income: Many insurance policies, like life and auto, generate predictable, ongoing revenue.

- Profitability: BB Seguridade's 2023 net income of R$5.1 billion highlights the financial success of this segment.

Treasury Operations and Trading Gains

Banco do Brasil generates revenue through treasury operations and trading gains, which stem from its proprietary trading activities in various financial markets. This includes engaging in foreign exchange, derivatives, and fixed income securities. These activities allow the bank to profit from market fluctuations and its expertise in financial instruments.

While these revenue streams can be more volatile than traditional banking services, they offer the potential for significant contributions to overall profitability. This volatility is directly linked to the bank's market insights and its willingness to take on calculated risks. For instance, in the first quarter of 2024, Banco do Brasil reported significant gains from its financial investments and trading operations, contributing positively to its net income.

- Proprietary Trading: Profits from the bank's direct trading in financial markets, including FX, derivatives, and fixed income.

- Market Expertise: Revenue reflects the bank's ability to leverage market knowledge for profitable trades.

- Risk Appetite: Trading gains are tied to the bank's strategic approach to risk-taking in financial markets.

- Volatility: This revenue stream can fluctuate significantly, impacting overall bank performance.

Diversified Revenue: A Financial Powerhouse

Banco do Brasil's revenue streams are robust and diversified, extending beyond traditional net interest income. Service fees and commissions from a wide array of banking activities, such as account maintenance and credit card usage, form a significant part of their income. Investment management and brokerage fees, driven by assets under management and successful investment products, also contribute substantially. Furthermore, insurance premiums from various policies like life and auto insurance, sold through partnerships and subsidiaries, provide a stable and recurring income. Finally, treasury operations and trading gains from proprietary trading in financial markets, while more volatile, can offer significant profits based on market expertise and calculated risk-taking.

| Revenue Stream | Description | 2023/Q1 2024 Data Point |

|---|---|---|

| Net Interest Income | Profit from lending vs. borrowing costs | R$87.7 billion (2023 Net Interest Income) |

| Fees and Commissions | Charges for banking services | Substantial revenue reported in Q1 2024 |

| Investment Management & Brokerage | Fees from managing assets and executing trades | Healthy growth in assets under management in Q1 2024 |

| Insurance Premiums | Income from selling insurance products | R$5.1 billion net income from BB Seguridade (2023) |

| Treasury & Trading Gains | Profits from proprietary trading activities | Significant gains reported in Q1 2024 |

Business Model Canvas Data Sources

The Banco do Brasil Business Model Canvas is built upon a robust foundation of internal financial data, extensive market research, and strategic analyses of the Brazilian banking sector. These diverse sources ensure each component of the canvas accurately reflects the bank's operational realities and strategic direction.