Bank of India Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Bank of India

Go Beyond the Preview—Access the Full Strategic Report

The Bank of India operates within a dynamic banking sector, facing significant competitive pressures. Understanding the intensity of rivalry, the power of buyers and suppliers, and the threats of new entrants and substitutes is crucial for its strategic positioning. This brief overview highlights key industry forces, but the full picture reveals the intricate web of influences shaping the Bank of India's landscape.

Ready to move beyond the basics? Get a full strategic breakdown of Bank of India’s market position, competitive intensity, and external threats—all in one powerful analysis.

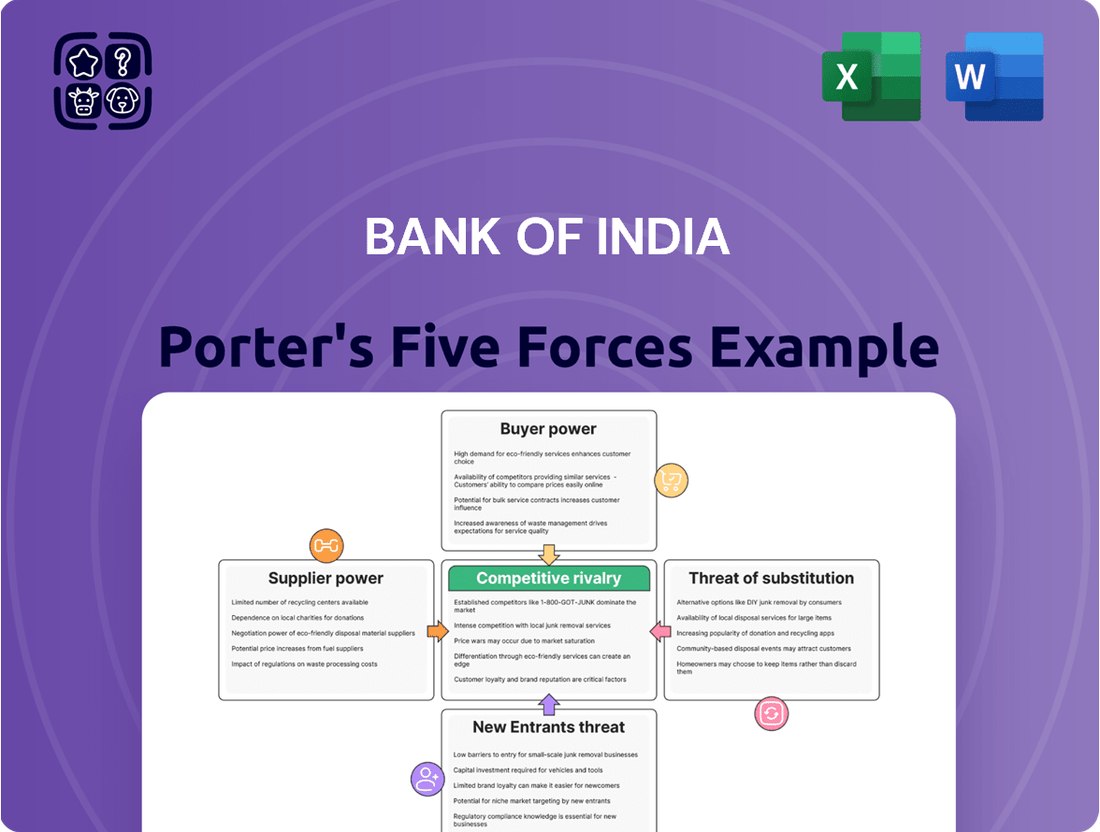

Suppliers Bargaining Power

Capital Providers (Depositors)

The bargaining power of most individual depositors with Bank of India is quite low. This is because there are many depositors, and the services offered, like savings accounts, are fairly standard. However, larger depositors, such as institutions or very wealthy individuals, can exert more influence, particularly if they are considering moving substantial sums or require tailored banking solutions. For instance, as of March 31, 2024, Bank of India’s total deposits stood at ₹6,65,638 crore, illustrating the sheer volume of smaller contributions that dilute individual power.

Technology and Software Vendors

Technology and software vendors, particularly those providing core banking systems, digital platforms, and cybersecurity solutions, wield considerable bargaining power over banks like Bank of India. These specialized providers can often dictate terms due to the high switching costs associated with integrating new systems and the critical nature of these technologies for a bank's operations and security. For instance, the global market for core banking software is dominated by a few major players, limiting options and increasing reliance on existing vendors. This dependence can significantly impact a bank's ability to negotiate favorable pricing and service level agreements, potentially hindering technological advancement and operational efficiency.

Skilled Labor and Talent

The availability of specialized talent in fields like AI, data analytics, cybersecurity, and fintech significantly bolsters the bargaining power of skilled employees. In 2024, the demand for AI specialists, for instance, saw a notable increase, with average salaries for AI engineers in India rising by an estimated 15-20% compared to the previous year.

Banks, including Bank of India, must therefore offer competitive compensation packages and attractive benefits to secure and retain this critical talent. This necessity directly impacts operational costs, especially within a fiercely competitive labor market where acquiring and keeping top performers is paramount for innovation and service delivery.

Regulatory Bodies and Government

Regulatory bodies, such as the Reserve Bank of India (RBI), wield significant influence over banks like Bank of India, acting as powerful 'suppliers' of essential operating licenses and compliance frameworks. Their directives on capital adequacy, lending norms, and risk management are non-negotiable, directly impacting a bank's operational costs and strategic flexibility. For instance, the RBI's mandate for higher provisioning for certain loan categories can immediately affect a bank's profitability and capital ratios.

The government's policy decisions also play a crucial role, shaping the broader economic and financial landscape in which Bank of India operates. Changes in fiscal policy, interest rate directions, or sector-specific regulations can fundamentally alter the competitive environment and the cost of doing business. In 2024, the Indian banking sector continued to navigate evolving regulatory landscapes, with a focus on strengthening governance and digital compliance.

- RBI's Capital Adequacy Ratio (CAR) mandates directly influence a bank's lending capacity and risk-taking.

- Government policies on priority sector lending impact loan portfolio composition and profitability.

- Compliance with evolving digital banking regulations requires significant investment in technology and security.

Infrastructure and Utility Providers

Infrastructure and utility providers, such as those offering real estate, electricity, and telecommunications, generally hold moderate bargaining power over a bank like Bank of India. Banks rely heavily on these services for their physical branches and crucial digital infrastructure. For instance, as of early 2024, the Indian real estate market saw varied rental yields across major cities, impacting the cost of branch operations. Similarly, telecommunication costs are influenced by competition among providers.

The bargaining power is somewhat tempered by the presence of multiple service providers, particularly in urban centers where Bank of India operates extensively. However, the indispensable nature of these services, especially reliable power and internet connectivity for digital banking operations, means suppliers can still exert significant influence. For example, in 2023, the average cost of broadband services in India varied, but the necessity for consistent high-speed internet for ATMs and online transactions remains a constant demand.

The bank's ability to negotiate terms is also influenced by the scale of its operations and its commitment to long-term contracts. For example, securing favorable lease agreements for a large number of branches can shift some power towards the bank. Conversely, the critical nature of utilities means that any disruption can have a substantial impact, giving utility providers leverage, especially during periods of high demand or limited supply, a factor that became more pronounced during India's monsoon season in 2024 impacting power availability.

- Real Estate: Rental costs for bank branches and offices are a significant operational expense, influenced by location and market conditions.

- Utilities: Consistent and affordable electricity is vital for branch operations and data centers.

- Telecommunications: Reliable internet and communication lines are essential for digital banking services and inter-branch connectivity.

- Provider Availability: The presence of multiple competing providers in key operating areas can moderate supplier bargaining power.

Bank of India's Supplier Power Dynamics: Key Influences on Costs & Strategy

The bargaining power of suppliers for Bank of India can be segmented across various categories, each with distinct implications for the bank's operational costs and strategic flexibility. Critical suppliers, such as core technology providers and specialized talent, often hold significant leverage due to high switching costs and the unique nature of their offerings. Conversely, suppliers of more commoditized goods and services, like general office supplies or basic utilities, typically have less power, especially when the bank can source from multiple vendors.

In 2024, the demand for specialized IT skills, particularly in cybersecurity and AI, continued to drive up labor costs, giving skilled employees substantial bargaining power. For example, salary benchmarks for cybersecurity analysts in India saw an upward trend, reflecting the critical need for these professionals. Similarly, vendors of essential banking software systems can command higher prices due to the complexity and integration challenges involved in changing providers.

The bank's reliance on regulatory frameworks, such as those set by the Reserve Bank of India (RBI), also represents a form of supplier power, as compliance with these mandates is non-negotiable and can necessitate significant investment. For instance, evolving digital banking regulations in 2024 required banks to enhance their IT infrastructure and cybersecurity measures, adding to operational expenses.

| Supplier Category | Bargaining Power Level | Key Factors Influencing Power | Example Data/Trend (2024) |

|---|---|---|---|

| Technology & Software Vendors | High | High switching costs, specialized nature of services, vendor concentration | Increased demand for cloud banking solutions, driving vendor pricing power. |

| Skilled Labor (IT, AI, Cybersecurity) | High | Shortage of specialized talent, high demand from the sector | Estimated 15-20% salary increase for AI engineers in India. |

| Regulatory Bodies (e.g., RBI) | High | Mandatory compliance, licensing authority | New RBI guidelines on digital lending requiring enhanced data security. |

| Infrastructure & Utilities | Moderate | Availability of multiple providers, essential nature of services | Varied rental yields impacting branch operating costs; consistent demand for reliable internet. |

What is included in the product

Tailored exclusively for Bank of India, this analysis dissects the intensity of rivalry, the bargaining power of customers and suppliers, the threat of new entrants, and the impact of substitute products, revealing the core competitive forces shaping its market.

Instantly identify and address competitive threats with a visual breakdown of the Bank of India's Porter's Five Forces, highlighting key areas of pressure.

Gain a strategic advantage by pinpointing vulnerabilities and opportunities within the Bank of India's competitive landscape, enabling targeted action.

Customers Bargaining Power

Individual Retail Customers

Individual retail customers generally possess moderate bargaining power. This is because the Indian banking landscape is diverse, offering a wide array of choices from public sector banks, private sector banks, and foreign banks, alongside a growing number of digital-only banking platforms. For instance, as of March 31, 2024, India had over 12 public sector banks, more than 20 private sector banks, and several foreign banks operating within the country, providing ample alternatives for customers.

While the costs associated with switching basic bank accounts can be relatively low, customer loyalty is increasingly influenced by factors like the convenience offered by digital banking services and the attractiveness of competitive interest rates. In 2023, the digital banking penetration in India continued to rise, with mobile banking transactions accounting for a significant portion of overall banking activity, highlighting the importance of these digital offerings in retaining customers.

Corporate and Institutional Clients

Large corporate and institutional clients possess considerable bargaining power. Their substantial business volumes, encompassing significant deposits, credit facilities, and trade finance, give them leverage. For instance, in 2023, the Bank of India reported a substantial portion of its advances to large corporations, highlighting the importance of these relationships.

These clients often participate in competitive bidding, demanding tailored solutions, better interest rates, and specialized services. This can put pressure on the bank's profit margins, as they may need to offer concessions to retain or attract such high-value customers.

Access to Information and Digital Literacy

The rise of digital banking and financial comparison sites has dramatically boosted customer access to information. For instance, by mid-2024, over 70% of Bank of India's transactions were conducted digitally, highlighting a significant shift in customer engagement and information seeking behavior. This ease of access allows customers to readily compare interest rates, fees, and service quality across various institutions.

This increased transparency directly empowers customers, giving them a stronger voice in demanding better terms and conditions. With readily available data, customers can easily identify more favorable offerings, thereby increasing their bargaining power and pushing banks like Bank of India to remain competitive on pricing and service.

Diverse Product Offerings and Alternatives

Customers today have a vast selection of financial products and services at their fingertips, extending far beyond what traditional banks offer. This includes options from Non-Banking Financial Companies (NBFCs), innovative fintech startups, and direct investment platforms, all vying for customer attention. This abundance of choice significantly boosts customer bargaining power.

Customers can easily switch to competitors if a bank's offerings don't align with their needs or if they find better pricing elsewhere. For instance, by mid-2024, the Indian fintech sector saw a surge in digital lending platforms, offering personalized loan products with competitive interest rates, directly challenging traditional bank lending models.

- Expanded Choices: Customers can access services from NBFCs, fintechs, and direct investment platforms, increasing competition for banks.

- Price Sensitivity: The availability of alternatives makes customers more sensitive to pricing and service quality offered by banks.

- Ease of Switching: Digitalization and open banking initiatives in 2024 have made it simpler for customers to move their accounts or services, reducing customer inertia.

- Product Innovation: Fintechs, in particular, are rapidly innovating with tailored products like buy-now-pay-later schemes and digital wallets, forcing banks to adapt or risk losing market share.

Low Switching Costs for Basic Services

For fundamental banking needs, such as maintaining savings accounts or utilizing digital payment platforms, customers face minimal barriers when considering a switch. The widespread adoption and integration of systems like India's Unified Payments Interface (UPI) have made transferring funds between different banks incredibly smooth and efficient. This ease of transition directly impacts banks, compelling them to consistently elevate their service standards, provide attractive interest rates, and ensure high levels of customer contentment to retain their client base.

The low switching costs are evident in the increasing adoption of digital banking solutions. As of December 2023, UPI transactions in India reached a staggering volume, processing over 11.5 billion transactions in that month alone. This highlights the customer's comfort and preference for seamless digital transfers, reinforcing the pressure on banks to maintain competitive offerings.

- Low Customer Switching Costs: Basic banking services exhibit low perceived switching costs for customers, facilitated by digital platforms and unified payment systems.

- Impact on Banks: This low cost of switching necessitates continuous improvement in service quality, competitive pricing, and customer engagement to prevent customer attrition.

- Digital Payment Growth: The surge in digital payments, with UPI processing over 11.5 billion transactions in December 2023, underscores customer ease and preference for inter-bank transfers, intensifying competitive pressures.

Customer Leverage: Digitalization Reshapes Banking Landscape

Customers' bargaining power is amplified by the sheer volume of choices available, including traditional banks, NBFCs, and fintechs, all competing for their business. This competitive landscape, particularly with the rise of digital platforms, means customers can easily compare offerings and switch providers if dissatisfied. For example, by mid-2024, the rapid growth of digital lending platforms in India provided customers with competitive interest rates and personalized loan products, directly challenging established banks.

The ease with which customers can switch is further facilitated by advancements in digital banking and payment systems. India's UPI, for instance, processed over 11.5 billion transactions in December 2023 alone, demonstrating the seamless inter-bank transfer capabilities that reduce customer inertia. This low switching cost compels banks like Bank of India to continuously enhance their service quality and pricing to retain their customer base.

| Factor | Impact on Bank of India | Supporting Data (as of mid-2024 or latest available) |

|---|---|---|

| Availability of Alternatives | Increases customer leverage, forcing competitive pricing and service. | Numerous public, private, and foreign banks; growing fintech sector. |

| Digitalization & Ease of Switching | Reduces customer inertia, demanding constant service improvement. | UPI transactions exceeded 11.5 billion in Dec 2023; >70% of Bank of India's transactions were digital by mid-2024. |

| Information Transparency | Empowers customers to demand better terms and conditions. | Widespread access to financial comparison sites and digital information. |

Full Version Awaits

Bank of India Porter's Five Forces Analysis

This preview showcases the complete Bank of India Porter's Five Forces analysis, offering a detailed examination of competitive forces within the Indian banking sector. You're viewing the exact document you'll receive immediately after purchase, ensuring transparency and no hidden surprises. This comprehensive analysis provides actionable insights into the industry's structure and potential profitability.

Rivalry Among Competitors

Presence of Numerous Public and Private Banks

The Indian banking landscape is incredibly crowded, featuring a vast array of public sector banks, private sector institutions, and foreign players all vying for customer attention. This intense fragmentation means that Bank of India faces constant pressure from a multitude of competitors, each eager to capture market share.

This fierce rivalry translates into aggressive tactics like competitive interest rates and novel product offerings, forcing Bank of India to continually innovate and differentiate itself. For instance, in 2023, the banking sector saw an average Net Interest Margin (NIM) hovering around 3.0-3.5%, a figure directly impacted by this intense competition.

Aggressive Growth of Private Sector Banks

The aggressive growth of private sector banks presents a formidable competitive rivalry for Bank of India. These private players, often more agile and technologically adept, are rapidly gaining market share. For instance, in the fiscal year 2023-24, private banks collectively saw a significant uptick in their customer base and asset growth, outperforming many public sector counterparts in certain digital service adoption metrics.

This intensified competition stems from private banks' customer-centric approach and their heavy investment in digital innovation. They are actively wooing customers with enhanced service quality and personalized offerings, forcing traditional banks like Bank of India to accelerate their own modernization efforts. The drive to improve efficiency and customer experience is now a critical imperative to remain competitive in this dynamic landscape.

Fintech Companies and Digital Disruption

Fintech companies are significantly intensifying competition for Bank of India. These agile players, focusing on areas like digital payments, peer-to-peer lending, and robo-advisory, are carving out niche markets. For instance, in India, the UPI (Unified Payments Interface) ecosystem, driven by companies like PhonePe and Google Pay, has seen massive transaction volumes, with over 13.4 billion transactions recorded in the fiscal year 2023-24 alone, directly impacting traditional payment avenues.

This digital disruption compels established banks like Bank of India to accelerate their own digital transformation initiatives. They must either develop in-house digital solutions, partner with fintechs, or even acquire them to retain market share and customer loyalty. Failure to adapt means losing out on younger, tech-savvy demographics who increasingly prefer seamless, app-based financial services.

Product Homogeneity and Price Sensitivity

The competitive rivalry within the Indian banking sector is significantly amplified by product homogeneity, particularly in core offerings like savings accounts, fixed deposits, and standard personal loans. This lack of differentiation means customers often choose based on price, leading to intense competition on interest rates and fees. For instance, in 2024, the average savings account interest rate offered by major public sector banks hovered around 2.70%, while private sector banks often competed with rates closer to 3.00-3.50%, illustrating the direct price competition.

This price sensitivity forces banks like Bank of India to constantly monitor and adjust their pricing strategies to remain competitive. It makes it difficult to command premium pricing and puts pressure on profit margins. As a result, banks must differentiate through other means, such as superior customer service, digital offerings, and specialized financial advice, to attract and retain customers.

- Product Homogeneity: Core banking products like deposits and loans lack significant differentiation.

- Price Sensitivity: Customers are highly influenced by interest rates and fees when choosing banks.

- Margin Pressure: Intense competition on price erodes profit margins for banks.

- Focus on Service: Banks must emphasize customer experience and digital innovation to stand out.

Regulatory Landscape and Consolidation

The Indian banking sector has experienced significant consolidation, particularly among public sector banks. For instance, the Indian government initiated a merger of ten public sector banks into four entities in 2019, aiming to create stronger, more competitive institutions. This consolidation, while reducing the overall number of banks, has led to the emergence of larger players with increased market share and capital bases.

Regulatory shifts also play a crucial role in shaping competitive rivalry. The Reserve Bank of India (RBI) continuously updates its guidelines on capital adequacy, risk management, and digital banking, influencing how banks operate and compete. For example, the RBI's push for enhanced cybersecurity measures and digital transformation necessitates significant investment, potentially widening the gap between well-capitalized banks and smaller ones.

- Consolidation Impact: Mergers like those of Andhra Bank and Corporation Bank into Union Bank of India in 2020 created a larger entity with an asset base exceeding INR 14.75 trillion, intensifying competition.

- Regulatory Influence: RBI's Basel III norms and digital banking mandates require substantial compliance investments, affecting competitive positioning.

- Market Dynamics: Increased competition from specialized banks and fintech firms, coupled with consolidation, necessitates strategic adaptation for established players like Bank of India.

India's Banking Sector: Intense Rivalry and Digital Disruption

Competitive rivalry is a dominant force for Bank of India, driven by a highly fragmented market with numerous public, private, and foreign banks. This intense competition forces constant innovation in product offerings and pricing, impacting net interest margins. For instance, in 2023, average NIMs in the Indian banking sector were around 3.0-3.5%, a direct consequence of this rivalry.

Private sector banks, with their agility and digital focus, are particularly aggressive competitors, often outperforming public sector banks in customer acquisition and digital service adoption. This trend was evident in fiscal year 2023-24, where private banks saw substantial growth. Fintech companies further intensify this rivalry through digital payment platforms like UPI, which recorded over 13.4 billion transactions in FY 2023-24, challenging traditional banking revenue streams.

The homogeneity of core banking products, such as savings accounts and loans, leads to price-driven competition, with interest rates on savings accounts differing by as much as 0.30-0.80% between public and private sector banks in 2024. This necessitates a strong emphasis on customer service and digital enhancements for differentiation. Consolidation, like the 2019 merger of ten public sector banks, has also created larger, more formidable competitors, while regulatory shifts from the RBI mandate significant investments in compliance, further shaping the competitive landscape.

| Competitor Type | Key Competitive Actions | Impact on Bank of India |

|---|---|---|

| Public Sector Banks | Market share defense, branch network leverage | Direct competition for existing customer base |

| Private Sector Banks | Digital innovation, customer-centricity, aggressive pricing | Loss of market share, pressure on NIMs |

| Fintech Companies | Niche product development, digital payment dominance (e.g., UPI) | Disruption of traditional payment and lending services |

SSubstitutes Threaten

Digital Payment Platforms (UPI, Mobile Wallets)

Digital payment platforms, such as India's Unified Payments Interface (UPI) and a multitude of mobile wallets, present a substantial threat of substitution to traditional banking services. These digital alternatives offer speed and convenience, often at no direct cost to the user, directly challenging the utility of bank transfers, cheques, and even card payments for everyday transactions. By mid-2024, UPI had processed over 100 billion transactions, a testament to its widespread adoption and its role in shifting consumer payment habits away from older methods.

Non-Banking Financial Companies (NBFCs)

Non-Banking Financial Companies (NBFCs) represent a significant threat of substitutes for traditional banks, especially in the retail lending segment. NBFCs often provide specialized loan products, such as those for vehicle financing, gold loans, and microfinance, with faster approval processes and more adaptable eligibility requirements compared to many banks. For instance, in fiscal year 2023, NBFCs disbursed over ₹4.5 lakh crore in retail loans, showcasing their substantial market penetration.

This flexibility makes them an attractive alternative for customers who might find bank lending criteria too stringent or the process too time-consuming. The rise of digital lending platforms, many operated by NBFCs, further intensifies this threat by offering seamless, online loan applications and quicker disbursals, thereby directly competing with banks for a growing customer base.

Peer-to-Peer (P2P) Lending Platforms

Peer-to-peer (P2P) lending platforms present a significant threat of substitutes for traditional banks like Bank of India. These platforms directly connect individual borrowers with individual lenders, offering an alternative to conventional bank loans, particularly for personal and small business financing. For instance, by mid-2024, the P2P lending market in India was projected to reach approximately $2.5 billion, showcasing its growing appeal.

This disintermediation allows borrowers to potentially secure funds faster and sometimes at more competitive rates, especially for those who might find it difficult to obtain credit through traditional banking channels. The ease of access and the flexibility offered by P2P platforms can therefore draw away a segment of Bank of India's potential customer base.

Direct Investment and Wealth Management Platforms

Online brokerage firms, direct mutual fund platforms, and robo-advisory services present a significant threat of substitutes to Bank of India's wealth management and investment advisory services. These platforms allow individuals to bypass traditional banking channels for direct investment in equities, bonds, and mutual funds. For instance, in 2024, the digital wealth management sector continued its rapid expansion, with many platforms offering significantly lower expense ratios and advisory fees compared to traditional bank offerings, thereby attracting cost-conscious investors.

These direct investment channels empower individuals with greater control over their portfolios and often provide access to a wider array of investment products. The ease of use and transparency offered by these fintech solutions directly challenge the value proposition of bank-led wealth management. In 2023, the assets under management for robo-advisors globally saw substantial growth, indicating a clear shift in investor preference towards these more accessible and often cheaper alternatives.

- Lower Fees: Digital platforms typically charge lower advisory and transaction fees, making them more attractive to retail investors.

- Accessibility: Online platforms offer 24/7 access and user-friendly interfaces, simplifying the investment process.

- Product Choice: Investors can often access a broader range of investment products directly, without being limited to a bank's proprietary offerings.

- Technological Advancements: Innovations in AI and data analytics by fintech firms provide personalized investment recommendations, directly competing with human advisors.

Crowdfunding and Alternative Financing

Crowdfunding and alternative financing models are increasingly acting as substitutes for traditional bank loans, especially for startups and small businesses. Platforms like Kickstarter and Indiegogo allow entrepreneurs to raise capital directly from a large pool of individuals, bypassing conventional banking channels. This trend is significant as it offers a more accessible route for funding projects that might not meet strict bank criteria.

In 2024, the global crowdfunding market continued its robust growth. For instance, equity crowdfunding, a key substitute for business loans, saw substantial activity. Data from Statista indicated that the crowdfunding market size was projected to reach over $300 billion by 2025, with a significant portion attributed to debt and equity-based models that directly compete with bank lending.

- Crowdfunding platforms offer an alternative to bank loans for startups and SMEs.

- Equity and debt-based crowdfunding models directly compete with traditional bank financing.

- The global crowdfunding market is expanding, indicating a growing threat of substitutes for banks.

- Specific sectors like creative projects and technology startups are particularly prone to adopting these alternative funding methods.

Banking's New Rivals: Digital Payments and NBFCs Reshape Finance

The threat of substitutes for Bank of India is multifaceted, encompassing digital payment systems, non-banking financial companies, peer-to-peer lending, and alternative investment platforms. These alternatives often offer greater convenience, speed, and sometimes lower costs, directly challenging traditional banking services. By mid-2024, UPI had processed over 100 billion transactions, highlighting a significant shift in payment behavior. Furthermore, NBFCs disbursed over ₹4.5 lakh crore in retail loans in FY23, demonstrating their competitive presence in lending.

| Substitute Type | Key Characteristics | Impact on Bank of India | Market Data (2023-2024) |

| Digital Payments (UPI, Wallets) | Speed, convenience, low cost | Reduces reliance on bank transfers, cheques | UPI transactions exceeded 100 billion by mid-2024 |

| NBFCs | Specialized loans, faster approvals | Competes in retail lending, especially for specific needs | Disbursed over ₹4.5 lakh crore in retail loans (FY23) |

| P2P Lending | Direct lender-borrower connection | Offers alternative to bank loans for personal/SME financing | Market projected at $2.5 billion by mid-2024 |

| Online Investment Platforms | Lower fees, direct access to products | Challenges wealth management and advisory services | Digital wealth management sector shows rapid expansion |

| Crowdfunding | Alternative financing for startups/SMEs | Bypasses traditional bank loans | Global market projected over $300 billion by 2025 |

Entrants Threaten

High Regulatory Barriers and Licensing Requirements

The threat of new entrants into the Indian banking sector is significantly mitigated by high regulatory barriers and licensing requirements. The Reserve Bank of India (RBI) mandates stringent capital adequacy norms, such as a minimum of ₹1,000 crore for universal banks and ₹200 crore for small finance banks, creating a substantial financial hurdle for potential new players.

Compliance with extensive prudential regulations, including Know Your Customer (KYC) norms and Anti-Money Laundering (AML) guidelines, alongside robust governance standards, further complicates market entry. These rigorous entry barriers, coupled with the need for substantial investment in technology and infrastructure, effectively deter new entities from challenging established banks like Bank of India.

Substantial Capital Investment and Infrastructure

Establishing a new bank demands immense capital, often running into billions of dollars, for physical branches, ATMs, and sophisticated IT infrastructure. For instance, setting up a new digital-only bank in a major market can still cost hundreds of millions to establish the necessary technology and regulatory compliance frameworks. This significant financial hurdle makes it exceptionally challenging for potential new entrants to match the scale and existing customer base of established institutions like the Bank of India.

Brand Loyalty and Customer Trust

Existing banks, particularly public sector institutions like the Bank of India, have cultivated strong brand loyalty over many years, a significant barrier for new entrants. This deep-seated trust is hard-won and difficult to replicate quickly in the financial services sector, where customer confidence is everything. For instance, in FY23, Bank of India reported a customer base of over 100 million, highlighting the scale of established relationships.

Established Distribution Networks and Reach

Established banks like the Bank of India benefit from deeply entrenched distribution networks. These include a vast number of branches and ATMs, ensuring widespread accessibility, particularly in both urban and rural geographies. For instance, as of March 31, 2023, Bank of India operated 5,077 branches, a significant physical footprint that is difficult and costly for new entrants to replicate quickly.

The sheer scale of existing branch and ATM infrastructure presents a formidable barrier. New entrants would face immense capital expenditure and a considerable time lag to build a comparable physical presence. This existing infrastructure provides incumbents with a significant advantage in customer reach and service delivery, deterring potential new competitors.

Consider these points regarding established distribution networks:

- Extensive Branch and ATM Footprint: Incumbent banks maintain a widespread physical presence, crucial for customer accessibility and trust.

- High Replication Costs: The capital investment and time required to build a similar network are substantial deterrents for new players.

- Customer Reach and Service: Existing networks facilitate broad customer engagement and service delivery, creating a competitive edge.

Emergence of Digital-Only Banks and Fintechs

While obtaining traditional banking licenses remains a significant barrier, the burgeoning landscape of digital-only banks and specialized fintech firms presents a distinct threat. These nimble, tech-focused players can carve out niches with considerably lower operating costs.

These entrants often target specific customer segments or services, offering streamlined digital experiences. For instance, by mid-2024, the global fintech market was projected to reach over $300 billion, showcasing the rapid growth and potential disruption these companies represent.

- Digital-first models reduce overhead: Fintechs often bypass the need for extensive physical branch networks, leading to lower operational expenses compared to traditional banks.

- Niche market penetration: Companies like BharatPe in India have successfully entered specific payment and lending segments, building substantial customer bases before expanding their offerings.

- Technological agility: Their reliance on modern technology allows for quicker adaptation to market changes and customer demands, a stark contrast to the legacy systems of many established banks.

India's Banking: High Barriers Deter New Entrants

The threat of new entrants into India's banking sector is generally low due to substantial regulatory hurdles and significant capital requirements. The Reserve Bank of India's stringent licensing process and capital adequacy norms, such as the ₹1,000 crore minimum for universal banks, create a formidable financial barrier. Furthermore, the extensive compliance requirements and the need for robust IT infrastructure and a widespread distribution network, exemplified by Bank of India's 5,077 branches as of March 31, 2023, make it very costly for newcomers to compete effectively.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for the Bank of India utilizes data from the Reserve Bank of India (RBI) filings, annual reports of major Indian banks, and reputable financial news outlets to assess competitive intensity and market dynamics.