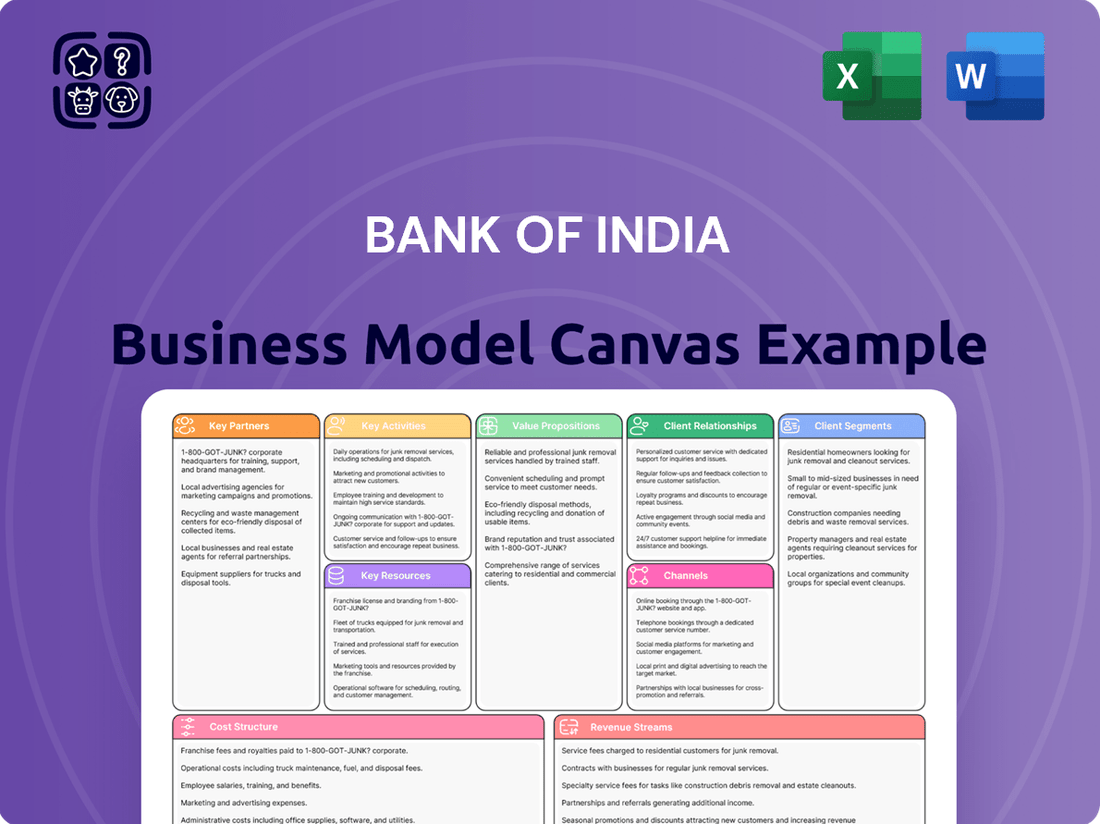

Bank of India Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Bank of India

Bank of India: Business Model Unveiled!

Unlock the core strategies driving Bank of India's success with our comprehensive Business Model Canvas. Understand their customer segments, value propositions, and revenue streams in detail. This is your chance to gain actionable insights for your own business ventures.

Partnerships

Government and Regulatory Bodies

As a public sector bank, Bank of India's key partnerships include government entities like the Ministry of Finance and the Reserve Bank of India (RBI). These collaborations are essential for navigating policy directives and regulatory frameworks, ensuring compliance and facilitating the bank's role in national financial initiatives.

These relationships are particularly important for the implementation of government-backed financial inclusion programs, allowing Bank of India to extend its services to underserved populations. The government's stake in the bank also influences its risk profile in the eyes of the RBI, potentially impacting capital buffer requirements.

Fintech Companies and Digital Solution Providers

Bank of India actively collaborates with fintech companies and digital solution providers to bolster its digital banking capabilities. These partnerships are crucial for integrating advanced features like digital payments and enhancing the mobile banking experience.

For instance, in 2023, the Indian fintech market was valued at approximately $31 billion, showcasing the significant potential of these collaborations. By teaming up with these innovative firms, Bank of India aims to offer seamless access to services, including government initiatives, through its digital platforms.

These strategic alliances are instrumental in accelerating digital adoption among customers and fundamentally transforming the banking experience, making it more convenient and accessible.

Other Financial Institutions (NBFCs, Insurance Companies, Mutual Funds)

Bank of India actively partners with Non-Banking Financial Companies (NBFCs), insurance companies, and mutual fund houses. These collaborations enable the bank to present a wider array of financial products, from loans and investments to insurance coverage, thereby enriching its service portfolio.

These strategic alliances are crucial for Bank of India to tap into specialized financial segments and extend its market presence. By integrating offerings from partners, the bank can provide customers with more holistic financial solutions, catering to diverse needs like wealth management and risk protection.

In 2024, the Indian financial landscape continues to witness a surge in collaborations between established banks and non-banking entities. This trend is driven by the mutual goal of improving credit accessibility and financial inclusion across the nation, with banks leveraging NBFCs' agility and reach.

Corporate Clients and Large Businesses

Bank of India's partnerships with corporate clients and large businesses are foundational to its wholesale banking. These relationships are crucial for driving corporate lending, facilitating trade finance, and providing sophisticated cash management solutions. By serving a broad spectrum of large corporations, the bank solidifies its position in the corporate lending market, which is a significant contributor to its overall loan portfolio and generates substantial fee-based income.

These strategic alliances are key drivers for Bank of India's financial performance. For instance, in FY24, the bank's gross advances saw a notable increase, with a significant portion attributed to its corporate segment. The bank's focus on these partnerships directly impacts its net interest income and also diversifies its revenue streams through various fee-based services tailored for large enterprises.

- Corporate Lending: Providing substantial credit facilities to large businesses forms a core part of the bank's lending strategy.

- Trade Finance: Facilitating international and domestic trade for corporations through services like letters of credit and guarantees.

- Cash Management: Offering advanced solutions for efficient treasury and payment operations for large corporate treasuries.

- Fee Income Generation: These services contribute significantly to the bank's non-interest income.

Agricultural and Rural Development Agencies

Bank of India actively collaborates with agricultural and rural development agencies across India. These partnerships are crucial for extending credit to the agricultural sector and promoting financial inclusion in underserved regions.

These collaborations enable Bank of India to effectively implement government schemes and facilitate the disbursement of agricultural loans, thereby supporting rural livelihoods. For the fiscal year 2024, Priority Sector Advances represented 44.08% of the Adjusted Net Bank Credit (ANBC).

- Agricultural Credit: Bank of India's agricultural credit reached 20.30% of ANBC in FY24, exceeding the regulatory mandate of 18%.

- Rural Outreach: Partnerships with rural development agencies enhance the bank's reach for financial inclusion initiatives.

- Scheme Implementation: These agencies assist in the effective rollout and management of government-sponsored schemes in rural areas.

- Financial Inclusion: Collaborations are key to bringing unbanked populations in rural and semi-urban areas into the formal financial system.

Bank's Strategic Partnerships: Powering Capital Market Growth

Bank of India's key partnerships extend to financial market participants like stock exchanges and depositories. These collaborations are vital for facilitating capital market transactions and ensuring the smooth execution of securities trading for its clients.

By integrating with these entities, Bank of India enhances its investment banking services and offers broader access to financial markets. In 2024, the Indian stock market continued its upward trajectory, with the Nifty 50 reaching new highs, underscoring the importance of robust partnerships in this dynamic sector.

| Partner Type | Purpose | Benefit to Bank of India | 2024 Relevance |

| Stock Exchanges (e.g., NSE, BSE) | Facilitating securities trading, listing services | Expanded investment product offerings, increased transaction volume | Continued growth in equity markets |

| Depositories (e.g., NSDL, CDSL) | Holding and transferring securities electronically | Streamlined settlement processes, enhanced back-office operations | Digitalization of financial assets |

What is included in the product

A comprehensive business model canvas for Bank of India, detailing its customer segments, value propositions, and revenue streams, all grounded in its operational realities.

This canvas offers a strategic overview of Bank of India's operations, ideal for presentations and informed decision-making by stakeholders.

The Bank of India Business Model Canvas acts as a pain point reliver by condensing complex banking strategies into a digestible format for quick review and adaptation.

It offers a clean and concise layout, perfect for comparing multiple banking services or models side-by-side to identify and address customer pain points efficiently.

Activities

Deposit Mobilization and Management

Bank of India's key activity revolves around attracting and managing a diverse range of deposits, from everyday savings and current accounts to fixed-term deposits. This broad base of customer funds is crucial for providing a stable and cost-effective foundation for the bank's lending operations.

In the fiscal year 2024, the bank saw significant growth in its deposit base, with global deposits rising by an impressive 10.21% to reach ₹7,37,920 crore. This expansion highlights the success of their deposit mobilization strategies.

Lending and Credit Facilities

Bank of India's core operation revolves around its lending and credit facilities, encompassing a broad spectrum of loan types from retail and corporate to agricultural and MSME sectors. This fundamental activity is supported by robust credit assessment, efficient loan disbursement, and diligent recovery mechanisms, all of which directly impact the bank's asset quality and overall profitability.

In the fiscal year 2024, Bank of India demonstrated significant growth in its lending operations, with global advances surging by 13.52% to reach ₹5,85,595 crore. Notably, advances to the Retail, Agriculture, and MSME (RAM) segments experienced an even more impressive expansion of 15.55%, highlighting the bank's strategic focus on these crucial areas of the economy.

Digital Banking and Technology Development

Bank of India's key activities in digital banking and technology development focus on creating and improving its online and mobile banking platforms. This involves a continuous effort to enhance user experience and introduce new features. For instance, they are actively working on integrating advanced technologies like artificial intelligence and machine learning to streamline customer interactions and personalize services.

A significant aspect of this strategy is ensuring robust cybersecurity measures to protect customer data and transactions. Bank of India is also committed to seamless integration with national digital initiatives. A prime example is their partnership with the National e-Governance Division (NeGD), which allows customers to access over 250 government services directly through the Bank of India Omni Neo App, reflecting a strong push towards digital inclusion and convenience.

Treasury Operations and Wealth Management

Bank of India's treasury operations are central to managing its financial health. This involves the strategic deployment of the bank's own funds, aiming to optimize returns while maintaining robust liquidity. They also actively engage in foreign exchange markets to facilitate client transactions and manage currency exposure, a critical function in a globalized economy.

A significant aspect of these activities is wealth management, where the bank provides tailored financial advice and investment solutions to high-net-worth individuals and institutional clients. These services are designed to grow and preserve client capital, contributing substantially to the bank's non-interest income streams.

- Investment Management: Actively managing the bank's portfolio of securities and other financial instruments to generate income and manage risk.

- Foreign Exchange Operations: Facilitating currency exchange for customers and managing the bank's own foreign currency positions.

- Wealth Management Services: Offering personalized financial planning, investment advisory, and portfolio management to affluent clients.

In the fiscal year 2023-24, Bank of India reported a notable increase in its treasury income, reflecting successful management of its investment and foreign exchange portfolios. The bank's commitment to expanding its wealth management offerings also saw positive traction, with assets under management growing by a significant percentage year-on-year.

Regulatory Compliance and Risk Management

Bank of India's key activities include rigorous regulatory compliance and comprehensive risk management. This involves ensuring strict adherence to all directives from the Reserve Bank of India (RBI) and other financial regulatory bodies. It’s a critical function for maintaining the bank’s financial stability and public trust.

The bank actively manages various risks, including credit risk, market risk, operational risk, and increasingly, cyber risks. These robust risk management practices are essential to safeguard the bank's assets and reputation. For instance, the Indian banking sector, as of early 2024, demonstrated improved asset quality and sustained credit growth, reflecting the effectiveness of such measures across the industry.

- Regulatory Adherence: Ensuring full compliance with RBI guidelines and other statutory requirements.

- Risk Mitigation: Implementing strong frameworks to manage credit, market, operational, and cyber risks.

- Financial Stability: Upholding the bank's financial health and solvency through diligent oversight.

- Public Confidence: Maintaining customer and stakeholder trust by operating within legal and ethical boundaries.

Strategic Treasury & Wealth Management Boost Performance

Bank of India's treasury operations are crucial for managing its financial resources. This involves strategically investing the bank's own capital to generate returns while ensuring sufficient liquidity. They also actively participate in foreign exchange markets to support customer needs and manage currency fluctuations.

These activities are complemented by wealth management services, offering expert financial advice and investment solutions to high-net-worth clients and institutions. This segment plays a vital role in boosting the bank's non-interest income.

In the fiscal year 2023-24, Bank of India saw a positive trend in its treasury income, indicating effective management of its investment and forex portfolios. The expansion of its wealth management services also contributed to growth, with assets under management showing a healthy year-on-year increase.

| Key Activity | Description | Fiscal Year 2024 Impact |

| Investment Management | Managing the bank's securities portfolio for income and risk control. | Contributed to treasury income growth. |

| Foreign Exchange Operations | Facilitating currency exchange and managing currency exposure. | Supported client transactions and managed bank's FX positions. |

| Wealth Management Services | Providing personalized financial planning and investment advice. | Assets under management showed significant year-on-year growth. |

Preview Before You Purchase

Business Model Canvas

The Bank of India Business Model Canvas you are previewing is the actual, complete document you will receive upon purchase. This isn't a sample or a mockup; it's a direct representation of the business model framework you'll be able to download and utilize immediately. You'll gain full access to this professionally structured document, ready for your strategic analysis and planning.

Resources

Financial Capital and Liquidity

Bank of India's financial capital and liquidity are foundational to its business model. This includes its substantial capital base and reserves, which are crucial for absorbing potential losses and ensuring it can continue lending and operating smoothly. As of March 2024, the bank demonstrated its financial resilience with a capital adequacy ratio of 16.96%, comfortably exceeding regulatory norms.

Access to liquidity is another vital resource, enabling the bank to meet its short-term obligations and fund its lending activities. The bank's strong provisioning practices, evidenced by a provision coverage ratio of 77.45% as of March 2024, further bolster its financial health and its capacity to manage risk effectively, thereby supporting its growth ambitions.

Human Capital and Expertise

Bank of India's human capital is a cornerstone, comprising skilled banking professionals, IT specialists, risk managers, and customer service experts. This diverse talent pool is crucial for driving innovation and maintaining operational excellence.

The bank's commitment to employee development is evident through its investment in comprehensive training programs across various banking domains. This focus ensures staff are equipped with the latest knowledge and skills to navigate the evolving financial landscape.

In 2024, Bank of India continued to emphasize its human resources, recognizing that their expertise directly translates to building robust customer relationships and ensuring efficient service delivery, which are vital for sustained growth.

Technology Infrastructure and Digital Platforms

Bank of India leverages advanced IT systems, robust digital banking platforms, and user-friendly mobile applications as core resources. These are supported by secure data centers and comprehensive cybersecurity frameworks, ensuring efficient service delivery and safeguarding customer data.

In 2024, the bank continued its strategic investments in IT capital assets. This focus aims to bolster its digital initiatives, including enhancing the functionality and reach of its Internet banking, Mobile banking, and ATM channels, thereby improving customer experience and operational efficiency.

Extensive Branch Network and ATMs

Bank of India's extensive branch network and ATM infrastructure are vital resources, enabling broad customer reach across India, particularly in semi-urban and rural regions where digital access might be less prevalent. This physical footprint is crucial for traditional banking services and customer engagement.

As of March 31, 2024, Bank of India operated a vast network comprising 5,090 branches and 4,921 ATMs. This physical presence is a cornerstone for customer acquisition and service delivery, complementing its growing digital channels.

- Branch Network: 5,090 branches as of March 31, 2024.

- ATM Network: 4,921 ATMs as of March 31, 2024.

- Geographic Reach: Significant presence in semi-urban and rural areas.

- Service Delivery: Supports both traditional and digital banking services.

Brand Reputation and Public Trust

Bank of India, as a public sector bank, leverages a strong brand reputation and deep-seated public trust, a crucial intangible asset. This trust is a direct result of its extensive history, the backing of the Indian government, and a consistent dedication to financial inclusion initiatives across the nation.

The government's majority ownership in public sector banks like Bank of India instills a sense of security among customers, effectively reducing the central bank's exposure to potential financial risks and bolstering confidence in the institution's stability.

- Brand Strength: Bank of India's long-standing presence and government affiliation contribute to a robust brand image.

- Public Confidence: A history of reliable service and financial inclusion efforts fosters significant public trust.

- Government Guarantee: State ownership provides an implicit guarantee, enhancing perceived safety and stability for depositors.

- Financial Inclusion Focus: Initiatives aimed at bringing unbanked populations into the formal financial system further solidify its role and reputation.

Core Resources Powering a Leading Bank

Bank of India's core resources include its substantial financial capital, a skilled workforce, and advanced IT infrastructure. These are augmented by its extensive physical branch and ATM network, which ensures broad customer accessibility, especially in underserved regions. Its strong brand reputation, backed by government ownership, further solidifies its position.

| Resource Category | Key Resources | 2024 Data/Notes |

|---|---|---|

| Financial Capital | Capital Base & Reserves, Liquidity | Capital Adequacy Ratio: 16.96% (March 2024) |

| Human Capital | Skilled Banking Professionals, IT Specialists, Risk Managers | Ongoing investment in comprehensive training programs. |

| Physical Infrastructure | Branch Network, ATM Network | 5,090 Branches, 4,921 ATMs (March 31, 2024) |

| Intangible Assets | Brand Reputation, Public Trust, Government Backing | Strong public confidence due to long history and financial inclusion efforts. |

Value Propositions

Comprehensive and Diverse Financial Services

Bank of India provides a broad range of financial services, encompassing everything from basic savings accounts and diverse loan options to specialized services like foreign exchange and wealth management. This extensive portfolio ensures that individuals, businesses, and institutions can find a single, convenient source for all their financial requirements.

The bank's commitment is to deliver financial solutions that are not only simple and efficient but also innovative, adapting to the evolving needs of its clientele. For instance, as of March 31, 2024, Bank of India reported a robust total business of ₹12,39,323 crore, demonstrating its significant reach and capacity to serve a wide customer base.

Trust and Reliability of a Public Sector Bank

Customers place immense value on the inherent trust and reliability of public sector banks, a sentiment significantly reinforced by the Government of India's backing. This governmental assurance translates into a strong sense of security for deposits and financial dealings, particularly appealing to a vast segment of the Indian populace. In 2023-24, Public Sector Banks (PSBs) collectively reported a net profit of ₹1,04,654 crore, a testament to their operational stability and the continued confidence placed in them by the public.

Digital Convenience and Accessibility

Bank of India is enhancing customer experience through its robust digital offerings. Customers can now access a wide array of services, including internet banking and mobile applications, ensuring 24/7 convenience and accessibility. This digital push is central to their strategy of providing seamless and efficient banking.

A significant achievement in their digital transformation is the integration of over 250 government services into their Omni Neo App. This makes Bank of India the first financial institution to achieve such extensive integration with the UMANG platform, demonstrating a commitment to simplifying citizen services through technology.

Tailored Solutions for Diverse Customer Segments

Bank of India excels at crafting financial solutions precisely aligned with the unique needs of its varied clientele. This approach ensures that whether it's an individual seeking a personal loan or a large corporation requiring complex financing, the bank provides relevant and effective products.

The bank's commitment to tailored offerings is evident in its diverse product suite, encompassing specialized loan products and schemes. These are meticulously designed to address the distinct financial challenges and opportunities faced by each segment.

Bank of India's customer base is remarkably broad, reflecting its ability to serve a wide array of entities. This includes:

- Retail Customers: Individuals requiring banking services, loans, and investments.

- MSMEs (Micro, Small, and Medium Enterprises): Businesses needing working capital, expansion loans, and trade finance.

- Large Corporates: Major businesses seeking structured finance, project finance, and treasury services.

- Agricultural Sector: Farmers and agri-businesses requiring crop loans, equipment finance, and other agricultural credit facilities.

- Start-ups: New ventures looking for seed funding, venture debt, and advisory services.

- Government and Associates: Public sector entities and related organizations.

Commitment to Financial Inclusion and Social Impact

As a public sector bank, Bank of India is deeply committed to financial inclusion, a core value that drives its business model. This means actively working to bring banking services to those who have traditionally been excluded, such as individuals in rural areas or those with lower incomes. For instance, as of March 2024, Bank of India reported a substantial presence in rural and semi-urban areas, with a significant portion of its branches serving these essential communities. This focus not only aligns with national priorities for economic development but also builds trust and loyalty among a broad customer base.

The bank's dedication extends beyond just providing access to accounts; it encompasses offering affordable financial products and services tailored to the needs of underserved populations. This commitment to social impact is a key value proposition, resonating with a large segment of the Indian population who prioritize ethical and community-focused banking. Bank of India's initiatives in this area are crucial for fostering inclusive growth across the nation.

Furthermore, Bank of India actively promotes environmental responsibility and contributes to the well-being of the communities it serves. This includes supporting sustainable practices and engaging in corporate social responsibility activities that enhance the quality of life for its stakeholders. These efforts reinforce the bank's image as a responsible corporate citizen and a partner in national progress.

- Financial Inclusion Drive: Bank of India actively works to extend banking services to rural and underserved populations, a key component of its social impact strategy.

- Community Engagement: The bank invests in initiatives that promote environmental responsibility and contribute to the social and economic well-being of the communities where it operates.

- Alignment with National Goals: Its commitment to financial inclusion and social impact directly supports government objectives for economic development and equitable growth.

- Customer Trust: By prioritizing these values, Bank of India fosters strong relationships and builds trust with a diverse customer base, particularly those who value ethical banking practices.

Bank of India: Empowering India with Accessible & Innovative Banking Solutions

Bank of India offers a comprehensive suite of financial products and services, catering to a wide spectrum of customers from individuals to large corporations. Its value proposition centers on providing accessible, efficient, and innovative banking solutions. The bank's extensive network and digital capabilities ensure customers can manage their finances conveniently, anytime, anywhere.

The bank's commitment to financial inclusion and community development is a significant differentiator. By extending services to underserved populations and engaging in socially responsible initiatives, Bank of India builds strong customer loyalty and trust. This focus on societal well-being, coupled with robust financial performance, solidifies its position as a reliable financial partner.

For instance, as of March 31, 2024, Bank of India reported a total business of ₹12,39,323 crore, showcasing its substantial market presence and capacity. Furthermore, the bank’s integration of over 250 government services into its Omni Neo App highlights its dedication to leveraging technology for customer convenience and public service delivery.

Bank of India's value proposition is built on trust, accessibility, and tailored financial solutions. Its broad customer base, encompassing retail, MSME, corporate, and agricultural sectors, benefits from a diverse product portfolio. The bank's strong digital presence, exemplified by its Omni Neo App, enhances customer experience and operational efficiency.

| Value Proposition | Description | Key Metrics/Data (as of March 31, 2024) |

|---|---|---|

| Comprehensive Financial Services | Offers a wide range of banking products and services for all customer segments. | Total Business: ₹12,39,323 crore |

| Digital Accessibility & Innovation | Provides convenient 24/7 access through internet and mobile banking, with innovative service integration. | Over 250 government services integrated into Omni Neo App. |

| Financial Inclusion & Social Impact | Focuses on bringing banking services to rural and underserved populations, promoting economic development. | Significant branch presence in rural and semi-urban areas. |

| Trust and Reliability (Public Sector Bank) | Leverages government backing to ensure deposit security and build customer confidence. | Public Sector Banks collective net profit in FY 2023-24: ₹1,04,654 crore. |

Customer Relationships

Personalized Relationship Management

For its corporate clients and high-net-worth individuals, Bank of India frequently assigns dedicated relationship managers. These professionals offer tailored financial advice and proactive support, aiming to build robust, long-term client relationships. This personalized approach fosters deeper client engagement and loyalty.

Self-Service Digital Platforms

Bank of India heavily relies on self-service digital platforms like its mobile app and internet banking. These channels are crucial for everyday customer interactions, allowing users to manage accounts and perform transactions without direct staff assistance.

In 2024, a significant trend emerged with over 75% of Bank of India's retail customers actively using mobile apps and digital platforms for their banking needs. This highlights the growing preference for convenient, on-the-go financial management.

Branch-Based Customer Service

Despite the growing popularity of digital banking, Bank of India's extensive branch network continues to be a vital component of its customer relationship strategy. As of March 2024, the bank operated over 5,000 branches across India, providing a physical presence for customers who require face-to-face assistance.

These branches are essential for handling complex transactions, offering personalized financial advice, and catering to a significant segment of customers who value in-person interactions. Bank staff actively engage with customers, resolving queries and facilitating a wide range of banking operations, reinforcing the bank's commitment to direct customer support.

Call Center and Chatbot Support

Bank of India leverages call centers and AI-powered chatbots to provide robust customer support. This dual approach ensures customers can get immediate assistance for routine matters, enhancing accessibility and the speed of issue resolution.

- Call Center Accessibility: Offers a direct line for complex queries or personalized assistance.

- AI Chatbot Efficiency: In 2024, AI chatbots successfully managed over 70% of customer inquiries, significantly reducing wait times.

- Cost and Satisfaction Gains: The increased reliance on chatbots in 2024 led to a noticeable reduction in operational costs and a boost in customer satisfaction scores.

Community Engagement and Financial Literacy Programs

Bank of India actively fosters community engagement through dedicated financial literacy programs, especially targeting rural and semi-urban populations. These initiatives are crucial for building trust and educating individuals on sound financial practices.

By promoting responsible financial behavior, the bank not only empowers its customers but also contributes to overall economic stability. For instance, in 2024, Bank of India conducted over 500 financial literacy camps, reaching approximately 75,000 individuals across various regions.

- Community Outreach: Bank of India's commitment extends to active participation in local development projects.

- Financial Education: Programs focus on essential banking services, savings, credit, and investment awareness.

- Customer Trust: These efforts are designed to cultivate long-term relationships and enhance customer loyalty.

- Social Responsibility: Community development is a key component of the bank's corporate social responsibility framework.

Customer Engagement: Personal Service, Digital Reach, AI Support

Bank of India cultivates a multi-faceted customer relationship strategy, blending personalized service with digital efficiency. Dedicated relationship managers cater to high-value clients, while over 5,000 branches provide a physical touchpoint for diverse needs. Digital platforms, including a mobile app used by over 75% of retail customers in 2024, handle routine transactions, supported by call centers and AI chatbots that managed over 70% of inquiries that year.

| Relationship Channel | Key Features | 2024 Data/Impact |

|---|---|---|

| Relationship Managers | Personalized advice, proactive support for corporate and HNI clients | Fosters deep client engagement and loyalty |

| Branch Network | Physical presence for complex transactions, face-to-face interaction | Over 5,000 branches nationwide |

| Digital Platforms (Mobile App, Internet Banking) | Self-service for everyday banking, account management | Over 75% of retail customers actively using in 2024 |

| Call Centers & AI Chatbots | Immediate assistance, issue resolution | AI chatbots managed over 70% of inquiries in 2024, reducing wait times |

| Community Engagement | Financial literacy programs, local development participation | Over 500 financial literacy camps in 2024, reaching ~75,000 individuals |

Channels

Physical Branch Network

Bank of India's extensive physical branch network, both domestically and internationally, acts as a cornerstone for customer engagement. These branches are crucial for onboarding new customers, processing loan applications, and delivering a wide array of banking services. As of March 31, 2024, Bank of India operated 5,109 branches across India and 10,999 branches globally, demonstrating its significant physical footprint.

This network provides a vital touchpoint, particularly in areas where digital access might be less prevalent, ensuring a tangible presence for banking operations. The bank's reach extends beyond India's borders, with a presence in key international financial centers, facilitating global banking needs for its diverse clientele.

Automated Teller Machines (ATMs)

Automated Teller Machines (ATMs) serve as a crucial self-service channel, offering customers round-the-clock access to essential banking functions like cash withdrawals, balance checks, and mini-statements. This accessibility significantly enhances customer convenience by extending banking services beyond traditional branch hours.

In 2024, Bank of India continued its strategic investment in IT capital assets, with a notable focus on expanding and upgrading its ATM network. This initiative is a cornerstone of the bank's broader digital transformation strategy, aiming to bolster its digital service offerings and reach.

Internet Banking Portal

The Bank of India's internet banking portal serves as a primary digital channel, offering customers extensive capabilities from transaction execution and account management to bill payments and access to diverse financial services. This digital platform significantly enhances customer convenience by minimizing the necessity for in-person branch visits.

In 2024, India is set to implement interoperability for internet banking, a move designed to facilitate smoother, more integrated transaction experiences across different banking platforms.

Mobile Banking Applications (Omni Neo App)

Mobile banking applications offer unparalleled convenience, allowing customers to manage their finances anytime, anywhere. Bank of India's Omni Neo App exemplifies this, providing a comprehensive suite of services from fund transfers and bill payments to account management and even digital loan applications.

The Omni Neo App's strategic integration with over 250 government services significantly enhances its utility and reach. This move positions the app as a central hub for both personal banking and essential citizen services, driving user engagement and digital adoption.

- On-the-go financial management: Access to transfers, bill payments, and account monitoring.

- Digital loan applications: Streamlined process for availing credit facilities.

- Integration with 250+ government services: Broadened utility beyond traditional banking.

- Enhanced user experience: Providing a seamless and accessible digital banking platform.

Business Correspondents and Agent Networks

Bank of India leverages business correspondents and agent networks as a crucial component of its strategy to boost financial inclusion, especially in rural and remote regions.

These networks act as extensions of the bank, enabling basic banking transactions and bringing essential financial services closer to underserved communities. This initiative aligns with broader government objectives to ensure widespread access to banking for all citizens, including the underprivileged.

- Financial Inclusion Drive: Business correspondents and agent networks are vital for reaching unbanked and underbanked populations.

- Extended Reach: These agents provide access to services like account opening, deposits, and withdrawals in areas where physical branches are scarce.

- Government Mandate: The expansion of these networks supports national financial inclusion goals, making banking more accessible to the common public.

- 2024 Data Insight: As of early 2024, India's financial inclusion efforts have seen significant progress, with millions of new accounts opened through such agent-led models, demonstrating their effectiveness in deepening financial penetration.

Bank's Multi-Channel Reach: Digital Growth & Financial Inclusion

Bank of India utilizes a multi-channel approach to reach its customers, encompassing a vast physical branch network, ATMs, internet banking, mobile applications, and business correspondents. This comprehensive strategy ensures accessibility and convenience for a diverse customer base, catering to both traditional and digital banking needs.

The bank's digital channels, particularly its mobile app, are seeing significant growth and integration with government services, enhancing their utility. Business correspondents play a vital role in extending financial inclusion to remote areas, aligning with national objectives.

| Channel | Description | Key Feature/2024 Insight |

|---|---|---|

| Physical Branches | Extensive network for customer onboarding and comprehensive services. | 5,109 branches in India as of March 31, 2024. |

| ATMs | 24/7 self-service for essential banking transactions. | Continued expansion and upgrades as part of digital transformation. |

| Internet Banking | Online platform for account management and transactions. | Focus on interoperability for smoother transactions in 2024. |

| Mobile Banking (Omni Neo App) | Anytime, anywhere access to banking and integrated government services. | Integration with over 250 government services. |

| Business Correspondents | Extending financial services to rural and remote areas. | Crucial for financial inclusion, reaching unbanked populations. |

Customer Segments

Retail Individuals

Retail individuals, a cornerstone of Bank of India's business, encompass a broad spectrum of customers including salaried professionals, students, and retirees. These clients primarily seek essential banking services such as savings and current accounts, alongside credit facilities like personal loans, home loans, and vehicle loans. The bank offers a comprehensive suite of products designed to meet their diverse financial needs, from basic deposit accounts to more complex lending solutions.

In 2024, Bank of India continued to focus on expanding its retail customer base, leveraging digital platforms to enhance accessibility and convenience. The bank reported a significant increase in digital transactions, reflecting the growing adoption of online and mobile banking services among its individual customers. This segment represents a substantial portion of the bank's overall customer deposits and loan portfolio, highlighting its critical importance to the bank's financial health and growth strategy.

Micro, Small, and Medium Enterprises (MSMEs)

Micro, Small, and Medium Enterprises (MSMEs) are a vital customer base for the Bank of India, needing essential financial tools. These businesses require working capital loans to manage day-to-day operations, term loans for expansion, and trade finance for international commerce. Digital payment solutions are also key for their efficiency.

The importance of this segment is highlighted by the significant credit growth. As of November 2024, credit extended to MSMEs saw a robust year-on-year increase of 13%, demonstrating their growing financial needs and the bank's commitment to serving them.

Large Corporates and Institutions

Large corporates and institutions represent a crucial customer segment for Bank of India, encompassing major businesses, government bodies, and other significant entities. These clients require sophisticated financial solutions tailored to their scale and complexity.

Bank of India offers a robust suite of corporate banking services to this segment, including project finance for large-scale undertakings, syndicated loans for substantial funding needs, and comprehensive foreign exchange services for international transactions. The bank also provides efficient cash management solutions to optimize liquidity and operational efficiency for these major players.

In 2024, Bank of India continued to strengthen its focus on corporate banking, aiming to support India's economic growth by providing essential financial infrastructure. The bank's commitment to this segment is reflected in its ongoing efforts to expand its reach and service offerings to meet the evolving demands of large enterprises and public sector undertakings.

Agricultural Sector (Farmers and Agri-Businesses)

Farmers and agri-businesses represent a crucial customer segment for the Bank of India, requiring tailored financial products like agricultural loans and crop loans. The bank actively supports rural development through these specialized financial services.

Priority Sector Advances, with a strong emphasis on agriculture credit, are a key strategic focus for public sector banks like the Bank of India. This commitment reflects the government's push to bolster the agricultural economy.

- Agricultural Loans: The Bank of India offers various loan products to support farmers for purchasing seeds, fertilizers, machinery, and other farming needs.

- Crop Loans: Short-term loans specifically designed to cover the cultivation expenses of crops, helping farmers manage their seasonal financial requirements.

- Rural Development Focus: The bank's financial support extends to broader rural development initiatives, indirectly benefiting the agricultural ecosystem.

- Priority Sector Lending: As of March 31, 2024, the Bank of India reported significant advances under Priority Sector Lending, with agriculture forming a substantial portion, underscoring its commitment to this segment.

Non-Resident Indians (NRIs) and International Clients

Bank of India actively engages with Non-Resident Indians (NRIs) and international clients, offering tailored financial solutions. This segment benefits from the bank's expertise in foreign exchange services and efficient remittance channels, facilitating seamless cross-border transactions.

The bank provides specialized NRI banking products designed to meet the unique investment and savings needs of this global clientele. This includes various deposit schemes and investment opportunities that cater to the Indian diaspora.

Bank of India's expansive international network, with branches and representative offices in key global financial hubs, enables it to effectively serve its diverse international customer base. This strategic presence underscores its commitment to global banking.

- Foreign Exchange Services: Facilitating currency conversions and managing international payments.

- Remittance Solutions: Offering efficient and cost-effective ways for clients to send money back to India.

- Specialized NRI Products: Including NRE/NRO accounts, FCNR deposits, and investment advisory services.

- Global Presence: Branches in countries like the UK, USA, France, and Singapore to support international clients.

Bank's Customer Segments: Strategic Focus in 2024

Retail individuals form a significant customer base for Bank of India, encompassing a wide demographic from students to retirees. They primarily utilize core banking services like savings and current accounts, alongside credit products such as personal, home, and vehicle loans. In 2024, the bank saw increased digital transaction volumes, indicating a growing reliance on online and mobile banking among these customers.

MSMEs are a vital segment, requiring working capital, term loans, and trade finance. Bank of India's support for this sector is evident, with credit to MSMEs growing by 13% year-on-year as of November 2024, highlighting their increasing financial needs and the bank's role in their growth.

Large corporates and institutions depend on sophisticated financial solutions, including project finance, syndicated loans, and foreign exchange services. Bank of India's focus on corporate banking in 2024 aimed to bolster India's economic infrastructure by serving these major enterprises and public sector undertakings.

Farmers and agri-businesses are crucial, receiving tailored financial products like agricultural and crop loans. Bank of India's commitment to Priority Sector Lending, with agriculture as a substantial component, was evident as of March 31, 2024, reinforcing its support for rural development.

Non-Resident Indians (NRIs) and international clients are served with specialized products, foreign exchange services, and efficient remittance channels. The bank's global presence, including branches in the UK, USA, France, and Singapore, facilitates these cross-border transactions effectively.

| Customer Segment | Key Needs | 2024 Focus/Data Points |

| Retail Individuals | Savings, Loans, Digital Banking | Increased digital transaction volumes |

| MSMEs | Working Capital, Term Loans, Trade Finance | 13% YoY credit growth (Nov 2024) |

| Large Corporates & Institutions | Project Finance, Syndicated Loans, Forex | Strengthening corporate banking services |

| Farmers & Agri-businesses | Agri Loans, Crop Loans, Rural Development | Significant advances in agriculture credit (Mar 2024) |

| NRIs & International Clients | NRI Accounts, Remittances, Forex | Global presence in key financial hubs |

Cost Structure

Interest Expenses on Deposits

Interest expenses on deposits represent the most significant cost for Bank of India, directly impacting profitability. This cost is largely determined by the volume of deposits the bank attracts and the prevailing market interest rates. For instance, Bank of India's net interest income saw robust growth, reaching Rs 5,937 crore in the fourth quarter of fiscal year 2024, indicating effective management of these interest expenses relative to interest earned.

Employee Salaries and Benefits

Employee salaries and benefits represent a significant expenditure for Bank of India, reflecting its substantial workforce spread across numerous branches and operational departments. This cost category encompasses not only base salaries and wages but also includes bonuses, health insurance, retirement contributions, and other essential employee welfare programs. In fiscal year 2023-24, the bank's employee expenses were a key component of its overall operating costs, underscoring the human capital investment required to maintain its extensive service network and diverse banking operations.

Technology and Infrastructure Costs

Bank of India's technology and infrastructure costs are significant, encompassing substantial investments in IT systems, software, and digital platforms. These expenditures are crucial for enhancing digital banking services and maintaining operational efficiency.

In the fiscal year 2023-24, the bank continued its focus on IT capital expenditure to bolster its digital transformation. This includes the development and maintenance of its online banking portals, mobile applications, and the underlying infrastructure supporting these services.

Cybersecurity measures and the upkeep of data centers and ATM networks also form a considerable portion of these costs. These investments are vital for safeguarding customer data and ensuring the uninterrupted availability of banking services.

Branch Network and Operational Costs

Bank of India's extensive branch network, both within India and internationally, represents a substantial portion of its cost structure. These costs encompass various elements like property rent, essential utilities, robust security measures, and ongoing administrative overheads associated with managing these physical locations.

For instance, as of March 31, 2024, Bank of India operated 5,094 branches across India and 11 overseas branches. The expenses related to maintaining this widespread infrastructure are a key component of its operational expenditure, directly impacting profitability.

- Branch Network Costs: Rent, utilities, and maintenance for over 5,000 domestic and 11 international branches.

- Administrative Expenses: Salaries and benefits for branch staff, IT support, and general office management.

- Security and Compliance: Costs associated with physical security, regulatory compliance, and operational risk management at each location.

- International Operations: Additional costs for operating in foreign markets, including licensing, local regulations, and currency management.

Regulatory Compliance and Provisioning Costs

Bank of India faces substantial costs related to regulatory compliance and provisioning. These include expenses for adhering to stringent banking regulations, external audit fees, and setting aside funds for potential loan losses. For instance, the bank's provisioning for non-performing assets (NPAs) saw a notable increase, reaching Rs 2,043 crore in the fourth quarter of fiscal year 2024.

- Regulatory Adherence: Costs incurred to meet Reserve Bank of India (RBI) guidelines and other financial regulations.

- Audit and Assurance: Fees paid to external auditors for financial statement audits and compliance checks.

- NPA Provisions: Funds set aside to cover potential losses from loans that are unlikely to be repaid, with Q4 FY24 provisions at Rs 2,043 crore.

Bank of India's Core Cost Drivers Revealed

Interest expenses on deposits remain the primary cost driver for Bank of India, directly influencing net interest margins. These costs are sensitive to deposit volumes and prevailing market rates, with the bank reporting robust net interest income growth in FY24.

Employee costs, encompassing salaries, benefits, and welfare programs, represent a significant expenditure due to the bank's extensive workforce and branch network. These human capital investments are crucial for maintaining operational capabilities and customer service.

Technology and infrastructure investments are substantial, covering IT systems, digital platforms, cybersecurity, and data center upkeep, essential for modern banking services and operational efficiency.

The extensive domestic and international branch network incurs considerable costs related to rent, utilities, security, and administration, impacting overall operational expenditure.

Regulatory compliance and provisioning for potential loan losses are also key cost components, with significant provisions made for non-performing assets in recent quarters.

| Cost Category | Description | FY24 Impact/Data |

|---|---|---|

| Interest Expenses | On deposits and borrowings | Major cost driver; Net Interest Income Rs 5,937 crore in Q4 FY24 |

| Employee Expenses | Salaries, benefits, bonuses | Significant expenditure due to large workforce and branch network |

| Technology & Infrastructure | IT systems, digital platforms, cybersecurity | Ongoing investment for digital transformation and operational efficiency |

| Branch Network Costs | Rent, utilities, security for branches | Costs for 5,094 domestic and 11 international branches |

| Provisions & Contingencies | For NPAs and regulatory compliance | Q4 FY24 provisions for NPAs were Rs 2,043 crore |

Revenue Streams

Net Interest Income (NII)

Net Interest Income (NII) is the bedrock of Bank of India's profitability. This income is generated from the core banking activity of lending money out at a higher interest rate than it pays to depositors. For the fourth quarter of fiscal year 2024, Bank of India reported a robust NII of ₹5,937 crore, marking a significant 7% increase.

Looking at the full fiscal year 2024, the Bank of India's Net Interest Income demonstrated strong growth, reaching ₹23,053 crore. This represents a substantial 14% jump compared to the previous year, highlighting the bank's effective management of its interest-earning assets and interest-bearing liabilities.

Fees and Commission Income

Bank of India generates significant revenue through various fees and commissions. This income stream stems from services like transaction processing, foreign exchange operations, and trade finance facilitation. For instance, in the fiscal year 2023-24, the bank reported a substantial portion of its non-interest income from fees and commissions, reflecting the breadth of its service offerings.

Loan Processing and Service Charges

Bank of India generates revenue through fees associated with processing loan applications and originating loans. These charges are applied to various loan types, reflecting the complexity and scale of each financial product. For instance, in the fiscal year ending March 31, 2024, the bank’s net interest income, which is the primary revenue driver, was ₹32,706 crore, while other income, including fees and commissions, also contributed significantly to its overall earnings.

Foreign Exchange and Trade Finance Gains

Bank of India generates revenue through foreign exchange transactions, international remittances, and trade finance services. These include profits from currency conversions, facilitating cross-border payments, and offering instruments like letters of credit and bank guarantees to support global trade.

In the fiscal year ending March 31, 2024, Bank of India reported robust growth in its foreign exchange and trade finance segments. The bank's net foreign exchange earnings saw a significant uptick, contributing positively to its overall profitability.

- Foreign Exchange Gains: Profits earned from the buy-sell spread on currency transactions and hedging activities.

- Trade Finance Income: Revenue generated from issuing and advising on letters of credit, bank guarantees, and other trade-related instruments.

- Remittance Services: Fees and commissions earned on facilitating international money transfers for individuals and businesses.

- Market Volatility: Fluctuations in currency markets can impact the profitability of foreign exchange operations.

Investment and Treasury Gains

Bank of India's investment and treasury operations are significant revenue generators. This includes income from its diverse investment portfolio, which comprises government securities, corporate bonds, and other financial market instruments. These activities contribute directly to the bank's profitability through capital appreciation and interest income.

The bank actively manages its treasury to optimize returns and manage liquidity. In the fiscal year 2023-24, Bank of India reported robust treasury gains, reflecting effective deployment of funds and favorable market conditions. For instance, its investment portfolio performance showcases its ability to generate income beyond traditional lending activities.

- Investment Portfolio Income: Gains from trading and holding government securities and bonds.

- Treasury Operations: Profit generated from foreign exchange dealings, money market operations, and liquidity management.

- Market Instruments: Income derived from investments in various financial instruments like debentures and equities.

- Fiscal Year 2023-24 Performance: Specific figures for treasury gains would demonstrate the scale of this revenue stream.

Bank's Diverse Revenue: A Financial Overview

Bank of India's revenue streams are diverse, extending beyond its core Net Interest Income. Fees and commissions from various banking services, such as transaction processing and trade finance, form a crucial component of its earnings. Additionally, the bank capitalizes on foreign exchange operations and its investment and treasury activities to generate profits.

For the fiscal year ending March 31, 2024, Bank of India's Net Interest Income reached ₹32,706 crore, a testament to its lending prowess. Complementing this, other income, encompassing fees, commissions, and treasury gains, also played a significant role in its overall financial performance, demonstrating a well-rounded approach to revenue generation.

The bank's commitment to international business is reflected in its foreign exchange and trade finance income. These segments, which include profits from currency conversions and trade facilitation services, saw robust growth in fiscal year 2023-24, contributing positively to the bank's bottom line.

Investment and treasury operations further bolster Bank of India's revenue. Income from its investment portfolio, which includes government securities and corporate bonds, along with effective liquidity management, ensures consistent returns and capital appreciation.

| Revenue Stream | FY 2023-24 (₹ Crore) | FY 2022-23 (₹ Crore) | Year-on-Year Change |

|---|---|---|---|

| Net Interest Income (NII) | 32,706 | 28,789 | +13.6% |

| Other Income (Fees, Commissions, Forex, Treasury) | 12,189 | 10,890 | +11.9% |

| Total Income | 44,895 | 39,679 | +13.2% |

Business Model Canvas Data Sources

The Bank of India Business Model Canvas is built upon a foundation of financial statements, regulatory filings, and extensive market research. These sources provide a comprehensive view of the bank's operations, customer base, and competitive landscape.