Shin Kong Financial Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Shin Kong Financial Bundle

Go Beyond the Preview—Access the Full Strategic Report

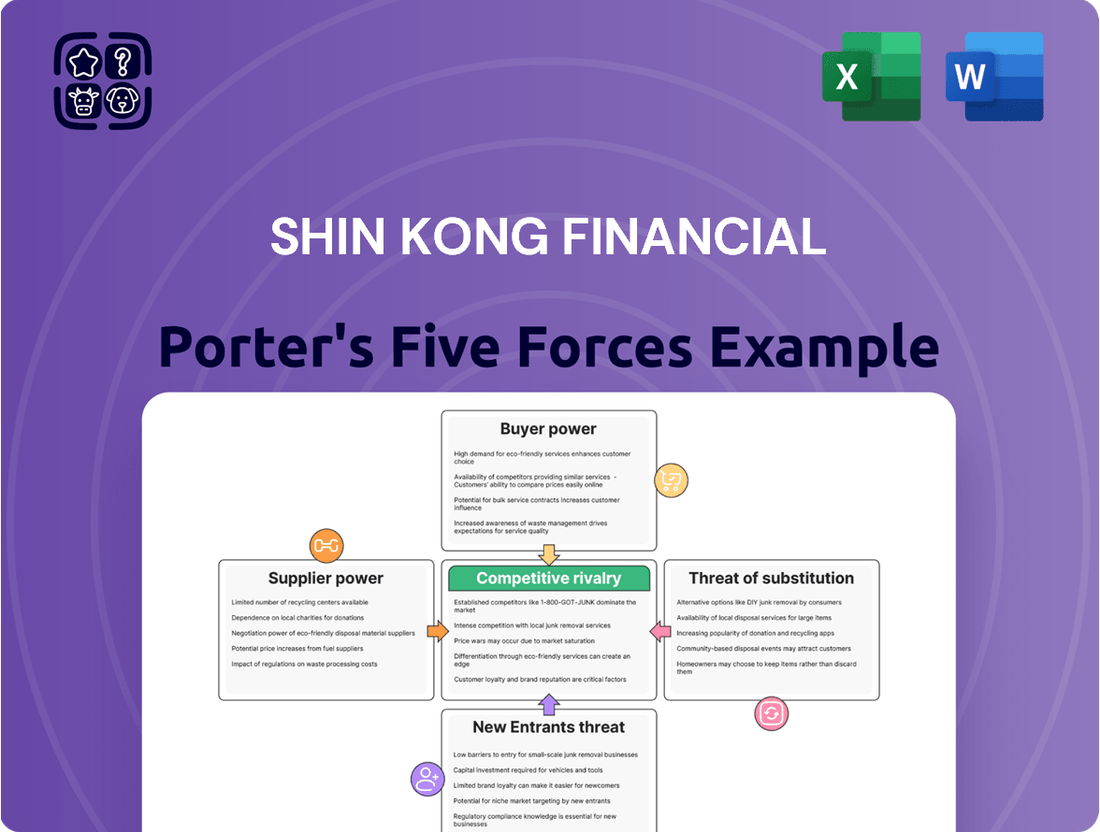

Shin Kong Financial navigates a competitive landscape shaped by the bargaining power of its customers and the threat of new entrants entering the financial services market. Understanding these forces is crucial for strategic planning.

The intensity of rivalry among existing competitors significantly impacts Shin Kong Financial's market share and profitability. Analyzing this dynamic reveals key competitive strategies.

Furthermore, the availability of substitute financial products and services presents a constant challenge, pushing Shin Kong Financial to innovate and differentiate its offerings.

The bargaining power of suppliers, though often less pronounced in finance, can still influence operational costs and service delivery for Shin Kong Financial.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shin Kong Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Capital Providers

In the financial industry, capital is a primary input, with suppliers including depositors, bondholders, and equity investors. For a large diversified group like Shin Kong Financial, the bargaining power of these capital providers is moderate. Shin Kong Financial’s substantial asset base, reaching NT$4.99 trillion by the end of 2023, and diversified revenue streams, reduce reliance on any single funding source. Its established reputation provides access to a wide range of capital markets, mitigating supplier influence. This broad access ensures funding stability for operations and growth.

Human Capital

Skilled professionals like actuaries, investment bankers, wealth managers, and specialized IT staff are vital suppliers of labor for Shin Kong Financial. Their bargaining power is notably high due to the specialized knowledge and certifications required, coupled with intense competition for top talent within Taiwan's financial sector. For instance, the demand for AI and data science professionals in finance surged by over 30% in Taiwan in 2024, driving up compensation packages. The ability to attract and retain these key employees is critical for fostering innovation and maintaining a competitive edge in a dynamic market.

Technology and Data Vendors

Suppliers of crucial technology, like core banking software, trading platforms, cybersecurity solutions, and financial data providers such as Bloomberg and Refinitiv, exert significant power over Shin Kong Financial. The substantial costs and operational disruptions involved in switching between these deeply integrated systems give vendors considerable leverage. For instance, global financial services IT spending was projected to exceed 650 billion USD in 2024. The increasing reliance on advanced AI and digital platforms further strengthens these vendors' negotiation positions due to their specialized offerings and the critical nature of their services.

Reinsurers

Reinsurers serve as critical suppliers for Shin Kong Financial’s life insurance subsidiary, enabling effective risk management and diversification across its portfolio. Their bargaining power significantly hinges on the global reinsurance market's overall capacity and the specific types of risks being underwritten. A concentrated reinsurance market, like the one seen in 2024 with major players dominating, can empower these suppliers to dictate more stringent terms and higher pricing for risk transfer. This directly impacts Shin Kong’s operational costs and profitability.

- Global reinsurance capacity in 2024 remained constrained, particularly for property catastrophe risks.

- Major reinsurers reported strong results in early 2024, indicating firm pricing conditions.

- Shin Kong must navigate a market where reinsurers hold leverage due to high demand.

- Increased capital requirements for reinsurers also contribute to higher pricing demands.

Regulatory and Compliance Services

Regulatory and compliance service providers, including consulting firms, auditors, and legal experts, hold significant bargaining power over Shin Kong Financial. Their specialized knowledge ensures adherence to Taiwan's stringent financial regulations, particularly from the Financial Supervisory Commission (FSC). Given the continuous updates to regulations, these services are non-negotiable for operating within the banking and insurance sectors, making their expertise essential in 2024.

- FSC's evolving regulatory landscape, including new directives on green finance and digital security, necessitates constant expert guidance.

- The cost of non-compliance, such as fines or operational restrictions, far outweighs the expense of these critical services.

Supplier Power: The $12T Digital Payment Influence

Payment network providers, like Visa and Mastercard, hold significant bargaining power over Shin Kong Financial’s banking operations. Their global infrastructure and near-monopoly in transaction processing make them indispensable. Switching costs are extremely high, given the deep integration required and the loss of network effects. In 2024, global digital payment transaction values are projected to exceed 12 trillion USD, underscoring the critical role and leverage of these essential suppliers.

| Supplier Type | Bargaining Power | 2024 Impact |

|---|---|---|

| Payment Networks | High | Projected $12T+ global digital payments |

| Reinsurers | High | Constrained global capacity, firm pricing |

| Skilled Labor | High | 30%+ surge in demand for AI/data talent in Taiwan |

What is included in the product

This analysis dissects Shin Kong Financial's competitive environment by examining the intensity of rivalry, bargaining power of buyers and suppliers, threat of new entrants, and the availability of substitutes.

Instantly visualize the competitive landscape of the financial services industry, identifying potential threats and opportunities with Shin Kong Financial's Porter's Five Forces Analysis.

Customers Bargaining Power

Individual (Retail) Customers

Individual customers hold significant collective bargaining power over Shin Kong Financial's banking, insurance, and securities offerings. Taiwan's highly competitive financial landscape, with over 30 domestic banks and numerous insurance providers in 2024, means retail clients face low switching costs for many standardized products. The increasing availability of online comparison platforms, such as those that saw a 15% rise in usage for financial products in 2024, further empowers customers. This transparency allows them to easily seek the best terms, pushing institutions like Shin Kong Financial to offer competitive rates and services.

Corporate Clients

Corporate clients, especially those with large transaction volumes, wield significant bargaining power over financial institutions like Shin Kong Financial.

In 2024, these major clients, often requiring substantial loans and intricate investment banking services, can negotiate highly favorable terms and customized financial solutions.

Shin Kong’s ability to offer an integrated suite of services, encompassing banking, insurance, and securities, helps to mitigate this power.

By fostering comprehensive and sticky relationships, Shin Kong aims to retain these valuable clients, despite their strong leverage in the competitive financial landscape.

High-Net-Worth Individuals (HNWIs)

High-Net-Worth Individuals (HNWIs) possess significant bargaining power within wealth management, including services offered by institutions like Shin Kong Financial. These clients demand highly personalized services, sophisticated investment products, and competitive fee structures. In 2024, the global HNWI population is projected to grow, intensifying the competition among financial institutions to attract and retain this lucrative segment. This fierce competition, with institutions vying for assets under management, grants HNWIs considerable leverage to negotiate terms and fees, impacting profitability.

Institutional Investors

Institutional investors, including major pension funds and large corporations, represent a formidable customer segment for Shin Kong Financial's asset management and securities businesses. Their significant asset base, often reaching hundreds of billions of New Taiwan Dollars in managed assets by 2024, grants them considerable leverage. This scale allows them to actively negotiate for reduced management fees and highly customized investment mandates. Their market sophistication and sheer volume of capital give them a very strong negotiating position.

- Major institutional clients typically manage portfolios exceeding NT$100 billion.

- Fee compression is a common demand, with institutional investors securing discounts of 10-20% on standard fees in 2024.

- Customized mandates often include specific ESG criteria or performance benchmarks.

- Their ability to switch providers due to scale enhances their bargaining power.

Price Sensitivity and Information Asymmetry

Customer bargaining power significantly rises due to heightened price sensitivity and reduced information asymmetry, driven by digital platforms. Consumers can readily compare financial products like Shin Kong Financial’s loan rates, insurance premiums, and investment fees online. For instance, in 2024, online comparison sites have seen a surge in users seeking competitive rates, empowering customers. Regulatory bodies, such as Taiwan’s Financial Supervisory Commission, further bolster consumer protection, reinforcing their position.

- Digital platforms facilitate instant rate comparisons, enhancing customer leverage.

- Increased transparency means customers are less reliant on single providers.

- Regulatory oversight strengthens consumer rights and bargaining power.

- The competitive landscape forces financial institutions to offer more attractive terms.

Empowered Clients Drive Terms in Taiwan's Finance Sector

Customers of Shin Kong Financial, spanning individuals to institutional investors, wield substantial bargaining power. This stems from Taiwan's competitive financial landscape, where over 30 banks and many insurers drive low switching costs. Digital platforms, seeing a 15% rise in financial product usage in 2024, empower customers to compare terms easily. Major clients and HNWIs leverage their scale and demand for tailored solutions, securing favorable rates.

| Customer Segment | Key Leverage Factor | 2024 Impact |

|---|---|---|

| Individual Customers | Low switching costs, online comparison | 15% rise in online financial product comparison usage |

| Corporate Clients | Large transaction volumes, complex needs | Negotiate highly favorable, customized solutions |

| High-Net-Worth Individuals | Demand for personalized services, competition for AUM | Intensified competition for lucrative segments |

| Institutional Investors | Significant asset base (NT$100B+), market sophistication | Secure 10-20% fee discounts on standard rates |

Preview the Actual Deliverable

Shin Kong Financial Porter's Five Forces Analysis

This preview displays the complete Shin Kong Financial Porter's Five Forces Analysis, ensuring you receive the exact, professionally formatted document you see here upon purchase. You can expect immediate access to this comprehensive analysis, ready for your strategic planning without any hidden elements or placeholder content. The insights into Shin Kong Financial's competitive landscape, including threats from new entrants, the bargaining power of buyers and suppliers, and the intensity of rivalry, are all present and accurate in this preview. This means the document you are currently viewing is precisely what will be delivered to you, allowing for confident decision-making.

Rivalry Among Competitors

Saturated and Fragmented Market

The Taiwanese financial services market is intensely competitive, marked by its highly saturated and fragmented nature. This environment sees numerous domestic financial holding companies, banks, and insurance firms vying for customer attention and market share. As of late 2023 and early 2024, Taiwan had over 35 domestic banks and numerous insurance providers, contributing to fierce rivalry. This intense competition often drives firms like Shin Kong Financial to compete aggressively on price, service quality, and product innovation, such as digital banking solutions and tailored insurance packages, making differentiation crucial.

Major Domestic Competitors

Shin Kong Financial faces intense direct competition from established Taiwanese financial powerhouses like Cathay Financial Holding and Fubon Financial Holding. These dominant rivals, each with significant market capitalization exceeding NT$1 trillion in 2024, offer a comprehensive suite of financial services, leading to head-to-head battles across all key segments, from banking to insurance. The proposed merger between Taishin FHC and Shin Kong FHC, a major development in 2024, highlights a clear industry trend towards consolidation to enhance competitive positioning and operational scale. This drive aims to create larger entities capable of capturing greater market share and achieving stronger profitability in a saturated market.

Foreign and Niche Players

Competition for Shin Kong Financial also stems from local branches of foreign banks and specialized niche players. These foreign entities, such as HSBC or Citibank branches in Taiwan, often target specific segments like wealth management or corporate banking, leveraging global networks. Niche players focus on specific product areas, for instance, fintech firms specializing in digital lending or payment solutions, which saw significant growth in 2024. While they may not offer Shin Kong's full breadth of services, their focused approach allows them to be highly competitive and agile in their target markets. This concentrated competition adds significant pressure, particularly in profitable segments.

Competition on Digital Innovation

Competitive rivalry increasingly centers on digital transformation, with firms like Shin Kong Financial fiercely competing to offer superior online and mobile banking experiences. Financial institutions are rapidly deploying robo-advisory services and innovative fintech solutions to attract and retain customers in 2024. This trend is significantly fueled by the Taiwanese government's proactive promotion of fintech development and open banking initiatives, pushing for greater digital integration across the sector.

- Taiwan's digital banking penetration reached nearly 70% by early 2024, highlighting the shift.

- Fintech investment in Taiwan continues to grow, with a focus on AI-driven services.

- Shin Kong Financial's peers are expanding mobile app functionalities and digital payment options.

- New regulations in 2024 support open banking APIs, intensifying data-driven service competition.

Regulatory-Driven Competition

Regulatory initiatives, such as the Financial Supervisory Commission's (FSC) promotion of Green Finance Action Plan 3.0, create new competitive arenas for Shin Kong Financial and its peers. Institutions are actively vying to establish leadership in ESG-related products, attracting socially conscious investors. For instance, the FSC aims for Taiwan's green and sustainability bonds to reach NT$1.5 trillion by 2027, fostering intense competition in 2024. This compliance and market positioning are crucial for long-term growth.

- FSC's Green Finance Action Plan 3.0 drives 2024 competition.

- Financial firms compete for ESG product leadership.

- Aim to attract socially conscious investors.

- FSC targets NT$1.5 trillion in green bonds by 2027.

Taiwan Finance: Competing Amidst Digital, ESG, and Consolidation

Shin Kong Financial operates within Taiwan's highly saturated financial market, facing intense competition from over 35 domestic banks and dominant rivals like Cathay and Fubon, both exceeding NT$1 trillion market capitalization in 2024. The competitive landscape is shaped by digital transformation, with nearly 70% digital banking penetration, and by the push for ESG-focused products under the FSC's Green Finance Action Plan 3.0. Industry consolidation, such as the proposed Taishin-Shin Kong merger in 2024, signals a strategic move to enhance competitive positioning against both established players and agile fintech firms.

| Competitive Factor | 2024 Market Data | Impact on Shin Kong Financial |

|---|---|---|

| Domestic Banks | Over 35 operating banks | High fragmentation, price competition |

| Major Rivals' Market Cap | Cathay, Fubon > NT$1 trillion | Significant scale disadvantage, intense direct competition |

| Digital Banking Penetration | Nearly 70% by early 2024 | Pressure for digital innovation, customer retention |

| ESG Bond Target (FSC) | NT$1.5 trillion by 2027 | New competitive arena for green finance products |

SSubstitutes Threaten

FinTech and Digital-Only Banks

FinTech startups and digital-only banks pose a substantial substitute threat to Shin Kong Financial, offering streamlined, often cheaper alternatives for various financial services. These digital players, like Rakuten Bank or Line Bank in Taiwan, leverage technology to provide user-friendly platforms for payments, lending, and investment, directly challenging traditional branch networks. For instance, digital-only banks have seen significant growth, with some projecting over 200 million users globally by 2024, attracting customers with lower fees and enhanced accessibility.

Robo-Advisors and Automated Investing

Robo-advisors and automated platforms pose a significant substitute threat to Shin Kong Financial's traditional wealth management services. These low-cost, algorithm-based solutions appeal strongly to younger, tech-savvy demographics seeking accessible investment options. Global robo-advisor assets under management are projected to reach approximately $2.5 trillion in 2024. This rapid growth puts considerable pressure on the fee structures and client acquisition strategies of established financial institutions like Shin Kong Financial.

Peer-to-Peer (P2P) Lending Platforms

Peer-to-Peer lending platforms offer an alternative for borrowing and lending, directly connecting individuals and small businesses with investors, thereby bypassing traditional financial institutions like Shin Kong Bank. Although P2P lending remains a relatively small segment of Taiwan's financial market, it presents a growing substitute for Shin Kong Bank's consumer and small business loan products. In 2024, the total loan volume on Taiwanese P2P platforms, while increasing, is still a fraction compared to the overall banking sector. These platforms provide competitive rates and faster processing, appealing to a segment of borrowers seeking alternatives outside conventional banking channels.

Cryptocurrencies and Decentralized Finance (DeFi)

Cryptocurrencies and DeFi platforms are emerging as substitutes for traditional financial services like payments and lending, posing a competitive threat to Shin Kong Financial. While the Taiwanese government, through the Financial Supervisory Commission (FSC), has maintained a cautious stance, it is actively establishing regulatory frameworks for virtual assets, signaling their increasing legitimacy. For instance, Taiwan's Virtual Asset Service Providers (VASPs) are subject to anti-money laundering (AML) regulations as of 2023, with further comprehensive frameworks expected to mature by 2025, indicating a long-term shift. The global DeFi market capitalization reached over $100 billion in early 2024, highlighting its growing scale.

- Taiwan's FSC is developing comprehensive VASP regulations for 2025.

- Global DeFi market cap exceeded $100 billion in early 2024.

- Crypto offers alternatives for payments, lending, and trading.

- Increased regulatory clarity could accelerate adoption in Taiwan.

Direct Investment and Disintermediation

Sophisticated investors and corporations increasingly bypass traditional financial intermediaries, opting for direct investment avenues. This disintermediation threat sees entities directly funding startups, acquiring real estate, or engaging capital markets without relying on institutions like Shin Kong Financial. For example, global direct private equity investments reached record highs in 2024, reflecting this trend.

- Direct private equity investments continue to grow, reducing reliance on traditional banks for corporate financing.

- Retail investors in 2024 have more accessible platforms for direct stock and bond purchases, bypassing brokerage fees.

- Real estate crowdfunding platforms allow direct fractional ownership, competing with traditional mortgage lending.

- Blockchain-based finance offers decentralized alternatives for lending and asset management.

Substitute Threats: Reshaping the Financial Landscape

Shin Kong Financial faces significant substitute threats from FinTech, digital-only banks, and robo-advisors, which offer more accessible and often cheaper financial services. For instance, global robo-advisor assets are projected to reach $2.5 trillion in 2024, attracting tech-savvy users. Emerging alternatives like P2P lending platforms and the rapidly growing global DeFi market, exceeding $100 billion in early 2024, further challenge traditional banking. Additionally, sophisticated investors increasingly bypass intermediaries, with direct private equity investments reaching record highs in 2024.

| Substitute Type | 2024 Market Trend | Impact on Shin Kong |

|---|---|---|

| Robo-Advisors | $2.5T AUM projected | Pressure on wealth management fees |

| Global DeFi | >$100B market cap | Alternative for payments, lending |

| Direct Investment | Record private equity highs | Disintermediation of corporate finance |

Entrants Threaten

High Regulatory Barriers

The threat of new entrants for Shin Kong Financial is notably low due to Taiwan's extremely high regulatory barriers in its financial services industry. Any new entity must secure a license from the Financial Supervisory Commission (FSC), a process known for its stringent requirements and lengthy approval timelines, often taking years. This applies uniformly across banking, insurance, and securities sectors, making it exceptionally difficult for new companies to establish operations from scratch. For instance, the FSC maintains strict capital adequacy ratios and operational compliance, making market entry prohibitive for all but the most well-resourced new players.

Substantial Capital Requirements

Establishing a new bank or insurance company, like those under Shin Kong Financial, demands substantial capital, which naturally deters many potential new entrants. For instance, setting up an online-only life insurance company in Taiwan requires a minimum capital of TWD 2 billion. These significant financial hurdles drastically limit the pool of potential new competitors. As of 2024, such stringent regulatory capital requirements remain a robust defense against new market disruption. This high barrier to entry protects established financial institutions.

Brand Recognition and Customer Trust

Established financial stalwarts like Shin Kong Financial, a prominent player in Taiwan, command significant brand recognition and deep-rooted customer trust cultivated over decades. A new entrant faces a formidable barrier, struggling to replicate this profound level of confidence, which is paramount for consumers selecting financial services. Building such trust often requires substantial investment in marketing and a flawless operational track record, a challenge for any newcomer. In 2024, customer loyalty remains a key competitive advantage, making it difficult for startups to divert significant market share from incumbents.

Economies of Scale and Scope

Large financial holding companies like Shin Kong Financial benefit significantly from economies of scale and scope, enabling them to offer diverse products at lower average costs. A new entrant faces substantial hurdles in competing on price and product breadth without achieving comparable operational scale. For instance, Shin Kong Financial Holding reported consolidated assets exceeding NT$4.9 trillion as of Q1 2024, demonstrating the vast capital and infrastructure required. This immense scale allows for efficient resource allocation across its banking, insurance, and securities arms, making it difficult for smaller, newer players to match. New entrants would struggle to replicate such an expansive network and integrated service offering competitively.

- Shin Kong Financial Holding reported consolidated assets over NT$4.9 trillion in Q1 2024.

- Established players leverage existing client bases and brand recognition.

- New entrants face high capital requirements for regulatory compliance and technology.

- Achieving competitive unit costs demands significant investment in infrastructure.

Established Distribution Networks

Shin Kong Financial Holdings, like other established players in Taiwan's financial sector, benefits from extensive and deeply rooted distribution networks. These include numerous physical branches and robust ATM networks across the island. Building a comparable physical and sophisticated digital footprint, such as those maintained by incumbents, presents a substantial financial and logistical hurdle for any new entrant. This high barrier to entry significantly reduces the threat posed by new competitors in 2024.

- Shin Kong Financial reported 107 bank branches and 27 insurance branches in its 2023 annual report, providing a broad physical presence.

- Developing new digital platforms to match the sophistication of existing ones, which process millions of transactions annually, requires significant capital investment and time.

Taiwan's Financial Fortress: High Barriers Protect Incumbents

The threat of new entrants for Shin Kong Financial is very low due to Taiwan's stringent regulatory hurdles and high capital requirements. Establishing operations demands significant investment, such as the TWD 2 billion minimum for an online life insurer. Entrants also struggle against established brand trust, economies of scale, and extensive distribution networks of incumbents like Shin Kong Financial, which reported over NT$4.9 trillion in consolidated assets in Q1 2024.

| Barrier Type | Impact on New Entrants | 2024 Data/Fact |

|---|---|---|

| Regulatory Hurdles | High; lengthy licensing process | FSC requires strict capital adequacy and compliance. |

| Capital Requirements | Substantial; deters many | Online life insurance: min. TWD 2 billion capital. |

| Economies of Scale | Difficult to match cost efficiency | Shin Kong Financial: >NT$4.9T consolidated assets (Q1 2024). |

| Brand & Trust | Years to build; hard to replicate | Incumbents leverage decades of customer loyalty. |

| Distribution Networks | Costly to build physical/digital presence | Shin Kong Financial: 107 bank, 27 insurance branches (2023). |

Porter's Five Forces Analysis Data Sources

Our Shin Kong Financial Porter's Five Forces analysis leverages data from financial statements, annual reports, and investor relations disclosures. We also incorporate insights from industry-specific research reports and market intelligence platforms to provide a comprehensive view of the competitive landscape.