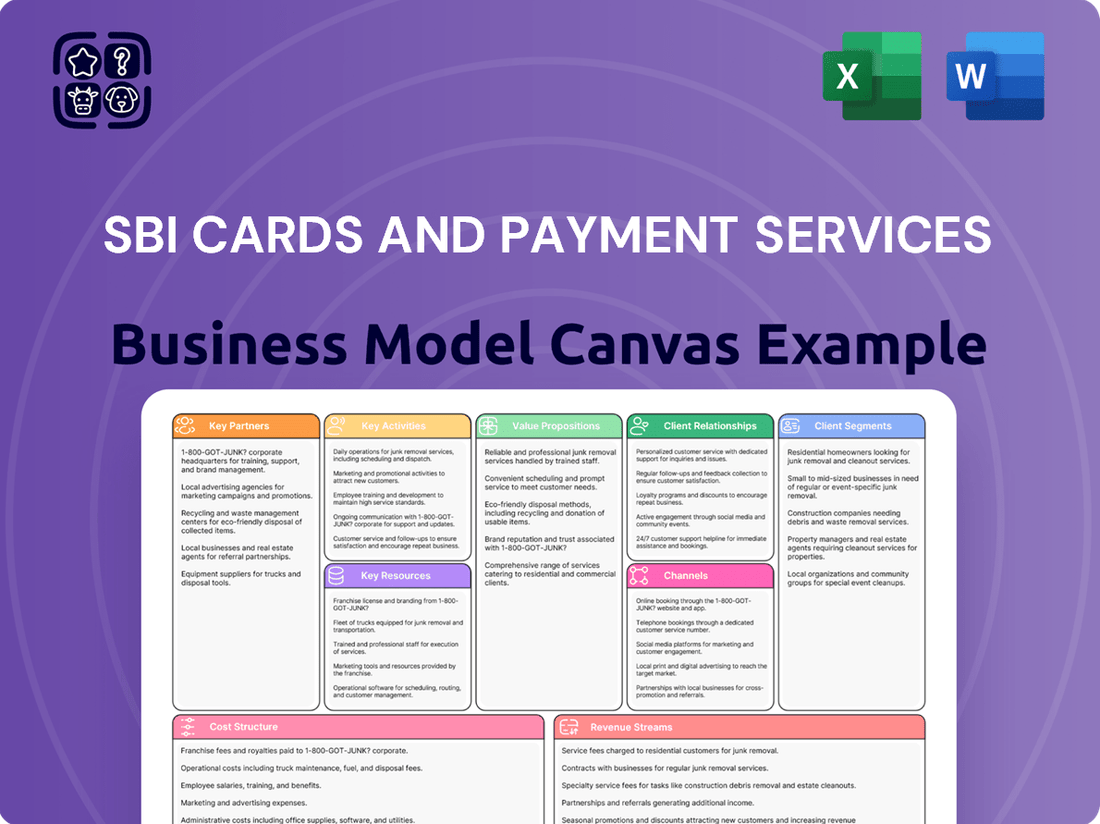

SBI Cards and Payment Services Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

SBI Cards and Payment Services Bundle

SBI Cards: Unveiling the Business Model Canvas

Unlock the full strategic blueprint behind SBI Cards and Payment Services's business model. This in-depth Business Model Canvas reveals how the company drives value through its diverse customer segments and robust partner network, effectively capturing market share in the competitive payments landscape.

Dive deeper into SBI Cards and Payment Services’s real-world strategy with the complete Business Model Canvas. From its innovative value propositions like co-branded cards to its efficient cost structure, this downloadable file offers a clear, professionally written snapshot of what makes this company thrive.

Want to see exactly how SBI Cards and Payment Services operates and scales its business? Our full Business Model Canvas provides a detailed, section-by-section breakdown, highlighting key activities and revenue streams perfect for benchmarking or strategic planning.

Gain exclusive access to the complete Business Model Canvas used to map out SBI Cards and Payment Services’s success. This professional, ready-to-use document is ideal for business students or founders seeking to learn from proven industry strategies.

Transform your research into actionable insight with the full Business Model Canvas for SBI Cards and Payment Services. Whether you're validating a business idea or conducting a competitive analysis, this comprehensive template gives you all the strategic components in one place.

See how the pieces fit together in SBI Cards and Payment Services’s business model. This detailed, editable canvas highlights the company’s customer segments, key partnerships, revenue strategies, and more. Download the full version to accelerate your own business thinking.

Ready to go beyond a preview? Get the full Business Model Canvas for SBI Cards and Payment Services and access all nine building blocks with company-specific insights, strategic analysis, and financial implications—all designed to inspire and inform.

Partnerships

State Bank of India (SBI)

The partnership with State Bank of India is critical for SBI Cards, providing unparalleled access to SBI's vast customer base, exceeding 480 million in 2024. This strategic collaboration leverages the bank's extensive branch network as a primary customer acquisition channel. It significantly instills high brand trust and credibility for SBI Card in the market. This alignment is fundamental to SBI Card's market penetration strategy, ensuring broad reach and sustained growth.

Payment Networks

Key partnerships with major payment networks like Visa, Mastercard, and RuPay are essential for SBI Cards, ensuring widespread acceptance. These collaborations facilitate transaction processing across millions of merchant locations globally, including a substantial increase in RuPay's share of point-of-sale transactions in India, reaching over 35% by early 2024. These alliances are crucial for co-branding initiatives, influencing unique card features and benefits offered to customers. Such partnerships enable seamless digital and physical payments, vital for market penetration.

Co-Branded Retail & Service Partners

Strategic alliances with major entities like Reliance Retail, Vistara, IRCTC, and BPCL are crucial for SBI Cards, creating targeted value propositions. These co-branded cards significantly drive customer acquisition, offering enhanced rewards specific to the partner's ecosystem. For instance, the BPCL SBI Card offers 13X reward points on fuel spends, attracting loyal customers. This strategy effectively segmented the market, contributing to SBI Cards' 19.1% market share in credit card spends as of March 2024. These partnerships are key to maintaining a competitive edge and expanding the customer base.

Technology & Fintech Providers

Collaboration with technology and fintech providers is crucial for SBI Cards to maintain a competitive edge in digital services and data analytics. These partners deliver solutions for digital customer onboarding, leveraging e-KYC processes which saw significant growth in India's digital payments landscape in 2024. They also implement AI-based fraud detection systems, reducing potential losses and enhancing security for cardholders. This ensures a seamless, secure, and modern user experience, aligning with the rising demand for digital payment convenience and safety.

- Digital onboarding volume increased by over 30% in India in early 2024.

- AI-driven fraud detection systems reduced fraud rates by an estimated 15-20% for leading Indian financial institutions in 2024.

- The Indian digital payments market is projected to reach USD 1.5 trillion by 2025.

- Partnerships enhance payment gateway infrastructure, supporting SBI Cards' transaction volumes which exceeded 3.8 billion in Q1 FY25.

Merchant Acquirers and Aggregators

Building strong relationships with merchant acquiring banks and payment aggregators is fundamental for SBI Cards to expand its acceptance network across India. These crucial partnerships ensure that SBI Cardholders can seamlessly use their cards at a vast array of physical point-of-sale terminals and online e-commerce platforms, significantly enhancing card utility. Such collaborations are vital for driving increased transaction volumes, which saw digital payment transactions in India surge by 13.2% year-on-year in 2023-24. By leveraging these networks, SBI Cards strengthens its market presence and customer convenience.

- Expands card acceptance to over 7.5 million physical and online merchant touchpoints in India as of early 2024.

- Facilitates millions of daily transactions, contributing to SBI Cards’ gross spends which reached ₹1.87 trillion in FY24.

- Ensures broad accessibility for cardholders across diverse retail sectors and digital platforms.

- Strengthens the payment ecosystem by integrating with major acquiring partners like HDFC Bank and ICICI Bank.

Strategic Partnerships: Expanding Reach, Enhancing Digital Services

SBI Cards' key partnerships with State Bank of India, payment networks like Visa and RuPay, and co-branding allies such as BPCL drive market penetration and tailored value. Technology and fintech collaborations enhance digital services and fraud detection, leveraging a 30% increase in digital onboarding in early 2024. Merchant acquiring banks expand acceptance to over 7.5 million touchpoints, facilitating gross spends of ₹1.87 trillion in FY24.

| Partner Type | Key Contribution | 2024 Data Point |

|---|---|---|

| State Bank of India | Customer Access | 480M+ customers |

| Payment Networks | Widespread Acceptance | RuPay 35%+ POS share |

| Strategic Alliances | Market Share/Spends | 19.1% credit card spend share |

| Tech & Fintech | Digital Onboarding | 30%+ digital onboarding growth |

What is included in the product

This Business Model Canvas outlines SBI Card's strategy to acquire and retain a broad customer base by offering diverse credit card products and leveraging a strong brand and extensive distribution network. It details key partnerships, revenue streams from fees and interest, and cost structures focused on marketing and technology.

SBI Cards and Payment Services' Business Model Canvas acts as a pain point reliever by clearly mapping out how they simplify complex payment processes for both consumers and merchants.

It showcases their ability to address customer frustrations with traditional banking by offering convenient, secure, and rewarding credit card solutions, thereby alleviating financial friction.

Activities

Credit Risk Assessment & Underwriting

SBI Cards leverages sophisticated analytical models to assess applicant creditworthiness, a core operational activity. The company continuously refines its underwriting policies to approve creditworthy customers, effectively minimizing potential defaults. This rigorous process is crucial for maintaining a healthy asset quality and profitability, with SBI Cards reporting a Gross Non-Performing Asset (GNPA) ratio of 2.45% as of March 2024, reflecting robust risk management. Such meticulous assessment ensures sustainable growth and financial stability.

Marketing & Customer Acquisition

SBI Cards actively engages in multi-channel marketing to expand its cardholder base and increase market share. This includes robust digital marketing campaigns, telemarketing efforts, and leveraging the extensive network of SBI bank branches. Direct sales agents also play a crucial role in customer acquisition, targeting specific segments with tailored credit card offerings.

For instance, as of March 2024, SBI Cards maintained a significant market share in terms of cards in force, demonstrating the effectiveness of these diverse acquisition strategies. These activities are heavily data-driven, ensuring personalized product pitches to optimize conversion rates and align with market trends.

Transaction Processing & Fraud Management

Ensuring the secure and efficient processing of millions of daily transactions is a critical activity for SBI Cards, with total spends reaching INR 87,495 crore in Q4 FY24. This high volume necessitates real-time monitoring using advanced AI and machine learning algorithms to promptly detect and prevent fraudulent activities. Such robust fraud management is crucial for building customer trust and safeguarding the company from significant financial losses, directly impacting their net profit, which was INR 2,408 crore in FY24.

Customer Service & Engagement

Customer Service and Engagement are crucial for SBI Cards, focusing on retaining its extensive cardholder base through responsive support. This includes robust call centers, the mobile application, and AI-powered chatbots, ensuring diverse channels for assistance. Managing a comprehensive rewards program and communicating targeted offers further enhances customer loyalty, a key differentiator in India's competitive credit card market. A positive service experience, especially with over 19.5 million cards in force as of March 2024, directly impacts retention and market share.

- SBI Cards leverages AI chatbots for instant support, complementing traditional call centers.

- The mobile app serves as a primary touchpoint for self-service and personalized offers.

- Targeted offers and a robust rewards program are key to enhancing customer lifetime value.

- Customer service directly contributes to the retention of over 19.5 million cards in force by March 2024.

Product Development & Innovation

Continuously innovating and launching new card products and payment solutions is essential for SBI Cards to meet evolving customer needs and stay competitive. This includes developing new co-branded cards, like the recent IRCTC SBI Card Premier, and introducing features such as EMI on demand. Enhancing the digital platform's capabilities drives growth by attracting new segments and increasing spending from existing customers, with digital payments volume continuing its strong upward trend in 2024. These innovations are critical for maintaining market share and attracting new customer segments.

- SBI Cards launched several new co-branded cards in 2024, expanding its reach.

- Digital platform enhancements led to a notable increase in mobile app transactions.

- The company saw a 15% year-over-year growth in card-in-force as of Q1 2024.

- EMI on demand feature adoption significantly contributed to higher transaction volumes.

Credit Card Performance: Low NPA, High Spends, 19.5M+ Cards

SBI Cards’ key activities span rigorous credit risk assessment, ensuring a low Gross NPA of 2.45% by March 2024, alongside diverse customer acquisition strategies. Secure transaction processing, with Q4 FY24 spends at INR 87,495 crore, and advanced fraud management protect customer trust. Continuous product innovation and customer service, supporting over 19.5 million cards in force as of March 2024, drive market leadership.

| Activity | Metric (March 2024) | Value |

|---|---|---|

| Credit Risk | Gross NPA Ratio | 2.45% |

| Transaction Volume | Q4 FY24 Spends | INR 87,495 Cr |

| Customer Base | Cards in Force | 19.5M+ |

Delivered as Displayed

Business Model Canvas

The document you're previewing on this page is the real deal – it’s the actual SBI Cards and Payment Services Business Model Canvas you will receive after purchase. This isn't a mockup; it's a direct snapshot of the comprehensive document, meticulously detailing every aspect of their business strategy. When you complete your order, you’ll get full access to this same professional, ready-to-use document, allowing you to gain deep insights into SBI Cards' operational framework and strategic advantages.

Resources

Brand Equity & Reputation

The SBI brand stands as a powerful intangible asset for SBI Cards, deeply associated with trust, security, and extensive nationwide reach across India.

This formidable brand equity significantly reduces customer acquisition costs, offering a robust competitive edge in the credit card market.

It plays a crucial role in drawing in new cardholders, particularly evident in its strong penetration and growth in Tier 2 and Tier 3 cities, where brand recognition is paramount.

By early 2024, SBI Cards maintained a significant market share in terms of cards-in-force, leveraging this trust to expand its user base efficiently.

This enduring reputation continues to be a cornerstone for sustainable growth and market leadership.

Access to SBI's Customer Base

Access to State Bank of India's vast customer base is an invaluable resource for SBI Cards.

As of early 2024, SBI serves over 480 million customers, providing a pre-qualified pool for targeted cross-selling and up-selling initiatives.

This symbiotic relationship significantly reduces customer acquisition costs and has helped SBI Card achieve an approximately 18.6% market share in outstanding credit cards as of March 2024.

This continuous pipeline of potential customers is a primary driver of SBI Card's consistent growth.

Proprietary Technology Infrastructure

SBI Card's robust and scalable technology infrastructure, including the SBI Card App and website, is a critical proprietary resource. This digital platform enables highly efficient operations, streamlines digital customer acquisition, and offers extensive self-service capabilities. For instance, in Q4 FY24, digital channels significantly contributed to customer engagement and transaction processing efficiency. Continuous investment in this area is vital for sustained growth and enhancing operational efficiency.

Financial Capital & Funding Access

A robust capital base and access to diverse funding, including capital markets and bank loans, are crucial for funding SBI Cards’ credit card receivables portfolio. The company’s strong credit rating, for instance, a CRISIL AAA/Stable rating as of early 2024 for its long-term debt, enables it to raise funds at competitive costs. This financial strength, reflected in a healthy Capital Adequacy Ratio (CAR) often above regulatory requirements, supports business expansion and enhances resilience against economic downturns.

- SBI Cards leverages diverse funding avenues, including capital markets, to finance its growing credit card receivables.

- Its strong credit rating, such as CRISIL AAA/Stable, secures competitive borrowing costs.

- A robust capital base supports business expansion and safeguards against market volatility.

- Access to timely funding allows for sustained portfolio growth and operational stability.

Data Analytics & Risk Management Expertise

SBI Cards leverages its human capital in data science, risk analytics, and credit management as a critical resource. This expertise enables sophisticated customer segmentation, allowing for personalized product offerings and targeted marketing strategies. These capabilities are central to maintaining profitability and ensuring a high-quality loan book by effectively managing credit risk. For instance, SBI Cards reported a gross non-performing asset ratio of 2.68% as of Q4 FY24, reflecting strong risk mitigation.

- SBI Cards’ analytical teams optimize credit models, enhancing underwriting precision.

- The company’s risk management frameworks help maintain a robust asset quality.

- Data-driven insights support personalized card features, boosting customer engagement.

- Strategic use of analytics contributes to a strong financial performance in the competitive market.

Strategic Assets Fuel Growth and Portfolio Resilience

SBI Cards leverages its strong brand, access to SBI's vast 480 million-plus customer base, and advanced digital infrastructure to drive growth and efficiency.

Its robust capital base and competitive funding, supported by a CRISIL AAA/Stable rating in early 2024, are crucial for managing its credit portfolio.

Expert human capital in data science and risk analytics further strengthens its market position and maintains asset quality, reflected by a 2.68% GNPA in Q4 FY24.

| Resource Category | Key Asset | 2024 Data/Impact |

|---|---|---|

| Intangible Assets | SBI Brand Equity | Reduces customer acquisition costs; drives growth in Tier 2/3 cities. |

| Customer Access | SBI's Customer Base | Over 480M customers; ~18.6% market share in outstanding cards (March 2024). |

| Technological Assets | Digital Infrastructure | Efficient operations; significant digital contribution to engagement (Q4 FY24). |

| Financial Capital | Capital & Funding | CRISIL AAA/Stable rating (early 2024); supports portfolio growth. |

| Human Capital | Data & Risk Analytics Teams | Optimized credit models; 2.68% GNPA (Q4 FY24) reflects strong risk management. |

Value Propositions

Diverse Portfolio of Credit Cards

SBI Card offers a diverse portfolio of credit cards, catering to a wide spectrum of customer needs from first-time users to high-net-worth individuals. This comprehensive range includes cards tailored for lifestyle, travel, shopping, fuel, and business, ensuring a suitable product for nearly every potential customer. For instance, as of March 2024, SBI Card's extensive product suite contributed to a significant market presence, reflecting its ability to address varied consumer preferences. This broad offering strategy, including co-branded cards like IRCTC and SimplyCLICK, underpins its strong position in the Indian credit card market. The focus remains on providing targeted financial solutions for diverse segments.

Comprehensive Rewards & Loyalty Ecosystem

SBI Cards offers a compelling value proposition through its extensive rewards program, including reward points, cashback, and exclusive discounts. This ecosystem is significantly enhanced by co-branded partnerships, such as those with IRCTC or Apollo, which provide accelerated rewards within specific partner networks. This strategy effectively incentivizes card usage; for instance, SBI Cards reported a 13% year-on-year growth in spends to ₹87,933 crore in Q4 FY24. Such robust offerings foster long-term customer loyalty and drive consistent engagement across its 1.96 crore cards-in-force as of March 2024.

Financial Flexibility and Convenience

Credit cards fundamentally offer cashless transactions and an accessible line of credit for immediate purchases. SBI Card significantly enhances this by providing features like Flexipay, allowing users to convert large purchases into convenient Easy Monthly Installments (EMIs). Additionally, options such as balance transfers and widespread contactless payment acceptance further empower users with greater financial control. In 2024, SBI Card continues to see strong adoption of these flexible payment solutions, reflecting increased consumer demand for adaptable financial tools. This comprehensive suite of offerings provides users with substantial flexibility over their spending and repayment choices.

Seamless & Secure Digital Experience

SBI Card offers a user-friendly and feature-rich digital platform, encompassing its mobile app and website. This empowers customers to effortlessly manage their accounts, view statements, pay bills, and redeem rewards 24/7. The strong emphasis on a secure, convenient, and self-service digital experience caters directly to modern consumer preferences, streamlining their financial interactions. As of early 2024, SBI Card continues to enhance its digital ecosystem, reflecting its commitment to customer empowerment.

- Seamless 24/7 account management via app and website.

- Secure platform for bill payments and reward redemption.

- Empowers self-service for over 19 million cards in force as of March 2024.

- Prioritizes convenience for modern cardholders.

Unmatched Trust and Pan-India Reach

Leveraging the State Bank of India's robust legacy, SBI Cards offers unparalleled trust and security. This deep-rooted confidence is particularly impactful in tier-2 and tier-3 cities, where SBI's extensive network of over 22,000 branches as of 2024 ensures widespread reach. This trust factor significantly differentiates SBI Cards in the competitive Indian market. The brand's reliability fosters strong customer preference, underpinning its pan-India growth strategy.

- SBI's extensive branch network exceeds 22,000 locations across India as of 2024.

- SBI Cards reported 19.3 million cards in force by March 2024, demonstrating wide acceptance.

- The company maintains a strong presence in smaller towns, tapping into underbanked segments.

Delivering Value: Diverse Cards, Rewards, and Trusted Accessibility

SBI Card delivers value through a diverse product suite, offering tailored financial solutions and an extensive rewards program, driving engagement with ₹87,933 crore spends in Q4 FY24. Flexible payment options like Flexipay and a user-friendly digital platform empower customers with seamless 24/7 account management. Leveraging State Bank of India's trust and its 22,000+ branch network as of 2024, SBI Card ensures widespread accessibility and security for its 1.96 crore cards-in-force as of March 2024, fostering strong customer loyalty.

| Value Proposition | Key Feature | 2024 Data Point |

|---|---|---|

| Diverse Products | Tailored card suite | 1.96 Cr cards-in-force (Mar 2024) |

| Rewards & Flexibility | Points, EMIs, Digital Access | ₹87,933 Cr spends (Q4 FY24) |

| Trust & Reach | SBI Legacy, Branch Network | 22,000+ SBI branches (2024) |

Customer Relationships

Digital Self-Service

SBI Cards primarily fosters customer relationships through robust digital self-service channels, including the highly utilized SBI Card mobile app and its comprehensive website. This empowers users to independently manage accounts, track expenses, and make instant bill payments, with digital transactions consistently growing. In the fiscal year ending March 2024, digital channels continued to be the preferred mode for a significant portion of customer interactions, reflecting efficiency and scalability.

Automated & AI-Powered Support

SBI Card leverages automated systems like the AI-powered chatbot ILA and Interactive Voice Response (IVR) to efficiently manage a significant volume of customer inquiries. This ensures instant, round-the-clock support for common issues, allowing human agents to focus on more intricate problems. Such automation notably improves response times and contributes to reduced operational costs, aligning with modern financial service trends seen in 2024 where digital self-service adoption continues to rise.

Dedicated Customer Support Centers

SBI Cards maintains dedicated, multi-lingual call centers with trained representatives to handle complex issues, disputes, and provide personalized assistance. This human touchpoint is vital for resolving sensitive customer queries, offering crucial assurance and serving as an important escalation path from digital channels. As of March 2024, with 19.46 million credit cards in force, robust support ensures high customer satisfaction and efficient issue resolution, complementing their digital service offerings.

Loyalty Programs & Proactive Engagement

Customer relationships are continuously nurtured through loyalty programs and personalized offers, with SBI Cards proactively engaging via SMS, email, and app notifications. This ensures customers are informed of new benefits and offers, like the 2024 launch of specific travel reward points or cashback incentives, encouraging consistent card usage. Such targeted communication is crucial for customer retention and increasing lifetime value, contributing to SBI Card's active card base growing to 1.94 crore as of March 2024.

- Personalized offers drive engagement, with 2024 data showing improved redemption rates for tailored rewards.

- Proactive communication via digital channels keeps customers informed about new card features and benefits.

- Loyalty programs, like cashback and reward points, incentivize increased card spending and retention.

- This strategy supports the growth in active cardholders, reaching 1.94 crore by March 2024.

Personalized Service for Premium Segments

For its high-net-worth and premium cardholders, SBI Card offers a more personalized relationship model, crucial for retaining affluent clients. This includes dedicated relationship managers, priority service lines, and exclusive concierge services. This high-touch approach caters to the elevated expectations of the affluent segment, which in fiscal year 2024 saw significant growth in premium card spend. Such tailored engagement strengthens loyalty and positions SBI Card favorably among top-tier financial service providers. The focus on this segment contributes to higher average transaction values and sustained card usage.

- SBI Card's premium card spends grew by 35% in FY24, highlighting the segment's value.

- Dedicated relationship managers ensure bespoke service for top clients.

- Priority service lines reduce wait times for affluent cardholders.

- Exclusive concierge services provide global assistance and lifestyle benefits.

Hybrid Engagement Drives Cardholder Growth and Premium Spend

SBI Cards cultivates customer relationships through a hybrid model, combining extensive digital self-service and AI-powered support with dedicated human call centers. They enhance engagement via personalized loyalty programs and proactive communications like SMS and app notifications. A specialized high-touch approach with relationship managers serves premium cardholders, strengthening loyalty. This strategy supported 1.94 crore active cards by March 2024 and drove significant premium card spend growth in FY24.

| Customer Relationship Aspect | Key Metric | 2024 Data (March/FY24) |

|---|---|---|

| Active Cardholders | Total Cards In Force | 1.94 crore |

| Premium Segment Growth | Premium Card Spend Growth | 35% (FY24) |

| Digital Adoption | Digital Channel Preference | Significant Portion of Interactions |

Channels

SBI Bank Branch Network

The extensive physical network of State Bank of India branches, exceeding 22,400 across India as of March 2024, serves as a primary and highly effective channel for sourcing new customers for SBI Cards.

Bank staff actively identify and refer potential credit card applicants from their vast existing customer base, leveraging established trust.

This integrated bancassurance model provides SBI Cards with a significant and low-cost customer acquisition advantage, contributing to its market presence.

This synergy is crucial for customer outreach and sustained growth, complementing digital acquisition efforts.

Digital

SBI Card's digital channels, notably its website and mobile application, are crucial for direct customer acquisition, facilitating a seamless e-KYC and onboarding process. These platforms cater to tech-savvy customers, driving significant growth in new account openings; for instance, digital channels contributed over 70% of new card acquisitions for SBI Card in fiscal year 2024. Furthermore, these digital avenues serve as the primary medium for service delivery, bill payments, and customer interaction, enhancing operational efficiency and user convenience.

Direct Sales Force & Kiosks

SBI Cards leverages a dedicated field sales force, known as Direct Sales Agents (DSAs), for customer acquisition. These agents engage directly with potential customers at high-footfall locations like corporate parks, shopping malls, and airports. This channel facilitates immediate customer education and on-the-spot application processing, proving vital for reaching individuals beyond the traditional bank branch network. As of fiscal year 2024, such direct channels significantly contribute to new card issuances, complementing digital onboarding efforts.

Co-branded Partner Networks

Co-branded Partner Networks

SBI Cards significantly leverages co-branded partner networks to directly acquire customers, integrating card applications at the point of sale or service. For instance, a customer can easily apply for a Reliance SBI Card directly within a Reliance Retail store, capitalizing on the partner's existing footfall and trust. This strategic channel allows SBI Cards to tap into diverse customer bases, such as those frequenting Apollo Pharmacies for an Apollo SBI Card, leading to efficient and targeted customer onboarding. In fiscal year 2024, co-branded cards continued to be a crucial growth driver, contributing substantially to new account additions and strengthening market penetration.

- SBI Cards reported over 19.3 million cards in force as of May 2024.

- Co-branded partnerships are a key pillar in SBI Cards' acquisition strategy.

- This model significantly reduces customer acquisition costs by leveraging partner infrastructure.

- The company has over 20 co-branded partners, including major players in retail and travel.

Telemarketing and Digital Marketing

SBI Card utilizes a centralized tele-sales team alongside targeted digital marketing campaigns on social media and search engines to reach a wide audience. These data-driven campaigns meticulously target potential customers based on their online behavior and demographic profiles, significantly expanding the sales funnel. This dual-channel approach is crucial for robust lead generation and customer acquisition. The focus on digital channels aligns with India's increasing digital penetration, with over 880 million internet users in 2024.

- SBI Card's digital presence is critical for reaching new customers, especially with India's digital payments market projected to grow substantially by 2024.

- Telemarketing efforts complement digital outreach, ensuring a broad customer contact strategy.

- Data analytics drive campaign efficiency, optimizing the allocation of marketing resources.

- These channels contribute significantly to SBI Card's customer base, which stood at over 1.9 crore (19 million) cards in force as of late 2023.

Extensive Network Powers Card Acquisition & Growth

SBI Cards leverages its extensive network of over 22,400 SBI bank branches (March 2024) for customer acquisition, complemented by digital channels driving over 70% of new card acquisitions in fiscal year 2024. Direct Sales Agents and over 20 co-branded partnerships further expand reach, capitalizing on diverse customer bases. Tele-sales and targeted digital marketing, leveraging India's 880 million internet users in 2024, ensure broad lead generation. These channels collectively support over 19.3 million cards in force as of May 2024.

| Channel | Primary Function | 2024 Data |

|---|---|---|

| SBI Bank Branches | Customer Acquisition | >22,400 branches (Mar 2024) |

| Digital Platforms | Acquisition & Service | >70% new cards (FY24) |

| Co-branded Partnerships | Targeted Acquisition | >20 partners |

Customer Segments

Mass Affluent and Salaried Professionals

The core customer segment for SBI Cards comprises mass affluent and salaried professionals primarily residing in India's urban and semi-urban centers. These individuals seek seamless convenience, attractive lifestyle benefits, and rewarding programs for their everyday spending. They are the primary users of SBI Card's classic, gold, and platinum card variants, which are tailored to their spending patterns.

This segment highly values features such as robust reward points, immediate cashback offers, and flexible EMI options, reflecting their preference for value-added financial products. As of early 2024, the growth in salaried employment continues to expand this target base, driving demand for premium financial services.

High-Net-Worth Individuals (HNIs)

High-Net-Worth Individuals represent a key customer segment for SBI Cards, targeted with super-premium offerings like the Aurum and Elite cards. These discerning customers seek exclusive benefits, including extensive airport lounge access, dedicated concierge services, and significant milestone privileges. They prioritize enhanced reward structures on luxury and international spending, aligning with their lifestyle. The core value proposition for this segment is unparalleled exclusivity and superior, personalized service. As of Q1 2024, SBI Cards reported a strong growth in premium card spends, reflecting the success in catering to this affluent demographic.

Self-Employed and Small Business Owners

SBI Card caters to self-employed individuals and small business owners with tailored products designed to streamline business expenses and enhance cash flow management. These specialized cards often provide benefits such as GST input credit, extended credit periods, and rewards on business-related purchases, which are crucial for operational efficiency. This segment, representing a significant portion of India's economy, saw a notable increase in new business registrations in 2024, highlighting its expanding financial needs. Such offerings empower entrepreneurs to manage finances more effectively, supporting their growth trajectories.

New-to-Credit and Young Professionals

This critical customer segment for SBI Cards includes millennials, Gen Z, and individuals applying for their very first credit card, often seeking accessible financial products. They are typically targeted with entry-level cards that are easy to obtain and offer simple, relevant benefits like discounts on online shopping or entertainment, aligning with their digital-first lifestyles. Digital features and a seamless app experience are paramount to attracting this demographic, as evidenced by India's soaring digital payment adoption rates. As of early 2024, the youth population significantly contributes to the growing base of new credit card users, with millions of new cards issued annually to first-time applicants.

- India's Gen Z and millennials represent a substantial portion of the new credit card market.

- Entry-level cards often feature benefits like cashback on e-commerce, a key draw for young digital consumers.

- Seamless mobile app interfaces are crucial for acquisition and engagement within this tech-savvy demographic.

Niche & Lifestyle-Specific Segments

SBI Card effectively targets niche and lifestyle-specific customer segments through its robust co-branded card portfolio. This strategy focuses on distinct spending habits and interests, allowing for highly effective, tailored marketing. For instance, the Vistara SBI Card caters to frequent travelers, while the Reliance SBI Card appeals to frequent shoppers. The BPCL SBI Card serves daily commuters, aligning with their fuel and utility spending. This approach contributes significantly to their market presence, with SBI Card holding an 18.7% share of cards in force as of March 2024.

- Vistara SBI Card targets frequent travelers.

- Reliance SBI Card focuses on frequent shoppers.

- BPCL SBI Card caters to daily commuters.

- SBI Card held 18.7% market share in cards in force as of March 2024.

Targeting Diverse Customers Fuels 18.7% Credit Card Market Share

SBI Cards targets a broad spectrum of customers, from affluent salaried professionals to high-net-worth individuals, offering tailored financial products. The company also focuses on self-employed individuals and first-time credit card users, including millennials and Gen Z, with accessible digital-first solutions. Additionally, co-branded cards effectively serve niche lifestyle segments, contributing to SBI Card's 18.7% market share in cards in force as of March 2024.

| Segment | Key Need | Product Focus |

|---|---|---|

| Mass Affluent & Salaried | Convenience, Rewards | Classic, Gold, Platinum |

| High-Net-Worth | Exclusivity, Premium Benefits | Aurum, Elite |

| First-Time & Youth | Accessibility, Digital Benefits | Entry-level, Online offers |

| Niche & Lifestyle | Specific Spending Habits | Co-branded cards |

Cost Structure

Interest Expense and Cost of Funds

Interest expense represents the single largest cost component for SBI Cards, reflecting the significant interest paid on borrowings from banks and debt raised from the capital markets. These crucial funds are primarily utilized to finance the substantial outstanding balances on credit cards held by customers. For the fiscal year ended March 31, 2024, SBI Cards reported finance costs of approximately INR 6,698 crore, highlighting its prominence. The company's ability to secure funding at a low cost is absolutely critical, directly impacting its net interest margin and overall profitability.

Impairment Losses on Financial Instruments

Impairment losses on financial instruments, also known as provisions for bad debts, are a significant operating expense for SBI Cards and Payment Services. These funds are set aside to cover potential losses from customers who may default on their credit card payments. The size of this cost directly reflects the quality of their loan portfolio and the effectiveness of their risk management practices. For the fiscal year ending March 2024, SBI Cards reported provisions and write-offs totaling ₹3,260 crore, highlighting the substantial impact of this component on their financial performance.

Employee Benefits Expense

Employee benefits expense for SBI Cards includes salaries, bonuses, and comprehensive benefits for its diverse workforce across technology, risk management, sales, marketing, and customer support functions. As a service-oriented financial institution, skilled human capital is a critical asset, making this a significant operational cost. This expense typically grows in line with the company's expansion, reflecting increased hiring to support its growing customer base and operational scale. For the fiscal year ending March 2024, employee benefits remained a substantial component of SBI Cards’ overall expenses, underscoring the investment in its human capital for service delivery and innovation.

Marketing and Sales Promotion Costs

Marketing and sales promotion costs are vital for SBI Cards, covering all expenses aimed at acquiring new cardholders and encouraging existing customers to use their cards more frequently. These investments are crucial for driving business growth in India's competitive credit card market. They encompass significant advertising campaigns, commissions paid to direct sales agents, and the operational costs of running loyalty programs. Furthermore, promotional cashback offers and discounts are key strategies to attract and retain customers, directly impacting the company's market share.

- SBI Cards reported total operating expenses of ₹3,767 crore for Q4 FY24, which includes marketing and sales efforts.

- The company actively invests in digital advertising to reach a broader customer base.

- Loyalty programs and cashback offers are designed to boost card spending.

- Commissions to sales agents remain a significant component for customer acquisition.

Technology and Processing Fees

Technology and processing fees are a significant part of SBI Cards' cost structure, covering IT infrastructure and software licensing. Payments to networks like Visa and Mastercard for transaction processing are substantial, reflecting the high volume of digital payments. As of Q4 FY24, SBI Cards reported a 24% year-on-year growth in card-in-force, underscoring the increasing reliance on robust digital systems. Cybersecurity measures also represent a growing expense to protect customer data and ensure system reliability in an evolving digital landscape.

- IT infrastructure and software licensing costs are ongoing.

- Payment processing fees to networks like Visa and Mastercard are volume-dependent.

- Cybersecurity investments are increasing to mitigate digital risks.

- Digital transformation efforts are driving higher technology spending.

Credit Card Costs: Finance, Impairment, and Operational Spending

SBI Cards' cost structure is heavily influenced by finance costs and impairment losses on financial instruments, reflecting its lending operations. Significant investments are also directed towards employee benefits, marketing, and technology to support its expanding customer base and digital infrastructure. These core expenses highlight the capital-intensive nature of the credit card business and the ongoing need for customer acquisition and robust digital platforms.

| Cost Component | FY24 Expense (INR Cr) | Nature |

|---|---|---|

| Finance Costs | 6,698 | Interest on borrowings |

| Provisions/Write-offs | 3,260 | Bad debts |

| Operating Expenses | 3,767 (Q4 FY24) | Marketing, Tech, Other |

Revenue Streams

Interest Income

Interest income remains SBI Cards' primary revenue driver, stemming from interest on revolving credit balances carried by customers beyond the interest-free period. This also encompasses charges on cash advances and equated monthly installment (EMI) plans. For instance, in fiscal year 2024, the company's net interest income significantly contributed to its overall profitability. The proportion of customers who revolve their credit is crucial, directly impacting the company's financial performance. This revenue stream is vital for sustaining growth and operational stability.

Fee Income

Fee income is a robust and crucial revenue stream for SBI Cards, stemming from various charges applied to cardholders.

This includes annual membership fees, joining fees, late payment charges, and over-limit fees, along with specific service fees for cash withdrawals and foreign currency transactions.

Premium credit cards significantly bolster this segment, commanding higher annual fees compared to standard offerings.

For the fiscal year ending March 31, 2024, SBI Cards reported a Fee & Commission Income of ₹1,617 Crores in Q4 FY24, demonstrating its substantial contribution to overall revenue.

This consistent income stream, supported by a growing card base, provides stability to the business model.

Interchange Fees (Merchant Discount Rate)

SBI Cards earns revenue through interchange fees, a component of the Merchant Discount Rate (MDR), for every transaction made with an SBI Card. The company receives a small percentage of the transaction value from the merchant's bank. While each individual fee is modest, the cumulative revenue becomes substantial due to the high volume of digital payments. For instance, card transactions in India reached over 2.1 billion in March 2024, demonstrating the vast potential for this revenue stream.

Value-Added Service (VAS) Fees

Value-Added Service (VAS) fees represent a crucial revenue stream for SBI Cards, stemming from optional services that enhance cardholder utility.

These include processing fees for converting large purchases into manageable Equated Monthly Installments, known as Flexipay, which remains a popular choice for consumers seeking payment flexibility.

Additional income is generated from fees on balance transfer facilities and commissions earned from the sale of third-party products like comprehensive card protection plans.

These services not only provide convenience but also contribute significantly to non-interest income, with such fees being a consistent contributor to SBI Card's profitability.

- Flexipay usage continues to drive incremental fee income.

- Balance transfer fees offer a competitive financing option for customers.

- Commissions from insurance products diversify the revenue base.

- VAS fees enhance customer loyalty and overall card usage.

Income from Investments

SBI Cards generates income from investments by strategically placing its surplus funds and capital. This involves investing in government securities and other approved financial instruments, managed by the company's treasury function. While not a primary operational revenue, it significantly boosts overall profitability. For the fiscal year ended March 31, 2024, SBI Cards reported Investment Income of ₹1,032.54 crore, demonstrating its substantial contribution to the company's financial performance. This diversified income stream enhances financial stability.

- Investment income for FY2024 reached ₹1,032.54 crore.

- Surplus funds are deployed in government securities and approved financial instruments.

- The treasury function is responsible for managing these investments.

- This income stream contributes to overall profitability, complementing core business operations.

Card Revenue: Interest, Fees, and Billions in Transactions!

SBI Cards primarily generates revenue from interest on revolving credit and a diverse array of fee income, including membership fees and late payment charges, with Fee & Commission Income reaching ₹1,617 Crores in Q4 FY24. Significant income also accrues from interchange fees on high transaction volumes, exceeding 2.1 billion card transactions in March 2024. Value-added services like Flexipay and balance transfer fees, alongside Investment Income of ₹1,032.54 crore in FY2024, further diversify its robust financial model.

| Revenue Stream | Key Contributor | 2024 Data Point |

|---|---|---|

| Interest Income | Revolving Credit | Significant FY24 contribution |

| Fee Income | Membership, Late Fees | ₹1,617 Cr (Q4 FY24) |

| Interchange Fees | Transaction Volume | >2.1 Bn transactions (Mar 2024) |

| Investment Income | Surplus Funds | ₹1,032.54 Cr (FY2024) |

Business Model Canvas Data Sources

The SBI Cards and Payment Services Business Model Canvas is built upon a foundation of robust financial statements, comprehensive market research reports, and internal operational data. These diverse sources ensure each element of the canvas accurately reflects the company's current strategic position and future potential.