RWE Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

RWE Group

From Overview to Strategy Blueprint

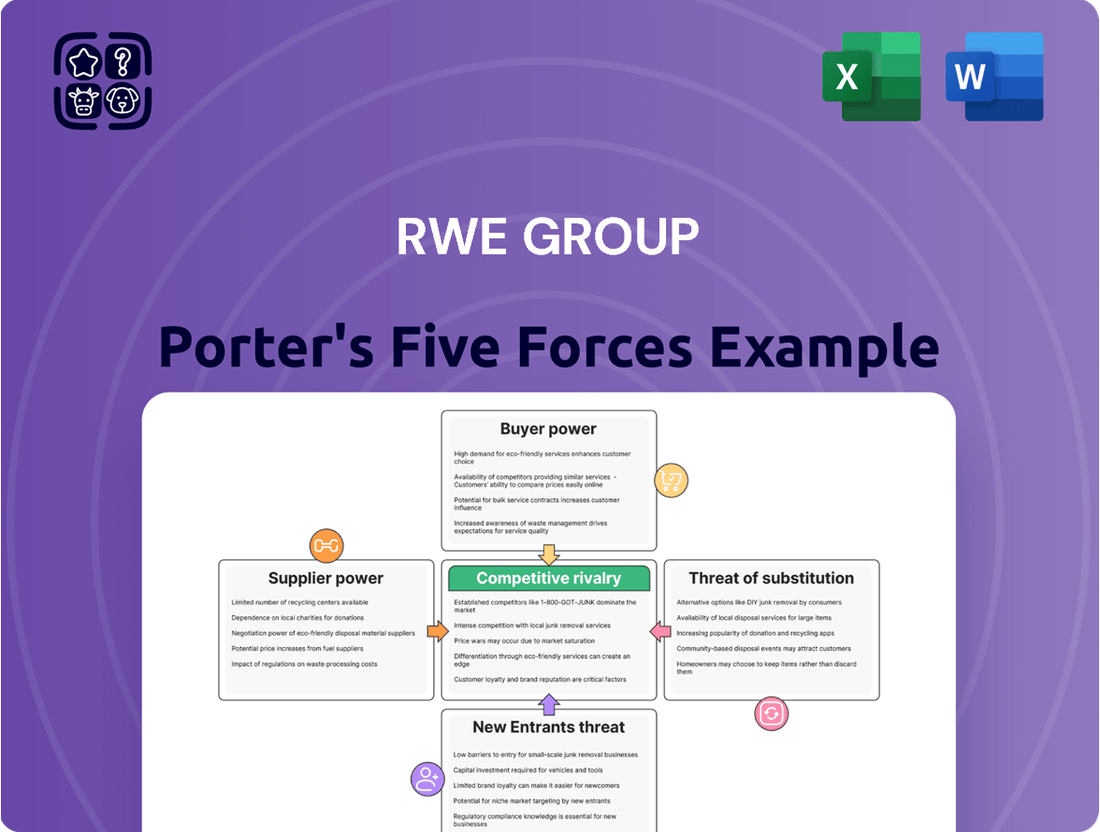

RWE Group operates in a dynamic energy sector where intense rivalry among existing players significantly shapes its market. The threat of new entrants, while present, is somewhat mitigated by high capital requirements and regulatory hurdles.

Bargaining power of suppliers for RWE Group is a critical factor, especially concerning fuel sources and technological components. Conversely, the bargaining power of buyers, particularly large industrial clients and governments, can impact pricing and contract terms.

The threat of substitute products or services, such as renewable energy alternatives to traditional power generation, presents a constant challenge to RWE Group's established business models.

The complete report reveals the real forces shaping RWE Group’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Key Component Suppliers

The market for crucial wind energy components, such as turbine blades, nacelles, and specialized installation vessels, often exhibits a high degree of concentration. This means a limited number of global manufacturers dominate the supply of these essential parts.

This concentration of suppliers, especially for cutting-edge or large-scale equipment, translates into considerable bargaining power for them. They can exert significant influence over energy developers like RWE, who are dependent on their specialized products and services.

RWE's substantial projects, for instance, the Sofia offshore wind farm which is one of the largest in the world, require specific manufacturers like Siemens Gamesa for its turbines. Similarly, specialized contractors such as Van Oord are essential for the complex installation process, highlighting RWE's reliance on a select group of suppliers.

Technological Specialization and IP

Suppliers with highly specialized technologies, like those developing advanced photovoltaic cells or cutting-edge grid-scale battery systems, wield significant influence. RWE's strategic pivot towards renewables and energy storage makes its reliance on these innovative suppliers particularly pronounced. For example, the rapid evolution in battery chemistries and performance metrics means RWE needs suppliers at the technological frontier to maintain its competitive edge.

Switching Costs for RWE

For RWE, the bargaining power of suppliers is significantly influenced by high switching costs, particularly in large-scale energy projects. Once RWE commits to specific technologies or suppliers, the expense and complexity of changing course can be considerable. This is especially true in sectors like offshore wind, where project-specific designs and intricate integration requirements make alternatives difficult and costly to implement.

Consider the construction of an offshore wind farm. The sheer scale of capital investment and the specialized logistics involved mean that RWE is often locked into a particular supplier's equipment and expertise for the duration of the project. For instance, if RWE deploys a specific turbine model from a single manufacturer, the costs of retooling, retraining, and reconfiguring the entire site to accommodate a different model later would be prohibitive. This dependency grants suppliers considerable leverage.

Availability of Raw Materials and Supply Chain Resilience

The availability of critical raw materials for renewable energy technologies significantly impacts the bargaining power of suppliers. For instance, RWE Group, like many in the energy sector, relies on materials such as rare earth elements essential for wind turbine magnets and lithium for battery storage solutions. Disruptions in these supply chains, often stemming from geopolitical tensions or concentrated production, can empower suppliers holding these vital resources.

While the cost of battery production has seen a downward trend, largely driven by expanded manufacturing capabilities, the market remains susceptible to price volatility. Rising raw material costs, coupled with the potential impact of evolving trade policies, present ongoing challenges. For example, in 2024, prices for key battery metals like lithium experienced fluctuations, underscoring the sensitivity of the sector to supply-side pressures.

- Reliance on Rare Earth Elements: Wind turbine manufacturers depend on rare earth elements, granting suppliers considerable leverage.

- Lithium Market Volatility: Fluctuations in lithium prices in 2024 highlight the vulnerability to raw material cost increases.

- Geopolitical Supply Chain Risks: Global events can disrupt the flow of essential materials, strengthening supplier positions.

- Trade Policy Impacts: Changes in international trade agreements can affect the cost and availability of renewable energy components.

Supplier's Ability to Forward Integrate

Suppliers' ability to forward integrate poses a significant threat to RWE Group. If suppliers, particularly those providing critical components for renewable energy projects, decide to develop and operate their own generation facilities, they could effectively bypass RWE. This would not only reduce RWE's access to essential equipment but could also lead to increased costs as RWE would face competition from its own former suppliers. For instance, a major wind turbine manufacturer entering the project development space could leverage its manufacturing scale and expertise to secure a competitive advantage, potentially squeezing margins for independent developers like RWE.

While major equipment manufacturers are often focused on their core business, the evolving energy landscape could incentivize some technology providers to explore direct project development. This move would shift the power dynamic, as these suppliers would then be competing with their existing customers. For example, a battery storage technology firm might decide to develop grid-scale storage projects that utilize its own technology, directly competing with RWE’s energy storage solutions.

- Supplier Incentive: Suppliers may be motivated to forward integrate if they see higher profit potential in operating energy projects compared to simply selling components.

- Market Dynamics: As renewable energy markets mature, suppliers might seek to capture more value chain revenue by moving into project development and operation.

- Impact on RWE: RWE could face reduced bargaining power and potentially higher input costs if key suppliers become direct competitors.

- Example Scenario: A solar panel manufacturer developing its own solar farms could control panel supply and pricing, impacting RWE's procurement strategies.

Renewable Energy: Suppliers Hold the Power

The bargaining power of RWE Group's suppliers is substantial, driven by the concentrated nature of the renewable energy component market. Key suppliers of specialized equipment like wind turbines and installation vessels often operate in oligopolistic structures, limiting RWE's options. High switching costs associated with complex, project-specific installations further solidify supplier leverage.

The reliance on critical raw materials, such as rare earth elements for magnets and lithium for batteries, also empowers suppliers. Geopolitical factors and trade policies can disrupt supply chains, increasing the cost and decreasing the availability of these essential inputs, as seen with lithium price fluctuations in 2024.

Forward integration by suppliers, where they might develop their own energy projects, presents a significant threat. This could transform RWE's suppliers into competitors, potentially increasing RWE's procurement costs and diminishing its negotiating strength.

| Factor | Impact on RWE | Supporting Data/Example (2024 Focus) |

|---|---|---|

| Supplier Concentration | High Bargaining Power | Limited number of global manufacturers for large-scale offshore turbines. |

| Switching Costs | Supplier Lock-in | Project-specific designs and integration in offshore wind require significant investment to change suppliers. |

| Raw Material Reliance | Vulnerability to Price Volatility | Lithium prices experienced fluctuations in 2024 due to supply-side pressures. |

| Forward Integration Potential | Threat of Competition | Technology providers may enter project development, competing with RWE. |

What is included in the product

This Porter's Five Forces analysis for RWE Group dissects the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the risk of substitute products within the energy sector.

Quickly identify and address competitive threats with a visual breakdown of RWE Group's industry landscape, making strategic planning more efficient.

Customers Bargaining Power

Large Industrial and Corporate Customers

Large industrial and corporate customers hold considerable sway when purchasing electricity directly from renewable energy producers like RWE, particularly through Power Purchase Agreements (PPAs). These buyers are increasingly focused on achieving their sustainability goals, which gives them leverage.

These significant consumers often negotiate for favorable pricing, commit to extended contract durations, and require authenticated green energy. This allows them a degree of control over the terms of their energy procurement.

A prime illustration of this dynamic is the growing trend of major technology firms securing substantial renewable energy PPAs to power their global data center operations. For instance, in 2023, Google announced plans to source 100% of its electricity consumption with carbon-free energy by 2030, driving demand for PPAs.

Market Liberalization and Customer Choice

In liberalized energy markets, RWE faces heightened customer bargaining power as consumers gain more choices for electricity and gas. This increased competition compels RWE to offer more competitive pricing, flexible contract terms, and additional services to retain and attract customers. For instance, in Germany, where RWE operates significantly, the number of electricity suppliers has grown substantially, leading to greater price transparency and a stronger position for consumers.

Customers can now readily switch providers based on factors like price, quality of service, or even a supplier's commitment to renewable energy. This ease of switching directly amplifies their influence over energy companies like RWE. By 2024, many European countries have seen significant shifts in customer loyalty driven by these very factors, with consumers actively seeking better deals and more sustainable energy options, putting pressure on established players.

Regulatory Frameworks and Consumer Protection

Energy market regulations frequently emphasize consumer protection, mandating fair pricing, transparency, and simplified processes for switching providers. This regulatory environment can curtail RWE's pricing influence, thereby bolstering the collective bargaining power of individual customers. For instance, in 2024, many European nations continued to implement price caps and consumer protection schemes to mitigate energy cost volatility.

Energy Efficiency and Demand-Side Management

Customers are increasingly able to reduce their overall energy consumption through efficiency measures and demand-side management. This lessens their reliance on energy providers and significantly increases their bargaining leverage. For example, in 2024, the International Energy Agency reported that energy efficiency improvements saved the equivalent of the European Union's total final energy consumption.

The rapid proliferation of energy-hungry artificial intelligence, coupled with the ongoing electrification of various sectors, is driving an exponential increase in electricity demand. However, advancements in energy storage technologies and continued focus on efficiency can effectively mitigate this rising consumption. By 2025, it's projected that AI could increase global electricity demand by as much as 10% compared to 2023 levels, highlighting the critical role of efficiency.

- Energy Efficiency Savings: In 2024, global investments in energy efficiency were estimated to reach over $600 billion, demonstrating a growing customer commitment to reducing consumption.

- Demand Response Participation: By late 2024, over 15 million US households were enrolled in some form of demand response program, allowing them to reduce usage during peak hours and gain financial benefits.

- Electrification Trends: The global electric vehicle market alone, a significant driver of electricity demand, is forecast to reach nearly 30 million units sold annually by 2025, underscoring the need for smart energy management.

Distributed Generation and Prosumers

The increasing adoption of distributed generation, like rooftop solar, transforms customers into prosumers, directly impacting their bargaining power. This shift allows them to generate their own electricity, lessening their dependence on traditional utility providers. In 2024, the residential solar market continued its robust growth, with many homeowners integrating battery storage solutions, further enhancing their energy independence and providing them with viable alternatives to grid supply.

This growing self-sufficiency translates into increased leverage for customers when negotiating terms or considering energy providers. As more households invest in behind-the-meter solutions, the traditional utility model faces pressure to adapt. The trend of customers becoming producers as well as consumers of energy is a significant factor in the evolving energy landscape, granting them more control over their energy consumption and costs.

- Prosumer Growth: Customers generating their own power reduces reliance on grid operators.

- Battery Storage Integration: Residential solar attachment rates to battery storage are rising, offering greater energy independence and backup options.

- Increased Alternatives: Distributed generation provides customers with more choices, enhancing their bargaining power.

- Reduced Grid Dependence: Prosumers can offset their consumption, leading to lower demand from traditional suppliers.

Customers Wield Power in Energy Market

Customers wield significant power by actively seeking competitive pricing and flexible contracts, especially in deregulated markets where switching providers is straightforward. This ability to choose, driven by factors like price and sustainability commitments, forces RWE to offer more attractive terms. For instance, by 2024, European consumers were increasingly prioritizing green energy and cost savings, directly impacting supplier negotiations.

| Factor | Impact on Customer Bargaining Power | RWE's Response |

|---|---|---|

| Market Liberalization | Increases choice, enabling customers to switch for better deals. | Offers competitive pricing and flexible contract terms. |

| Sustainability Focus | Large corporate buyers demand verifiable green energy. | Develops and markets renewable energy solutions. |

| Distributed Generation | Prosumers reduce reliance on grid supply. | Adapts business models to integrate distributed energy resources. |

| Energy Efficiency | Reduced consumption lessens dependence on providers. | Promotes energy-saving programs and smart grid technologies. |

Same Document Delivered

RWE Group Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis of the RWE Group, detailing the competitive landscape and strategic positioning of this energy giant. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file, which delves into the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the energy sector. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy, providing actionable insights into RWE's market dynamics.

Rivalry Among Competitors

Fragmented European Renewable Energy Market

The European renewable energy sector, while experiencing significant growth, is characterized by intense competition. RWE operates within a landscape populated by many established utilities, agile independent power producers, and emerging companies all seeking to capture market share.

This rivalry is underscored by the market's dynamism; in 2024, renewable sources supplied a record 48% of the European Union's electricity. Such a substantial contribution highlights the high level of activity and the ongoing struggle for dominance among numerous participants.

Intense Bidding for Project Development Rights

Competition is fierce for securing grid connection capacities and development rights for new renewable projects, particularly in high-demand sectors like offshore wind.

This intense bidding environment can significantly drive down project returns for developers like RWE Group. For example, Germany's 2024 offshore wind auctions demonstrated this, with successful bidders committing over €4 billion in concession fees, reflecting the high stakes involved.

Pricing Pressure from Overcapacity in Manufacturing

The energy sector, particularly renewables, is experiencing intense pricing pressure. This stems from overcapacity in manufacturing for key components like solar panels. For instance, global solar panel manufacturing capacity in 2023 was estimated to be around 1,100 GW, significantly exceeding the approximately 400 GW of installations, creating a surplus that drives down prices.

This oversupply, coupled with ongoing cost reductions in renewable technologies, forces companies like RWE to operate with tighter margins. The declining costs, while beneficial for consumers, directly translate into pressure on RWE to optimize its own operational expenses and ensure its electricity offerings remain competitive in a market where cheaper alternatives are readily available.

The potential for similar overcapacity in electrolyzer manufacturing for green hydrogen production also looms, which could further exacerbate pricing challenges in emerging clean energy markets. RWE must therefore focus on efficiency and strategic cost management to navigate this competitive landscape effectively.

Strategic Investments and Expansion by Competitors

Established utilities and emerging energy firms are significantly boosting their investments in renewable energy projects, a move that directly mirrors RWE's own 'Growing Green' strategy and heightens competitive pressures. This aggressive expansion by numerous market participants intensifies the rivalry, as evidenced by RWE's substantial €10 billion net investment in 2024 and ambitious plans for €35 billion in net investments between 2025 and 2030.

The competitive landscape is characterized by strategic investments and expansion efforts across the sector. Key players are actively pursuing growth in renewable portfolios, leading to a more crowded and competitive market.

- Aggressive Investment in Renewables: Competitors are channeling significant capital into expanding their renewable energy capacity, mirroring RWE's strategic focus.

- Intensified Rivalry: This widespread investment drive leads to fiercer competition for resources, projects, and market share among energy companies.

- RWE's Investment Commitment: RWE's planned €10 billion net investment in 2024 and €35 billion net investment target for 2025-2030 underscore the scale of capital deployment in the sector.

- Market Share Battles: The race to build out green energy infrastructure means companies are directly competing to capture market share in a rapidly evolving energy transition.

Policy and Regulatory Landscape Volatility

Policy and regulatory volatility significantly shapes the competitive rivalry within the energy sector, impacting RWE Group. Shifting government subsidies, evolving auction mechanisms, and changing permitting processes create a dynamic and often unpredictable landscape. Companies demonstrating agility in adapting to these policy shifts, or those strategically positioned to benefit from specific national incentives, often achieve a distinct competitive advantage.

This policy uncertainty can directly influence investment decisions. For instance, RWE itself has indicated adjustments to its investment strategy due to policy unpredictability in key growth areas, such as US offshore wind development and the burgeoning European hydrogen market. Such shifts mean that what might be a favored technology or market one year could face altered support or increased hurdles the next.

- Policy Uncertainty Impact: In 2024, a notable example of policy-driven shifts was the recalibration of renewable energy targets in several European nations, influenced by geopolitical energy security concerns and evolving economic conditions. This led to some companies reassessing project pipelines.

- Adaptability as a Differentiator: Companies with robust government affairs teams and flexible project planning capabilities are better equipped to navigate these changes, potentially securing favorable terms in new regulatory frameworks or auction rounds.

- Subsidies and Market Access: Changes in feed-in tariffs or renewable energy certificate schemes directly affect project economics. For example, a reduction in subsidies in a key market could make projects there less attractive compared to those in regions with more stable or enhanced support.

- Permitting Process Efficiency: Streamlined or, conversely, more complex permitting processes can significantly alter the speed to market for new projects, creating a competitive edge for those who can navigate these requirements more efficiently.

Billions Fuel Europe's Renewable Energy Rivalry

The competitive rivalry within the European renewable energy sector is exceptionally high, with RWE facing numerous established utilities, agile independent power producers, and emerging players.

This intense competition is driven by substantial investments from all sides. For instance, RWE's commitment of €10 billion net investment in 2024 and a target of €35 billion between 2025 and 2030 reflects the capital-intensive nature of the market and the aggressive expansion strategies of its competitors.

The market dynamics in 2024, where renewable sources supplied a record 48% of the EU's electricity, underscore the high level of activity and the ongoing battle for market share and project acquisition. This fierce competition extends to securing grid connection capacities and development rights, particularly in lucrative areas like offshore wind, as evidenced by Germany's 2024 offshore wind auctions which saw over €4 billion in concession fees committed.

Furthermore, overcapacity in key component manufacturing, such as solar panels, with global capacity in 2023 exceeding installations by a significant margin, creates pricing pressure that forces companies like RWE to optimize costs and maintain competitive margins.

| Key Competitor Investment & Activity (Illustrative) | 2024 Investment (Approx.) | Project Pipeline Focus | Market Share Goal |

| RWE Group | €10 Billion (Net) | Offshore Wind, Solar, Hydrogen | Leading European Generator |

| Iberdrola | €11 Billion (Global) | Onshore/Offshore Wind, Solar, Networks | Global Renewable Leader |

| Enel Green Power | €7 Billion (Global) | Solar, Wind, Geothermal | Expanding European Presence |

| Orsted | €5 Billion (Global) | Offshore Wind, Onshore Wind, Solar | Global Offshore Wind Leader |

SSubstitutes Threaten

Alternative Renewable Technologies

While RWE Group is a major player in wind and solar power, other renewable energy sources present a threat of substitution. Technologies such as geothermal energy, biomass, and wave or tidal power can fulfill similar energy needs, potentially drawing investment and market share away from RWE's core offerings.

The landscape of clean energy is constantly evolving, with ongoing innovation leading to the emergence of new substitutes. For instance, advancements in long-duration energy storage solutions and more efficient solar cell technologies mean that the competitive set is always expanding, requiring RWE to remain agile.

In 2024, the global renewable energy market continued to see significant growth, with solar PV and wind power leading the charge, but investments in other areas like green hydrogen, which can be produced using renewables, also saw substantial increases, indicating a diversification of energy solutions that could act as substitutes.

Energy Efficiency and Demand Reduction

Improvements in energy efficiency across industrial, commercial, and residential sectors represent a significant threat of substitution for RWE Group. By reducing overall electricity consumption, these efficiency gains lessen the demand for new generation capacity and existing power supply, directly impacting RWE's core business.

While the burgeoning integration of AI and data centers is projected to increase electricity demand, the persistent focus on energy efficiency remains a crucial counteracting force. For instance, in 2024, initiatives aimed at optimizing building energy management systems and industrial processes are gaining traction, potentially mitigating some of this new demand.

Grid Modernization and Smart Grids

Investments in grid modernization and smart grids by utilities, including RWE Group, directly address the threat of substitutes. These advancements allow for greater integration of distributed energy resources (DERs) like solar and wind, which can reduce reliance on traditional, large-scale centralized power generation.

For instance, the European Union's renewable energy targets, with a goal of at least 42.5% renewable energy by 2030, drive significant investment in smart grid technologies to manage the intermittency of these sources. This technological shift effectively substitutes for the consistent output of conventional power plants.

Energy storage solutions are a prime example of a substitute. By 2024, global battery storage capacity is projected to reach hundreds of gigawatts, enabling better load balancing and grid resilience. This stored energy can be dispatched when needed, lessening the demand for immediate generation from fossil fuel plants.

Furthermore, advancements in demand-side management technologies empower consumers to reduce their electricity consumption during peak hours. This behavioral change, facilitated by smart meters and intelligent home energy systems, acts as a substitute for building additional generation capacity.

Green Hydrogen and Other Energy Carriers

Green hydrogen, generated using renewable electricity, presents a significant threat of substitution for traditional fossil fuels, particularly in sectors that are difficult to decarbonize, such as heavy industry and long-distance transportation. RWE's strategic investments in green hydrogen production mean they are both a player in this emerging market and subject to its disruptive potential. The increasing viability of green hydrogen could divert demand from direct electricity consumption in these specific applications, impacting RWE's core business segments.

The global green hydrogen market is projected for substantial growth, with estimates suggesting it could reach hundreds of billions of dollars by 2030. For instance, the International Energy Agency (IEA) has highlighted the crucial role of hydrogen in achieving net-zero emissions, with a significant portion needing to be green hydrogen. This growth indicates a tangible shift in energy carrier preferences that RWE must continually monitor and adapt to.

- Growing Demand: The demand for green hydrogen is anticipated to rise considerably as industries seek low-carbon alternatives.

- Sectoral Impact: Hard-to-abate sectors, responsible for a substantial portion of global emissions, are prime targets for green hydrogen adoption.

- RWE's Position: RWE is investing heavily in green hydrogen projects, aiming to be a leading producer and user.

- Substitution Risk: The success of green hydrogen could lead to a reduction in direct electricity sales for RWE in certain industrial and transport markets.

Advanced Energy Storage Solutions

The threat of substitutes for RWE's advanced energy storage solutions is significant, driven by the accelerating pace of innovation and adoption across the energy sector. Beyond RWE's direct investments in battery storage, alternative technologies like long-duration storage and advancements in pumped hydro are gaining traction.

These substitutes can directly challenge the need for flexible generation assets that RWE might offer or rely on. For instance, improved pumped hydro systems can provide grid stability and manage peak demand, effectively performing a similar function to battery storage. The global energy storage market saw remarkable growth, with installations increasing by over 75% in 2024 alone, and this trend is projected to persist, underscoring the competitive landscape.

- Technological Alternatives: Innovations in long-duration storage technologies (e.g., flow batteries, compressed air energy storage) offer alternatives to short-duration battery solutions.

- Established Solutions: Traditional methods like pumped hydro storage, which has a long operational history and increasing efficiency, continue to be a viable substitute.

- Market Growth: The substantial rise in global energy storage installations, exceeding 75% in 2024, indicates a broadening market for storage solutions, including those not directly developed by RWE.

- Cost Competitiveness: As substitute technologies mature, their cost-effectiveness can improve, potentially making them more attractive than RWE's offerings in certain applications.

Emerging Substitutes Challenge Core Renewable Offerings

The threat of substitutes for RWE Group's core renewable energy offerings, particularly wind and solar, is multifaceted. Emerging technologies in energy generation and storage, alongside improvements in energy efficiency, all present viable alternatives for meeting energy demands.

Innovations in geothermal, biomass, and tidal power continue to mature, offering diverse pathways for clean energy generation. Furthermore, advancements in energy efficiency across all sectors directly reduce the overall demand for electricity, acting as a substitute for new generation capacity.

For example, global investments in green hydrogen saw substantial increases in 2024, with projections indicating significant market growth. This burgeoning sector, while potentially synergistic with renewables, also represents a substitute energy carrier for hard-to-abate industries.

Additionally, the expanding capacity and decreasing costs of energy storage solutions, including battery and pumped hydro technologies, provide alternatives to direct electricity consumption from RWE's generation assets. The global energy storage market saw installations increase by over 75% in 2024 alone.

| Substitute Technology | Description | 2024 Relevance | Potential Impact on RWE |

|---|---|---|---|

| Green Hydrogen | Energy carrier produced using renewable electricity. | Significant investment and market growth projected; IEA highlights its role in net-zero. | Potential diversion of demand from direct electricity use in heavy industry and transport. |

| Energy Efficiency | Reducing overall electricity consumption. | Growing traction in building management and industrial processes. | Directly lessens demand for new generation capacity. |

| Advanced Energy Storage | Long-duration storage, pumped hydro, etc. | Global installations up over 75% in 2024; cost-effectiveness improving. | Can provide grid stability and peak load management, substituting for flexible generation. |

Entrants Threaten

High Capital Intensity

The energy generation sector, especially for large-scale renewable projects like offshore wind farms, demands massive upfront capital. This high capital intensity acts as a formidable barrier, deterring many potential new competitors from entering the market.

RWE Group's own financial commitments underscore this challenge. The company invested €10 billion net in 2024 and has a strategic plan to invest €35 billion net between 2025 and 2030, illustrating the sheer scale of financial resources required to compete effectively in this industry.

Complex Regulatory and Permitting Environment

The complex regulatory and permitting environment poses a significant threat to new entrants in the energy sector, particularly for companies looking to establish themselves in markets where RWE Group operates. Navigating these intricate processes, which often involve multiple layers of government and environmental reviews, can be a substantial deterrent. For instance, obtaining permits for a new offshore wind farm can take several years, with delays frequently pushing back project timelines and increasing initial capital outlays. This lengthy approval cycle, coupled with the need for specialized expertise to manage compliance, creates a high barrier to entry for smaller or less experienced players.

Access to Grid Infrastructure

Securing access to existing electricity grids and the necessary new grid connections presents a significant barrier for new entrants in the energy sector. For RWE Group and other established players, this infrastructure is fundamental to delivering generated power to consumers. In 2024, the ongoing need for grid upgrades and the persistent issue of grid bottlenecks continue to constrain the ability of new companies to effectively market their energy output.

Technological Expertise and Scale

The threat of new entrants for RWE Group, particularly concerning technological expertise and scale, is moderate. Developing, operating, and maintaining large-scale renewable energy assets requires significant specialized technical know-how, sophisticated project management skills, and substantial economies of scale that are difficult for newcomers to replicate quickly. RWE benefits from decades of accumulated experience and a deeply entrenched skilled workforce, giving it a distinct advantage.

New entrants face considerable hurdles in matching the operational efficiency and cost-effectiveness that established players like RWE have achieved through years of investment and learning. For instance, RWE's substantial portfolio, which includes over 10 GW of offshore wind capacity as of early 2024, represents a significant barrier to entry for smaller, less experienced companies. The capital investment required to build comparable infrastructure is immense, and the learning curve for managing complex projects, grid integration, and ongoing maintenance is steep.

- High Capital Requirements: Building a new offshore wind farm, for example, can cost billions of euros, a sum many new entrants cannot easily secure.

- Specialized Technical Skills: Expertise in areas like turbine technology, offshore engineering, and grid connection are critical and take years to develop.

- Economies of Scale: RWE's existing scale allows for bulk purchasing, optimized logistics, and shared overheads, which new entrants cannot immediately leverage.

- Regulatory and Permitting Expertise: Navigating complex permitting processes for large-scale projects is a significant challenge for new players.

Established Customer Relationships and Market Access

Established players like RWE Group enjoy significant advantages due to deep-rooted customer relationships and extensive market access. These incumbents have cultivated trust and loyalty with large industrial clients, municipal authorities, and a vast residential customer base over many years, creating substantial barriers for newcomers. Furthermore, RWE possesses an existing and sophisticated energy trading infrastructure, a critical asset that new entrants would struggle to replicate quickly.

New entrants find it exceptionally challenging to penetrate markets where incumbent firms have already secured strong customer loyalty and built robust distribution networks. Building this level of trust and market presence from scratch requires considerable time, investment, and strategic effort. For instance, in the German energy market, where RWE is a major player, customer switching rates can be influenced by perceived reliability and long-term contracts, making it harder for new companies to gain traction.

- Established Customer Base: RWE benefits from long-standing contracts with key industrial and municipal partners, ensuring stable demand and revenue streams.

- Market Access and Infrastructure: Existing grid connections, trading platforms, and logistical networks provide incumbents with a critical advantage in service delivery and cost efficiency.

- Brand Trust and Reputation: Decades of operation have built significant brand recognition and trust, which new entrants must work hard to achieve.

- Regulatory Familiarity: Incumbents possess deep understanding and experience navigating complex energy regulations, a hurdle for new market participants.

High Barriers Protect Energy Incumbents from New Rivals

The threat of new entrants for RWE Group is generally considered low to moderate due to substantial barriers. These include the immense capital required for large-scale renewable projects, complex regulatory landscapes, and the established infrastructure and customer relationships RWE already possesses. Newcomers struggle to match the economies of scale and technical expertise that RWE has cultivated over years of operation.

| Barrier | Description | Impact on New Entrants |

|---|---|---|

| Capital Intensity | Renewable energy projects, especially offshore wind, demand billions in upfront investment. | High barrier; limits the pool of potential competitors. |

| Regulatory Complexity | Navigating permits and environmental reviews can take years. | Significant deterrent; requires specialized expertise and patience. |

| Infrastructure Access | Securing grid connections and upgrades is crucial and often constrained. | Challenging for new players to integrate and deliver power efficiently. |

| Technical Expertise & Scale | Operating and maintaining large assets requires deep knowledge and experience. | Difficult for newcomers to replicate RWE's operational efficiency and cost advantages. |

| Customer Relationships | Established trust and long-term contracts create loyalty for incumbents. | New entrants face a long road to build brand recognition and secure market share. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a foundation of diverse and credible data sources, including company annual reports, industry-specific market research, regulatory filings, and economic indicators. This multifaceted approach ensures a comprehensive understanding of the competitive landscape.