Lloyds Banking Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Lloyds Banking Group

From Overview to Strategy Blueprint

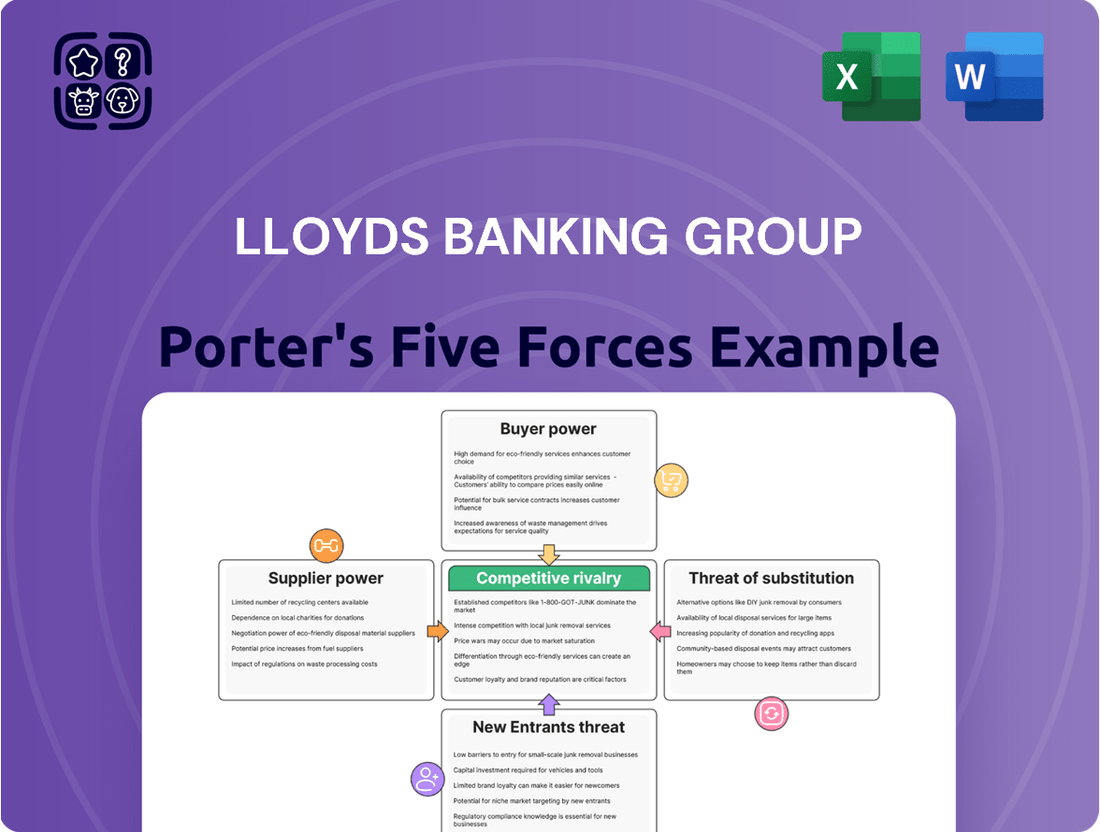

Lloyds Banking Group navigates a dynamic financial landscape, shaped by intense competition and evolving customer expectations. Understanding the forces at play is crucial for strategic success.

The threat of new entrants, while somewhat mitigated by regulatory hurdles, remains a consideration, potentially introducing innovative disruption.

Buyer power is significant, with customers demanding competitive rates and superior digital experiences, forcing constant service improvements.

The bargaining power of suppliers, particularly technology providers, can influence operational costs and efficiency.

The threat of substitute products, such as challenger banks and FinTech solutions, continuously pushes traditional institutions to adapt.

The complete report reveals the real forces shaping Lloyds Banking Group’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentrated Technology and Software Providers

In 2024, Lloyds Banking Group heavily relies on a concentrated group of technology providers for essential core banking systems and cloud infrastructure. Key vendors such as Temenos, Finastra, Microsoft, and AWS command significant market share, giving them considerable influence over pricing and contract terms. The high costs associated with switching these core systems, estimated to be in the hundreds of millions, cement the power of these incumbent suppliers. This dependency means any disruptions or price increases from these few providers can directly impact the bank's operational efficiency and overall costs.

Specialized Financial Services Professionals

The banking sector, including Lloyds Banking Group, heavily relies on professionals with specialized skills in areas like risk management, financial analysis, and compliance. The demand for expertise in emerging fields such as artificial intelligence, data analytics, and cybersecurity is particularly high, with some reports indicating a 2024 UK finance salary increase of 5-10% for in-demand tech roles. This creates a competitive labor market where skilled individuals possess greater bargaining power for higher compensation and improved working conditions. Lloyds must strategically invest in attracting and retaining this critical talent to maintain its competitive edge and ensure operational resilience.

Regulatory and Compliance Consultants

The UK financial services industry, overseen by bodies like the FCA and PRA, necessitates specialized expertise for regulatory compliance. Lloyds Banking Group heavily relies on consultants to navigate complex rules, especially given the FCA levied over £250 million in fines in 2024. These firms possess unique knowledge, which grants them significant bargaining power. The high costs of non-compliance, including potential fines and reputational damage, make their services indispensable for banks like Lloyds.

Depositors as Capital Suppliers

While individual depositors typically hold limited power, large corporate clients and groups of high-net-worth individuals possess significant leverage over Lloyds Banking Group. These entities are crucial capital suppliers, directly funding the bank's lending operations. Their ability to move substantial funds to competitors, especially in the competitive 2024 UK banking market, grants them power to negotiate better interest rates and bespoke services. Therefore, attracting and retaining these significant capital suppliers is paramount for Lloyds' liquidity and profitability.

- Lloyds' retail and commercial deposits stood at approximately £474 billion as of Q1 2024.

- Large corporate and high-net-worth deposits represent a significant portion of the total, impacting funding costs.

- The Bank of England's base rate in 2024 influences deposit rate negotiations.

- Competitive pressures from challenger banks enhance depositors' bargaining power for better returns.

Critical Third-Party Service Providers

Lloyds Banking Group, like other major banks, heavily relies on critical third-party providers for essential functions such as payment processing and cloud infrastructure. UK regulators, including the Bank of England and PRA, have intensified scrutiny on these relationships, noting in 2024 the potential for systemic risk from a single point of failure. The operational disruption from a critical supplier's failure could be severe, giving these providers substantial bargaining power over the bank.

- In 2024, the PRA emphasized that over 70% of UK financial firms use third-party cloud services for critical operations.

- The Bank of England's 2024 Financial Stability Report highlighted cyber resilience and operational continuity risks from third parties.

- Significant outages from critical third-party IT providers have impacted major UK banks, underscoring their leverage.

Bank's Vendor Leverage: Tech, Talent, & Regulatory Costs

Lloyds Banking Group faces significant supplier power from concentrated technology vendors like Microsoft and AWS, due to high switching costs. Critical third-party service providers and specialized talent in AI and cybersecurity also hold leverage, reflected in 2024 UK finance salary increases. Furthermore, regulatory compliance consultants and large corporate depositors can negotiate favorable terms, impacting the bank's operational efficiency and funding costs.

What is included in the product

Tailored exclusively for Lloyds Banking Group, analyzing its position within its competitive landscape by evaluating buyer and supplier power, threat of new entrants and substitutes, and the intensity of rivalry.

Quickly identify and mitigate competitive threats by visualizing the intensity of each of Porter's Five Forces, enabling targeted strategic responses.

Customers Bargaining Power

High Price Sensitivity in a Competitive Market

UK banking customers, spanning both retail and commercial sectors, demonstrate significant price sensitivity, diligently comparing interest rates and fees on various financial products. The ease of switching accounts, greatly facilitated by the Current Account Switch Service (CASS), intensifies this sensitivity, with CASS reporting over 260,000 completed switches in Q1 2024 alone. This competitive environment compels Lloyds Banking Group to maintain highly competitive pricing for loans, savings accounts, and other offerings. Consequently, Lloyds must continuously optimize its pricing strategies to retain its customer base and prevent attrition to rivals offering more attractive terms.

Low Switching Costs for Current Accounts

The Current Account Switch Service (CASS) empowers customers, making it easier to switch their primary bank account within seven working days. This low switching cost increases customer bargaining power, as they can readily move to competitors for better services or rates. In 2024, CASS reported over 1.3 million switches, demonstrating customers' willingness to change banks for improved offerings. Lloyds Banking Group faces pressure to retain customers through competitive products and features.

Increasing Demand for Digital and Mobile Banking

Customers now wield significant bargaining power due to the widespread demand for sophisticated digital and mobile banking. UK online banking adoption reached 91% in 2024, highlighting this shift. Customers expect intuitive platforms for payments and financial management, making digital experience a key differentiator. Failure to meet these evolving expectations risks losing customers to agile fintechs and neobanks, which often offer superior digital interfaces.

Access to Information and Comparison Tools

Customers of Lloyds Banking Group now wield significant power due to unprecedented access to financial information. The proliferation of online comparison tools and financial websites, for instance, allows easy comparison of products like mortgages or savings accounts across various providers. This transparency empowers customers to make highly informed decisions, strengthening their negotiating position considerably as they can readily identify the most competitive offerings. For example, in 2024, an estimated 85% of UK adults actively use online banking, showcasing widespread digital engagement.

- Digital platforms facilitate instant product comparisons.

- Consumers can easily switch providers based on better terms.

- Increased transparency drives competitive pricing among banks.

- Customer loyalty is challenged by readily available alternatives.

Regulatory Protection and the Consumer Duty

The Financial Conduct Authority’s (FCA) Consumer Duty, fully effective for new and existing products by July 2024, significantly enhances customer bargaining power. This regulation mandates that banks like Lloyds Banking Group act in their customers’ best interests, ensuring fair value and clear communication. It compels firms to provide products and services that deliver good outcomes, shifting the onus onto the financial institution. This regulatory backing empowers individual customers by holding banks to a higher standard of conduct and care, potentially influencing pricing and service quality.

- FCA Consumer Duty came into full effect for closed products by July 2024, strengthening customer protections.

- It requires banks to prioritize customer outcomes, ensuring fair value and transparent dealings.

- This regulation increases the leverage of retail customers against financial institutions.

- Lloyds Banking Group, like other UK banks, must demonstrate compliance, impacting product design and customer service.

Customer Power: Switches, Digital Tools, and FCA Duty Reshape Banking

Customers wield significant power due to easy account switching, with CASS reporting 1.3 million switches in 2024, and widespread digital transparency. Their access to online comparison tools, used by 85% of UK adults in 2024, enables informed choices. The FCA Consumer Duty, fully effective by July 2024, further strengthens customer leverage, mandating fair outcomes from banks like Lloyds.

| Factor | 2024 Data | Impact on Power |

|---|---|---|

| CASS Switches | 1.3 Million | High |

| UK Online Banking Adoption | 91% | High |

| FCA Consumer Duty | Fully Effective July | High |

What You See Is What You Get

Lloyds Banking Group Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It details Lloyds Banking Group's competitive landscape through Porter's Five Forces, examining the threat of new entrants, the bargaining power of buyers, the bargaining power of suppliers, the threat of substitute products or services, and the intensity of rivalry among existing competitors. Understanding these forces provides critical insights into the strategic challenges and opportunities facing Lloyds in the UK banking sector. This comprehensive analysis is ready for your immediate use.

Rivalry Among Competitors

Intense Competition from Incumbent Banks

The UK banking market experiences intense rivalry, predominantly from established players like NatWest, Barclays, and HSBC, alongside Lloyds itself. These major incumbent banks fiercely compete for market share across all segments, from retail mortgages to commercial banking and wealth management. This rivalry manifests in competitive pricing, with average 2-year fixed mortgage rates around 4.88% in early 2024, and significant investment in technology. Intense marketing campaigns are also common as each bank strives to attract and retain its customer base.

Growing Threat from Challenger Banks

Digital-first challenger banks like Monzo, Starling Bank, and Revolut have gained significant traction, particularly with younger, tech-savvy customers. These neobanks often offer superior digital experiences, innovative features, and lower fees, directly challenging traditional models. For instance, Starling Bank reported profitability in 2024, demonstrating their growing viability. While they pose a limited immediate threat to displacing primary banking relationships, their collective UK customer base, exceeding 20 million by early 2024, represents a significant competitive pressure on Lloyds to innovate.

Competition for Customer Deposits

Competition for customer deposits has notably intensified, driven by elevated interest rates, such as the Bank of England's base rate holding at 5.25% into 2024, and the critical need for stable funding sources. Banks are actively offering more attractive savings rates and incentives to both attract new depositors and retain existing ones. This fierce rivalry directly impacts net interest margins, a crucial profitability driver for institutions like Lloyds Banking Group. For example, Lloyds reported a Net Interest Margin of 3.11% for the full year 2023, reflecting these competitive pressures. This ongoing battle for deposits continues to shape banking sector profitability in 2024.

Mergers and Acquisitions Leading to Consolidation

The UK banking sector continues to see significant consolidation, with larger institutions acquiring smaller challenger banks and building societies. This trend, highlighted by Nationwide's agreement to acquire Virgin Money in March 2024 and Coventry Building Society's planned purchase of The Co-operative Bank announced in April 2024, directly impacts competitive rivalry. While reducing the sheer number of competitors, it strengthens the market position of the remaining dominant players like Lloyds Banking Group. This ongoing consolidation reinforces the established major banks' market share and influence.

- Nationwide's acquisition of Virgin Money (announced March 2024) consolidates retail banking.

- Coventry Building Society's purchase of The Co-operative Bank (announced April 2024) further reduces independent entities.

- This trend decreases the number of competitors, potentially increasing market power for remaining large banks.

- The reduced competitive landscape could lead to less aggressive pricing pressures for major players.

Innovation in Financial Products and Services

Competition in banking extends beyond price to the constant innovation of new products and services. Financial institutions, including Lloyds Banking Group, are continuously launching new offerings, from specialized mortgage products to advanced wealth management platforms and sustainable investment options. For example, in 2024, Lloyds aimed to expand its digital wealth proposition to meet evolving customer needs and compete with fintech disruptors. Lloyds must continually invest in research and development to keep pace with competitors and maintain its market position.

- Lloyds' 2024 capital allocation included significant investment in digital transformation and new product development to enhance customer experience.

- The group has focused on expanding its sustainable finance options, reflecting a growing market demand.

- Rival banks are also heavily investing; for instance, NatWest Group reported increased spending on digital innovation in 2024 to improve customer journeys.

- Innovation is key to attracting and retaining customers, especially younger demographics seeking seamless digital banking solutions.

UK Banking: Fierce Competition and Digital Disruption

Competitive rivalry in the UK banking sector is exceptionally high for Lloyds Banking Group, stemming from established giants like NatWest and Barclays, alongside agile digital challengers such as Starling Bank, which reported profitability in 2024. This fierce competition drives aggressive pricing, with average 2-year fixed mortgage rates around 4.88% in early 2024, and intense battles for customer deposits, influenced by the Bank of England's base rate holding at 5.25% into 2024. Consolidation, like Nationwide's acquisition of Virgin Money in March 2024, reshapes the landscape, while continuous innovation in digital offerings remains crucial for maintaining market share.

| Metric | Lloyds Banking Group (2023/2024) | UK Banking Sector (2024) |

|---|---|---|

| Net Interest Margin (FY2023) | 3.11% | Varies by institution |

| Avg. 2-Year Fixed Mortgage Rate (Early 2024) | N/A (Market Average) | ~4.88% |

| Digital Challenger Customer Base (Early 2024) | N/A (Collective) | >20 million (e.g., Monzo, Starling) |

SSubstitutes Threaten

Fintech and Peer-to-Peer (P2P) Lending Platforms

Financial technology companies and peer-to-peer lending platforms offer significant alternatives to traditional banking services. These platforms often streamline the loan approval process, providing faster access to funds and potentially more competitive rates than conventional banks. For instance, the UK P2P lending market, while smaller than traditional banking, has seen sustained activity, with total P2P lending volumes reaching billions of pounds annually. This directly substitutes Lloyds Banking Group's offerings, particularly for smaller, unsecured loans to individuals and SMEs, pushing for digital innovation and efficiency.

Robo-Advisors and Digital Investment Platforms

Robo-advisors and digital investment platforms present a significant substitute threat to Lloyds Banking Group's wealth management. These automated services, leveraging algorithms, offer low-cost portfolio management, making investing accessible to a broader market segment. For instance, global robo-advisor assets under management are projected to reach over $3.5 trillion in 2024, reflecting strong customer adoption. This trend directly competes with Lloyds' traditional advisory offerings, pressuring fees and client retention.

Digital Payment Solutions

The rise of digital payment solutions, like those from Apple Pay and Google Pay, presents a significant substitute threat to Lloyds Banking Group's traditional services. These platforms, often linked to bank accounts, reduce the need for customers to directly interact with the bank's own payment interfaces for everyday transactions. In 2024, mobile payment users in the UK were projected to exceed 35 million, demonstrating a strong shift away from conventional card usage. The convenience and seamless integration offered by these fintech alternatives directly compete with the bank's core transactional functions.

Crowdfunding Platforms

Crowdfunding platforms pose a growing threat of substitution to Lloyds Banking Group, particularly in business financing. For startups and small to medium-sized enterprises, platforms like Crowdcube and Seedrs have emerged as viable alternatives to traditional loans. These platforms allow businesses to raise capital directly from a large pool of individual investors, bypassing the need for a conventional banking relationship for initial funding. This trend significantly impacts Lloyds' potential market share in business lending, as companies increasingly diversify their funding sources. The continued growth of these alternative financing channels in 2024 further intensifies this competitive pressure.

- In 2023, the UK equity crowdfunding market facilitated over 300 million pounds in investment, demonstrating its significant role.

- Globally, the crowdfunding market is projected to reach substantial figures by 2024, indicating broad adoption.

- Platforms enable businesses to secure capital faster and with less stringent requirements than traditional banks.

- This shift directly reduces the reliance on established banking institutions for early-stage and growth funding.

Cryptocurrencies and Decentralized Finance (DeFi)

The rise of cryptocurrencies and Decentralized Finance (DeFi) presents a long-term substitute threat to Lloyds Banking Group, potentially disrupting traditional services like payments and lending. While still volatile, these platforms could challenge banks' intermediary role as technology matures. The UK government and regulators, including the FCA, are actively developing a comprehensive regulatory regime for cryptoassets, with new rules on crypto promotions effective from October 2023.

- The global crypto market capitalization exceeded $2 trillion in early 2024, indicating growing adoption.

- The UK Treasury's 2024 consultation outlined plans for regulating stablecoins and broader crypto assets.

Banking Faces Digital Substitutes

The threat of substitutes for Lloyds Banking Group is high, driven by fintech innovations like peer-to-peer lending, digital payments, and robo-advisors. These alternatives offer faster, more convenient, and often lower-cost services, directly competing with traditional banking. Emerging decentralized finance and crypto solutions also pose a long-term risk. This forces Lloyds to innovate to retain market share across payments, lending, and wealth management.

| Substitute Type | 2024 Projection/Data | Impact on Lloyds |

|---|---|---|

| Robo-Advisors AUM | >$3.5 trillion | Wealth management competition |

| UK Mobile Payments Users | >35 million | Reduced traditional payment reliance |

| Global Crypto Market Cap | >$2 trillion | Long-term disruptive potential |

Entrants Threaten

High Regulatory Barriers to Entry

The UK banking industry presents high regulatory barriers, primarily driven by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA). New entrants must navigate a rigorous authorization process, meeting stringent capital requirements like those under Basel III, which in 2024 mandate significant common equity tier 1 ratios. These aspiring banks face substantial costs and time commitments to establish robust governance and risk management frameworks. Such complex and demanding regulatory hurdles deter many potential new competitors, solidifying the position of established players like Lloyds Banking Group.

Strong Brand Loyalty and Customer Trust

Established banks like Lloyds Banking Group benefit from deep-rooted brand recognition and customer trust, cultivated over decades. New entrants face a significant hurdle in building a credible brand from scratch to convince customers to entrust them with their finances. Lloyds, for instance, serves over 26 million customers as of 2024, highlighting its extensive reach and established relationships. This strong customer loyalty and the perception of security associated with major financial institutions make it challenging for newcomers to gain significant market share.

Economies of Scale of Incumbent Banks

Established banks like Lloyds Banking Group significantly benefit from economies of scale, stemming from their extensive IT infrastructure, marketing reach, and regulatory compliance. This allows them to offer a diverse range of products at a lower cost per customer than new entrants can achieve. For instance, Lloyds reported a cost-to-income ratio of 49.6% in Q1 2024, reflecting their operational efficiency. New banks often struggle to compete on price and product breadth until they can amass a substantial customer base, making market penetration difficult.

Access to Distribution Channels

Access to distribution channels remains a significant barrier for new entrants in the UK banking sector. While digital banking is growing, a physical branch network like Lloyds Banking Group's, which still maintains hundreds of branches across the UK in 2024, provides a distinct advantage. This extensive reach caters to customer segments who prefer in-person service or require cash access, making it costly and challenging for new, digital-only banks to replicate such widespread physical presence.

- Lloyds Banking Group operated hundreds of physical branches across the UK as of early 2024.

- Many UK customers, particularly older demographics, still value in-person banking services.

- New digital-only banks face high customer acquisition costs without a physical footprint.

- Access to cash services remains a key differentiator for established branch networks.

The Rise of 'Smarter' Regulation

While strict regulation historically presents a high barrier for new entrants into the UK financial services sector, the government is actively fostering competition. Initiatives like the FCA's 'Innovate' program and the broader push for a 'smarter' regulatory framework, alongside support for emerging financial technologies, could gradually lower some barriers for specialized FinTech firms over the long term. However, the comprehensive compliance burden, including meeting stringent capital requirements and consumer protection standards, remains substantial. For instance, the cost of securing a UK banking license and establishing robust regulatory reporting frameworks can easily run into millions, a significant hurdle for any aspiring new player.

- The FCA reported over 2,000 firms engaged with its 'Innovate' services by 2024, signaling regulatory support for new models.

- Despite innovation efforts, the average cost of regulatory compliance for a mid-sized UK bank can exceed £50 million annually.

- The Digital Markets, Competition and Consumers Act 2024 aims to empower regulators to promote competition, potentially aiding smaller entrants.

- New banking license applications in the UK still face rigorous scrutiny, with only a few full licenses granted each year.

Banking's High Walls: New Entrants Face Steep Climb

The threat of new entrants for Lloyds Banking Group remains relatively low due to significant regulatory hurdles, high capital requirements, and the substantial costs of establishing brand trust and extensive distribution channels. While FinTech innovation is encouraged, the comprehensive compliance burden and need for significant investment, often millions for a UK banking license, deter most potential new players. Established banks benefit from deeply ingrained customer loyalty and operational efficiencies, making it challenging for newcomers to gain significant market share without substantial capital and time.

| Barrier Type | Impact on New Entrants | 2024 Data Point | Lloyds' Advantage | New Entrant Challenge |

|---|---|---|---|---|

| Regulatory & Capital | High Compliance Burden | Basel III capital requirements are stringent. | Established regulatory frameworks. | Millions for licensing & compliance. |

| Brand & Trust | Customer Acquisition Difficulty | Lloyds serves over 26 million customers. | Decades of established trust. | Building credibility from scratch. |

| Economies of Scale | Cost & Price Competition | Lloyds' Q1 2024 cost-to-income ratio: 49.6%. | Efficient operations, diverse products. | Higher per-customer costs initially. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Lloyds Banking Group is built upon a robust foundation of data, incorporating insights from their annual reports, financial statements, and investor relations disclosures. We also leverage industry-specific reports from leading market research firms and analyses from financial data providers like Bloomberg and S&P Capital IQ to ensure a comprehensive understanding of the competitive landscape.