IDFC First Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

IDFC First Bank Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

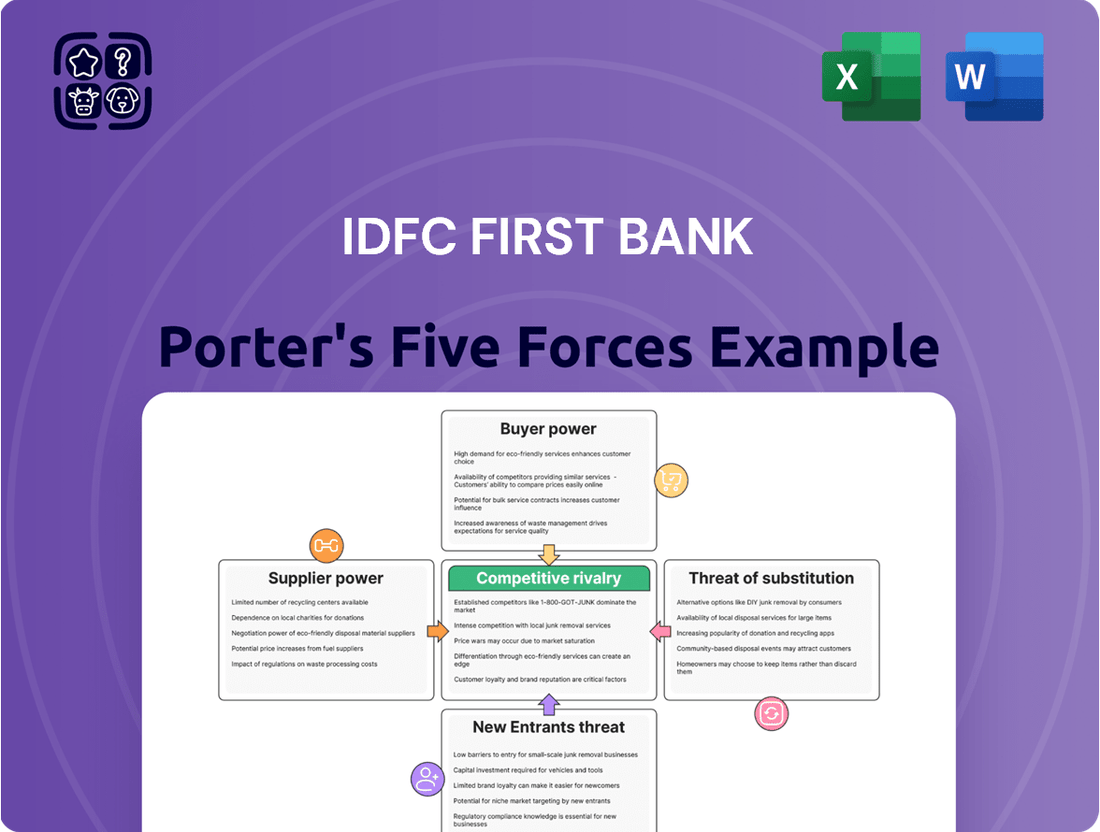

IDFC First Bank navigates a competitive landscape shaped by moderate buyer power and the significant threat of substitute products like fintech solutions. The bargaining power of suppliers, while present, is generally less impactful in the banking sector. However, the intense rivalry among existing players and the looming threat of new entrants demand strategic agility.

The complete report reveals the real forces shaping IDFC First Bank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Depositors as Key Suppliers

Depositors, especially retail customers, act as vital suppliers of capital for IDFC First Bank. The bank's success in attracting and keeping stable, low-cost deposits, like those in Current and Savings Accounts (CASA), directly influences its funding expenses and overall profitability.

For the fiscal year ending March 31, 2025, IDFC First Bank reported a significant 25.2% year-on-year increase in customer deposits, reaching ₹2,42,543 crore. This growth is particularly strong given that retail deposits made up 79% of the total, underscoring the bank's reliance on this key supplier group.

Technology and Infrastructure Providers

Technology vendors supplying core banking, digital platforms, and cybersecurity are crucial for IDFC First Bank. Their reliability directly impacts the bank's operational efficiency and customer service, especially as digital banking and AI integration become more prominent in financial services.

In 2024, the global IT spending for financial services was projected to reach over $300 billion, underscoring the significant investment and reliance on technology providers. The bargaining power of these specialized suppliers is amplified by the critical nature of their solutions and the ongoing digital transformation within the banking sector.

Human Capital and Talent

Skilled human capital, encompassing IT professionals, risk managers, and customer service staff, forms a crucial supplier group for IDFC First Bank. The intense competition for talent in financial services, especially for digital and analytical roles, can significantly sway employee bargaining power. For instance, in 2023, the average salary for a data scientist in India, a key role for digital transformation, saw an increase of approximately 15-20% compared to the previous year, reflecting this competitive pressure.

Interbank Market and Wholesale Funding

While IDFC First Bank has made strides in growing its retail deposit base, the interbank market and other wholesale funding avenues still represent crucial suppliers of liquidity. The bank's strategic pivot has demonstrably lessened its dependence on costly legacy long-term borrowings.

This reduction is evident in the figures: high-cost legacy long-term borrowings fell from 4.7% to just 1.6% of total borrowings and deposits as of March 31, 2025. This significant decrease directly translates to a diminished bargaining power for these previously high-cost funding suppliers.

- Reduced Reliance on High-Cost Borrowings: Legacy long-term borrowings as a percentage of total borrowings and deposits decreased from 4.7% to 1.6% by March 31, 2025.

- Shift to Retail Deposits: Strategic focus on retail deposits strengthens the bank's funding profile and reduces dependence on wholesale markets.

- Lowered Supplier Bargaining Power: The decline in reliance on expensive wholesale funds curtails the ability of these suppliers to dictate terms.

Regulatory Bodies and Compliance Frameworks

Regulatory bodies, particularly the Reserve Bank of India (RBI), exert significant bargaining power over IDFC First Bank. They act as gatekeepers, providing essential operating licenses and defining the rules of engagement. The RBI’s directives, such as those on capital adequacy ratios and digital lending practices, directly influence how IDFC First Bank operates and the associated costs.

For instance, the RBI’s focus on strengthening the banking sector’s resilience, as seen in its pronouncements throughout 2023 and early 2024 regarding enhanced capital requirements and risk management, means IDFC First Bank must continually adapt its strategies and potentially incur higher compliance costs. This power is amplified by the potential for penalties or restrictions if compliance standards are not met.

- RBI’s influence on capital adequacy: Banks like IDFC First Bank must adhere to evolving capital requirements, impacting their lending capacity and profitability.

- Digital lending regulations: New guidelines on digital lending directly shape product development and operational models for banks.

- Compliance costs: Meeting stringent regulatory frameworks necessitates significant investment in technology, personnel, and processes.

- Strategic flexibility: Regulatory changes can limit or expand a bank's ability to pursue certain business strategies or enter new markets.

Supplier Power: Deposits, Tech, and Regulations Shape Bank's Future

The bargaining power of suppliers for IDFC First Bank is influenced by its deposit base, technology vendors, and human capital. The bank's success in attracting retail deposits, which constituted 79% of total deposits reaching ₹2,42,543 crore by March 31, 2025, demonstrates a strong position against depositors. However, specialized technology providers for critical systems and skilled personnel in areas like data science, where salaries saw a 15-20% increase in 2023, still hold considerable sway due to the essential nature of their services and the competitive talent market.

IDFC First Bank has significantly reduced its reliance on high-cost wholesale funding, with legacy long-term borrowings falling from 4.7% to 1.6% of total borrowings and deposits by March 31, 2025. This strategic shift diminishes the bargaining power of these former suppliers. Conversely, regulatory bodies like the RBI retain substantial power, dictating operational frameworks and compliance requirements, as evidenced by ongoing directives on capital adequacy and digital lending practices throughout 2023-2024.

| Supplier Group | Impact on IDFC First Bank | Bargaining Power Level |

|---|---|---|

| Retail Depositors | Primary source of stable, low-cost funding. | Moderate to Low |

| Technology Vendors | Crucial for operational efficiency and digital services. | High |

| Skilled Human Capital (e.g., Data Scientists) | Essential for digital transformation and risk management. | High |

| Wholesale Funding Markets (Legacy) | Decreased reliance reduces their influence. | Low |

| Regulatory Bodies (e.g., RBI) | Dictate operational rules, compliance, and strategic direction. | Very High |

What is included in the product

This Porter's Five Forces analysis for IDFC First Bank meticulously examines the intensity of rivalry, the bargaining power of customers and suppliers, the threat of new entrants, and the impact of substitute products within the Indian banking sector.

IDFC First Bank's Porter's Five Forces analysis acts as a pain point reliever by providing a clear, one-sheet summary of all competitive forces, perfect for quick, informed decision-making.

Customers Bargaining Power

High Customer Switching Costs for Comprehensive Services

While switching banks for basic checking accounts might be relatively simple, customers deeply integrated with IDFC First Bank's comprehensive financial offerings, such as loans, investments, and multiple linked accounts, face significant switching costs. These costs stem from inertia, the complexity of unbundling bundled services, and the sheer effort required to transfer and re-establish these financial relationships. IDFC First Bank actively cultivates these deeper relationships by focusing on personalized service and accessibility.

Increased Digital Empowerment and Information Access

Customers today are more informed than ever, thanks to the digital revolution. With just a few clicks, they can compare interest rates, fees, and product features across numerous banks and FinTech providers. This ease of access to information directly translates to increased bargaining power, as customers can readily switch to institutions offering better terms.

The proliferation of digital banking platforms and financial comparison websites has created a transparent marketplace. For instance, by mid-2024, over 70% of banking customers in India reported using digital channels for at least one banking transaction, highlighting a significant shift in consumer behavior and expectation.

IDFC First Bank's strategic investment in its digital offerings, including user-friendly mobile apps and online services, directly addresses this trend. By providing competitive digital products and clear information, the bank aims to meet customer expectations for convenience and choice, thereby managing their amplified bargaining power.

Price Sensitivity in Basic Products

For standardized banking products like savings accounts and basic loans, customers are highly price sensitive, frequently selecting institutions based on competitive interest rates or reduced fees. This means banks must constantly offer attractive terms to attract and retain customers.

The Indian banking sector is intensely competitive, compelling banks to offer appealing deposit rates to expand their customer base. For instance, in early 2024, several leading private banks were offering savings account interest rates ranging from 3% to 4%, while some smaller banks and new entrants were pushing rates closer to 5% to attract deposits.

This competitive pressure on deposit rates can significantly impact a bank's net interest margins, as the cost of funds rises. IDFC First Bank, like its peers, navigates this environment by balancing the need for competitive pricing with the imperative to maintain profitability.

Diversified Customer Base

IDFC First Bank’s broad customer base, encompassing both retail and corporate clients, naturally dilutes the bargaining power of any single customer segment. This wide reach, from individual savings accounts to substantial corporate financing, means no single customer group holds significant leverage over the bank's pricing or terms.

The bank's strategic focus on expanding its small and medium-sized enterprise (SME) lending portfolio by an ambitious 20% annually is a key driver in further diversifying its customer base. This proactive approach not only broadens the bank's market reach but also inherently weakens the collective bargaining power of its customers by spreading risk across a larger, more varied clientele.

- Retail Customers: IDFC First Bank offers a comprehensive suite of products for individual customers, including savings accounts, current accounts, fixed deposits, and various loan products.

- Corporate Clients: The bank provides tailored financial solutions to large corporations, covering areas like working capital finance, term loans, trade finance, and treasury services.

- SME Focus: A significant strategic imperative is the growth in lending to SMEs, targeting a 20% annual increase, which directly contributes to customer base diversification.

- Reduced Concentration Risk: This diversification strategy is designed to minimize reliance on any one customer segment, thereby tempering the potential for concentrated customer bargaining power.

Impact of Loyalty Programs and Customer Experience

Customer loyalty programs and a superior customer experience are powerful tools to lessen the bargaining power of customers. By creating a sticky environment and making it less appealing to switch, banks can retain their client base. In India, the banking and financial services sector actively uses these programs, often rewarding credit card usage and digital transactions. For example, in 2023, the Indian digital payments market saw significant growth, with UPI transactions alone reaching over 100 billion. This trend highlights the importance of rewarding digital engagement.

IDFC First Bank, recognizing this, places a strong emphasis on customer-centricity and digital solutions. Their strategy aims to boost customer satisfaction and foster loyalty, thereby reducing the likelihood of customers seeking alternatives. This focus is crucial in a competitive market where customer retention directly impacts profitability and market share. The bank's commitment to improving the overall customer journey is a key factor in managing this aspect of Porter's Five Forces.

- Customer Loyalty Programs: Schemes designed to reward repeat business and encourage continued engagement.

- Customer Experience: The overall perception a customer has of a company or its brand, based on all their interactions.

- Digital Payment Growth in India: A significant increase in the adoption and usage of digital payment methods, creating opportunities for loyalty-based rewards.

- Customer Retention: The ability of a company to keep its customers over a period of time, directly impacting revenue stability.

IDFC First Bank: Countering Customer Power in Digital Banking

Customers possess considerable bargaining power due to the transparency of digital platforms, allowing easy comparison of rates and fees. This is amplified by the increasing adoption of digital banking, with over 70% of Indian banking customers using digital channels by mid-2024. IDFC First Bank counters this by enhancing its digital offerings to meet customer expectations for convenience and choice.

The banking sector's intense competition, with interest rates on savings accounts ranging from 3-5% in early 2024, forces banks to offer attractive terms. IDFC First Bank must balance competitive pricing with profitability. Furthermore, the bank's diversified customer base, including a 20% annual growth target in SME lending, dilutes the power of any single customer segment.

| Factor | Impact on IDFC First Bank | Mitigation Strategy |

|---|---|---|

| Information Availability | High customer bargaining power due to easy rate comparison. | Invest in user-friendly digital platforms and transparent product information. |

| Switching Costs | Moderate for basic accounts, high for integrated services. | Cultivate deeper relationships through personalized service and bundled offerings. |

| Price Sensitivity | High for standardized products, driving competition on rates. | Offer competitive interest rates while managing net interest margins. |

| Customer Base Diversification | Dilutes individual customer power. | Expand SME lending by 20% annually to broaden market reach. |

Preview the Actual Deliverable

IDFC First Bank Porter's Five Forces Analysis

This preview showcases the comprehensive IDFC First Bank Porter's Five Forces Analysis, detailing the competitive landscape and strategic positioning of the bank. The document you see here is the exact, fully formatted analysis you'll receive immediately after purchase, providing actionable insights without any surprises.

Rivalry Among Competitors

Intense Competition from Public and Private Sector Banks

The Indian banking landscape is fiercely competitive, with a multitude of public sector banks, established private sector giants like HDFC Bank and ICICI Bank, smaller finance banks, and foreign institutions all vying for market share. This crowded field means IDFC First Bank faces constant pressure from these players, who are also actively innovating and broadening their customer bases.

Major banks such as State Bank of India (SBI), with its extensive network and substantial deposit base, and the digitally advanced HDFC Bank, often set the pace for product development and customer acquisition strategies. For instance, HDFC Bank reported a net profit of INR 14,214 crore for the fiscal year ending March 31, 2024, showcasing its strong market position.

This intense rivalry directly impacts IDFC First Bank, compelling it to continually enhance its service quality and invest in digital capabilities to stand out. The need to attract and retain customers in such a dynamic environment necessitates a focus on differentiated offerings and a superior customer experience to maintain and grow its market share.

Rise of Digital-First Banks and Fintech Companies

The banking sector is experiencing intensified competition from digital-first banks and nimble FinTech firms. These new entrants are capitalizing on technology to deliver specialized services, often at reduced operational expenses and with a superior customer journey. For instance, in 2023, FinTech funding globally reached over $100 billion, highlighting the rapid growth and investment in this space.

These disruptors are specifically targeting traditional banks by concentrating on lucrative niches such as digital payments, peer-to-peer lending platforms, and the integration of financial services into non-financial applications, known as embedded finance. This strategic focus allows them to attract customers seeking convenience and efficiency, directly challenging established players like IDFC First Bank.

Focus on Retail and SME Segments

IDFC First Bank's strategic pivot to emphasize retail and Small and Medium-sized Enterprise (SME) segments places it squarely in a fiercely competitive arena. As of March 31, 2025, approximately 82% of its loan book was concentrated in retail, rural, and SME banking, areas where numerous financial institutions actively pursue market share.

This intense competition drives aggressive marketing campaigns and rapid product development as banks strive to attract and retain customers in these lucrative, yet crowded, markets. The focus on these segments means IDFC First Bank is constantly innovating to differentiate its offerings and capture a larger piece of the pie.

Innovation in Products and Services

Banks are in a constant race to innovate, rolling out personalized financial products, AI-driven chatbots, and cutting-edge digital banking platforms. This relentless pursuit of new offerings means that every bank, including IDFC First Bank, must significantly boost its investment in technology and customer-focused solutions to remain competitive and attract new clients.

The competitive rivalry in product and service innovation is intense. For instance, by the end of fiscal year 2024, many Indian banks reported substantial increases in their digital spending. IDFC First Bank, in particular, has been focusing on enhancing its digital capabilities to offer a seamless customer experience, which is crucial in this evolving landscape.

- Product Innovation: Banks are introducing tailored financial products, such as customized loan packages and investment portfolios, to meet diverse customer needs.

- Digital Transformation: Investment in AI-powered chatbots and advanced mobile banking applications is a key strategy for customer engagement and operational efficiency.

- Customer-Centric Solutions: The focus is shifting towards creating intuitive and user-friendly platforms that simplify banking for all customer segments.

- Technological Investment: Banks are allocating significant resources to upgrade their IT infrastructure and develop proprietary digital solutions to stay ahead.

Regulatory Environment and Consolidation

The regulatory environment, overseen by the Reserve Bank of India (RBI), plays a crucial role in shaping the competitive landscape for banks like IDFC First Bank. While these regulations are designed to ensure stability and protect depositors, they also influence market structure and competitive intensity.

RBI's guidelines, particularly those pertaining to mergers and acquisitions, can directly impact consolidation trends within the banking sector. These directives can either encourage or restrict such activities, thereby altering the number and size of players in the market.

The Indian banking sector has indeed witnessed a trend towards consolidation. For instance, the merger of HDFC Bank and Housing Development Finance Corporation (HDFC) in 2023 created a banking behemoth, significantly altering the competitive dynamics for other institutions.

- Regulatory Oversight: The RBI's stringent norms on capital adequacy, asset quality, and lending practices create a baseline for all players, influencing operational strategies and profitability.

- Merger and Acquisition Guidelines: RBI's policies on M&A can facilitate or hinder consolidation, directly impacting the competitive intensity among remaining larger entities.

- Consolidation Trend: The sector has seen significant consolidation, with the HDFC-HDFC Bank merger being a prime example, leading to fewer, larger, and potentially more dominant players.

- Impact on Competition: Consolidation often leads to increased competition among the surviving larger banks, as they vie for market share and customer loyalty in a more concentrated market.

Indian Banking: Intense Rivalry Shapes IDFC First Bank's Strategy

Competitive rivalry is a defining characteristic of the Indian banking sector, impacting IDFC First Bank significantly. The presence of large public sector banks, established private players like HDFC Bank and ICICI Bank, and emerging digital banks creates a highly saturated market. This intense competition forces IDFC First Bank to continuously innovate its product offerings and enhance its digital capabilities to attract and retain customers.

The relentless pursuit of market share by competitors, particularly in the retail and SME segments where IDFC First Bank is focusing, necessitates aggressive marketing and rapid product development. For instance, HDFC Bank's net profit of INR 14,214 crore for FY24 underscores the financial strength of major rivals. Furthermore, the rise of FinTech firms, which attracted over $100 billion in global funding in 2023, introduces agile disruptors focused on specialized services and improved customer journeys.

IDFC First Bank's strategic emphasis on retail and SME segments, which constituted approximately 82% of its loan book as of March 31, 2025, places it directly in the path of these aggressive competitors. This environment demands constant investment in technology, such as AI-powered chatbots and advanced mobile platforms, to ensure a superior customer experience and maintain relevance.

The banking sector's competitive intensity is further shaped by consolidation trends, exemplified by the 2023 merger of HDFC Bank and HDFC. This event created a larger, more dominant entity, intensifying the competitive pressure on other banks. Regulatory oversight from the RBI also plays a role, influencing market structure and the competitive dynamics among institutions.

| Key Competitor | Market Position Indicator | Recent Performance Highlight (FY24 unless specified) |

| HDFC Bank | Largest private sector bank | Net profit of INR 14,214 crore |

| ICICI Bank | Major private sector bank | Net profit of INR 12,000 crore (approx.) |

| State Bank of India (SBI) | Largest public sector bank | Significant deposit base and extensive network |

| FinTech Sector | Emerging disruptors | Global funding exceeded $100 billion in 2023 |

SSubstitutes Threaten

Digital Payment Platforms and Wallets

Digital payment platforms and mobile wallets, like those powered by UPI, present a significant threat of substitution to traditional banking payment services. These digital solutions offer unparalleled convenience and speed, often at no cost to the user, directly challenging the established methods of fund transfer and cash usage.

The rapid adoption of UPI in India underscores this disruptive potential. With transactions soaring from 12.5 billion in FY20 to an impressive 131 billion in FY24, these platforms are fundamentally altering consumer payment behavior, thereby diminishing the necessity for conventional bank-initiated transactions.

Non-Banking Financial Companies (NBFCs) and Digital Lenders

Non-Banking Financial Companies (NBFCs) and digital lenders present a significant threat of substitutes for traditional banks like IDFC First Bank. These entities often provide specialized credit products, such as quick personal loans or tailored business financing, with streamlined digital application processes that can be faster than conventional bank loans. For instance, digital lending platforms saw substantial growth, with the Indian digital lending market projected to reach $1 trillion by 2025, indicating a strong appetite for these alternative credit sources.

Direct Investment in Capital Markets

Customers increasingly opt for direct investments in capital markets, bypassing traditional bank deposits for their savings and investments. This trend is fueled by the accessibility and potential for higher returns offered by instruments like mutual funds and stocks.

The shift is evident in the growth figures; while bank deposits saw minimal expansion, mutual fund assets under management experienced a multi-fold surge. For instance, as of March 2024, India's mutual fund industry managed assets worth over ₹53 lakh crore, a stark contrast to the more modest growth in bank deposit bases for many institutions.

Peer-to-Peer (P2P) Lending Platforms

Peer-to-peer (P2P) lending platforms present a growing threat of substitution for traditional banks like IDFC First Bank. These platforms directly connect individual borrowers with lenders, bypassing conventional financial institutions. This is particularly relevant for individuals and small businesses seeking alternative credit channels.

The P2P lending market, though still developing, offers a viable substitute, especially for segments that might find traditional banking routes more cumbersome or less accessible. For instance, P2P platforms often cater to smaller loan amounts, a niche where banks might focus less attention. This direct lending model can offer competitive interest rates and faster processing times, making them an attractive alternative.

- P2P platforms bypass traditional banking infrastructure, directly linking borrowers and lenders.

- They offer an alternative for retail and small business financing, especially for those facing challenges with conventional credit access.

- The growth of P2P lending signals a shift in consumer preference towards more direct and potentially faster financing options.

- In 2023, the global P2P lending market was valued at over $100 billion, indicating its increasing significance as a substitute.

Embedded Finance Solutions

Embedded finance solutions pose a significant threat by integrating financial services directly into non-financial platforms. This means customers can access services like payments or credit within their favorite apps, bypassing traditional banking channels. For instance, a retail app might offer point-of-sale financing, reducing the need for a customer to visit IDFC First Bank for a loan.

This trend makes financial services more convenient and ubiquitous, diminishing reliance on distinct banking interfaces. By 2024, the global embedded finance market was projected to reach hundreds of billions of dollars, demonstrating its rapid growth and potential to disrupt traditional banking models.

- Reduced Customer Dependence: Embedded finance lessens customer reliance on traditional bank branches or websites for everyday transactions.

- Increased Competition: Non-financial companies entering the financial services space through partnerships create new competitive pressures.

- Shift in Customer Acquisition: Banks may find it harder to acquire new customers if financial needs are met within other platforms.

- Margin Compression: The integration of financial services into other platforms could lead to lower transaction fees and interest margins for banks.

Digital & Market Alternatives: A Substantial Threat to Banking

The threat of substitutes for IDFC First Bank is substantial, driven by the rise of digital payment platforms, NBFCs, and direct capital market investments. These alternatives offer greater convenience, specialized products, and potentially higher returns, directly challenging traditional banking services.

Digital payment solutions, particularly UPI, have fundamentally altered consumer behavior, with transactions reaching 131 billion in FY24, diminishing the need for conventional bank transfers. Similarly, digital lenders and NBFCs provide streamlined credit access, with the Indian digital lending market projected to hit $1 trillion by 2025, catering to a strong demand for alternative financing.

Customers are increasingly bypassing bank deposits for direct investments in mutual funds and stocks, which saw assets under management exceed ₹53 lakh crore by March 2024. This shift highlights a growing preference for instruments offering potentially higher returns and greater accessibility, reducing reliance on traditional banking savings products.

| Substitute Category | Key Characteristics | Impact on IDFC First Bank | Supporting Data (as of latest available) |

|---|---|---|---|

| Digital Payment Platforms (e.g., UPI) | Convenience, speed, low/no cost | Reduced transaction volumes, competition for payment services | 131 billion UPI transactions in FY24 |

| NBFCs & Digital Lenders | Specialized credit, streamlined processes | Loss of credit market share, increased competition for loans | Indian digital lending market projected to reach $1 trillion by 2025 |

| Direct Capital Market Investments | Higher potential returns, accessibility | Reduced deposit base, competition for savings and investment products | Mutual fund AUM over ₹53 lakh crore (March 2024) |

| Peer-to-Peer (P2P) Lending | Direct lending, alternative credit channels | Competition for retail and small business financing | Global P2P lending market valued at over $100 billion (2023) |

| Embedded Finance | Financial services within non-financial platforms | Reduced customer dependence on banks, harder customer acquisition | Global embedded finance market projected to reach hundreds of billions by 2024 |

Entrants Threaten

High Capital Requirements and Regulatory Hurdles

The Indian banking landscape presents a formidable challenge for new entrants due to significant capital requirements. For instance, the Reserve Bank of India (RBI) mandates substantial minimum capital, often in the billions of rupees, to secure a universal banking license, effectively deterring many potential players.

Beyond capital, navigating the intricate regulatory environment is a major hurdle. New entrants must meticulously comply with a complex array of approvals, licensing procedures, and ongoing supervisory expectations, which are designed to ensure stability and customer protection, thereby acting as a strong deterrent.

Need for Trust and Brand Recognition

The banking sector inherently relies on trust, presenting a significant hurdle for new entrants aiming to establish credibility and brand recognition. Established players like IDFC First Bank have invested considerable time and resources in building this trust and a loyal customer base, making it challenging for newcomers to swiftly capture market share.

For instance, by the end of fiscal year 2024, IDFC First Bank reported a customer base exceeding 10 million, a testament to years of relationship building and service delivery. This deep-seated trust is not easily replicated, requiring new entrants to demonstrate consistent reliability and superior customer service to even begin competing.

Established Distribution Networks and Economies of Scale

Established banks like IDFC First Bank leverage vast distribution networks, including numerous branches and ATMs, which new entrants would find incredibly costly to replicate. For instance, as of March 2024, IDFC First Bank operated over 650 branches and more than 800 ATMs, a significant physical footprint that facilitates widespread customer access and operational efficiencies.

These existing players also benefit from substantial economies of scale in their operations, from technology investments to marketing efforts. A new entrant would require massive capital infusion to build comparable infrastructure or develop disruptive digital platforms that can effectively challenge the established customer base and cost structures of incumbents.

RBI's 'On-Tap' Licensing and Small Finance Banks

While the banking sector generally presents high barriers to entry, the Reserve Bank of India's (RBI) 'on-tap' licensing for universal banks and the evolving framework for Small Finance Banks (SFBs) create a dynamic environment. This means that while formidable hurdles exist, there's a regulated avenue for new players or existing SFBs to potentially enter or expand their universal banking operations. For instance, as of early 2024, several SFBs have been actively exploring or are on the path to universal banking status, signaling a tangible, albeit regulated, threat.

The RBI's approach allows for a controlled influx of new entities that can demonstrate robust financial health, governance, and a clear business plan. This policy, in effect, moderates the threat of new entrants by ensuring that only well-prepared and compliant entities can gain a foothold. The ongoing performance and growth of existing SFBs, many of which are nearing the criteria for universal bank licenses, represent a direct potential for increased competition.

- RBI's 'On-Tap' Licensing: Continues to provide a structured pathway for new universal bank licenses, subject to stringent eligibility criteria.

- Small Finance Bank (SFB) Transition: Guidelines allow SFBs meeting specific capital and performance benchmarks to apply for universal banking licenses, increasing the potential competitive landscape.

- Controlled Entry: The regulatory framework ensures that new entrants or transitioning SFBs must meet significant prudential norms, thereby mitigating immediate, disruptive threats.

- Market Dynamics: The success and capital accumulation of SFBs in recent years, such as AU Small Finance Bank and Equitas Small Finance Bank, demonstrate their growing capacity to challenge established players once they achieve universal banking status.

Talent Acquisition and Technology Infrastructure Costs

New entrants into the banking sector face substantial hurdles in attracting and retaining top talent, especially in specialized areas like AI, cybersecurity, and digital transformation. For instance, in 2024, the demand for skilled IT professionals in the financial services industry continued to outpace supply, leading to increased salary expectations and recruitment costs for new players aiming to compete with established institutions like IDFC First Bank.

Building and maintaining a cutting-edge technology infrastructure presents another significant barrier. This includes the substantial capital required for secure cloud computing, advanced data analytics platforms, and robust cybersecurity measures to protect customer data and comply with evolving regulations. These upfront and ongoing technology investments are critical for offering competitive digital banking services.

The financial commitment for both talent acquisition and technology infrastructure can deter potential new entrants. For example, a new digital bank might need to allocate hundreds of millions of dollars in its initial years to build a competitive platform and attract the necessary expertise to challenge incumbents. This high cost of entry limits the number of viable new competitors.

- Talent Acquisition Costs: Banks must offer competitive compensation packages to attract skilled IT and data professionals, driving up operational expenses for new entrants.

- Technology Infrastructure Investment: Significant capital is required for secure, scalable, and modern digital banking platforms, including cloud services and cybersecurity.

- Digital Competitiveness: A strong technological foundation and skilled workforce are no longer optional but essential prerequisites for competing in the contemporary banking landscape.

Banking's High Barriers Deter New Entrants

The threat of new entrants for IDFC First Bank is generally considered moderate to low due to substantial barriers. High capital requirements, stringent regulatory approvals from the RBI, and the need to build significant customer trust and brand loyalty are major deterrents.

Established players like IDFC First Bank benefit from extensive branch networks, as evidenced by their over 650 branches as of March 2024, and significant economies of scale in operations and marketing, making it costly for newcomers to match their reach and efficiency.

While the RBI's 'on-tap' licensing and the potential transition of Small Finance Banks (SFBs) to universal banking status introduce some dynamism, these pathways are regulated and require entrants to meet rigorous financial and governance standards, thus controlling the pace and nature of new competition.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for IDFC First Bank is built upon a foundation of publicly available information, including the bank's annual reports, investor presentations, and filings with regulatory bodies like the Reserve Bank of India. We also incorporate insights from reputable financial news outlets and industry-specific research reports to provide a comprehensive view of the competitive landscape.