Intermediate Capital Group Plc (ICP:LSE) Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Intermediate Capital Group Plc (ICP:LSE)

Don't Miss the Bigger Picture

Intermediate Capital Group Plc (ICP:LSE) operates in a landscape shaped by moderate buyer power and significant barriers to entry, primarily due to its specialized expertise and established reputation.

The threat of substitutes is relatively low, given the unique nature of private market investments, but the bargaining power of suppliers, particularly in securing deal flow, warrants close attention.

Competitive rivalry within the asset management sector is intense, demanding continuous innovation and differentiation for ICP to maintain its market position.

The complete report reveals the real forces shaping Intermediate Capital Group Plc (ICP:LSE)’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

LP Demand and Capital Allocation

The primary suppliers for Intermediate Capital Group (ICG) are its Limited Partners (LPs), the institutional investors who commit capital to ICG's funds. These LPs, including pension funds, sovereign wealth funds, and endowments, are increasingly allocating capital to private markets. Global LP allocations to private markets are projected to reach $13.9 trillion by 2028, up from $7.3 trillion in 2022, demonstrating a robust and growing demand for private market investments.

While the supply of capital is strong, LPs are becoming more selective, scrutinizing fund managers' track records, fees, and alignment of interests. This discerning approach means that while LPs have significant bargaining power due to the abundance of choices, they also seek stable, long-term partnerships with proven managers like ICG, especially given the pursuit of diversification and enhanced returns in the current economic climate.

LP Consolidation and Influence

The increasing consolidation of pension funds, particularly in the UK, is creating larger institutional investors, often referred to as megfunds. This trend significantly bolsters their bargaining power. For instance, by mid-2024, the largest UK pension schemes are managing assets well into the tens of billions of pounds, enabling them to negotiate more favorable terms and fees with asset managers like Intermediate Capital Group.

These megfunds can leverage their substantial capital to gain easier access to private markets, which are a key focus for Intermediate Capital Group. This increased access allows them to influence the structure of investment vehicles and demand competitive fee arrangements, directly impacting the profitability and operational flexibility of firms like Intermediate Capital Group.

Pressure for Returns and Liquidity

Limited Partners (LPs) are intensifying their demands for quicker returns and easier access to their capital, particularly as a significant number of funds are nearing their scheduled wind-down periods. This heightened pressure means Intermediate Capital Group (ICG) must consistently showcase strong performance and successful divestments to secure future investments from these LPs.

For instance, in 2023, ICG reported a significant increase in distributions to its investors, reflecting its efforts to meet these LP expectations for liquidity. The firm's ability to generate attractive exit multiples on its portfolio investments is crucial for maintaining LP confidence and ensuring continued capital inflows in a competitive fundraising environment.

Preference for Established Managers

Investor appetite for direct lending and other private credit strategies remains robust, yet fundraising is increasingly consolidating around established, top-tier managers. This trend significantly curtails the bargaining power of newer or smaller alternative asset managers seeking capital.

This concentration means that investors, particularly institutional ones, are demonstrating a clear preference for managers with a long history and a demonstrated track record of success in private credit. For instance, by the end of 2023, the top 10 private debt managers globally accounted for a substantial portion of total assets under management in the sector, highlighting this preference for established players.

- Established managers benefit from investor confidence due to their proven performance.

- Newer or smaller managers face greater challenges in attracting capital, thus reducing their bargaining power.

- The trend reflects a flight to quality and a desire for predictable returns in a complex market.

Talent Acquisition and Retention

The bargaining power of suppliers, particularly concerning talent acquisition and retention, presents a significant factor for Intermediate Capital Group Plc (ICG). Highly skilled professionals in private markets are a critical resource, and intense competition for this talent can drive up compensation and benefits costs.

Escalating competition for top-tier talent within the alternative asset management sector directly impacts ICG's operational efficiency and its capacity to execute strategic initiatives effectively. This dynamic can lead to increased recruitment expenses and higher employee turnover, both of which can affect profitability.

- Talent as a Key Supplier: Skilled professionals in private equity and credit are essential for ICG's deal sourcing, due diligence, and portfolio management.

- Industry Competition: The alternative asset management industry, including firms like Apollo Global Management and Blackstone, actively competes for the same limited pool of experienced talent.

- Cost Implications: Increased demand for talent can lead to higher salary expectations, bonus structures, and retention packages, directly impacting ICG's operating expenses.

- Strategic Impact: The ability to attract and retain top performers is crucial for ICG to maintain its competitive edge and successfully deploy capital in its investment strategies.

LPs and Talent: Shaping Private Market Supplier Power

The bargaining power of suppliers for Intermediate Capital Group (ICG) is primarily influenced by its Limited Partners (LPs) and the talent it employs. LPs, comprising institutional investors like pension funds and sovereign wealth funds, are becoming more selective, demanding strong track records and favorable terms. By mid-2024, large UK pension schemes manage tens of billions, enhancing their negotiation leverage with firms like ICG.

Furthermore, the intense competition for skilled professionals in private markets significantly impacts ICG. Firms like Apollo Global Management and Blackstone vie for the same talent, driving up compensation and retention costs. This talent scarcity directly affects ICG's operational efficiency and ability to execute strategies, with higher recruitment and turnover expenses impacting profitability.

| Supplier Type | Key Characteristics | Bargaining Power Influence | Example Data/Trend |

|---|---|---|---|

| Limited Partners (LPs) | Institutional investors, increasing capital in private markets, growing selectivity. | High due to capital abundance and consolidation into larger entities (megfunds). | Global LP allocations to private markets projected to reach $13.9 trillion by 2028. |

| Talent (Skilled Professionals) | Experts in private equity and credit, crucial for deal sourcing and management. | High due to intense industry competition and limited pool of experienced individuals. | Increased demand leads to higher salary expectations and retention packages impacting operating expenses. |

What is included in the product

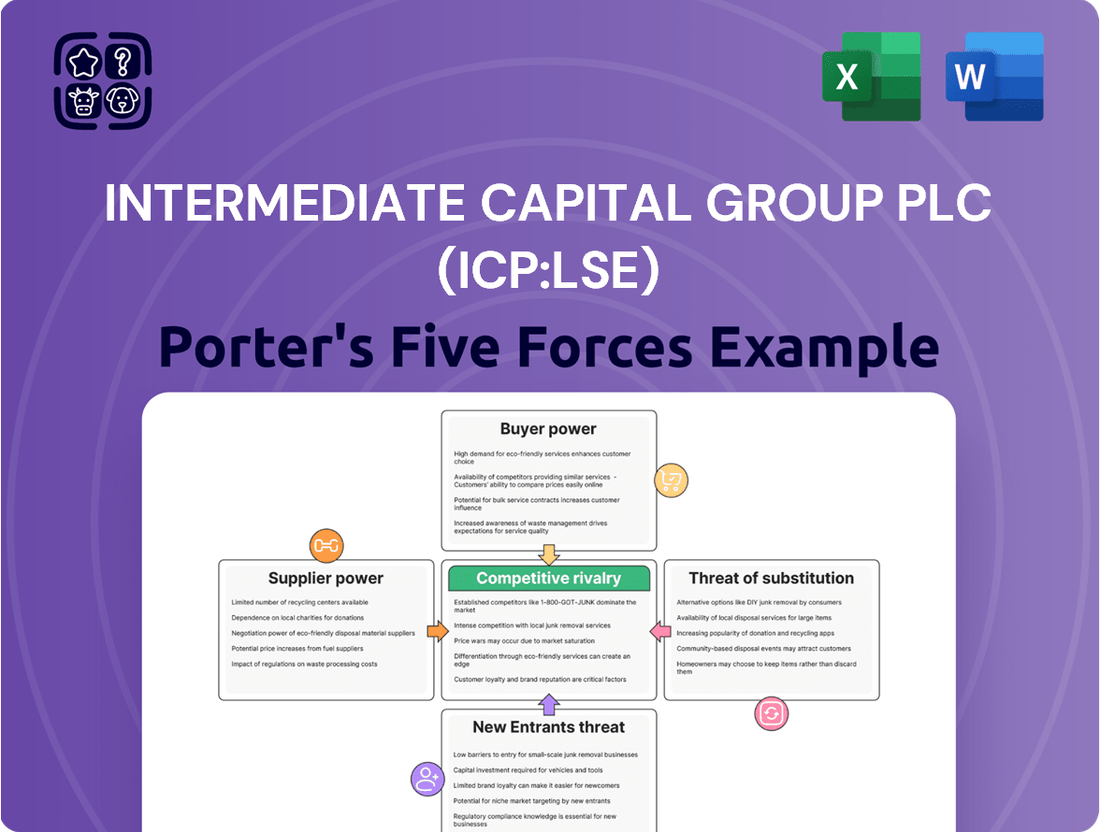

This analysis of Intermediate Capital Group Plc (ICP:LSE) dissects the competitive landscape by examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the private markets sector.

A streamlined Porter's Five Forces analysis for Intermediate Capital Group Plc (ICP:LSE) that simplifies complex competitive dynamics, offering immediate insights into profit-driving pressures.

Customers Bargaining Power

LP Demand for Diversification and Yield

Institutional investors and wealth clients, ICG's primary customers, are actively seeking diversification and higher yields. In 2024, a significant portion of these investors continued to shift capital towards alternative assets, including private debt and private equity, aiming to outperform traditional fixed-income and equity markets.

This growing demand for alternative exposures means clients have more choices for where to deploy their capital. As of mid-2024, the global alternative investment market was valued in the trillions, with private debt alone experiencing robust growth, offering clients numerous avenues to achieve their diversification and yield objectives.

Focus on Risk-Adjusted Returns

Customers are increasingly scrutinizing investment opportunities through the lens of risk-adjusted returns, demanding consistent outperformance from asset managers like Intermediate Capital Group (ICG). This focus means ICG must not only generate alpha but also do so with a keen eye on managing volatility and downside risk across its various investment strategies.

Private credit, for instance, has emerged as a particularly attractive area for institutional investors seeking robust risk-adjusted returns. In 2024, the demand for private credit solutions from pension funds and sovereign wealth funds remained exceptionally strong, as these investors looked to diversify away from traditional fixed income and capture yield premiums while managing credit risk effectively.

Demand for Specialized Strategies

As limited partners (LPs) grow more confident in private debt, they are increasingly exploring specialized areas like asset-based lending, litigation finance, and net asset value (NAV) lending. This trend requires Intermediate Capital Group (ICG) to present a diverse and appealing range of investment products to cater to these evolving client preferences.

In 2024, the demand for these niche strategies has been a significant driver in asset allocation within the private markets. For instance, the global litigation finance market alone was projected to reach over $20 billion by 2025, indicating substantial LP interest in non-traditional debt avenues.

ICG's ability to offer a comprehensive suite of solutions, from core direct lending to these specialized strategies, is crucial for retaining and attracting capital. This broad product offering directly addresses the bargaining power of customers who seek managers capable of meeting a wide spectrum of their investment objectives.

Transparency and Reporting Requirements

Customers, particularly institutional investors, are increasingly demanding greater transparency in how their assets are managed and require sophisticated risk management frameworks. This push for clarity empowers them, as they can more readily compare offerings and assess value.

For Intermediate Capital Group (ICG), meeting these heightened expectations is crucial for fostering enduring client relationships and maintaining a strong reputation for trust. The asset management landscape in 2024 and beyond emphasizes clear communication and robust risk oversight.

- Enhanced Reporting: Clients expect detailed, regular reports on portfolio performance, underlying assets, and fee structures.

- Risk Management Scrutiny: Investors are closely examining the risk management processes and stress-testing capabilities of asset managers.

- Data-Driven Insights: The ability to provide data-backed justifications for investment decisions and risk mitigation strategies is paramount.

- Regulatory Compliance: Transparency requirements often align with evolving regulatory landscapes, making adherence a competitive advantage.

Access to New Client Channels

Intermediate Capital Group (ICG) is enhancing its client reach, which could influence customer bargaining power. By launching new wealth-focused evergreen strategies in the US, ICG is tapping into a broader client base. This expansion means more diverse demands and varied access points for these clients.

ICG's strategic focus on attracting new institutional clients globally is a significant growth driver. As the firm broadens its client franchise, it also potentially increases the number of alternative investment providers available to these clients. This wider selection can empower clients, giving them more options and thus greater bargaining leverage.

- Expanded Client Base: ICG's move into wealth-focused evergreen strategies in the US broadens its customer segments.

- Global Institutional Reach: Attracting new institutional clients worldwide diversifies the investor pool.

- Increased Alternatives: A larger client base may lead to more clients seeking diverse investment avenues, potentially with other managers.

Client Power: Navigating a Competitive Alternative Investment Landscape

Customers, particularly institutional investors, have significant bargaining power due to the increasing availability of alternative investment options. In 2024, the global alternative investment market, valued in the trillions, offered a wide array of choices for yield and diversification, empowering clients to demand superior risk-adjusted returns from asset managers like ICG.

Clients are also scrutinizing fees and demanding greater transparency in reporting and risk management, allowing them to compare providers more effectively. This heightened scrutiny means ICG must consistently demonstrate value and robust oversight to retain and attract capital.

ICG's expansion into new client segments, such as the US wealth market, while broadening its global institutional reach, further amplifies customer choice. As more clients gain access to a wider range of managers and strategies, their ability to negotiate terms and demand performance increases.

| Customer Demand Driver | 2024 Market Trend | Impact on ICG |

|---|---|---|

| Diversification & Yield Seeking | Shift towards alternatives, private debt growth | Increased client options, pressure on ICG to outperform |

| Transparency & Reporting | Demand for detailed performance, risk, and fee disclosures | ICG must provide enhanced reporting and clear communication |

| Risk-Adjusted Returns | Focus on managing volatility and downside risk | ICG needs to demonstrate strong risk management capabilities |

| Product Specialization | Interest in niche strategies like litigation finance | ICG must offer a diverse and appealing product suite |

Same Document Delivered

Intermediate Capital Group Plc (ICP:LSE) Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis for Intermediate Capital Group Plc (ICP:LSE), detailing the competitive landscape including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry within the private equity and asset management sectors. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. This analysis provides actionable insights into the strategic positioning of ICP and the key factors influencing its profitability and market dynamics.

Rivalry Among Competitors

Intense Competition in Private Markets

The private markets, encompassing private credit and private equity, are witnessing a surge in competition, fueled by substantial growth in assets under management. This escalating rivalry is translating into more favorable terms for borrowers, such as compressed pricing and relaxed covenant structures, which can ultimately affect investor returns.

Growth of Private Credit and Equity

The private credit market has experienced explosive growth, nearly a tenfold increase to an estimated $1.5 trillion in 2024. This rapid expansion, with projections reaching $3.5 trillion by 2028, underscores a significantly more competitive landscape for firms like Intermediate Capital Group.

This burgeoning private credit sector directly intensifies competition by attracting a wider array of lenders and investors, all vying for deal flow and attractive risk-adjusted returns. Furthermore, the uptick in private equity dealmaking observed in 2024 adds another layer of competitive pressure, as both private credit and private equity firms often compete for the same investment opportunities.

Consolidation and Scale Advantages

The alternative asset management sector is seeing a significant trend towards consolidation. Major players are expanding their fund sizes, which naturally benefits established firms like Intermediate Capital Group (ICG) that already have the infrastructure and track record to manage larger pools of capital. This creates a competitive advantage, as their scale and incumbency make them more attractive to institutional investors seeking to allocate substantial amounts.

This consolidation makes it increasingly challenging for smaller, less established managers to gain traction and compete effectively for investor mandates. For instance, as of early 2024, many private equity and credit funds have seen record fundraising rounds, with the largest managers often securing the lion's share of commitments. ICG's ability to raise and deploy significant capital, as evidenced by its €20.4 billion of new capital raised in 2023, positions it well within this consolidating landscape.

Differentiation Through Strategy and Performance

In today's competitive asset management arena, differentiation is paramount. Intermediate Capital Group (ICG) stands out by focusing on distinct strategies and delivering robust performance. This approach is crucial for attracting and retaining investor capital in a crowded market.

ICG's success is built on a foundation of strategic diversification, particularly in areas like European direct lending and GP-led secondaries. These flagship strategies are designed to capture specific investor needs and market opportunities.

- Strategic Focus: ICG's emphasis on European direct lending and GP-led secondaries provides clear differentiation.

- Performance Metrics: Superior performance in these areas is key to attracting and retaining investor capital.

- Diversification Advantage: A diversified strategy across different asset classes and geographies helps mitigate risk and capture broader market trends.

- Investor Capital: In 2024, ICG continued to demonstrate its ability to raise significant investor capital, reflecting confidence in its strategic positioning and performance.

Traditional Lenders and Banks as Competitors

Competition between private credit providers like Intermediate Capital Group (ICG) and traditional banks has heated up significantly, making it a more borrower-friendly market. Banks are increasingly looking to collaborate with private credit funds, which blurs the lines between these entities and adds layers of complexity to the competitive environment.

This dynamic means borrowers have more options than ever before. For instance, in 2024, many mid-market companies that might have previously relied solely on bank loans are now actively exploring private credit solutions for their financing needs, attracted by potentially more flexible terms and faster execution.

- Increased Competition: Traditional banks are facing more direct competition from private credit funds, forcing them to adapt their offerings and pricing.

- Partnership Opportunities: Banks are actively seeking partnerships with private credit lenders, creating new avenues for deal origination and distribution.

- Borrower Advantage: The intensified competition benefits borrowers by providing greater choice and potentially more favorable financing terms.

- Market Evolution: The financial landscape is evolving, with private credit playing an increasingly prominent role alongside traditional banking services.

Private Credit: Intense Competition Drives Borrower Advantages

The competitive rivalry within the private markets, particularly private credit, is fierce, driven by substantial growth in assets under management, reaching an estimated $1.5 trillion in 2024. This intense competition benefits borrowers through compressed pricing and relaxed covenants, potentially impacting investor returns.

Intermediate Capital Group (ICG) navigates this landscape by focusing on distinct strategies like European direct lending and GP-led secondaries, aiming for superior performance to attract and retain capital. The consolidation trend in alternative asset management further amplifies rivalry, favoring established players like ICG with significant capital-raising capabilities, as demonstrated by its €20.4 billion raised in 2023.

Traditional banks are also increasingly competing with private credit funds, leading to a more borrower-friendly market where mid-market companies are exploring private credit for flexible financing. This dynamic blurs the lines between banks and private credit, creating new partnership opportunities and intensifying overall competition.

| Metric | 2023 Data (ICG) | 2024 Trend (Market) | Impact on Rivalry |

|---|---|---|---|

| New Capital Raised | €20.4 billion | Record fundraising rounds for large managers | Favors established players, intensifies competition for smaller firms |

| Private Credit Market Size | ~$1.5 trillion (est.) | Projected to reach $3.5 trillion by 2028 | Increased number of lenders, greater borrower choice |

| Deal Flow Competition | High | High, with PE and Credit firms vying for opportunities | Leads to compressed pricing and relaxed covenants for borrowers |

SSubstitutes Threaten

Traditional Bank Lending

Traditional bank lending continues to serve as a substitute for private debt offerings by firms like Intermediate Capital Group (ICG). While private credit has captured significant market share, partly due to stricter bank lending standards and its own advantages in speed, certainty, and flexibility, the competitive landscape is evolving. The reopening and robust appetite seen in the broadly syndicated loan (BSL) markets in 2024, with significant deal volumes returning, directly increases the competitive pressure on private debt providers.

Public Market Financing (Bonds & IPOs)

Companies can turn to public markets for funding, like issuing bonds or going public through an IPO, as substitutes for private equity or private debt. This offers an alternative capital raising avenue, potentially impacting the reliance on private financing sources.

While the pace of IPOs in 2024 has been somewhat subdued compared to prior years, the overall economic outlook suggests a potential rebound in public market activity. For instance, in the first half of 2024, global IPO volumes saw a notable increase compared to the same period in 2023, indicating a growing appetite for public listings.

Internal Corporate Financing

Larger, established companies often possess robust internal cash flow, allowing them to self-finance projects and reduce their dependence on external capital providers like Intermediate Capital Group (ICG). For instance, in 2024, many FTSE 100 companies reported strong free cash flow generation, enabling them to fund growth initiatives internally rather than seeking private debt or equity. This internal financing capability serves as a significant substitute, diminishing the need for ICG's specialized financing solutions.

Alternative Investment Structures

The rise of alternative investment structures like evergreen funds and retail-focused products presents a significant threat of substitutes for Intermediate Capital Group (ICG). These evolving vehicles can attract capital that might otherwise flow into ICG's traditional closed-end private funds, thereby broadening the competitive landscape.

For instance, the global alternative investment market reached an estimated $13.4 trillion in assets under management by the end of 2023, with projections indicating continued growth. This expansion means more capital is available through diverse structures.

These new structures offer different liquidity profiles and accessibility, potentially appealing to a wider range of investors than traditional private equity or debt funds. This diversification of investment options means ICG faces competition not just from similar fund managers but from entirely different ways capital can be allocated.

- Broader Investor Base: Evergreen and retail-focused funds can tap into a wider pool of capital, including individual investors previously excluded from private markets.

- Increased Competition: The proliferation of these structures intensifies competition for deal flow and investor mandates.

- Capital Diversion: Investors may choose these more flexible or accessible alternatives over ICG's traditional offerings, diverting capital.

- Evolving Market Dynamics: The shift towards more liquid and accessible alternative products necessitates ICG's adaptation to remain competitive.

Hedge Funds and Other Liquid Alternatives

Hedge funds and other liquid alternatives present a notable threat of substitutes for Intermediate Capital Group's (ICG) private market strategies. These vehicles offer investors similar diversification and return profiles but with significantly shorter lock-up periods, making them more appealing to those wary of illiquidity. For instance, in 2024, the global hedge fund industry managed approximately $4.5 trillion in assets, demonstrating a substantial pool of capital that could be diverted from private markets.

The appeal of liquid alternatives lies in their ability to provide exposure to various asset classes and strategies without the extended commitment required by private equity or private debt funds. This flexibility allows investors to react more swiftly to changing market conditions. By 2024, the market for liquid alternatives, excluding hedge funds, was also substantial, with many investors allocating capital to strategies like liquid alternatives and registered funds that mimic private market exposures.

- Hedge Funds as Substitutes: Hedge funds offer diversification and potentially uncorrelated returns, acting as a substitute for private market investments by providing liquidity.

- Liquid Alternatives Market Size: The global hedge fund industry managed around $4.5 trillion in assets in 2024, indicating a significant alternative for investor capital.

- Investor Preference for Liquidity: Investors increasingly favor strategies with shorter lock-up periods, making liquid alternatives more attractive than traditional private market allocations.

- Reduced Illiquidity Risk: Liquid alternatives mitigate the illiquidity risk inherent in private equity and private debt, a key consideration for many asset allocators.

Capital Competition: Diverse Alternatives Threaten Private Credit

The threat of substitutes for Intermediate Capital Group (ICG) is multifaceted, encompassing traditional bank lending, public markets, internal corporate financing, and evolving alternative investment structures. While private credit has gained traction, the resurgence of the broadly syndicated loan (BSL) market in 2024, with substantial deal volumes, directly increases competition. Similarly, companies can access capital through public offerings like bonds or IPOs, a viable alternative, especially as global IPO volumes saw a notable increase in the first half of 2024 compared to 2023.

Furthermore, robust internal cash flow generation, a trend observed among many larger companies in 2024, allows for self-financing, reducing reliance on external providers like ICG. The rise of evergreen funds and retail-focused products also presents a significant substitute threat, attracting capital that might otherwise flow into traditional private funds. These structures offer greater liquidity and accessibility, competing for investor mandates and potentially diverting capital. The global alternative investment market, estimated at $13.4 trillion by the end of 2023, highlights the growing availability of capital through diverse vehicles.

Hedge funds and liquid alternatives pose another substantial threat, offering similar diversification and return profiles but with much shorter lock-up periods. The global hedge fund industry managed approximately $4.5 trillion in assets in 2024, representing a significant pool of capital that can substitute for private market investments due to their enhanced liquidity. This preference for shorter commitment periods makes these alternatives increasingly attractive to investors seeking to mitigate illiquidity risk.

| Substitute Type | Key Characteristic | 2024 Market Trend/Data Point | Impact on ICG |

|---|---|---|---|

| Traditional Bank Lending | Established, regulated financing | Reopening and robust appetite in BSL markets | Increased competitive pressure |

| Public Markets (Bonds/IPOs) | Access to broad investor base | Global IPO volumes increased H1 2024 vs H1 2023 | Alternative capital raising avenue |

| Internal Corporate Financing | Self-funding via cash flow | Strong free cash flow generation reported by FTSE 100 companies | Reduced reliance on external capital |

| Evergreen/Retail Funds | Increased liquidity & accessibility | Global Alternative Investment Market ~$13.4T (end 2023) | Capital diversion, broader competition |

| Hedge Funds/Liquid Alternatives | Shorter lock-ups, diversification | Global Hedge Fund Industry ~$4.5T (2024) | Preference for liquidity over illiquidity |

Entrants Threaten

High Capital and Experience Requirements

The alternative asset management sector, especially in private markets, presents substantial hurdles for newcomers. Significant capital is needed to establish operations and attract investors. Furthermore, Limited Partners, the institutional investors in these funds, typically favor managers with a proven history of success and the experience to weather various economic conditions.

Regulatory Scrutiny

Increasing regulatory scrutiny globally, such as the ongoing implementation of Basel III reforms, presents a significant hurdle for potential new entrants into the financial services sector. These evolving compliance requirements can translate into substantial upfront investment in technology and personnel, creating a higher barrier to entry. For instance, in 2024, financial institutions continue to adapt to stringent capital adequacy ratios and enhanced reporting obligations, which disproportionately impact smaller, newer firms lacking established operational frameworks.

Need for Origination Capabilities

The need for robust origination capabilities presents a substantial barrier for new entrants aiming to compete in the private markets landscape. Successful firms, like Intermediate Capital Group (ICG), invest heavily in cultivating extensive networks and deep relationships to source unique and attractive investment opportunities. This process is not easily replicated and requires significant time and resources, making it difficult for newcomers to establish a competitive foothold.

Brand Reputation and Client Relationships

Established firms like Intermediate Capital Group (ICG) leverage significant brand recognition and long-standing client relationships. These are vital for successfully raising capital and securing attractive investment mandates, a process that takes years to cultivate. For instance, ICG's ability to attract significant investor commitments, as demonstrated by its substantial assets under management (AUM) which stood at £77.1 billion as of December 31, 2023, is a testament to this established trust.

New entrants face a considerable hurdle in replicating this level of credibility and market presence. Building the necessary trust with both investors and companies seeking capital requires a proven track record, which is inherently absent in a new firm. This makes it difficult for them to compete for the same high-quality deal flow that ICG can readily access.

The threat of new entrants is therefore moderated by the significant barriers to entry associated with establishing a strong reputation and deep client networks in the alternative asset management industry. These factors are critical differentiators that new players struggle to overcome quickly.

- Brand Reputation: ICG's established name provides a significant advantage in attracting both capital and investment opportunities.

- Client Relationships: Deep, long-term relationships with investors and portfolio companies are hard for new entrants to replicate.

- Fundraising Barriers: New firms must overcome skepticism and demonstrate a history of successful capital raising and deployment.

- Deal Sourcing: Established firms like ICG benefit from a robust network for identifying and winning investment mandates.

Niche Opportunities for Specialised Entrants

While Intermediate Capital Group (ICG) operates in a market with significant barriers to entry, such as established reputations and extensive networks, opportunities still exist for new players in specialized areas. Niche segments within specialty finance or opportunistic credit strategies can offer a pathway for new managers to gain a foothold. These areas allow differentiation without direct confrontation with ICG's larger, more diversified offerings.

For instance, a new entrant might focus on a specific type of private debt, like venture debt for early-stage technology companies, or distressed debt in a particular geographic region. These focused strategies can attract investors looking for targeted exposure and allow new managers to build a track record. By concentrating on underserved markets, new entrants can carve out a space and gradually build scale.

- Niche Specialization: New entrants can target specific financial products or sectors where ICG may have less focus.

- Opportunistic Credit: Emerging managers can identify and capitalize on unique credit opportunities not broadly covered by larger firms.

- Lower Initial Scale: Focusing on niche areas allows new managers to operate with smaller initial capital requirements compared to broad-based private equity or credit funds.

High Barriers Protect Private Market Leaders

The threat of new entrants for Intermediate Capital Group (ICG) is significantly moderated by high barriers to entry. These include the substantial capital required to establish operations, the need for proven track records to attract Limited Partners, and the extensive networks essential for deal sourcing in private markets. Regulatory compliance, as seen with ongoing Basel III reforms in 2024, adds further complexity and cost for newcomers. ICG's established brand reputation and deep client relationships, evidenced by its £77.1 billion in assets under management as of December 31, 2023, are difficult for new firms to replicate, making it challenging to compete for high-quality investment opportunities.

| Barrier Type | Description | Impact on New Entrants | ICG Advantage |

|---|---|---|---|

| Capital Requirements | Significant upfront investment needed for infrastructure and operations. | High hurdle; new firms may struggle to raise sufficient capital. | Established fundraising capabilities and investor trust. |

| Reputation & Track Record | Investors prefer managers with a history of successful performance. | New entrants lack credibility, making it hard to attract LPs. | Proven success and long-standing client relationships. |

| Deal Sourcing Networks | Access to proprietary investment opportunities through established relationships. | New firms have limited networks, impacting deal flow quality. | Extensive global network for origination. |

| Regulatory Compliance | Increasingly stringent regulations require significant investment in technology and personnel. | Disproportionately impacts smaller, newer firms. | Established compliance infrastructure and expertise. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Intermediate Capital Group Plc (ICP:LSE) is built upon a foundation of comprehensive data, including the company's annual reports, investor presentations, and regulatory filings. We also incorporate insights from reputable financial news outlets and industry-specific market research reports to ensure a thorough understanding of the competitive landscape.