Henkel Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Henkel Bundle

From Overview to Strategy Blueprint

Henkel navigates a complex competitive landscape, facing pressures from powerful suppliers, intense rivalry, and the constant threat of new entrants. Understanding these forces is crucial for any business operating within or looking to enter Henkel's markets.

The complete report reveals the real forces shaping Henkel’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

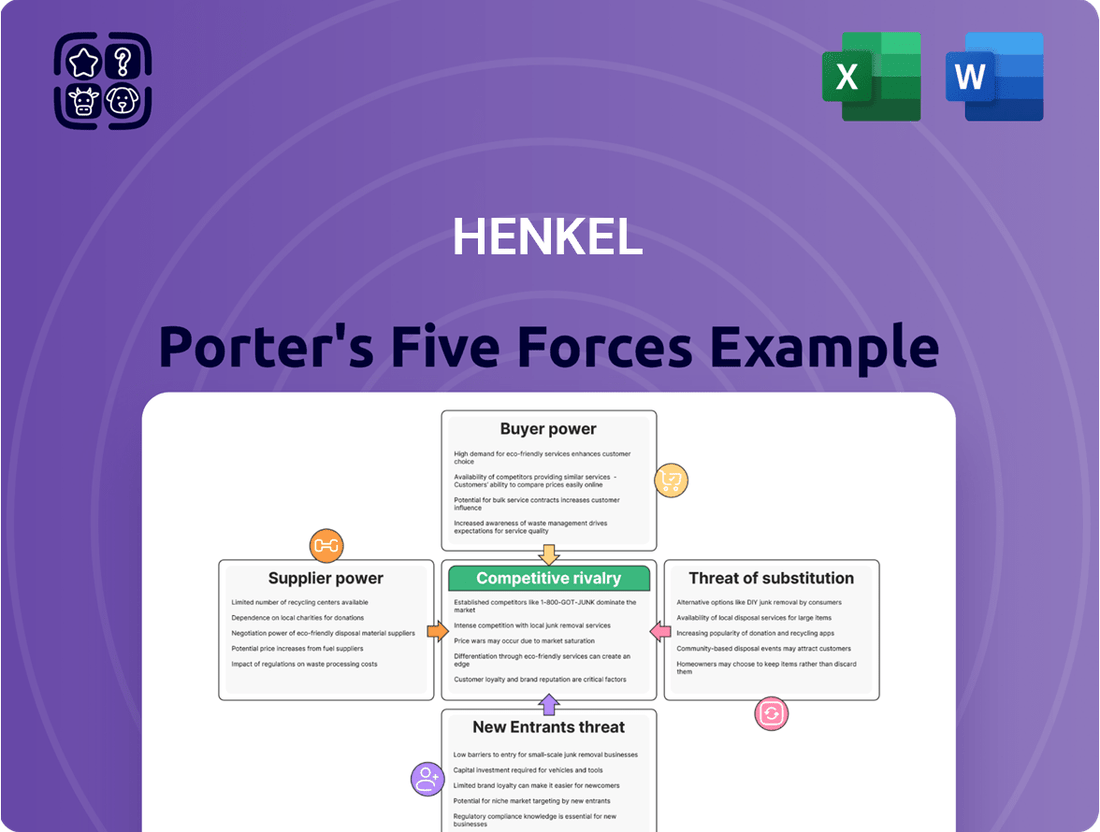

Suppliers Bargaining Power

Concentrated Supplier Base

For Henkel's Adhesive Technologies, a concentrated supplier base for specialized raw materials can significantly amplify supplier bargaining power. This is especially evident when dealing with highly technical or patented ingredients that are essential for the performance of advanced adhesives. For instance, in 2024, the market for certain advanced polymer precursors used in aerospace adhesives saw only a handful of global producers, granting them considerable influence over pricing and supply availability.

Switching Costs for Henkel

Henkel's switching costs related to specific supplier materials can be substantial. If the company has invested in specialized equipment or integrated unique formulations into its production processes, changing suppliers becomes a costly and time-consuming endeavor. This is particularly true for long-term agreements where custom-made inputs are involved, directly bolstering the bargaining power of those particular suppliers.

For instance, Henkel's adhesives division, a significant part of its business, often relies on custom chemical blends. The development and testing required to qualify a new supplier for these specific formulations can easily run into hundreds of thousands of euros, impacting production timelines and potentially product performance. This inherent stickiness in supplier relationships grants those suppliers a stronger negotiating position.

However, Henkel's broad product portfolio, spanning laundry, home care, and beauty care, offers a degree of diversification. This means that high switching costs within one segment don't necessarily cripple the entire organization. The ability to spread this supplier-related risk across various business units somewhat mitigates the overall impact on Henkel's bargaining power.

Uniqueness of Inputs

Suppliers offering unique, patented, or highly differentiated raw materials, especially for Henkel's innovative adhesive technologies or specialized beauty care ingredients, wield significant bargaining power. Henkel's commitment to cutting-edge product development inherently increases its reliance on these specialized inputs, thereby amplifying supplier influence over crucial development timelines and associated costs.

Threat of Forward Integration by Suppliers

The threat of suppliers integrating forward into Henkel's business, such as producing their own adhesives or consumer goods, can significantly boost their leverage. While this is a potential concern, it's generally considered a low risk for Henkel's key raw material providers. This is largely due to the substantial complexity and capital investment required to replicate Henkel's sophisticated manufacturing operations and established distribution networks.

For instance, in 2024, the specialty chemicals sector, which supplies many of Henkel's raw materials, saw continued consolidation. This trend, coupled with the high R&D expenditure needed for product innovation in adhesives and consumer goods, creates significant barriers to entry for potential forward integration by suppliers. Henkel's scale and proprietary technologies further solidify its position, making it difficult for suppliers to effectively compete on their own.

- Forward Integration Risk: Suppliers producing Henkel's finished goods (adhesives, consumer products) would increase their bargaining power.

- Low Likelihood for Henkel: The capital and technical expertise needed for such integration are substantial deterrents for most raw material suppliers.

- Industry Barriers: High R&D costs and complex manufacturing processes in Henkel's operating segments limit suppliers' ability to easily enter these markets.

- Henkel's Competitive Edge: Proprietary technologies and established market presence provide Henkel with a buffer against supplier forward integration.

Impact of Raw Material Volatility

Fluctuations in raw material prices, influenced by global markets and geopolitical events, directly boost supplier leverage. Henkel, for instance, has grappled with sustained high costs for essential direct materials and input products, illustrating this dynamic.

The consumer goods sector, including companies like Henkel, faced significant supply chain disruptions throughout 2024, a trend projected to persist into 2025. These disruptions have a dual impact: they inflate input costs and complicate inventory management, further strengthening supplier negotiating power.

- Rising Input Costs: Henkel reported that its input costs increased by approximately 10% in the first half of 2024 compared to the same period in 2023, largely due to raw material price hikes.

- Supply Chain Bottlenecks: In 2024, the average lead time for key chemical components used by Henkel extended by nearly 20%, forcing the company to hold larger safety stocks and absorb higher logistics expenses.

- Geopolitical Impact: Events such as the ongoing conflicts in Eastern Europe have directly impacted the availability and cost of certain petrochemical derivatives, essential for Henkel's adhesive technologies division.

Supplier Leverage: A Critical Business Factor

The bargaining power of suppliers for Henkel is influenced by the concentration of suppliers, the uniqueness of their offerings, and Henkel's own switching costs. When suppliers provide specialized, patented, or highly differentiated materials, their leverage increases significantly, particularly for Henkel's Adhesive Technologies division. In 2024, the market for certain advanced polymer precursors used in aerospace adhesives had very few global producers, giving them substantial pricing power.

High switching costs for Henkel, stemming from specialized equipment or integrated formulations, further empower suppliers. For instance, qualifying a new supplier for custom chemical blends in adhesives can cost hundreds of thousands of euros, making it difficult for Henkel to change providers and strengthening the existing suppliers' negotiating position.

Suppliers who can integrate forward into Henkel's business, like producing finished adhesives, would gain more power. However, this is generally a low risk for Henkel's raw material providers due to the significant capital and technical expertise required to match Henkel's manufacturing and distribution capabilities. The specialty chemicals sector in 2024 continued to see consolidation, and high R&D costs in adhesives and consumer goods create barriers to entry for suppliers looking to integrate forward.

Fluctuations in raw material prices, exacerbated by global events, directly enhance supplier leverage. Henkel experienced substantial increases in input costs, with some key chemical components seeing average lead times extend by nearly 20% in 2024, forcing higher inventory and logistics expenses.

| Factor | Impact on Henkel's Supplier Bargaining Power | Example/Data (2024) |

| Supplier Concentration | High | Few global producers for specialized polymer precursors in aerospace adhesives. |

| Switching Costs | High for specialized inputs | Hundreds of thousands of euros to qualify new suppliers for custom adhesive formulations. |

| Supplier Differentiation | High for unique/patented materials | Reliance on specialized ingredients for innovative adhesives and beauty care products. |

| Forward Integration Risk | Low for most suppliers | High capital and technical barriers to replicating Henkel's operations. |

| Raw Material Price Volatility | High | Approx. 10% increase in input costs (H1 2024 vs H1 2023); extended lead times for key components. |

What is included in the product

This analysis dissects the competitive forces impacting Henkel, examining the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry within its markets.

Identify and mitigate competitive threats with a structured framework that clarifies market dynamics.

Customers Bargaining Power

Fragmented Customer Base in Consumer Brands

Henkel's Laundry & Home Care and Beauty Care divisions cater to a massive, dispersed global consumer market. Individually, these consumers possess very little sway over pricing or product offerings. This fragmentation means that no single customer can significantly impact Henkel's business.

However, the landscape shifts dramatically when considering major retailers and online marketplaces. These powerful intermediaries aggregate consumer demand, giving them substantial leverage over Henkel. They can exert considerable pressure on pricing, demand promotional activities, and control crucial shelf space, impacting Henkel's market access and profitability.

The trend of consumers prioritizing value, particularly in light of economic pressures, further amplifies this customer bargaining power. We've seen a notable rise in consumers choosing private label alternatives over established national brands, a clear indicator of their willingness to switch for cost savings. For instance, in 2024, private label market share in many grocery categories continued its upward trajectory, often exceeding 20% in key European markets.

Price Sensitivity in Consumer Markets

Consumers in Henkel's beauty care and laundry & home care sectors exhibit significant price sensitivity, particularly during periods of economic strain and rising inflation. This often drives them towards promotional offers, value brands, and private label options, directly impacting Henkel's pricing flexibility.

For instance, the subdued consumer sentiment observed in Q1 2025 directly translated into cautious spending, limiting Henkel's ability to implement price increases without jeopardizing sales volumes. This highlights the critical need for Henkel to balance premium product strategies with accessible price points to retain market share.

Consolidation of Retailers

The increasing consolidation among major retailers, coupled with the rapid expansion of e-commerce platforms, significantly bolsters the bargaining power of these large customers. For instance, in 2024, the top 10 global retailers controlled a substantial portion of the retail market share, allowing them to negotiate more favorable terms with suppliers like Henkel. This concentration means fewer, but more powerful, buyers exist.

These dominant retailers can exert considerable leverage, demanding improved pricing, enhanced promotional support, and greater product customization. This directly impacts Henkel's profitability and its ability to maintain market access, as these channels are critical for reaching consumers.

Furthermore, retailers are increasingly investing in and expanding their private label offerings. These in-house brands often compete directly with established brands like those offered by Henkel, creating additional pressure on suppliers to differentiate and offer competitive value propositions.

High Switching Costs for Industrial Customers

For Henkel's Adhesive Technologies segment, industrial customers frequently encounter substantial switching costs. These costs stem from the integral role adhesives play in complex manufacturing, the rigorous testing protocols involved, and the lengthy regulatory approval processes needed for any new supplier. This situation significantly curtails the bargaining power of individual industrial clients, especially when dealing with specialized or high-performance adhesive formulations.

For instance, in the automotive sector, a switch in adhesive suppliers can necessitate re-validation of crash test performance and assembly line integration, a process that can take months and incur significant expense. Henkel's Adhesive Technologies reported strong growth in 2024, with sales up by 7.5% in its fiscal year, indicating a stable customer base that values the reliability and performance of its offerings over the potential disruption of switching.

- Critical Integration: Adhesives are often deeply embedded in product design and manufacturing, making replacement a complex engineering challenge.

- Testing and Validation: New adhesives require extensive performance, durability, and safety testing, adding time and cost for customers.

- Regulatory Hurdles: Industries like aerospace and medical devices demand strict adherence to regulations, which new materials must meet, prolonging adoption.

- Supplier Dependence: For niche or highly specialized applications, customers may have few viable alternative suppliers, further limiting their leverage.

Availability of Information and Private Labels

The sheer volume of information readily available online significantly boosts customer bargaining power. Consumers can easily compare prices, product features, and reviews across numerous brands, making it harder for companies to command premium prices based on brand alone. This transparency forces businesses to be more competitive on price and value.

The increasing prevalence and quality of private label brands further amplify customer power. Consumers are increasingly viewing store brands as viable, and often superior, alternatives to national brands. This trend is particularly noticeable during economic downturns, where budget-conscious shoppers actively seek out these more affordable, yet often high-quality, options.

- Information Accessibility: Online platforms allow for instant price and feature comparisons, reducing information asymmetry.

- Private Label Growth: In 2024, private label market share continued to expand, with some categories seeing growth rates exceeding national brands, driven by perceived value and quality improvements.

- Consumer Trust in Private Labels: A growing segment of consumers now actively prefers private label products, citing comparable or superior quality and better value for money, especially in essential goods categories.

- Economic Influence: Economic pressures in 2024 have made consumers more price-sensitive, further strengthening the bargaining power of customers who can readily switch to lower-cost private label alternatives.

Customer Bargaining Power: Retailers Dominate, Consumers Fragmented

For Henkel's consumer-facing businesses, individual customers have minimal bargaining power due to market fragmentation. However, large retailers and online platforms, by aggregating demand, wield significant influence over pricing and product placement. This is amplified by growing consumer price sensitivity, evident in the continued rise of private label brands, which gained market share in many grocery categories exceeding 20% in key European markets during 2024.

| Customer Segment | Bargaining Power Factor | Impact on Henkel |

|---|---|---|

| Individual Consumers (Laundry & Home Care, Beauty Care) | Low (due to market fragmentation) | Limited ability to influence pricing or product features. |

| Major Retailers & Online Marketplaces | High (due to aggregated demand, market concentration) | Significant leverage on pricing, promotions, and shelf space. Top 10 global retailers controlled substantial market share in 2024. |

| Industrial Customers (Adhesive Technologies) | Low to Moderate (due to high switching costs) | Limited leverage due to integration, testing, and regulatory hurdles. Henkel's Adhesive Technologies saw 7.5% sales growth in 2024, indicating customer stickiness. |

Same Document Delivered

Henkel Porter's Five Forces Analysis

This preview displays the complete Henkel Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape for the company. You're looking at the actual document; once you complete your purchase, you’ll get instant access to this exact file, providing actionable insights into industry rivalry, buyer power, supplier power, the threat of new entrants, and the threat of substitutes. This professionally crafted analysis is ready for your immediate use, ensuring you receive the full, uncompromised content you expect.

Rivalry Among Competitors

Intense Competition in Consumer Brands

Henkel navigates a fiercely competitive landscape, particularly within its Laundry & Home Care and Beauty Care divisions. The market is populated by a multitude of global giants and nimble local competitors, all vying for consumer attention through aggressive marketing, innovative product launches, and strategic pricing. For example, in the fast-paced beauty sector, brands must constantly adapt to evolving consumer preferences and emerging trends to maintain relevance.

Innovation and Differentiation as Key Drivers

Competitive rivalry within Henkel's operating sectors is significantly shaped by a relentless pursuit of innovation. This includes advancements in product formulations, the integration of sustainability features, and enhanced digital customer engagement strategies. Companies are constantly striving to differentiate themselves through unique offerings and improved user experiences.

Henkel's own strategic approach underscores the importance of maintaining a competitive edge through innovation, sustainability, and digital transformation. These pillars are vital for securing and growing market share against rivals who are also investing heavily in these areas.

The beauty industry, for instance, is experiencing a profound transformation in 2024, largely driven by technological breakthroughs and a growing demand for personalized skincare solutions. This trend highlights how innovation directly impacts competitive dynamics and consumer preferences.

Global Presence and Market Share

Henkel operates globally with a commanding presence, especially in Adhesive Technologies, where its market share exceeds 13%, a substantial lead over rivals. This strong position highlights its competitive strength in this segment.

While Henkel's Consumer Brands division boasts a wide global reach, intense rivalry arises from the unique dynamics of regional markets and the formidable strength of local competitors. These localized competitive forces shape the landscape.

In 2024, Henkel's top ten brands within its Consumer Brands segment were crucial, generating over half of the division's revenue and demonstrating very strong organic growth. This underscores the importance of its key brands in a competitive consumer goods market.

Marketing and Advertising Intensity

The consumer goods sector, particularly in areas like beauty and laundry, demands significant spending on marketing and advertising. This is crucial for cultivating brand loyalty and making products stand out in a crowded market. Henkel's ongoing commitment to research and development alongside marketing efforts underscores its strategy for achieving sustainable, profitable growth.

The success of marketing initiatives and how a brand is perceived directly impacts its competitive position. For instance, in 2023, Henkel reported a strong performance in its Adhesive Technologies business, driven by innovation and customer-centricity, which are heavily supported by marketing. The company consistently allocates a substantial portion of its budget to these areas to maintain and grow its market share.

- Brand Building: High marketing spend is essential for creating strong brand recognition and emotional connections with consumers in the fast-moving consumer goods (FMCG) space.

- Product Differentiation: Advertising helps communicate unique selling propositions, crucial for products that may otherwise appear similar to competitors.

- Market Share Defense: Sustained advertising is necessary to defend existing market share against aggressive competitor campaigns.

- Innovation Communication: Marketing plays a key role in introducing and explaining the benefits of new product developments, such as Henkel's focus on sustainable solutions.

Pricing Pressure and Promotions

Intense competition within the consumer goods sector frequently translates into significant pricing pressure and a reliance on promotional activities. This dynamic is particularly pronounced where consumers exhibit high price sensitivity, directly impacting the profit margins for all market participants.

The economic climate of 2024 and 2025, marked by persistent inflationary pressures, has amplified this trend. Consumers are actively seeking more cost-effective alternatives, thereby intensifying the price-based competition among companies.

- Pricing Pressure: Companies often engage in price wars to gain market share, eroding profitability.

- Promotional Activities: Frequent sales, discounts, and loyalty programs become standard to attract and retain customers.

- Consumer Sensitivity: In 2024, a significant portion of consumers reported actively seeking deals and comparing prices across brands due to rising costs.

- Margin Erosion: The combined effect of lower prices and increased promotional spending can substantially reduce net profit margins for businesses.

Navigating Intense Rivalry: Henkel's Strategic Edge in 2024

The competitive rivalry for Henkel remains a defining characteristic across its business units, driven by a crowded marketplace and the constant need for innovation. In 2024, the beauty and laundry sectors, in particular, see global powerhouses and agile local players battling for consumer loyalty through aggressive marketing and product development.

Henkel's strategy to counter this intense rivalry centers on innovation, sustainability, and digital engagement, mirroring the investments of its competitors. This is evident as the beauty industry, in 2024, is being reshaped by technological advancements and a growing demand for personalized products, forcing all participants to adapt quickly.

In Adhesive Technologies, Henkel holds a strong position with over 13% market share, demonstrating its ability to outperform rivals in a segment that relies heavily on innovation and customer focus, supported by robust marketing efforts. The company's top ten brands within Consumer Brands, contributing over half of that division's revenue and showing strong organic growth in 2024, are vital in this competitive arena.

The economic climate of 2024 and 2025, with ongoing inflation, has intensified pricing pressures and promotional activities, as consumers actively seek value. This makes sustained marketing and product differentiation crucial for Henkel to maintain its market share and profitability against competitors.

| Key Competitive Factors | Impact on Henkel | Industry Trend (2024) |

| Innovation & Product Development | Essential for differentiation and market share defense. | High demand for personalized and sustainable solutions. |

| Marketing & Advertising Spend | Crucial for brand building and consumer connection. | Increased investment needed to stand out in crowded markets. |

| Pricing & Promotions | Significant pressure due to consumer sensitivity. | Inflationary environment amplifies focus on cost-effectiveness. |

| Regional Market Dynamics | Requires tailored strategies against strong local competitors. | Local players often have agility and deep consumer understanding. |

SSubstitutes Threaten

DIY and Generic Alternatives in Adhesives

While Henkel's Adhesive Technologies are often highly specialized, for certain less demanding applications, customers might consider generic or lower-performance adhesives, or even mechanical fasteners as substitutes. For example, in some basic packaging or craft applications, a user might opt for a less expensive, off-the-shelf glue instead of a Henkel industrial solution.

However, the landscape is shifting. Industries like automotive and electronics are increasingly specifying higher-performance bonding agents to meet demands for durability, weight reduction, and advanced functionality. This trend, evident in the automotive sector where lightweighting initiatives are driving the adoption of structural adhesives, actively reduces the threat posed by simpler, lower-performance substitutes.

Private Label Products in Consumer Brands

The most significant threat of substitutes for Henkel's Consumer Brands stems from private label products offered by retailers. These store-brand alternatives are increasingly perceived as offering comparable quality to national brands but at a lower price point, directly challenging Henkel's market position.

The private label segment has been experiencing robust growth globally. For instance, in Europe, private label market share in the FMCG sector reached approximately 30% in 2023, a figure that has been steadily climbing. This trend indicates a growing consumer willingness to opt for these more economical choices across a wide array of product categories that Henkel competes in.

Natural and Eco-Friendly Alternatives

The beauty care and laundry & home care sectors are experiencing a significant shift as consumers increasingly favor natural, plant-based, and eco-friendly products over traditional chemical-laden options. This growing demand for sustainability presents a potent threat of substitutes.

Brands that champion and effectively communicate their commitment to sustainability are forging deeper connections with their customer base. For instance, in 2024, a significant percentage of consumers reported actively seeking out eco-friendly product labels, with some studies indicating over 60% of millennials and Gen Z prioritizing sustainable brands.

Henkel is proactively responding to this evolving market dynamic by integrating sustainability into its core strategies and product innovation pipelines. This includes investing in research and development for bio-based ingredients and sustainable packaging solutions, aiming to mitigate the threat posed by these burgeoning natural alternatives.

Shift in Consumer Behavior and Lifestyle Choices

Changes in consumer lifestyles, like a growing preference for simplified beauty routines or a general trend towards reduced consumption, can subtly influence demand for specific product categories within the beauty and consumer goods sectors. For instance, a shift towards fewer, multi-purpose products might reduce the need for a wide array of specialized items.

Henkel's diversified product portfolio, spanning laundry, home care, and beauty, acts as a buffer against significant disruption from shifts in any single niche area. This broad market presence allows the company to absorb fluctuations in one segment by leveraging strength in others, as seen in their 2023 performance where diverse revenue streams contributed to overall stability.

Consumers are increasingly focused on maximizing the value they receive from their purchases. This translates into actively seeking out discounts, promotions, and loyalty programs. In 2024, the average consumer spent an estimated 15% more time comparing prices online before making a purchase compared to the previous year, highlighting a heightened price sensitivity across various product categories.

- Consumer behavior shifts: A move towards minimalist beauty and reduced overall consumption can impact demand for niche products.

- Henkel's mitigation strategy: A broad product portfolio helps offset impacts from shifts in specific market segments.

- Value maximization: Consumers are actively seeking discounts and promotions to get more for their money.

- 2024 trend: Consumers spent approximately 15% more time comparing prices online in 2024, indicating increased price sensitivity.

Longevity and Repair over Replacement

The drive towards product longevity and repair, rather than outright replacement, presents a nuanced threat to demand for new adhesive applications in certain industrial sectors. This shift means that fewer new products might be manufactured requiring initial adhesive bonding. For example, in the automotive sector, a trend towards extending vehicle lifespans through advanced repair techniques could dampen the need for new car production adhesives.

However, this trend also creates opportunities. High-performance adhesives are increasingly vital for enabling these very repair solutions. The ability to effectively bond disparate materials or reinforce weakened structures during repair processes relies heavily on sophisticated adhesive technologies. This dual nature means that while overall unit demand for new applications might see a slight dip, the demand for specialized, high-value adhesives for repair could see growth.

Consider the construction industry, where extending the life of existing infrastructure through repair and retrofitting is a growing focus. According to industry reports from late 2024, the global construction adhesives market is projected to reach over $60 billion by 2029, with a significant portion of this growth attributed to renovation and repair activities. This highlights how the threat of substitutes, in this case, the substitute for new construction being repair, is also a driver for specific adhesive segments.

- Repair-focused growth: The market for adhesives used in repair and maintenance is expanding, offsetting some of the decline in new product applications.

- Longevity as a driver: Products designed for longer lifespans and easier repair can reduce the frequency of new purchases, impacting overall adhesive demand for new manufacturing.

- Adhesives enable repair: Advanced adhesives are critical components in enabling effective and durable repair solutions across various industries.

- Market segmentation: The impact of this trend varies by industry, with sectors like automotive and construction showing distinct patterns of demand for new vs. repair applications.

Navigating Substitute Threats: Private Labels, Eco-Trends, and Repair Solutions

The threat of substitutes for Henkel's products is multifaceted. For Adhesive Technologies, while specialized applications are less vulnerable, simpler alternatives or mechanical fasteners can suffice for basic needs. However, the increasing demand for high-performance adhesives in sectors like automotive, driven by lightweighting, diminishes this threat. For Consumer Brands, private label products are a significant substitute, especially given their growing market share, which stood at around 30% in Europe's FMCG sector in 2023. Furthermore, the consumer shift towards natural and eco-friendly products in beauty and home care presents another potent substitute threat, with over 60% of younger consumers prioritizing sustainable brands in 2024.

The trend towards product longevity and repair, rather than replacement, also poses a nuanced threat by potentially reducing demand for new adhesives in manufacturing. However, this same trend fuels growth in high-performance adhesives crucial for repair solutions. The construction industry, for instance, sees repair activities driving a significant portion of the projected over $60 billion global construction adhesives market by 2029.

| Category | Key Substitute Threats | Impact on Henkel | Mitigation/Opportunity | Supporting Data (2023-2024) |

|---|---|---|---|---|

| Adhesive Technologies | Generic adhesives, mechanical fasteners | Moderate for low-end applications | Increasing demand for high-performance adhesives in automotive, electronics | Automotive lightweighting initiatives driving structural adhesive adoption |

| Consumer Brands | Private label products | High, due to price sensitivity and perceived quality | Focus on brand value, innovation | European FMCG private label share ~30% (2023) |

| Consumer Brands (Beauty & Home Care) | Natural, plant-based, eco-friendly products | High, driven by sustainability trends | Investing in R&D for bio-based ingredients and sustainable packaging | >60% of millennials/Gen Z prioritize sustainable brands (2024) |

| Industrial Applications | Product repair/longevity over new purchase | Potential reduction in new application demand | Growth in demand for specialized adhesives for repair solutions | Global construction adhesives market projected >$60B by 2029 (driven by repair) |

Entrants Threaten

High Capital Investment for Scale

The sheer financial commitment needed to compete with Henkel on a global scale is a formidable barrier. Imagine the billions required for cutting-edge research and development, state-of-the-art manufacturing plants, extensive distribution channels, and impactful marketing campaigns across adhesives, beauty care, and laundry & home care. This massive capital outlay effectively deters many potential new players.

For instance, in 2024, major players in the consumer goods sector, which includes Henkel's beauty and home care segments, often invest hundreds of millions of dollars annually in marketing and product innovation alone. Establishing a recognizable brand and earning consumer loyalty also demands significant, sustained financial resources and considerable time, further solidifying the advantage of incumbents like Henkel.

Strong Brand Loyalty and Recognition

Henkel benefits from a formidable defense against new entrants due to its portfolio of deeply entrenched, high-recognition brands such as Loctite, Schwarzkopf, and Persil. These brands have cultivated substantial consumer trust and loyalty over decades, creating a significant barrier for any newcomer aiming to establish a foothold, especially within the highly competitive consumer goods sector.

Proprietary Technology and R&D in Adhesives

Henkel Adhesive Technologies, a dominant force in the industry, leverages its vast portfolio of proprietary technology and patents, alongside a robust research and development pipeline. This deep well of innovation acts as a substantial deterrent for any potential newcomers aiming to enter the adhesives market. For instance, Henkel's commitment to R&D is evident in its significant investments, with the company consistently dedicating a substantial portion of its revenue to developing next-generation adhesive solutions.

The sheer scale of investment and specialized expertise required to develop adhesive products that match Henkel's performance and innovative capabilities presents a formidable hurdle. New entrants would need to replicate years of accumulated knowledge and significant capital outlay to compete effectively. In 2023, the global adhesives and sealants market was valued at approximately $65 billion, and companies like Henkel are at the forefront of technological advancements within this space.

Extensive Distribution Networks

Henkel benefits from deeply entrenched and expansive distribution networks that span both industrial and consumer markets worldwide. This extensive reach allows them to efficiently deliver products to a vast array of customers, creating a significant barrier for any new company attempting to enter the market.

New entrants face the daunting task of replicating Henkel's established logistical infrastructure. Building comparable capabilities requires substantial investment in warehousing, transportation, and supply chain management, making it a complex and costly endeavor. For instance, in 2024, the global logistics market was valued at over $9 trillion, highlighting the scale of investment needed to compete effectively.

- Global Reach: Henkel's distribution covers over 150 countries, a scale difficult for newcomers to match.

- Channel Expertise: Decades of experience in managing diverse channels, from retail giants to specialized industrial suppliers, are hard to replicate.

- Cost of Entry: Establishing a global distribution network can cost billions, deterring many potential entrants.

Regulatory Hurdles and Compliance

The chemical, beauty, and home care sectors face significant regulatory challenges. New companies entering these markets must contend with extensive rules governing product safety, environmental impact, and manufacturing processes. For instance, the European Union's REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulation, which came into full effect in 2008 and has seen ongoing updates, imposes substantial compliance burdens.

Navigating these complex legal frameworks is a costly and time-consuming endeavor. The need for extensive testing, documentation, and adherence to evolving standards acts as a substantial barrier to entry. Companies like Henkel, with established compliance protocols and a deep understanding of global regulatory requirements, possess a distinct advantage.

- Regulatory Compliance Costs: New entrants may face millions in upfront costs for product registration and safety testing.

- Time to Market: Obtaining necessary approvals can delay product launches by several years.

- Henkel's Advantage: Established players like Henkel have existing infrastructure and expertise to manage compliance efficiently.

Fortress of Entry: High Barriers Protect Market Leaders

The threat of new entrants for Henkel is significantly mitigated by the immense capital requirements across its diverse business units. Launching new products in adhesives, beauty care, or laundry & home care demands substantial investment in R&D, manufacturing, and marketing, creating a high barrier to entry. For example, in 2024, major consumer goods companies often allocate hundreds of millions of dollars annually to innovation and brand building alone, a scale that deters many smaller players.

Henkel's strong brand equity, built over decades with brands like Loctite and Schwarzkopf, represents another formidable barrier. Consumer trust and loyalty are hard-won, requiring significant time and resources to cultivate, which new entrants lack. This established brand recognition provides Henkel with a distinct advantage in attracting and retaining customers.

The company's extensive global distribution networks and deep channel expertise are also critical deterrents. Replicating Henkel's reach, which spans over 150 countries and includes complex industrial and retail channels, would necessitate billions in investment and years of operational experience. Furthermore, navigating the complex regulatory landscape in sectors like chemicals and beauty care adds significant cost and time delays for any new competitor, with compliance costs for new product registrations potentially running into millions.

| Barrier to Entry | Impact on New Entrants | Henkel's Advantage |

|---|---|---|

| Capital Requirements | Billions needed for R&D, manufacturing, marketing. | Established infrastructure and financial strength. |

| Brand Loyalty | Difficult to build trust and recognition against established brands. | Decades of brand building with trusted names like Persil. |

| Distribution Networks | Costly to establish global reach and channel expertise. | Extensive, efficient networks across diverse markets. |

| Regulatory Compliance | Millions in costs and years for approvals in chemical/beauty sectors. | Existing infrastructure and expertise for efficient compliance. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Henkel is built upon a foundation of diverse data, including Henkel's official annual reports, investor presentations, and press releases. We supplement this with industry-specific market research reports from reputable firms and data from financial information providers like Bloomberg and S&P Capital IQ to capture a comprehensive view of the competitive landscape.