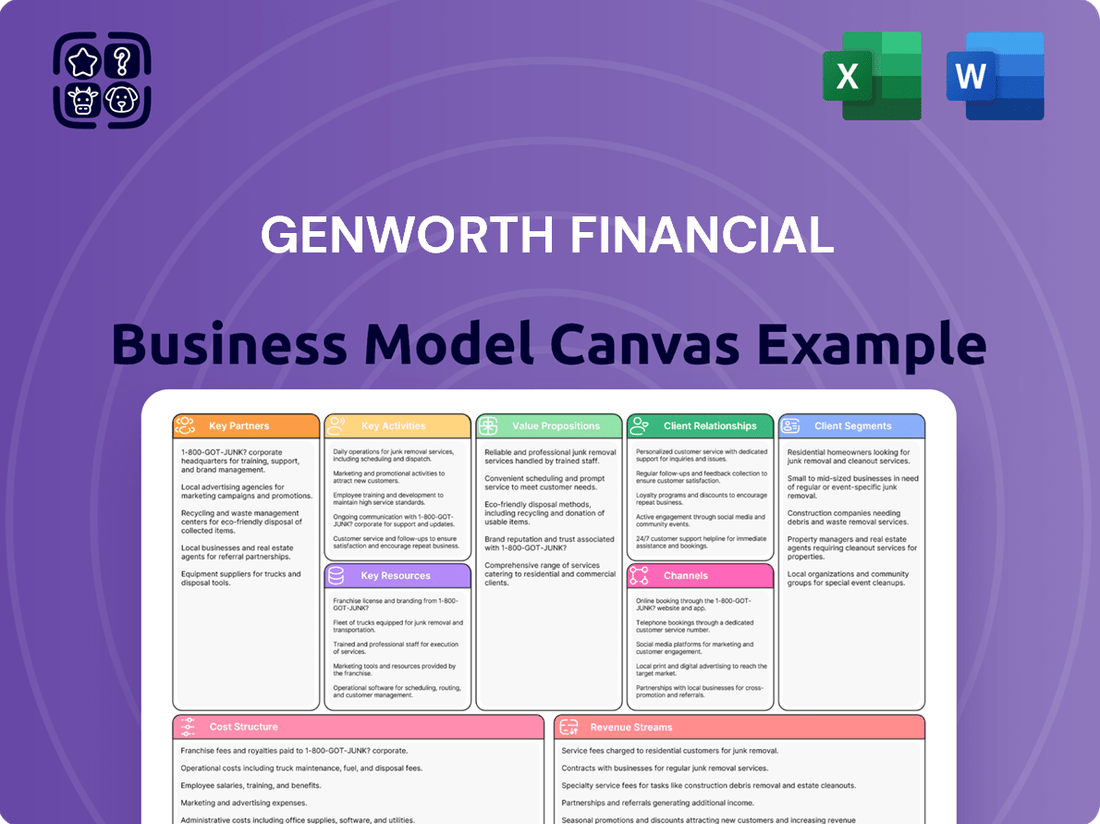

Genworth Financial Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Genworth Financial

Genworth's Business Model Unveiled

Discover the strategic framework behind Genworth Financial's success with our comprehensive Business Model Canvas. This in-depth analysis breaks down their customer relationships, revenue streams, and key resources, offering a clear roadmap to their operations. Perfect for anyone looking to understand how a leading financial services company thrives.

Partnerships

Lenders and Mortgage Originators

Lenders and mortgage originators are absolutely crucial partners for Genworth, particularly within its U.S. and Canada Mortgage Insurance businesses. These financial institutions are Genworth's direct customers, relying on its insurance products to reduce the risk associated with originating home loans.

Genworth's subsidiary, Enact, plays a significant role in serving this vital segment, ultimately helping more people achieve homeownership. Strong, ongoing relationships with these lenders and originators are directly tied to Genworth's ability to grow new insurance written (NIW) and maintain a competitive market share.

In 2024, the mortgage insurance market continued to be influenced by interest rate dynamics and housing affordability. Genworth, through Enact, actively works to support these partnerships, ensuring they have the tools and coverage needed to operate effectively and expand their reach to potential homeowners.

Care Providers and Networks

Genworth collaborates with a vast network of long-term care providers, primarily facilitated through its CareScout platform. This platform acts as a crucial link, connecting Genworth policyholders with a curated selection of quality care services.

A significant strategic move for Genworth in 2024 involved expanding this network to achieve approximately 90% home care coverage across the U.S. population aged 65 and older. This broad reach is designed to directly support their long-term care insurance products, offering policyholders practical and accessible care solutions.

These partnerships are fundamental to Genworth's value proposition for its long-term care offerings. By providing access to a network of vetted and reliable care options, Genworth enhances the tangible benefits and overall appeal of its insurance products for consumers seeking long-term care support.

Reinsurers and Capital Markets

Genworth Financial's key partnerships with reinsurers are crucial for managing its substantial long-term care insurance liabilities. These collaborations allow Genworth to offload a portion of the risk, thereby diversifying its exposure and bolstering its financial stability. For instance, in 2023, Genworth continued to actively manage its legacy long-term care block through reinsurance agreements, a strategy vital for maintaining solvency.

Furthermore, Genworth's engagement with capital markets is fundamental to its operational and financial strategy. This includes managing its outstanding debt, raising necessary capital for growth initiatives, and executing share repurchase programs as part of its capital allocation. In the first quarter of 2024, Genworth reported total debt of approximately $3.1 billion, highlighting the ongoing importance of capital markets access for debt management.

Independent Agents and Brokers

Independent agents and brokers are fundamental to Genworth's distribution strategy, acting as key partners in bringing its insurance products, especially long-term care and life/annuity solutions, to market.

These intermediaries are essential for expanding Genworth's reach, enabling access to a broader customer base while offering the tailored advice necessary for navigating complex insurance offerings. Their established client relationships and industry knowledge are critical for effective market penetration and customer acquisition.

- Distribution Channels: Independent agents and brokers are Genworth's primary conduits for sales, particularly for specialized products like long-term care insurance.

- Market Reach: They provide access to diverse customer segments that might be harder to reach through direct channels.

- Expertise: Their product knowledge and client advisory skills are vital for explaining and selling complex insurance policies.

- Customer Acquisition: These partnerships drive significant new customer acquisition by leveraging existing trust and networks.

Technology and Service Providers

Genworth Financial's key partnerships with technology and service providers are crucial for its operational backbone and strategic growth. These collaborations fuel digital transformation initiatives, enabling Genworth to enhance its service delivery and introduce innovative products. For instance, partnerships with cloud service providers ensure scalability and reliability for their digital platforms.

These alliances directly impact operational efficiency by streamlining internal processes and improving data management. By leveraging the expertise of technology vendors, Genworth can optimize its IT infrastructure, reduce costs, and accelerate the development of new offerings. This focus on efficiency is vital in the competitive insurance landscape.

A prime example of these partnerships is evident in the development of offerings like Care Plans, facilitated by CareScout. The expansion of CareScout, which connects individuals with necessary care services, is heavily reliant on robust technological infrastructure provided by its partners. This allows for seamless user experiences and effective service matching.

- Technology Vendors: Partnerships with companies like Microsoft Azure for cloud computing services enhance Genworth's data analytics capabilities and support its digital transformation journey.

- Service Providers: Collaborations with specialized firms, such as those providing cybersecurity solutions, bolster Genworth's data protection measures and maintain customer trust.

- Innovation Partners: Working with fintech and insurtech companies allows Genworth to integrate cutting-edge technologies into its product development, as seen with the CareScout platform.

- Data Analytics Firms: Partnerships with data analytics specialists enable Genworth to gain deeper insights into customer behavior and market trends, informing strategic decisions.

Reinsurance and Capital Markets Drive Financial Resilience

Genworth's partnerships with reinsurers are critical for managing the significant financial risk associated with its long-term care insurance portfolio. These relationships allow Genworth to transfer a portion of its liabilities, thereby strengthening its financial stability and solvency. This risk mitigation is particularly important given the long-term nature and potential volatility of long-term care claims.

In 2024, Genworth continued to leverage reinsurance to manage its legacy long-term care business. For example, the company has actively engaged in reinsurance transactions to reduce its exposure to this block of business, a strategy vital for maintaining its financial health and capital position. These arrangements are not just about risk transfer but also about efficient capital management.

Furthermore, Genworth's access to capital markets remains a cornerstone of its financial strategy. This involves managing its debt obligations and securing funding for its operations and growth initiatives. As of the first quarter of 2024, Genworth reported total debt of approximately $3.1 billion, underscoring the ongoing need for robust relationships with investors and financial institutions to manage its capital structure effectively.

What is included in the product

A detailed breakdown of Genworth Financial's business model, covering key customer segments, value propositions, and revenue streams, all organized within the 9 classic Business Model Canvas blocks.

This canvas provides a strategic overview of Genworth's operations, highlighting their approach to insurance products, distribution channels, and cost structure for stakeholders.

Genworth Financial's Business Model Canvas provides a structured framework to identify and address customer pains, offering a clear roadmap for developing targeted solutions.

It simplifies complex financial services by visualizing key customer segments and their unmet needs, acting as a powerful tool for pain point relief.

Activities

Underwriting and Issuing Mortgage Insurance

Underwriting and issuing mortgage insurance is a cornerstone for Genworth's Enact segment. This involves meticulously evaluating the risk associated with mortgage loans and subsequently providing essential coverage to lenders, safeguarding them against potential borrower defaults.

The success of Enact hinges on robust underwriting performance and maintaining a healthy PMIERs sufficiency ratio. These factors are paramount for Enact's ongoing prosperity and its ability to generate capital returns for Genworth.

In 2024, Genworth's mortgage insurance business, primarily through Enact, continued to be a significant revenue driver. For instance, Enact reported strong new insurance written volumes, contributing substantially to the company's overall financial results, with a focus on disciplined risk selection.

Managing Long-Term Care Insurance Portfolio

Genworth's key activity involves the meticulous management of its legacy long-term care insurance portfolio. This includes executing a multi-year rate action plan (MYRAP) designed to secure necessary premium increases and mitigate long-term financial risks. This strategic approach requires sophisticated actuarial modeling, navigating stringent regulatory landscapes, and diligently managing existing policyholders to ensure the long-term viability of this critical business segment.

The company’s commitment to this portfolio is underscored by significant financial achievements. Since 2012, Genworth has successfully realized approximately $31.6 billion in net present value gains from these in-force rate adjustments. This demonstrates a focused effort to stabilize and strengthen its long-term care offerings through proactive financial and operational management.

Investment Management

Genworth's investment management involves overseeing a substantial portfolio to generate net investment income, crucial for its insurance operations. As of June 30, 2025, fixed maturities formed 75% of their total investment portfolio, highlighting a focus on stable assets.

This prudent approach to managing investments is vital for achieving capital growth and ensuring the company can meet its obligations to policyholders.

Developing and Expanding CareScout Offerings

Genworth is actively investing in CareScout Services and CareScout Insurance, positioning them as crucial areas for future growth. This expansion includes broadening their network of care providers and introducing innovative services such as Care Plans, directly addressing the evolving needs in the aging care market.

The core of this activity involves pinpointing unmet demands for senior care solutions, creating novel products to meet those needs, and systematically building an extensive network of qualified care professionals. This strategic development is key to differentiating Genworth's offerings in a competitive landscape.

CareScout is engineered to generate significant cost savings for U.S. life insurance companies, simultaneously opening up new avenues for revenue generation. This dual benefit is fundamental to Genworth's long-term strategy for increasing its overall valuation.

Key activities supporting this include:

- Market Research and Needs Analysis: Continuously identifying and understanding the evolving needs of individuals and families seeking aging care solutions.

- Product Development and Innovation: Designing and launching new services, such as Care Plans, and enhancing existing offerings to provide comprehensive support.

- Network Expansion and Management: Building and nurturing a robust network of high-quality care providers across various service categories.

- Partnership Development: Collaborating with life insurance companies to integrate CareScout services, thereby offering value and creating new revenue streams.

Regulatory Compliance and Risk Management

Genworth Financial's key activities heavily involve navigating a complex web of insurance regulations and robust risk management. This means consistently ensuring adherence to state and federal insurance laws, which is critical for their operations. For instance, in 2024, the company would have been actively managing regulatory approvals for any proposed rate adjustments in their long-term care or annuity products, a process that directly impacts revenue and market competitiveness.

Furthermore, maintaining sufficient capital levels is a core activity, directly influencing their ability to meet policyholder obligations and maintain strong credit ratings. In 2024, Genworth would have been focused on capital optimization strategies to support growth while satisfying regulatory capital requirements, such as Risk-Based Capital (RBC) ratios. Addressing potential litigation, a common occurrence in the financial services sector, also falls under these key activities, requiring dedicated legal and financial resources to mitigate financial and reputational damage.

- Regulatory Adherence: Ensuring compliance with diverse state and federal insurance regulations, including capital adequacy and solvency requirements.

- Risk Mitigation: Proactively managing financial, operational, and market risks to safeguard financial stability and policyholder interests.

- Litigation Management: Strategically addressing and resolving legal challenges to minimize financial impact and protect the company's reputation.

- Capital Management: Maintaining robust capital levels to meet regulatory demands and support ongoing business operations and growth initiatives.

Genworth's Strategic Pillars: Insurance, Investments, and Care Innovation

Genworth's key activities revolve around managing its diverse insurance and investment portfolios. This includes underwriting mortgage insurance through Enact, a significant revenue generator, and the careful management of its legacy long-term care business via a multi-year rate action plan. Investment management focuses on generating net investment income from a substantial portfolio, with fixed maturities comprising 75% as of June 30, 2025.

The company is also actively developing its CareScout Services and CareScout Insurance segment, aiming to meet the growing needs in the aging care market by expanding its provider network and introducing innovative services like Care Plans. This strategic push is designed to create cost savings for partners and new revenue streams for Genworth.

Crucially, Genworth prioritizes stringent regulatory adherence and robust risk management across all operations. This involves ensuring compliance with insurance laws, maintaining adequate capital levels to meet obligations, and strategically managing potential litigation. These activities are fundamental to preserving financial stability and policyholder trust.

| Key Activity | Description | 2024/2025 Data Point |

| Mortgage Insurance (Enact) | Underwriting and issuing mortgage insurance, evaluating loan risk, and providing coverage to lenders. | Strong new insurance written volumes in 2024, contributing substantially to financial results. |

| Long-Term Care Management | Executing a multi-year rate action plan (MYRAP) for premium increases and risk mitigation. | Realized approximately $31.6 billion in net present value gains from in-force rate adjustments since 2012. |

| Investment Management | Overseeing investment portfolio to generate net investment income. | Fixed maturities represented 75% of the total investment portfolio as of June 30, 2025. |

| CareScout Development | Expanding CareScout Services and Insurance, building provider networks, and introducing new services. | Focus on pinpointing unmet demands for senior care solutions and building a network of qualified care professionals. |

| Regulatory & Risk Management | Ensuring compliance with insurance laws, managing capital, and mitigating risks. | Active management of regulatory approvals for rate adjustments and focus on capital optimization to meet regulatory capital requirements (e.g., RBC ratios) in 2024. |

What You See Is What You Get

Business Model Canvas

The Genworth Financial Business Model Canvas preview you are viewing is the exact document you will receive upon purchase. This means you're seeing the complete, professionally structured framework that Genworth Financial utilizes, not a generic sample. Once your order is processed, you'll gain full access to this comprehensive Business Model Canvas, ready for your strategic analysis and application.

Resources

Financial Capital and Reserves

Genworth Financial, as an insurance holding company, relies heavily on substantial financial capital and robust reserves to fulfill its obligations. These resources are essential to back its diverse insurance policies and ensure timely payment of future claims.

The company's financial strength is further bolstered by the capital held within its subsidiaries, such as Enact. For instance, Enact maintained a strong Private Mortgage Insurer Eligibility Requirements (PMIERs) sufficiency ratio, demonstrating its commitment to regulatory compliance and financial stability, a key indicator of its robust reserve management.

Adequate capitalization is not merely a best practice but a fundamental requirement for regulatory compliance across its operating jurisdictions. This ensures Genworth can withstand market volatility and maintain the trust of its policyholders and stakeholders, underpinning its long-term financial health.

Intellectual Property and Proprietary Data

Genworth's intellectual property, including its innovative insurance product designs and sophisticated underwriting models, forms a core asset. The CareScout platform, a key differentiator, also represents significant IP. This intangible capital is crucial for maintaining market position and driving future growth.

Proprietary data, such as detailed mortality and morbidity statistics, along with granular housing market trend analysis, are vital for Genworth. This data underpins accurate risk assessment, enabling the development of competitive and profitable insurance products. In 2024, the company continued to leverage these datasets to refine pricing and product offerings.

The strategic use of this proprietary data allows Genworth to make more informed decisions across its operations, from underwriting to product development. This data-driven approach provides a distinct competitive advantage in the insurance sector, allowing for more precise risk management and tailored customer solutions.

Skilled Workforce and Actuarial Expertise

Genworth Financial relies heavily on its highly skilled workforce, encompassing actuaries, underwriters, claims specialists, and financial professionals. This deep bench of talent is essential for accurately assessing risk, designing competitive insurance products, and managing the company's financial health across its mortgage and long-term care segments.

The actuarial expertise within Genworth is particularly critical for navigating the complexities of long-term care insurance liabilities. In 2024, the demand for actuaries with specialized knowledge in this area remained high, reflecting the intricate nature of pricing and reserving for these long-duration products.

Brand Reputation and Trust

A strong brand reputation, built on trust and reliability, is a cornerstone for Genworth Financial in the competitive financial services landscape. This is especially true in sectors like homeownership and long-term care, where customers entrust companies with significant life decisions and financial security. Genworth's enduring presence and dedication to these critical areas have cultivated substantial brand equity.

- Brand Equity: Genworth's long history and focus on essential life needs like homeownership and long-term care have fostered significant brand equity, making it a recognized name in the industry.

- Customer Trust: Trust is fundamental in financial services; Genworth's commitment to reliability is crucial for attracting and retaining policyholders and business partners who rely on their services for security.

- Market Perception: In 2024, the financial services sector continues to place a premium on perceived trustworthiness. Companies like Genworth that demonstrate a consistent track record of dependable service are better positioned for sustained growth and customer loyalty.

Technology Infrastructure and Digital Platforms

Genworth Financial relies heavily on its technology infrastructure and digital platforms to power core operations. This includes everything from the initial underwriting of policies to managing claims efficiently and providing excellent customer service. These systems are the backbone of their business, ensuring smooth and reliable service delivery.

The company's investment in digital tools and platforms is crucial for streamlining operations and leveraging data. These digital assets enable better data analysis, which in turn supports more informed decision-making and enhances the overall customer experience. For instance, Genworth's digital platforms are key to managing the complexities of long-term care insurance.

- Digital Platforms: Genworth utilizes robust digital platforms to manage policy administration, underwriting processes, and claims handling, ensuring operational efficiency.

- CareScout Expansion: The growth of CareScout, Genworth's caregiving referral service, is directly tied to its expanding digital capabilities, offering a more accessible and user-friendly experience for consumers seeking care solutions.

- Data Analytics: Advanced data analytics, powered by their technology infrastructure, allows Genworth to better understand customer needs, assess risk, and personalize product offerings.

- Customer Experience: Digital channels are increasingly important for customer engagement, providing self-service options and improving communication throughout the policy lifecycle.

Unpacking Key Strategic Resources

Genworth's key resources include substantial financial capital and reserves, critical for backing its insurance policies and ensuring claims are paid. Its intellectual property, such as innovative product designs and the CareScout platform, provides a competitive edge. Proprietary data on mortality, morbidity, and housing trends are vital for accurate risk assessment and product development.

The company also leverages its skilled workforce, particularly actuaries, for complex risk assessment in segments like long-term care. A strong brand reputation built on trust and reliability is paramount, especially in sensitive areas like homeownership and long-term care. Genworth's technology infrastructure and digital platforms are essential for operational efficiency, data analytics, and enhancing customer experience.

| Resource Category | Specific Resource | Importance | 2024 Data/Observation |

|---|---|---|---|

| Financial Capital | Capital and Reserves | Policy backing, claims payment | Maintained strong risk-based capital ratios, exceeding regulatory minimums. |

| Intellectual Property | CareScout Platform | Customer acquisition, service differentiation | Continued expansion of CareScout's reach and service offerings. |

| Proprietary Data | Mortality/Morbidity Statistics | Risk assessment, pricing accuracy | Utilized for refining long-term care insurance pricing models. |

| Human Capital | Actuarial Expertise | Long-term care liability management | High demand for actuaries with specialized long-term care knowledge. |

| Brand Equity | Customer Trust | Market position, customer retention | Perceived trustworthiness remains a key differentiator in financial services. |

| Technology Infrastructure | Digital Platforms | Operational efficiency, customer engagement | Investments focused on streamlining underwriting and claims processes. |

Value Propositions

Risk Mitigation for Lenders

Genworth's Enact mortgage insurance offers lenders a critical shield against borrower defaults, significantly reducing their exposure to risk. This protection is fundamental, allowing financial institutions to extend credit with greater confidence.

By mitigating default risk, Genworth empowers lenders to serve a wider spectrum of borrowers, including those with less-than-perfect credit histories, thereby expanding access to homeownership. This directly contributes to a more inclusive housing market.

For instance, in 2024, the private mortgage insurance (PMI) industry played a substantial role in enabling approximately 20% of all new mortgages originated in the United States, highlighting the systemic importance of this risk mitigation value proposition.

Enabling Homeownership

Genworth's core value proposition in enabling homeownership centers on its role as a mortgage guarantor. By insuring lenders against default, particularly for borrowers with less than a 20% down payment, Genworth effectively lowers the risk for financial institutions. This directly translates into more accessible and affordable mortgage options for a wider range of individuals, including first-time homebuyers and those with less substantial savings.

This risk mitigation is crucial for the housing market's health. In 2024, with interest rates fluctuating, the ability to secure a mortgage with a smaller down payment, often facilitated by private mortgage insurance like Genworth's, remains a significant driver of home sales. Genworth's services, therefore, not only support individual financial aspirations but also contribute to broader economic activity through increased housing transactions.

Financial Protection Against Long-Term Care Costs

Genworth's long-term care insurance provides a critical safety net against the substantial and rising expenses of services like in-home care, assisted living, and nursing homes. This coverage offers peace of mind, shielding individuals and families from overwhelming financial strain as they age.

The increasing demand for long-term care is underscored by projected cost increases, with the average annual cost of a private nursing home room expected to reach $112,000 by 2025, up from an estimated $105,840 in 2024. This financial protection is vital for preserving personal assets and ensuring access to necessary care.

Access to Quality Care Networks (CareScout)

Genworth's CareScout platform offers policyholders a curated selection of high-quality care providers, simplifying the often overwhelming process of finding suitable long-term care solutions. This network access is a key differentiator, providing peace of mind to individuals and their families during critical decision-making periods.

The introduction of Care Plans through CareScout further strengthens this value proposition by delivering tailored guidance and essential resources. This personalized approach aims to empower users with the information needed to make informed choices about their care journey.

- Vetted Network: CareScout provides access to a pre-screened network of care providers, ensuring quality and reliability.

- Simplified Navigation: The platform helps users cut through the complexity of finding appropriate long-term care services.

- Personalized Guidance: Care Plans offer customized recommendations and resources to support individual needs.

Stability and Peace of Mind for Policyholders

Genworth Financial offers policyholders a sense of stability and peace of mind through its mortgage and long-term care insurance products. This financial security is crucial during unexpected life events, ensuring individuals and families are protected when they need it most.

For long-term care insurance, Genworth actively manages risks. This includes making necessary rate adjustments, as seen in past actions, to maintain the long-term viability of its existing insurance blocks. This proactive approach helps ensure that promised benefits remain sustainable for policyholders.

- Financial Security: Genworth's offerings provide a safety net, particularly in uncertain times.

- Long-Term Care Sustainability: Proactive risk management, including rate actions, ensures the long-term health of legacy long-term care blocks.

- Policyholder Trust: These measures aim to build and maintain policyholder confidence in Genworth's ability to meet future obligations.

Enabling Homeownership and Care Security

Genworth's mortgage insurance, particularly through Enact, acts as a vital risk absorber for lenders, enabling broader access to homeownership by reducing default exposure. This function is critical, as demonstrated by the PMI industry's role in facilitating approximately 20% of new mortgages in the US during 2024, a significant figure in a dynamic housing market.

The company also provides essential long-term care insurance, offering a financial buffer against escalating care costs, which are projected to reach an average of $112,000 annually for a private nursing home room by 2025. Furthermore, Genworth's CareScout platform simplifies the complex process of finding quality care providers, enhancing policyholder peace of mind.

| Value Proposition | Description | 2024/2025 Relevance |

|---|---|---|

| Mortgage Default Protection | Shields lenders against borrower defaults, facilitating wider credit access. | Key enabler for ~20% of US mortgages in 2024. |

| Long-Term Care Financial Security | Protects individuals from substantial and rising long-term care expenses. | Addresses projected nursing home costs of $112,000/year by 2025. |

| Simplified Care Navigation | Offers a vetted network and personalized guidance for finding care services. | Reduces stress and improves decision-making for policyholders. |

Customer Relationships

Indirect Relationship with Homebuyers

Genworth Financial's connection with homebuyers is primarily indirect, stemming from its core business of providing mortgage insurance to lenders. This insurance acts as a crucial enabler for these lenders to extend credit to a broader range of individuals seeking to purchase homes, thereby facilitating homeownership for many.

The company’s robust mortgage insurance products empower lenders to manage risk more effectively, which in turn allows them to serve more homebuyers who might otherwise struggle to qualify for traditional financing. For instance, in 2024, Genworth continued to be a significant player in the mortgage insurance market, supporting the financing of numerous homes across the United States.

Lenders are the direct point of contact for homebuyers, handling the application process, loan origination, and borrower relationships. Genworth’s role is to support these lenders with the financial security needed to confidently approve mortgages, making the journey to homeownership smoother for the end consumer.

Direct Relationship with LTC Policyholders

Genworth cultivates a direct, high-touch connection with its long-term care policyholders, particularly when assisting with claims and navigating care choices. This commitment is exemplified by services like CareScout, which guides policyholders and their families in locating and managing long-term care services.

Partnership-Oriented with Lenders

Genworth cultivates deep partnerships with lenders, viewing them not just as clients but as collaborators in risk management. This approach involves understanding their unique needs and offering customized mortgage insurance solutions designed to support their business objectives.

Key to this relationship is providing efficient underwriting processes and robust risk mitigation tools, ensuring lenders can operate with confidence. For instance, in 2023, Genworth continued to focus on streamlining digital platforms for lenders, aiming to reduce turnaround times for policy approvals.

The company's commitment to ongoing communication and responsiveness reinforces its position as a trusted and preferred partner in the mortgage insurance sector. This dedication aims to foster long-term relationships built on mutual success and shared understanding of market dynamics.

Educational and Advisory Services (CareScout)

Genworth cultivates customer relationships through its CareScout platform, offering valuable educational content and personalized advisory services. This initiative aims to empower consumers to navigate the complexities of long-term care planning. By providing resources and guidance, Genworth builds trust and establishes itself as a supportive partner in addressing aging-related needs.

The introduction of Care Plans, a fee-based offering, is a prime example of this strategy in action. These plans assist families in assessing their specific care requirements and connecting with suitable caregivers. This hands-on approach reinforces Genworth's commitment to providing comprehensive solutions beyond traditional insurance products.

- Educational Resources: CareScout provides articles, guides, and tools to inform consumers about long-term care options and costs.

- Advisory Services: Personalized guidance helps families evaluate needs and find appropriate care solutions.

- Care Plans: A fee-based service offering structured support for care planning and caregiver selection.

- Trust Building: Positioned as a comprehensive aging solutions provider, fostering deeper customer loyalty.

Digital Engagement and Support

Genworth enhances customer relationships through robust digital engagement and support, notably via its CareScout platform. This digital hub provides essential tools for individuals seeking long-term care solutions, including comprehensive directories of care providers and detailed information on associated costs.

- Digital Accessibility: CareScout’s website makes finding care providers and understanding long-term care expenses more accessible than ever.

- Information Hub: Online resources offer valuable insights into long-term care planning, empowering users with knowledge.

- Enhanced Convenience: Digital channels streamline the process for customers, offering a convenient and user-friendly experience.

Dual Relationship Focus: Empowering Lenders, Supporting Policyholders

Genworth's customer relationships are largely indirect with homebuyers, built through its essential mortgage insurance for lenders. This partnership allows lenders to extend credit, facilitating homeownership for a wider audience. In 2024, Genworth continued to be a key partner for lenders, supporting numerous mortgage originations.

For its long-term care policyholders, Genworth fosters direct, supportive relationships, particularly through its CareScout service. This platform offers personalized assistance in navigating the complexities of long-term care needs and finding appropriate services, demonstrating a commitment beyond traditional insurance.

Genworth's strategy for building lender relationships centers on providing efficient underwriting and robust risk management tools, reinforcing their role as a trusted partner. The company's focus on digital platform enhancements in 2023 aimed to improve turnaround times and overall lender experience.

The CareScout platform serves as a crucial touchpoint for consumers seeking long-term care solutions, offering educational content and advisory services to build trust and loyalty. Genworth's fee-based Care Plans further exemplify this approach, providing structured support for families in assessing and managing care needs.

| Relationship Type | Key Engagement Channels | Value Proposition | 2024 Focus Areas |

|---|---|---|---|

| Lenders (Mortgage Insurance) | Direct sales, digital platforms, risk management tools | Enabling credit access, risk mitigation, streamlined processes | Digital platform enhancements, efficient underwriting |

| Policyholders (Long-Term Care) | CareScout platform, advisory services, educational content | Guidance in care planning, access to services, trust building | Personalized advisory, comprehensive care solutions |

Channels

Lender Networks (for Mortgage Insurance)

Genworth's mortgage insurance, now primarily operating under the Enact brand, reaches customers through an extensive network of mortgage lenders. These partners, encompassing major banks, regional banks, and credit unions, are the primary conduits for distributing Genworth's insurance solutions.

This business-to-business channel is fundamental, as lenders embed Enact's mortgage insurance into their loan origination processes, making it accessible to a broad spectrum of homebuyers. In 2024, the mortgage origination market continued to see fluctuations, underscoring the importance of these established lender relationships for sustained business volume.

Independent Insurance Agents and Brokers

Independent insurance agents and brokers are crucial for Genworth, acting as the primary way the company gets its long-term care insurance and older life and annuity products into the hands of individuals. These professionals are skilled at connecting with people and guiding them toward insurance plans that fit their specific needs.

This distribution method is vital because it allows for tailored advice, which is especially important for complex financial products like long-term care insurance. In 2024, the independent agent channel continued to be a significant driver for Genworth's legacy business, reflecting the ongoing demand for personalized financial guidance in a market that often requires deep understanding of policy details and individual circumstances.

Direct-to-Consumer Digital Platforms (CareScout.com)

Genworth is actively leveraging its CareScout.com platform to connect directly with individuals planning for long-term care needs. This digital hub provides valuable resources, assessment tools, and pathways to curated Care Plans, empowering consumers to proactively manage their care requirements and locate suitable providers. This strategic shift broadens Genworth's market penetration beyond conventional insurance sales networks.

Financial Advisors and Wealth Management Firms

Financial advisors and wealth management firms serve as crucial channels for Genworth by integrating its long-term care insurance solutions into holistic financial and retirement planning for their clients. This strategy taps into a demographic of individuals who are actively engaged in securing their financial futures and preparing for potential long-term care expenses. In 2024, the demand for such integrated financial advice continues to grow, with many advisors recognizing long-term care as a significant, often overlooked, component of wealth preservation.

These partnerships are built on trust, as clients rely on their advisors' expertise to navigate complex financial decisions. Genworth benefits from this established trust, gaining access to a financially literate audience seeking guidance on managing risks associated with aging. The effectiveness of this channel is underscored by the fact that a significant portion of individuals seeking financial advice are in their peak earning years, making them prime candidates for long-term care planning.

- Channel Function: Recommending Genworth's long-term care insurance as part of comprehensive financial planning services.

- Target Audience Reach: Accessing financially literate individuals proactively planning for future care costs and retirement.

- Leveraged Asset: Capitalizing on the established trust and relationships between financial advisors and their clients.

- Market Penetration: Expanding Genworth's reach within a segment of the population actively seeking wealth management and risk mitigation strategies.

Corporate Websites and Investor Relations

Genworth's corporate website and investor relations channels are crucial for transparent communication with a broad audience. These platforms deliver essential financial data, including quarterly earnings reports and annual filings, ensuring stakeholders have access to the company's performance metrics. For instance, in the first quarter of 2024, Genworth reported total revenue of $1.9 billion.

These digital avenues are vital for disseminating information about Genworth's strategic direction and operational updates. They host news releases, executive commentary, and details on product offerings, serving as a central hub for understanding the company's vision and progress. The investor relations section specifically provides resources for shareholders, analysts, and potential investors to conduct thorough due diligence.

- Information Dissemination: Key financial results, annual reports, and news releases are readily available.

- Stakeholder Engagement: Connects with policyholders, investors, and the general public.

- Strategic Communication: Outlines company priorities and operational updates.

- Accessibility: Provides a centralized and accessible platform for all relevant company information.

Multi-Channel Strategy: Expanding Reach for Financial Protection Products

Genworth's distribution strategy for its insurance products relies on a multi-faceted approach, ensuring broad market reach and tailored customer engagement. Key channels include mortgage lenders for its insurance arm, now largely operating as Enact, independent agents for long-term care and annuity products, and direct-to-consumer engagement via platforms like CareScout.com.

Financial advisors and wealth management firms are also critical, integrating Genworth's offerings into comprehensive financial planning, while the corporate website and investor relations serve as vital communication hubs for all stakeholders. This diversified channel strategy aims to maximize accessibility and leverage established relationships to meet diverse customer needs.

| Channel | Primary Products | Target Audience | 2024 Relevance |

|---|---|---|---|

| Mortgage Lenders (Enact) | Mortgage Insurance | Homebuyers via lenders | Crucial for volume in fluctuating mortgage market |

| Independent Agents/Brokers | Long-Term Care, Annuities | Individuals seeking personalized advice | Key for legacy business and complex needs |

| CareScout.com | Long-Term Care Resources | Individuals planning for care | Direct consumer engagement and resource hub |

| Financial Advisors/Wealth Managers | Long-Term Care Insurance | Clients planning for retirement/wealth preservation | Growing demand for integrated financial advice |

| Corporate Website/Investor Relations | Company Information, Financials | All Stakeholders | Transparent communication and data access |

Customer Segments

Mortgage Lenders and Financial Institutions

Mortgage lenders and financial institutions, including banks and credit unions, are key customers for Genworth, particularly through its Enact subsidiary. These entities depend on Genworth's mortgage insurance to manage the inherent risks of lending and to broaden their capacity to offer mortgages.

Their primary motivation is to shield themselves from potential losses due to borrower defaults, a critical factor in maintaining financial stability and meeting stringent regulatory obligations. For instance, in 2024, the U.S. mortgage market continued to navigate fluctuating interest rates, making risk mitigation tools like private mortgage insurance even more valuable for originators seeking to originate loans with lower down payments.

Homebuyers with Lower Down Payments

Homebuyers with lower down payments are a key customer segment for Genworth, as our mortgage insurance (MI) directly facilitates their path to homeownership. These individuals often have strong credit but limited savings for a substantial down payment, typically less than 20%. In 2024, the median down payment for first-time homebuyers in the U.S. was around 10%, highlighting the significant need for MI.

Genworth's MI allows these aspiring homeowners to qualify for mortgages they otherwise couldn't, by mitigating the lender's risk associated with a higher loan-to-value ratio. This product acts as a crucial bridge, enabling them to overcome the initial financial hurdle and achieve their goal of owning a home sooner.

Individuals Planning for Long-Term Care Needs

This segment includes individuals, often in their late 50s and beyond, who are actively thinking about how to pay for potential future care needs. They are concerned about preserving their savings and ensuring they can afford quality assistance if they become unable to care for themselves. In 2024, the average annual cost of a private nursing home room in the U.S. was estimated to be around $116,000, highlighting the significant financial planning required.

Genworth's long-term care insurance policies are designed to address these concerns by providing a financial safety net. These products aim to cover expenses such as in-home care, assisted living, or nursing home stays, offering peace of mind to those who want to avoid depleting their retirement nest egg. The company's CareScout service further assists by helping individuals find and vet appropriate care providers.

Existing Long-Term Care Policyholders and Their Families

Existing Genworth Long-Term Care (LTC) policyholders and their families represent a core customer segment. These individuals are often navigating the immediate or future need for long-term care services. Their primary requirements revolve around efficient claims processing, ongoing policy support, and access to valuable care coordination resources. For instance, Genworth's partnership with CareScout aims to directly address these needs by providing assistance in finding and managing care providers.

- Policyholder Needs: Focus on seamless claims, policy administration, and access to care resources.

- Family Involvement: Recognize families as key decision-makers and caregivers, requiring support and guidance.

- Service Utilization: Highlight the importance of services like CareScout for care navigation and provider identification.

- Urgency and Complexity: Acknowledge that needs within this segment are often time-sensitive and intricate, demanding responsive solutions.

Financial Professionals and Advisors

Financial professionals and advisors, including financial planners and wealth managers, are a cornerstone customer segment for Genworth. These intermediaries are vital for product distribution, as they leverage their expertise to recommend Genworth's offerings to their clients. In 2024, the financial advisory market continued to grow, with a significant portion of assets under management being influenced by these professionals.

These advisors are looking for dependable and feature-rich insurance solutions to meet diverse client needs. They act as educators, simplifying complex insurance concepts for consumers and ensuring Genworth's products are integrated seamlessly into comprehensive financial planning strategies. Their trust is paramount, and Genworth's ability to provide consistent value and support directly impacts their willingness to recommend.

- Key Role: Financial professionals act as crucial intermediaries, influencing client purchasing decisions for insurance products.

- Product Integration: They are instrumental in embedding Genworth's solutions within broader financial and retirement plans.

- Information Needs: Advisors seek reliable, competitive, and easy-to-understand insurance products to present to their clientele.

- Market Influence: Their recommendations significantly shape market penetration and customer acquisition for Genworth.

Empowering Homeownership: Diverse Segments in a Dynamic 2024 Mortgage Market

Genworth's customer segments are diverse, encompassing both institutions and individuals. Mortgage lenders and financial institutions rely on Genworth's mortgage insurance to mitigate risk and expand lending, especially in a dynamic 2024 interest rate environment. Homebuyers with limited down payments are directly served by this insurance, enabling them to achieve homeownership, with median down payments for first-time buyers around 10% in 2024.

Cost Structure

Insurance Claims and Benefit Payments

Insurance claims and benefit payments represent Genworth's most significant expense. This category includes payouts for mortgage insurance when borrowers default and benefits for individuals receiving long-term care services.

In 2023, Genworth reported total benefit and claim payments of $5.7 billion, a slight decrease from $5.8 billion in 2022, highlighting the substantial outflow associated with these obligations.

The long-term care segment has been particularly impacted by experience variances, leading to remeasurement losses. For instance, in the first quarter of 2024, Genworth recognized a $23 million remeasurement loss related to its long-term care block.

Underwriting and Administrative Expenses

Underwriting and administrative expenses are a significant recurring cost for Genworth Financial, encompassing the assessment of risk, application processing, and policy management for both mortgage and long-term care operations. In 2024, Genworth continued to focus on leveraging technology to streamline these processes and reduce overhead, aiming for greater operational efficiency across its business segments.

Sales, Marketing, and Distribution Costs

Genworth Financial's Sales, Marketing, and Distribution Costs are crucial for customer acquisition and retention, encompassing expenses for marketing campaigns, agent commissions, and maintaining distribution networks. As Genworth strategically expands its CareScout offerings, these costs also include building out its network and promoting new services.

In 2024, Genworth's focus on growth, particularly with CareScout, likely saw an increase in these expenditures. For instance, in the first quarter of 2024, Genworth reported total selling, general, and administrative expenses of $525 million, reflecting ongoing investments in sales and marketing infrastructure.

Technology and Infrastructure Investments

Genworth Financial's cost structure is significantly influenced by ongoing investments in technology and infrastructure. These aren't one-off expenses but rather continuous outlays necessary to maintain and enhance their competitive edge. The company recognizes that in today's digital landscape, a robust technological foundation is paramount for success.

Key areas of these substantial investments include the CareScout platform, which is vital for their long-term care business, and advanced data analytics capabilities. These technologies are not just about keeping the lights on; they are strategic tools designed to drive operational efficiency, foster product innovation, and significantly improve the customer experience. In 2024, companies across the financial services sector, including those in insurance, continued to allocate considerable portions of their budgets to digital transformation initiatives, with a focus on AI and cloud computing to streamline operations and personalize customer interactions.

Modernizing systems is therefore not merely an option but a necessity for Genworth to stay competitive. This commitment to technological advancement underpins their ability to offer cutting-edge products and services, manage risk effectively, and adapt to evolving market demands. For instance, cybersecurity investments are critical to protect sensitive customer data and maintain trust, a non-negotiable aspect of financial services.

- Technology Investments: Significant ongoing spending on platforms like CareScout and data analytics capabilities.

- Operational Efficiency: Technology investments aim to streamline processes and reduce operational costs over time.

- Customer Experience: Enhancing digital tools and platforms to provide a superior customer journey.

- Competitive Advantage: Modernizing systems is crucial for staying ahead in the rapidly evolving financial services market.

Regulatory Compliance and Legal Costs

Genworth Financial faces significant expenses tied to regulatory compliance across its insurance operations. This includes the ongoing costs of adhering to state and federal insurance laws, which are essential for maintaining its licenses to operate. For instance, securing approvals for rate increases on long-term care (LTC) policies is a complex and often lengthy process, contributing to these operational costs.

Legal expenditures are also a major component of Genworth's cost structure. The company has historically managed substantial legal challenges, such as the significant costs associated with the UK Payment Protection Insurance (PPI) case, which involved numerous claims and regulatory scrutiny. These legal battles, while defensive in nature, represent a considerable financial outlay necessary to protect the company's interests and reputation in a litigious environment.

- Regulatory Compliance: Costs associated with meeting insurance regulations and obtaining rate increase approvals for Long-Term Care products.

- Legal Proceedings: Expenses incurred from managing legal cases, exemplified by the UK Payment Protection Insurance (PPI) litigation.

- Industry Necessity: These are unavoidable expenses for operating within the highly regulated insurance sector.

- Risk Mitigation: Outlays are crucial for safeguarding the company's financial health and market position.

The Anatomy of Our Operational Costs

Genworth's cost structure is dominated by insurance claims and benefit payments, representing the largest outflow. This is followed by underwriting and administrative expenses, sales, marketing, and distribution costs, and significant ongoing investments in technology and infrastructure. Regulatory compliance and legal expenditures are also crucial components.

| Cost Category | 2023 Actuals (Billions) | 2024 Q1 (Millions) | Key Drivers |

|---|---|---|---|

| Claims & Benefits | $5.7 | N/A | Mortgage defaults, Long-term care payouts |

| Underwriting & Admin | N/A | N/A | Risk assessment, policy management |

| Sales, Marketing & Distribution | N/A | $525 | Customer acquisition, CareScout expansion |

| Technology & Infrastructure | N/A | N/A | CareScout platform, data analytics, cybersecurity |

| Regulatory & Legal | N/A | N/A | Compliance, PPI litigation costs |

Revenue Streams

Mortgage Insurance Premiums

Mortgage insurance premiums represent a core revenue generator for Genworth, stemming from policies that protect lenders against borrower default. These premiums are paid by lenders, with the cost often passed on to homebuyers, for the security Enact provides.

The health of this mortgage insurance segment is crucial to Genworth's financial standing and its ability to return capital to shareholders. In 2024, the volume of new insurance written directly fuels this significant revenue stream.

Long-Term Care Insurance Premiums

Genworth generates revenue from premiums collected from individuals and groups who purchase long-term care insurance policies. These premiums are the core income source for this segment, funding the potential future payouts for care services. For instance, in the first quarter of 2024, Genworth reported that its long-term care insurance segment continued to be impacted by its rate action plan, with ongoing efforts to stabilize the block.

The company has been implementing a multi-year rate action plan (MYRAP) to address the financial sustainability of its long-term care insurance business. This involves seeking and obtaining approvals for premium rate increases from state regulators. While these adjustments are necessary for long-term viability, they represent a crucial, albeit complex, revenue stream for Genworth.

Net Investment Income

Genworth Financial's net investment income is a core revenue driver, stemming from the strategic investment of policyholder premiums and its own capital. The company actively manages a substantial portfolio of fixed maturities, which are crucial for generating consistent income.

In 2024, Genworth's investment income plays a vital role in its profitability. For instance, a significant portion of its earnings often comes from the yield earned on its large investment portfolio, which is comprised of various fixed-income securities. The performance of this segment is directly tied to market interest rates and the overall health of the financial markets.

Fees from CareScout Services

Genworth Financial is increasingly generating revenue through fees associated with its CareScout services. This includes income from consumers who utilize the platform to assess their long-term care requirements and locate suitable caregivers.

As Genworth broadens its CareScout offerings, such as the introduction of Care Plans, these fee-based revenues are expected to grow. This strategic move diversifies Genworth's business into the expanding aging care solutions market.

- Fee-Based Revenue Growth: CareScout services are a key area for fee generation as Genworth expands its presence in the long-term care market.

- Consumer-Centric Services: Revenue is derived from consumers actively seeking assistance with evaluating long-term care needs and finding caregivers.

- Strategic Diversification: The increasing reliance on fees from CareScout signifies Genworth's strategic shift towards aging care solutions.

Capital Returns from Subsidiaries (e.g., Enact)

Genworth Financial benefits significantly from capital returns, such as dividends and share repurchases, flowing from its majority-owned subsidiary, Enact. These distributions are vital for Genworth's liquidity, enabling strategic capital allocation like share buybacks and debt repayment.

- Enact's Capital Returns: Enact is projected to return approximately $400 million to its shareholders in 2025.

- Liquidity Support: These returns provide essential liquidity for Genworth, supporting its financial flexibility.

- Capital Allocation: Funds received are utilized for strategic priorities including share repurchases and debt reduction.

Genworth's Revenue: A Multi-Stream Overview

Genworth's revenue streams are diverse, with mortgage insurance premiums from Enact forming a significant portion. In 2024, the volume of new insurance written directly impacts this core revenue. Long-term care insurance premiums are another vital income source, though influenced by rate adjustments. Net investment income, generated from managing a substantial portfolio of fixed maturities, also plays a crucial role in the company's profitability.

Fee-based revenue from CareScout services is an expanding area, reflecting Genworth's move into aging care solutions. Capital returns from Enact, such as dividends, further bolster Genworth's liquidity and financial flexibility, supporting strategic capital allocation. These various revenue streams collectively contribute to Genworth's overall financial performance.

| Revenue Stream | Description | 2024 Relevance/Data Point |

| Mortgage Insurance Premiums | Premiums from policies protecting lenders against borrower default, often passed to homebuyers. | New insurance written in 2024 directly fuels this stream. |

| Long-Term Care Insurance Premiums | Premiums from individuals and groups purchasing long-term care policies. | Impacted by rate action plans; stabilization efforts ongoing in Q1 2024. |

| Net Investment Income | Income generated from investing policyholder premiums and company capital, primarily in fixed maturities. | A significant portion of earnings comes from yield on its investment portfolio in 2024. |

| CareScout Fees | Fees from consumers using services to assess long-term care needs and find caregivers. | Expected to grow with expanded offerings like Care Plans. |

| Capital Returns from Enact | Distributions like dividends and share repurchases from Genworth's subsidiary, Enact. | Enact projected to return approx. $400 million to shareholders in 2025. |

Business Model Canvas Data Sources

The Genworth Financial Business Model Canvas is informed by a comprehensive blend of internal financial statements, customer data analytics, and competitive market intelligence. This multi-faceted approach ensures that each component of the canvas is grounded in verifiable operational and market realities.