Fidelity National Financial Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Fidelity National Financial Bundle

Go Beyond the Preview—Access the Full Strategic Report

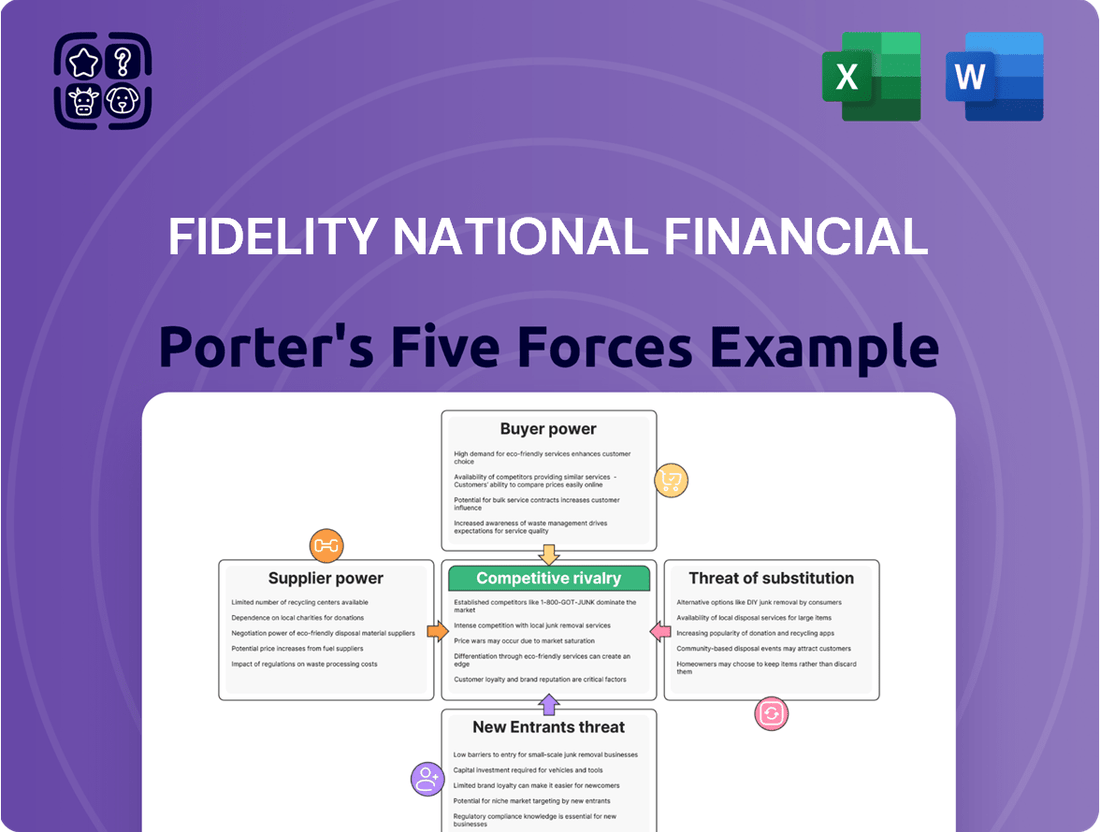

Fidelity National Financial navigates a landscape shaped by moderate buyer power and significant rivalry within the title insurance sector. Understanding these forces is crucial for any stakeholder looking to grasp the company's strategic positioning.

The complete report reveals the real forces shaping Fidelity National Financial’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Fragmented Supplier Base

Fidelity National Financial's (FNF) primary 'suppliers' are the numerous individual abstractors, title plants, and public record offices that furnish the essential data for title searches. This supplier landscape is characterized by its high degree of fragmentation, meaning no single entity possesses substantial leverage over a major entity like FNF.

Technology and Data Providers

Fidelity National Financial (FNF) relies on technology and data providers for crucial operational efficiencies. The bargaining power of these suppliers hinges on how unique and essential their services are, and how easily FNF could find replacements. In 2024, the increasing demand for specialized data analytics and AI-driven solutions means providers with proprietary offerings can command higher prices.

Human Capital/Expertise

Fidelity National Financial (FNF) relies heavily on skilled title examiners, abstractors, and legal professionals. The availability and cost of this specialized human capital directly impact FNF's operational efficiency and profitability. In 2024, the demand for experienced real estate legal professionals remained robust, potentially increasing their leverage.

Regulatory Information Access

Access to public records and regulatory databases is fundamental for Fidelity National Financial (FNF). While not a traditional supplier, changes in regulations or fees for accessing this information can impact FNF's operational costs.

For instance, in 2024, the cost of accessing certain property records or regulatory filings could see minor adjustments based on government agency budgets. FNF relies heavily on timely and accurate data for its title insurance and transaction services.

- Regulatory Data Costs: Potential increases in fees for accessing public land records or financial regulatory databases could marginally affect FNF's operating expenses.

- Information Accuracy: The reliability and accessibility of regulatory information directly influence FNF's ability to underwrite policies and manage risk effectively.

- Compliance Burden: Evolving regulatory landscapes might necessitate increased investment in compliance technologies and personnel, indirectly impacting supplier relationships related to data and analytics.

Reinsurance Providers

Fidelity National Financial (FNF), particularly within its F&G segment, uses flow reinsurance. This means FNF relies on reinsurance providers to transfer risk, which can give these providers a degree of bargaining power. The terms and pricing of these reinsurance contracts are therefore influenced by the concentration and overall market conditions within the global reinsurance industry.

Several factors contribute to the bargaining power of reinsurance providers. These include:

- Concentration of Reinsurers: A smaller number of large, dominant reinsurers can exert more influence over pricing and contract terms.

- Market Conditions: Periods of high catastrophe losses or reduced underwriting capacity in the reinsurance market can lead to higher prices and more restrictive terms for cedents like FNF.

- Availability of Alternatives: If FNF has limited alternative reinsurance options, the bargaining power of existing providers increases.

In 2024, the global reinsurance market continued to navigate a complex landscape. While some segments saw capacity return, others remained constrained, particularly in property catastrophe lines. This dynamic can shift the balance of power, making it crucial for companies like FNF to manage their reinsurance relationships strategically.

Supplier Power Shifts: FNF's 2024 Landscape

The bargaining power of suppliers for Fidelity National Financial (FNF) is generally low, primarily due to the fragmented nature of its core suppliers like abstractors and title plants. However, specialized data providers and reinsurance companies can exert more influence. In 2024, the demand for advanced analytics and AI solutions gave technology suppliers an edge, potentially increasing costs for FNF. Similarly, the reinsurance market's capacity and conditions in 2024 influenced the terms FNF could secure.

| Supplier Type | Bargaining Power Factor | 2024 Impact |

|---|---|---|

| Abstractors/Title Plants | High Fragmentation | Low Power |

| Data & Analytics Providers | Demand for Specialization (AI/Analytics) | Moderate to High Power |

| Reinsurance Providers | Market Capacity & Catastrophe Losses | Moderate to High Power |

What is included in the product

This analysis delves into the competitive forces impacting Fidelity National Financial, examining the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry within the title insurance and real estate services sectors.

Instantly grasp the competitive landscape of the title insurance industry, identifying key pressures to proactively address potential threats and capitalize on opportunities.

Customers Bargaining Power

Fragmented Customer Base (Residential)

For residential title insurance, Fidelity National Financial's (FNF) customers are primarily individual homebuyers and mortgage lenders. While lenders can exert some influence due to the potential for repeat business, the bargaining power of individual homebuyers is generally quite low. Title insurance is a mandated component of most real estate transactions, and it's often viewed by consumers as a standardized product, limiting their ability to negotiate prices or terms.

Lender Influence

Mortgage lenders, acting as substantial and recurring clients for Fidelity National Financial (FNF), wield considerable bargaining power. Their significant transaction volumes allow them to negotiate terms, potentially impacting FNF's pricing and service agreements.

These lenders frequently specify preferred title insurance providers or maintain long-standing partnerships, which can directly influence FNF's opportunities to secure new business and retain existing client relationships.

Commercial Customer Sophistication

Commercial real estate clients, such as major developers and institutional investors, often possess enhanced bargaining power. Their transactions are typically large and intricate, allowing them to negotiate terms more effectively and compare service offerings from various providers. For instance, in 2024, the average deal size for institutional investors in commercial real estate remained substantial, indicating their capacity to influence pricing and contract conditions.

Price Sensitivity and Transparency

The bargaining power of customers in the title insurance sector, particularly concerning price sensitivity and transparency, is a significant factor for companies like Fidelity National Financial. There’s an ongoing discussion about how clear and competitive title insurance pricing truly is. Consumer advocacy groups are pushing for more straightforward pricing and potential changes that could reduce overall closing costs for homebuyers.

This heightened focus on pricing could make customers more sensitive to the costs associated with title insurance. For instance, in 2023, the average closing costs for a home purchase in the U.S. were estimated to be around $6,000, with title insurance being a substantial component of that. This figure highlights the potential impact of price changes on consumers.

- Increased Scrutiny: Consumer groups are actively questioning the pricing structures of title insurance.

- Advocacy for Reform: There's a push for greater transparency and potential reforms to lower closing costs.

- Price Sensitivity: Homebuyers are becoming more aware of and sensitive to the costs of title insurance.

- Impact on Costs: Changes in pricing transparency could directly influence the affordability of homeownership.

Technology-Enabled Comparison

The proliferation of PropTech platforms significantly enhances the bargaining power of customers. These digital marketplaces, which saw substantial investment and growth throughout 2023 and into early 2024, provide unprecedented access to information and comparison tools for real estate services. For instance, platforms like Zillow and Redfin offer detailed property data and agent reviews, enabling consumers to easily compare service providers and pricing. This transparency directly challenges traditional service models by allowing buyers and sellers to more readily identify and negotiate for better rates and terms. In 2023, the online real estate market continued its expansion, with a notable increase in user engagement on these comparison-focused platforms.

This technology-enabled comparison empowers customers by:

- Increased Transparency: PropTech platforms provide easy access to service provider information, pricing, and customer reviews, reducing information asymmetry.

- Enhanced Comparison Tools: Digital marketplaces allow for side-by-side comparisons of real estate agents, mortgage lenders, and title companies based on various metrics.

- Greater Negotiation Leverage: Armed with readily available market data and competitor offerings, customers can negotiate more effectively for favorable rates and service agreements.

- Shift in Market Dynamics: The ease of comparison incentivizes service providers to offer competitive pricing and superior service to attract and retain clients in a more transparent market.

Customer Power: Varied Leverage in Real Estate

Fidelity National Financial (FNF) faces varying degrees of customer bargaining power across its segments. Individual homebuyers generally have low power due to the mandated nature of title insurance and its perception as a standardized service, limiting price negotiation. However, large commercial clients and institutional investors, engaging in substantial transactions, possess significant leverage to negotiate terms and pricing, as evidenced by the continued high average deal sizes in commercial real estate in 2024.

The increasing influence of PropTech platforms amplifies customer bargaining power by offering enhanced transparency and comparison tools. These platforms allow consumers to easily evaluate service providers, including title insurance companies, leading to greater price sensitivity and a demand for competitive offerings. This trend is supported by the continued growth of online real estate markets and user engagement on comparison-focused platforms observed through 2023.

| Customer Segment | Bargaining Power Level | Key Influencing Factors |

|---|---|---|

| Individual Homebuyers | Low | Mandatory purchase, perceived standardization, low transaction volume per buyer |

| Mortgage Lenders | High | Repeat business potential, significant transaction volumes, ability to specify preferred providers |

| Commercial Clients/Institutional Investors | High | Large transaction values, complex needs, ability to compare multiple providers, 2024 average deal sizes remain substantial |

| PropTech Platform Users | Increasingly High | Access to price comparison, transparency, detailed reviews, negotiation leverage |

Preview the Actual Deliverable

Fidelity National Financial Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces Analysis for Fidelity National Financial, offering a detailed examination of competitive forces within the title insurance and transaction services industry. The document you see here is precisely the same professionally formatted analysis you will receive instantly upon purchase, ensuring full transparency and immediate usability.

Rivalry Among Competitors

Market Concentration

The title insurance sector is quite concentrated, featuring major players like First American Title Insurance Company, Old Republic National Title Insurance Company, and Stewart Title Guaranty Company, all competing fiercely with Fidelity National Financial (FNF). This means FNF faces significant rivalry from established, well-resourced competitors.

Service Quality and Coverage

Competitive rivalry in the title insurance sector is intense, with companies like Fidelity National Financial (FNF) vying for market share based on service quality, coverage breadth, and pricing. Differentiation often hinges on streamlined processing and robust policy options to attract and retain customers.

In 2024, the title insurance industry continues to see strong competition. Fidelity National Financial, a major player, competes against companies such as Old Republic Title and First American Title. The focus remains on providing superior customer service, rapid turnaround times, and comprehensive title search and examination services to gain an edge.

Technology Adoption and Innovation

Fidelity National Financial faces intense competition as rivals aggressively adopt new technologies. Companies are investing heavily in automation, artificial intelligence, and big data analytics to speed up title searches and underwriting processes. This technological race aims to boost efficiency and create a superior customer experience, putting pressure on FNF to keep pace.

Impact of Real Estate Market Cycles

The competitive rivalry within the title insurance industry, as experienced by Fidelity National Financial, is significantly shaped by the ebb and flow of the real estate and mortgage markets. When transaction volumes decline, such as during periods of rising interest rates or economic slowdown, the fight for each piece of business becomes fiercer. This intensified competition can put pressure on pricing and margins for all players.

Conversely, during real estate market upturns, when sales and refinancing activity surge, the competitive pressure can somewhat ease. For instance, in 2023, while mortgage origination volumes generally decreased compared to the previous year, the housing market still saw substantial activity, albeit with regional variations. This environment means that while there's more business to go around, the underlying cyclicality still dictates the intensity of competition.

- Market Volatility: Real estate cycles directly impact demand for title insurance, leading to periods of heightened and diminished competition.

- Pressure on Margins: During downturns, companies like Fidelity National Financial may face pressure to lower prices to secure market share, impacting profitability.

- Strategic Adjustments: Companies must adapt their strategies to navigate these cycles, focusing on efficiency and diversification during slower periods.

- 2024 Outlook: Analysts in early 2024 projected a stabilization or modest recovery in mortgage origination volumes, potentially easing some competitive pressures compared to late 2023, though the overall economic climate remained a key factor.

Geographic Reach and Underwriting Capacity

Fidelity National Financial (FNF) boasts a formidable competitive advantage through its vast geographic reach and substantial underwriting capacity. As the nation's largest title insurance company, FNF operates an extensive network of title insurance underwriters and subsidiaries spanning the United States.

- Extensive Underwriter Network: FNF's ability to underwrite policies across a wide geographic area is supported by its numerous licensed underwriters and subsidiaries.

- Market Dominance: In 2023, FNF held a significant share of the title insurance market, demonstrating its capacity to handle a large volume of transactions nationwide.

- Capacity for Large Transactions: This broad reach and deep underwriting bench allow FNF to effectively service both local and large-scale national real estate transactions, a key differentiator in the industry.

Title Insurance Giants Clash: Innovation and Market Share

The competitive rivalry within the title insurance sector is intense, with Fidelity National Financial (FNF) facing strong opposition from established giants like First American Title and Old Republic Title. This competition is not just about price, but also about delivering superior service, offering broad coverage, and streamlining processes through technological innovation.

In 2024, companies like FNF are heavily investing in AI and automation to quicken title searches and underwriting, aiming to enhance efficiency and customer experience. This technological arms race means FNF must continuously innovate to maintain its market position. The cyclical nature of the real estate market also amplifies this rivalry, as periods of lower transaction volumes intensify the fight for market share and can pressure profit margins.

Fidelity National Financial's position as the largest title insurance company in the U.S. provides a significant advantage, bolstered by its extensive network of underwriters and substantial underwriting capacity. This allows FNF to handle a wide range of transactions, from local deals to large national ones, a key factor in its competitive standing.

| Competitor | Approximate Market Share (2023) | Key Competitive Focus |

|---|---|---|

| Fidelity National Financial (FNF) | ~35-40% | Scale, technology, underwriting capacity |

| First American Title Insurance Company | ~25-30% | Technology, customer service, data analytics |

| Old Republic National Title Insurance Company | ~15-20% | Underwriting expertise, financial strength, agent relationships |

| Stewart Title Guaranty Company | ~5-10% | Customer service, regional strength, specialized services |

SSubstitutes Threaten

Attorney Opinion Letters (AOLs)

Attorney Opinion Letters (AOLs) are emerging as a potential substitute for traditional title insurance, especially following new guidelines from Fannie Mae and Freddie Mac. This shift offers a different way to confirm property titles, potentially impacting the demand for existing title insurance products.

The adoption of AOLs could reduce the market share for traditional title insurance providers like Fidelity National Financial. While specific 2024 adoption rates for AOLs in lieu of title insurance are still developing, the regulatory push suggests a growing acceptance of this alternative.

Blockchain and Smart Contracts

Blockchain and smart contracts present a significant threat by enabling direct, secure, and transparent property transactions. This technology can automate processes typically handled by intermediaries, potentially bypassing traditional title insurance services. For instance, smart contracts could automatically transfer property ownership upon fulfillment of predefined conditions, reducing reliance on title insurers for verification and escrow services.

Direct-to-Consumer Digital Platforms

Direct-to-consumer digital platforms, including PropTech innovators, present a growing threat by simplifying property searches and enabling digital transactions. These platforms can bypass traditional intermediaries, offering a more streamlined experience for consumers, even if their current service scope is narrower than established title companies. For instance, in 2024, the real estate technology sector continued its expansion, with significant investment flowing into companies aiming to digitize the home buying process from start to finish.

Government-Sponsored Enterprise (GSE) Waivers

The Federal Housing Finance Agency's (FHFA) revival of its title waiver pilot program poses a significant threat. This initiative aims to cut costs for certain refinance transactions by waiving the requirement for lender's title insurance. This directly targets a segment of Fidelity National Financial's (FNF) market, offering a lower-cost alternative for consumers and lenders.

This waiver program, particularly its expansion or continued implementation, creates a substitute for traditional title insurance services. For instance, if the pilot proves successful and becomes more widespread, it could lead to a reduction in the volume of title insurance policies written by companies like FNF.

The potential impact is substantial, as title insurance is a core revenue stream for FNF. Data from 2024 indicates that the mortgage industry is sensitive to cost-saving measures, making such waivers an attractive proposition.

- FHFA Title Waiver Pilot: A direct substitute threat by reducing or eliminating lender's title insurance on specific refinance deals.

- Cost Reduction Incentive: Appeals to lenders and borrowers seeking to lower closing costs in the current economic climate.

- Market Share Erosion: Potential for a portion of FNF's title insurance business to be captured by this waiver program.

- 2024 Mortgage Market Sensitivity: Increased focus on efficiency and cost savings within the mortgage sector amplifies the threat.

Enhanced Public Record Accessibility

Enhanced public record accessibility, driven by digitization and centralized databases, presents a potential threat to title insurance providers. As land records become more readily available and reliable, the perceived need for extensive title searches and insurance might diminish, as potential title defects could be identified more easily and at a lower cost.

This trend could lead to a reduction in demand for traditional title insurance services. For instance, in 2024, several states continued to invest in modernizing their county-level land record systems, aiming for greater online accessibility and searchability.

- Digitization Efforts: Increased investment in digitizing historical land records is making them more accessible.

- Centralized Databases: The creation of unified, searchable land record databases simplifies the title search process.

- Reduced Information Asymmetry: Easier access to reliable data lowers the barrier for buyers and legal professionals to identify potential title issues.

- Potential Cost Savings: Streamlined searches could reduce the overall cost of property transactions, impacting the value proposition of title insurance.

Evolving Title Verification: New Threats to Traditional Insurance

The threat of substitutes for traditional title insurance is evolving, with regulatory changes and technological advancements offering alternative pathways for property title verification. The FHFA's title waiver pilot program, which waives lender's title insurance for certain refinances, directly substitutes for a portion of FNF's business. In 2024, the mortgage market's focus on cost reduction made such waivers particularly appealing, potentially impacting FNF's revenue from this segment.

Attorney Opinion Letters (AOLs) are also gaining traction as a substitute, especially with Fannie Mae and Freddie Mac's updated guidelines. While adoption rates for AOLs in 2024 are still materializing, the regulatory support suggests a growing acceptance that could erode traditional title insurance market share. Furthermore, advancements in blockchain and direct-to-consumer digital platforms are streamlining property transactions, potentially bypassing traditional title insurance altogether.

Digitization of public land records is another significant substitute threat. As records become more accessible and reliable, the perceived necessity and value of extensive title searches conducted by insurers may diminish. Many states continued to invest in modernizing these systems in 2024, enhancing online accessibility and searchability, which could lead to reduced demand for FNF's core services.

| Substitute | Mechanism | Potential Impact on FNF | 2024 Relevance |

|---|---|---|---|

| FHFA Title Waiver Pilot | Waives lender's title insurance for specific refinances | Reduces policy volume and revenue | Increased focus on cost savings in mortgage market |

| Attorney Opinion Letters (AOLs) | Alternative title verification method | Erodes market share for traditional title insurance | Growing regulatory acceptance (Fannie Mae/Freddie Mac) |

| Blockchain/Smart Contracts | Automates secure property transactions | Bypasses intermediaries, reduces reliance on insurers | Continued innovation in PropTech |

| Digital Platforms/PropTech | Streamlines property search and transactions | Offers simplified, potentially lower-cost alternatives | Sector expansion and investment |

| Public Record Digitization | Increases accessibility and reliability of land records | Diminishes perceived need for extensive title searches | State investments in record modernization |

Entrants Threaten

High Capital Requirements

Entering the title insurance sector demands significant financial resources. Companies need substantial capital for underwriting reserves, ensuring they can cover potential claims. For instance, in 2023, the title insurance industry in the U.S. reported direct premiums written of approximately $25.6 billion, indicating the scale of financial backing required.

Beyond reserves, regulatory compliance across various states necessitates considerable investment. Establishing a broad operational network to serve diverse geographic markets also adds to the upfront capital expenditure, posing a formidable hurdle for potential new entrants.

Regulatory Complexity and Licensing

The title insurance sector is deeply entwined with state-level regulations, dictating everything from licensing requirements and the management of escrow funds to the maintenance of premium reserves. This intricate web of rules creates a significant hurdle for any company looking to enter the market.

For instance, in 2024, navigating these varying state regulations, which can differ substantially in their stringency and specific demands, requires substantial legal and compliance investment. New entrants must dedicate considerable resources to understand and adhere to these diverse frameworks, making market entry a costly and time-consuming endeavor.

Established Brand Recognition and Trust

Established players like Fidelity National Financial (FNF) benefit from decades of ingrained brand recognition and deep-seated trust within the real estate and lending sectors. This makes it incredibly challenging for newcomers to rapidly acquire market share and build the necessary credibility. For instance, FNF's long-standing presence has cultivated strong relationships with real estate agents, mortgage brokers, and title companies, creating a significant barrier to entry.

Economies of Scale and Network Effects

Large, established players like Fidelity National Financial (FNF) possess significant advantages due to economies of scale. FNF's extensive infrastructure for processing transactions and its broad network of agents and offices contribute to operational efficiencies that are difficult for newcomers to match. This scale allows for lower per-unit costs in areas like technology development and customer service.

Network effects further bolster FNF's position. The more agents and customers that utilize FNF's services, the more valuable those services become to all participants. This creates a powerful barrier, as new entrants would need to build a comparable network from scratch, a costly and time-consuming endeavor. For instance, in the title insurance sector, a larger agent network often translates to quicker closing times and wider geographic reach, which are highly attractive to real estate professionals and consumers.

- Economies of Scale: FNF leverages its size for cost efficiencies in transaction processing and operational overhead.

- Network Effects: A larger base of agents and customers increases the value proposition for all users, deterring new entrants.

- Market Coverage: FNF's established presence across numerous geographic regions provides a competitive edge that new firms would find challenging to replicate quickly.

Technological Investment and Expertise

The threat of new entrants in the title insurance and transaction services sector, particularly concerning technological advancements, is moderated by substantial barriers related to investment and expertise. Developing and deploying advanced PropTech solutions, artificial intelligence, and sophisticated data analytics, as FNF and its peers do, requires considerable financial outlay and highly specialized knowledge. For instance, companies looking to compete on technological grounds would need to invest heavily in R&D, cybersecurity infrastructure, and skilled personnel, potentially running into tens of millions of dollars annually.

Newcomers face a steep climb in matching the technological capabilities and operational efficiencies of established players like Fidelity National Financial. The sheer cost of acquiring or developing the necessary AI algorithms for risk assessment or the data analytics platforms for market insights can be prohibitive. In 2024, the average investment in technology for large financial services firms often exceeded 15% of their operating budget, a figure that would be challenging for a new entrant to replicate without significant backing.

- High Capital Requirements: Significant upfront investment is needed for proprietary software development, AI integration, and robust data infrastructure.

- Specialized Talent Gap: Acquiring and retaining experts in PropTech, AI, and data science is crucial but difficult due to high demand and competitive salaries.

- Regulatory Hurdles: Navigating compliance and data privacy regulations for new technological solutions adds complexity and cost for potential entrants.

- Economies of Scale: Established firms benefit from existing technological investments spread across a larger customer base, creating a cost advantage for new entrants to overcome.

Title Insurance: A Fortress Against New Competitors

The threat of new entrants in the title insurance sector is significantly low due to high capital requirements and established brand loyalty. For instance, the U.S. title insurance industry's direct premiums written reached approximately $25.6 billion in 2023, underscoring the substantial financial backing needed. New companies must also navigate complex state-specific regulations, demanding considerable investment in legal and compliance expertise.

Established players like Fidelity National Financial (FNF) benefit from strong brand recognition and extensive networks, making it difficult for newcomers to gain traction. FNF's decades of operation have fostered deep relationships with real estate professionals, creating a significant barrier. Furthermore, economies of scale allow FNF to operate more efficiently, a cost advantage that new entrants struggle to match.

Technological advancements, while offering potential disruption, also present high entry barriers. Developing and implementing advanced PropTech, AI, and data analytics requires substantial financial investment and specialized talent, often exceeding tens of millions of dollars annually. In 2024, many large financial services firms allocated over 15% of their operating budgets to technology, a benchmark difficult for new entrants to meet.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Fidelity National Financial leverages a comprehensive suite of data, including their annual reports, SEC filings, and industry-specific market research from sources like IBISWorld and Statista. This ensures a robust understanding of competitive dynamics.