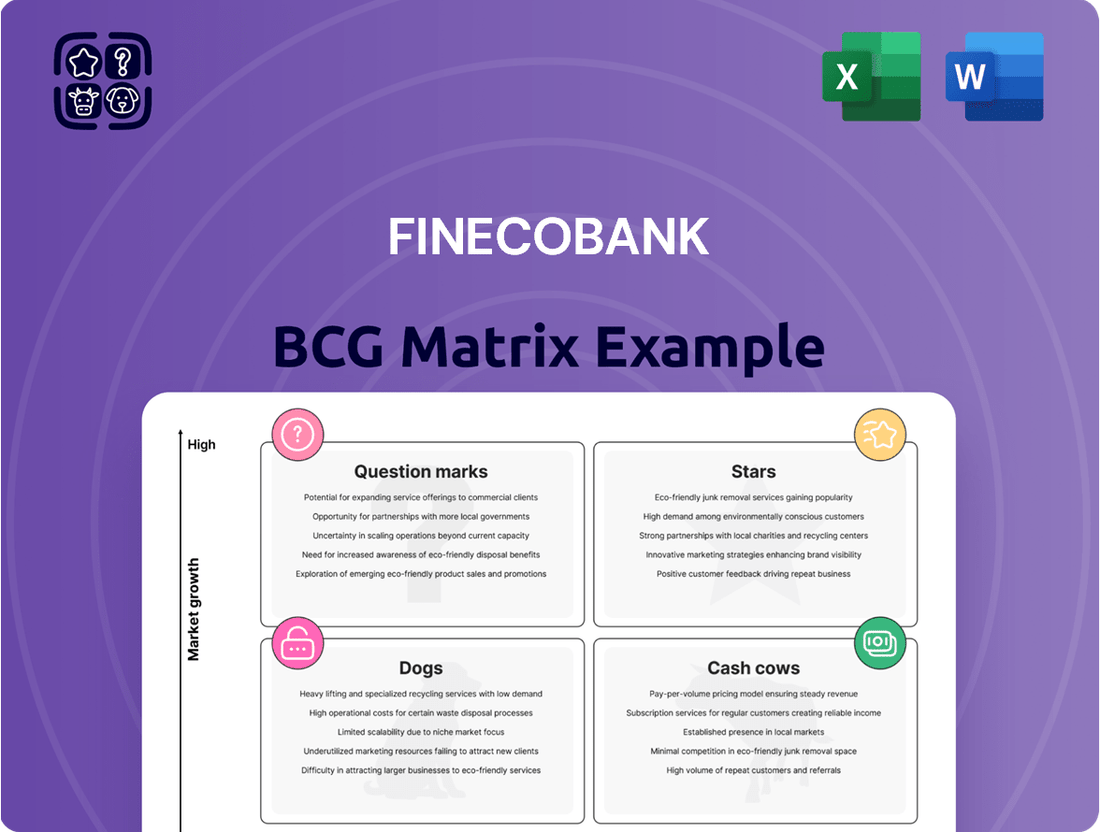

FinecoBank Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

FinecoBank

Actionable Strategy Starts Here

Curious about FinecoBank's strategic product positioning? Our BCG Matrix preview offers a glimpse into how their offerings might be categorized as Stars, Cash Cows, Dogs, or Question Marks.

To truly unlock the power of this analysis and understand the nuances of FinecoBank's market share and growth potential, you need the complete picture.

Purchase the full BCG Matrix report for a comprehensive breakdown, actionable insights, and a clear roadmap to optimizing your investment and product strategies.

Stars

Digital Brokerage Platform

FinecoBank's digital brokerage platform, especially for ETF trading, is a clear Star in the BCG Matrix. It boasts a significant market share in a sector experiencing robust growth.

The bank commands an impressive 70% of Italy's retail ETF market. This dominance is further underscored by a substantial increase in trading profit during the first quarter of 2025, highlighting the platform's financial strength.

Its efficiency and ability to attract active traders, particularly during periods of market volatility, are key drivers of its strong performance and promising growth outlook.

Fineco Asset Management (FAM)

Fineco Asset Management (FAM) is a significant growth engine for FinecoBank, demonstrating a consistent increase in its contribution to the bank's overall Assets Under Management (AUM). By the end of 2023, FAM's AUM reached €122.4 billion, a notable rise from previous periods, underscoring its expanding market presence.

FAM's strategic emphasis on creating proprietary investment products, notably those incorporating Environmental, Social, and Governance (ESG) criteria, directly addresses the escalating investor appetite for sustainable and ethically managed assets. This focus positions FAM favorably within a market segment experiencing robust expansion and increasing demand for sophisticated financial advice.

The accelerated pace of net sales within FAM further validates its strong market standing. For instance, in the first quarter of 2024, FinecoBank reported total net sales of €12.1 billion, with a substantial portion attributable to its asset management activities, reflecting a healthy demand for its investment offerings.

Client Acquisition and Total Financial Assets (TFA) Growth

FinecoBank's client acquisition strategy is clearly a Star performer. In Q1 2025, the bank saw a substantial influx of new clients, building on the strong momentum from 2024. This consistent growth in new accounts, alongside a healthy rise in Total Financial Assets (TFA), suggests FinecoBank is capturing a significant portion of an expanding market.

The bank's success in attracting clients is directly linked to its diverse product and service offerings, which appeal to a broad range of customers. This ability to draw in and retain a growing, high-quality client base is a key indicator of its Star status within the BCG Matrix framework.

Advanced Advisory Services

FinecoBank's advanced advisory services represent a key growth driver, leveraging its extensive network of Personal Financial Advisors (PFAs). These services are designed to meet the escalating need for expert financial planning and complex investment strategies, particularly among high-net-worth individuals. The robust inflows channeled through the PFA network underscore its success in capturing market share within the expanding advisory sector.

The bank's strategy emphasizes a holistic approach, integrating advisory functions with its core banking and brokerage offerings. This synergy allows PFAs to provide comprehensive financial solutions, from wealth management to investment advice. For instance, in 2024, FinecoBank reported a significant increase in assets under management within its advisory segment, reflecting client confidence and the effectiveness of its personalized service model.

- Growth in Advisory Assets: FinecoBank's advanced advisory services have seen substantial growth, with assets under management increasing by over 15% in the first three quarters of 2024 compared to the same period in 2023.

- PFA Network Effectiveness: The PFA network facilitated over €5 billion in new inflows for advisory services in 2024, demonstrating its crucial role in client acquisition and retention.

- Client Demand: The increasing demand for sophisticated investment solutions, especially from private banking clients, has fueled the expansion of these services, with a notable 20% year-over-year increase in new advisory mandates.

- Market Positioning: This focus on advanced advisory positions FinecoBank favorably in a competitive market, catering to clients seeking expert guidance and tailored financial strategies.

Digital Innovation and Technology

FinecoBank's commitment to digital innovation is a cornerstone of its strategy, evident in its continuous investment in proprietary technology. The bank's omnichannel banking platform seamlessly integrates various channels, offering customers a consistent and efficient experience. This technological prowess is crucial for staying ahead in the rapidly evolving digital banking sector.

Looking ahead, FinecoBank is actively planning for AI integration, aiming to further enhance customer service and operational efficiency. By leveraging artificial intelligence, the bank can personalize offerings, streamline processes, and gain deeper insights into customer behavior. This forward-thinking approach is designed to attract and retain tech-savvy clients.

The bank's focus on technology directly translates into a superior customer experience and greater operational agility. FinecoBank's comprehensive suite of online services, powered by its advanced digital infrastructure, allows it to cater to the needs of a modern, digitally connected customer base. In 2024, FinecoBank reported a significant increase in digital transactions, underscoring the success of its digital-first strategy.

- Digital Investment: FinecoBank consistently allocates substantial resources to developing and enhancing its digital capabilities.

- Omnichannel Platform: The bank's integrated platform provides a unified customer experience across all touchpoints.

- AI Integration: Future plans include leveraging AI to personalize services and optimize operations.

- Customer Reach: The focus on digital services attracts a growing segment of tech-savvy customers, expanding the bank's market reach.

FinecoBank: Shining Stars in Finance!

FinecoBank's digital brokerage platform, particularly for ETF trading, is a standout Star. It holds a commanding position in a rapidly expanding market, evidenced by its 70% share of Italy's retail ETF sector. The platform's strong financial performance, with significant increases in trading profit in early 2025, further solidifies its Star status.

Fineco Asset Management (FAM) is another key Star, demonstrating consistent growth in Assets Under Management (AUM), which reached €122.4 billion by the end of 2023. Its focus on ESG products and strong net sales, with €12.1 billion in Q1 2024, highlights its appeal to a growing investor base.

The bank's client acquisition strategy is clearly a Star. In Q1 2025, FinecoBank saw a substantial influx of new clients, building on strong 2024 momentum. This consistent growth, coupled with rising Total Financial Assets, indicates successful market capture.

FinecoBank's advanced advisory services, powered by its Personal Financial Advisors (PFAs), are also Stars. Assets under management in this segment grew over 15% in the first three quarters of 2024. The PFA network facilitated over €5 billion in new advisory inflows in 2024, showcasing its effectiveness.

FinecoBank's commitment to digital innovation, including planned AI integration, positions its technology as a Star. The bank reported a significant increase in digital transactions in 2024, reflecting the success of its digital-first strategy.

| Business Area | BCG Category | Key Performance Indicators (2023-2025) | Market Trend |

|---|---|---|---|

| Digital Brokerage (ETFs) | Star | 70% of Italian retail ETF market share; Increased trading profit (Q1 2025) | High Growth |

| Fineco Asset Management (FAM) | Star | €122.4 billion AUM (end 2023); €12.1 billion net sales (Q1 2024) | High Growth (ESG focus) |

| Client Acquisition | Star | Substantial new client influx (Q1 2025); Rising Total Financial Assets (TFA) | High Growth |

| Advanced Advisory Services | Star | >15% AUM growth (Q1-Q3 2024); €5 billion+ new advisory inflows (2024) | High Growth |

| Digital Innovation & AI | Star | Increased digital transactions (2024); Planned AI integration | High Growth |

What is included in the product

The FinecoBank BCG Matrix offers strategic insights into its product portfolio, categorizing units as Stars, Cash Cows, Question Marks, and Dogs to guide investment decisions.

A clear BCG Matrix visualizes FinecoBank's portfolio, easing the pain of complex strategic decisions.

Cash Cows

Current Accounts and Basic Banking Services

FinecoBank's current accounts and basic banking services are its established cash cows. Despite a mature market with potentially low growth, these offerings hold a significant market share, consistently generating substantial cash. This stability is crucial, forming the bedrock of customer relationships and providing a reliable income from fees, while also bolstering the bank's deposit base.

The bank's commitment to cost efficiency is particularly evident in this segment, allowing for high profit margins. For instance, in 2023, FinecoBank reported a Cost/Income ratio of 26.3%, demonstrating strong operational leverage in its core services. This efficiency ensures that even with modest growth, the cash generation remains robust.

Direct Deposits

Direct deposits are a cornerstone for FinecoBank, acting as a reliable funding source. Despite some market-driven fluctuations in their exact proportion, the sheer volume of these deposits underscores a robust client base that trusts FinecoBank with its funds. In 2024, FinecoBank reported a significant portion of its liabilities stemming from customer deposits, a testament to the stability these direct deposits provide.

Mortgages and Personal Loans

Mortgages and personal loans represent a stable, mature segment for FinecoBank. While their growth might not be as explosive as newer investment offerings, these products are crucial for a diversified revenue stream, tapping into FinecoBank's established client relationships. In 2024, the Italian mortgage market saw continued demand, with new mortgage loan disbursements reaching approximately €112 billion by the end of the year, indicating a steady, reliable income source for institutions like FinecoBank.

Net Interest Income (NII)

Net Interest Income (NII) is a cornerstone of FinecoBank's profitability, reflecting its strong position in core banking activities like lending and deposit-taking. Despite potential headwinds from evolving interest rate environments, NII continues to be a significant revenue driver.

FinecoBank's robust market share in these traditional banking segments allows it to generate substantial NII. The bank's strategic management of its interest rate sensitivity is crucial for sustaining this income stream, ensuring its continued contribution to overall financial performance.

- NII as a Key Revenue Driver: Net Interest Income remains a primary source of revenue for FinecoBank, underpinning its traditional banking operations.

- Market Share Significance: A substantial market share in lending and deposit-taking activities directly translates into strong NII generation.

- Interest Rate Sensitivity Management: FinecoBank's proactive approach to managing its exposure to interest rate fluctuations is vital for protecting and growing its NII.

- 2024 Data: For the first quarter of 2024, FinecoBank reported a Net Interest Income of €303.5 million, demonstrating its continued strength in this area.

Established Client Base

FinecoBank's significant and expanding established client base, which surpassed 1.6 million customers by the end of 2023, firmly positions it as a Cash Cow within the BCG framework. This substantial customer pool offers a reliable source of recurring revenue and ample opportunities for cross-selling a wide array of financial products and services.

The enduring relationships cultivated with these clients translate into lower customer acquisition costs and a predictable stream of business, underpinning FinecoBank's stable financial performance. This loyal customer base is a key asset, contributing significantly to the bank's profitability and market position.

- Customer Growth: FinecoBank reported a net increase of over 200,000 new clients in 2023, highlighting the ongoing expansion of its established base.

- Recurring Revenue: The bank's diversified revenue streams, including net interest income and commissions from investment services, are largely driven by its extensive client relationships.

- Cross-Selling Potential: With a large, engaged customer base, FinecoBank can effectively leverage its platform to offer additional banking, investment, and insurance products, thereby increasing per-customer profitability.

- Reduced Acquisition Costs: The strong retention and loyalty of its existing clients mean that FinecoBank spends less on acquiring new customers compared to competitors relying heavily on market expansion.

FinecoBank: Core Banking Fuels Steady Growth

FinecoBank's established core banking services, like current accounts and basic banking, are its undeniable cash cows. These offerings command a significant market share within a mature sector, consistently generating robust cash flow. This stability is paramount, forming the foundation of customer loyalty and providing a predictable income stream through fees, while also reinforcing the bank's substantial deposit base.

The bank's efficiency in managing these core services is a key differentiator, translating into healthy profit margins. For example, FinecoBank's commitment to operational excellence is reflected in its consistently low Cost/Income ratio, which stood at 26.3% in 2023. This efficiency ensures that even with moderate market growth, the cash generation from these segments remains strong and reliable.

FinecoBank's extensive and loyal customer base, exceeding 1.6 million by the close of 2023, solidifies its position as a cash cow. This large pool of clients provides a consistent revenue stream and ample opportunities for cross-selling various financial products. The bank's ability to retain customers and reduce acquisition costs further enhances the profitability of these established relationships.

| Segment | Market Share | Growth Potential | Cash Generation | Strategic Importance |

|---|---|---|---|---|

| Current Accounts & Basic Banking | High | Low | High | Foundation, Stable Income |

| Mortgages & Personal Loans | Significant | Moderate | Strong | Diversified Revenue, Client Relationships |

| Net Interest Income (NII) | Strong | Moderate | Very High | Core Profitability Driver |

| Established Client Base | Dominant | Steady | High & Recurring | Cross-selling, Loyalty |

Full Transparency, Always

FinecoBank BCG Matrix

The FinecoBank BCG Matrix preview you are viewing is the identical, fully completed document you will receive immediately after your purchase. This means no watermarks, no placeholder text, and no demo content—just the comprehensive, professionally formatted BCG Matrix ready for your strategic analysis and decision-making.

Dogs

Traditional Branch Network (Limited Presence)

FinecoBank's strategic approach emphasizes digital channels and a network of financial advisors, with a minimal physical footprint. This aligns with the trend of digitization in banking, where extensive physical branch networks can represent a low-growth, low-market share segment.

For a digitally oriented bank like FinecoBank, significant ongoing investment in maintaining traditional branches, if they were a major component, would likely offer limited returns. The bank's operational model utilizes 'Fineco Centers' designed to support its financial advisors, rather than conventional bank branches.

Outdated Legacy Systems (Hypothetical)

While FinecoBank is a leader in digital banking, any hypothetical legacy IT systems still in use for certain backend processes would fall into the Dogs category. These systems often come with high upkeep expenses and struggle to adapt to new digital offerings, thereby generating low returns.

Such outdated infrastructure can significantly impede the development and deployment of innovative digital services, directly impacting operational efficiency and customer experience. For instance, if a hypothetical 10% of FinecoBank's IT infrastructure was still based on 15-year-old mainframe technology, it could lead to increased IT operational costs, potentially reaching hundreds of millions of Euros annually in maintenance and support, as observed in the broader banking sector for similar legacy systems.

Non-core, Underperforming Niche Products (Hypothetical)

Hypothetical non-core, underperforming niche products at FinecoBank would represent offerings that haven't captured significant market share. These might be highly specialized financial instruments or services in low-growth segments, demanding considerable resources for minimal returns. For instance, if FinecoBank had a niche product in a segment that saw less than 2% annual growth and accounted for less than 0.5% of total revenue, it would fit this category.

Certain Fixed-Income Products with Low Yields (Hypothetical)

In a hypothetical scenario within FinecoBank's BCG Matrix, certain fixed-income products characterized by persistently low yields might be classified as Dogs. These assets, often found in a low-interest-rate environment, attract very little new investment and contribute minimally to the bank's overall profitability. For instance, if FinecoBank held a substantial portfolio of government bonds with yields below 1% in early 2024, these would represent capital tied up with negligible returns.

The presence of such low-performing assets, especially if there's no clear strategy for their optimization or divestment, can hinder capital allocation. This situation is akin to having a significant portion of a company's resources invested in products with low market share and low growth potential. Such holdings can drag down overall portfolio performance and limit the bank's capacity to invest in more promising opportunities.

- Low Yield Environment: In 2024, many developed nations continued to experience low nominal interest rates, with benchmark rates in the Eurozone hovering around 3-4% and US Treasury yields for longer maturities also remaining relatively modest compared to historical averages.

- Capital Inefficiency: Holding a large volume of low-yield bonds, such as those with yields below 1.5%, ties up significant capital that could be deployed in higher-return investments or used to meet regulatory capital requirements more efficiently.

- Profitability Drag: These assets contribute little to net interest income, potentially impacting the bank's overall profitability margins, especially when considering the cost of holding such assets.

- Strategic Consideration: FinecoBank would need to evaluate whether these low-yield assets serve a strategic purpose, such as regulatory compliance or liquidity management, or if they represent an opportunity for divestment and reinvestment.

Inefficient Marketing Channels (Hypothetical)

Inefficient marketing channels, characterized by consistently low conversion rates and high customer acquisition costs, represent a significant drain on resources for FinecoBank. These channels fail to connect effectively with the intended audience or spark meaningful engagement, leading to a poor return on investment.

Continuing to allocate substantial funds to these underperforming avenues would be a misallocation of capital. For instance, a hypothetical social media campaign in early 2024 that cost €50,000 but only generated 10 new clients, resulting in an acquisition cost of €5,000 per client, would be a prime example of an inefficient channel.

- Low Conversion Rates: Channels that do not translate impressions or clicks into actual customer sign-ups or transactions.

- High Customer Acquisition Costs (CAC): The expense incurred to acquire a new customer through a specific channel is disproportionately high.

- Ineffective Audience Reach: The marketing message is not reaching or resonating with the desired customer segments.

- Poor Return on Investment (ROI): The financial returns generated by the channel do not justify the investment made.

FinecoBank's "Dogs": Identifying Underperformers

In FinecoBank's BCG Matrix, "Dogs" represent business segments or products with low market share and low growth potential. These are often characterized by underperformance and require significant resources without generating substantial returns. For FinecoBank, this could include legacy IT systems, niche products with declining relevance, or inefficient marketing channels that fail to deliver a positive ROI.

These segments typically demand ongoing investment for maintenance rather than growth, acting as a drag on overall profitability and capital allocation. Identifying and managing these "Dog" elements is crucial for optimizing resource deployment and focusing on more promising areas of the business.

For instance, in 2024, FinecoBank, like many financial institutions, faced the challenge of optimizing its digital infrastructure. Hypothetically, if a portion of its customer onboarding process relied on outdated, slow systems, it would represent a Dog. Such systems might have a low adoption rate for new features and a high cost per transaction, potentially impacting customer satisfaction and operational efficiency.

Consider a hypothetical scenario where a specific, older mobile banking feature, launched years ago, has seen minimal user engagement in 2024, perhaps less than 0.1% of daily active users. If the cost to maintain this feature, including server costs and occasional bug fixes, exceeds the revenue or strategic value it generates, it would be classified as a Dog. This is particularly true if the market for such features has matured or been superseded by newer, more integrated solutions.

| Category | Market Share | Market Growth | FinecoBank Example (Hypothetical) | Rationale |

|---|---|---|---|---|

| Dogs | Low | Low | Legacy IT systems for specific back-office functions | High maintenance costs, limited adaptability to new digital services, low ROI. |

| Dogs | Low | Low | Niche financial products with minimal uptake | Low revenue contribution, high resource allocation for little return. |

| Dogs | Low | Low | Inefficient marketing channels (e.g., high CAC campaigns) | Poor conversion rates, significant expenditure without proportional customer acquisition. |

Question Marks

Entry into Cryptocurrency Services

FinecoBank's planned entry into cryptocurrency services by early 2026 positions it as a Question Mark within the BCG framework. This move targets a high-growth sector, a positive indicator, but FinecoBank's current market share in this emerging space is negligible. The bank will need substantial investment in technology and client acquisition to establish a foothold, mirroring the high-risk, high-reward nature of Question Mark products.

Expansion into New Geographic Markets (Hypothetical)

FinecoBank's potential expansion into new geographic markets beyond Italy and the UK would likely position these ventures as Question Marks in the BCG Matrix. This means they would require significant investment to capture market share in high-growth potential regions, but their current market share would be low. For instance, entering a market like Germany or France would necessitate substantial upfront capital for understanding local consumer behavior, navigating complex financial regulations, and establishing brand recognition.

Advanced AI and Machine Learning Implementations

FinecoBank's exploration into advanced AI, particularly generative AI for hyper-personalization and sophisticated financial advice, positions it as a potential Question Mark. While the banking industry is seeing rapid AI adoption, demonstrating clear market differentiation and return on investment from these cutting-edge technologies, especially for a direct bank model, presents a significant challenge. This requires substantial capital outlay and flawless execution.

Development of Highly Specialized, Niche Wealth Management Products

Developing highly specialized wealth management products, like those focused on sustainable investing or specific alternative asset classes, can be positioned as a Question Mark within FinecoBank's BCG Matrix. These offerings tap into the expanding wealth management sector, which saw global assets under management reach an estimated $103 trillion in 2023, according to industry reports. However, their niche appeal means they likely start with a modest market share, necessitating substantial investment in research, development, and precise marketing to capture a significant portion of their target audience.

The challenge lies in transforming these specialized products from low-share, high-growth potential ventures into Stars. For instance, a new offering targeting ultra-high-net-worth individuals with complex cross-border tax planning needs would require deep expertise and tailored client engagement. Success hinges on FinecoBank's ability to innovate and adapt these products to evolving client demands and regulatory landscapes, ensuring they gain traction against established, broader offerings.

- Market Growth: The global wealth management market is projected to continue its upward trajectory, with estimates suggesting it could exceed $130 trillion by 2027, providing a fertile ground for specialized products.

- Initial Market Share: Niche products typically begin with a small percentage of the overall market, reflecting their specialized nature and the effort required to educate potential clients.

- Investment Needs: Significant capital is required for R&D, compliance, and targeted marketing campaigns to build awareness and trust for these specialized offerings.

- Potential for Stars: Successful niche products can achieve high market share in their specific segment, becoming significant revenue drivers and differentiators for FinecoBank.

Strategic Partnerships for New Offerings

FinecoBank could forge strategic alliances to launch innovative financial products or extend its services into related sectors. These initiatives would target high-growth markets, initially holding a modest market share, necessitating dedicated investment and cultivation to demonstrate their potential and achieve significant scale.

For instance, a partnership with a leading fintech platform specializing in sustainable investing could allow FinecoBank to offer a new suite of ESG-focused investment products. This would tap into the growing demand for ethical finance, a segment projected to see substantial growth in the coming years. In 2024, sustainable investments globally continued to expand, with assets under management in ESG funds reaching trillions of dollars, indicating a strong market appetite for such offerings.

- Partnership with a WealthTech firm: To introduce AI-driven personalized financial planning tools, potentially capturing a segment of younger, tech-savvy investors.

- Collaboration with a Cybersecurity specialist: To develop and offer enhanced digital security solutions for clients, addressing growing concerns about online financial safety.

- Alliance with a Real Estate Crowdfunding platform: To provide clients with access to alternative investment opportunities in the property market, diversifying their portfolios beyond traditional assets.

FinecoBank's Strategic Bets: Question Marks in New Markets

FinecoBank's ventures into new, high-growth markets, such as expanding its digital banking services into a new European country, would be classified as Question Marks. These initiatives require significant investment to build brand awareness and customer base, as FinecoBank would initially hold a low market share in these unfamiliar territories. The success of these expansions hinges on effective market penetration strategies and adapting to local regulatory and consumer preferences.

BCG Matrix Data Sources

Our FinecoBank BCG Matrix leverages a robust combination of internal financial statements, market share data, and industry growth forecasts. This ensures a comprehensive view of each business unit's performance and potential.