Enerpac Tool Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Enerpac Tool Group

Go Beyond the Preview—Access the Full Strategic Report

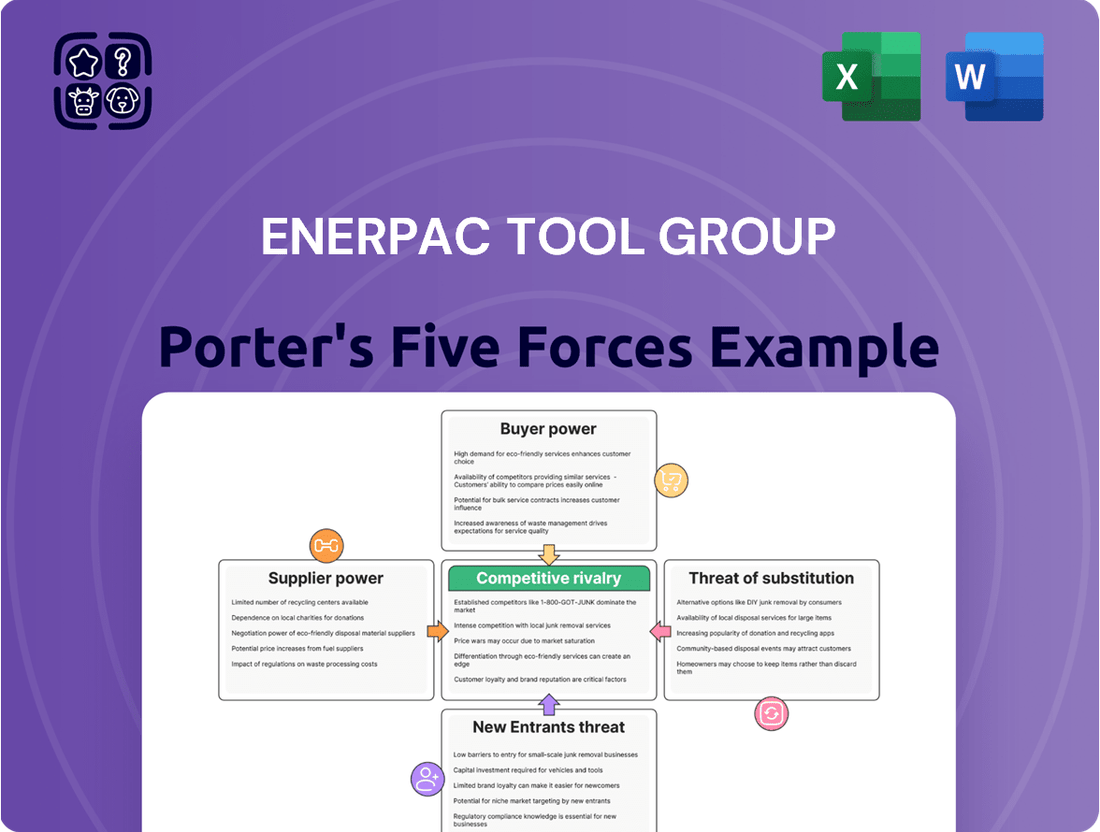

Enerpac Tool Group operates in a landscape shaped by significant buyer power and the constant threat of substitutes, impacting their pricing and product innovation. The intensity of rivalry among existing competitors also plays a crucial role in their market strategy.

The complete report reveals the real forces shaping Enerpac Tool Group’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Suppliers

The bargaining power of suppliers for Enerpac Tool Group is significantly influenced by the concentration of those supplying specialized components. For critical items such as high-pressure hydraulic pumps, cylinders, and precision-engineered parts, if only a limited number of manufacturers exist, these suppliers gain considerable leverage. This concentration can translate into higher costs for Enerpac, as fewer alternatives mean less room for negotiation on pricing and terms.

Uniqueness of Inputs

Suppliers gain significant leverage when they offer unique or highly differentiated inputs that are critical for Enerpac's specialized hydraulic tools and integrated solutions. For instance, if a supplier provides a proprietary alloy or a precision-engineered component essential for the high-pressure performance of Enerpac's pumps, their bargaining power increases substantially.

When these crucial inputs have limited or no viable substitutes, and are indispensable for ensuring the performance, reliability, and safety standards of Enerpac's advanced product lines, suppliers are in a stronger position to dictate terms, including pricing. This is particularly relevant for Enerpac, given its strategic focus on highly engineered, mission-critical equipment.

Enerpac's commitment to innovation and specialized applications means it likely relies on a select group of suppliers for key technologies. For example, in 2024, the demand for advanced materials in high-strength steel alloys, crucial for heavy-duty lifting and bolting solutions, saw price increases due to limited global production capacity, impacting manufacturers like Enerpac.

Switching Costs for Enerpac

The bargaining power of suppliers for Enerpac is influenced by the costs and complexities associated with switching. If Enerpac faces significant expenses like retooling production lines or requalifying components, its existing suppliers gain leverage. For instance, in 2024, companies in similar industrial sectors reported that integrating new supplier components could add 10-15% to initial production setup costs.

Enerpac's focus on operational efficiency and continuous improvement likely involves proactive measures to mitigate these switching costs. This could include standardizing components where possible or developing strong relationships with multiple suppliers to foster competition and reduce dependence on any single entity.

Threat of Forward Integration by Suppliers

The threat of suppliers integrating forward, meaning they start producing hydraulic tools or controlled force products themselves, directly impacts Enerpac Tool Group. If suppliers possess the capability and intent to become competitors, they gain significant leverage over Enerpac's pricing and supply agreements. This potential shift turns a supplier into a rival, altering the competitive landscape.

While this forward integration is less prevalent for highly specialized industrial components, its mere possibility can influence negotiations. Suppliers might use this threat to secure more favorable terms from Enerpac, knowing that their own entry into the market could disrupt Enerpac's operations and market share. For instance, if a key component supplier for specialized hydraulic pumps sees a clear path to manufacturing the final product efficiently, they might demand better pricing or exclusivity from Enerpac.

Enerpac's established brand reputation and extensive distribution network serve as a crucial defense against this supplier threat. These assets create a barrier to entry for potential integrating suppliers, making it more challenging for them to replicate Enerpac's market reach and customer relationships. In 2023, Enerpac reported a revenue of $558.7 million, underscoring the scale of its established market presence that new entrants would need to overcome.

- Supplier Capability: Assess if key suppliers have the technical expertise and manufacturing capacity to produce Enerpac's core products.

- Market Attractiveness: Evaluate the profitability and growth potential of the hydraulic tools and controlled force products market, which could incentivize supplier integration.

- Enerpac's Defenses: Leverage Enerpac's brand strength, intellectual property, and distribution network as deterrents to supplier forward integration.

Importance of Enerpac to Suppliers

Enerpac Tool Group's substantial global reach and significant sales volume position it as a crucial customer for many of its suppliers. This scale means that if Enerpac constitutes a considerable portion of a supplier's revenue, that supplier is likely motivated to offer favorable pricing and terms to secure Enerpac's continued business. Conversely, if Enerpac's purchases represent a minor fraction of a supplier's overall sales, its bargaining power would be considerably diminished.

For instance, in 2023, Enerpac Tool Group reported total net sales of approximately $1.6 billion. This significant revenue figure suggests that many of its suppliers, particularly those providing specialized components or raw materials, may rely heavily on Enerpac's orders. This reliance can translate into a stronger negotiating position for Enerpac.

- Supplier Dependence: The degree to which suppliers depend on Enerpac for their revenue directly impacts their willingness to concede on pricing and terms.

- Volume Discounts: Enerpac's large order volumes likely enable it to negotiate volume discounts, further enhancing its purchasing power.

- Strategic Partnerships: For suppliers whose products are critical to Enerpac's operations, the potential for long-term, stable business can foster more collaborative and favorable supplier relationships.

Enerpac's Supply Chain: Volume Advantage vs. Critical Component Leverage

The bargaining power of suppliers for Enerpac Tool Group is moderated by the company's significant purchasing volume. In 2023, Enerpac reported net sales of approximately $1.6 billion, indicating that many suppliers likely depend heavily on its orders, which can lead to more favorable pricing and terms for Enerpac. This scale allows Enerpac to negotiate volume discounts, strengthening its overall purchasing power.

The critical nature of certain components for Enerpac's high-performance hydraulic equipment means suppliers of these specialized parts, such as proprietary alloys or precision-engineered parts, hold considerable leverage. If few suppliers offer these essential inputs, Enerpac faces higher costs and limited negotiation flexibility. For example, in 2024, limited production capacity for high-strength steel alloys used in heavy-duty lifting solutions led to price increases for manufacturers like Enerpac.

Switching suppliers for critical components can be costly and complex for Enerpac, involving expenses like retooling or requalifying parts, which can add 10-15% to initial production setup costs, as seen in similar industrial sectors in 2024. This cost creates leverage for existing suppliers. Furthermore, the threat of suppliers integrating forward into Enerpac's market, while less common for highly specialized components, can influence negotiations by creating potential future competition.

| Factor | Impact on Enerpac | 2023/2024 Data/Observation |

|---|---|---|

| Supplier Concentration | High for specialized inputs, increasing supplier leverage. | Limited production capacity for key alloys in 2024 drove price increases. |

| Switching Costs | Significant costs can enhance supplier power. | Estimated 10-15% increase in setup costs for new components in similar sectors (2024). |

| Forward Integration Threat | Potential for suppliers to become competitors. | Possibility influences negotiations, though less prevalent for highly specialized components. |

| Enerpac's Purchasing Volume | Significant volume strengthens Enerpac's negotiating position. | Approx. $1.6 billion in net sales (2023) indicates supplier dependence. |

What is included in the product

This analysis dissects the competitive forces impacting Enerpac Tool Group, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes on its market position.

Easily visualize competitive intensity and strategic positioning with a dynamic Porter's Five Forces analysis, offering a clear, actionable roadmap for Enerpac Tool Group.

Gain immediate insight into market dynamics and potential threats with a user-friendly, customizable Five Forces framework, simplifying complex competitive landscapes for Enerpac Tool Group.

Customers Bargaining Power

Concentration of Customers

The bargaining power of Enerpac Tool Group's customers is significantly shaped by their concentration. If Enerpac primarily serves a small number of major industrial or infrastructure clients who account for substantial purchase volumes, these key customers gain considerable leverage. This leverage allows them to negotiate for lower prices, more favorable payment terms, or customized product specifications, thereby increasing their bargaining power.

However, Enerpac's customer base is characterized by its broad global reach and diversity. Serving a wide array of customers across various industries and geographies tends to dilute the power of any single customer. This widespread customer distribution means that no single entity typically represents a large enough portion of Enerpac's total revenue to exert significant individual pressure on pricing or terms. For instance, in 2023, Enerpac's revenue was generated across numerous segments, with no single customer segment dominating its sales, indicating a lower concentration of customer power.

Switching Costs for Customers

Customers face significant hurdles if they decide to switch from Enerpac's hydraulic tools. These hurdles can include the expense of retraining staff on new equipment, the cost and complexity of reconfiguring existing machinery to be compatible with different systems, and the potential for operational downtime during the transition. These factors inherently increase the bargaining power of Enerpac by making it less appealing for customers to switch.

Enerpac's focus on specialized, high-performance hydraulic solutions, particularly those critical for demanding industrial applications, naturally embeds high switching costs. For instance, in sectors like heavy lifting or specialized manufacturing, the integration of Enerpac's systems often requires deep technical knowledge and precise calibration, making a changeover a complex and potentially disruptive undertaking. This complexity reinforces Enerpac's market position.

Customer Price Sensitivity

Customer price sensitivity is a significant lever in the bargaining power of buyers. If Enerpac's products were seen as interchangeable commodities, customers would have more power to demand lower prices. For instance, if a large industrial customer could easily switch to a competitor offering similar basic hydraulic jacks at a lower cost, their leverage would be substantial.

However, Enerpac specializes in engineered solutions for critical applications, meaning customers often prioritize performance and reliability. In 2024, industries relying on precise lifting and controlled force, such as heavy construction and aerospace, are less likely to compromise on quality for minor price differences. This focus on specialized, high-performance equipment inherently reduces customer price sensitivity.

Threat of Backward Integration by Customers

The threat of backward integration by customers is a key factor influencing Enerpac Tool Group's bargaining power. If customers could realistically produce their own high-pressure hydraulic tools or controlled force products, their leverage over Enerpac would increase significantly.

However, for many of Enerpac's diverse customer base, this threat is relatively low. The specialized knowledge, advanced manufacturing processes, and substantial capital investment required to produce these sophisticated tools make backward integration a challenging proposition. For instance, developing the precision engineering capabilities needed for Enerpac's advanced hydraulic cylinders and pumps would demand considerable R&D and production infrastructure.

Enerpac's commitment to continuous innovation further mitigates this risk. By consistently introducing new technologies and improving product performance, Enerpac makes it increasingly difficult for customers to replicate their offerings effectively. This ongoing technological advancement creates a competitive moat, ensuring that customers benefit more from purchasing Enerpac's specialized products than from attempting to manufacture them in-house.

- Customer Backward Integration Threat: Customers can gain power if they can produce Enerpac's products themselves.

- Technical & Capital Barriers: Producing high-pressure hydraulic tools requires specialized expertise and significant investment, limiting customer integration.

- Innovation as a Deterrent: Enerpac's ongoing technological advancements make it harder for customers to replicate their product lines.

Availability of Substitute Products for Customers

The availability of substitute products significantly impacts Enerpac Tool Group's customers' bargaining power. If customers can easily find alternative tools or methods to achieve similar results, they are less reliant on Enerpac and can demand lower prices or better terms. While specialized hydraulic tools like those Enerpac offers may not have many direct, identical substitutes, customers can explore alternative technologies or less sophisticated equipment for certain tasks.

For instance, in some construction or maintenance scenarios, customers might opt for electric or pneumatic tools if the specific high-pressure hydraulic capabilities are not absolutely critical. This creates a ceiling on how much Enerpac can charge. The global hydraulic equipment market is projected to see growth, with some reports suggesting a compound annual growth rate around 4.5% through 2028, but this growth occurs within a competitive landscape where alternatives are always a consideration for cost-conscious buyers.

- Limited Direct Substitutes: For highly specialized, high-pressure hydraulic applications, direct substitutes are often scarce, giving Enerpac some pricing leverage.

- Alternative Methods Exist: Customers can sometimes achieve desired outcomes using different technologies (e.g., electric, pneumatic) or less advanced equipment, increasing their bargaining power.

- Price Sensitivity: The existence of alternatives makes customers more sensitive to Enerpac's pricing, potentially forcing price reductions or concessions.

- Market Dynamics: While the hydraulic equipment market grows, the presence of alternative solutions ensures that customers retain a degree of control over their purchasing decisions.

Customer Leverage: Balancing High Switching Costs and Alternatives

Enerpac's customers generally have moderate bargaining power. While the company's specialized, high-performance hydraulic tools often come with high switching costs and limited direct substitutes, reducing customer leverage, the overall market dynamics and the availability of alternative technologies prevent customers from wielding overwhelming power. In 2024, industries requiring precision and reliability are less price-sensitive, but the general availability of alternative solutions means customers retain some ability to negotiate or seek different approaches.

| Factor | Impact on Customer Bargaining Power | Enerpac's Position |

|---|---|---|

| Customer Concentration | Low (Diverse customer base) | Reduces individual customer leverage |

| Switching Costs | High (Technical integration, retraining) | Increases Enerpac's leverage |

| Price Sensitivity | Moderate (Prioritize performance over minor price differences) | Limits extreme price demands |

| Backward Integration Threat | Low (High technical & capital barriers) | Minimizes customer threat |

| Availability of Substitutes | Moderate (Alternative technologies exist) | Provides customers with some alternatives |

Preview the Actual Deliverable

Enerpac Tool Group Porter's Five Forces Analysis

This preview showcases the complete Enerpac Tool Group Porter's Five Forces analysis, offering a detailed examination of competitive forces within its industry. The document you see here is precisely what you'll receive immediately after purchase, ensuring no surprises and full usability. This professionally formatted analysis is ready for your immediate download and application.

Rivalry Among Competitors

Number and Size of Competitors

Enerpac Tool Group operates in a market with a diverse array of competitors, from large, multi-faceted industrial corporations to niche specialists. This competitive environment includes significant players such as ESAB, JBT Marel, Gates Industrial, Zurn Elkay Water Solutions, Moog, ChampionX, Weatherford International, Cactus, Hayward, and ATS.

The presence of established companies like Helios Technologies and SPX Technologies further intensifies this landscape. For instance, in 2023, Helios Technologies reported revenue of $1.1 billion, demonstrating the scale of some of Enerpac's rivals.

Industry Growth Rate

The pace at which the hydraulic equipment and industrial power tools sectors expand significantly shapes the intensity of competition. When growth is sluggish, companies tend to battle more fiercely for existing market share, leading to heightened rivalry.

The broader global hydraulic equipment market is anticipated to see a compound annual growth rate of 5.2% between 2024 and 2025. Similarly, the power tools market is demonstrating robust growth. However, the mobile hydraulics segment is projected to experience a contraction in 2024, with a rebound expected in 2025.

Product Differentiation

The intensity of competition among rivals is significantly shaped by how distinct products are. Enerpac Tool Group distinguishes itself through its focus on highly engineered products, precise controlled force solutions, and tailored services. This approach aims to create offerings that stand apart from those of its competitors.

Enerpac's strategy hinges on maintaining strong brand leadership and consistently innovating based on customer needs. For instance, in 2023, Enerpac reported a significant portion of its revenue derived from its industrial tools segment, highlighting the importance of its specialized product lines in a competitive landscape.

Exit Barriers

High exit barriers in the industrial tools and hydraulic equipment sector can significantly intensify competitive rivalry. Companies often find themselves compelled to continue operations, even at reduced profitability, simply to recoup substantial sunk costs associated with specialized assets and long-term investments. This dynamic can lead to prolonged periods of intense competition as firms are reluctant to exit the market.

For Enerpac Tool Group and its peers, exit barriers are substantial, stemming from heavy investments in advanced manufacturing facilities, dedicated research and development for specialized hydraulic technologies, and the establishment of extensive global distribution and service networks. These capital-intensive commitments make a swift or easy departure from the market exceedingly difficult.

Enerpac's long operational history and its established infrastructure further contribute to these high exit barriers. The company’s significant physical assets and ingrained market presence mean that ceasing operations would involve substantial write-offs and potential liabilities, reinforcing the inclination to remain active even in challenging market conditions.

- High Capital Investment: The industrial tools sector demands significant upfront capital for specialized machinery and plant infrastructure, creating a substantial barrier to exit.

- Specialized R&D and Technology: Continuous investment in research and development for hydraulic technology requires long-term commitment, making it costly to abandon.

- Global Distribution Networks: Establishing and maintaining worldwide sales, service, and support infrastructure represents a considerable investment that is difficult to divest.

- Sunk Costs: The cumulative expenditure on plant, equipment, and intellectual property acts as a powerful disincentive to exit, even if current profitability is low.

Switching Costs for Customers

High switching costs can significantly dampen competitive rivalry, making it more challenging for rivals to lure away Enerpac's established customer base. This is a key factor in maintaining market stability.

Enerpac's solutions are often deeply embedded in mission-critical industrial applications. This integration, coupled with the specialized nature of their hydraulic tools and systems, creates substantial switching costs for customers who would face considerable expense and operational disruption in transitioning to an alternative provider.

- Deep Integration: Enerpac's tools are frequently integral to complex industrial processes, where downtime for a switch carries immense financial penalties.

- Specialized Training & Maintenance: Customers often invest in specialized training for their personnel to operate and maintain Enerpac equipment, adding to the cost of switching.

- Compatibility Issues: Replacing specialized hydraulic components can lead to compatibility problems with existing infrastructure, further deterring customers from switching.

- Reliability Factor: In industries where failure is not an option, the proven reliability of Enerpac's established systems often outweighs the perceived benefits of a cheaper, less proven alternative.

Industrial Tools & Hydraulics: High-Stakes Sector Rivalry

Competitive rivalry within the industrial tools and hydraulic equipment sector is elevated due to the presence of numerous established players like ESAB, Gates Industrial, and SPX Technologies, with some, like Helios Technologies, generating over $1 billion in annual revenue. This intensity is further fueled by the sector's growth, projected at 5.2% CAGR for the global hydraulic equipment market between 2024 and 2025, although mobile hydraulics are expected to contract in 2024. Enerpac's differentiation through highly engineered, precise solutions and strong brand leadership helps mitigate direct price competition, but the high exit barriers, including substantial investments in manufacturing and R&D, keep many firms committed to the market, thus maintaining rivalry.

| Competitor | Reported Revenue (2023) | Key Product Areas |

|---|---|---|

| Helios Technologies | $1.1 billion | Hydraulic and electronic control systems |

| SPX Technologies | Not specified | Engineered solutions, industrial products |

| ESAB | Not specified | Welding and cutting equipment |

| Gates Industrial | Not specified | Power transmission and fluid power products |

SSubstitutes Threaten

Availability of Alternative Technologies

The threat of substitutes for Enerpac's specialized hydraulic tools is present, primarily from alternative technologies that can perform similar tasks. While hydraulics excel in high-pressure and controlled force applications, advancements in electric, pneumatic, and mechanical systems are continually emerging. For instance, the increasing electrification of off-highway vehicles is gradually reshaping the mobile hydraulics market, potentially offering new substitute solutions in those segments.

Price-Performance Trade-off of Substitutes

The appeal of substitute products for Enerpac Tool Group hinges significantly on their price-performance ratio. When alternative tools can match Enerpac's capabilities at a lower price, or even offer better performance for a comparable cost, the threat posed by these substitutes escalates. This dynamic is particularly relevant as Enerpac is known for its high-quality, precision equipment, which often comes with a premium price tag.

Customer Propensity to Substitute

Customer propensity to substitute for Enerpac Tool Group's products is generally low, particularly in critical sectors like construction, manufacturing, and energy. This reluctance stems from the high stakes involved; safety and reliability are non-negotiable, making customers hesitant to adopt unproven alternatives. For instance, in heavy lifting operations, a failure in a hydraulic tool can lead to catastrophic damage and severe injury, reinforcing a preference for established, trusted brands like Enerpac.

Evolution of Non-Hydraulic Solutions

The growing sophistication of non-hydraulic alternatives presents a significant threat. Advanced electric actuators and high-torque electric motors are becoming more powerful and efficient, potentially replacing hydraulic systems in certain applications. For instance, the global electric vehicle market, a sector where electric actuation is paramount, saw sales of over 10 million units in 2023, indicating a strong shift towards electric power. This trend could spill over into industrial tooling, impacting demand for hydraulic solutions.

Enerpac's commitment to customer-driven innovation is crucial in mitigating this threat. By actively developing and improving its own product lines, including exploring advanced electric and mechanical solutions, Enerpac aims to offer competitive alternatives and retain market share. Their focus on integrating new technologies ensures they are not just reacting to market shifts but actively shaping them. This proactive approach is vital as the industrial landscape continues to embrace electrification and alternative power sources.

The competitive landscape is also evolving with new entrants and existing players investing heavily in non-hydraulic technologies. Companies are recognizing the potential cost savings and environmental benefits associated with electric and mechanical systems. This means Enerpac faces not only the threat of technology itself but also the competitive pressure from those who adopt it effectively and quickly. For example, reports from 2024 indicate significant R&D spending by major industrial equipment manufacturers on next-generation electric power solutions.

Key considerations for Enerpac include:

- Technological Advancements: Continuous monitoring and integration of improvements in electric motor torque density and actuator efficiency.

- Market Adoption Rates: Tracking the speed at which industries are shifting away from hydraulics for specific tasks.

- R&D Investment: Allocating resources to develop and enhance Enerpac's own non-hydraulic offerings.

- Customer Preference Shifts: Understanding evolving customer demands for performance, sustainability, and integration in tooling solutions.

Regulatory or Environmental Shifts

Changes in regulations or environmental concerns could push users towards alternative technologies that are perceived as more sustainable than traditional hydraulic systems. For instance, if hydraulic fluids face stricter environmental controls or if there's a significant push for leak-free operations, this could make alternatives more attractive. Enerpac, like others in the industry, is aware of this, as evidenced by their focus on developing more eco-friendly hydraulic solutions.

The increasing global emphasis on sustainability and green technologies presents a significant threat. For example, by 2024, many regions are expected to have enhanced regulations on industrial fluid containment and disposal. This could directly impact the cost-effectiveness and operational feasibility of hydraulic systems if they are not designed with advanced environmental safeguards. The market is already seeing a rise in demand for electric or battery-powered alternatives in various industrial applications, which could siphon demand away from hydraulic tools if they offer comparable performance with a lower environmental footprint.

- Regulatory Pressure: Stricter environmental regulations on hydraulic fluids and waste disposal could increase operating costs for hydraulic systems.

- Environmental Concerns: Growing public and corporate demand for eco-friendly solutions may favor non-hydraulic alternatives.

- Technological Advancements: Innovations in electric or battery-powered tools could offer competitive performance with reduced environmental impact.

- Market Perception: If hydraulic systems are broadly perceived as less environmentally sound, it can shift customer preference towards substitutes.

Hydraulic Tools Face Growing Threat from Electric & Pneumatic Rivals

The threat of substitutes for Enerpac's hydraulic tools is growing as electric and pneumatic alternatives become more powerful and cost-effective. While hydraulics remain dominant in high-force applications, advancements in electric actuation, particularly in the booming electric vehicle sector, are creating viable substitutes. For instance, global electric vehicle sales surpassed 10 million units in 2023, showcasing the rapid progress in electric power systems that could translate to industrial tooling.

The price-performance ratio is a key driver for substitute adoption. If alternatives can match Enerpac's quality and reliability at a lower cost, the threat intensifies. Customers are increasingly scrutinizing the total cost of ownership, making premium-priced hydraulic tools face greater competition. This is underscored by significant R&D investments in electric power solutions by major industrial players in 2024, signaling a competitive push towards alternatives.

Customer loyalty to hydraulics is strong in critical sectors due to safety and reliability concerns, but this is not impenetrable. As non-hydraulic technologies mature, they offer competitive performance with potential benefits like lower maintenance or environmental impact. The market's increasing focus on sustainability also favors alternatives that can demonstrate a greener footprint, potentially influencing purchasing decisions away from traditional hydraulics.

| Technology | Key Advantage | Potential Impact on Hydraulics | Market Trend Example (2023-2024) |

|---|---|---|---|

| Electric Actuation | High precision, energy efficiency, cleaner operation | Direct replacement in lighter-duty and automated applications | Over 10 million EVs sold globally in 2023; significant industrial automation investment |

| Pneumatic Systems | Fast actuation, simplicity, lower initial cost | Substitute for certain speed-dependent or less precise tasks | Continued adoption in assembly lines and material handling |

| Advanced Mechanical Systems | High reliability, no fluid leaks, potentially lower maintenance | Alternative for specific lifting and positioning tasks | Growth in robotics and automated machinery |

Entrants Threaten

Capital Requirements

The industrial hydraulic tools market, where Enerpac Tool Group competes, demands significant upfront capital. Establishing modern manufacturing facilities, investing in cutting-edge research and development, and building robust global distribution and service networks are all costly endeavors. For instance, a new entrant might need to invest hundreds of millions of dollars just to reach a competitive scale.

Economies of Scale

Established players like Enerpac Tool Group leverage significant economies of scale in manufacturing and procurement, allowing them to achieve lower per-unit costs. For instance, in 2023, Enerpac reported a gross profit margin of 37.7%, partly a reflection of their efficient production processes.

New entrants would find it challenging to match these cost efficiencies, especially in areas like global distribution networks, which Enerpac has cultivated over years of operation. This cost disadvantage makes it difficult for newcomers to compete effectively on price against a company with such established operational advantages.

Product Differentiation and Brand Loyalty

Enerpac Tool Group benefits from significant product differentiation and strong brand loyalty, making it challenging for new entrants. Decades of building a reputation for highly engineered, reliable products under well-known brands like Enerpac and Hydratight mean new competitors must invest substantially in brand development and product innovation to gain traction.

Access to Distribution Channels

New companies face significant challenges in replicating Enerpac's established global distribution network, which spans over 100 countries. This extensive reach is crucial for delivering specialized industrial tools and services efficiently to a diverse customer base. The cost and complexity of building such a robust infrastructure present a substantial barrier.

Enerpac's existing channel partner network acts as a strong competitive moat, making it difficult for new entrants to gain comparable market access. These established relationships streamline logistics and customer service, offering a distinct advantage. Securing similar partnerships requires considerable time, investment, and proven reliability.

- Global Reach: Enerpac operates in over 100 countries, demonstrating a vast and intricate distribution system.

- Channel Partner Network: The company leverages a network of specialized partners to ensure efficient delivery and service.

- Barrier to Entry: The cost and effort required to establish a comparable distribution network are substantial deterrents for new competitors.

Proprietary Technology and Patents

Enerpac's significant investment in research and development, particularly in high-pressure hydraulics and controlled force technology, has resulted in a portfolio of proprietary technology and patents. For instance, their advancements in electric torque wrenches and advanced hydraulic pump controls create substantial barriers for potential newcomers. These intellectual property rights make it difficult and costly for new entrants to replicate Enerpac's product performance and innovation without significant licensing fees or lengthy development cycles.

The threat of new entrants is therefore moderated by Enerpac's established technological leadership. Developing comparable precision and reliability in controlled force applications requires substantial capital and specialized engineering expertise, which new companies may lack. Enerpac's ongoing commitment to customer-driven innovation, evidenced by their continuous introduction of new product lines and upgrades, further solidifies this technological moat.

- Proprietary Technology: Enerpac holds numerous patents related to hydraulic systems and controlled force applications, such as advanced valve designs and integrated sensor technologies.

- R&D Investment: In fiscal year 2023, Enerpac reported significant R&D expenditures, underscoring their commitment to maintaining a technological edge.

- Barriers to Entry: The cost and time required to develop equivalent proprietary technology or secure necessary licenses present a considerable hurdle for potential competitors.

- Customer-Driven Innovation: Enerpac's focus on collaborating with customers to develop tailored solutions leads to the creation of unique, often patented, product features.

Industrial Hydraulics: Entry Barriers Limit New Competition

The threat of new entrants into the industrial hydraulic tools market is somewhat limited due to the substantial capital required for manufacturing and distribution. Enerpac Tool Group's established economies of scale, as reflected in their 37.7% gross profit margin in 2023, create a cost advantage that newcomers would struggle to match.

Furthermore, Enerpac's strong brand recognition and extensive global distribution network, serving over 100 countries, represent significant barriers. Replicating this reach and the associated channel partner relationships would demand considerable investment and time, making it difficult for new competitors to gain immediate market access or compete on service delivery.

Enerpac's proprietary technology and patents in areas like high-pressure hydraulics also deter new entrants. The cost and expertise needed to develop comparable product performance and innovation, or to license existing technology, pose a considerable hurdle for potential competitors seeking to enter the market.

| Barrier Type | Description | Impact on New Entrants | Enerpac Advantage Example |

|---|---|---|---|

| Capital Requirements | High costs for manufacturing facilities and R&D. | Significant financial hurdle. | Hundreds of millions needed for competitive scale. |

| Economies of Scale | Lower per-unit costs for established players. | Difficulty competing on price. | 37.7% gross profit margin (2023) reflects efficient production. |

| Distribution & Network | Extensive global reach and partner relationships. | Challenging market access and service delivery. | Operations in over 100 countries. |

| Proprietary Technology | Patented innovations in hydraulic systems. | Requires significant R&D or licensing costs. | Advanced valve designs and integrated sensor technologies. |

Porter's Five Forces Analysis Data Sources

Our Enerpac Tool Group Porter's Five Forces analysis is built upon a foundation of publicly available financial statements, industry-specific market research reports from firms like IBISWorld, and competitor news releases to capture a comprehensive view of the competitive landscape.