Duke Energy Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Duke Energy

A Must-Have Tool for Decision-Makers

Duke Energy operates within a complex energy landscape shaped by powerful competitive forces. Understanding the intensity of buyer power, the threat of new entrants, and the influence of suppliers is crucial for navigating this sector. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Duke Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel Suppliers

Duke Energy's reliance on diverse fuel sources like natural gas, coal, and nuclear fuel exposes it to the bargaining power of fuel suppliers. Fluctuations in commodity prices, driven by market dynamics and geopolitical events, directly impact Duke Energy's operational expenses. For instance, natural gas prices saw significant volatility in 2023 and early 2024, with spot prices for Henry Hub reaching highs not seen in years before moderating. This volatility underscores the suppliers' ability to influence costs.

Renewable Energy Equipment Manufacturers

As Duke Energy ramps up its clean energy investments, including solar, wind, and battery storage, manufacturers of essential equipment like solar panels and wind turbines gain some leverage. These suppliers are crucial for Duke's 2024 renewable energy project pipeline, which aims to add significant capacity.

However, this supplier power is somewhat tempered by the growing competition within the renewable energy equipment market and rapid technological progress. For instance, the global solar panel market saw a substantial increase in production capacity in 2024, leading to more competitive pricing and a broader range of suppliers for Duke to consider.

Technology and Grid Modernization Providers

Duke Energy's significant investments in grid modernization and digital transformation, including the use of AI for demand forecasting, amplify the bargaining power of technology and grid modernization providers. These suppliers offer specialized software, hardware, and cybersecurity solutions that are critical for smart grids and operational technology, making their offerings indispensable.

The complexity and specialized nature of these advanced technologies mean that few suppliers can meet Duke Energy's specific needs, thereby increasing their leverage. For instance, companies providing AI-driven grid management platforms or advanced cybersecurity for operational technology are in a strong position, especially as utilities like Duke Energy aim to enhance grid resilience and efficiency.

Construction and Infrastructure Contractors

Duke Energy's significant infrastructure investments, including its largest build-out to date, heighten the bargaining power of construction and infrastructure contractors. This extensive project pipeline for new power plants, transmission lines, and distribution upgrades creates substantial demand for specialized services.

The availability of skilled labor, essential specialized equipment, and critical raw materials directly impacts contractor leverage. Furthermore, the competitive environment among large-scale infrastructure contractors can influence pricing and project execution timelines, potentially increasing costs for Duke Energy.

- High Demand: Duke Energy's ongoing infrastructure expansion creates a robust demand for construction services.

- Resource Scarcity: Limited availability of skilled labor and specialized equipment can empower contractors.

- Competitive Landscape: The number and capacity of large-scale contractors influence their pricing power.

- Project Complexity: The scale and technical requirements of Duke Energy's projects often necessitate specialized expertise, further strengthening contractor bargaining power.

Specialized Labor and Human Capital

The utility sector, including Duke Energy, increasingly requires specialized labor for managing intricate energy infrastructure and adopting new technologies. This demand for skilled professionals in areas like engineering, IT, and clean energy implementation significantly bolsters the bargaining power of suppliers of this human capital.

These specialized talent suppliers, whether direct employers or contracting agencies, can leverage their position to negotiate higher wages and more favorable terms. For instance, in 2024, the demand for cybersecurity professionals in critical infrastructure sectors, which utilities fall under, saw average salaries rise by 15-20% year-over-year, according to industry reports.

- High Demand for Specialized Skills: The transition to renewable energy and the modernization of grids create a critical need for engineers with expertise in areas like grid modernization, renewable integration, and advanced analytics.

- Talent Shortages: Reports in late 2023 and early 2024 indicated persistent shortages in specialized STEM fields, giving skilled workers and the firms that supply them greater leverage.

- Increased Labor Costs: This elevated bargaining power translates directly into higher labor costs for utility companies, impacting operational expenses and potentially project timelines.

Supplier Bargaining Power Shapes 2024 Operations

Duke Energy faces supplier bargaining power across its operations, from fuel sources to specialized technology. The company's significant investments in renewable energy projects in 2024, such as expanding solar and wind capacity, increase leverage for equipment manufacturers. However, growing competition in the renewable sector, evidenced by a substantial increase in global solar panel production capacity in 2024, helps mitigate this power.

The demand for advanced grid modernization technology and cybersecurity solutions, critical for Duke Energy's smart grid initiatives, empowers specialized providers. These suppliers, often with unique offerings, can command higher prices due to the critical nature and complexity of their solutions. Similarly, substantial infrastructure investments in 2024, including new power plants and transmission lines, amplify the bargaining power of construction contractors, especially given the demand for skilled labor and specialized equipment.

The utility sector's need for specialized talent, particularly in clean energy and IT, has significantly boosted the bargaining power of labor suppliers. For example, the demand for cybersecurity professionals in critical infrastructure saw average salaries rise by 15-20% in 2024, directly increasing labor costs for companies like Duke Energy.

| Supplier Category | Key Drivers of Bargaining Power | Impact on Duke Energy | Relevant 2024 Data/Trends |

|---|---|---|---|

| Fuel Suppliers (Natural Gas, Coal) | Commodity price volatility, geopolitical factors | Increased operational costs | Henry Hub natural gas spot prices saw significant volatility in late 2023/early 2024. |

| Renewable Equipment Manufacturers (Solar Panels, Wind Turbines) | Demand for clean energy projects, technological advancements | Potential for higher equipment costs, but offset by competition | Global solar panel production capacity increased significantly in 2024, leading to more competitive pricing. |

| Technology & Grid Modernization Providers | Specialized nature of solutions, critical infrastructure needs | Higher costs for essential software, hardware, and cybersecurity | AI-driven grid management platforms and advanced cybersecurity are in high demand. |

| Construction & Infrastructure Contractors | High demand from large-scale projects, resource scarcity (skilled labor, equipment) | Increased project costs and potential timeline impacts | Duke Energy's largest build-out to date creates substantial demand for specialized services. |

| Specialized Labor Suppliers | Shortages in STEM fields, demand for clean energy expertise | Elevated labor costs, impacting operational expenses | Demand for cybersecurity professionals in critical infrastructure rose 15-20% year-over-year in 2024. |

What is included in the product

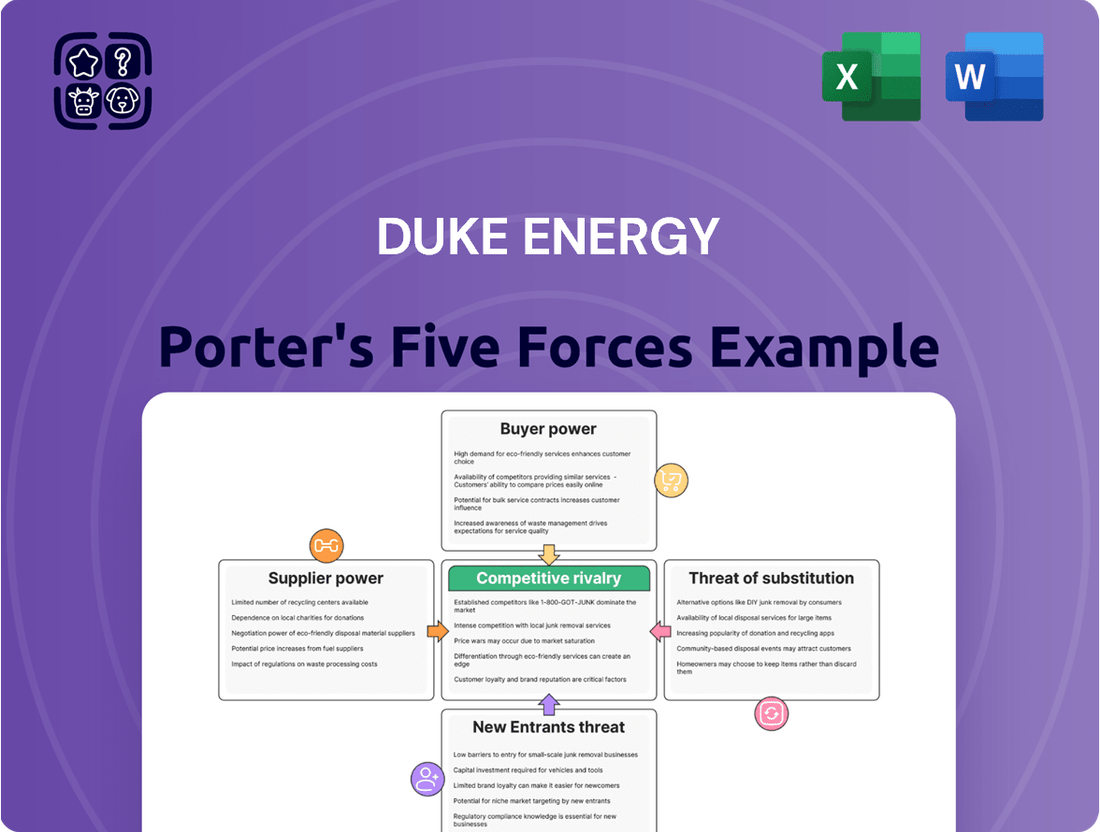

Duke Energy's Porter's Five Forces analysis reveals the intense rivalry among existing energy providers, the significant bargaining power of large industrial customers, and the moderate threat of new entrants in the regulated utility market.

Instantly visualize competitive pressures with a dynamic Porter's Five Forces analysis, allowing Duke Energy to proactively address market challenges and strengthen its strategic position.

Customers Bargaining Power

Regulated Monopoly Status

Duke Energy's status as a regulated monopoly in its service areas significantly curbs customer bargaining power. Because customers generally cannot switch providers for electricity and natural gas distribution, their ability to negotiate lower prices or better terms is severely restricted. This regulatory structure, common for utilities, effectively insulates Duke Energy from direct competitive pressure from its customer base.

Essential Service and Inelastic Demand

Electricity and natural gas are fundamental necessities, making demand for Duke Energy's services largely inelastic. This means customers generally cannot significantly reduce their consumption or easily switch providers when prices change, limiting their bargaining power.

For instance, residential electricity consumption in Duke Energy's service territories, while showing some seasonal variation, remains critical for daily operations. In 2023, Duke Energy reported serving approximately 8.2 million customers across six states, highlighting the broad reliance on their essential services.

Regulatory Oversight and Rate Cases

Customer bargaining power at Duke Energy is significantly influenced by regulatory oversight, particularly through state utility commissions. These commissions act as proxies for customer interests, reviewing and approving rate cases and major capital expenditure proposals. For instance, in 2023, Duke Energy sought rate increases in several states, with the outcomes heavily scrutinized by these regulatory bodies, demonstrating the indirect power customers wield through this channel.

While customers don't directly negotiate prices with Duke Energy, the state utility commissions ensure that rates remain just and reasonable, and that proposed investments are beneficial to the ratepayers. This regulatory framework provides a crucial check on pricing and service quality, effectively channeling customer concerns and limiting Duke Energy's ability to unilaterally dictate terms. The commission's role in approving rate adjustments, such as those Duke Energy files annually, underscores this indirect but potent form of customer bargaining power.

Large Commercial and Industrial Customers

Large commercial and industrial customers, especially those with significant energy needs like data centers and advanced manufacturing plants, possess considerable bargaining power. Their substantial consumption volumes can translate into negotiation leverage, prompting utilities to develop tailored tariffs and incentives to secure and maintain their business. For instance, in 2024, Duke Energy's industrial customer base often represents a substantial portion of their revenue, giving these entities a stronger voice in rate negotiations compared to individual residential users.

- Significant Energy Consumption: Large industrial and commercial clients consume vast amounts of electricity, giving them a stronger position to negotiate terms.

- Tariff and Incentive Negotiation: Their size allows them to lobby for specific energy tariffs and incentives, influencing utility pricing structures.

- Attracting and Retaining Business: Utilities are motivated to offer favorable terms to these key customers to ensure stable revenue streams and operational efficiency.

Demand-Side Management and Energy Efficiency

Customers can significantly influence demand-side management and energy efficiency, impacting Duke Energy's operational landscape. By adopting energy-saving measures, customers reduce their overall consumption, which can alter the utility's load growth forecasts and necessitate adjustments in future infrastructure planning.

Duke Energy's 2024 initiatives, such as its residential energy efficiency programs, aim to engage customers in reducing peak demand. For instance, their smart thermostat programs encourage voluntary load reduction during high-demand periods. These collective actions, while not direct price negotiations, represent a form of customer power that shapes the utility's revenue and investment strategies.

- Customer Investments in Efficiency: Widespread adoption of energy-efficient appliances and home insulation directly lowers electricity usage.

- Demand Response Programs: Duke Energy's participation in programs where customers voluntarily reduce usage during peak times can save the company millions in avoided generation costs.

- Impact on Load Growth: Reduced per-customer consumption can slow the need for new power plants and transmission lines, influencing Duke Energy's capital expenditure plans.

- Smart Technology Adoption: Increased use of smart meters and thermostats provides customers with more control and data, enabling them to manage their energy use more effectively.

Customer Leverage in Regulated Utility Markets

Duke Energy's bargaining power with customers is constrained by its regulated monopoly status, meaning customers typically cannot switch providers for essential electricity and gas services. This lack of direct competition limits customers' ability to negotiate prices or terms. However, large industrial and commercial clients, due to their significant energy consumption, wield more influence, prompting Duke Energy to offer tailored tariffs and incentives to retain their business. For example, in 2024, these major customers often represent a substantial revenue stream, giving them a stronger negotiating position.

| Customer Segment | Bargaining Power Factor | Impact on Duke Energy |

|---|---|---|

| Residential Customers | Low (due to monopoly and inelastic demand) | Limited ability to negotiate prices; reliant on regulatory oversight for fair rates. |

| Large Commercial/Industrial Customers | High (significant consumption volumes) | Can negotiate specific tariffs and incentives; crucial for revenue stability. |

| All Customers (collectively) | Moderate (through demand-side management and regulatory advocacy) | Influence operational planning and capital expenditures through energy efficiency and participation in rate case proceedings. |

Preview Before You Purchase

Duke Energy Porter's Five Forces Analysis

This preview showcases the comprehensive Duke Energy Porter's Five Forces Analysis, detailing competitive rivalry, the threat of new entrants, the bargaining power of buyers and suppliers, and the threat of substitute products. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. You can confidently assess the strategic landscape of Duke Energy with this exact, professionally prepared report.

Rivalry Among Competitors

Regulated Geographic Monopolies

Duke Energy operates in regulated geographic monopolies, meaning it holds exclusive rights for electricity transmission and distribution within its defined service territories. This structure significantly limits direct competition from other utility companies within the same areas. Consequently, competitive rivalry isn't characterized by typical price wars for existing customers.

In 2024, Duke Energy's service territories, encompassing North Carolina, South Carolina, Ohio, Kentucky, Indiana, and Florida, are largely protected from direct utility competition. For instance, in North Carolina, Duke Energy Progress and Duke Energy Carolinas serve vast regions with limited overlap from other major electric providers. This regulatory framework means rivalry is more about operational efficiency and meeting regulatory requirements than competing for customer share within a given zone.

Competition for Economic Development

Duke Energy, like other utilities, faces indirect competition for economic development across state lines. Utilities vie to attract major business investments, such as large manufacturing plants or data centers, by offering attractive power rates, reliable service, and necessary infrastructure upgrades.

This competition for load growth is significant, as securing new, large customers can substantially impact a utility's revenue and growth trajectory. For instance, in 2023, North Carolina, Duke Energy's primary state, saw significant interest from the semiconductor industry, a sector that demands massive amounts of electricity and robust grid capacity.

Competition for Capital and Investment

Duke Energy faces significant competition for investor capital within the broader financial markets, going head-to-head with other regulated utilities. Its success hinges on showcasing stable regulatory frameworks, consistent earnings expansion, and the effective management of substantial capital expenditure projects to draw in investment.

In 2024, the utility sector continues to be a key area for infrastructure investment, with companies like Duke Energy needing to present a compelling case for capital allocation. For instance, Duke's planned capital expenditures for 2024-2028 are substantial, requiring it to compete against other energy infrastructure projects and broader market investment opportunities that offer comparable or potentially higher risk-adjusted returns.

Energy Transition and Decarbonization Pace

Duke Energy faces intense competition as utilities race to decarbonize. This pressure stems from environmental mandates and evolving customer expectations, pushing companies to invest heavily in renewable energy sources and grid modernization. The urgency to meet climate goals means a constant evaluation of new technologies and operational efficiencies. This dynamic fosters a rivalry focused on demonstrating leadership and achieving cleaner energy portfolios.

The push for decarbonization creates a competitive landscape where utilities vie for market share and investor confidence by showcasing their progress. For instance, by the end of 2023, Duke Energy had retired over 50% of its coal-fired generation capacity, a significant step in its transition. This strategic move positions them against peers who are also actively divesting from coal and investing in wind, solar, and battery storage. The pace at which companies adopt and deploy these cleaner technologies directly impacts their standing in this evolving market.

- Renewable Energy Growth: Utilities are competing to build out substantial renewable energy portfolios. Duke Energy's 2024-2028 capital plan includes billions for clean energy investments, reflecting this competitive drive.

- Grid Modernization Race: Modernizing aging infrastructure to accommodate distributed energy resources and enhance reliability is another competitive front. Investments in smart grid technologies are crucial for staying ahead.

- Meeting Emissions Targets: The race to meet state and federal emissions reduction goals creates direct competition. Utilities that can achieve these targets more efficiently or ahead of schedule gain a competitive advantage.

- Technological Innovation: Companies are also competing on the adoption and integration of new technologies like advanced battery storage and carbon capture, which can significantly alter generation economics and environmental impact.

Emergence of Distributed Energy Resources (DERs)

The growing adoption of distributed energy resources (DERs), like customer-owned solar panels and battery storage, is subtly altering the competitive landscape for utilities. These resources enable customers to generate their own power or decrease their demand from the traditional grid, creating a more decentralized energy system.

This shift means some customers are less reliant on Duke Energy's centralized generation, introducing a form of competition by offering alternative energy supply options. While not a direct replacement for the utility, it does fragment demand and can impact revenue streams derived from traditional energy sales.

- Customer-owned solar capacity in the U.S. is projected to grow significantly, with installations expected to reach over 40 GW by the end of 2024.

- Energy storage systems paired with solar are also seeing rapid expansion, offering enhanced grid flexibility and customer self-sufficiency.

- This trend challenges the traditional utility model by empowering consumers to become active participants in energy generation and management.

Navigating Utility Rivalry: Customers, Capital, and Clean Energy

While Duke Energy operates in largely regulated monopolies for electricity transmission and distribution, competitive rivalry exists in nuanced ways. This rivalry is less about direct customer acquisition within its service territories and more focused on attracting large industrial customers, securing investor capital, and leading in the transition to cleaner energy sources.

In 2024, Duke Energy competes for economic development by offering competitive rates and infrastructure to attract major businesses, a critical strategy for load growth. Simultaneously, it faces intense rivalry in the financial markets for investor capital, needing to demonstrate strong performance and strategic execution against other utility companies.

The decarbonization race is a significant competitive arena, pushing utilities to invest in renewables and grid modernization. Duke Energy's progress, such as its substantial coal-fired generation retirement by late 2023, positions it against peers vying for leadership in clean energy portfolios and investor confidence.

The rise of distributed energy resources, like customer-owned solar, presents an indirect competitive challenge by offering alternative energy supply options and fragmenting traditional demand, impacting revenue streams derived from energy sales.

| Competitive Factor | 2024 Context/Data | Impact on Duke Energy |

|---|---|---|

| Economic Development Competition | Utilities vie to attract large businesses; North Carolina (Duke's key state) saw significant interest from electricity-intensive semiconductor firms in 2023. | Securing new, large customers is vital for revenue and growth. |

| Investor Capital Competition | Duke Energy competes with other regulated utilities for investment; its 2024-2028 capital expenditure plans are substantial, requiring a compelling case against broader market opportunities. | Attracting capital is essential for funding infrastructure and clean energy projects. |

| Decarbonization Leadership | Utilities are racing to adopt renewables and reduce emissions; Duke Energy retired over 50% of its coal capacity by the end of 2023. | Demonstrating progress in clean energy enhances market standing and investor appeal. |

| Distributed Energy Resources (DERs) | Customer-owned solar capacity in the U.S. is projected to exceed 40 GW by the end of 2024. | DERs offer alternative energy supply, potentially impacting traditional utility revenue streams. |

SSubstitutes Threaten

Distributed Generation (e.g., Rooftop Solar)

The threat of distributed generation, such as rooftop solar, presents a significant challenge for utilities like Duke Energy. Customers can increasingly install their own solar panels, directly reducing their reliance on the utility for electricity. This is particularly true as solar technology costs continue to fall; for instance, the average cost of residential solar photovoltaic (PV) systems in the US saw a notable decrease in recent years, making it a more accessible option for consumers.

This trend is further amplified by government incentives and net metering policies that can make self-generation financially attractive. As more households and businesses adopt these solutions, the demand for electricity purchased from traditional utility providers like Duke Energy is likely to decline, impacting revenue streams and potentially requiring adjustments to the utility's business model to remain competitive.

Energy Storage Solutions

The threat of substitutes for Duke Energy's traditional electricity supply is growing, primarily from advancements in energy storage solutions. Customers can now store electricity, either from their own generation or during cheaper off-peak times, and use it when demand is high. This directly challenges the utility's role in providing consistent power and reliability.

For instance, the cost of lithium-ion battery storage has fallen dramatically. By the end of 2023, prices had decreased by over 90% compared to a decade prior, making home and commercial battery systems increasingly economically viable. This trend empowers consumers to become more self-sufficient, reducing their dependence on the grid and its associated capacity charges, thereby posing a significant substitute threat.

Energy Efficiency and Demand-Side Management

The threat of substitutes for Duke Energy is amplified by advancements in energy efficiency and demand-side management. Consumers are increasingly adopting energy-efficient appliances, enhancing building insulation, and implementing smart energy systems, all of which directly reduce their reliance on purchased electricity. For instance, in 2024, the U.S. Department of Energy reported a continued rise in the adoption of ENERGY STAR certified appliances, which can reduce household energy bills by up to 10% annually.

Furthermore, utility-sponsored demand response programs, where customers are incentivized to reduce their energy usage during peak demand periods, function as a direct substitute for Duke Energy's electricity supply. These programs effectively flatten the demand curve, diminishing the need for Duke Energy to generate or procure additional power during those critical times, thereby presenting a tangible alternative to traditional consumption.

Self-Generation by Large Industrial Consumers

Large industrial and commercial consumers, especially those with consistent and significant energy demands, are increasingly exploring self-generation options. This can involve building their own power plants, often utilizing natural gas or combined heat and power (CHP) systems.

These on-site facilities allow businesses to produce their own electricity and thermal energy, directly reducing their reliance on utility providers like Duke Energy. For example, in 2024, the U.S. Department of Energy reported a continued uptick in distributed generation projects, with industrial sectors being key adopters.

- On-site generation reduces reliance on utility providers.

- Natural gas and CHP are common self-generation technologies.

- Predictable, high energy needs incentivize self-generation.

- Distributed generation adoption is growing across industrial sectors.

Alternative Heating and Transportation Fuels

While electricity is central to Duke Energy's operations, substitutes exist for specific applications. For heating, alternatives like propane or heating oil can compete with electric heat pumps, especially in regions where these fuels are readily available and cost-effective. Similarly, in transportation, gasoline and diesel engines remain significant substitutes for electric vehicles, although the market share of EVs is growing rapidly.

Despite these substitutes, the broader trend is a significant shift towards electrification across various sectors. This trend, driven by environmental concerns and technological advancements, generally increases the overall demand for electricity. For instance, the U.S. electric vehicle market saw substantial growth, with sales in 2023 reaching over 1.2 million units, a significant increase from previous years, indicating a growing reliance on electricity for transportation.

- Heating Substitutes: Propane and heating oil offer alternatives to electric heating systems, impacting demand for electric heating solutions.

- Transportation Substitutes: Internal combustion engine vehicles using gasoline and diesel are prevalent substitutes for electric vehicles, though EV adoption is accelerating.

- Electrification Trend: The overarching movement towards electrification in heating and transportation is a key factor, generally boosting electricity demand for companies like Duke Energy.

- EV Market Growth: U.S. EV sales surpassed 1.2 million in 2023, highlighting the increasing adoption of electric-powered transportation.

Electricity Substitutes: A Growing Challenge for Utilities

The threat of substitutes for Duke Energy's core electricity service is multifaceted, primarily stemming from distributed generation technologies like rooftop solar and advancements in energy storage. These options allow consumers to generate and store their own power, directly reducing their reliance on the utility. For instance, the cost of residential solar PV systems in the US continued to decline, making it a more accessible alternative for many households.

Energy efficiency measures and demand-side management programs also act as substitutes by lowering overall electricity consumption. Consumers adopting ENERGY STAR certified appliances, for example, can see significant reductions in their energy bills. Furthermore, large industrial users are increasingly turning to on-site generation, such as natural gas or combined heat and power (CHP) systems, to meet their substantial energy needs, thereby bypassing traditional utility supply.

While substitutes like propane for heating and gasoline for transportation exist, the broader trend of electrification in these sectors generally benefits electricity providers. The rapid growth of the electric vehicle market, with over 1.2 million units sold in the U.S. in 2023, illustrates this shift. However, the increasing viability of self-generation and storage solutions presents a persistent challenge to utility revenue models.

| Substitute Category | Key Technologies/Strategies | Impact on Duke Energy | Supporting Data (2023-2024) |

|---|---|---|---|

| Distributed Generation | Rooftop Solar PV | Reduced demand for grid electricity, potential revenue loss | Continued cost declines in solar PV systems |

| Energy Storage | Home/Commercial Battery Systems | Decreased reliance on grid during peak hours, reduced capacity charges | Lithium-ion battery costs down >90% in a decade |

| Energy Efficiency | Efficient Appliances, Smart Home Tech | Lower overall electricity consumption | Increased adoption of ENERGY STAR appliances |

| On-site Generation | Natural Gas, CHP Systems | Direct bypass of utility supply for large consumers | Uptick in industrial distributed generation projects |

| Alternative Fuels (Specific Applications) | Propane/Heating Oil (Heating), Gasoline/Diesel (Transportation) | Competition for specific energy end-uses | U.S. EV sales surpassed 1.2 million in 2023 |

Entrants Threaten

High Capital Requirements

The energy utility sector, including companies like Duke Energy, presents a significant barrier to new entrants due to exceptionally high capital requirements. Building new power plants, extensive transmission lines, and robust distribution networks demands billions of dollars in upfront investment. For instance, the average cost to build a new natural gas power plant can range from $1 billion to over $2 billion, while large-scale renewable projects like offshore wind farms can cost tens of billions.

These substantial financial hurdles make it incredibly difficult for new companies to establish a foothold in the market. The sheer scale of investment needed to compete with established players like Duke Energy, which already possesses vast, depreciated infrastructure, effectively deters most potential competitors. This capital intensity ensures that only well-funded entities can even consider entering, and even then, the risk is immense.

Extensive Regulatory Hurdles and Approvals

Extensive regulatory hurdles and approvals act as a significant barrier to entry for new companies. Operating as a regulated utility, like Duke Energy, requires navigating a complex web of state and federal regulations, obtaining numerous permits, and undergoing lengthy approval processes for rates and infrastructure projects. For instance, the U.S. electric utility sector is heavily regulated by agencies such as the Federal Energy Regulatory Commission (FERC) and state Public Utility Commissions (PUCs), which dictate everything from pricing to environmental compliance. These substantial compliance costs and time-consuming processes deter potential new entrants, thereby protecting incumbent players.

Established Infrastructure and Economies of Scale

Duke Energy's entrenched position, built on decades of infrastructure development and massive economies of scale across generation, transmission, and distribution, presents a formidable barrier to new market entrants. Replicating this extensive network and achieving comparable cost efficiencies would necessitate enormous upfront capital investment and a considerable timeframe, placing any newcomer at a significant disadvantage from the outset.

Access to Transmission and Distribution Grids

Gaining access to Duke Energy's established transmission and distribution grids presents a formidable hurdle for new entrants. This control over essential infrastructure acts as a significant barrier, making it difficult for independent power producers and other new energy companies to connect their generation facilities to the market.

The lengthy and intricate interconnection queues are a prime example of this challenge. In 2024, the backlog of projects seeking grid connection across the US continued to grow, with some regions experiencing delays of several years. For instance, the Federal Energy Regulatory Commission (FERC) has been working to reform the interconnection process, acknowledging that current timelines are unsustainable and hinder renewable energy deployment.

- Infrastructure Control: Duke Energy owns and operates the vital transmission and distribution networks, giving it significant leverage over who can access the market.

- Interconnection Delays: New projects face substantial wait times in interconnection queues, often stretching for years, which delays revenue generation and increases project risk.

- Regulatory Hurdles: Navigating the complex regulatory landscape for grid access adds another layer of difficulty and cost for potential new competitors.

- Capital Investment: Building new transmission infrastructure to bypass existing networks is prohibitively expensive, further entrenching incumbent advantages.

Brand Recognition and Customer Loyalty

Duke Energy benefits from deeply ingrained brand recognition and customer loyalty, a significant barrier for potential new entrants in the utility sector. As an incumbent, Duke has cultivated millions of customer relationships over decades, fostering trust through consistent reliability and service delivery. This established reputation makes it challenging for newcomers to gain traction, especially in a market where consumers historically have limited choices for electricity and gas providers.

The threat of new entrants, specifically concerning brand recognition and customer loyalty, is amplified by the nature of the utility industry. For instance, in 2024, Duke Energy continued to serve approximately 8.4 million customers across its service territories. Building a comparable level of trust and brand equity would require substantial investment and time for any new company attempting to enter this established market.

- Established Brand Equity: Duke Energy's long history and consistent service have built a strong brand, making it difficult for new entrants to compete on trust.

- Customer Inertia: In regulated utility markets, customers often face high switching costs or simply lack the option to change providers, reinforcing loyalty to incumbents.

- Service Reliability Perception: Duke’s operational track record contributes to a perception of reliability, which is paramount for customers and a difficult attribute for new players to immediately replicate.

- Scale of Operations: Serving millions of customers provides Duke with economies of scale and a broad customer base that new entrants would struggle to match initially.

Capital and Regulation: Utility Entry's Formidable Walls

The threat of new entrants for Duke Energy is significantly low due to the immense capital required to build new power generation and distribution infrastructure. For instance, constructing a new nuclear power plant can cost upwards of $20 billion, a sum that most new companies cannot readily access. Furthermore, the lengthy and complex regulatory approval processes, often taking years and involving multiple state and federal agencies, act as a substantial deterrent. In 2024, companies seeking to enter the utility market still face these entrenched barriers, making it exceedingly difficult to establish a competitive presence.

| Barrier Type | Description | Example Cost/Timeframe |

| Capital Requirements | Building new generation and distribution infrastructure | Nuclear Plant: $20+ billion; Gas Plant: $1-2 billion |

| Regulatory Hurdles | Navigating permits, rate approvals, and compliance | Years for approval processes; significant compliance costs |

| Infrastructure Access | Gaining access to existing transmission and distribution grids | Long interconnection queues (years in some regions in 2024) |

| Economies of Scale | Replicating established players' operational efficiencies | Requires massive scale to match incumbent cost structures |

Porter's Five Forces Analysis Data Sources

Our Duke Energy Porter's Five Forces analysis is built upon a foundation of comprehensive data, including Duke Energy's annual reports, SEC filings, and investor presentations. We also incorporate industry-specific reports from reputable sources like the Edison Electric Institute and government regulatory filings from agencies such as the FERC and state public utility commissions.