Central Pacific Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Central Pacific Bank

Go Beyond the Preview—Access the Full Strategic Report

Central Pacific Bank faces significant competitive pressures, with moderate buyer power and a constant threat from new entrants in the banking sector. Understanding the intensity of these forces is crucial for strategic planning.

The complete report reveals the real forces shaping Central Pacific Bank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Availability of Capital (Depositors)

Central Pacific Bank, like many financial institutions, heavily relies on deposits from individuals and businesses as its core funding source. The bargaining power of these depositors is directly tied to how much interest they can earn elsewhere. If other banks or investment vehicles offer more attractive rates, depositors have more leverage to demand better terms from Central Pacific Bank.

In 2024, as interest rates remained a key factor in consumer financial decisions, the availability of capital from depositors became even more critical. While Central Pacific Bank benefits from a loyal customer base in Hawaii, the competitive landscape for deposits means they must continually monitor and adjust their offerings to retain and attract funds. For instance, if the Federal Reserve signals further rate adjustments, depositors will actively seek out the highest yields, increasing their bargaining power.

Wholesale Funding Markets

Central Pacific Bank can tap into wholesale funding markets to manage its liquidity and capital needs. The influence of these institutional providers hinges on prevailing market conditions, including interbank lending rates and the bank's own creditworthiness, which directly affect the expense and accessibility of these funds.

For instance, in early 2024, the Federal Reserve maintained its benchmark interest rate, influencing the cost of borrowing in these markets. Central Pacific Bank's robust capital ratios and solid liquidity, as highlighted in its latest financial reports, serve to lessen the bargaining power of these wholesale funding suppliers.

Technology and Software Providers

Central Pacific Bank’s reliance on technology and software providers for its digital banking infrastructure, including core systems and cybersecurity, grants these suppliers considerable leverage. This is particularly true given the high costs and complexities associated with switching providers in this specialized sector.

The banking industry’s ongoing digital transformation, with significant investments in new technologies, underscores the critical nature of these supplier relationships. For instance, the global fintech market was valued at over $110 billion in 2023 and is projected to grow substantially, indicating the increasing importance and potential pricing power of key technology vendors.

Human Capital and Labor Market

The availability of skilled human capital is a significant factor influencing the bargaining power of suppliers in the financial sector, particularly for institutions like Central Pacific Bank. This includes a wide range of roles, from experienced financial advisors and compliance officers to IT specialists and customer-facing branch staff. The ability to attract and retain top talent directly impacts operational efficiency and service quality.

In a geographically concentrated market like Hawaii, the pool of specialized talent can be limited. This scarcity can empower employees, giving them greater leverage in wage negotiations and benefit demands. For instance, a shortage of cybersecurity experts or seasoned loan officers in the region could drive up compensation expectations, thereby increasing labor costs for Central Pacific Bank.

- Talent Scarcity: Limited availability of specialized financial and technical roles in Hawaii increases employee bargaining power.

- Wage Pressures: A tight labor market for skilled professionals can lead to higher salary and benefit demands.

- Retention Challenges: Financial institutions may face increased costs to retain key personnel due to competitive offers.

- Operational Impact: Difficulty in filling critical positions can hinder service delivery and strategic initiatives.

Regulatory and Compliance Services

While not traditional suppliers, regulatory bodies and the compliance services they mandate exert significant influence on banks like Central Pacific Bank. The need to adhere to ever-changing regulations necessitates substantial investment in legal, audit, and compliance expertise. This creates a bargaining power for specialized service providers who are essential for avoiding penalties and maintaining operational integrity.

- Critical Nature of Services: Compliance and legal services are non-negotiable for banks, making these providers indispensable.

- Penalties for Non-Compliance: Failure to meet regulatory standards can result in severe financial penalties and reputational damage, amplifying the power of compliance service providers.

- Specialized Expertise: The complex and evolving nature of banking regulations requires highly specialized knowledge, limiting the pool of qualified service providers.

Supplier Bargaining Power: Impacting Bank's Financial and Talent Landscape

Central Pacific Bank's bargaining power with its suppliers is influenced by the concentration of providers and the necessity of their services. For critical technology and compliance services, where specialized expertise is paramount and switching costs are high, suppliers often hold significant leverage. This is particularly true in the rapidly evolving fintech landscape, where access to cutting-edge solutions can be a competitive differentiator.

The bank's ability to attract and retain talent also plays a role, especially in specialized areas. In 2024, the demand for financial professionals, particularly those with digital and cybersecurity skills, remained strong across the industry. Central Pacific Bank's strategic location in Hawaii, while offering a unique market, can also present challenges in sourcing specialized talent, potentially increasing the bargaining power of individuals and recruitment firms.

| Supplier Category | Key Factors Influencing Bargaining Power | 2024 Context/Data Point |

|---|---|---|

| Depositors (Individuals & Businesses) | Interest rate competitiveness, availability of alternative investments | Interest rates remained a key factor; depositors actively sought higher yields. |

| Wholesale Funding Providers | Market conditions, bank's creditworthiness, interbank lending rates | Federal Reserve maintained benchmark rates, impacting borrowing costs. |

| Technology & Software Providers | Switching costs, specialization, industry demand for fintech | Global fintech market valued over $110 billion in 2023; high switching costs for core systems. |

| Skilled Human Capital (Employees) | Talent scarcity, wage pressures, retention challenges | Tight labor market for specialized financial and IT roles, especially in concentrated markets like Hawaii. |

| Regulatory & Compliance Services | Complexity of regulations, penalties for non-compliance, specialized expertise | Evolving regulatory landscape necessitates significant investment in compliance and legal services. |

What is included in the product

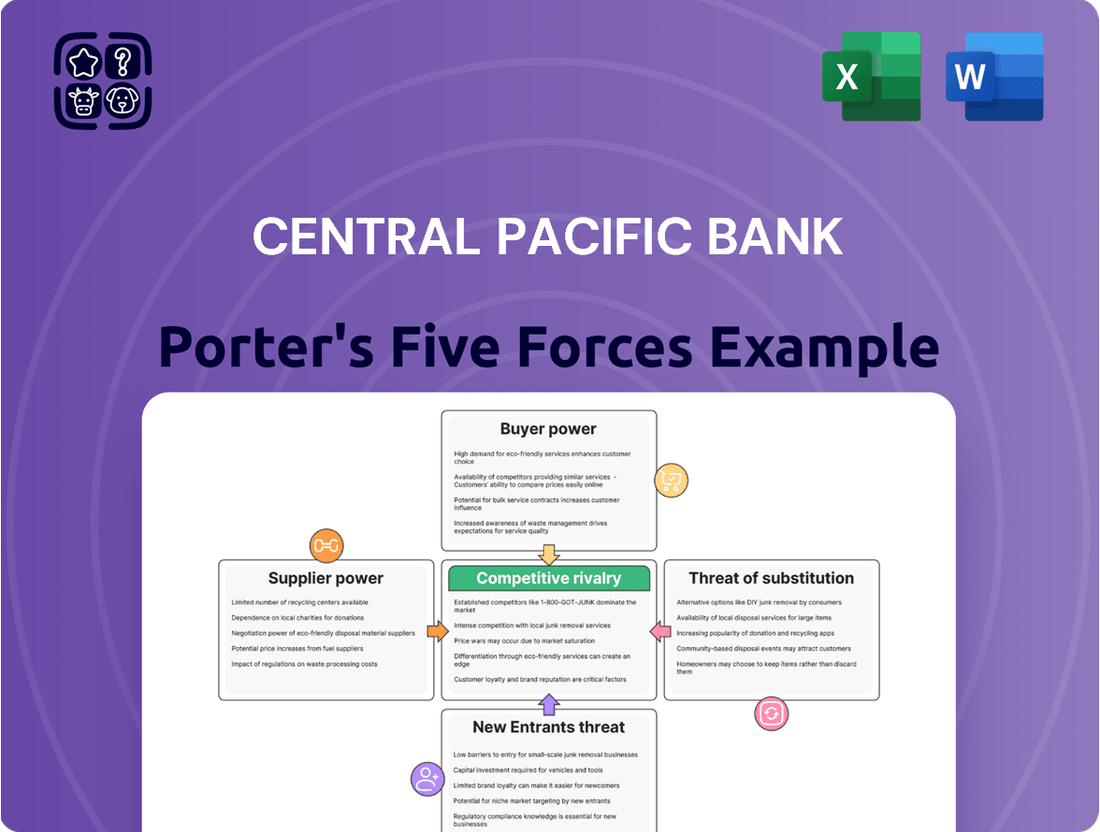

This analysis uncovers the competitive forces impacting Central Pacific Bank, including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry among existing competitors.

Easily assess competitive threats and opportunities with a visual breakdown of each force, simplifying complex market dynamics for Central Pacific Bank.

Customers Bargaining Power

Low Switching Costs for Basic Services

For basic banking products like checking and savings accounts, switching costs for individual customers can be relatively low, especially with the rise of digital banking options. In 2024, many fintech solutions offer seamless account transfers, making it easier than ever for consumers to change banks. This ease of movement gives customers leverage to seek out better rates, lower fees, or improved service elsewhere, potentially impacting Central Pacific Bank's ability to retain customers solely on convenience.

Access to Diverse Financial Options

Customers in Hawaii, both individuals and businesses, are not limited to Central Pacific Bank. They have a wide array of choices, including other local banks, large national banks with a presence in the state, and numerous credit unions. This broad access means customers can easily shop around for the best rates and services.

This abundance of financial providers significantly strengthens the bargaining power of customers. For instance, in 2024, Hawaii's banking sector saw continued competition, with deposits across all financial institutions in the state reaching hundreds of billions of dollars. This competitive landscape allows customers, especially those with substantial deposits or complex financial requirements like business loans or investment accounts, to effectively negotiate terms and fees.

Influence of Digital Banking & Fintech

The rise of digital banking and fintech has dramatically shifted power to customers. With numerous apps and online services, consumers can easily compare rates, manage accounts, and even access loans from non-traditional providers, diminishing their dependence on established banks like Central Pacific Bank. This accessibility means customers can readily switch providers if they find better terms or services elsewhere.

Central Pacific Bank, recognizing this trend, has been actively investing in its digital capabilities. In 2024, the bank continued to enhance its mobile banking app and online platforms, aiming to offer seamless digital experiences that rival those of fintech companies. This strategic move is crucial for retaining customers who increasingly prioritize convenience and digital accessibility over physical branch interactions.

Price Sensitivity and Interest Rate Environment

In today's financial landscape, customers are increasingly attuned to interest rate differentials. For Central Pacific Bank, this means that if their deposit rates lag behind competitors, or if their loan pricing isn't attractive, customers with significant funds or borrowing requirements are likely to seek better deals elsewhere. This dynamic directly pressures the bank's profitability by squeezing its net interest margin.

The current interest rate environment, which has seen fluctuations, amplifies this customer sensitivity. For instance, as of early 2024, the Federal Reserve's monetary policy has led to higher benchmark rates, making deposit yields more attractive. Customers are therefore more likely to shop around for the best APY on savings accounts and CDs. Central Pacific Bank's ability to offer competitive rates on both deposits and loans is crucial to retaining these price-sensitive customers.

- Price Sensitivity: Customers actively compare deposit yields and loan rates across financial institutions.

- Impact on Net Interest Margin: Uncompetitive rates can lead to deposit outflows or increased borrowing costs, directly reducing profitability.

- Market Benchmarks (Early 2024): Average savings account rates have seen increases, prompting customer vigilance.

- Customer Retention: Offering competitive pricing is key to preventing customer attrition to rival banks.

Information Transparency

Information transparency significantly boosts customer bargaining power. With readily available online comparison tools and enhanced financial literacy, individuals can easily research and contrast banking products. This allows them to negotiate better terms and services with institutions like Central Pacific Bank, compelling banks to offer more competitive and clear offerings.

For instance, in 2024, the growth of financial comparison websites and apps has made it simpler than ever for consumers to assess interest rates, fees, and features across multiple banks. This accessibility directly translates into a stronger negotiating position for customers.

- Informed Decisions: Customers can now easily compare Central Pacific Bank's offerings against competitors, driving down prices and improving service quality.

- Online Aggregators: Websites and apps in 2024 provide detailed breakdowns of banking products, empowering consumers with knowledge.

- Reduced Switching Costs: The ease of accessing information lowers the perceived effort and risk associated with switching banks, increasing customer leverage.

Customer Bargaining Power: The New Banking Reality

The bargaining power of customers for Central Pacific Bank is substantial, fueled by low switching costs and increased price sensitivity. In 2024, the proliferation of digital banking and fintech solutions means customers can easily compare rates and fees, making it simpler to move their business. This environment pressures Central Pacific Bank to offer competitive pricing and superior digital experiences to retain its customer base.

| Factor | Impact on Central Pacific Bank | 2024 Context |

|---|---|---|

| Switching Costs | Low, especially for basic accounts | Digital tools simplify account transfers. |

| Information Transparency | High, customers easily compare offerings | Comparison websites and apps are prevalent. |

| Price Sensitivity | High, customers seek better rates/fees | Interest rate fluctuations increase vigilance. |

| Availability of Alternatives | Numerous local and national competitors | Hawaii's banking sector remains competitive. |

Preview Before You Purchase

Central Pacific Bank Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces Analysis for Central Pacific Bank, detailing the competitive landscape and strategic implications for the institution. The document displayed here is the exact, fully formatted analysis you'll receive immediately after purchase, offering actionable insights without any placeholders or surprises. You're looking at the final, professionally written report, ensuring you get precisely the information needed to understand Central Pacific Bank's market position and competitive pressures.

Rivalry Among Competitors

Presence of Established Local Banks

Central Pacific Bank faces significant rivalry from established local banks in Hawaii, such as Bank of Hawaii and First Hawaiian Bank. These institutions possess deep community ties and substantial market share, creating a highly competitive environment for acquiring customers and assets.

Bank of Hawaii, in particular, holds a dominant position within the Hawaiian banking sector, intensifying the competitive pressure on Central Pacific Bank. This entrenched local presence means these competitors have well-developed distribution networks and strong brand recognition, making it challenging for newer or smaller players to gain traction.

Competition from Credit Unions

Credit unions in Hawaii present a notable competitive challenge to Central Pacific Bank. These member-owned institutions often provide comparable banking services, frequently with a community-centric approach that can lead to more favorable fees and interest rates for their members. Newsweek's 2025 recognition of several Hawaii-based credit unions for their community impact underscores their strong local presence and appeal.

Impact of Digitalization and Fintech

The banking sector's digital transformation is a major driver of competitive rivalry. New, digitally-focused players can enter the market more easily, while established banks like Central Pacific Bank are enhancing their digital offerings to compete. This means customers have more choices for convenient and accessible banking services.

Central Pacific Bank is actively embracing digitalization to stay competitive. In 2023, the bank reported strong engagement with its digital banking platforms, indicating successful adoption by its customer base. This focus on digital channels is crucial for meeting evolving customer expectations and fending off competition from fintechs and other digitally-savvy institutions.

Economic Conditions in Hawaii

Hawaii's economy, while demonstrating resilience, is susceptible to broader macroeconomic shifts. Its heavy reliance on tourism means that downturns in travel can significantly impact loan demand and deposit growth for banks. For instance, while visitor arrivals showed a strong recovery post-pandemic, reaching near pre-pandemic levels in late 2023 and early 2024, any future global economic slowdown could dampen this crucial sector.

Fluctuations in the real estate market also play a significant role. Hawaii's property values have seen considerable appreciation, but a cooling market or rising interest rates could lead to increased competition among financial institutions for a smaller pool of lending opportunities and customer deposits. This heightened rivalry directly impacts Central Pacific Bank's ability to attract and retain profitable business.

Economic forecasts for Hawaii in 2025 present a mixed picture. While some projections anticipate continued moderate growth, others highlight potential headwinds from inflation and interest rate policies. This uncertainty amplifies the competitive pressures as banks vie for market share in a potentially constrained economic environment.

- Tourism Dependency: Hawaii's economy relies heavily on tourism, making it vulnerable to external shocks.

- Real Estate Market Volatility: Fluctuations in property values and interest rates can intensify competition for loans and deposits.

- 2025 Economic Outlook: Varied forecasts for 2025 suggest a potentially challenging environment for banking sector growth.

Product and Service Differentiation

Banks, including Central Pacific Bank (CPB), go beyond just interest rates to attract customers. They differentiate by offering a wide array of services like wealth management, specialized commercial lending, and advanced digital banking tools. This breadth and quality of offerings are crucial in a competitive market.

CPB actively works to stand out by providing a comprehensive suite of financial solutions. Their commitment to service excellence has been recognized, for instance, by Forbes naming them one of America's Best Banks in 2023 and 2024. This highlights their success in differentiating through superior product and service delivery.

- Service Breadth: Central Pacific Bank offers a full spectrum of banking services, from personal and business accounts to wealth management and commercial lending.

- Digital Innovation: The bank invests in user-friendly digital platforms and mobile banking solutions to enhance customer convenience.

- Brand Recognition: Being named one of Forbes' Best Banks in 2023 and 2024 provides significant differentiation and builds customer trust.

Hawaii's Banking Sector: Navigating Intense Competition

Central Pacific Bank faces intense competition from established local banks like Bank of Hawaii and First Hawaiian Bank, which boast strong community ties and significant market share. Credit unions also pose a challenge, often offering competitive rates and a community-focused approach, as highlighted by Newsweek's 2025 recognition of Hawaii-based credit unions. The ongoing digital transformation is further intensifying rivalry, with new digital players and established banks like CPB enhancing their online services to meet customer expectations. CPB's own digital engagement, strong in 2023, is a key strategy in this competitive landscape.

| Competitor | Market Share (Approx.) | Key Differentiators |

|---|---|---|

| Bank of Hawaii | ~40-50% | Dominant local presence, extensive branch network |

| First Hawaiian Bank | ~30-40% | Strong community banking, established brand |

| Hawaii Credit Unions | Varies by institution | Member-owned, often competitive rates and fees |

SSubstitutes Threaten

Rise of Fintech Payment Solutions

Fintech payment solutions represent a significant threat of substitution for traditional banking services. Companies offering mobile payment apps and digital wallets provide convenient alternatives to standard bank transactions, often with specialized features that attract consumers. For example, the global digital wallet market is anticipated to reach $10.5 trillion by 2025, indicating a substantial shift in consumer preference away from traditional payment methods.

Alternative Lending Platforms

Alternative lending platforms, such as online lenders and peer-to-peer platforms, present a significant threat to Central Pacific Bank. These platforms offer direct competition for personal loans, small business loans, and even mortgages, often with streamlined digital processes. For instance, in 2024, the online lending market continued its robust growth, with many platforms boasting significantly faster approval times compared to traditional banks, potentially diverting customers seeking quick financing solutions.

Investment and Wealth Management Platforms

For savings and wealth management, Central Pacific Bank faces numerous substitutes. These include a wide range of options like established brokerage firms, increasingly popular robo-advisors, diversified mutual funds, and user-friendly direct investment apps that are attracting significant capital.

These alternative platforms can divert funds that might otherwise be deposited in traditional bank accounts or managed through Central Pacific Bank's trust services. For instance, the robo-advisor market alone saw substantial growth, with assets under management reaching hundreds of billions of dollars by 2024, directly impacting the potential asset base for banks.

Credit Unions and Community Financial Institutions

Credit unions and smaller community financial institutions pose a significant threat of substitution for Central Pacific Bank. These entities often attract customers with lower fees and a strong community focus, directly competing for retail banking services. For example, in 2023, credit unions across the U.S. saw a deposit growth of 7.1%, indicating their increasing appeal.

While Central Pacific Bank serves the unique Hawaiian market, credit unions provide an alternative banking model that resonates with consumers prioritizing personalized service and potentially better rates. This is further amplified by credit unions' strategic moves to integrate with fintech companies, enhancing their digital capabilities and broadening their competitive reach. In 2024, many credit unions are investing heavily in digital transformation to offer more seamless online and mobile banking experiences.

- Lower Fees: Credit unions typically offer lower account fees and loan interest rates compared to traditional banks.

- Community Focus: Many consumers prefer the community-centric approach of credit unions.

- Fintech Partnerships: Credit unions are enhancing their digital offerings through collaborations with technology firms.

- Growing Membership: Credit union membership in the U.S. reached over 136 million by the end of 2023, demonstrating their expanding market share.

Cryptocurrencies and Decentralized Finance (DeFi)

Cryptocurrencies and decentralized finance (DeFi) are emerging as potential substitutes for traditional banking services, particularly in areas like remittances, lending, and investment. While still in their early stages for widespread adoption, these technologies offer a vision of financial transactions without traditional intermediaries. This could significantly disrupt conventional financial institutions in the long run.

The threat is amplified by DeFi's ability to offer alternative avenues for financial activities. For instance, as of early 2024, the total value locked (TVL) in DeFi protocols has seen fluctuations, but the underlying technology continues to mature, demonstrating its capacity to handle significant transaction volumes. This growth indicates a tangible shift in how some users are accessing financial services, bypassing traditional banks.

- Remittances: Blockchain-based solutions can offer lower fees and faster transaction times compared to traditional wire transfers, potentially attracting customers seeking cost-effective international money movement.

- Lending and Borrowing: DeFi platforms enable peer-to-peer lending and borrowing without traditional financial institutions, offering alternative yield opportunities for lenders and access to capital for borrowers.

- Investment: The rise of tokenized assets and decentralized exchanges provides new avenues for investment, potentially drawing capital away from traditional brokerage and investment services.

- Market Growth: The global cryptocurrency market capitalization, while volatile, has reached trillions of dollars at various points, signaling substantial user engagement and capital allocation in this alternative financial ecosystem.

Digital Disruption: New Rivals Reshape Banking Landscape

Central Pacific Bank faces a significant threat from substitutes across its core service offerings. Fintech payment solutions, alternative lending platforms, and even credit unions offer more convenient or cost-effective alternatives to traditional banking. For instance, the global digital wallet market is projected to reach $10.5 trillion by 2025, highlighting a clear shift in consumer behavior. Furthermore, online lending platforms in 2024 continued to offer faster loan approvals, directly competing for Central Pacific Bank's loan customers.

The rise of robo-advisors and direct investment apps also presents a substantial substitute for wealth management services, with assets under management in robo-advisors reaching hundreds of billions by 2024. Even credit unions, with their lower fees and community focus, are growing their deposit base, having seen a 7.1% growth in 2023. These substitutes collectively challenge Central Pacific Bank's market share by offering specialized, often cheaper, or more accessible financial solutions.

Entrants Threaten

High Regulatory and Capital Barriers

The banking sector, particularly in a market like Hawaii, presents formidable barriers to entry due to substantial capital requirements and intricate regulatory frameworks. Aspiring banks must secure significant funding and comply with a host of licensing, operational, and capital adequacy regulations, making it exceptionally difficult for new players to establish themselves.

Central Pacific Bank, as a member of the Federal Reserve System, operates under stringent capital standards, a testament to the high regulatory bar that new entrants must clear. For instance, as of the first quarter of 2024, U.S. banks are generally required to maintain a Common Equity Tier 1 (CET1) ratio, a key measure of capital strength, often above 4.5%, with additional buffers often pushing this higher in practice.

Established Brand Loyalty and Trust

Established brand loyalty and trust represent a significant barrier for new entrants looking to compete with banks like Central Pacific Bank. For decades, Central Pacific Bank has cultivated deep relationships and a strong reputation within Hawaii, making it difficult for newcomers to attract customers. The bank's repeated recognition as the 'Best Bank in Hawaii' underscores this deeply ingrained customer trust and loyalty, a formidable hurdle for any new competitor.

Need for Local Market Knowledge

The unique cultural and economic landscape of Hawaii creates a significant barrier for new entrants. Financial institutions looking to enter this market must invest substantially in understanding local market dynamics, customer preferences, and deeply ingrained community relationships. This is crucial for competing effectively against established players like Central Pacific Bank.

Emergence of Digital-Only Banks (Neobanks)

The threat of new entrants for Central Pacific Bank is evolving. While the capital and regulatory hurdles for traditional brick-and-mortar banks remain significant, the landscape is being reshaped by digital-only banks, often called neobanks. These nimble competitors operate with substantially lower overheads, as they bypass the significant costs associated with maintaining a physical branch network. This cost advantage allows them to potentially offer more attractive rates or lower fees on their digital services. For instance, by mid-2024, neobanks globally continued to attract significant venture capital, with some reporting customer acquisition costs that were a fraction of traditional banks. However, for a market like Hawaii, where personal relationships and established trust are highly valued, these digital newcomers still face the challenge of building a strong brand presence and cultivating customer confidence to truly compete with established institutions.

Fintech companies, in general, are increasingly viewed as a substantial competitive threat by incumbent banks like Central Pacific Bank. These firms are adept at leveraging technology to offer specialized financial services, often with a focus on user experience and efficiency. Their ability to innovate rapidly and target specific customer segments can disrupt traditional banking models. For example, by early 2024, reports indicated that a significant percentage of banking customers were open to using fintech solutions for at least one financial product, highlighting the growing acceptance and potential market share erosion for traditional players.

- Neobanks' Lower Overhead: Digital-only banks avoid the substantial costs of physical branches, enabling more competitive pricing.

- Fintech Disruption: Financial technology firms are increasingly offering specialized services that challenge traditional banking models.

- Trust and Brand Building: New digital entrants must overcome the challenge of establishing trust and brand recognition in markets like Hawaii.

- Customer Adoption of Digital Services: By mid-2024, a notable portion of consumers were willing to use fintech services, indicating a shift in market dynamics.

Access to Distribution Channels

New entrants into the banking sector, particularly in Hawaii, would find it difficult to gain access to established distribution channels. Central Pacific Bank, for instance, has a significant physical footprint with 27 branches and 55 ATMs throughout the islands. This extensive network offers a level of customer accessibility that a new competitor would struggle to match in the short to medium term.

Replicating Central Pacific Bank's established physical presence and its robust digital infrastructure presents a considerable barrier. Building out a comparable branch and ATM network, alongside developing a user-friendly and secure digital banking platform, requires substantial capital investment and time. This makes it challenging for new entrants to compete on convenience and reach.

- Established Network: Central Pacific Bank's 27 branches and 55 ATMs provide widespread accessibility across Hawaii.

- Digital Infrastructure: The bank's digital platforms offer a competitive advantage that new entrants must replicate.

- Capital Investment: Significant financial resources are needed to build a comparable distribution network.

New Entrants: Digital Agility Meets Banking's Deep Roots

The threat of new entrants for Central Pacific Bank remains moderate, primarily due to high capital requirements and stringent regulatory oversight within the banking industry. However, the rise of digital-only banks and fintech companies presents a more dynamic challenge, as these entities can operate with lower overheads and innovative service models.

While traditional banking entry barriers are substantial, digital challengers are finding ways to bypass some of these. For instance, by early 2024, neobanks continued to attract significant investment, demonstrating their potential to offer competitive digital services. Despite this, building the deep customer trust and local market understanding that Central Pacific Bank possesses in Hawaii is a significant hurdle for any new player.

Central Pacific Bank’s established physical presence, with 27 branches and 55 ATMs as of mid-2024, provides a distinct advantage in customer accessibility that new entrants would find costly and time-consuming to replicate. This extensive distribution network, combined with decades of cultivated brand loyalty, significantly deters new competition.

Porter's Five Forces Analysis Data Sources

Our Central Pacific Bank Porter's Five Forces analysis is built upon a foundation of reliable data, including the bank's annual reports, investor presentations, and filings with the Securities and Exchange Commission (SEC).

We supplement this with industry-specific research from financial publications, market analysis firms, and macroeconomic data to provide a comprehensive view of the competitive landscape.