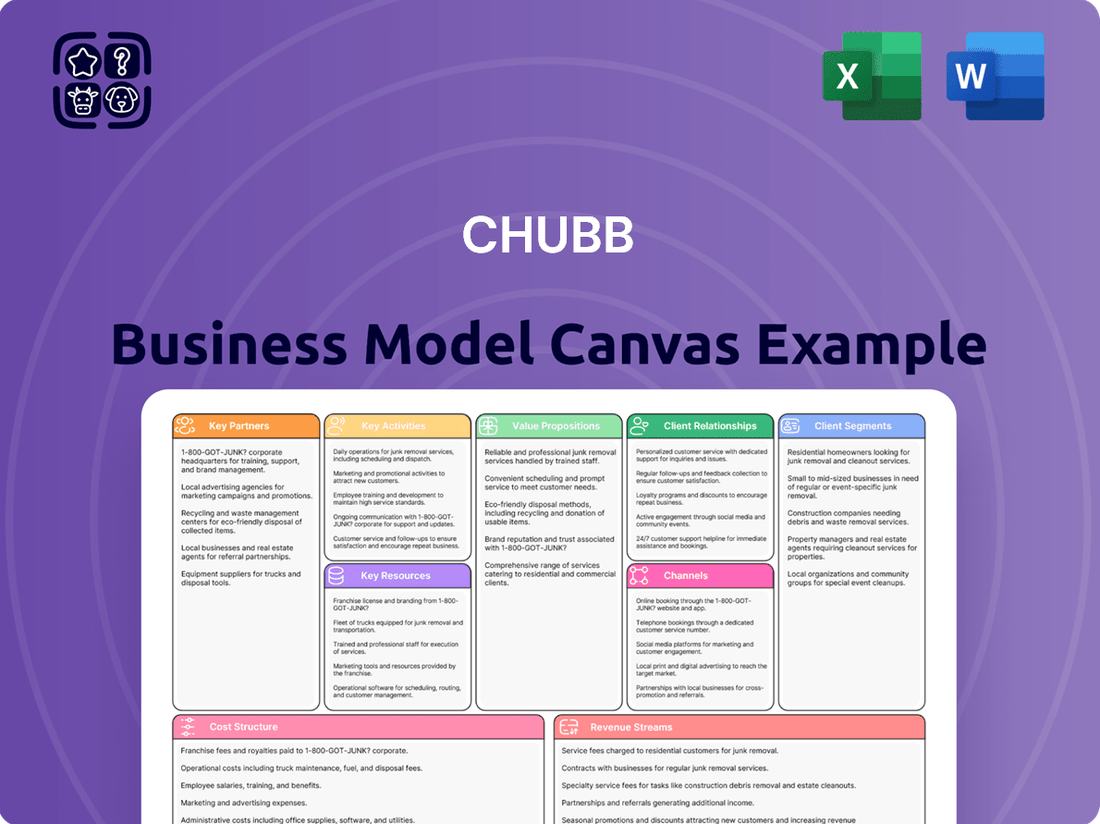

Chubb Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Chubb Bundle

Chubb's Business Model: A Deep Dive

Unlock the full strategic blueprint behind Chubb's business model. This in-depth Business Model Canvas reveals how the company drives value, captures market share, and stays ahead in a competitive landscape. Ideal for entrepreneurs, consultants, and investors looking for actionable insights.

Partnerships

Independent Agents and Brokers

Chubb's success is deeply intertwined with its extensive network of independent agents and brokers worldwide. These partners are essential for distributing Chubb's wide array of property, casualty, and life insurance products. Their local market expertise and established client relationships are critical for Chubb's ability to penetrate markets and drive sales growth across both commercial and personal insurance segments.

Digital Platform Partners

Chubb actively cultivates key partnerships with a diverse range of digital platforms, spanning retail, e-commerce, banking, fintech, airlines, and telecommunications. These collaborations, exemplified by initiatives like Chubb Studio, are crucial for embedding insurance solutions directly within partner ecosystems.

Through these strategic alliances, Chubb facilitates the rapid deployment of 'insurance in a box' offerings, significantly broadening its market access. For instance, by integrating with major e-commerce players, Chubb can offer product protection at the point of sale to millions of online shoppers.

These digital platform partnerships allow Chubb to reach a vast customer base efficiently, tapping into existing user journeys. In 2024, Chubb continued to expand its digital distribution channels, with a substantial portion of new business originating through these integrated partner platforms, underscoring their growing importance.

Reinsurance Providers

Chubb collaborates with reinsurance providers to share substantial risks, particularly those associated with major catastrophes. This strategic engagement allows Chubb to manage its capital more effectively and maintain financial resilience, even after significant claims events. For instance, in 2023, the global insurance industry saw substantial demand for reinsurance capacity, with gross written premiums for reinsurers reaching hundreds of billions of dollars, reflecting the critical role these partnerships play in risk transfer.

Technology and AI Firms

Chubb actively collaborates with prominent technology and AI firms, including Cytora, to drive its digital transformation. These partnerships are crucial for modernizing operations, especially in claims handling and underwriting. For instance, in 2024, Chubb continued to integrate advanced AI solutions to streamline complex processes.

These collaborations focus on leveraging cutting-edge technologies like generative AI. The goal is to automate routine tasks, refine data analysis capabilities, and boost overall operational efficiency across the organization. This strategic approach accelerates Chubb's transition to a digitally-centric business model.

- Cytora Partnership: Enhancing underwriting accuracy and speed through AI-driven risk assessment.

- Generative AI Integration: Automating claims processing and improving customer service interactions.

- Digital Transformation: Accelerating the shift to a digital-first operating model for greater efficiency.

- Data Analytics: Utilizing advanced AI for deeper insights into risk and market trends.

Financial Institutions

Chubb actively partners with financial institutions, particularly banks, to leverage their extensive networks for insurance distribution. This bancassurance model is crucial for reaching new customer segments and expanding Chubb's global footprint. For instance, in 2024, Chubb continued to solidify these relationships in key growth regions.

These collaborations enable Chubb to offer a comprehensive suite of life and non-life insurance products through established banking channels, enhancing customer convenience and broadening market penetration. This strategic alignment is particularly evident in international markets such as Latin America and Asia, where banking penetration is high.

The benefits of these partnerships are significant, providing Chubb with immediate access to a vast customer base and facilitating efficient geographic expansion. In 2024, Chubb's bancassurance initiatives contributed to its overall revenue growth by tapping into the transactional and relationship-based nature of banking.

- Bancassurance Growth: Chubb's bancassurance partnerships in 2024 saw an increase in new policy issuances, particularly in emerging markets.

- International Expansion: These financial institution collaborations were instrumental in Chubb's successful entry into or deepening of presence in markets across Latin America and Asia.

- Customer Acquisition: By integrating insurance offerings within banking services, Chubb effectively acquired new customers who might not have otherwise considered insurance.

Strategic Partnerships: The Engine of Insurance Evolution

Chubb's strategic alliances with independent agents and brokers remain foundational, providing critical market access and distribution for its diverse insurance products. These partnerships are vital for reaching both commercial and personal insurance clients through localized expertise and established relationships.

Furthermore, Chubb's expansion into digital platforms, including retail, e-commerce, and fintech, is significantly broadening its reach. By embedding insurance solutions within these ecosystems, Chubb can offer products like 'insurance in a box' at the point of sale, a strategy that saw substantial new business originate through these channels in 2024.

Collaborations with financial institutions, particularly banks, through bancassurance models are also key, enabling Chubb to tap into new customer segments and expand its global footprint. These alliances proved instrumental in Chubb's 2024 revenue growth, especially in international markets.

Chubb also leverages partnerships with reinsurance providers to manage significant risks, ensuring financial resilience. In 2023, global reinsurance premiums exceeded hundreds of billions, highlighting the importance of these risk-sharing relationships for insurers like Chubb.

Finally, partnerships with technology and AI firms, such as Cytora, are driving Chubb's digital transformation, enhancing underwriting and claims processing with AI-driven solutions throughout 2024.

| Partnership Type | Key Role | 2024 Impact/Focus |

|---|---|---|

| Independent Agents & Brokers | Distribution & Market Access | Continued core channel for sales growth. |

| Digital Platforms (E-commerce, Fintech) | Embedded Insurance & Broad Reach | Significant source of new business; expansion of 'insurance in a box'. |

| Financial Institutions (Bancassurance) | Customer Acquisition & Geographic Expansion | Drove revenue growth, particularly in Latin America and Asia. |

| Reinsurance Providers | Risk Management & Financial Resilience | Essential for managing catastrophic event exposures. |

| Technology & AI Firms | Digital Transformation & Operational Efficiency | Integration of AI for underwriting and claims processing advancement. |

What is included in the product

This Chubb Business Model Canvas provides a detailed breakdown of how the company creates, delivers, and captures value, focusing on its diverse customer segments and extensive distribution channels.

It maps out Chubb's core value propositions, key resources, and activities, alongside its cost structure and revenue streams, offering a holistic view of its insurance operations.

Chubb's Business Model Canvas acts as a pain point reliever by offering a clear, structured overview of their complex insurance operations, making it easier to identify and address inefficiencies.

It streamlines the understanding of Chubb's value proposition and customer segments, simplifying the process of pinpointing and resolving strategic challenges.

Activities

Underwriting and Risk Assessment

Chubb's central function revolves around meticulously evaluating, accepting, and overseeing diverse risks, spanning commercial and personal property, casualty, accident and health, and life insurance sectors. This demands profound underwriting acumen and a rigorous approach to risk selection to guarantee profitable outcomes.

The company is committed to achieving industry-leading combined ratios, a testament to its robust underwriting capabilities and disciplined execution. For instance, in the first quarter of 2024, Chubb reported a net written premiums of $11.7 billion, with a strong focus on underwriting excellence.

Claims Management and Processing

Claims management and processing are core to Chubb's operations, focusing on fair and timely resolution to build customer trust. In 2023, Chubb reported a combined ratio of 85.6%, indicating strong performance in managing claims costs relative to premiums earned.

Chubb is actively integrating digital tools and generative AI to streamline claims document handling. This technological push is designed to accelerate processing times and boost accuracy, ultimately improving the customer's experience during a critical interaction.

Investment Management

Chubb actively manages a vast investment portfolio, a crucial element that significantly boosts its profitability through substantial investment income. In 2024, the company's investment income was a major driver of its financial performance.

The company's investment strategy is anchored in a conservative philosophy, with a primary focus on fixed maturity securities. This deliberate allocation strategy is designed to ensure consistent and stable returns, bolstering Chubb's overall financial resilience.

Product Development and Innovation

Chubb is a leader in continuously developing and innovating a wide array of insurance products. This spans from traditional offerings to specialized lines such as cyber risk and complex construction risks. The company actively tailors these solutions to meet the unique needs of various customer segments.

Leveraging technology is a cornerstone of Chubb's approach to creating new and enhanced insurance products. This focus on a broad product portfolio enables Chubb to effectively address evolving market demands and foster sustained growth. For instance, in 2023, Chubb continued to expand its digital capabilities, aiming to streamline the customer experience and introduce more innovative products.

- Product Diversification: Chubb offers a comprehensive suite of insurance products, including property, casualty, specialty lines, accident and health, and life insurance.

- Innovation Focus: The company invests in developing new products and services, particularly in emerging areas like cyber insurance and parametric solutions.

- Customer Segmentation: Chubb tailors its product development to cater to the specific needs of diverse customer groups, from individuals to large corporations.

- Technological Integration: Chubb utilizes technology to enhance product design, delivery, and claims processing, driving efficiency and customer satisfaction.

Global Market Expansion and Acquisition

Chubb is aggressively pursuing global market expansion, focusing on organic growth and strategic acquisitions in key emerging regions like Asia and North America. This strategy is designed to diversify revenue streams and tap into new growth avenues.

Recent moves highlight this expansion; in 2024, Chubb completed the acquisition of Cigna’s catastrophe business in the UK and continued to increase its stake in China's Huatai Insurance Group, signaling a clear intent to deepen its presence in these vital markets.

These activities are crucial for Chubb's business model, enabling it to capture market share and leverage its global capabilities. For instance, the acquisition of Liberty Mutual's operations in Thailand and Vietnam further solidifies its Asian footprint.

- Global Footprint Growth Chubb is actively expanding its presence in high-growth emerging markets across Asia and North America.

- Strategic Acquisitions Recent acquisitions, including Liberty Mutual's Thailand and Vietnam businesses, underscore this expansion strategy.

- Diversification and Opportunity Capture These activities aim to diversify Chubb's revenue base and capitalize on new market opportunities.

- Market Deepening Increased stakes in entities like China's Huatai Insurance Group demonstrate a commitment to deepening market penetration.

Driving Profitability: Underwriting, Claims, and Investment Management

Chubb's key activities encompass underwriting, claims management, and investment management. The company meticulously evaluates and accepts risks across various insurance sectors, aiming for profitable outcomes. In Q1 2024, net written premiums reached $11.7 billion, reflecting strong underwriting performance.

Claims handling is central, focusing on fair and timely resolutions. Chubb's 2023 combined ratio was 85.6%, demonstrating efficient claims cost management. The company is also leveraging generative AI to enhance claims processing efficiency.

Investment management is critical for profitability, with a conservative strategy focused on fixed maturity securities. This approach ensures stable returns, contributing significantly to Chubb's financial performance throughout 2024.

| Activity | Description | 2023/2024 Data Point |

|---|---|---|

| Underwriting | Risk evaluation and acceptance across diverse insurance lines. | Q1 2024 Net Written Premiums: $11.7 billion |

| Claims Management | Processing and settling claims efficiently and fairly. | 2023 Combined Ratio: 85.6% |

| Investment Management | Managing a portfolio to generate investment income. | Significant driver of financial performance in 2024 |

Preview Before You Purchase

Business Model Canvas

This preview offers a genuine glimpse into the Chubb Business Model Canvas you will receive. It is not a simplified sample, but rather an authentic section of the complete document. Upon purchase, you will gain full access to this exact Business Model Canvas, ready for your strategic planning and business development needs.

Resources

Financial Capital and Reserves

Chubb's financial capital and reserves are a cornerstone of its business model, enabling it to confidently underwrite significant risks and fulfill its commitments. As of the close of 2024, the company commanded over $245 billion in assets, a testament to its financial might.

This substantial financial foundation is further solidified by the consistently strong financial strength ratings awarded to its core operating insurance entities. These ratings underscore the robustness of Chubb's balance sheet, assuring stakeholders of its capacity to manage its obligations effectively.

Underwriting Expertise and Talent

Chubb's underwriting expertise and talent are paramount, drawing on a deep bench of seasoned underwriters, claims specialists, and risk engineers. This human capital is crucial for accurately evaluating intricate risks across diverse business lines and international territories, enabling the creation of bespoke insurance products.

This specialized knowledge forms a significant competitive edge for Chubb. For instance, in 2023, Chubb reported a combined ratio of 86.1% for its P&C insurance businesses, reflecting strong underwriting discipline and profitability, a direct testament to the skill of its underwriting teams.

Global Network and Infrastructure

Chubb leverages a robust global network and infrastructure, operating in 54 countries and territories. This expansive reach, coupled with a vast network of offices and local expertise, enables Chubb to effectively serve multinational clients and navigate diverse regulatory landscapes.

The company's international footprint is significant, with nearly half of its business conducted outside the United States. This demonstrates Chubb's established presence and ability to adapt to varied market conditions worldwide.

Advanced Technology and Data Analytics

Chubb's commitment to advanced technology is evident in its substantial investments. For instance, in 2023, the company reported information and communication technology (ICT) spending of $2.5 billion, underscoring its dedication to digital transformation. This investment fuels the use of artificial intelligence, the Internet of Things (IoT), cloud computing, and big data analytics.

These technologies are instrumental in refining Chubb's core operations. They enable more precise underwriting, streamline the claims handling process through automation, and foster deeper, more personalized customer interactions. The strategic deployment of these advanced tools directly supports the company's pursuit of operational efficiency and competitive advantage.

- AI-driven underwriting: Enhances risk assessment accuracy and pricing.

- IoT integration: Facilitates real-time data collection for risk management and claims validation.

- Cloud computing: Provides scalable infrastructure for data processing and application deployment.

- Big data analytics: Uncovers trends for product development and customer insights.

Brand Reputation and Trust

Chubb's brand reputation and the trust it has cultivated are cornerstones of its business model. This long-standing image, built on financial strength, rigorous underwriting, and dependable claims handling, acts as a significant intangible asset.

The insurance sector heavily relies on trust, making Chubb's century-old reputation vital for attracting and keeping both customers and business partners. This enduring credibility directly influences client acquisition and retention rates.

Reinforcing this strong reputation are Chubb's consistent high financial strength ratings. For instance, as of mid-2024, Chubb maintained an A++ rating from A.M. Best and an AA rating from S&P, reflecting its robust financial stability and ability to meet its obligations.

- Financial Strength: Chubb's consistent high ratings from agencies like S&P (AA) and A.M. Best (A++) underscore its stability.

- Underwriting Discipline: A reputation for careful risk assessment and pricing attracts clients seeking reliable coverage.

- Claims Service: A history of efficient and fair claims processing builds loyalty and word-of-mouth referrals.

- Client Retention: This strong trust directly translates into higher customer loyalty and reduced churn.

Resources Powering Global Insurance Leadership

Chubb’s key resources are multifaceted, encompassing substantial financial capital, deep underwriting expertise, a vast global network, significant technology investments, and a powerful brand reputation built on trust.

These elements collectively enable Chubb to underwrite complex risks, serve a diverse international clientele, and maintain operational efficiency, driving its competitive advantage in the global insurance market.

The company’s commitment to leveraging advanced technologies, such as AI and big data analytics, further enhances its risk assessment capabilities and customer engagement strategies.

| Resource Category | Key Components | 2024/2023 Data Point | Impact on Business Model |

|---|---|---|---|

| Financial Capital | Assets, Financial Strength Ratings | $245 billion+ in assets (2024); A++ (A.M. Best), AA (S&P) | Enables underwriting large risks, ensures solvency |

| Human Capital | Underwriting Expertise, Claims Specialists | 86.1% P&C combined ratio (2023) | Drives underwriting profitability and product innovation |

| Network & Infrastructure | Global Presence, Local Offices | Operates in 54 countries; ~50% of business outside US | Facilitates multinational client service and market penetration |

| Technology | AI, IoT, Cloud, Big Data | $2.5 billion ICT spending (2023) | Enhances underwriting, claims processing, and customer experience |

| Brand & Reputation | Trust, Financial Stability, Claims Service | Century-old reputation, consistent high ratings | Attracts and retains clients and partners, builds loyalty |

Value Propositions

Comprehensive Risk Coverage

Chubb's comprehensive risk coverage is a cornerstone value proposition, extending across a wide spectrum of property and casualty insurance. This includes offerings for commercial enterprises, personal property protection, accident and health coverage, and even life insurance, ensuring clients are shielded from a diverse range of potential threats.

This extensive product suite serves a broad client base, from individual policyholders to small businesses and large, globally operating corporations. The ability to bundle and customize insurance solutions across these multiple lines of business presents a significant advantage, offering a one-stop shop for robust risk management.

For instance, in 2024, Chubb reported a strong performance in its commercial lines, a testament to the demand for its comprehensive coverage. The company's commitment to providing tailored solutions across various insurance needs solidifies its position as a key player in the global insurance market.

Global Reach and Local Expertise

Chubb offers clients the powerful combination of a truly global insurer with deep-seated local market understanding. This means clients get consistent, high-quality service worldwide, while also benefiting from solutions tailored to specific regional regulations and cultural preferences.

With a presence in 54 countries and territories, Chubb's expansive global network ensures they can support clients' operations and risks no matter where they are located. This widespread reach is complemented by a commitment to providing localized expertise, making them a reliable partner across diverse international landscapes.

This unique blend of global scale and granular local insight is a key differentiator for Chubb. For instance, in 2024, Chubb continued to adapt its product offerings to meet evolving regional demands, demonstrating its agility in leveraging local knowledge to serve a global client base effectively.

Financial Strength and Reliability

Chubb's commitment to superior financial strength is a cornerstone of its value proposition. Consistently earning top ratings from agencies like A.M. Best and S&P, Chubb assures policyholders of its robust capacity to meet claims, even in challenging economic environments. This reliability is backed by substantial assets; as of 2024, Chubb reported over $245 billion in assets, providing a tangible measure of its financial stability and ability to honor its commitments.

This financial fortitude translates directly into peace of mind for clients. Knowing that their insurer possesses the resources to handle claims efficiently and effectively is paramount. Chubb's conservative investment strategy further bolsters this assurance, demonstrating a prudent approach to managing its capital and ensuring long-term solvency. This focus on financial resilience underscores Chubb's dedication to being a dependable partner for its customers.

Efficient and Empathetic Claims Service

Chubb's value proposition centers on delivering an efficient and empathetic claims service, a crucial interaction point for policyholders. This commitment is supported by significant investments in technology.

The company is leveraging digital tools and artificial intelligence to streamline claims processing, aiming for faster resolutions. This technological push is balanced with the expertise of skilled adjusters, ensuring a human element remains central to the service.

This dual approach, combining digital efficiency with human empathy, is designed to provide policyholders with timely and supportive assistance, particularly during stressful situations. For example, Chubb reported that in 2024, they continued to enhance their digital claims portals, leading to a notable increase in customer satisfaction scores related to claims handling speed and clarity.

- Digital Investment: Chubb's ongoing investment in AI and digital platforms aims to accelerate claims processing times.

- Human Expertise: Skilled adjusters remain integral to providing personalized and empathetic support.

- Customer Focus: The objective is to offer timely resolution and support during challenging times for policyholders.

- 2024 Impact: Enhancements to digital claims portals in 2024 contributed to improved customer satisfaction regarding claims handling.

Innovative Digital Insurance Solutions

Chubb's innovative digital insurance solutions, exemplified by platforms like Chubb Studio, are revolutionizing how insurance is integrated and distributed. This 'insurance in a box' approach significantly accelerates the speed to market for embedded insurance, allowing partners to offer tailored coverage seamlessly.

For consumers, these digital offerings translate into a more convenient and accessible insurance experience. Chubb's commitment to digital innovation ensures that insurance products are readily available and align with modern, digitally-driven lifestyles. For instance, in 2024, Chubb continued to expand its digital partnerships, aiming to reach millions of new customers through embedded channels.

- Streamlined Integration: Chubb Studio provides a robust platform for partners to easily integrate Chubb's insurance products into their existing digital ecosystems.

- Accelerated Speed to Market: The 'insurance in a box' model enables a rapid deployment of new embedded insurance offerings, a critical advantage in fast-evolving digital markets.

- Enhanced Customer Access: Digital solutions offer customers more intuitive and convenient ways to purchase and manage insurance, fitting seamlessly into their daily digital interactions.

- Tailored Digital Lifestyles: Chubb focuses on creating insurance solutions that are specifically designed to meet the needs of customers living and operating within digital environments.

Global Risk Management, Financial Strength, and Digital Innovation

Chubb's value proposition is built on providing comprehensive risk management solutions. This includes a wide array of property and casualty insurance, personal protection, accident and health, and life insurance, catering to both individuals and businesses of all sizes. Their ability to offer customized and bundled solutions across these diverse lines makes them a convenient, single source for robust risk management.

The company's global reach, operating in 54 countries, is a significant draw, allowing clients to receive consistent, high-quality service worldwide. This expansive network is coupled with a deep understanding of local markets, ensuring that solutions are tailored to specific regional regulations and cultural nuances, a key differentiator that Chubb actively leveraged in 2024 to adapt its offerings.

Chubb's financial strength is a core element of its appeal, backed by top-tier ratings from agencies like A.M. Best and S&P. With over $245 billion in assets reported in 2024, the company offers policyholders a high degree of confidence in its ability to meet claims, supported by a prudent investment strategy that emphasizes long-term solvency and stability.

The firm prioritizes an efficient and empathetic claims process, enhanced by substantial investments in technology. By integrating AI and digital tools to speed up resolutions, while retaining skilled adjusters for personalized support, Chubb aims to provide timely and supportive assistance. In 2024, improvements to digital claims portals led to notable increases in customer satisfaction scores for claims handling.

Chubb is also a leader in digital insurance innovation, particularly through platforms like Chubb Studio. This 'insurance in a box' model accelerates the market entry for embedded insurance, allowing partners to seamlessly offer tailored coverage. In 2024, Chubb expanded its digital partnerships, aiming to reach millions of new customers through these embedded channels, making insurance more accessible and convenient.

Customer Relationships

Dedicated Agent and Broker Support

Chubb cultivates enduring partnerships with its independent agents and brokers, recognizing them as vital conduits to customers. In 2024, Chubb continued to invest heavily in providing these crucial intermediaries with advanced digital tools and comprehensive training programs, designed to enhance their ability to offer personalized insurance solutions.

This commitment to supporting its distribution network ensures agents and brokers are well-equipped to deliver exceptional client service, thereby strengthening Chubb's market presence and fostering deep loyalty within its agent community.

Digital Self-Service Platforms

Chubb provides robust digital self-service platforms, allowing policyholders to manage their accounts, file claims, and access policy details anytime, anywhere. This digital-first approach aligns with the growing consumer demand for convenience and immediate access to services. In 2024, Chubb continued to invest in enhancing these platforms, aiming to streamline the customer journey and improve overall satisfaction.

Personalized Client Engagement

Chubb focuses on deeply personalized client engagement, customizing insurance solutions for everyone from high-net-worth individuals to multinational corporations. This tailored approach is key to their strategy, ensuring clients receive coverage that precisely fits their unique circumstances. In 2024, Chubb continued to invest heavily in digital platforms designed to enhance this personalized interaction, aiming to foster stronger, longer-lasting relationships.

Proactive Risk Management Services

Chubb goes beyond insurance coverage by offering proactive risk engineering and pre-loss solutions. This consultative approach helps clients identify and mitigate potential incidents before they occur, demonstrating a strong commitment to their well-being.

By actively assisting clients in reducing future claims, Chubb enhances its value proposition. This focus on prevention strengthens client relationships, fostering loyalty and trust.

- Risk Engineering: Chubb’s dedicated teams provide on-site assessments and guidance to improve safety and reduce operational risks.

- Pre-Loss Solutions: This includes training programs, safety audits, and customized strategies to prevent accidents and minimize potential losses.

- Value Enhancement: By preventing claims, Chubb not only saves clients money but also solidifies its role as a strategic partner, not just an insurer.

Responsive Claims Handling

Chubb prioritizes a responsive and supportive approach to customer relationships, particularly during the often stressful claims process. They aim for clarity, fairness, and swift resolution, understanding the importance of these elements in rebuilding trust. In 2024, Chubb continued to invest in a blend of skilled claims professionals and advanced digital platforms to streamline this critical interaction.

This strategy is designed to expedite claims handling while ensuring a human touch, offering reassurance when customers need it most. For instance, Chubb's digital tools can facilitate faster initial assessments, while experienced adjusters provide personalized guidance. This dual approach is key to maintaining strong customer loyalty.

- Claims Efficiency: Chubb's commitment to responsive claims handling aims to reduce settlement times, a crucial factor for customer satisfaction.

- Digital Integration: The company leverages technology to enhance communication and expedite processing, as seen in their 2024 digital transformation efforts.

- Customer Support: Empathy and clear communication are central to their strategy, ensuring policyholders feel supported during challenging times.

- Trust Building: A positive claims experience is fundamental to fostering long-term customer relationships and brand loyalty.

Client Loyalty: Partner Empowerment, Digital Access, Risk Prevention

Chubb's customer relationships are built on a dual foundation of strong intermediary partnerships and direct digital engagement. In 2024, Chubb continued to empower its network of independent agents and brokers with advanced digital tools and training, enhancing their ability to deliver personalized service. This strategic focus on supporting its distribution channels is crucial for maintaining deep client loyalty.

The company also provides robust self-service digital platforms, allowing policyholders convenient account management and claims filing, reflecting a commitment to meeting evolving customer expectations for accessibility and efficiency.

Chubb’s customer relationship strategy emphasizes proactive risk mitigation and consultative support, extending beyond traditional insurance coverage. By offering risk engineering and pre-loss solutions, Chubb positions itself as a strategic partner dedicated to preventing claims and enhancing client well-being.

This approach not only adds significant value for clients but also strengthens their bond with Chubb, fostering trust and long-term loyalty through a shared commitment to loss prevention.

Channels

Independent Agents and Brokers

Independent agents and brokers represent a cornerstone of Chubb's distribution strategy, enabling the company to offer its broad portfolio of commercial and personal property and casualty insurance products. These intermediaries are crucial for providing expert advice and tailored service, effectively reaching a wide array of customer segments across the market.

Chubb's reliance on this channel is significant, as evidenced by its position as a leading insurer that partners with many of the top brokers in the United States. This extensive network allows Chubb to maintain a substantial market presence and connect with policyholders who value specialized guidance.

Direct (Online and Digital)

Chubb leverages its direct online and digital channels, including dedicated websites and targeted digital marketing, to connect with specific customer groups, notably in Asian markets. This direct approach enables Chubb to engage customers personally and provide a smooth, digital-first experience for policy acquisition and management, especially for select product offerings.

Bancassurance and Affinity Partnerships

Chubb leverages bancassurance and affinity partnerships to distribute its insurance products. This involves collaborating with banks and organizations like associations, unions, and major retailers. These partnerships tap into established customer bases, allowing Chubb to offer integrated insurance solutions directly to consumers.

In 2024, the global bancassurance market continued its growth trajectory, driven by the increasing demand for convenient financial services. Chubb's strategic alliances within this channel are crucial for accessing a broad customer segment efficiently. For instance, in 2023, the European bancassurance market alone generated over €300 billion in premiums, highlighting the significant potential of this distribution method.

Captive Agents

Chubb utilizes captive agents, notably within its Combined Insurance Company, a key player in its U.S. worksite business. These agents are exclusively dedicated to selling Chubb's diverse product portfolio, ensuring a concentrated sales approach and fostering in-depth product expertise.

This exclusive agency model facilitates a highly focused distribution strategy, enabling Chubb to implement specialized sales tactics and cultivate a deeper understanding of customer needs within specific market segments. As of 2024, Chubb's worksite segment, including Combined Insurance, continues to be a significant contributor to its overall revenue, demonstrating the effectiveness of this dedicated channel.

- Exclusive Distribution: Captive agents focus solely on Chubb products, leading to specialized sales efforts.

- Enhanced Product Knowledge: Agents develop deep expertise, improving customer interactions and sales effectiveness.

- Targeted Market Penetration: This channel allows for tailored strategies to reach specific customer bases, such as employees at worksites.

- Brand Consistency: Ensures a unified brand message and sales experience for customers.

Chubb Studio and API Integrations

Chubb Studio serves as a crucial digital channel, offering partners robust APIs, mobile SDKs, and dedicated microsites. This allows for the seamless integration of Chubb's insurance products directly into their existing digital ecosystems, creating a truly embedded insurance experience.

This digital-first approach facilitates the swift rollout of 'insurance in a box' solutions, catering to diverse industries and their specific needs. For instance, Chubb has been actively expanding its embedded insurance offerings in areas like travel and small business, leveraging platforms like Chubb Studio.

Chubb Studio is instrumental in extending Chubb's digital footprint and unlocking new revenue streams. By enabling partners to offer tailored insurance at the point of need, Chubb can reach a wider customer base and enhance customer loyalty through convenient, integrated solutions.

- Digital Channel: APIs, mobile SDKs, and microsites for partner integration.

- Product Offering: Facilitates 'insurance in a box' solutions.

- Strategic Benefit: Expands digital reach and creates new revenue opportunities.

- Market Impact: Enables embedded insurance across various sectors.

Global Reach: Innovative Distribution Channels

Chubb's distribution strategy is multifaceted, employing a blend of traditional and digital channels to reach its diverse customer base. Independent agents and brokers are a primary avenue, complemented by direct online and digital platforms, bancassurance partnerships, and exclusive captive agents. Chubb Studio further enhances this by enabling embedded insurance solutions through robust digital integrations.

| Channel | Description | Key Benefit | 2024 Relevance/Data |

|---|---|---|---|

| Independent Agents & Brokers | Partnerships with external agents and brokers | Expert advice, tailored service, broad market reach | Chubb is a leading insurer partnering with top U.S. brokers. |

| Direct Online & Digital | Dedicated websites, digital marketing | Direct customer engagement, digital-first experience | Strong focus in Asian markets for specific products. |

| Bancassurance & Affinity | Collaborations with banks and organizations | Access to established customer bases, integrated solutions | Global bancassurance market projected for continued growth in 2024; European market exceeded €300 billion in premiums in 2023. |

| Captive Agents (e.g., Combined Insurance) | Exclusive agents dedicated to Chubb products | Specialized sales, deep product knowledge, targeted market penetration | Significant contributor to Chubb's worksite business revenue in 2024. |

| Chubb Studio | Digital platform with APIs, SDKs, microsites | Embedded insurance, 'insurance in a box' solutions, new revenue streams | Actively expanding embedded offerings in travel and small business sectors. |

Customer Segments

Large Corporations and Multinationals

Chubb's large corporations and multinational segment demands sophisticated insurance products. These clients, operating globally, need tailored property, casualty, and financial lines coverage. For instance, in 2024, Chubb reported significant growth in its international commercial P&C business, indicating strong demand from these larger entities seeking seamless global program management.

The appeal for these clients lies in Chubb's extensive global network and specialized underwriting acumen. Risk engineering services are also a critical component, helping these complex organizations mitigate potential exposures. Chubb's capacity to deliver integrated, worldwide insurance programs is a cornerstone of its value proposition for this segment.

Middle Market Companies

Chubb's middle market segment focuses on businesses that require extensive and tailored insurance solutions for a wide array of risks. These companies, often characterized by revenues between $50 million and $1 billion, are a key growth area for Chubb.

In 2024, Chubb's strategic focus on this segment is evident in its streamlined North America Middle Market organization, designed to improve how it delivers its diverse product offerings and services. This allows Chubb to better meet the complex needs of these businesses.

Middle market companies are actively seeking comprehensive coverage, looking for insurers that can provide both standardized and highly customized packages to address their unique operational and financial exposures.

Small Businesses

Chubb offers a comprehensive suite of insurance products tailored for small businesses, encompassing property, casualty, financial lines, and crucial cyber insurance. This segment is a major focus for Chubb, with a strategic emphasis on simplifying and digitizing the distribution channels to ensure a swift and efficient underwriting process.

The company recognizes small businesses as a significant growth engine. In 2024, Chubb continued to invest in digital platforms designed to streamline policy issuance and claims handling for this vital market segment, aiming to provide accessible and responsive insurance solutions.

Affluent and High-Net-Worth Individuals

Chubb tailors specialized personal insurance for affluent and high-net-worth individuals and families. This includes comprehensive protection for their homes, valuable possessions, automobiles, and umbrella liability needs, often requiring customized policies and exceptional service.

This discerning clientele values Chubb's established reputation for superior quality and extensive coverage. In 2024, the global affluent segment, defined by investable assets between $1 million and $5 million, continued to grow, demonstrating the significant market opportunity for Chubb's premium offerings.

- Market Focus: High-net-worth individuals and families seeking specialized insurance solutions.

- Product Offering: Bespoke policies for homes, valuables, automobiles, and umbrella liability.

- Value Proposition: Emphasis on quality, comprehensive coverage, and white-glove service.

- Clientele Preference: Discerning individuals who prioritize reputation and tailored protection.

Individuals and Families (Mass Market)

Chubb's Individuals and Families segment, often referred to as the mass market, is a cornerstone of their business. They provide a comprehensive suite of personal insurance products designed to meet the everyday needs of households. This includes essential coverage like homeowners insurance, auto insurance, personal accident protection, and supplemental health insurance. In 2024, Chubb continued to emphasize its commitment to this demographic by expanding its digital offerings, making it easier for individuals and families to access and manage their policies. The company reported significant growth in its direct-to-consumer channels, indicating a successful strategy in reaching this broad customer base.

The strategy for engaging this segment relies heavily on accessibility and convenience. Chubb leverages a multi-channel approach, utilizing direct marketing campaigns alongside robust digital platforms. This allows them to connect with a wide array of consumers, from those who prefer traditional methods to those who are digitally native. Their aim is to simplify the insurance purchasing and management process, ensuring that individuals and families can secure the protection they need with minimal friction. For instance, in the first half of 2024, Chubb saw a notable increase in online policy applications, underscoring the effectiveness of their digital investments.

- Broad Product Portfolio: Homeowners, auto, personal accident, and supplemental health insurance are key offerings.

- Distribution Channels: Direct marketing and digital platforms are primary methods for reaching customers.

- Focus on Accessibility: The company strives to make insurance solutions easy to obtain and manage.

- Digital Growth: Significant increases in online policy applications were observed in 2024.

Protecting Diverse Clients: From Global Firms to Families

Chubb serves a diverse customer base, from large corporations requiring complex global insurance programs to affluent individuals seeking specialized personal coverage. The company also targets the middle market with tailored solutions and small businesses with simplified digital offerings. Furthermore, Chubb caters to the mass market with accessible, everyday insurance products for individuals and families, emphasizing digital convenience and broad reach.

Cost Structure

Claims Payouts

Claims payouts represent the largest single cost for Chubb, directly reflecting the core business of providing insurance protection. In 2024, like previous years, these payouts encompass a wide range of events, from everyday accidents to major natural disasters. The effective management of these disbursements is critical for maintaining financial stability and customer trust.

The magnitude of claims payouts can be volatile, heavily influenced by the frequency and severity of insured events. For instance, significant weather events or economic downturns can lead to a surge in claims, impacting profitability. Chubb's operational focus remains on efficiently processing these claims while ensuring fair compensation to policyholders, a balancing act that directly shapes its cost structure.

Underwriting and Operational Expenses

Underwriting and operational expenses are fundamental to Chubb's cost structure, covering the intricate processes of risk assessment, policy issuance, and ongoing administration. These costs are directly tied to the efficiency of their core insurance operations. For instance, in 2023, Chubb reported an underwriting expense ratio of 31.7%, demonstrating their focus on managing these essential costs.

Sales and Marketing Costs

Chubb dedicates significant resources to its sales and marketing efforts to reach a broad customer base. These costs include substantial commissions paid to its vast network of independent agents and brokers, a crucial element of its distribution strategy.

Advertising and digital marketing campaigns are also key expenditures, designed to build and maintain Chubb's strong brand presence in a highly competitive insurance landscape. In 2023, Chubb reported $23.04 billion in total selling, general, and administrative expenses, highlighting the investment in customer acquisition and brand awareness.

Technology and Innovation Investments

Chubb consistently allocates substantial capital towards technology and innovation. In 2024, these investments are crucial for modernizing its extensive legacy systems, a common challenge in the insurance sector. This includes upgrading infrastructure to support advanced AI-driven analytics, which are becoming essential for risk assessment and personalized customer offerings.

The company's commitment to cloud adoption is a significant part of its technology spending, aiming to increase agility and scalability. Digital transformation initiatives, such as the development and expansion of Chubb Studio, a digital platform for agents and brokers, are also key drivers of these expenditures. These efforts are designed to streamline operations, improve the overall customer and partner experience, and build new digital revenue streams.

- Modernizing Legacy Systems: Ongoing efforts to update and replace older IT infrastructure.

- AI and Analytics Enhancement: Investing in artificial intelligence and data analytics capabilities for better insights and decision-making.

- Cloud Adoption: Migrating services and data to cloud platforms for improved flexibility and efficiency.

- Digital Transformation: Developing and expanding digital platforms like Chubb Studio to enhance customer and partner engagement.

Personnel Costs

Chubb's personnel costs are substantial given its global reach and diverse operations. These costs encompass salaries, comprehensive benefits packages, and ongoing training for a vast workforce. As of the first quarter of 2024, Chubb reported consolidated net written premiums of $10.4 billion, underscoring the scale of its operations which necessitate a significant investment in human capital. This investment is vital for maintaining the high level of expertise and service quality expected by clients.

The company employs a wide array of professionals, including specialized underwriters, experienced claims adjusters, meticulous risk engineers, essential IT personnel, and dedicated administrative staff. These individuals are spread across Chubb's operations in 54 countries and territories, each playing a critical role in the company's success. For instance, Chubb's commitment to talent development is evident in its continuous training programs designed to keep its workforce at the forefront of industry knowledge and best practices.

- Global Workforce: Chubb operates in 54 countries and territories, requiring a substantial investment in personnel across diverse geographies.

- Talent Expertise: Costs include salaries and benefits for specialized roles such as underwriters, claims adjusters, and risk engineers.

- Service Quality: Investment in training and development is crucial for maintaining Chubb's reputation for expertise and high-quality customer service.

Key Cost Drivers for a Global Insurer

Chubb's cost structure is dominated by claims payouts, reflecting the core insurance business. Underwriting and operational expenses are also significant, covering risk assessment and administration, with an underwriting expense ratio of 31.7% reported in 2023. Sales and marketing, including agent commissions and advertising, are substantial, with total selling, general, and administrative expenses reaching $23.04 billion in 2023.

Technology and innovation are key investments, focusing on modernizing legacy systems and enhancing AI capabilities, with cloud adoption and digital platforms like Chubb Studio driving these expenditures. Personnel costs, covering salaries, benefits, and training for a global workforce across 54 countries, are also a major component, supporting specialized roles essential for service quality.

| Cost Category | 2023 Data Point | Significance |

|---|---|---|

| Claims Payouts | Largest single cost | Directly tied to core insurance operations and risk events. |

| Underwriting & Operational Expenses | 31.7% (Underwriting Expense Ratio) | Essential for risk assessment, policy issuance, and administration efficiency. |

| Sales, General & Administrative Expenses | $23.04 billion | Covers commissions, marketing, and brand building efforts. |

| Technology & Innovation | Ongoing investment | Modernizing systems, AI enhancement, cloud adoption, and digital platforms. |

| Personnel Costs | Significant for global workforce | Salaries, benefits, and training for specialized roles across 54 countries. |

Revenue Streams

Insurance Premiums

Chubb's primary revenue stream comes from the premiums it collects on a broad spectrum of insurance policies. This includes coverage for commercial and personal property, casualty, accident and health, life insurance, and reinsurance.

The company demonstrated robust performance in this area, reporting substantial growth in total company premiums, measured in constant dollars, during both the first and second quarters of 2025. This indicates strong demand for Chubb's diverse insurance offerings.

Investment Income

Chubb's investment income is a powerhouse, stemming from its vast portfolio of invested assets, particularly fixed maturity securities. This income isn't just a side hustle; it's a major driver of the company's operating income and profitability. For instance, in the first quarter of 2024, Chubb reported adjusted net investment income of $1.5 billion, a notable increase that highlights its consistent growth in this crucial area.

Reinsurance Premiums

Chubb, as a significant global reinsurer, generates revenue from reinsurance premiums by offering risk protection to other insurance companies. This allows insurers to offload portions of their own risk portfolios, thereby stabilizing their financial results and capacity. This segment is a crucial component of Chubb's diversified income streams.

The global reinsurance market experienced robust growth, with Chubb's reinsurance business demonstrating strong premium increases. For instance, in the first quarter of 2024, Chubb reported that its reinsurance segment saw substantial premium growth, reflecting a healthy demand for its services and favorable market conditions.

Fees for Services

Chubb generates revenue from fees for specialized services, including risk engineering and loss prevention consulting, which go beyond basic insurance coverage for commercial clients. These value-added offerings enhance client retention and foster deeper relationships.

- Risk Engineering Fees: Charges for expert assessments to identify and mitigate potential risks, improving operational safety and efficiency for clients.

- Loss Prevention Consulting: Fees for advisory services aimed at reducing the frequency and severity of claims, directly benefiting the client's bottom line.

- Value-Added Services: Revenue from ancillary services that complement insurance policies, such as claims management support or data analytics for risk assessment.

Digital Partnership Revenue

Chubb is increasingly leveraging digital partnerships to generate revenue, a trend prominently seen through initiatives like Chubb Studio. This platform enables Chubb to embed its insurance products directly into the digital ecosystems of third-party businesses.

Revenue from these digital partnerships can manifest as commissions or a direct share of the premiums collected from policies sold through these integrated channels. Examples include offering insurance via e-commerce websites, mobile banking applications, or other digital marketplaces, tapping into existing customer bases.

This evolving revenue stream is poised for significant growth, reflecting a strategic shift towards embedded finance and a more digitally integrated approach to insurance distribution. By meeting customers where they already are online, Chubb expands its reach and creates new avenues for premium acquisition.

- Digital Partnerships: Revenue generated by offering Chubb insurance via third-party digital platforms.

- Chubb Studio: A key enabler for embedding insurance products into partner ecosystems.

- Revenue Models: Primarily based on commissions and premium sharing from policies sold digitally.

- Growth Potential: This channel represents a significant and expanding area for future revenue generation.

Chubb's Revenue: Premiums, Investments, and Digital Growth

Chubb's revenue streams are diverse, anchored by insurance premiums across various lines like property, casualty, and life insurance. The company also benefits significantly from investment income generated by its substantial asset portfolio, particularly fixed maturity securities. Furthermore, Chubb earns revenue through its reinsurance operations, providing risk transfer solutions to other insurers, and from specialized fee-based services such as risk engineering and loss prevention consulting. The company is also actively expanding its digital partnerships, embedding insurance into third-party platforms for new distribution channels.

| Revenue Stream | Description | 2024 Data Example |

|---|---|---|

| Insurance Premiums | Collected from policyholders for various insurance coverage. | Total company premiums grew in constant dollars in Q1 and Q2 2025. |

| Investment Income | Earnings from Chubb's extensive investment portfolio. | Adjusted net investment income was $1.5 billion in Q1 2024. |

| Reinsurance Premiums | Premiums received from other insurers for risk coverage. | Reinsurance segment saw substantial premium growth in Q1 2024. |

| Fee-Based Services | Revenue from specialized consulting like risk engineering. | Fees for risk mitigation and loss prevention consulting. |

| Digital Partnerships | Revenue from embedding insurance into third-party digital platforms. | Chubb Studio facilitates embedding insurance into partner ecosystems. |

Business Model Canvas Data Sources

The Chubb Business Model Canvas is built upon a foundation of extensive market research, internal operational data, and financial disclosures. These sources provide the granular insights needed to accurately define customer segments, value propositions, and revenue streams.