Cembra Money Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Cembra Money Bank

Go Beyond the Preview—Access the Full Strategic Report

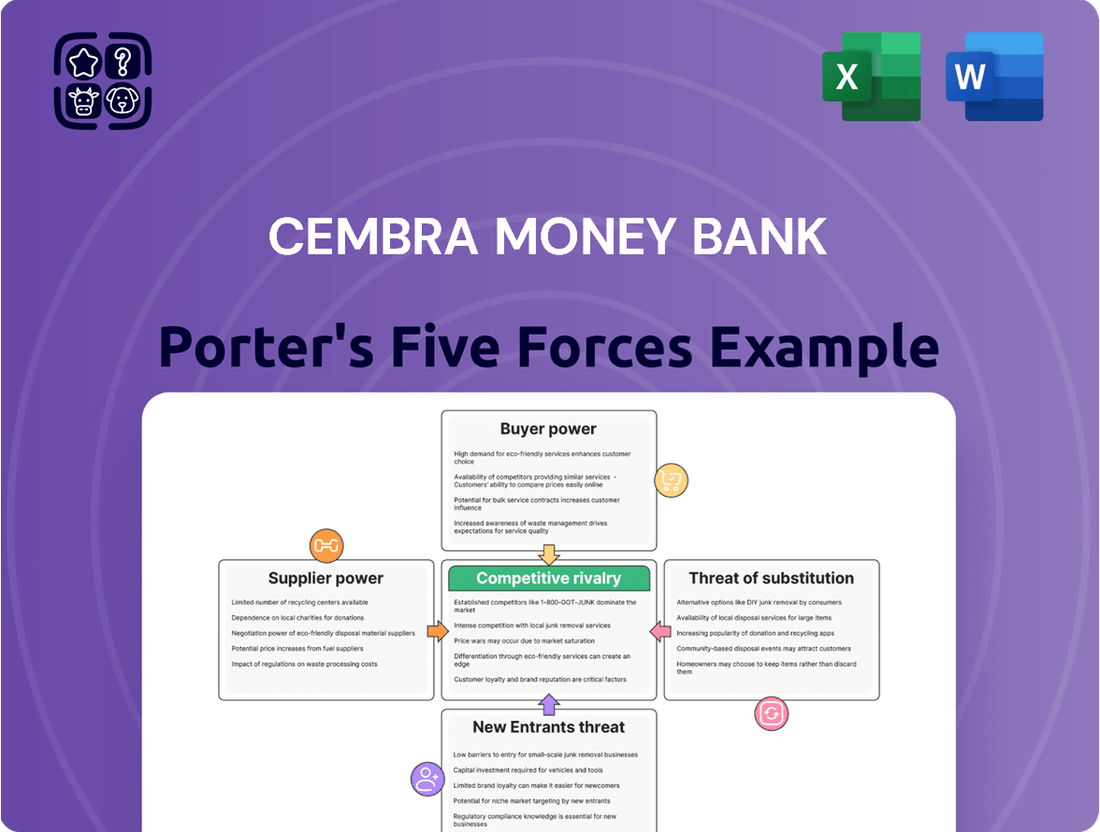

Cembra Money Bank faces moderate bargaining power from buyers due to a competitive market and the availability of alternative financing options. The threat of new entrants is also a significant factor, as the fintech landscape allows for agile new players to emerge. Understanding these dynamics is crucial for strategic planning.

The full analysis reveals the real forces shaping Cembra Money Bank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Access to Funding Sources

Cembra Money Bank's ability to provide financing hinges on its access to funding. Suppliers like depositors and capital markets dictate the cost and availability of its capital. In 2024, for instance, the Swiss banking sector, which Cembra operates within, saw continued reliance on stable deposit bases, though rising interest rates also influenced wholesale funding costs.

Technology and Software Providers

Cembra Money Bank's reliance on technology and software means that providers of core banking systems, digital platforms, and cybersecurity solutions wield significant bargaining power. This is particularly true when these solutions are specialized or deeply integrated, making switching costs high for Cembra.

The increasing demand for advanced digital banking services and robust cybersecurity measures in 2024 further amplifies the leverage of these key technology suppliers. For instance, the global IT spending for financial services was projected to reach over $600 billion in 2024, highlighting the critical role and influence of technology vendors in the sector.

Data and Analytics Providers

In the increasingly data-centric financial services sector, providers of essential credit scoring models, real-time market data, and sophisticated customer analytics hold significant sway. Cembra Money Bank, like its peers, relies heavily on these suppliers for accurate risk assessment and informed product innovation. For instance, a provider offering a proprietary, highly predictive credit scoring algorithm can command higher fees due to its unique value proposition.

Human Capital/Skilled Labor

The bargaining power of suppliers, particularly concerning human capital and skilled labor, plays a crucial role for Cembra Money Bank. The availability of professionals in finance, technology, risk management, and customer service directly influences operational costs and efficiency. A tight labor market in Switzerland, especially for specialized financial roles, can significantly drive up wages.

For instance, in 2024, Switzerland continued to experience a demand for IT and financial specialists, leading to competitive salaries. This scarcity can empower skilled individuals and staffing agencies, allowing them to negotiate higher compensation and better benefits, thereby increasing Cembra's personnel expenses and potentially impacting its ability to attract and retain top talent. This directly affects the bank's capacity for innovation and service delivery.

- Shortage of IT and Finance Professionals: In 2024, Switzerland faced ongoing challenges in filling roles requiring advanced digital skills and financial expertise.

- Increased Labor Costs: This talent scarcity translates into higher salary expectations and recruitment costs for banks like Cembra.

- Impact on Operational Efficiency: Difficulty in securing skilled staff can hinder the smooth functioning of departments and slow down strategic initiatives.

- Innovation Capabilities: A lack of specialized talent can impede Cembra's ability to develop and implement new financial products and technological solutions.

Regulatory and Legal Services

Cembra Money Bank operates in a highly regulated Swiss financial market, meaning its reliance on specialized legal and regulatory advisory services is substantial. The complexity and constant evolution of these regulations mean that firms providing these services hold significant sway. Failure to adhere to these rules can result in hefty fines and reputational damage, underscoring the critical nature of this expertise.

Suppliers of regulatory and legal services, such as prominent Swiss law firms and dedicated compliance consulting groups, wield considerable bargaining power. This strength stems from the unique and often scarce expertise required to navigate the intricate Swiss financial legal landscape. For instance, the Swiss Financial Market Supervisory Authority (FINMA) regularly updates its directives, requiring continuous adaptation and specialized knowledge from legal advisors, thereby increasing their leverage.

- High Demand for Specialized Expertise: The need for deep knowledge in Swiss financial law and compliance creates a concentrated supplier market.

- Risk of Non-Compliance: Penalties for regulatory breaches, such as those related to anti-money laundering (AML) or data protection, can be severe, making compliance essential.

- Limited Number of Qualified Providers: The pool of law firms and consultants with proven track records in Swiss financial regulation is not infinite, granting them pricing power.

- Impact of Regulatory Changes: As of 2024, ongoing adjustments to financial market regulations, including those related to digital assets and consumer protection, further enhance the bargaining power of those who can interpret and implement them effectively.

A Swiss Bank's 2024 Supplier Power Dynamics

Cembra Money Bank's access to capital is a critical supplier relationship, with depositors and wholesale funding markets acting as key suppliers. The cost and availability of funds directly impact its lending capacity and profitability. In 2024, Swiss banks like Cembra continued to balance stable deposit funding with potentially more volatile wholesale market conditions influenced by interest rate movements.

Technology providers, offering everything from core banking systems to cybersecurity, hold significant power due to high switching costs and the specialized nature of their services. The financial sector's increasing reliance on digital transformation, with global IT spending in financial services projected to exceed $600 billion in 2024, underscores this leverage.

Suppliers of essential data and analytics, such as credit scoring models and market data providers, also exert considerable influence. Cembra's need for accurate risk assessment and market intelligence means these specialized services are vital, allowing providers with unique algorithms or comprehensive data sets to command premium pricing.

The bargaining power of human capital suppliers, particularly in specialized IT and finance roles, remains a key factor for Cembra. Switzerland's competitive labor market in 2024, especially for digital and risk management expertise, drives up recruitment and retention costs, impacting operational budgets.

| Supplier Type | Key Considerations for Cembra | 2024 Context | Impact on Cembra |

|---|---|---|---|

| Capital Providers (Depositors, Wholesale Funding) | Cost and availability of funds | Stable deposits, but wholesale funding costs influenced by interest rates | Directly affects lending capacity and net interest margin |

| Technology & Software Vendors | Specialization, integration, switching costs | High IT spending in financial services (> $600B globally) | Increases operational costs, potential for vendor lock-in |

| Data & Analytics Providers | Accuracy, proprietary models, data comprehensiveness | Reliance on credit scoring and market data for risk management | Influences pricing power of suppliers, essential for informed decisions |

| Human Capital (Skilled Labor) | Scarcity of IT and finance professionals | Tight labor market in Switzerland for specialized roles | Drives up personnel costs, impacts talent acquisition and retention |

What is included in the product

This analysis dissects the competitive forces impacting Cembra Money Bank, evaluating the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Instantly visualize the competitive landscape for Cembra Money Bank, highlighting key threats and opportunities to proactively address market pressures.

Customers Bargaining Power

Fragmented Customer Base

Cembra Money Bank's customer base is largely composed of individual consumers and small businesses, a characteristic that significantly fragments its market. This broad distribution means that no single customer accounts for a substantial percentage of Cembra's overall revenue.

Consequently, the bargaining power of any individual customer is inherently limited. Their inability to influence Cembra's pricing or terms due to their small individual contribution to the bank's financial performance is a key factor.

Availability of Alternatives

Customers seeking consumer credit in 2024 have a wealth of choices. Beyond traditional banks, they can turn to specialized finance companies, online lenders, and a growing number of fintech platforms offering innovative credit solutions.

The ease of switching between these providers is a significant factor. Consumers can readily compare interest rates, fees, and customer service levels, with many providers offering streamlined online application processes. This accessibility empowers customers, as a slight disadvantage in pricing or service quality from one provider can quickly lead customers to a competitor.

For instance, in 2023, the Swiss consumer credit market saw increased competition with new digital-first lenders gaining traction, suggesting a trend that is likely to continue and intensify in 2024. This heightened competition directly translates to greater bargaining power for customers.

Price Sensitivity

For standardized financial products such as personal loans and credit cards, customers often exhibit significant price sensitivity. This means they actively seek out the lowest interest rates and most advantageous terms available in the market. This intense focus on price directly pressures Cembra's profit margins, necessitating a constant effort to maintain competitive pricing.

In 2024, the average interest rate for unsecured personal loans in Switzerland hovered around 7.5%, a figure that directly influences customer decisions when comparing offerings. Cembra's ability to offer rates at or below this benchmark is crucial for attracting and retaining these price-conscious individuals. Failing to do so can lead to a substantial loss of market share.

Information Transparency

Customers now have unprecedented access to information thanks to online comparison platforms and financial aggregators. This allows them to easily compare interest rates, fees, and product features from various providers, significantly reducing information asymmetry.

This enhanced transparency directly translates into increased bargaining power for customers. They can readily identify the most competitive offers, forcing providers like Cembra Money Bank to compete more aggressively on price and terms.

- Information Accessibility: Over 70% of consumers in major European markets use online comparison tools for financial products.

- Price Sensitivity: A significant portion of customers, often above 60%, prioritize price when choosing financial services.

- Provider Choice: The availability of numerous online platforms means customers can easily switch providers if they find better deals elsewhere.

- Reduced Switching Costs: Digitalization has lowered the effort required to switch financial institutions, further empowering customers.

Digital Sophistication and Expectations

Customers today are far more tech-savvy, demanding intuitive and personalized digital interactions. Cembra's digital platforms, including its online banking and mobile app, are key battlegrounds for customer loyalty.

In 2024, a significant portion of banking transactions are expected to occur digitally. For instance, studies indicate that over 80% of consumers prefer digital channels for routine banking tasks. This trend highlights how Cembra's investment in user-friendly interfaces and secure online services directly impacts its ability to retain customers and attract new ones who prioritize convenience and efficiency.

- Digital Sophistication: Customers expect seamless, personalized experiences across all digital touchpoints.

- Convenience and Accessibility: Easy-to-use online and mobile platforms are crucial for customer satisfaction and retention.

- Competitive Advantage: Cembra's ability to meet these evolving digital expectations can differentiate it from competitors.

- Customer Loyalty: Superior digital offerings can foster stronger customer relationships and reduce churn.

Customers Gain Power: Digitalization and Choice Reshape Banking

The bargaining power of Cembra Money Bank's customers is moderate to high, driven by market fragmentation and increasing customer choice. With a vast array of financial providers, including traditional banks, fintechs, and online lenders, customers can easily compare offerings. This heightened competition, particularly evident in 2024 with continued digital innovation, forces Cembra to offer competitive rates and terms.

Customers, especially those seeking standardized products like personal loans, demonstrate significant price sensitivity. In 2024, with average unsecured loan rates around 7.5% in Switzerland, customers actively seek the best deals, directly impacting Cembra's pricing strategies. The ease of switching, facilitated by digital platforms and readily available comparison tools, further amplifies this power.

Digitalization plays a crucial role, with over 80% of consumers preferring digital channels for banking. Cembra's investment in user-friendly digital interfaces is therefore vital for retaining customers who expect convenience and efficiency. This digital savviness, coupled with widespread access to information, empowers customers to make informed decisions, pressing Cembra to maintain competitive advantages in service and pricing.

| Factor | Impact on Cembra | Supporting Data (2024 Estimates/Trends) |

|---|---|---|

| Customer Choice & Competition | Moderate to High Bargaining Power | Increasing number of fintech and online lenders entering the Swiss market. |

| Price Sensitivity | High Pressure on Margins | Average unsecured personal loan rates around 7.5% in Switzerland, driving comparison shopping. |

| Information Accessibility | Empowers Customers | Over 70% of consumers use online comparison tools for financial products. |

| Digital Preference | Drives Need for Digital Investment | Over 80% of consumers prefer digital channels for routine banking. |

Preview the Actual Deliverable

Cembra Money Bank Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It details the Cembra Money Bank Porter's Five Forces Analysis, examining the intensity of rivalry, bargaining power of buyers and suppliers, threat of new entrants, and the threat of substitute products within the Swiss financial services sector. This comprehensive analysis provides actionable insights into the competitive landscape Cembra Money Bank operates within.

Rivalry Among Competitors

Number and Diversity of Competitors

The Swiss consumer finance sector is a crowded space, featuring a broad array of competitors. This includes established traditional banks, nimble specialized lenders, and a growing number of innovative fintech firms.

Major financial institutions like UBS, alongside numerous cantonal banks, exert significant pressure, intensifying the competition for customer acquisition and market share. This diverse competitive environment means Cembra Money Bank faces rivalry from many different angles.

Market Growth Rate

The growth rate of Switzerland's consumer credit market directly impacts how fiercely competitors like Cembra Money Bank vie for business. While the market has experienced expansion, it’s showing signs of maturity. This maturity often translates into intensified competition as established players and new entrants alike fight harder to capture a larger share of the existing customer base.

Product Differentiation

In the consumer credit sector, Cembra Money Bank faces intense rivalry where differentiating products like personal loans, auto leases, and credit cards is tough. This often pushes competition towards price, interest rates, and fees, making it hard to stand out. For instance, in 2024, the average interest rate for personal loans in Switzerland hovered around 6-8%, a key battleground for customers.

Cembra attempts to carve out a niche by emphasizing personalized customer service, aiming to build loyalty beyond just the product's features. They also leverage a variety of distribution channels, from online platforms to partnerships, to reach a broader customer base and offer a more accessible experience.

Exit Barriers

Cembra Money Bank, like other financial institutions, faces considerable exit barriers. These include substantial investments in technology infrastructure, specialized personnel, and the ongoing costs associated with stringent regulatory compliance. For instance, the Swiss Financial Market Supervisory Authority (FINMA) imposes rigorous capital adequacy ratios and operational standards that are costly to maintain and divest from. These high fixed costs and regulatory hurdles make it difficult for less successful players to simply shut down operations, thereby keeping them in the market and potentially intensifying competition.

The banking sector is particularly susceptible to these exit barriers. Regulatory complexity is a prime example; unwinding a bank involves navigating intricate legal frameworks, managing customer data securely, and ensuring financial stability during the process. Cembra's commitment to digital transformation also represents a significant investment, creating a barrier for any competitor considering exiting the market without realizing a substantial return on these technological assets. In 2023, the Swiss banking sector saw significant consolidation, yet the underlying costs of exiting remain a deterrent for smaller or struggling entities.

- High Capital Investment: Banks require significant capital to operate, making it difficult to recoup investments upon exit.

- Regulatory Hurdles: Strict regulations from bodies like FINMA create complex and costly exit procedures.

- Technological Obsolescence: Investments in IT infrastructure can become a sunk cost if not fully utilized or transferred.

- Customer Contracts: Long-term customer agreements and data management add to the complexity of ceasing operations.

Digitalization and Innovation Pace

The financial services industry is experiencing a relentless surge in digitalization and innovation, largely fueled by agile fintech companies. This forces established players like Cembra Money Bank to constantly invest in cutting-edge technology and develop novel products to stay relevant. For instance, in 2024, global fintech investment reached an estimated $100 billion, highlighting the intense focus on technological advancement.

Failure to keep pace with these rapid changes can significantly erode a bank's market share and competitive edge. Cembra must therefore prioritize agile development and explore partnerships or acquisitions to integrate new digital capabilities. The increasing adoption of AI in customer service and risk management, with an estimated 40% of financial institutions planning to increase AI spending in 2024, underscores this imperative.

- Digital Transformation Investment: Cembra needs to allocate significant capital towards upgrading its digital infrastructure and developing user-friendly online and mobile platforms.

- Fintech Collaboration: Exploring strategic partnerships with fintech firms can provide access to specialized technologies and accelerate the introduction of new services.

- Customer Experience Focus: Innovation should be geared towards enhancing customer experience through personalized offerings, seamless onboarding, and efficient digital support channels.

- Regulatory Adaptation: Staying ahead of evolving digital regulations is crucial to ensure compliance and build trust in new technological offerings.

Swiss Finance: Price Wars & Personalized Service Drive Competition

Competitive rivalry within the Swiss consumer finance sector is fierce, with Cembra Money Bank facing pressure from traditional banks, specialized lenders, and fintechs. The market, while growing, is maturing, leading to intensified competition for customers. Differentiation is challenging, often pushing competition towards price and interest rates, with average personal loan rates around 6-8% in 2024. Cembra counters this by focusing on personalized service and diverse distribution channels.

SSubstitutes Threaten

Traditional Bank Loans and Overdrafts

Customers needing funds have readily available alternatives to Cembra Money Bank's offerings, such as personal loans and overdraft facilities from traditional retail banks. These options are often more convenient as they can be accessed through a customer's existing banking relationship.

In 2024, the Swiss banking sector saw continued competition in consumer lending, with major banks like UBS and Credit Suisse (now integrated) offering a wide range of personal loan products. For instance, personal loan interest rates from these institutions can be competitive, sometimes starting as low as 4.9% for well-qualified borrowers, directly challenging specialized lenders.

Buy Now, Pay Later (BNPL) Services

The proliferation of Buy Now, Pay Later (BNPL) services, often from fintech innovators, presents a potent substitute for conventional credit cards and personal loans, especially for everyday, smaller transactions. These flexible payment options are increasingly popular, offering consumers an alternative to traditional credit lines.

Cembra Money Bank's own engagement in offering BNPL solutions underscores its awareness of this competitive landscape and the growing consumer preference for such alternatives. This strategic move acknowledges the significant threat posed by these readily available payment methods.

For instance, by mid-2024, BNPL services facilitated billions in transactions globally, capturing a notable share of consumer spending that might otherwise have gone to traditional credit providers. This rapid adoption highlights the direct substitution effect on established financial products.

Peer-to-Peer (P2P) Lending Platforms

Online peer-to-peer (P2P) lending platforms, which directly link borrowers with investors, are emerging as a significant substitute for traditional bank loans. These platforms, while still gaining traction in Switzerland, can offer borrowers more competitive interest rates and adaptable repayment schedules compared to conventional personal loans.

In 2024, the P2P lending market continued its growth trajectory, with platforms like CreditGate24 and Cashare facilitating a growing volume of transactions. For instance, CreditGate24 reported a significant increase in loan origination volume in early 2024, demonstrating the increasing adoption of P2P lending as a viable alternative for consumer credit.

Internal Company Financing (for businesses)

For small businesses, internal financing options can act as substitutes for external credit facilities that Cembra Money Bank might offer. These include using retained earnings from profitable operations, securing equity injections directly from the business owners, or leveraging trade credit from suppliers. These internal methods can reduce a business's need to seek financing from banks like Cembra.

In 2023, a significant portion of small and medium-sized enterprises (SMEs) in Switzerland relied on internal funding. For instance, data from the Swiss Federal Statistical Office indicated that retained earnings constituted a substantial part of SME financing, lessening their dependence on external debt. This trend suggests a direct substitute for services such as invoice financing or business loans provided by financial institutions.

- Retained Earnings: Profits reinvested back into the business.

- Owner Equity: Capital contributed directly by the business owners.

- Trade Credit: Payment terms extended by suppliers, acting as short-term financing.

Savings and Self-Financing

The threat of substitutes for Cembra Money Bank's consumer credit offerings is significantly influenced by individuals' ability to self-finance purchases. This means customers can opt to use their existing savings or postpone spending altogether rather than obtaining a loan. This fundamental substitute is directly tied to broader economic conditions and prevailing consumer confidence levels. For instance, in periods of high inflation or economic uncertainty, consumers may be more inclined to rely on their own funds, reducing the demand for credit products.

In 2024, a notable trend is the increasing emphasis on personal savings, driven by a desire for financial resilience. Data from various financial institutions suggests a rise in savings rates among certain demographics, indicating a preference for self-funding. This behavioral shift presents a direct challenge to credit providers like Cembra Money Bank, as it represents a viable alternative to borrowing.

- Self-Financing as a Core Substitute: Consumers can leverage accumulated savings or delay discretionary spending, bypassing the need for external credit facilities.

- Economic Sensitivity: The attractiveness of self-financing is amplified during economic downturns or periods of high inflation, where borrowing costs may rise or future income is uncertain.

- Consumer Confidence Impact: Higher consumer confidence often correlates with a greater willingness to spend and potentially borrow, while lower confidence encourages a more conservative, savings-focused approach.

The Broadening Spectrum of Financial Alternatives

The threat of substitutes for Cembra Money Bank's offerings is substantial, encompassing traditional banking products, emerging fintech solutions, and even the customer's own financial resources. Personal loans and overdrafts from major Swiss banks, often with competitive rates like those seen in 2024 starting around 4.9%, directly compete. Buy Now, Pay Later (BNPL) services are rapidly gaining traction, facilitating billions in transactions globally by mid-2024, offering a flexible alternative for consumers. Furthermore, peer-to-peer lending platforms, such as CreditGate24 and Cashare, are growing in Switzerland, providing alternative credit avenues with potentially more adaptable terms. Even self-financing through savings or delaying purchases remains a potent substitute, particularly in uncertain economic climates where consumers prioritize financial resilience, a trend observed in 2024 with rising savings rates.

| Substitute Type | Examples | Key Characteristics | 2024 Relevance |

|---|---|---|---|

| Traditional Bank Products | Personal Loans, Overdrafts | Established relationships, often competitive rates | Major banks like UBS offer rates as low as 4.9% |

| Fintech Solutions | Buy Now, Pay Later (BNPL), P2P Lending | Convenience, flexibility, potentially lower rates | BNPL facilitated billions globally; P2P platforms like CreditGate24 saw increased origination |

| Internal Financing (for SMEs) | Retained Earnings, Owner Equity, Trade Credit | Reduces reliance on external debt | SMEs in Switzerland heavily utilized retained earnings in 2023 |

| Self-Financing | Using Savings, Postponing Purchases | Reduces need for borrowing, influenced by economic confidence | Rising savings rates observed in 2024 indicate preference for self-funding |

Entrants Threaten

Regulatory Barriers

The Swiss financial sector operates under a rigorous regulatory framework, demanding substantial capital reserves, adherence to strict licensing procedures, and continuous compliance with evolving rules. For instance, the Swiss Financial Market Supervisory Authority (FINMA) enforces robust capital adequacy ratios, often aligned with international standards like Basel III, which can require new entrants to demonstrate significant financial backing before even launching operations.

These demanding regulatory hurdles, including extensive documentation and operational readiness checks, effectively deter many potential new competitors. The cost and complexity associated with meeting these requirements, such as establishing robust anti-money laundering (AML) and know-your-customer (KYC) protocols, create a high barrier to entry. In 2024, the ongoing focus on cybersecurity and data protection further adds to the compliance burden for any aspiring financial institution in Switzerland.

Capital Requirements

Establishing a new bank or a significant consumer finance operation, like Cembra Money Bank, requires immense capital. Think millions, if not billions, to cover everything from physical branches and robust IT systems to meeting stringent regulatory capital requirements. For instance, in 2024, many European banking regulators maintained or even increased capital adequacy ratios, making it even more costly for newcomers to enter the market and compete on a level playing field.

Brand Recognition and Trust

Established players like Cembra Money Bank benefit significantly from strong brand recognition and customer trust, cultivated over years of dedicated service in the Swiss financial landscape. This deep-rooted trust acts as a formidable barrier, making it difficult for newcomers to gain a foothold.

New entrants must invest substantial resources and time to build similar credibility and trust with potential customers. For instance, in 2024, the Swiss banking sector saw continued consolidation, with smaller banks often being acquired due to their inability to compete with the scale and established reputations of larger institutions.

Economies of Scale and Experience

Existing financial institutions, including Cembra Money Bank, leverage significant economies of scale. This allows them to spread fixed costs like technology infrastructure and regulatory compliance over a larger customer base, resulting in lower per-unit operating expenses. For instance, in 2024, major Swiss banks reported operating expenses as a percentage of average total assets often below 1%, a benchmark difficult for new, smaller players to match.

New entrants often face substantial hurdles in achieving comparable cost efficiencies. Without the established volume in loan origination, risk management, and marketing, their initial operating costs per customer are likely to be considerably higher. This disadvantage in cost structure can make it challenging for them to compete on price or achieve profitability in the short to medium term.

- Economies of Scale: Established players like Cembra benefit from lower per-unit costs in operations, marketing, and technology due to their size.

- Experience Curve: Years of operation have allowed incumbents to refine processes, leading to greater efficiency and reduced errors.

- Capital Requirements: The significant capital needed to establish a competitive presence acts as a barrier, particularly for firms without a proven track record.

- Customer Acquisition Costs: New entrants typically face higher initial costs to attract customers compared to established brands with existing loyalty.

Access to Distribution Channels

Cembra Money Bank benefits from a robust distribution network, encompassing physical branches, digital platforms, and strategic alliances with car dealerships and independent brokers. This established presence presents a significant hurdle for new entrants aiming to replicate its reach and customer access.

New players would face substantial capital requirements to develop comparable distribution channels, whether through physical expansion or digital infrastructure. Alternatively, they might need to forge less established or potentially less effective partnerships to gain market traction.

- Established Network: Cembra leverages its existing infrastructure of branches and online services.

- Partnership Leverage: Strong relationships with car dealers and intermediaries provide direct customer access.

- High Entry Barriers: New entrants require significant investment to build comparable distribution capabilities.

- Cost of Customer Acquisition: Building a new distribution network can lead to higher initial customer acquisition costs for competitors.

Swiss Finance: A Fortress Against New Competitors

The threat of new entrants for Cembra Money Bank is generally considered low, primarily due to the high barriers to entry in the Swiss financial services sector. Stringent regulatory requirements, substantial capital needs, and the established brand loyalty of incumbents like Cembra create a challenging environment for newcomers.

For instance, in 2024, the Swiss Financial Market Supervisory Authority (FINMA) continued to emphasize robust capital adequacy ratios and comprehensive compliance protocols, making it financially demanding for new entities to establish themselves. This regulatory landscape, coupled with the significant investment required for technology and distribution networks, effectively deters many potential competitors.

| Barrier to Entry | Impact on New Entrants | Example for Cembra (2024 Context) |

|---|---|---|

| Regulatory Compliance | High Cost & Time Investment | Meeting FINMA's capital and operational standards requires substantial upfront capital and ongoing adherence. |

| Capital Requirements | Significant Financial Outlay | Establishing a financial institution necessitates millions in capital for infrastructure, licensing, and reserves. |

| Brand Loyalty & Trust | Difficulty in Customer Acquisition | Cembra's established reputation makes it hard for new players to attract customers without significant marketing spend. |

| Economies of Scale | Cost Disadvantage for Newcomers | Cembra's larger operational scale allows for lower per-unit costs, which new entrants struggle to match initially. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Cembra Money Bank is built upon a foundation of robust data, including Cembra's annual reports, investor presentations, and regulatory filings. We also integrate insights from industry-specific market research reports and financial news outlets to capture the competitive landscape.