Cellularline Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Cellularline

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

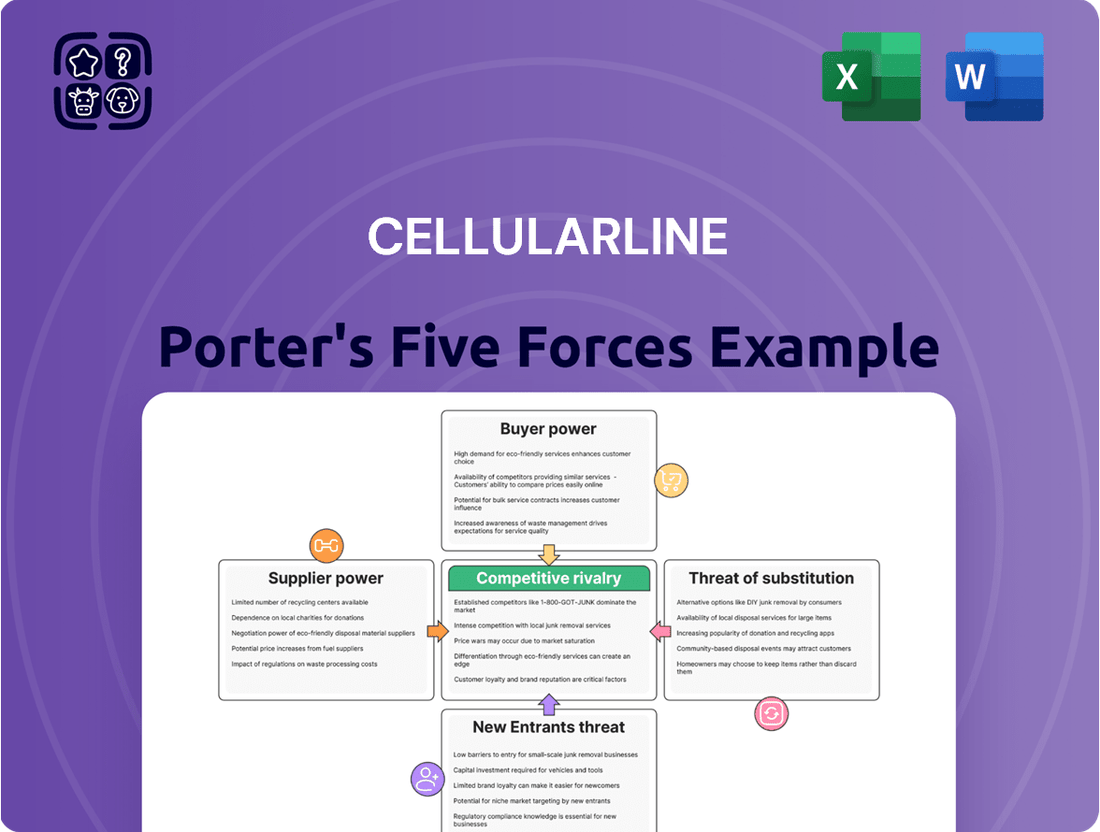

Cellularline's competitive landscape is shaped by intense rivalry, the bargaining power of buyers, and the constant threat of new entrants. Understanding these forces is crucial for navigating its market.

The complete report reveals the real forces shaping Cellularline’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration

Supplier concentration significantly impacts Cellularline's bargaining power. If the market for specialized electronic components, like advanced charging chips or unique casing materials, is dominated by a small number of manufacturers, these suppliers gain considerable leverage. For instance, in 2024, the global semiconductor market, crucial for smartphone accessories, saw a handful of companies controlling a substantial share of advanced chip production, potentially increasing costs for accessory makers like Cellularline.

Switching Costs for Cellularline

Switching suppliers for Cellularline, particularly for specialized components in their extensive mobile accessory portfolio, can incur substantial costs. These can range from the expense of redesigning products to retooling manufacturing lines and the lengthy process of re-certifying new components. For example, if a key supplier for their advanced charging technology changes, Cellularline might face millions in R&D and revalidation expenses.

These high switching costs effectively grant existing suppliers greater bargaining power. When it's difficult and costly for Cellularline to find and integrate a new supplier, the current supplier can often command higher prices or less favorable terms. This leverage is particularly pronounced for suppliers providing proprietary or highly specialized parts essential to Cellularline's product differentiation.

While Cellularline's broad product range, which includes everything from phone cases to power banks, means they likely engage with a diverse supplier base, this doesn't eliminate the risk entirely. The sheer volume of suppliers might dilute the power of any single one, but reliance on a few key suppliers for critical, high-performance components can still create significant dependencies. For instance, a sole source for a unique battery chemistry could give that supplier considerable sway.

Uniqueness of Supplier Offerings

Suppliers offering unique or patented technologies, specialized materials, or highly integrated components significantly enhance their bargaining power. For instance, if a supplier provides a proprietary fast-charging chip or a unique protective material, Cellularline's reliance on them increases. This is especially critical in a rapidly evolving market characterized by innovations like advanced wireless charging and AI integration, where specialized inputs are key differentiators.

Threat of Forward Integration by Suppliers

The threat of suppliers integrating forward into manufacturing and distributing their own branded accessories directly impacts Cellularline. If a supplier, particularly a larger electronics manufacturer, decides to enter the accessories market, they could compete directly with Cellularline. This scenario is less common for basic component suppliers but becomes a more significant concern if component standardization allows for easier entry.

While the threat of forward integration by suppliers is generally considered low for Cellularline, it's not entirely absent. For instance, if the market for specific smartphone accessories, like charging cables or cases, sees a significant increase in standardized components, larger electronics firms that supply these components might find it economically viable to develop and market their own branded accessory lines. This could potentially increase competitive pressure on Cellularline, especially if these suppliers leverage their existing brand recognition and distribution channels. In 2023, the global mobile accessories market was valued at approximately $25 billion, indicating a substantial market that could attract new entrants or encourage existing players to expand their offerings.

- Supplier Forward Integration: Suppliers moving into manufacturing and selling their own branded accessories poses a direct competitive threat to Cellularline.

- Potential Entrants: Larger electronics manufacturers, rather than simple component providers, are the primary potential actors for forward integration.

- Impact of Standardization: High standardization of components can lower the barrier to entry for suppliers, thus increasing this threat.

- Market Context: The significant size of the mobile accessories market, estimated to be worth billions, makes such integration a possibility for well-positioned suppliers.

Importance of Cellularline to Suppliers

Cellularline's significance to its suppliers plays a crucial role in determining supplier bargaining power. If Cellularline constitutes a substantial portion of a supplier's overall revenue, that supplier might exhibit less power, as they would be more dependent on maintaining their relationship with Cellularline. This dependence can lead to more favorable terms for Cellularline.

Conversely, for large, diversified suppliers of electronic components, Cellularline might represent only a small fraction of their business. In such scenarios, the supplier's bargaining power increases. They are less reliant on Cellularline and can therefore exert more pressure on pricing and terms, potentially impacting Cellularline's cost of goods sold.

For instance, in 2024, the global market for electronic components was valued at over $2.7 trillion, with many suppliers serving a wide array of industries beyond just mobile accessories. This broad customer base for component manufacturers generally shifts power towards these suppliers when dealing with individual companies like Cellularline, unless Cellularline can secure exceptionally large, exclusive orders that make them a key client.

- Supplier Dependence: If Cellularline is a major client, suppliers have less leverage.

- Market Diversification: If suppliers serve many clients, their power over Cellularline is enhanced.

- Component Market Size: The vast global electronic component market in 2024 suggests many suppliers have diverse customer bases.

Supplier Power: Decoding Component Control and Influence

The bargaining power of suppliers for Cellularline is influenced by several factors, including supplier concentration, switching costs, and the uniqueness of their offerings. When a few suppliers dominate the market for critical components, like specialized chips in 2024, they gain leverage. High switching costs for Cellularline, due to redesign and revalidation needs, further empower these suppliers.

Suppliers who provide proprietary technologies or unique materials significantly increase their bargaining power. For example, a sole provider of a unique battery chemistry could dictate terms. While Cellularline's diverse product range might dilute the power of individual suppliers, reliance on key component providers remains a significant factor.

| Factor | Impact on Cellularline | Example/Data (2024) |

| Supplier Concentration | High concentration = High supplier power | Few companies control advanced chip production. |

| Switching Costs | High costs = High supplier power | Millions in R&D/revalidation for new charging tech. |

| Uniqueness of Offering | Proprietary tech = High supplier power | Unique fast-charging chips or materials. |

| Supplier Dependence | Cellularline is a small client = High supplier power | Global component market ($2.7T+) means many suppliers serve diverse industries. |

What is included in the product

This analysis dissects the competitive forces impacting Cellularline, evaluating the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry within the mobile accessories market.

Instantly visualize competitive intensity with a dynamic five forces dashboard, highlighting key pressure points for Cellularline.

Customers Bargaining Power

Price Sensitivity of Customers

Customers in the smartphone accessories market, especially for everyday items like cases and screen protectors, often exhibit high price sensitivity. This is largely due to the wide availability of numerous alternatives, including cheaper, unbranded, and even counterfeit options, which directly impacts Cellularline's pricing strategies and profit margins.

Availability of Substitutes for Customers

Customers considering smartphone accessories like cases, chargers, and headphones have a vast selection available. They can choose from budget-friendly, unbranded options, accessories directly from smartphone makers like Apple or Samsung, or products from well-known third-party brands such as Anker or Belkin. This abundance of alternatives means customers can easily switch if they find a better price or feature set elsewhere.

The ease with which customers can access these substitutes, whether through major online retailers like Amazon or Best Buy, or even direct-to-consumer websites, further amplifies their bargaining power. For instance, in 2024, the global market for mobile phone accessories was estimated to be worth over $250 billion, indicating a highly competitive landscape where consumers have significant leverage due to the sheer volume of choices and competitive pricing strategies employed by manufacturers and sellers.

Customer Information and Transparency

The internet and e-commerce have dramatically increased market transparency for consumers. Customers can now easily access detailed product information, compare prices across numerous retailers, and read reviews from other buyers. This readily available data empowers them to make more informed decisions, putting pressure on companies like Cellularline to offer competitive pricing and superior value.

Low Switching Costs for Customers

For most smartphone accessories, the cost and effort for a customer to switch from one brand to another are very low. There's little loyalty penalty for trying a different brand of charger, case, or headphones, which amplifies customer power. This encourages constant innovation and competitive pricing from companies like Cellularline.

This low switching barrier means customers can easily explore alternatives, putting pressure on brands to offer compelling value. For instance, a customer might switch from a €30 Cellularline case to a €25 competitor if the features are comparable, directly impacting market share and pricing strategies.

- Low Switching Costs: Customers face minimal financial or effort-based barriers when changing accessory brands.

- Brand Loyalty Impact: The ease of switching reduces brand loyalty, making customers more price-sensitive and open to new entrants.

- Competitive Pricing: This dynamic forces companies like Cellularline to maintain competitive pricing and continuously innovate to retain customers.

Volume of Purchases by Customers

While individual consumers usually buy small quantities, Cellularline’s direct customers, such as major retail chains and significant online distributors, purchase products in much larger volumes. This substantial purchasing power allows these large buyers to negotiate more favorable terms, including lower prices and enhanced service expectations, directly impacting Cellularline’s profitability.

For instance, in 2024, large electronics retailers in Europe, a key market for Cellularline, accounted for over 60% of accessory sales. These retailers often consolidate their purchasing power, demanding volume discounts and exclusive product offerings, thereby increasing their leverage over suppliers like Cellularline.

- High Volume Purchases: Major retail chains and online distributors are Cellularline's primary direct customers, driving significant sales volume.

- Negotiating Power: These large buyers leverage their volume to demand better pricing, payment terms, and service levels from Cellularline.

- Market Influence: Their substantial orders can influence Cellularline's production schedules and product development priorities.

- 2024 Data Context: In 2024, large retailers represented a significant portion of accessory sales in key European markets, underscoring their bargaining strength.

Customer Power Shapes Accessory Market

The bargaining power of customers in the smartphone accessory market is substantial, driven by low switching costs and the availability of numerous alternatives. This allows consumers to easily shift between brands based on price and features, pressuring companies like Cellularline to remain competitive. For example, the global mobile phone accessory market's value exceeding $250 billion in 2024 highlights the intense competition consumers face, granting them significant leverage.

Furthermore, Cellularline's large wholesale customers, such as major electronics retailers, wield considerable influence due to their high-volume purchases. In 2024, these large retailers accounted for over 60% of accessory sales in key European markets, enabling them to negotiate favorable pricing and terms, directly impacting Cellularline's profit margins and strategic decisions.

| Customer Segment | Bargaining Power Factors | Impact on Cellularline |

|---|---|---|

| Individual Consumers | Low switching costs, high price sensitivity, access to abundant alternatives | Pressure on pricing, need for continuous product differentiation |

| Wholesale Customers (e.g., Retail Chains) | High purchase volumes, consolidation of buying power | Negotiation of discounts, favorable payment terms, influence on product mix |

Same Document Delivered

Cellularline Porter's Five Forces Analysis

This preview showcases the complete Cellularline Porter's Five Forces Analysis, providing a thorough examination of the competitive landscape. The document displayed here is the exact, professionally formatted report you'll receive immediately after purchase, ensuring no discrepancies or missing information. You're looking at the actual, ready-to-use analysis, which will be instantly accessible for your strategic planning needs.

Rivalry Among Competitors

Number and Diversity of Competitors

The smartphone accessories market is incredibly crowded, with a vast array of companies vying for consumer attention. This includes giants like Apple and Samsung, who offer their own branded accessories, alongside numerous specialized brands catering to various niches and price points. For instance, in 2024, the global smartphone accessories market was valued at approximately USD 25.8 billion and is projected to grow significantly.

This sheer number and variety of competitors, from high-end designers to budget-friendly manufacturers, create intense pressure on companies like Cellularline. The presence of both integrated device manufacturers and independent accessory makers means that rivalry spans across product categories and distribution channels, making it challenging to maintain market share and pricing power.

Industry Growth Rate

The mobile accessories market is showing consistent growth, with forecasts pointing to further expansion. For instance, the global mobile accessories market was valued at approximately $25.7 billion in 2023 and is expected to reach over $40 billion by 2030, growing at a compound annual growth rate (CAGR) of around 6.5% during this period.

This steady upward trend, while generally positive, doesn't eliminate intense competition. The sheer size of the market, which is already in the tens of billions of dollars, naturally draws in new companies and motivates established ones to fight harder for their piece of the pie.

Product Differentiation

Cellularline faces a significant challenge in differentiating its smartphone accessories. Many products offer similar basic features, making it tough to stand out. For instance, in 2024, the global smartphone accessory market, valued at over $250 billion, saw a substantial portion driven by functional, rather than truly innovative, products.

The company strives to differentiate through its emphasis on design aesthetics, perceived quality, and building a strong brand image. They also explore innovation, such as developing accessories with AI capabilities or focusing on sustainable materials. However, the relatively low barriers to entry for many accessory categories mean that competitors can often replicate features quickly, intensifying competition, particularly on price.

Exit Barriers

Exit barriers in the smartphone accessories market, while not universally insurmountable, present a notable challenge for established firms like Cellularline. Significant investments in specialized manufacturing equipment, dedicated supply chains, and extensive brand building contribute to these barriers.

For Cellularline, the cost of exiting the market would likely involve substantial write-offs of specialized assets and potential damage to its brand reputation built over years of operation. This financial and reputational risk incentivizes continued competition, even when market conditions are unfavorable, as staying in the market might be perceived as less costly than a complete withdrawal.

Consider these factors contributing to exit barriers:

- Specialized Assets: Investments in manufacturing lines tailored for specific accessory types can be difficult to repurpose or sell at their book value.

- Brand Equity: The cost and effort invested in building brand recognition and customer loyalty mean that abandoning the market would forfeit this valuable intangible asset.

- Contractual Obligations: Existing distribution agreements, supplier contracts, and leases can impose financial penalties for early termination.

- Reputational Costs: A disorderly exit can negatively impact a company's standing with suppliers, distributors, and future potential markets.

Brand Identity and Loyalty

While a portion of consumers demonstrates strong brand loyalty, especially for premium accessories that complement specific technology ecosystems, many are more price-sensitive or convenience-driven for generic items. For instance, a 2024 report indicated that while 60% of smartphone users consider brand reputation when buying accessories, only 35% prioritize it over price for non-essential items.

Cellularline's approach of utilizing a multi-brand strategy is designed to appeal to diverse consumer preferences and foster loyalty across different market segments. However, this strategy contends with a market where brand perception can shift rapidly, making sustained loyalty a challenge.

- Brand Loyalty Factors: Consumers often exhibit loyalty to brands offering seamless integration or perceived higher quality, particularly within established tech ecosystems.

- Price Sensitivity: For many, especially with more commoditized accessories, price and immediate availability are primary purchasing drivers.

- Cellularline's Strategy: The company employs a multi-brand portfolio to capture various market niches and build brand affinity.

- Market Dynamics: The accessory market is characterized by fluid brand identity, requiring continuous effort to maintain consumer engagement and loyalty.

Smartphone Accessory Market: Fierce Rivalry, Growth, and Price Wars

Competitive rivalry in the smartphone accessories market is exceptionally fierce, driven by a multitude of players ranging from global tech giants to smaller, specialized brands. This intense competition, evident in the market's projected growth from approximately USD 25.8 billion in 2024 to over USD 40 billion by 2030, forces companies like Cellularline to constantly innovate and differentiate to capture market share.

The presence of numerous competitors, many with similar product offerings and varying price points, intensifies pressure on pricing and profit margins. For instance, in 2024, the global smartphone accessory market saw significant activity from both established brands and emerging players, making it challenging to maintain a competitive edge without continuous product development and effective marketing strategies.

Companies must navigate a landscape where differentiation is key, yet many products offer comparable functionality. Cellularline's efforts to stand out through design and brand building are crucial, but the ease with which competitors can replicate features means that price often becomes a significant factor in consumer purchasing decisions, further fueling rivalry.

SSubstitutes Threaten

Functionality of Core Devices

As smartphones and tablets become more powerful, they can absorb functions previously handled by accessories. For example, advancements in mobile photography might decrease reliance on separate camera accessories.

Improved battery efficiency in 2024 smartphones, with many flagship models now exceeding 4500 mAh, could indeed reduce the perceived need for external power banks for everyday users.

Similarly, the integration of high-quality speakers and advanced audio processing in devices like the latest iPhone and Samsung Galaxy models might lessen the demand for some portable Bluetooth speakers.

Multi-functional Devices

The increasing prevalence of multi-functional devices poses a significant threat of substitution for individual accessories. For instance, smartwatches now integrate health tracking, communication, and even payment functions, directly competing with dedicated fitness trackers and basic smart bands. This convergence means consumers can potentially consolidate multiple single-purpose gadgets into one, reducing the demand for specialized accessories.

Furthermore, the push towards universal connectivity and charging standards, such as USB-C, diminishes the need for a wide array of proprietary cables and chargers. In 2024, the market saw continued adoption of these universal standards across smartphones, laptops, and tablets, making it easier for users to rely on a single charging solution, thereby substituting the market for numerous single-purpose charging accessories.

Generic or Unbranded Alternatives

The market for smartphone accessories is saturated with generic, unbranded options that often come at a significantly lower price point. These alternatives, while potentially lacking in quality control or warranty support, directly compete with established brands like Cellularline, especially for budget-conscious buyers.

DIY Solutions or Minimalist Trends

The rise of DIY solutions and minimalist trends presents a subtle but growing threat to accessory makers like Cellularline. Some consumers are embracing a less-is-more philosophy, opting to use their smartphones without protective cases, thereby bypassing the need for purchases. This trend is amplified by the availability of readily accessible, often cheaper, generic components or DIY repair kits, which can reduce reliance on branded accessories for minor fixes or replacements.

While the market for complex electronic accessories remains largely insulated from DIY, simpler items like chargers or basic screen protectors can be affected. For instance, a significant portion of consumers may choose to stick with the charger included in their device's original packaging rather than purchasing an aftermarket one. This avoidance of additional accessory purchases directly impacts the potential revenue streams for companies in this sector.

- Minimalist Consumer Behavior: A segment of consumers actively avoids protective cases, reducing demand for products like those offered by Cellularline.

- DIY Repair and Generic Components: Availability of cheaper alternatives and self-repair options can substitute for purchasing new, branded accessories, particularly for simpler items.

- Impact on Charger Market: Many users continue to use manufacturer-provided chargers, limiting the market penetration for third-party charger sales.

Technological Advancements in Core Devices

Rapid technological advancements in smartphones present a significant threat of substitutes for accessory makers like Cellularline. For instance, the increasing durability of core devices, such as the widespread adoption of Corning's Gorilla Glass Victus and Victus 2, which offer enhanced scratch and drop resistance, might lessen consumer demand for separate screen protectors. This trend was evident in 2024 as manufacturers continued to prioritize robust build quality in their flagship models.

Furthermore, the integration of advanced charging solutions directly into everyday environments poses another substitution risk. As wireless charging capabilities become more prevalent in public spaces, office furniture, and automotive interiors, the necessity for portable power banks, a key product category for Cellularline, could diminish. By mid-2024, many new vehicle models offered integrated Qi wireless charging pads, reducing the need for users to carry separate charging devices.

These technological shifts create substitute solutions that bypass traditional accessory markets:

- Enhanced Smartphone Durability: Improved screen glass and water resistance reduce the perceived need for protective cases and screen protectors.

- Ubiquitous Wireless Charging: Integration of charging technology into furniture and vehicles offers convenient power without external accessories.

- Built-in Device Features: Advancements in smartphone battery technology and power management can extend usage times, decreasing reliance on supplementary power sources.

Core Devices Replace Traditional Accessories

The increasing self-sufficiency of core devices, particularly smartphones, directly substitutes for many traditional accessories. For example, enhanced battery life in 2024 models, with many premium phones now offering over 5000 mAh capacity, lessens the need for portable power banks. Similarly, the integration of advanced camera systems and high-fidelity audio components within smartphones reduces the demand for specialized camera lenses or portable speakers.

The trend towards consolidated functionality means consumers can often achieve similar outcomes with their primary device, bypassing the need for add-on accessories. Smartwatches, for instance, now offer robust fitness tracking and contactless payment, directly competing with dedicated fitness trackers and wallet accessories. This convergence, accelerated by advancements in processing power and sensor technology throughout 2024, allows users to carry fewer items.

The market faces substitution from both technological integration within devices and evolving consumer behavior. As smartphones become more durable, with advanced screen protection like Gorilla Glass Victus 2 common in 2024 flagships, the demand for screen protectors may decrease. Concurrently, a growing minimalist segment of consumers is opting out of protective cases altogether, reducing the market for these items.

| Accessory Category | Substituting Factor | Impact on Demand |

|---|---|---|

| Power Banks | Improved smartphone battery capacity (e.g., 5000+ mAh in 2024 models) | Decreased |

| Screen Protectors | Enhanced smartphone screen durability (e.g., Gorilla Glass Victus 2) | Decreased |

| Portable Speakers | Integrated high-fidelity audio in smartphones | Decreased |

| Fitness Trackers | Advanced health monitoring in smartwatches | Decreased |

Entrants Threaten

Low Capital Requirements for Basic Accessories

The threat of new entrants in the cellular accessories market is amplified by low capital requirements for basic items. For instance, producing simple phone cases or charging cables often necessitates minimal upfront investment, especially when leveraging existing manufacturing infrastructure in countries like China, where production costs are competitive.

This accessibility allows numerous small businesses and startups to enter the market, particularly those focusing on niche designs or budget-friendly options. In 2024, the global market for mobile phone accessories was valued at over $250 billion, indicating substantial opportunity but also a crowded landscape where new, low-cost entrants can quickly gain traction.

Access to Distribution Channels

New entrants into the mobile accessories market, like Cellularline, can bypass traditional retail gatekeepers by utilizing robust online marketplaces and direct-to-consumer e-commerce platforms. This dramatically reduces the capital and effort required to establish a sales presence. For instance, in 2024, the global e-commerce market reached an estimated $6.3 trillion, demonstrating the vast reach available to new players through digital channels.

The ability to leverage platforms such as Amazon, eBay, and even specialized tech retailers' online stores means that a new company doesn't need to negotiate shelf space in physical stores, a historically significant barrier. This accessibility to distribution channels fundamentally lowers the threat of new entrants, making it easier for innovative brands to gain traction and market share without the legacy costs associated with physical retail networks.

Brand Recognition and Loyalty

Established players like Cellularline have cultivated significant brand recognition and customer loyalty, making it difficult for newcomers to break in. In 2024, the smartphone accessory market continues to be dominated by brands with strong recall, with studies showing that over 70% of consumers consider brand reputation when purchasing these items.

New entrants must overcome the hurdle of building trust and differentiating their offerings in a saturated landscape. While this presents a challenge, innovative marketing campaigns, distinctive product features, or competitive pricing strategies, as seen with some direct-to-consumer brands in 2023, can still allow new players to capture market share.

Technological Know-how and R&D

While the market for basic smartphone accessories might seem accessible, the development of advanced or specialized products presents a significant barrier to new entrants. Companies need substantial investment in research and development (R&D) and a deep understanding of cutting-edge technology to create innovative items like AI-powered cases or high-fidelity audio peripherals.

This technological know-how is crucial because it directly impacts product differentiation and performance. For instance, in 2024, the demand for smart accessories integrating IoT capabilities is growing, requiring expertise in areas like miniaturized electronics and software integration. Without this specialized knowledge, new players struggle to compete effectively against established brands with proven R&D capabilities.

- High R&D Investment: Developing advanced accessories requires significant capital outlay for research, prototyping, and testing, often running into millions of dollars for innovative product lines.

- Technological Expertise: Entry into sophisticated segments like audio or power solutions demands specialized engineering skills and a proven track record in product development.

- Intellectual Property: Patents and proprietary technologies developed through R&D create a competitive moat, making it harder for new entrants to replicate successful products.

Supply Chain Access and Relationships

Newcomers face significant hurdles in securing reliable access to essential components and building robust supply chains. Established players, such as Cellularline, benefit from pre-existing, strong relationships with suppliers and well-developed global logistics networks. These established connections provide a distinct advantage, making it difficult for new entrants to match the efficiency and cost-effectiveness of existing operations.

For instance, in 2024, the semiconductor shortage continued to impact the electronics industry, highlighting the critical nature of supplier relationships. Companies with long-standing contracts and preferred supplier status, like those Cellularline likely possesses, were better positioned to navigate these disruptions. New entrants would struggle to secure the same volume and quality of components at competitive prices without these established ties.

- Established Supplier Relationships: Cellularline likely has deep, long-term partnerships with key component manufacturers, ensuring consistent supply and potentially better pricing.

- Global Logistics Expertise: Years of operation have allowed Cellularline to refine its international shipping and distribution processes, minimizing transit times and costs.

- Barriers to Entry: The difficulty in replicating these established supply chain networks and supplier relationships presents a substantial barrier for potential new competitors in the mobile accessories market.

New Entrants: Moderate Threat, Established Market Barriers

The threat of new entrants for Cellularline is moderate. While the market for basic accessories has low capital requirements and accessible e-commerce channels, established brand loyalty and the need for R&D in advanced products create significant barriers. Securing reliable supply chains and components also poses a challenge for newcomers.

| Factor | Impact on New Entrants | Relevance to Cellularline |

|---|---|---|

| Capital Requirements | Low for basic items, high for advanced tech. | Cellularline benefits from established R&D for advanced products. |

| Distribution Channels | E-commerce offers broad access. | Cellularline leverages both online and established retail presence. |

| Brand Loyalty & Differentiation | High barrier for new entrants. | Cellularline benefits from strong brand recognition. |

| Supplier Access & Logistics | Difficult for new players to replicate. | Cellularline has established, efficient supply chains. |

Porter's Five Forces Analysis Data Sources

Our Cellularline Porter's Five Forces analysis is built upon a foundation of verified data, including company annual reports, industry-specific market research from firms like Statista and IBISWorld, and regulatory filings.