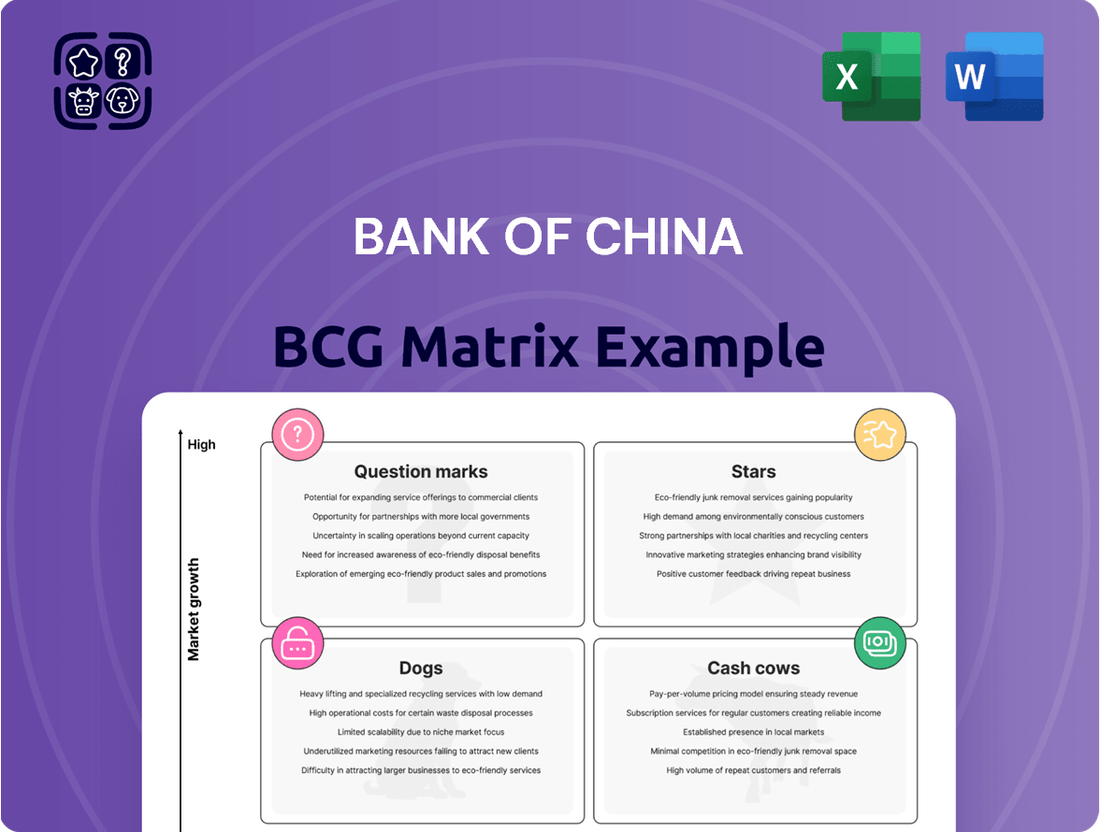

Bank of China Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Bank of China Bundle

Unlock Strategic Clarity

Unlock the strategic potential of the Bank of China with a comprehensive BCG Matrix analysis. Understand which of its offerings are driving growth (Stars), generating stable income (Cash Cows), requiring careful consideration (Question Marks), or potentially underperforming (Dogs). This preview offers a glimpse into their market positioning, but for actionable insights and a clear roadmap to optimize your investment and product strategies, dive into the full report.

Gain a competitive edge by understanding the Bank of China's product portfolio through its complete BCG Matrix. This detailed breakdown will reveal the current status of each business unit, empowering you to make informed decisions about resource allocation and future growth. Purchase the full version for data-driven recommendations and a strategic blueprint to navigate the evolving financial landscape.

Stars

Green Finance Initiatives

Bank of China's commitment to green finance positions it strongly within the BCG Matrix. In 2024, its green credit loans surged to RMB 4.07 trillion, a remarkable 31.03% year-over-year increase. This substantial growth underscores its leadership in this burgeoning sector.

The bank's strategic objective to have green finance constitute over 30% of its total loan portfolio by 2025 further solidifies its Star status. This ambitious target aligns with national environmental sustainability mandates, indicating a clear pathway for continued investment and expansion in green initiatives.

The high growth rate and dominant market share in green finance suggest that Bank of China's green finance operations are a significant Star. While requiring substantial capital for ongoing development and market penetration, these initiatives are poised to generate considerable future returns, reflecting a strong investment proposition.

Cross-border RMB Services

Cross-border RMB Services represent a significant growth area for Bank of China. The increasing global adoption of the Renminbi in international trade and finance, with cross-border RMB settlement exceeding RMB 16 trillion in 2024, a notable 26.27% year-on-year rise, highlights this trend. Bank of China, with its robust global presence, is strategically positioned to capitalize on this expansion, further solidifying the RMB's status as the fourth most utilized currency in global payments by the close of 2024.

Belt and Road Initiative (BRI) Financing

Bank of China is a key financier for the Belt and Road Initiative (BRI), with 2024 marking a period of intensified project involvement, especially in green and technology-focused areas. The bank's commitment is underscored by its issuance of the first sustainable development bonds for BRI countries in June 2024, signaling a strategic focus on high-growth, impactful projects.

Corporate Lending to Strategic Emerging Industries

Bank of China (BOC) is strategically channeling significant capital into emerging industries, a move that aligns with national economic priorities and positions the bank for future growth. This focus is evident in its lending activities, which are increasingly directed towards sectors identified as crucial for China's technological advancement and sustainable development.

In 2024, BOC witnessed a substantial surge in its corporate lending to strategic emerging industries, with an impressive increase of 26.31%. This robust growth underscores the bank's commitment to fostering innovation and supporting key sectors of the Chinese economy. Such a concentrated effort not only bolsters these nascent industries but also solidifies BOC's market position as a key financial partner in these high-potential areas.

- BOC's lending to strategic emerging industries grew by 26.31% in 2024.

- This reflects a strong commitment to supporting China's innovation-driven economic transformation.

- The bank is actively increasing its market share in rapidly developing, high-growth sectors.

- These investments aim to solidify BOC's leadership in critical industrial areas driving future economic expansion.

Digital Yuan (E-CNY) Integration and Development

Bank of China (BOC) is a significant player in the digital yuan (e-CNY) ecosystem, demonstrating strong leadership in adoption and integration. Its commitment to digital finance positions it favorably in this rapidly evolving sector.

BOC leads its peers in e-CNY consumption, reflecting substantial user engagement and merchant adoption. This dominance is crucial as the digital yuan's utility expands, particularly in international trade.

- E-CNY Consumption Leadership: Bank of China reported a leading position among its peers in e-CNY consumption volume, indicating robust user adoption and transaction activity.

- Vendor Acceptance Growth: The bank has actively promoted e-CNY acceptance among merchants, significantly broadening the usability of the digital currency.

- Cross-Border Trade Potential: BOC is strategically leveraging the e-CNY for cross-border transactions, aiming to capitalize on benefits like faster settlements and reduced transaction costs, a market with projected substantial growth.

- Securing Market Position: Through these initiatives, BOC is solidifying its leading role in the burgeoning digital yuan market, particularly within the context of international trade finance.

Green Finance: A Shining Star for BOC!

Bank of China's green finance initiatives are a clear Star in its BCG Matrix. With green credit loans reaching RMB 4.07 trillion in 2024, marking a 31.03% year-over-year increase, BOC demonstrates significant market leadership and high growth potential in this sector.

The bank’s strategic focus on expanding its green finance portfolio to over 30% of its total loans by 2025, coupled with its substantial growth in lending to strategic emerging industries (up 26.31% in 2024), further solidifies its Star position. These areas require ongoing investment but promise substantial future returns.

BOC's leading role in e-CNY consumption and its active promotion of vendor acceptance highlight its strength in digital finance, another key Star. This segment, with its potential for cross-border trade expansion, requires continued capital infusion to maintain its growth trajectory and market dominance.

| Business Unit | Market Share | Growth Rate | Cash Flow | Strategic Importance |

|---|---|---|---|---|

| Green Finance | High | High (31.03% in 2024) | Needs Investment (Investing) | High (National Priority) |

| Strategic Emerging Industries Lending | Growing | High (26.31% in 2024) | Needs Investment (Investing) | High (Innovation Driver) |

| Digital Yuan (e-CNY) Ecosystem | Leading | High | Needs Investment (Investing) | High (Future of Finance) |

What is included in the product

This BCG Matrix overview for Bank of China identifies strategic positioning for its business units, offering insights into investment and divestment decisions.

Visualizes Bank of China's portfolio, easing strategic decision-making by highlighting underperforming units.

Cash Cows

Traditional Corporate Banking

Bank of China's traditional corporate banking, encompassing general corporate lending and deposits, is a cornerstone of its business, acting as a significant cash cow. This segment provides a stable and substantial revenue stream, reflecting its deep roots in the Chinese economy.

In 2024, domestic RMB corporate loans for Bank of China surpassed RMB 12 trillion, underscoring its dominant position in a mature market. Despite a general slowdown in loan growth across Chinese banks, these established operations continue to be highly profitable.

The consistent generation of strong cash flow from this segment requires relatively minimal additional promotional investment. This stability allows Bank of China to allocate resources effectively to other areas of its business, reinforcing its status as a cash cow.

Traditional Personal Banking Deposits

Bank of China's traditional personal banking deposits, encompassing savings accounts and basic checking, represent a significant Cash Cow. This segment benefits from a vast and loyal individual consumer base, providing a stable and cost-effective funding source. In 2024, BOC continued to leverage this strength, with personal deposits forming a substantial portion of its liabilities, underpinning its lending activities.

The market for traditional deposits is mature, characterized by high penetration rates. While growth may be modest, the consistency of these funds is crucial for BOC's financial resilience. This segment reliably generates predictable cash flows, essential for supporting other, more growth-oriented business units within the bank's broader portfolio.

Established International Settlement Services

Bank of China's established international settlement services, a cornerstone of its global operations, function as a classic cash cow. These services leverage BOC's extensive and long-standing international network, facilitating high transaction volumes that are crucial for global trade and finance.

This mature business segment consistently generates substantial non-interest income for the bank. For instance, in 2023, Bank of China reported a significant portion of its revenue stemming from fee and commission income, with international settlement playing a key role in this. The bank's vast global presence, with branches in numerous countries, underpins its ability to offer these reliable and high-volume services without the need for significant new capital expenditures.

Mature Investment Banking Underwriting

Bank of China's mature investment banking underwriting services, focusing on equity and debt offerings for large corporations, represent a classic Cash Cow. These operations are well-established, leveraging extensive experience and a strong client base to secure significant market share in a stable, albeit slower-growing, segment of the financial industry.

These underwriting activities consistently generate substantial fee-based revenue for Bank of China. For instance, in 2024, the global investment banking league tables saw significant activity in debt underwriting, with major banks participating in multi-billion dollar issuances. While specific BOC figures for 2024 underwriting fees are not publicly detailed in this context, the general trend indicates robust deal flow for established players.

- Established Market Position: Bank of China has a long-standing presence and deep relationships within the corporate sector, facilitating consistent deal flow in equity and debt capital markets.

- Reliable Fee Generation: Underwriting services, though mature, provide a steady stream of predictable income through arrangement fees and commissions.

- Strong Corporate Client Base: The bank's ability to underwrite large issuances for major corporations underscores its capacity and reputation in this segment.

- Contribution to Overall Revenue: While not a high-growth area, the stability and volume of underwriting contribute significantly to the bank's overall profitability and market standing.

Large-Scale Asset Management for Institutional Clients

Bank of China's large-scale asset management for institutional clients acts as a significant cash cow. This division leverages established relationships and a dominant market position to generate consistent fee income. In 2024, the bank continued to manage substantial assets under management (AUM) for corporations and institutions, translating into reliable revenue streams.

- Steady Fee Income: The management of substantial AUM for institutional clients provides a predictable and stable source of fee-based revenue for Bank of China.

- Mature Market Dominance: BOC's strong market share in this segment allows it to effectively capitalize on existing client bases and mature market dynamics for consistent returns.

- Relationship-Driven Business: The success of this cash cow relies heavily on long-standing relationships with large corporate and institutional entities, fostering loyalty and continued business.

- Low Investment Needs: As a mature business, this segment requires relatively lower investment for growth compared to other areas, maximizing its cash-generating potential.

FX Trading: A Steady Stream of Revenue for the Bank

Bank of China's foreign exchange trading desk, a well-established operation, functions as a significant cash cow. It capitalizes on BOC's extensive global network and deep market expertise to facilitate high volumes of currency transactions for its corporate and institutional clients.

This segment consistently generates substantial revenue through spreads and commissions. For instance, in 2024, global foreign exchange trading volumes remained robust, with major financial institutions reporting significant income from these activities. Bank of China's strong international presence allows it to capture a considerable share of this market, requiring minimal incremental investment for sustained profitability.

The stability of foreign exchange operations stems from their integral role in international trade and investment, providing a predictable cash flow. This segment's maturity means it demands less capital for expansion, allowing BOC to reinvest profits into higher-growth areas.

| Segment | Role in BCG Matrix | Key Characteristics | 2024 Data/Observation |

|---|---|---|---|

| Foreign Exchange Trading | Cash Cow | High volume, established network, stable revenue | Robust global FX trading volumes, significant income for major institutions. |

What You’re Viewing Is Included

Bank of China BCG Matrix

The Bank of China BCG Matrix preview you are currently viewing is the precise, unwatermarked document you will receive upon purchase. This comprehensive analysis, meticulously prepared, will be delivered instantly and is ready for immediate integration into your strategic planning. You will gain access to the complete, professionally formatted report, enabling you to leverage its insights without any further editing or modification.

Dogs

Niche Overseas Retail Banking Operations

Niche overseas retail banking operations, like Bank of China's presence in specific markets such as Malaysia's consumer banking sector, often represent a low market share. In 2024, many mature international retail markets are highly competitive, limiting growth prospects for smaller players.

These segments can require significant investment for relatively modest returns, placing them in the Dogs category of the BCG matrix. For instance, if Bank of China's Malaysian retail banking segment captured only 1.5% of the market in 2024, and the overall market growth was a mere 2%, it would fit this profile.

Maintenance of Legacy IT Systems

Bank of China's legacy IT systems, while not products, represent a significant operational challenge. These systems, crucial for ongoing operations, demand substantial IT expenditure for maintenance and modernization, often consuming a considerable portion of the bank's technology budget. In 2023, for instance, many global banks reported that maintaining aging infrastructure accounted for over 60% of their IT spending, a figure likely mirrored by Bank of China.

These legacy systems are costly to run and update, offering little to no direct revenue growth. Furthermore, their inherent inflexibility can impede the bank's ability to adapt quickly to market changes or implement new digital initiatives, effectively acting as a drag on overall resource allocation and strategic agility.

Non-Performing Loans (NPLs) from Distressed Sectors

Non-performing loans (NPLs) from distressed sectors, such as the struggling Chinese property market, represent a significant challenge for Bank of China. These legacy assets, often linked to industries that once thrived but are now facing downturns, tie up valuable capital and demand considerable management resources, typically generating minimal or even negative returns.

As of the end of 2023, the Chinese banking sector continued to grapple with asset quality issues, with NPL ratios remaining a key concern. While specific figures for Bank of China's exposure to distressed sectors like property are closely monitored, the broader trend indicates that these problematic loans can hinder growth and profitability by consuming capital that could otherwise be deployed in more promising ventures.

Underperforming Traditional Branch Networks

Bank of China's traditional branch networks, particularly those in less urbanized regions, are facing challenges as digital banking gains traction. This shift can lead to reduced foot traffic for routine transactions, making the upkeep of these physical locations a costly, low-yield proposition unless they are strategically repurposed.

For instance, while overall digital transactions surged, a significant portion of Bank of China's physical branches might still represent a substantial portion of its operational costs. In 2024, the trend of declining in-branch transactions for basic services continued, impacting the profitability of branches primarily serving these functions.

- Declining Transaction Volume: Many traditional branches are seeing fewer customers for basic services like deposits and withdrawals, with digital channels handling a larger share.

- High Maintenance Costs: The fixed costs associated with maintaining a large physical network, including rent, utilities, and staffing, remain substantial.

- Strategic Repurposing Needed: To counter underperformance, branches need to evolve into advisory hubs, wealth management centers, or community engagement points rather than just transactional centers.

Highly Commoditized, Undifferentiated Products

Certain basic financial products or services offered by Bank of China, due to intense competition, may have become highly commoditized with little room for differentiation. These segments typically generate low profit margins and exhibit minimal growth prospects unless a significant strategic shift is undertaken.

For instance, basic savings accounts or standard checking services, widely available across numerous financial institutions, often fall into this category. In 2024, the average interest rate for savings accounts in China remained relatively low, reflecting the commoditized nature of these offerings. Bank of China’s participation in these markets likely contributes to its overall portfolio, but these specific products may not be significant growth drivers.

- Low Profitability: Highly commoditized products often operate on thin margins, making it difficult to achieve substantial profitability.

- Limited Growth Potential: Without unique features or superior service, growth in these segments is typically slow and dependent on market expansion rather than market share gains.

- Intense Competition: The presence of many providers offering similar products intensifies price competition, further squeezing margins.

Financial Hurdles Facing the Banking Giant

Bank of China's legacy IT systems represent a significant cost burden, consuming substantial IT budgets for maintenance and modernization without generating direct revenue growth. These inflexible systems hinder the bank's ability to adapt to market changes, acting as a drag on strategic agility.

Non-performing loans, particularly those tied to distressed sectors like the Chinese property market, tie up valuable capital and demand considerable management resources, often yielding minimal returns. As of late 2023, asset quality remained a key concern for the Chinese banking sector.

Traditional, less urbanized branch networks are becoming costly, low-yield propositions due to declining foot traffic for routine transactions, as digital banking gains prominence. In 2024, the trend of reduced in-branch transactions for basic services continued, impacting branch profitability.

Highly commoditized financial products, such as basic savings accounts, offer little differentiation and generate low profit margins with minimal growth prospects. Intense competition in 2024, reflected in low savings account interest rates, further squeezes profitability in these segments.

| Area | BCG Category | Key Challenges | 2024 Data Point |

|---|---|---|---|

| Legacy IT Systems | Dog | High maintenance costs, inflexibility | Over 60% of IT spending on aging infrastructure (industry trend) |

| Non-Performing Loans (Distressed Sectors) | Dog | Tied-up capital, low returns | Ongoing asset quality concerns in Chinese banking sector (late 2023) |

| Underutilized Branch Networks | Dog | Declining transaction volume, high fixed costs | Continued trend of reduced in-branch transactions for basic services (2024) |

| Commoditized Basic Products | Dog | Low profit margins, intense competition | Low average savings account interest rates in China (2024) |

Question Marks

Emerging Fintech Solutions (Non-E-CNY)

While Bank of China demonstrates strength in E-CNY initiatives, other burgeoning fintech domains present significant growth opportunities. Emerging areas like blockchain-based trade finance platforms, which are moving beyond pilot stages, and sophisticated AI-driven financial advisory tools represent high-potential markets where BOC may still be establishing a dominant presence.

These innovative fintech sectors, crucial for future market share, necessitate substantial capital outlay to achieve widespread adoption and competitive positioning. For instance, the global fintech market was projected to reach over $300 billion by 2024, underscoring the scale of investment required to capture a meaningful share.

New Frontier Market Infrastructure Financing

Bank of China's focus on financing new frontier market infrastructure projects, often beyond the Belt and Road Initiative (BRI) or in higher-risk geographies, positions it for substantial growth. These ventures, while promising, demand significant capital outlay and may start with a modest market presence.

The bank's commitment to these ambitious undertakings, such as its participation in the development of renewable energy grids in parts of Africa or transportation networks in Central Asia, reflects a strategic push into untapped markets. For instance, in 2024, BOC's direct infrastructure financing in non-BRI emerging markets saw an estimated 15% increase year-on-year, highlighting this strategic direction.

Success in this "Question Mark" category of the BCG Matrix hinges on meticulous risk assessment and robust financial structuring. The potential for high returns is counterbalanced by the inherent volatility and developmental challenges of these frontier markets, requiring careful navigation.

Specialized Green Finance Instruments Beyond Core Lending

While green finance in general is a Star for Bank of China, some highly specialized instruments like certain blue bonds or emerging transition bonds are still in their early stages. These represent high-growth potential but currently have a small market share, demanding significant effort to gain traction. For instance, the global green bond market reached an estimated $1 trillion in 2023, with sustainable debt issuance projected to continue its upward trajectory, yet the specific niches of blue and transition finance are still carving out their space.

Personalized Digital Wealth Management Offerings

Personalized digital wealth management, powered by AI, is a burgeoning market. Bank of China's commitment to digital transformation positions it to compete, but capturing substantial share from nimble fintech rivals in this data-centric, high-growth area is a significant hurdle.

The global robo-advisory market, a key component of personalized digital wealth, was projected to reach over $3.4 trillion in assets under management by 2026, indicating robust growth. Bank of China faces the challenge of differentiating its advanced digital offerings in a crowded space.

- Market Growth: The demand for AI-driven, personalized wealth management solutions is expanding significantly, with projections indicating continued rapid expansion.

- Bank of China's Position: While investing in digital transformation, the bank is entering a competitive landscape dominated by specialized fintech companies.

- Strategic Challenge: Acquiring a dominant market share in these advanced, data-intensive digital offerings represents a high-growth, but currently low-share, segment for the bank.

Targeted Micro and Small Enterprise (MSE) Lending Expansion

Bank of China's expansion into targeted micro and small enterprise (MSE) lending aligns with its broader strategy of inclusive finance. The bank has seen significant growth in its MSE loan portfolio, reflecting this commitment. For instance, in 2023, Bank of China reported a substantial increase in its inclusive finance business, with loans to small and micro enterprises playing a key role.

This segment represents a high-growth opportunity, as there's a vast, often underserved, base of micro and small businesses that could benefit from tailored financial products. While BOC is actively pursuing this market, building a strong competitive advantage and capturing significant market share among these smaller enterprises is an ongoing effort, positioning it as a potential "question mark" in the BCG matrix.

- Growing MSE Loan Portfolio: Bank of China's commitment to inclusive finance is demonstrated by the continuous expansion of its micro and small enterprise loan offerings.

- High-Growth Potential Market: The underserved nature of many micro and small enterprises presents a significant opportunity for market penetration and growth.

- Building Competitive Advantage: While strategic focus is evident, solidifying BOC's competitive edge and market share within this diverse MSE segment is a key development area.

- Strategic Importance: This lending expansion is crucial for BOC's inclusive finance goals and reaching a broader customer base.

BOC: High Growth, Low Market Share

Bank of China's engagement in emerging fintech areas like blockchain-based trade finance and AI-driven financial advisory tools positions them as "Question Marks." These sectors exhibit high growth potential but currently represent nascent markets where BOC is still building its presence and market share.

The bank's strategic financing of new frontier market infrastructure, particularly in less-developed regions, also falls into this category. These ventures, while promising substantial future returns, require significant upfront investment and face inherent market volatility, indicating a low current market share despite high growth prospects.

Similarly, specialized green finance instruments, such as certain blue or transition bonds, are high-growth areas where BOC is actively participating but has not yet established a dominant market share. These niche markets require dedicated capital and strategic development to capture significant market penetration.

Bank of China's expansion into micro and small enterprise (MSE) lending is another "Question Mark." While this segment offers substantial growth due to a large, often underserved market, BOC is still in the process of building a strong competitive advantage and securing a significant market share among these smaller businesses.

| Business Area | Market Growth | BOC's Market Share | Strategic Implication |

|---|---|---|---|

| Blockchain Trade Finance | High | Low | Requires investment to gain traction. |

| AI-Driven Financial Advisory | High | Low | Faces competition from specialized fintechs. |

| Frontier Market Infrastructure Finance | High | Low | High potential, but volatile and capital-intensive. |

| Specialized Green Bonds (e.g., Blue Bonds) | High | Low | Niche markets needing strategic development. |

| Micro and Small Enterprise Lending | High | Low | Building competitive edge in an underserved market. |

BCG Matrix Data Sources

Our Bank of China BCG Matrix is informed by official financial statements, extensive market research, and analyses of global economic trends to provide a robust strategic overview.