Ahlers Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Ahlers

From Overview to Strategy Blueprint

Porter's Five Forces Analysis provides a powerful lens through which to examine the competitive landscape of Ahlers. Understanding the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the presence of substitutes is crucial for strategic planning. This framework highlights the external pressures that shape market profitability and influence Ahlers's business decisions.

The complete report reveals the real forces shaping Ahlers’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Fragmented Fabric and Component Suppliers

Ahlers AG, like many in the apparel industry, relies on a wide array of global suppliers for fabrics, trims, and other essential components. The broad availability of many standard inputs from a multitude of vendors significantly dilutes the bargaining power of any single supplier.

While certain highly specialized materials might grant a degree of leverage to their specific providers, the overall supplier landscape for Ahlers AG is characterized by fragmentation. This limits the ability of individual suppliers to dictate terms or significantly impact the company's costs.

Impact of Production Facilities

Ahlers' ownership of two production facilities, one in Poland and another in Sri Lanka, significantly curtails the bargaining power of external manufacturers. This vertical integration means Ahlers is not solely dependent on outside suppliers for its production needs.

By managing its own production, Ahlers gains greater control over critical aspects like product quality, the speed of delivery, and overall manufacturing costs. For instance, in 2023, Ahlers' in-house production likely contributed to its ability to maintain competitive pricing in a challenging global apparel market.

This internal capability acts as a strong counterweight against suppliers who might otherwise leverage their position to dictate terms. It allows Ahlers to respond more flexibly to market demands and mitigate potential disruptions from external manufacturing partners.

The strategic advantage of these facilities lies in their ability to ensure consistency and efficiency throughout the supply chain, directly impacting Ahlers' cost structure and ability to deliver value to its customers.

Logistics and Technology Providers

The fashion industry's dependency on smooth logistics and cutting-edge technology for managing supply chains and e-commerce operations means that providers of these services hold a degree of influence. Ahlers, like many in the sector, leverages a range of technology solutions to maintain efficiency.

While specific, highly specialized software providers might exert moderate bargaining power due to unique capabilities, the broader market for logistics and general IT services remains competitive. This competition generally limits the overall bargaining power of these suppliers.

In 2024, the global logistics market was valued at approximately $11.5 trillion, demonstrating its significant scale. Furthermore, the fashion industry's increasing emphasis on sustainability also plays a role in shaping supplier relationships, as companies like Ahlers often prioritize partners who align with their environmental and social governance goals, thereby influencing supplier selection and negotiation leverage.

Sustainability and Ethical Sourcing Demands

Growing consumer and regulatory pressures for sustainable and ethically sourced products are significantly influencing the bargaining power of suppliers. Companies like Ahlers, which are increasingly prioritizing these standards, find that suppliers meeting stringent environmental and social criteria can command higher prices or offer fewer alternatives. This shift means that suppliers with robust sustainability credentials gain leverage, as their offerings become more critical for companies aiming to maintain brand reputation and comply with evolving regulations.

Ahlers' own sustainability reports highlight a commitment to responsible sourcing, suggesting a strategic focus on suppliers who align with these values. This focus can translate into increased costs if these specialized suppliers are scarce or have higher operating expenses due to their ethical practices. For instance, in 2024, the global market for sustainable fashion, a key area for apparel companies like Ahlers, was projected to reach over $9 billion, indicating a substantial demand for ethically produced goods but also a potential concentration of power among compliant suppliers.

- Increased Supplier Leverage: Suppliers adhering to strict environmental and social standards gain greater bargaining power.

- Cost Implications: Meeting these demands can lead to higher raw material or production costs for Ahlers.

- Limited Supplier Pool: The availability of suppliers meeting advanced sustainability criteria may be restricted, reducing sourcing options.

- Strategic Sourcing: Ahlers' commitment to sustainability necessitates prioritizing suppliers with proven ethical and environmental track records.

Licensing Agreements

Licensing agreements, such as those Ahlers holds for brands like Pierre Cardin, can be a double-edged sword. While these licenses grant Ahlers access to valuable brand recognition, the licensors possess significant bargaining power. They can dictate terms related to brand usage, design conformity, and royalty percentages, directly impacting Ahlers' costs and creative freedom.

However, Ahlers' substantial scale as a major licensee can offer a degree of leverage, potentially moderating the licensors' absolute power. This symbiotic relationship is delicate, and shifts in market dynamics or brand popularity can influence the bargaining positions of both parties.

Recent antitrust actions, such as the €22 million fine imposed on a major fashion group in 2024 for anti-competitive licensing practices, underscore the regulatory scrutiny and potential for costly disputes within these arrangements. These fines highlight the critical need for transparency and fair dealing in licensing negotiations.

The bargaining power of suppliers through licensing agreements for Ahlers is therefore influenced by:

- Brand Equity: The strength and appeal of the licensed brand directly correlate to the licensor's leverage.

- Ahlers' Market Position: Ahlers' status as a significant licensee can counterbalance licensor demands.

- Contractual Terms: Royalty rates, exclusivity clauses, and design approval rights are key negotiation points.

- Regulatory Environment: Antitrust concerns and compliance requirements shape the negotiation landscape.

Ahlers' Supplier Power: Fragmentation, Integration, and Sustainability

Ahlers AG benefits from a fragmented supplier base for many standard materials, limiting individual supplier leverage. However, the increasing focus on sustainability by 2024 has empowered suppliers with strong environmental and social credentials, potentially increasing costs for Ahlers due to higher demand and fewer compliant options. For example, the global sustainable fashion market was projected to exceed $9 billion in 2024.

Ahlers' ownership of production facilities in Poland and Sri Lanka significantly reduces reliance on external manufacturers, thereby curbing their bargaining power. This vertical integration provides greater control over quality, delivery, and costs, a strategic advantage noted in its competitive pricing in 2023.

While technology and logistics providers hold some influence, the competitive nature of these markets generally limits their overall bargaining power. The global logistics market's substantial valuation of around $11.5 trillion in 2024 highlights its importance, but also the availability of numerous service providers.

Licensing agreements present a mixed bag, with licensors like those for Pierre Cardin holding significant power over brand usage and royalties. Ahlers' scale as a licensee can moderate this, but regulatory actions, such as a €22 million fine in 2024 for anti-competitive practices in licensing, emphasize the need for fair negotiations.

| Factor | Impact on Ahlers' Supplier Bargaining Power | Key Considerations |

| Supplier Fragmentation (Standard Inputs) | Low | Broad availability of materials limits individual supplier leverage. |

| Sustainability Focus (2024) | Increasing for compliant suppliers | Suppliers with strong ESG credentials gain power; potential for higher costs for Ahlers. |

| Vertical Integration (Production) | Reduces supplier power | Internal production facilities decrease dependency on external manufacturers. |

| Technology & Logistics Providers | Moderate | Competitive market limits overall leverage, despite industry scale. |

| Licensing Agreements | High (for licensors) | Brand equity and contractual terms grant licensors significant power; regulatory scrutiny is a factor. |

What is included in the product

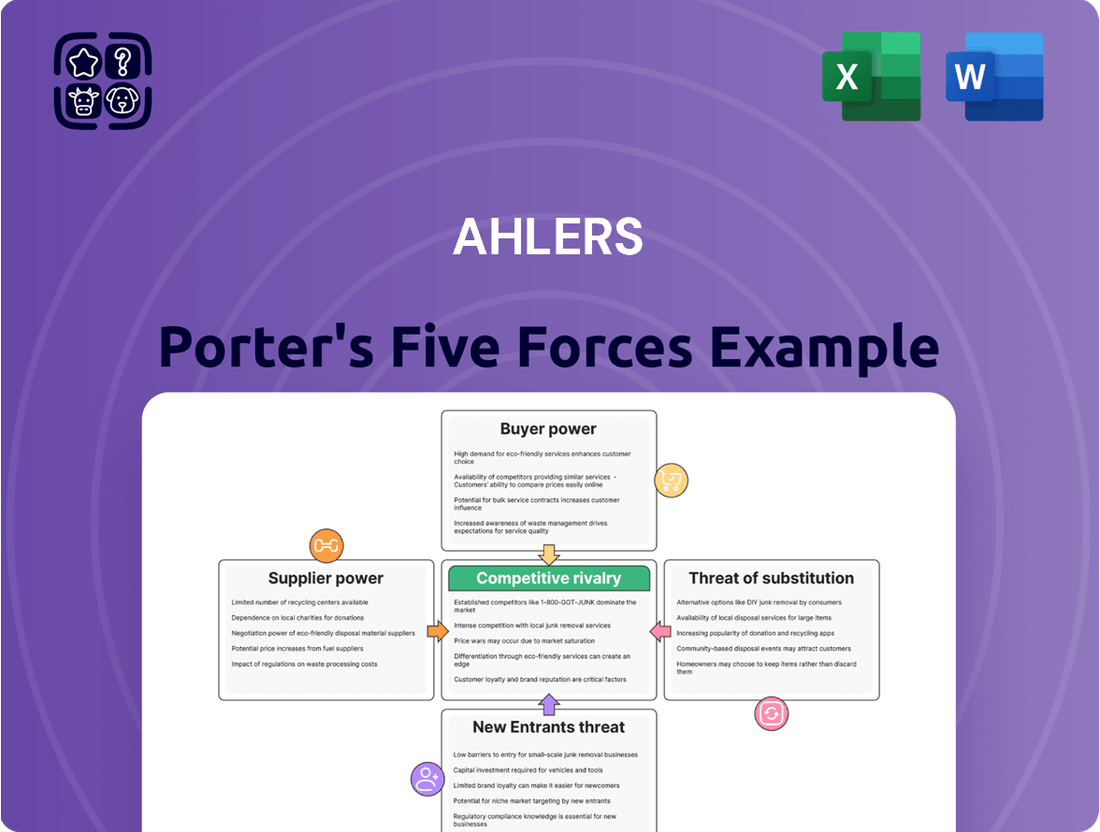

Ahlers' Five Forces Analysis unpacks the competitive intensity and profitability potential of its operating environment by examining industry rivals, potential new entrants, buyer and supplier power, and the threat of substitutes.

Instantly identify and address competitive threats with a comprehensive overview of all five forces, streamlining strategic planning.

Customers Bargaining Power

Diverse Customer Base

Ahlers benefits from a broad customer spectrum, encompassing wholesale partners like retailers and direct consumers via its own stores and online platforms. This wide reach naturally moderates the influence of any single customer segment, as sales volume isn't concentrated. For instance, in 2023, Ahlers reported that its wholesale business represented a significant portion of its revenue, underscoring the importance of these relationships while also highlighting their potential leverage.

Price Sensitivity in Fashion

In the menswear market, particularly for casual and business wear, consumers often exhibit significant price sensitivity. This is especially true for items that aren't positioned as premium luxury goods. For instance, a 2024 report indicated that over 60% of consumers consider price a primary factor when purchasing apparel, even impacting brand loyalty.

The fashion industry is characterized by a vast array of brands and retailers, both in brick-and-mortar stores and online. This abundance makes it incredibly simple for customers to compare prices across different options. In 2024, online price comparison tools and marketplaces saw a 15% increase in usage for apparel purchases, directly amplifying consumer bargaining power.

This heightened price sensitivity and ease of comparison necessitate that companies like Ahlers maintain competitive pricing strategies. However, the challenge lies in balancing this with the need to preserve brand value and perceived quality. Failing to do so can erode market share, as consumers readily switch to more affordable alternatives.

E-commerce and Information Availability

The proliferation of e-commerce has dramatically shifted the landscape for consumers, granting them unprecedented access to product details, customer reviews, and cross-platform price comparisons. This heightened transparency directly fuels their bargaining power, forcing companies like Ahlers to remain highly competitive on pricing, invest in smooth online functionalities, and prioritize excellent customer support. For instance, in 2024, online sales in Germany for apparel and footwear continued their upward trajectory, with projections indicating a substantial portion of the total market, underscoring the critical need for Ahlers to maintain a strong digital presence and customer-centric approach.

Brand Loyalty and Differentiation

Ahlers operates with a portfolio of distinct brands such as Baldessarini, Otto Kern, and PIONEER, each targeting specific consumer segments within the fashion industry. For brands like Baldessarini, which often sits in a more premium space, fostering strong customer loyalty can significantly diminish the power customers wield. In 2024, the fashion retail landscape remains intensely competitive, meaning Ahlers must continually invest in innovation, maintain high product quality, and craft compelling brand stories to sustain this crucial loyalty.

Customer bargaining power is also influenced by the availability of substitutes and the switching costs associated with changing brands. In the fast-paced fashion sector, where trends evolve rapidly, customers can easily shift to competitors if they perceive better value or style elsewhere. This dynamic means that even with established brands, Ahlers faces constant pressure to differentiate and offer compelling reasons for customers to remain loyal, impacting pricing strategies and profitability.

- Brand Portfolio: Ahlers manages brands like Baldessarini, Otto Kern, and PIONEER, serving diverse market segments.

- Loyalty as a Shield: Strong brand loyalty for premium offerings can directly counter customer bargaining power.

- Competitive Pressures: The fashion market demands continuous innovation and quality to maintain customer allegiance.

- Switching Costs: Low switching costs in fashion empower customers to easily opt for alternative brands, increasing their leverage.

Impact of Economic Conditions

Broader economic conditions significantly impact consumer purchasing power, directly affecting the bargaining power of customers. Ahlers' Q1 2023/24 financial results highlighted consumer caution and high retail inventories, signaling a shift where customers are more discerning with their spending. This cautious sentiment means customers can exert greater pressure on fashion companies for better pricing or terms.

During times of economic uncertainty, consumers tend to postpone non-essential purchases. They also actively seek out more budget-friendly options. This collective behavior amplifies their bargaining power, as companies must compete more aggressively to capture sales. For instance, if inflation remains elevated, as seen in many economies throughout 2024, consumers' reduced real incomes will force them to prioritize essential goods over discretionary fashion items, thereby strengthening their negotiating position.

- Consumer Caution: Increased economic uncertainty leads consumers to delay discretionary spending, enhancing their bargaining leverage.

- Inventory Levels: High retail inventories, as noted by Ahlers, give customers more options and reduce their urgency to buy, increasing their power.

- Price Sensitivity: In a challenging economic climate, consumers become more price-sensitive, demanding better value and potentially forcing price concessions from brands.

- Shift to Value: The preference for affordable alternatives during economic downturns allows customers to collectively negotiate better terms or switch to competitors offering lower prices.

Customer Power: Price Dominates Fashion Choices

The bargaining power of customers is a significant force, especially in the fashion industry where choices abound. In 2024, consumer behavior clearly shows a heightened emphasis on price, with a substantial majority prioritizing cost in their purchasing decisions. This trend is amplified by the ease of online comparison shopping, which grants customers considerable leverage.

For Ahlers, managing a diverse brand portfolio means that while premium brands like Baldessarini can foster loyalty to offset this power, the overall market remains competitive. Low switching costs mean customers can easily move to alternatives if value propositions aren't met. Economic headwinds in 2023/24 further emboldened consumers, making them more cautious and demanding of better pricing, directly impacting how companies like Ahlers must strategize.

| Factor | Impact on Ahlers | Supporting Data (2024 unless noted) |

| Price Sensitivity | Customers demand competitive pricing. | Over 60% of consumers cite price as a primary purchase factor. |

| Availability of Substitutes | Easy to switch to competitors. | 15% increase in usage of online apparel price comparison tools. |

| Economic Conditions | Consumers are more cautious with spending. | Ahlers Q1 2023/24 results noted consumer caution and high inventories. |

| Brand Loyalty | Can mitigate customer power, especially for premium brands. | Ongoing investment in brand story and quality is crucial. |

Same Document Delivered

Ahlers Porter's Five Forces Analysis

The preview you see is the exact, professionally formatted Ahlers Porter's Five Forces Analysis document you will receive immediately after purchase. This comprehensive report details each of the five competitive forces impacting the industry, providing actionable insights for strategic decision-making. You'll gain a thorough understanding of buyer power, supplier power, the threat of new entrants, the threat of substitutes, and the intensity of rivalry. No surprises, no placeholders – just the complete analysis ready for your use.

Rivalry Among Competitors

Fragmented German Menswear Market

The German menswear market is notably fragmented, featuring a multitude of domestic and international brands vying for market share across business, casual, and formal wear categories. This intense competition, exacerbated by steady value growth observed in 2024, presents a significant challenge for Ahlers. Key competitors in this dynamic landscape include global giants like H&M and Adidas, alongside established German powerhouses such as Hugo Boss, all of whom command substantial presence and consumer loyalty.

Brand Portfolio and Market Positioning

Ahlers AG navigates competitive rivalry through its multifaceted brand portfolio, encompassing premium offerings like Baldessarini alongside more accessible lines such as Pioneer Jeans and Pionier Workwear. This strategic breadth allows Ahlers to engage with a wider customer base across various price points, but it also means the company contends with a diverse array of competitors tailored to each specific market segment.

The menswear sector, particularly in 2024, exhibits a pronounced polarization trend. Growth is notably strong at the super-premium end, where exclusivity and craftsmanship command higher prices, and also at the economy end, driven by value-conscious consumers. Ahlers must therefore maintain a sharp strategic focus to differentiate its brands effectively within these diverging market dynamics.

E-commerce and Retail Channel Competition

Competitive rivalry in the fashion sector, including for brands like Ahlers, is fierce across both traditional wholesale and retail avenues, with a rapidly expanding e-commerce landscape. Ahlers' strategic push into e-commerce aims to capture a larger share of this digital market, but this requires ongoing significant investment.

The online environment is particularly crowded, demanding continuous spending on digital marketing campaigns, optimizing website user experience, and bolstering logistics to ensure timely delivery. In 2024, the German menswear market continues to show strong consumer preference for online retail, which directly translates to heightened competition in the digital space for all players.

Differentiation and Innovation

Competitive rivalry in fashion, particularly menswear, intensifies through design, quality, brand perception, and a growing emphasis on sustainability and technological advancements. The menswear sector is witnessing a significant shift towards smart and sustainable features, fueling the expansion of techwear, which demands continuous innovation from brands like Ahlers.

To stand out, Ahlers must actively pursue innovation in its product designs, explore advanced fabric technologies, and refine its marketing strategies. This ensures differentiation against rivals who are also investing heavily in these areas. For instance, the global menswear market was valued at approximately USD 692.9 billion in 2023 and is projected to grow, highlighting the competitive landscape.

- Design Innovation: Ahlers needs to consistently introduce fresh and appealing designs that resonate with evolving consumer tastes.

- Fabric Technology: Incorporating advanced materials, such as those offering enhanced comfort, durability, or smart functionalities, can provide a competitive edge.

- Sustainability Focus: Demonstrating a commitment to eco-friendly practices and materials is increasingly crucial for brand differentiation and consumer loyalty.

- Digital Integration: Leveraging technology in product development, marketing, and customer engagement is key to staying relevant in the modern fashion market.

Industry Consolidation and Market Dynamics

The apparel retail sector is characterized by intense competitive rivalry, significantly influenced by ongoing industry consolidation. Ahlers AG's insolvency proceedings in April 2023, leading to the Röther Group acquiring several of its brands, exemplifies this trend. This strategic shift among key players reshapes market dynamics.

These consolidations necessitate continuous adaptation for companies like Ahlers to preserve market standing. Competitors are actively seeking to strengthen their positions through mergers, acquisitions, and brand portfolio management. For instance, in 2024, the German fashion market saw continued M&A activity as companies aimed to achieve economies of scale and broader market reach.

- Intense Competition: The market is crowded with numerous brands, both established and emerging, vying for consumer attention and loyalty.

- Consolidation Trends: Events like the Röther Group's acquisition of Ahlers' brands in 2023 demonstrate a clear move towards industry consolidation.

- Market Share Shifts: Such M&A activities can lead to significant changes in market share, forcing existing players to re-evaluate their strategies.

- Adaptability is Key: Companies must remain agile to respond to competitive pressures and evolving market conditions shaped by these consolidations.

German Menswear: Competition Heats Up, Consolidation Reshapes Market

The German menswear market is highly competitive, featuring numerous domestic and international brands. In 2024, this fragmentation intensified with strong growth at both the premium and economy ends, forcing companies like Ahlers to strategically differentiate their brands. Consolidation within the apparel sector, such as the Röther Group's acquisition of Ahlers' brands in 2023, further reshapes market dynamics, demanding continuous adaptation and strategic focus from all players.

SSubstitutes Threaten

Second-hand and Rental Markets

The burgeoning second-hand and rental markets pose a significant threat of substitution for new apparel sales. Consumers are increasingly embracing pre-owned fashion and rental services, driven by both environmental consciousness and a desire for cost savings. For instance, the global second-hand apparel market was projected to reach $350 billion by 2027, according to ThredUp's 2023 Resale Report, highlighting a substantial shift in consumer behavior. This trend directly impacts the demand for new garments across all market segments, offering a more budget-friendly or temporary fashion solution.

Casualization of Dress Codes

The growing casualization of dress codes presents a significant threat of substitutes for companies like Ahlers, whose portfolio includes traditional business and formal wear. This long-term trend sees consumers opting for more comfortable and versatile casual clothing, directly impacting the demand for suits, dress shirts, and ties. For instance, a 2024 survey indicated that over 70% of US office workers now have some form of casual dress code, a stark contrast to previous decades.

This shift encourages consumers to seek alternatives from a wider array of providers, including athleisure brands and direct-to-consumer casual wear companies, which may not have historically competed in the formal wear market. These substitutes offer perceived value through comfort and everyday usability, directly challenging the necessity of specialized formal attire. The market for casual apparel saw significant growth in 2023, with global sales reaching an estimated $1.7 trillion, underscoring the consumer preference shift.

Emergence of Athleisure and Hybrid Apparel

The rise of athleisure and hybrid apparel presents a significant threat of substitutes for traditional menswear. These categories blur the lines between athletic wear and everyday clothing, offering consumers comfortable yet stylish alternatives for casual occasions. For instance, the global athleisure market was valued at over $325 billion in 2023 and is projected to continue its strong growth trajectory.

Hybrid apparel, designed for versatility and functionality, can directly substitute conventional menswear items like suits or more formal casual wear. Consumers increasingly seek garments that transition seamlessly from active pursuits to social settings, prioritizing comfort and adaptability. This shift means Ahlers must consider how its product offerings align with these evolving consumer demands for multi-functional clothing.

Customization and DIY Fashion

Custom tailoring and do-it-yourself (DIY) fashion represent a significant threat of substitutes for ready-to-wear apparel. For consumers prioritizing unique styles or precise fits, these alternatives offer a compelling value proposition. This trend is particularly noticeable among younger demographics and those with specific fit requirements.

While not a direct competitor in terms of scale, the growing popularity of DIY fashion and bespoke tailoring can siphon demand from mass-produced garments. This is especially true for special occasion wear or items where personal expression is paramount. In 2024, the global custom clothing market was estimated to be worth billions, indicating a substantial segment of consumers willing to pay a premium for personalized items.

- Growing DIY Culture: Online tutorials and accessible sewing machines have lowered the barrier to entry for DIY fashion, empowering consumers to create their own garments.

- Personalization Demand: A rising consumer desire for unique, personalized items fuels the demand for custom tailoring, offering a distinct alternative to off-the-rack options.

- Niche Market Appeal: While a smaller segment, the custom and DIY market caters to specific needs, such as adaptive clothing or avant-garde styles, which mass-market brands may not address.

- Impact on Volume Sales: Increased adoption of these substitutes can lead to reduced sales volume for standardized, ready-to-wear clothing, particularly in higher-margin categories.

Non-Apparel Alternatives for Expression

The threat of substitutes for apparel as a primary means of self-expression is evolving. Consumers are increasingly channeling their desire for personal identity into other categories like high-tech gadgets, unique travel experiences, or specialized hobby equipment. For instance, spending on experiences, including travel and entertainment, saw robust growth in 2024, with global tourism revenue projected to reach $1.7 trillion by year-end, according to various market analyses. This diversion of discretionary income means less is available for new clothing purchases.

This trend poses an indirect but significant challenge to the apparel industry. While not a direct clothing replacement, these alternative spending avenues can siphon off consumer budgets that might otherwise be allocated to fashion. Consider the burgeoning market for wearable technology, which blends personal expression with functionality. The global market for smart wearables was estimated to exceed $100 billion in 2024, indicating a strong consumer appetite for tech-driven self-expression.

- Shifting Discretionary Spending: Consumers allocate more budget towards experiences and technology, impacting apparel demand.

- Growth in Tech Gadgets: Wearable technology and other gadgets offer alternative avenues for personal expression.

- Experience Economy: Increased spending on travel and entertainment diverts funds from traditional fashion purchases.

- Indirect Impact: While not direct substitutes, these alternatives reduce the overall pool of disposable income available for apparel.

Apparel's New Reality: Substitutes Reshape Consumer Choices

The threat of substitutes for traditional apparel is multifaceted, encompassing shifts in consumer behavior and the emergence of alternative spending categories. The growing popularity of the second-hand and rental markets directly offers consumers more affordable and sustainable fashion choices, impacting new garment sales. Furthermore, the increasing prevalence of casual dress codes and the rise of athleisure and hybrid apparel provide comfortable and versatile alternatives to formal or business wear, challenging established menswear categories.

Consumers are also diverting discretionary spending towards experiences and technology, such as travel and wearable gadgets, as new avenues for self-expression. This shift in consumer priorities means less disposable income is available for apparel purchases, posing an indirect but significant challenge to the industry. For instance, the global athleisure market's valuation exceeded $325 billion in 2023, and the custom clothing market is worth billions, demonstrating significant consumer interest in these alternative fashion and self-expression avenues.

| Substitute Category | 2023/2024 Market Data | Impact on Apparel |

|---|---|---|

| Second-hand Apparel | Projected $350 billion by 2027 (ThredUp 2023 Report) | Reduces demand for new garments, offers cost savings. |

| Casualization of Dress Codes | 70%+ US office workers have casual dress codes (2024 survey) | Decreases demand for formal and business wear. |

| Athleisure & Hybrid Apparel | Global market valued over $325 billion (2023) | Offers comfortable, versatile alternatives to traditional menswear. |

| Custom Tailoring & DIY Fashion | Global custom clothing market worth billions (2024 est.) | Siphons demand from ready-to-wear, caters to personalization. |

| Experiences & Technology | Global tourism revenue projected $1.7 trillion (2024 est.) | Diverts discretionary spending from apparel purchases. |

Entrants Threaten

Brand Building and Marketing Costs

Building a recognizable brand in the fashion industry, particularly for segments like Ahlers targets, demands considerable upfront capital for marketing and advertising. This investment is crucial for establishing consumer awareness and fostering loyalty, effectively raising the barrier for newcomers. For instance, in 2024, major fashion houses continued to allocate substantial portions of their revenue to brand promotion, with some reporting marketing budgets exceeding 15% of sales.

Access to Distribution Channels

Securing effective distribution channels presents a significant hurdle for new entrants. Whether it's forging wholesale partnerships with established retailers or developing a robust direct-to-consumer (DTC) e-commerce infrastructure, the path is often fraught with challenges. Ahlers, in contrast, leverages an extensive international sales and distribution network, currently operating in approximately 20 countries, which significantly lowers this barrier to entry for them.

Capital Requirements for Production and Inventory

Ahlers Porter's need for substantial capital to establish and maintain its physical retail footprint and manage a broad inventory across various brands presents a significant barrier for new entrants. While digital-first strategies can lower initial costs, the operational complexities of a multi-brand, multi-location brick-and-mortar presence demand considerable financial resources. For instance, setting up just one new retail store can easily cost hundreds of thousands of dollars in leasehold improvements, fixtures, and initial stock. Newcomers must therefore secure substantial funding not only for production but also for the ongoing management of working capital, which includes inventory holding costs and supply chain logistics, often running into millions for a company of Ahlers' scale.

Economies of Scale and Experience

Established players like Ahlers Porter often enjoy significant economies of scale. This means they can produce and distribute goods at a lower cost per unit compared to newcomers. For instance, in 2024, major apparel manufacturers reported average production costs that were 15-20% lower for volumes exceeding one million units, a threshold difficult for new entrants to reach quickly.

This cost advantage makes it challenging for new entrants to compete on price. Without the same scale, new businesses may have to accept lower profit margins or charge higher prices, deterring customers. Furthermore, the ability to invest in research and development is often tied to financial capacity, which is amplified by scale.

- Cost Efficiency: Ahlers Porter's scale allows for reduced per-unit costs in sourcing raw materials and manufacturing.

- Market Penetration: Higher volumes enable more aggressive pricing strategies, making it difficult for new entrants to gain market share.

- Innovation Investment: Larger companies can allocate more resources to R&D, creating a technological or product innovation barrier.

- Distribution Networks: Established firms have developed efficient and cost-effective distribution channels that are expensive to replicate.

Regulatory and Compliance Hurdles

The fashion industry faces significant regulatory and compliance challenges that act as a barrier to new entrants. These regulations span product safety, ethical labor practices, and a growing emphasis on environmental sustainability. For instance, Ahlers, a prominent player, faced considerable antitrust fines in 2024, underscoring the intricate nature of adhering to these evolving legal frameworks.

New businesses entering the fashion market must meticulously navigate these complex regulatory landscapes. This compliance process inevitably increases both the cost and the operational complexity associated with establishing a presence.

- Product Safety Standards: Regulations ensuring materials and manufacturing processes do not pose health risks to consumers.

- Labor Practice Laws: Compliance with minimum wage, working conditions, and anti-child labor laws throughout the supply chain.

- Sustainability Directives: Adherence to environmental regulations concerning waste management, chemical usage, and carbon emissions.

- Antitrust and Fair Competition: Avoiding monopolistic practices and ensuring fair pricing, as highlighted by recent fines.

Capital Demands Block New Fashion Brands

The threat of new entrants for Ahlers Porter is moderate, primarily due to significant capital requirements for branding, distribution, and retail presence. Established brand recognition and extensive distribution networks represent substantial barriers. For example, in 2024, the cost of launching a new fashion brand with a comparable market reach to Ahlers could easily run into tens of millions of dollars, encompassing marketing, inventory, and supply chain setup.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a robust foundation of data, incorporating financial statements, investor presentations, and industry-specific market research reports to accurately assess competitive pressures.