Works Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Works

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Porter's Five Forces analysis offers a powerful lens to understand the competitive landscape for Works. It meticulously dissects the bargaining power of buyers and suppliers, the threat of new entrants and substitute products, and the intensity of rivalry within the industry. This framework helps to identify the key forces shaping Works's profitability and market position. By understanding these dynamics, businesses can develop more effective strategies to navigate and thrive.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Works’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse Product Categories

The Works sources a broad spectrum of products, encompassing books, stationery, arts and crafts, toys, and gifts. This wide variety necessitates engagement with a multitude of suppliers across diverse sectors, inherently diluting the bargaining power of any individual supplier.

While this diversification generally weakens supplier leverage, the situation can be nuanced. For instance, in 2024, the book retail sector saw continued dominance from major publishers, meaning that for certain popular book titles or exclusive editions, publishers could still exert significant influence over terms and pricing for The Works.

Similarly, in the arts and crafts segment, specialized suppliers offering unique or high-demand materials might retain a degree of power, especially if those materials are critical to popular product lines or seasonal offerings. However, The Works' overall purchasing volume across its many categories likely mitigates this to a degree.

Volume Purchasing Leverage

As a discount retailer with a substantial physical store network and a strong online presence, The Works benefits from significant volume purchasing leverage. This scale allows them to negotiate more favorable terms and prices with their suppliers, which is crucial for maintaining their value-for-money proposition.

In 2023, UK retail sales volume increased by 1.9% year-on-year, indicating a generally robust consumer demand that larger retailers like The Works can tap into to amplify their purchasing power. This ability to buy in bulk directly impacts their cost of goods sold.

The Works' ability to commit to large order quantities gives them considerable sway. Suppliers, eager to secure these substantial orders, are often more willing to offer discounts or more flexible payment terms to maintain a relationship with such a significant client.

Supplier Concentration and Specialization

The Works faces potential supplier power where its product sourcing is concentrated. For instance, if a significant portion of its arts and crafts inventory comes from a few specialized manufacturers, those suppliers could dictate terms. In 2024, the global arts and crafts market was valued at approximately $40 billion, indicating substantial demand for these products, which can embolden key suppliers.

Similarly, popular branded toys often have limited distribution channels. If The Works relies heavily on a few suppliers for high-demand toy lines, these suppliers can leverage their exclusivity to negotiate better pricing and delivery schedules, impacting The Works' margins.

Impact of Raw Material Costs and Supply Chain Issues

The bargaining power of suppliers for The Works is significantly influenced by the volatility of raw material costs and the complexities of global supply chains. For instance, in 2024, the price of paper pulp, a key input for The Works' products, saw notable increases due to reduced production in some regions and sustained demand. This upward pressure on input costs forces suppliers to seek higher prices, directly impacting The Works' profitability.

Global supply chain disruptions, such as the ongoing challenges in international shipping and logistics experienced throughout 2024, further embolden suppliers. Increased freight costs and lead times mean suppliers incur higher operational expenses, which they are likely to pass on. This situation forces The Works to make difficult decisions regarding absorbing these increased costs, potentially squeezing margins, or passing them to customers, which could affect sales volume.

- Increased Raw Material Costs: The price of paper, a primary input for The Works, experienced an average increase of 8-12% in early to mid-2024 compared to the previous year.

- Supply Chain Disruptions: Freight costs for ocean shipping rose by an average of 15% in the first half of 2024, impacting import expenses for many retailers.

- Supplier Pricing Power: These elevated costs empower suppliers to negotiate higher prices, potentially reducing The Works' gross profit margins if these increases cannot be fully passed on to consumers.

- Impact on Profitability: Failure to effectively manage these supplier-driven cost increases could lead to a direct reduction in The Works' net income for the 2024 fiscal year.

Switching Costs for The Works

The cost and effort a company like The Works incurs when changing suppliers significantly impacts supplier power. If The Works has developed deep integrations or relies on suppliers for highly specialized products, switching could involve substantial financial outlay and operational disruption. While The Works likely seeks competitive pricing from all its suppliers, the presence of these switching costs grants incumbent suppliers a leverage point.

For instance, if a supplier provides a unique component essential to The Works' product offering, or if the company has invested in specialized training for its staff to work with a particular supplier's system, these factors increase switching costs. This can give that supplier more bargaining power in price negotiations or contract renewals. The Works' recent appointment of a new third-party online fulfillment provider, announced in early 2024, suggests a strategic move to potentially reduce reliance on certain existing supply chain relationships or to gain greater flexibility, which could indirectly influence supplier negotiations by demonstrating a willingness and capability to change partners.

- Switching Costs: The expense and complexity of moving from one supplier to another.

- Bespoke Products: If suppliers provide unique or customized items, switching becomes more difficult and costly.

- Integrated Systems: Supply chain systems deeply intertwined with a specific supplier's technology can create high switching barriers.

- New Fulfillment Partner: The 2024 appointment of a new online fulfillment provider indicates The Works' proactive approach to supply chain optimization, potentially mitigating some supplier leverage by increasing operational agility.

Supplier Power Dynamics: Navigating Influence and Costs

The bargaining power of suppliers for The Works is generally moderated by the company's scale and diversified sourcing strategy. However, specific product categories and market conditions can empower certain suppliers. For example, in 2024, the book publishing industry continued to see concentrated power among major houses, allowing them to influence terms for popular titles. Similarly, specialized suppliers in the arts and crafts sector, offering unique or in-demand materials, can retain leverage, especially when these items are critical for The Works' popular product lines.

The Works' substantial purchasing volume, amplified by its broad retail presence, grants it considerable negotiation power. This scale allows for favorable pricing and terms, a key element of its discount retail model. In 2023, UK retail sales volume saw a 1.9% year-on-year increase, reflecting a market where large buyers like The Works can leverage demand to their advantage.

The bargaining power of suppliers is also shaped by factors like raw material costs and supply chain complexities. In 2024, increased prices for paper pulp, a key input for The Works, and rising global freight costs, averaging a 15% increase for ocean shipping in early 2024, have empowered suppliers to seek higher prices, potentially impacting The Works' margins.

Switching costs can also empower suppliers if The Works relies on specialized or bespoke products. The company's 2024 appointment of a new online fulfillment provider suggests a strategy to enhance supply chain flexibility, which could indirectly influence supplier negotiations by reducing dependence on specific partners.

What is included in the product

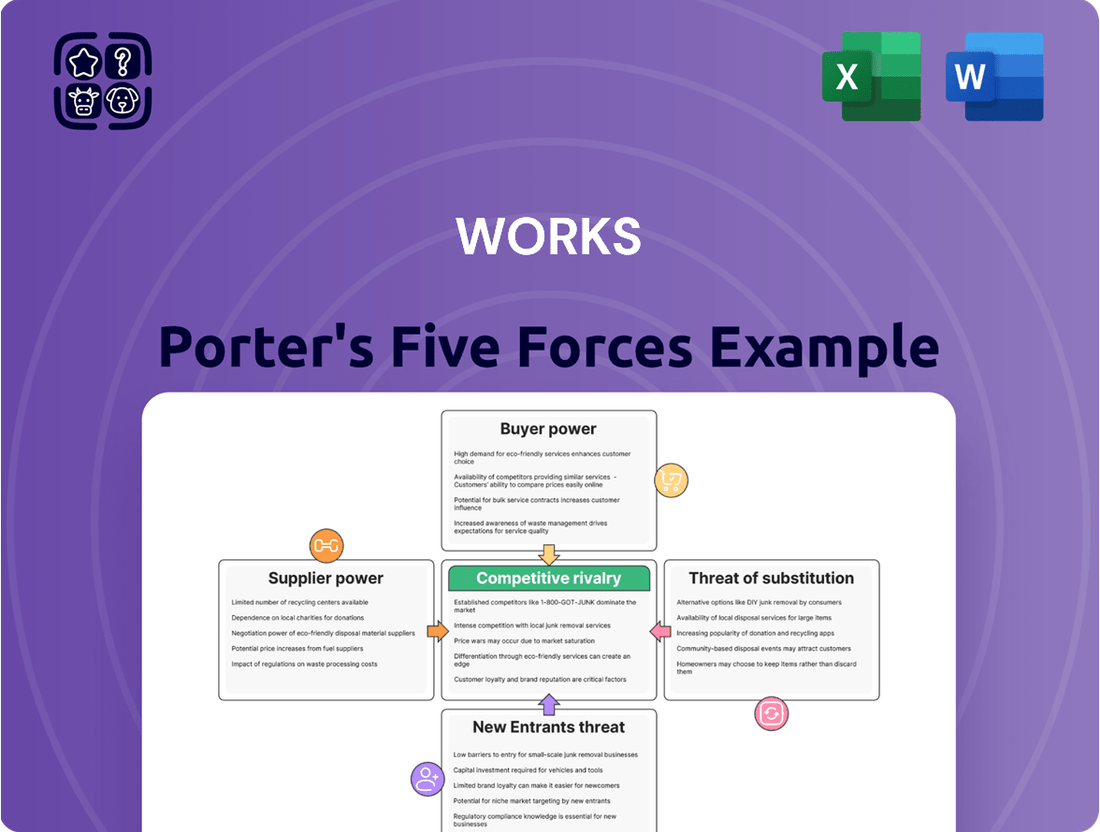

This analysis details the five competitive forces impacting Works, revealing industry attractiveness and strategic opportunities.

Visually pinpoint competitive threats and opportunities with an intuitive spider chart, clarifying strategic pressure points at a glance.

Customers Bargaining Power

Price Sensitivity of Target Market

The Works' customer base is inherently price-sensitive, drawn to its value-for-money offerings. This means customers wield considerable power, actively comparing prices and opting for the cheapest alternatives available. For instance, in 2024, the average UK consumer continued to prioritize affordability, with retail price inflation remaining a significant factor in purchasing decisions.

Given this high price sensitivity, customers can easily switch to competitors if The Works fails to meet their price expectations. This pressure forces The Works to maintain competitive pricing, directly impacting its profit margins and strategic flexibility.

Low Switching Costs for Consumers

Customers have very little reason to stay with one retailer for books, stationery, arts and crafts, or toys. The ease with which they can find comparable or even better deals elsewhere means The Works must constantly work to keep them. This low switching cost is a significant factor influencing customer power.

With so many options available, both online giants and local shops, consumers can easily shift their spending. If The Works’ prices are too high or their selection isn't quite right, a customer can be in a competitor's store or website within moments. This constant threat of customer defection is a key aspect of their bargaining power.

For example, in the UK retail sector, online sales reached an estimated £82.5 billion in 2024, highlighting the vast digital marketplace consumers can access. This massive online presence means consumers can compare prices and product ranges across numerous retailers for items like those The Works sells, significantly strengthening their position.

Availability of Information and Online Comparison

The Works' customers benefit greatly from the widespread availability of information online. This easy access allows them to compare product details and prices across various retailers, including The Works' own robust online platform and other e-commerce sites.

This transparency significantly boosts customer bargaining power. For instance, in the book retail sector, a 2024 study by Statista indicated that 75% of consumers compare prices online before making a purchase, directly impacting the pricing strategies of retailers like The Works.

Customers can readily identify the most competitive offers in the market. This means The Works must remain price-competitive to retain its customer base, as switching costs for many products are relatively low.

Diverse Product Offering and Broad Appeal

The Works’ extensive product assortment, encompassing everything from crafting and stationery to books and toys, attracts a wide demographic. This broad appeal necessitates consistent performance in both product quality and pricing to cultivate customer loyalty across these varied segments.

This wide reach means customers have numerous alternatives if their expectations aren't met, increasing their bargaining power. For instance, in the UK market, the price sensitivity of consumers remains a key factor; a 2024 report indicated that over 60% of shoppers prioritize value for money when making purchasing decisions.

- Diverse Appeal: The Works caters to hobbyists, students, families, and gift-givers, creating a broad customer base.

- Price Sensitivity: In 2024, UK consumer surveys highlighted that a significant majority of shoppers actively seek out deals and compare prices.

- Expectation Management: Meeting varied demands for quality and price across such a diverse product range is crucial for customer retention.

- Competitive Landscape: The breadth of The Works' offering also means it competes with a wide array of specialized and general retailers, further empowering customers.

Influence of Online Retail on Customer Expectations

The rapid expansion of e-commerce has significantly amplified customer expectations. Shoppers now demand unparalleled convenience, instant product availability, and consistently competitive pricing, directly impacting the bargaining power of customers. Works' own online presence, while essential for reaching modern consumers, simultaneously exposes the company to a wider array of competitors in the digital marketplace, necessitating ongoing strategic adjustments to satisfy and attract digitally adept clientele.

This shift means that customers, armed with easy access to price comparisons and product reviews, can exert considerable pressure on pricing and service levels. For Works, this translates to a constant need to innovate and differentiate. For instance, by mid-2024, the global e-commerce market size was projected to reach over $6.3 trillion, highlighting the sheer scale of online competition and the elevated standards customers now hold.

- Increased Price Sensitivity: Customers can readily compare prices across numerous online retailers, forcing companies like Works to offer competitive pricing strategies.

- Demand for Convenience: Online shopping has fostered an expectation of seamless purchasing processes, fast delivery, and easy returns, all of which add to customer leverage.

- Access to Information: Extensive online reviews and product information empower customers to make informed decisions, amplifying their ability to negotiate or switch to alternatives.

- Global Competition: Works' online platform opens it up to global competition, meaning customers have a vast selection of suppliers, further strengthening their bargaining position.

Customer Bargaining Power: A Retail Reality

The bargaining power of customers for The Works is significant due to several key factors. Their price sensitivity, amplified by readily available online comparisons, means they can easily switch to competitors if pricing or offerings aren't favorable. This forces The Works to maintain competitive pricing, directly impacting its profit margins.

The ease of switching retailers for products like books, stationery, and crafts is a major driver of customer power. With numerous online and physical alternatives, customers have little incentive to remain loyal if better deals are available elsewhere. For example, the UK retail landscape in 2024 saw continued consumer focus on value, with online sales contributing substantially to this competitive environment.

Access to information through the internet empowers customers to compare prices and product details extensively. A 2024 Statista report indicated that a large majority of consumers research prices online before purchasing, a trend that directly influences retailers like The Works to remain price-competitive and offer compelling value.

| Factor | Impact on The Works | 2024 Data Point |

|---|---|---|

| Price Sensitivity | Customers prioritize affordability, leading to pressure on The Works' pricing. | Over 60% of UK shoppers prioritize value for money. |

| Low Switching Costs | Customers can easily move to competitors, requiring The Works to offer continuous value. | Online sales in the UK reached an estimated £82.5 billion in 2024. |

| Information Accessibility | Customers compare prices and products online, strengthening their negotiation power. | 75% of consumers compare prices online before buying books. |

Full Version Awaits

Works Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The comprehensive analysis of the Works Porter's Five Forces is meticulously detailed, offering a deep dive into competitive rivalry, the threat of new entrants, the bargaining power of buyers, the bargaining power of suppliers, and the threat of substitute products. This complete, ready-to-use analysis file is professionally formatted and ready for your strategic decision-making needs.

Rivalry Among Competitors

Presence of Large Supermarket Chains

The Works contends with formidable rivalry from established supermarket giants like Tesco and Sainsbury's. These behemoths have expanded their product assortments to include books, stationery, and toys, directly challenging The Works' core offerings.

The competitive threat is amplified by the supermarkets' ability to leverage their extensive store networks and high customer traffic. For instance, in 2024, major UK supermarkets reported average weekly footfall figures well into the millions, a significant advantage over specialist retailers.

Furthermore, these large chains often possess greater purchasing power, enabling them to secure more favorable pricing and pass those savings onto consumers. This price competition makes it challenging for The Works to maintain its market share in these overlapping product categories.

Strong Competition from Online Giants

The competitive rivalry for The Works is intense, largely due to the formidable presence of online retail giants, most notably Amazon. Amazon's extensive product catalog, coupled with its consistently aggressive pricing strategies and highly efficient delivery network, poses a substantial challenge to The Works. This dominance directly impacts both The Works' online sales channels and its physical store performance, as consumers often find comparable or superior offerings at lower price points online.

In 2024, Amazon continued to solidify its market share across various segments relevant to The Works, including books, stationery, and toys. Reports indicate that online retail sales in the UK, particularly for these categories, saw continued growth, with Amazon being a primary beneficiary. For instance, UK consumers spent an estimated £70 billion on online retail in the first half of 2024, a significant portion of which flowed to major platforms like Amazon, highlighting the scale of the competitive pressure The Works faces.

Other Discount Retailers and Variety Stores

The UK discount retail landscape is intensely competitive, featuring strong players like B&M, Home Bargains, and Poundland. These rivals frequently offer very similar product assortments, intensifying direct price wars and a constant battle for market dominance.

In 2024, the discount store sector in the UK continued its robust growth. For instance, B&M European Value Retail S.A. reported a revenue of £2.4 billion for the third quarter of its fiscal year 2024, highlighting the significant market traction these discounters command.

This intense rivalry means that discounters must constantly innovate in sourcing and operations to maintain their low-price advantage. Their ability to pass on savings to consumers directly impacts customer loyalty and overall market share in this price-sensitive segment.

Specialist Retailers and Niche Players

The Works, while operating as a general discount retailer, faces competition from specialist and niche players within its core product categories. For instance, in the books segment, it directly contends with established chains like Waterstones, which often boast a more extensive selection and a focus on higher-quality editions. Similarly, dedicated art supply stores offer a depth of product and expertise that can attract customers prioritizing specialized needs and willing to invest more.

These specialist retailers can exert significant competitive pressure by offering a curated range, superior product knowledge, and a more tailored customer experience, which The Works, with its broader discount model, may not always match. For example, while The Works might carry a selection of popular craft kits, a dedicated craft store would likely offer a far wider array of individual components, specialist tools, and expert advice, catering to a more discerning hobbyist. This differentiation allows specialists to capture a segment of the market that values expertise and product breadth over sheer price point.

- Specialist Competition: The Works competes with specialized retailers in books (e.g., Waterstones) and art supplies, offering deeper ranges and higher quality.

- Customer Segmentation: Niche players appeal to customers willing to pay a premium for specialized products and expertise.

- Differentiation Impact: Specialists can attract customers seeking tailored experiences and a broader product assortment not typically found in general discount stores.

Intense Price Competition and Margin Pressure

The Works operates in a market segment where affordability is paramount, leading to fierce price competition. This constant battle for customer value puts significant pressure on profit margins.

To counteract these pressures, The Works must continually seek ways to enhance its product margins and reduce operational costs. Recent strategic actions have been taken to mitigate rising cost headwinds, demonstrating a proactive approach to maintaining profitability amidst a challenging competitive landscape.

- Intense Price Competition: The core of The Works' appeal is its low-price offering, directly placing it in a market segment where competitors frequently engage in price wars to attract value-conscious consumers.

- Margin Pressure: This aggressive pricing environment inherently squeezes profit margins, requiring efficient operations and cost management to remain viable.

- Strategic Cost Reduction: The company actively pursues strategies to offset rising costs, such as optimizing its supply chain or improving operational efficiencies, to protect its margins.

- Focus on Affordability: The Works' business model is built on providing accessible products, which means it must navigate the inherent challenges of low-margin retailing.

Specialty Retailer Faces Intense Supermarket Rivalry

The competitive rivalry for The Works is intense, primarily driven by large supermarket chains like Tesco and Sainsbury's. These giants, with their vast store networks and high customer traffic, directly challenge The Works by offering overlapping product categories such as books and stationery. In 2024, UK supermarkets reported millions in weekly footfall, a clear advantage. Their substantial purchasing power also allows for more aggressive pricing, making it difficult for The Works to compete on cost alone.

SSubstitutes Threaten

Digital Content and E-books

The proliferation of digital content, including e-books and audiobooks, presents a substantial threat to The Works' traditional print book sales. Consumers increasingly favor the convenience and accessibility of digital formats, often at competitive price points. For instance, the global e-book market was valued at approximately USD 17.9 billion in 2023 and is projected to grow, indicating a sustained shift in consumer preference. This trend could erode demand for physical books, impacting The Works' revenue streams.

Online Tutorials and DIY Content

The rise of free online tutorials and do-it-yourself (DIY) content significantly threatens the arts and crafts supply market. Platforms like YouTube and Pinterest offer an abundance of free guidance, enabling consumers to create projects using readily available materials instead of specialized kits. This trend means a crafter might bypass purchasing a specific embroidery kit by finding a free pattern and instructions online, sourcing floss and fabric separately. For instance, a 2024 survey indicated that over 70% of individuals interested in crafting turned to online video tutorials for inspiration and instruction, directly impacting the demand for curated craft kits.

Second-hand Markets and Resale Platforms

The proliferation of second-hand markets and resale platforms presents a significant threat of substitutes for The Works. Platforms like eBay, Vinted, and local Facebook marketplace groups allow consumers to purchase used books, toys, and craft supplies at considerably lower price points. This accessibility to pre-owned goods directly competes with The Works' core offerings, particularly for budget-conscious shoppers who prioritize value over newness.

General Merchandise Stores and Supermarket Offerings

Many general merchandise stores and supermarkets offer basic stationery, toy, and gift items. These can act as convenient substitutes for consumers who don't need the specialized, extensive range that The Works provides. While these outlets may lack the depth of inventory, they often compete effectively on accessibility and cost.

For instance, by mid-2024, major supermarket chains in the UK, like Tesco and Sainsbury's, reported significant growth in their non-food categories, including stationery and gifts, driven by customer convenience. This trend highlights the competitive pressure from these broad-line retailers.

- Convenience Factor: Consumers can bundle their grocery shopping with purchases of everyday items like pens, notebooks, and small gifts, reducing the need for separate trips.

- Price Competition: Supermarkets often leverage bulk purchasing power to offer competitive pricing on these substitute goods.

- Limited Specialization: While they offer substitutes, these retailers typically do not match the curated selection or specialized appeal of dedicated craft and hobby stores.

DIY and Homemade Alternatives for Gifts and Crafts

The threat of substitutes for gifts and crafts is significant as consumers increasingly turn to DIY and homemade alternatives. This trend allows individuals to create personalized or unique items, bypassing traditional retail channels. For instance, a 2024 survey indicated that over 60% of consumers reported making at least one handmade gift in the past year, a notable increase from previous years.

These homemade options can range from knitted scarves and baked goods to custom-designed artwork. The appeal lies in the sentimental value and the ability to tailor the product to the recipient's preferences, which mass-produced items often cannot replicate. This directly diverts potential sales from established gift and craft retailers.

- DIY Gift Market Growth: The global handmade gifts market was valued at approximately $25 billion in 2023 and is projected to grow, fueled by online platforms and social media trends showcasing DIY creations.

- Cost Savings for Consumers: Many consumers opt for DIY gifts to save money, especially during economic downturns. The average cost of a handmade gift can be 30-50% lower than a comparable retail item.

- Personalization Appeal: A key driver is personalization. Studies show that 75% of consumers are willing to pay more for personalized products, a need met effectively by the DIY sector.

- Shift from Traditional Retail: This shift impacts retailers specializing in gifts, stationery, and hobby supplies, forcing them to adapt by offering customization services or focusing on unique, hard-to-replicate items.

Consumer Shifts: The Rise of Digital, DIY, and Second-Hand

The threat of substitutes for The Works is multifaceted, encompassing digital media, DIY alternatives, and the second-hand market. Consumers are increasingly opting for digital books over physical copies, with the global e-book market valued at approximately USD 17.9 billion in 2023. Similarly, the DIY movement, fueled by free online tutorials, allows consumers to create crafts and gifts, with over 60% of consumers making handmade gifts in 2023. The resale market, featuring platforms like eBay and Vinted, offers pre-owned items at lower prices, directly competing with new product sales.

| Substitute Category | Key Driver | Impact on The Works | 2023/2024 Data Point |

|---|---|---|---|

| Digital Media (e-books, audiobooks) | Convenience, Accessibility, Price | Erodes demand for physical books | Global e-book market valued at USD 17.9 billion (2023) |

| DIY & Homemade Goods | Personalization, Cost Savings, Creativity | Reduces demand for craft kits and gift items | 60%+ consumers made handmade gifts (2023) |

| Second-Hand Market | Affordability, Value for Money | Competes directly with new product sales | Growth in resale platforms like Vinted and eBay |

| Broad-Line Retailers (Supermarkets) | Convenience, Price Competition | Offers basic substitutes for stationery and gifts | Supermarkets reported growth in non-food categories (mid-2024) |

Entrants Threaten

Low Barriers for Online-Only Retailers

The threat of new entrants in the online discount retail sector remains significant. Lower startup costs for e-commerce ventures, bypassing the substantial capital needed for brick-and-mortar stores, allow new players to emerge more readily. For instance, in 2024, the global e-commerce market continued its robust growth, with new online-only retailers frequently testing the waters with specialized product offerings or aggressive promotional tactics to gain initial traction.

High Capital Requirements for Physical Store Networks

Establishing a substantial physical store network, akin to The Works' more than 500 outlets, demands considerable capital for leases, inventory, and staffing. This high upfront investment creates a formidable barrier for potential new entrants seeking to match The Works' extensive brick-and-mortar footprint.

For instance, acquiring and outfitting even a single new store can easily run into hundreds of thousands of pounds, making it a significant hurdle for smaller players. The sheer scale of The Works' existing infrastructure means that replicating its reach would require millions in initial investment, deterring many from entering the market.

Established Supply Chains and Supplier Relationships

The Works benefits from deeply ingrained relationships with a wide array of suppliers, ensuring consistent product flow and favorable pricing. Newcomers would struggle to replicate these established connections, likely facing higher procurement costs and less advantageous payment terms in their initial stages. For example, the average lead time for importing goods can be significantly higher for new entrants without existing supplier trust.

Brand Recognition and Customer Loyalty

The Works, while known for its value proposition in creative and educational supplies, faces a significant hurdle for new entrants due to established brand recognition and customer loyalty. Building a similar level of trust in a competitive retail landscape requires substantial marketing expenditure and a considerable time investment. For instance, in 2024, major UK retailers continued to invest heavily in brand building, with the top 100 UK brands spending over £12 billion on advertising. Newcomers would need to surmount this existing brand equity to attract and retain customers.

New entrants must contend with the existing customer base that The Works has cultivated over time. This loyalty means potential competitors need to offer a compelling reason beyond just price to draw customers away. The challenge lies in replicating the perceived value and reliability that The Works offers its shoppers, a feat that historically takes years and consistent performance to achieve.

- Brand Equity: The Works benefits from years of operating as a go-to value retailer for families and hobbyists.

- Marketing Investment: New entrants would need to allocate significant funds to marketing campaigns to even begin matching The Works' visibility.

- Customer Trust: Loyalty is built on consistent product quality and service, which new entrants lack initially.

- Market Saturation: The UK retail sector, particularly for arts, crafts, and educational supplies, is already crowded with both online and brick-and-mortar players.

Market Saturation in Discount Retail

The UK discount retail sector is already a crowded space, making it tough for newcomers to carve out a significant presence. Established players are locked in a fierce competition for the same value-seeking shoppers.

This high level of competition means any new entrant would likely need to adopt aggressive pricing strategies or present a truly unique proposition to attract customers. Simply entering with a similar model to existing giants like Aldi and Lidl would be an uphill battle.

Consider the market share dynamics: Aldi and Lidl collectively held a record 16.7% of the UK grocery market share by early 2024, demonstrating the dominance of established discount retailers. This solidifies the difficulty for new entrants to disrupt the status quo.

- Highly Competitive Landscape: The UK discount grocery market is characterized by intense competition among established players, limiting opportunities for new entrants.

- Market Saturation: With major players already serving a large portion of the value-conscious consumer base, the market exhibits signs of saturation.

- Barriers to Entry: Significant capital investment for store rollouts and the need for efficient supply chains present considerable barriers for newcomers.

- Aggressive Pricing: Existing retailers often engage in price wars, making it challenging for new entrants to compete on price alone without substantial cost advantages.

Strong barriers protect established UK retailers from new competitors

The threat of new entrants for The Works is moderated by significant barriers. While online retail offers lower entry points, replicating the established physical store network, supplier relationships, brand equity, and customer loyalty of The Works requires substantial capital and time. The competitive UK discount retail market, already saturated with dominant players like Aldi and Lidl, further challenges newcomers.

For instance, by early 2024, Aldi and Lidl commanded a combined 16.7% of the UK grocery market share, illustrating the difficulty for new entrants to gain traction against such established giants.

The capital required to establish a comparable physical presence to The Works' over 500 stores, including inventory and staffing, easily runs into millions, posing a significant hurdle.

Furthermore, building brand recognition and customer trust in a market where major UK brands invested over £12 billion in advertising in 2024 necessitates considerable marketing expenditure for any new entrant to compete effectively.

| Barrier Type | Description | Impact on New Entrants | Example Data (2024) |

|---|---|---|---|

| Capital Requirements | Cost of establishing physical stores, inventory, and supply chains. | High; requires significant upfront investment. | Opening a single retail store can cost hundreds of thousands of pounds. |

| Brand Recognition & Loyalty | Established customer base and trust built over years. | Moderate to High; difficult to replicate quickly. | Top 100 UK brands spent over £12 billion on advertising. |

| Supplier Relationships | Existing contracts and preferential terms with suppliers. | Moderate; new entrants face higher procurement costs and longer lead times. | Average lead times for imported goods can be significantly higher for new entrants. |

| Market Saturation | Presence of dominant, established competitors. | High; limits market share opportunities. | Aldi and Lidl held 16.7% of UK grocery market share by early 2024. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis leverages proprietary market intelligence, company financial reports, and expert interviews to gain deep insights into industry structure and competitive dynamics.