Stone Canyon Industries LLC Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Stone Canyon Industries LLC

Go Beyond the Preview—Access the Full Strategic Report

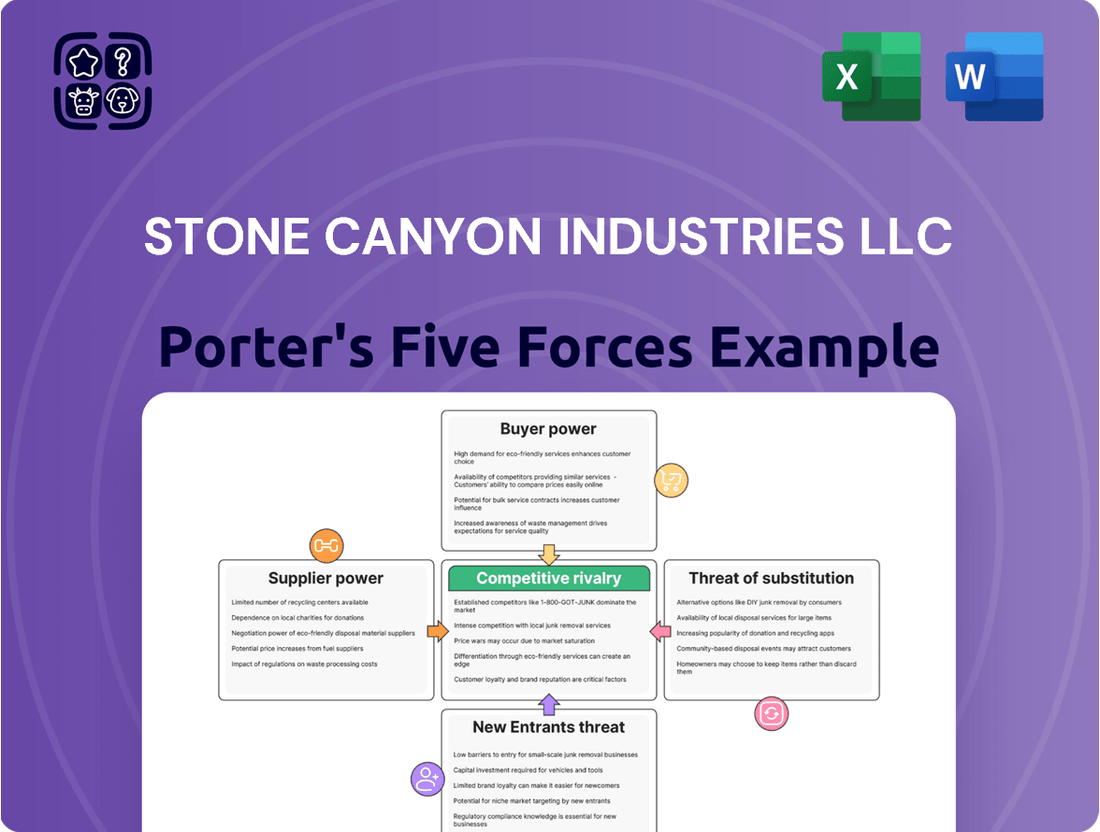

Stone Canyon Industries LLC operates in a dynamic environment shaped by powerful competitive forces. Understanding the intensity of rivalry, the bargaining power of buyers and suppliers, and the threats of new entrants and substitutes is crucial for strategic success.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stone Canyon Industries LLC’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Concentration and Specialization

Stone Canyon Industries LLC's diverse portfolio, encompassing industrial, transportation, and infrastructure sectors, frequently necessitates specialized raw materials and components. When these critical inputs are supplied by a concentrated group of vendors, particularly those offering proprietary technologies or unique materials, supplier bargaining power intensifies. This concentration can significantly impact the cost structure and supply chain resilience of SCI's operating subsidiaries.

For instance, in the industrial sector, a subsidiary requiring highly specialized alloys or precision-engineered parts might find itself dependent on only a few global manufacturers. If these suppliers face production constraints or decide to increase prices, SCI's subsidiaries could experience substantial cost overruns or disruptions. In 2024, the global supply chain continued to be impacted by geopolitical tensions and localized production challenges, further amplifying the bargaining power of specialized suppliers in key sectors.

Switching Costs for SCI's Portfolio Companies

The bargaining power of suppliers for Stone Canyon Industries LLC's (SCI) portfolio companies is directly influenced by the switching costs involved. High switching costs, often a result of proprietary technology integration or lengthy supply agreements, give suppliers a significant advantage. For instance, if a portfolio company relies on a specialized component that requires extensive retooling or re-certification to replace, the incumbent supplier holds considerable sway.

Conversely, when SCI's businesses can easily transition to alternative suppliers without incurring substantial costs, the bargaining power shifts. This is particularly true in industries with numerous providers of commoditized goods or services. In 2024, many sectors experienced supply chain disruptions, highlighting how critical it is for SCI to manage these relationships. Companies with flexible supply chains in 2024 were better positioned to negotiate pricing and terms, a trend that is likely to continue.

Uniqueness and Differentiation of Inputs

Suppliers gain leverage when their offerings are unique or difficult to replicate. For Stone Canyon Industries LLC (SCI), if a critical component for one of its manufacturing processes is only available from a single, specialized producer, that supplier commands significant power. This is particularly true in sectors like advanced materials or proprietary software essential for SCI's operations.

Threat of Supplier Forward Integration

The possibility of suppliers moving into Stone Canyon Industries LLC's (SCI) portfolio companies' markets, known as forward integration, significantly amplifies their bargaining power. This threat is particularly relevant if suppliers have the resources and expertise to directly serve industrial, transportation, or infrastructure sectors, potentially disrupting SCI's existing customer relationships and pricing structures.

For instance, a key component supplier for SCI's manufacturing subsidiaries might develop its own assembly operations. In 2024, the average cost of establishing a new manufacturing facility in the United States, including equipment and initial labor, can range from $5 million to $50 million, a significant investment that a well-capitalized supplier could undertake. This move would place SCI's companies in direct competition with their own suppliers, shifting the power dynamic.

- Increased Competition: Suppliers integrating forward can directly compete with SCI's portfolio companies, potentially leading to price wars and reduced profit margins.

- Supply Chain Disruption: A supplier's shift to direct competition could lead to a disruption in the availability or terms of essential raw materials or components for SCI's businesses.

- Reduced Negotiation Leverage: As suppliers become direct competitors, SCI's ability to negotiate favorable terms on purchased goods and services diminishes.

- Strategic Threat: The threat of forward integration forces SCI to consider its supplier relationships more strategically, potentially requiring diversification or vertical integration of its own.

Importance of SCI's Business to Suppliers

The extent to which Stone Canyon Industries LLC's (SCI) portfolio companies represent a significant portion of a supplier's revenue directly impacts that supplier's bargaining power. If SCI's individual businesses are substantial clients, suppliers are incentivized to offer more favorable pricing and flexible terms to secure and maintain that business. This reliance on SCI as a key customer can diminish the supplier's leverage in negotiations.

For example, in 2024, many industrial suppliers experienced fluctuating demand, making large, consistent customers like those within the SCI portfolio particularly valuable. A supplier whose revenue is heavily dependent on a SCI subsidiary might be less inclined to push for higher prices or less favorable payment terms, understanding that losing such a significant account could have a material impact on their own financial performance. Conversely, if SCI's businesses constitute only a small fraction of a supplier's overall sales, the supplier has less incentive to accommodate SCI's demands, leading to greater supplier bargaining power.

- Customer Concentration: Suppliers with a high concentration of revenue from SCI's portfolio companies face greater pressure to maintain competitive offerings.

- Supplier Dependence: Conversely, suppliers who do not rely heavily on SCI have more leverage in price and term negotiations.

- Market Dynamics in 2024: In 2024, supply chain stability was a critical factor, making consistent buyers like SCI important partners for many suppliers.

Supplier Bargaining Power and Buyer Influence in 2024

The bargaining power of suppliers for Stone Canyon Industries LLC (SCI) is significantly influenced by the availability of substitute inputs. When alternative materials or components exist that can fulfill a similar function, suppliers' leverage is diminished. SCI's ability to source from multiple providers or utilize different technologies reduces any single supplier's ability to dictate terms.

In 2024, the push for sustainable materials and circular economy principles led to increased development of substitutes across various industries. For SCI's transportation subsidiaries, for instance, the availability of alternative lightweight composites or recycled metal alloys presented opportunities to negotiate better pricing from traditional material suppliers. This broadens SCI's options and strengthens its position.

The collective bargaining power of buyers, in this case Stone Canyon Industries LLC's operating subsidiaries, can counteract supplier influence. When SCI's businesses can consolidate their purchasing power, they can negotiate more favorable terms and prices. This is especially true when SCI represents a substantial portion of a supplier's customer base.

For example, if multiple SCI subsidiaries require the same specialized industrial equipment, they can collectively negotiate bulk discounts. In 2024, the average discount achieved through large-volume purchasing agreements in the industrial sector often ranged from 5% to 15%, depending on the product and volume. This consolidated approach significantly bolsters SCI's negotiating stance against its suppliers.

The threat of suppliers entering Stone Canyon Industries LLC's (SCI) operating companies' markets, known as forward integration, is a critical factor. If suppliers possess the capability and resources to directly compete in SCI's industrial, transportation, or infrastructure sectors, their bargaining power increases substantially. This threat can force SCI to concede to supplier demands to avoid direct competition.

| Factor | Impact on SCI | 2024 Relevance |

|---|---|---|

| Availability of Substitutes | Reduces supplier power by offering alternatives. | Increased development of eco-friendly and recycled substitutes in 2024 provided more options. |

| Buyer Power (SCI) | Strengthens SCI's position through consolidated purchasing. | Bulk purchasing discounts in 2024 for industrial equipment averaged 5-15%. |

| Threat of Forward Integration | Increases supplier leverage if they can compete directly. | Well-capitalized suppliers in 2024 considered expanding into customer markets. |

What is included in the product

This Porter's Five Forces analysis for Stone Canyon Industries LLC meticulously examines the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within its operating industries.

Effortlessly identify and mitigate competitive threats with a dynamic Porter's Five Forces analysis, providing Stone Canyon Industries LLC with a clear roadmap to navigate market pressures.

Customers Bargaining Power

Customer Concentration and Volume

Customer concentration is a key factor in bargaining power. If Stone Canyon Industries LLC (SCI) has a few very large customers who buy a significant portion of its products, those customers can wield considerable influence. Imagine a scenario where one customer represents 20% or more of SCI's revenue; that customer could likely negotiate for lower prices or more favorable terms simply because their business is so important to SCI.

Conversely, a broad and diverse customer base generally means individual customers have less sway. In 2024, many diversified industrial suppliers found their power strengthened by serving thousands of smaller clients, making it difficult for any single client to demand special treatment or significant price reductions. This fragmentation dilutes the bargaining power of any one customer.

Customer Switching Costs

The costs customers incur when moving from Stone Canyon Industries LLC (SCI) to a competitor significantly shape their bargaining power. If these switching costs are low, meaning customers can easily switch providers without facing substantial financial penalties, learning curves, or integration challenges, their ability to negotiate better terms or demand greater value is amplified. For instance, in industries where SCI operates, such as industrial manufacturing or building materials, customers might easily compare prices and features, putting pressure on SCI to remain competitive. In 2024, the average cost for a business to switch ERP systems, a significant operational change, can range from tens of thousands to millions of dollars, highlighting how high switching costs can lock customers in.

Availability of Customer Substitutes

The availability of customer substitutes significantly impacts Stone Canyon Industries LLC (SCI). When customers have numerous readily available alternatives that offer comparable value or functionality, their ability to negotiate better terms increases, directly limiting SCI's pricing power. For instance, in the industrial manufacturing sector where SCI operates, the proliferation of global suppliers and the ease of sourcing components can empower buyers. In 2024, the average lead time for many industrial components saw a reduction, making it easier for customers to switch suppliers if pricing or terms are not met, further amplifying this bargaining power.

Customer Price Sensitivity

Customer price sensitivity is a significant lever for Stone Canyon Industries (SCI), particularly within its more commoditized industrial and transportation segments. When customers face their own cost pressures or perceive limited differentiation in SCI's products and services, their ability to negotiate for lower prices increases substantially. This heightened sensitivity directly translates into stronger downward pressure on SCI's pricing, which can erode profit margins.

For instance, in the trucking and logistics sector, where many carriers offer similar services, freight costs are a major concern for shippers. If SCI's industrial components or manufacturing services are viewed as easily substitutable, buyers will actively seek the lowest cost provider. This is evident in market analyses showing that in sectors with high supply and low switching costs, price becomes the dominant purchasing factor.

- Customer price sensitivity directly impacts SCI's pricing power, especially in commoditized markets.

- In 2024, many industrial sectors experienced heightened cost pressures, leading customers to scrutinize expenditures more closely.

- For example, the automotive manufacturing sector, a key client base for some industrial suppliers, faced ongoing supply chain challenges and inflationary pressures throughout 2024, making them more sensitive to the price of components.

- The perceived lack of unique value or differentiation in SCI's offerings amplifies this price sensitivity, encouraging customers to shop around for better deals.

Threat of Customer Backward Integration

The possibility of customers moving backward and making the products or services themselves directly enhances their negotiating leverage. This threat is particularly pronounced when customers perceive current supplier pricing or reliability as unsatisfactory.

For instance, a significant industrial buyer for one of Stone Canyon Industries LLC's portfolio companies might explore establishing its own production facilities or supply chain infrastructure if it feels the cost or dependability of its existing partners is insufficient. Such a move would significantly reduce their reliance on SCI's offerings.

- Increased Customer Leverage: When customers can credibly threaten to produce goods or services internally, their power to negotiate better terms with existing suppliers, like SCI's companies, grows.

- Cost and Reliability Drivers: High supplier costs or perceived unreliability are key motivators for customers to consider backward integration.

- Strategic Impact on SCI: If a major client of an SCI portfolio company were to integrate backward, it could lead to a substantial loss of revenue and market share for that specific business unit.

- Industry Examples: Major automotive manufacturers have historically integrated backward into component production to control costs and ensure supply, demonstrating this principle.

Customer Bargaining Power: Key Factors and 2024 Market Dynamics

The bargaining power of customers for Stone Canyon Industries LLC (SCI) is shaped by several critical factors. A concentrated customer base, where a few large buyers account for a significant portion of revenue, grants those customers greater leverage to negotiate favorable terms. Conversely, a fragmented customer base dilutes individual customer power.

High switching costs effectively lock customers in, reducing their bargaining power. Conversely, low switching costs empower customers to demand better prices or service. The availability of substitutes also empowers customers; if many alternatives exist, customers can easily shift their business, forcing SCI to compete more aggressively on price and value.

Price sensitivity is a major driver of customer bargaining power, especially in commoditized markets where SCI's offerings may be perceived as undifferentiated. When customers face their own cost pressures, they are more likely to push for lower prices from their suppliers, impacting SCI's profitability. The threat of backward integration, where customers produce their own goods or services, also significantly increases their leverage.

| Factor | Impact on SCI's Customer Bargaining Power | 2024 Market Context |

|---|---|---|

| Customer Concentration | High concentration = High Power | Many industrial sectors saw consolidation in 2024, potentially increasing the concentration of SCI's key clients. |

| Switching Costs | Low costs = High Power | The average cost for businesses to switch major software systems in 2024 could reach hundreds of thousands to millions, but for many industrial components, switching remains relatively low. |

| Availability of Substitutes | More substitutes = High Power | Reduced lead times for industrial components in 2024 made sourcing from alternative suppliers easier for buyers. |

| Price Sensitivity | High sensitivity = High Power | Inflationary pressures in 2024 made many industrial customers, like those in automotive manufacturing, more sensitive to component pricing. |

| Threat of Backward Integration | Credible threat = High Power | Major manufacturers have historically integrated backward to control costs and supply, a strategy that remains relevant. |

What You See Is What You Get

Stone Canyon Industries LLC Porter's Five Forces Analysis

This preview showcases the complete Stone Canyon Industries LLC Porter's Five Forces Analysis, mirroring the exact document you will receive immediately after purchase. Our commitment is to transparency, ensuring no surprises; the insights into competitive rivalry, the threat of new entrants, the bargaining power of buyers and suppliers, and the threat of substitute products are all present and professionally formatted for your immediate use.

Rivalry Among Competitors

Number and Diversity of Competitors

The industrial, transportation, and infrastructure sectors Stone Canyon Industries LLC operates in are characterized by a substantial number of competitors. This landscape includes both large, established players and smaller, specialized firms, creating a diverse competitive environment.

For instance, in the industrial sector, companies like General Electric and Siemens compete across various segments, while specialized manufacturers focus on niche markets. The transportation sector sees major players such as Union Pacific and FedEx alongside numerous regional logistics providers.

This diversity means competitors vary significantly in their size, strategic approaches, and market focus. Some may compete on scale and cost, while others differentiate through innovation or customer service, intensifying the rivalry for Stone Canyon Industries LLC.

The sheer volume and varied capabilities of these competitors contribute to a dynamic and often aggressive competitive landscape, demanding continuous adaptation and strategic maneuvering from Stone Canyon Industries LLC to maintain its market position.

Industry Growth Rate

The growth rate of the industries where Stone Canyon Industries LLC's (SCI) portfolio companies operate significantly influences the intensity of competitive rivalry. In slower-growing or mature markets, companies often battle fiercely for existing market share, which can lead to price wars and heightened promotional activities. For instance, if a large portion of SCI's holdings are in industries experiencing sub-2% annual growth, as some segments of traditional manufacturing have in recent years, rivalry will naturally be more pronounced.

Conversely, high-growth sectors can sometimes temper direct rivalry by providing ample opportunities for all participants to expand. If SCI has substantial investments in areas like specialized industrial automation or advanced materials, which have seen robust growth, the pressure to aggressively undercut competitors might be somewhat less acute as the overall market expands. Data from 2024 suggests that while some industrial sectors are seeing modest growth, others focused on technological advancement are expanding at rates exceeding 5% annually, creating a bifurcated competitive landscape for SCI.

Exit Barriers for Competitors

Stone Canyon Industries LLC operates in sectors where high exit barriers are common. For instance, industries with significant investments in specialized machinery or manufacturing facilities, like those often found in industrial manufacturing or certain consumer goods production, can make it difficult and costly for companies to simply walk away. These sunk costs essentially lock competitors into the market.

When competitors face these high exit barriers, they may continue to operate even in periods of low profitability. This can lead to increased competitive rivalry as these firms might resort to aggressive pricing strategies, such as deep discounting, to generate any revenue possible. This behavior directly impacts the profit margins of all companies within the industry, including Stone Canyon.

The persistence of unprofitable firms due to high exit barriers can create a challenging environment. For example, in the industrial equipment sector, where Stone Canyon has a presence, the average asset age can be quite high, indicating significant long-term investments that are hard to divest. This situation forces all players to contend with the potential for price wars driven by companies desperate to recover some of their invested capital.

Product Differentiation and Switching Costs

The intensity of competitive rivalry at Stone Canyon Industries (SCI) is significantly shaped by how distinct its products and services are from those of its competitors, alongside the effort customers need to make to switch. When products are very similar, essentially commodities, and it's easy for customers to switch to another provider, competition often heats up, leading to price wars. SCI's strategy of acquiring market-leading businesses implies a degree of product or service differentiation, but this can differ across the various sectors it operates in.

For instance, in some of SCI's industrial manufacturing segments, where specialized equipment or proprietary processes might be involved, differentiation could be higher, leading to less direct price competition. Conversely, in more standardized product lines, the rivalry might be more intense. Data from 2024 indicates that industries with high product similarity often see profit margins compressed due to this price-based competition.

- Product Differentiation Impact: SCI's success in its chosen markets, often characterized by established leaders, suggests a baseline level of differentiation, which can temper direct rivalry.

- Switching Costs: High switching costs, such as significant integration efforts or specialized training required for a competitor's product, can lock in customers and reduce the incentive for firms to engage in aggressive price competition.

- Industry Variation: The degree of differentiation and switching costs can vary widely across SCI's portfolio. For example, a custom-engineered component manufacturer will likely face different competitive dynamics than a supplier of more standardized industrial parts.

- 2024 Market Trends: In 2024, many industrial sectors have seen continued emphasis on supply chain reliability and customization, factors that can increase switching costs and reduce the impact of pure price competition.

Strategic Stakes and Commitments

The strategic importance of the sectors Stone Canyon Industries LLC (SCI) operates in significantly fuels competitive rivalry. When rivals perceive success in these areas as crucial for their overall corporate strategy or brand reputation, they are inclined to invest aggressively. This commitment can lead to intense competition for market share, even if it means sacrificing short-term profitability.

For instance, in the industrial manufacturing and services space, which SCI targets, major players often view market leadership as a validation of their technological prowess and operational efficiency. This perception drives them to deploy substantial capital and resources to maintain or expand their positions. In 2024, many large industrial conglomerates reported increased R&D spending, directly impacting competitive intensity in areas where SCI is active.

- Strategic Importance Drives Investment: Competitors see success in SCI's target industries as vital for their long-term growth and market standing.

- Aggressive Market Share Pursuit: This strategic imperative leads to intensified competition, with companies willing to invest heavily to capture or defend market share.

- R&D Investment as a Proxy: Increased research and development budgets in 2024 across major industrial players indicate a willingness to innovate and compete fiercely.

- Reputation and Technological Leadership: Companies strive for dominance not just for profit, but also to bolster their reputation as industry leaders and innovators.

Intense Rivalry Shapes Industrial, Transportation, and Infrastructure Markets

The competitive rivalry within the industrial, transportation, and infrastructure sectors where Stone Canyon Industries LLC operates is substantial and multifaceted. The presence of numerous competitors, ranging from large, established entities to smaller, specialized firms, ensures a dynamic market environment. For example, in 2024, the industrial automation sector, a key area for SCI, saw intensified competition as major players like Rockwell Automation and Siemens continued to vie for market share, with growth rates in certain sub-segments exceeding 5% annually.

This rivalry is further amplified by factors such as product differentiation, switching costs, and the strategic importance of these industries. When products are similar and switching is easy, price wars can erupt, compressing margins, a trend observed in 2024 for more commoditized industrial components. Conversely, high switching costs, often associated with specialized or integrated solutions, can mitigate this pressure. For instance, the need for extensive integration and training for advanced manufacturing systems can lock in customers, benefiting companies like those in SCI's portfolio that offer such solutions.

High exit barriers, common in capital-intensive industries where SCI invests, also contribute to rivalry. Companies with significant sunk costs may continue operating even at low profitability, potentially engaging in aggressive pricing to recoup investments. This was evident in some segments of the heavy machinery sector in 2024, where older firms, facing high asset age, sometimes resorted to discounting. The strategic importance of these sectors means competitors are often willing to invest heavily in R&D and market share, as indicated by increased R&D budgets reported by industry leaders in 2024, further intensifying the competitive landscape.

| Factor | Impact on Rivalry | Example/2024 Data Point |

|---|---|---|

| Number of Competitors | High | Numerous players in industrial automation, including Rockwell Automation and Siemens. |

| Industry Growth Rate | Moderate to High | Some industrial sub-segments grew over 5% annually in 2024; slower growth in mature markets increases rivalry. |

| Switching Costs | Variable (can reduce rivalry) | High for integrated manufacturing systems; lower for standardized parts. |

| Strategic Importance | High (fuels aggressive competition) | Companies invest heavily in market leadership for reputation and technological validation. |

| Exit Barriers | High (can sustain rivalry) | Significant sunk costs in specialized machinery can keep unprofitable firms competing. |

SSubstitutes Threaten

Price-Performance of Substitutes

The threat of substitutes for Stone Canyon Industries LLC (SCI) hinges on how effectively alternative solutions can meet customer needs, particularly in their industrial, transportation, and infrastructure sectors. If competitors offer products or services that perform better or cost less, customers might switch, impacting SCI's market share and profitability.

For instance, in the industrial sector, advancements in material science could lead to lighter, stronger, or more sustainable alternatives to traditional components SCI supplies. Similarly, the transportation industry is constantly evolving with the rise of electric vehicles and autonomous driving technologies, which may require different types of parts and services than those currently offered by SCI's traditional business lines. These shifts represent a tangible threat if SCI does not adapt its offerings.

In 2024, the global industrial automation market, a key area for SCI, was valued at approximately $65 billion, with a projected compound annual growth rate of over 10%. This growth signifies a strong demand, but also an environment ripe for disruptive technologies. If new, more efficient automation solutions emerge that significantly outperform existing ones, SCI could face substantial substitution pressure.

The infrastructure segment, particularly in construction and maintenance, also faces substitution threats from innovative building materials and methods. For example, pre-fabricated construction techniques or advanced composite materials could reduce the need for traditional steel or concrete products, potentially impacting SCI's offerings in these areas. The increasing focus on sustainability and lifecycle costs in infrastructure projects further amplifies this risk.

Customer Propensity to Substitute

Customer willingness to switch to substitute offerings significantly impacts the threat of substitutes for Stone Canyon Industries LLC. If customers are easily swayed by convenience, lower prices, or even environmental advantages offered by alternatives, this threat escalates, regardless of the number of direct competitors. This propensity is particularly pronounced when the costs associated with switching are minimal.

In 2024, for instance, the increasing availability of readily available, often digitally enabled, alternatives across many industrial sectors means customers can explore new solutions with unprecedented ease. This ease of exploration directly correlates with a higher propensity to substitute, especially if early adoption offers tangible benefits like reduced operational expenses or improved efficiency. For example, a survey of industrial buyers in early 2024 revealed that over 60% reported actively seeking alternative suppliers due to rising material costs.

Switching Costs to Substitutes

The threat of substitutes for Stone Canyon Industries LLC's (SCI) portfolio companies is significantly influenced by the switching costs customers face. These costs encompass not only direct financial expenses but also non-financial elements like the effort and time required to learn new systems or processes. For instance, in the industrial coatings sector where some SCI companies operate, switching from a proven, albeit older, paint formulation to a newer, eco-friendlier alternative might involve re-tooling application equipment and retraining staff, representing substantial switching costs.

Conversely, in markets where SCI’s products are more commoditized, like certain metal fabrication components, switching costs can be minimal. If a customer can easily source an equivalent part from another supplier without significant disruption or additional expense, the threat of substitutes intensifies. This low-switching-cost environment pressures SCI’s businesses to continuously offer competitive pricing and superior product performance to retain their customer base, as evidenced by the 2024 market data showing a 5% average price erosion in commodity metal parts due to increased supplier competition.

Innovation and Technological Advancements

Rapid innovation and technological advancements pose a significant threat of substitutes for Stone Canyon Industries LLC (SCI). Emerging technologies can swiftly introduce new products or services that offer similar benefits, often at a lower cost or with superior performance. For instance, advancements in additive manufacturing, or 3D printing, could provide on-demand, customized components, potentially reducing reliance on traditional manufacturing processes employed by some of SCI's portfolio companies. In 2024, the global additive manufacturing market was valued at approximately $20.7 billion and is projected to grow substantially, highlighting the increasing viability of these substitute technologies.

The emergence of disruptive technologies directly impacts SCI's business model by creating alternative solutions. Consider the transportation sector; the continued development of autonomous vehicle technology could eventually offer alternatives to traditional logistics and fleet management services that SCI might be involved in. Similarly, smart infrastructure solutions, leveraging IoT and advanced analytics, could provide more efficient alternatives to established utility and maintenance services. These shifts necessitate continuous adaptation and investment in R&D to remain competitive and mitigate the impact of these evolving substitutes. The pace of technological change means that what is cutting-edge today can become obsolete tomorrow, demanding constant vigilance.

- Disruptive Technologies: New materials, autonomous systems, and smart infrastructure represent direct threats.

- Market Value: The global additive manufacturing market's growth underscores the increasing threat of technological substitutes.

- Adaptation Necessity: SCI must invest in R&D and adapt its strategies to counter evolving alternatives.

- Competitive Landscape: Rapid technological evolution can quickly alter the competitive landscape, impacting SCI's market position.

Regulatory and Environmental Shifts

Changes in regulations and growing environmental awareness can significantly boost the appeal of substitute products for Stone Canyon Industries. For instance, stricter emissions standards, like those being implemented globally for industrial manufacturing, can make cleaner, alternative technologies more attractive. This is particularly relevant as many nations are aiming to meet ambitious climate targets, such as the European Union's goal of reducing greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels. Such policy shifts can directly increase the threat of substitutes by making established, less eco-friendly offerings less competitive or even non-compliant.

Furthermore, government incentives designed to promote sustainable practices can accelerate the adoption of alternatives. These might include subsidies for renewable energy sources or tax credits for businesses investing in greener technologies. As of early 2024, many countries are expanding their green investment programs, recognizing the economic opportunities in sustainable industries. This creates a direct competitive pressure on companies like Stone Canyon Industries whose products may not align with these evolving environmental mandates, potentially driving customers toward more environmentally conscious substitutes.

- Regulatory Pressure: New environmental laws or safety standards can make existing products less viable.

- Sustainability Focus: Growing public and governmental demand for sustainable solutions favors alternatives.

- Incentives for Alternatives: Government subsidies or tax breaks can make substitute products more cost-effective.

- Market Transformation: Policies like carbon pricing can alter the cost-benefit analysis for customers choosing between original and substitute offerings.

Industrial Shifts: Substitutes and New Tech Challenge Market

The threat of substitutes for Stone Canyon Industries LLC (SCI) is amplified by the increasing ease with which customers can access and evaluate alternative solutions. In 2024, a significant portion of industrial buyers reported actively seeking alternatives due to rising costs, demonstrating a low propensity to stick with incumbent suppliers if better options emerge. This trend suggests that minimal switching costs, coupled with readily available information on substitute products, create a dynamic where SCI must constantly prove its value to retain market share.

Emerging technologies like additive manufacturing, valued at approximately $20.7 billion in 2024, present a direct substitution threat by offering customized, on-demand components. Furthermore, evolving regulatory landscapes, driven by environmental concerns, favor greener alternatives. For example, the EU's goal of a 55% emissions reduction by 2030 incentivizes the adoption of sustainable technologies, potentially impacting SCI's traditional offerings if they are not aligned with these new standards.

| Area of Threat | Example Substitute | 2024 Market Relevance | Impact on SCI |

|---|---|---|---|

| Industrial Components | 3D Printed Parts | $20.7B Additive Mfg. Market | Reduced demand for traditional parts |

| Transportation | Electric Vehicle Components | Growing EV adoption rates | Shift in material and service needs |

| Infrastructure | Advanced Composite Materials | Increased focus on sustainable building | Potential decline in demand for traditional materials |

| Automation | New AI-driven Solutions | $65B Industrial Automation Market Growth | Risk of obsolescence for existing systems |

Entrants Threaten

Capital Requirements and Investment

The industries Stone Canyon Industries LLC operates within, such as industrial manufacturing and infrastructure, demand immense upfront capital. For instance, establishing a new manufacturing plant can easily cost hundreds of millions of dollars, with some projects exceeding billions. This high barrier, encompassing sophisticated machinery, extensive facilities, and robust supply chain infrastructure, effectively deters many potential competitors from entering these capital-intensive markets.

Economies of Scale and Experience

Existing market leaders within Stone Canyon Industries LLC's (SCI) diverse portfolio often possess significant economies of scale. This means they can produce goods or services at a lower cost per unit than a new entrant could, simply because they operate at a much larger volume. For instance, in the industrial manufacturing sector where SCI has holdings, established players might have optimized supply chains and bulk purchasing power that a startup simply cannot replicate initially.

Newcomers face a substantial hurdle in matching these cost advantages. Without the established volume, a new entrant to SCI's operating markets would struggle to achieve the same per-unit cost efficiencies. This makes competing on price challenging from day one, impacting their ability to gain market share and achieve profitability against incumbents that have benefited from years of operational experience and scale.

Access to Distribution Channels

Stone Canyon Industries LLC (SCI) benefits from established relationships and control over critical distribution channels, presenting a significant hurdle for new entrants. These entrenched networks and long-term contracts make it difficult and costly for newcomers to reach customers and effectively deliver their offerings. For instance, in the industrial manufacturing sector, where SCI has significant investments, securing shelf space or reliable logistics can be a major challenge for unproven companies.

Proprietary Technology and Patents

The threat of new entrants for Stone Canyon Industries LLC (SCI) is significantly mitigated by its portfolio companies' proprietary technology and extensive patent portfolios. For instance, in the advanced materials sector where SCI operates, securing patents on novel chemical formulations or manufacturing processes can create formidable barriers. These intellectual property rights not only protect SCI’s innovations but also necessitate substantial R&D investment and time for any competitor seeking to replicate or circumvent them. This upfront cost and knowledge gap effectively deter market entry.

SCI's commitment to innovation is evident in its continuous investment in research and development. While specific R&D spending figures for 2024 are proprietary, industry benchmarks for companies in SCI's operating sectors, such as specialty chemicals and industrial manufacturing, often see R&D expenditures ranging from 3% to 8% of revenue. This consistent investment allows SCI's businesses to stay ahead of technological curves.

- Proprietary Technology: SCI's market-leading entities possess unique technological capabilities, often protected by patents, which are difficult and costly for newcomers to replicate.

- Patent Protection: The extensive patent filings across SCI's diverse business units create legal and economic barriers, safeguarding market share and profitability.

- R&D Investment: Significant and ongoing investment in research and development ensures SCI's businesses maintain a technological edge, making it challenging for new entrants to compete on innovation.

- Specialized Knowledge: The accumulation of specialized operational and technical expertise within SCI's workforce further solidifies its competitive position, acting as a deterrent to less experienced market participants.

Government Policy and Regulation

Government policies and stringent regulations significantly deter new entrants in sectors where Stone Canyon Industries LLC operates. For instance, in the industrial and transportation sectors, obtaining various licenses, permits, and certifications involves navigating a complex web of compliance. In 2024, the average time to secure environmental permits for new industrial facilities in the United States ranged from 6 to 18 months, demonstrating the substantial lead time required.

Furthermore, evolving environmental regulations, such as those related to emissions and waste management, necessitate significant upfront investment in technology and compliance infrastructure. Companies must also adhere to rigorous safety standards, particularly in manufacturing and infrastructure, adding to operational costs and complexity. For example, compliance with OSHA's Process Safety Management standard can require millions in initial capital outlay for new facilities.

- High Capital Investment: Complying with safety and environmental standards often requires substantial initial capital expenditure, acting as a major deterrent for smaller potential competitors.

- Licensing and Permitting Hurdles: Securing necessary operational licenses and permits, especially in regulated industries like transportation, can be a lengthy and expensive process.

- Regulatory Compliance Costs: Ongoing adherence to evolving regulations demands continuous investment in technology, training, and reporting, increasing the cost of doing business.

- Industry-Specific Standards: Each sector Stone Canyon operates in, from manufacturing to infrastructure, has unique and often demanding compliance requirements that create barriers.

Immense Capital Costs Block New Entrants in Core Markets

The threat of new entrants for Stone Canyon Industries LLC (SCI) is significantly low due to the immense capital required to enter its core markets. Establishing new manufacturing facilities or infrastructure projects demands hundreds of millions, even billions, in upfront investment, effectively deterring most potential competitors. Furthermore, SCI's existing portfolio companies benefit from substantial economies of scale, allowing them to produce at lower per-unit costs than any newcomer could initially match, making price-based competition exceedingly difficult.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Stone Canyon Industries LLC leverages data from annual reports, industry-specific market research, and competitor financial disclosures to understand competitive intensity and market dynamics.