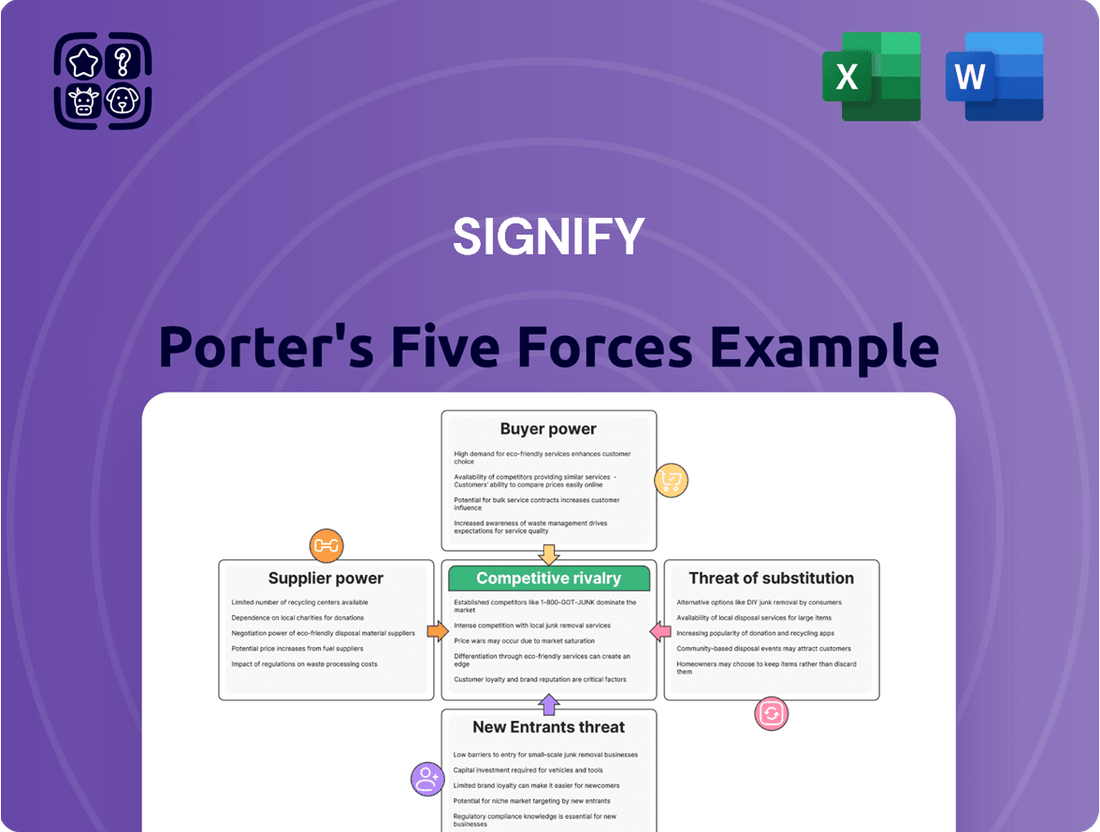

Signify Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Signify Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Signify operates within a dynamic lighting industry, facing distinct competitive pressures. Understanding the intensity of rivalry, the bargaining power of buyers and suppliers, and the threats of new entrants and substitutes is crucial for strategic positioning. These forces collectively shape Signify's profitability and market opportunities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Signify’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Suppliers

Suppliers of highly specialized components, such as advanced LED chips or complex electronic drivers, hold considerable bargaining power over Signify. This power stems from the unique nature of their products and the substantial costs Signify would incur if it switched to alternative suppliers. For instance, the development and manufacturing of cutting-edge LED technology often involve proprietary processes and significant R&D investment, making direct substitutes scarce.

Signify actively cultivates long-term, strategic relationships with these specialized suppliers. This approach is designed to encourage ongoing innovation and secure a reliable supply chain for critical components. By fostering these partnerships, Signify aims to gain early access to new technologies and ensure the consistent availability of high-quality materials necessary for its lighting solutions.

Raw Material Cost Fluctuations

Raw material and energy price volatility significantly impacts supplier bargaining power, directly affecting manufacturers like Signify. For instance, the global energy crisis and supply chain disruptions experienced in 2022 and extending into 2023 led to substantial increases in the cost of key components and manufacturing inputs for the lighting industry. Signify's strategy to counter this involves optimizing its worldwide production network and diversifying its supplier base to absorb these shocks and maintain cost stability.

To further manage these pressures, Signify actively pursues internal cost reduction initiatives and implements strategic price adjustments. In 2023, the company continued its focus on operational efficiencies and leveraging economies of scale across its diverse product lines. This proactive approach helps to offset the impact of fluctuating input costs, ensuring that Signify can maintain its competitive pricing while managing the inherent risks associated with raw material cost fluctuations.

Supplier Concentration and Diversification

Signify faces potential challenges if critical components for its lighting solutions come from a limited number of suppliers. This concentration grants those suppliers greater leverage in price negotiations and supply terms. For instance, if a specific type of LED chip is produced by only two or three global manufacturers, Signify’s ability to dictate terms is significantly reduced.

To mitigate this, Signify actively pursues a strategy of supplier diversification. By onboarding a wider range of suppliers for essential materials and components, the company dilutes the power of any single entity. This approach is crucial for maintaining stable production and cost control, especially in a dynamic global market where disruptions can occur.

Furthermore, Signify is implementing nearshoring initiatives, bringing production closer to its assembly facilities. This not only shortens lead times but also reduces dependence on distant suppliers, thereby lessening the bargaining power of those located far away. This strategic shift aims to build a more resilient and cost-effective supply chain for 2024 and beyond.

Technological Advancements and IP

Suppliers possessing patents or proprietary intellectual property for cutting-edge lighting, like advanced IoT sensors or LiFi technology, gain significant leverage. This allows them to dictate higher prices for their specialized components, directly impacting Signify's cost structure. For instance, the development of next-generation LED chips with enhanced efficiency or unique spectral properties could create such a situation.

Signify actively pursues collaborations to integrate these innovations, as seen in its partnership with EDZCOM for LiFi deployment. Such alliances can mitigate the bargaining power of individual suppliers by fostering a more integrated ecosystem, potentially leading to more favorable terms or shared development costs. This strategic approach aims to embed advanced technologies while managing supplier influence.

- Proprietary Technology: Suppliers with patents on critical components for smart lighting systems, such as advanced control chips or energy-efficient materials, hold considerable sway.

- Integration Partnerships: Signify's collaborations, like those involving LiFi or IoT integration, aim to secure access to new technologies and potentially reduce reliance on single, high-bargaining-power suppliers.

- Innovation Costs: The high cost of research and development for novel lighting technologies means suppliers who successfully innovate can demand premium pricing.

Sustainability Requirements

Signify's robust commitment to sustainability and responsible sourcing significantly shapes its supplier relationships. Suppliers must adhere to stringent environmental, social, and governance (ESG) standards, a requirement that can bolster the bargaining power of those already compliant or those actively investing in sustainable operations.

This focus means suppliers who can demonstrate strong ESG performance, such as reduced carbon emissions or ethical labor practices, become more valuable to Signify. For instance, in 2023, Signify reported that 84% of its total procurement spend was covered by its supplier sustainability assessments, highlighting the importance of these criteria.

- Suppliers meeting Signify's ESG criteria gain leverage due to the company's preference for sustainable partners.

- Signify actively engages with suppliers to improve their sustainability performance, creating opportunities for those willing to adapt.

- Suppliers who can offer verifiable sustainable materials or processes may command higher prices or better terms.

- The increasing global emphasis on ESG compliance within supply chains further strengthens the position of eco-conscious suppliers.

Supplier Power: Navigating Costs & Building Supply Chain Resilience

Suppliers of specialized, patented components or those with unique technological advantages can wield significant bargaining power over Signify. This is particularly true for advanced materials or proprietary software essential for smart lighting systems. For example, suppliers of next-generation LED chips with unique spectral properties or advanced IoT integration capabilities can dictate higher prices due to limited alternatives.

Signify mitigates this by fostering strategic partnerships and diversifying its supplier base. In 2023, Signify continued its focus on operational efficiencies and nearshoring initiatives to reduce reliance on distant suppliers and strengthen its supply chain resilience. The company's commitment to sustainability also influences supplier relationships, with 84% of its procurement spend covered by supplier sustainability assessments in 2023, favoring those with strong ESG performance.

| Factor | Impact on Signify | Mitigation Strategy |

| Proprietary Technology | Higher component costs, limited sourcing options | Strategic partnerships, integration collaborations |

| Supplier Concentration | Reduced negotiation leverage, supply disruption risk | Supplier diversification, nearshoring initiatives |

| ESG Compliance | Preference for compliant suppliers, potential premium pricing | Supplier engagement for ESG improvement, focus on compliant partners |

What is included in the product

Signify's Porter's Five Forces Analysis unpacks the competitive intensity within the lighting industry, assessing the power of buyers and suppliers, the threat of new entrants and substitutes, and the rivalry among existing players.

Instantly visualize competitive intensity and identify key leverage points with a dynamic, interactive Porter's Five Forces dashboard.

Customers Bargaining Power

Diverse Customer Base

Signify's diverse customer base, spanning professional clients like cities and stadiums alongside individual consumers, helps to dilute the overall bargaining power of customers. While major projects for municipalities or large commercial entities might involve significant purchasing volumes, giving those specific customers more leverage, the sheer number of individual home users creates a more fragmented and less powerful collective buying force.

Price Sensitivity in Commodity Segments

In commodity lighting segments, where products are largely undifferentiated, customers exhibit significant price sensitivity. This means they have considerable power to negotiate lower prices because switching to a competitor involves minimal switching costs. For Signify, this translates into pressure on margins within its conventional lighting business, which has seen a decline. For instance, in 2023, the general lighting division, which includes many of these conventional products, experienced a revenue decrease, underscoring the impact of price-driven competition.

Switching Costs and Ecosystem Lock-in

For smart lighting systems, especially those integrated into larger ecosystems like Signify's Philips Hue or Interact, customers can face significant switching costs. Once a user has invested in a range of smart bulbs, hubs, and potentially smart home integrations, moving to a competitor's system can be expensive and disruptive. This lock-in effect inherently reduces the bargaining power of these customers.

Signify's strategy of connecting lighting to data, extending its reach to devices, places, and people, further strengthens this ecosystem. As of 2024, the smart home market, which includes connected lighting, continues to grow, with many consumers prioritizing seamless integration and ease of use. This trend reinforces the stickiness of established platforms like Signify's.

Demand for Energy Efficiency and Sustainability

Customers, both in professional and consumer markets, are increasingly prioritizing energy efficiency and sustainability in their purchasing decisions. This growing demand for eco-friendly lighting solutions significantly enhances their bargaining power.

Signify's strategic alignment with these customer preferences, particularly through its strong emphasis on LED technology and circular economy initiatives, directly addresses this trend. Their commitment to achieving net-zero emissions by 2040 further solidifies their appeal to environmentally conscious buyers, giving these customers more leverage.

- Growing Demand: Consumer and business surveys consistently show a preference for sustainable products, with a significant portion willing to pay a premium for them. For instance, a 2024 report indicated that over 70% of consumers consider sustainability when making purchasing decisions.

- Signify's Response: Signify's substantial investment in LED technology, which offers significant energy savings over traditional lighting, directly caters to this demand. Their ongoing efforts in product lifecycle management and the adoption of recycled materials in manufacturing further bolster their sustainability credentials.

- Impact on Bargaining Power: The widespread availability of energy-efficient alternatives means customers can easily switch to competitors if Signify's offerings do not meet their sustainability criteria or price expectations, thereby increasing customer bargaining power.

Availability of Information and Comparison

The ease with which customers can access and compare product information, pricing, and features across various brands significantly amplifies their bargaining power, particularly in the standardized LED market. This transparency allows buyers to readily identify the best value, putting pressure on manufacturers to compete on price and specification.

Signify actively mitigates this by cultivating strong brand loyalty through its well-established names like Philips, Philips Hue, and WiZ. Furthermore, the company emphasizes innovation and the delivery of value-added services to differentiate its offerings beyond mere product comparison.

- Brand Loyalty: Philips Hue, a key Signify brand, reported strong growth in its smart lighting segment, indicating successful customer retention and premium pricing power.

- Innovation Focus: Signify's continuous investment in R&D, including advancements in connected lighting and energy-efficient technologies, creates product differentiation that lessens price sensitivity.

- Value-Added Services: The company's ecosystem of smart lighting solutions, including app integration and professional services, provides a comprehensive value proposition that moves beyond simple product features.

Customer Power Dynamics in Lighting Solutions

The bargaining power of customers for Signify is influenced by product differentiation and switching costs. While commodity lighting faces intense price competition, Signify's smart lighting systems, like Philips Hue, create customer lock-in through integrated ecosystems, reducing their power.

Brand loyalty and innovation are key strategies Signify employs to counter customer bargaining power. The strong recognition of brands like Philips Hue, coupled with continuous R&D in connected and energy-efficient lighting, helps differentiate offerings and lessen price sensitivity.

Transparency in product information and pricing amplifies customer leverage, especially in the standardized LED market. Signify addresses this by focusing on value-added services and the overall ecosystem, moving beyond simple product comparisons to build stronger customer relationships.

| Factor | Impact on Signify | Mitigation Strategy |

|---|---|---|

| Price Sensitivity (Commodity Lighting) | Pressures margins due to low differentiation and switching costs. | Focus on innovation and efficiency in higher-margin segments. |

| Switching Costs (Smart Lighting) | Lowers customer bargaining power due to ecosystem investment. | Continue to expand and integrate smart lighting ecosystems (e.g., Philips Hue). |

| Sustainability Demand | Increases customer leverage if offerings are not eco-friendly. | Invest in LED technology and circular economy initiatives. |

| Information Transparency | Empowers customers to compare and negotiate prices. | Build brand loyalty and emphasize value-added services. |

What You See Is What You Get

Signify Porter's Five Forces Analysis

This preview showcases the complete Signify Porter's Five Forces Analysis, offering a detailed examination of competitive forces within the lighting industry. The document you see here is precisely what you will receive, fully formatted and ready for your immediate strategic planning. This comprehensive analysis delves into the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry among existing competitors. You're previewing the final version—precisely the same document that will be available to you instantly after buying.

Rivalry Among Competitors

Market Concentration and Key Players

The global lighting market, while featuring a world leader in Signify, exhibits moderate concentration. Key competitors such as Acuity Brands, OSRAM, Eaton, and GE Current also command substantial market presence. This concentration among the top five players, holding a significant collective market share, underscores a landscape characterized by robust and intense rivalry.

Innovation and Technology Pace

The lighting industry is characterized by a relentless pace of innovation, especially in LED, smart, and connected lighting technologies. This drives fierce competition as companies vie to introduce cutting-edge features, superior energy efficiency, and seamless integration with the Internet of Things (IoT). Signify, a major player, actively fuels this rivalry through significant investments in research and development, focusing on advanced LED solutions, sophisticated connected lighting systems, and valuable data-driven services.

Product Differentiation and Value-Added Services

Competitors within the lighting industry, including Signify, actively differentiate themselves through a combination of advanced product features, robust brand recognition, and the offering of value-added services that extend beyond basic illumination. This strategic emphasis on differentiation is crucial in a market characterized by intense competition.

Signify, for instance, has strategically shifted its focus towards services-heavy solutions and the burgeoning area of connected lighting. This pivot complements its established strength in traditional product sales, aiming to capture greater market share and customer loyalty by providing integrated systems and ongoing support.

For example, Signify's Interact connected lighting systems offer data analytics and remote management capabilities, creating recurring revenue streams and deeper customer engagement. This move towards a service-oriented model is a direct response to evolving market demands and a key tactic to stand out against rivals who may still primarily focus on hardware sales.

In 2023, the global smart lighting market, a key area for Signify's service-led strategy, was estimated to be worth over $15 billion and is projected to grow significantly in the coming years. This growth underscores the importance of product differentiation and the increasing value placed on connected, intelligent lighting solutions.

Market Growth and Saturation

The LED lighting market is expanding, driven by energy efficiency mandates and smart city development, yet the traditional lighting sector is shrinking. This dynamic creates intense competition as companies vie for dominance in the burgeoning LED segments. Signify, for instance, has experienced a downturn in its conventional lighting sales, with projections for 2025 indicating a target of low single-digit topline growth once these legacy products are excluded.

This competitive landscape is further intensified by the differing growth trajectories within the broader lighting industry.

- Market Segmentation: Growth is concentrated in LED and smart lighting, while conventional lighting faces decline.

- Competitive Pressure: Companies are aggressively competing for market share in the expanding LED and smart lighting sectors.

- Signify's Strategy: The company is focusing on growing its LED and connected lighting portfolio, aiming for low single-digit growth in 2025, excluding conventional products, to navigate this shift.

Global Footprint and Regional Dynamics

Competitive rivalry in the lighting industry is intense, with players like Signify navigating a global landscape where regional market dynamics significantly influence competitive intensity. While global sales might fluctuate, a company's strength in specific regions, such as Signify's robust performance in the U.S. market, highlights the critical role of localized strategies in managing competitive pressures.

Signify's ability to maintain strong U.S. market performance, even amidst a global sales decline, underscores the varied competitive forces at play across different geographies. This regional resilience suggests effective adaptation to local market conditions, competitive pricing, and customer preferences, which are crucial for retaining market share.

- Global Competition, Regional Nuances: Companies vie for market share worldwide, but the intensity of this competition can differ considerably from one region to another.

- Signify's U.S. Strength: In 2023, Signify reported a notable positive development in its Americas segment, indicating a stronger competitive position in the U.S. market compared to other regions, despite overall global challenges.

- Localized Strategy Impact: This regional outperformance suggests that Signify's localized strategies, tailored to the specific demands and competitive landscape of the U.S. market, are proving effective.

- Varying Competitive Intensity: The contrast in performance points to differing levels of competitive rivalry, potentially due to the presence of strong local players, different economic conditions, or varying adoption rates of new technologies in other global markets.

Lighting Industry: Fierce Competition Fuels Innovation

The competitive rivalry within the lighting industry remains a significant force, compelling companies like Signify to constantly innovate and adapt. This intense competition is driven by a market that, while consolidating at the top, still features several strong global and regional players.

The ongoing shift towards LED and connected lighting technologies means companies must invest heavily in R&D to stay ahead. Signify's strategic focus on these growth areas, evidenced by its investment in Interact connected lighting systems, is a direct response to this dynamic. The global smart lighting market, projected for substantial growth beyond its over $15 billion valuation in 2023, highlights the lucrative nature of these innovations and the fierce race to capture market share.

Signify's performance, particularly its strength in the U.S. market in 2023, demonstrates how localized strategies can effectively counter intense global competition. This regional success is crucial as the company aims for low single-digit topline growth in 2025, excluding its declining conventional lighting segment.

| Competitor | Market Focus | Key Strengths |

|---|---|---|

| Signify | LED, Connected Lighting, Services | Innovation, Brand Recognition, Interact Systems |

| Acuity Brands | Smart Lighting, Building Management | Strong North American Presence, Integrated Solutions |

| OSRAM | LEDs, Automotive Lighting, Specialty Lighting | Technology Expertise, Global Reach |

| Eaton | Electrical Components, Lighting Controls | Diversified Portfolio, Energy Management |

| GE Current | LED Retrofits, Smart Lighting, Controls | Legacy Brand, Focus on Energy Efficiency |

SSubstitutes Threaten

Natural Lighting Solutions

Architectural designs that prioritize natural light penetration represent a significant indirect substitute for artificial lighting solutions. By maximizing daylight, these designs can substantially reduce the daytime reliance on electric lighting, thereby impacting the demand for Signify's indoor lighting products. For instance, buildings incorporating advanced daylight harvesting systems and passive solar design principles can achieve considerable energy savings. In 2023, the global smart lighting market, which includes systems that optimize natural light integration, was valued at approximately $15.6 billion, and it's projected to grow, indicating a growing trend towards such energy-efficient architectural approaches.

Non-Lighting Technologies for Similar Functions

For certain applications, technologies outside of traditional lighting can fulfill similar roles. For instance, advanced security systems incorporating cameras and motion sensors can decrease the need for extensive security lighting, and sophisticated sound systems can create atmosphere, potentially reducing the demand for mood lighting.

Signify is actively addressing this by broadening its offerings. The company is investing in data-enabled services through its connected lighting solutions. This strategic move aims to meet a wider range of customer requirements, extending beyond the primary function of illumination and creating new value propositions.

Alternative Energy-Saving Technologies

The threat of substitutes for energy-efficient lighting, particularly LED technology, arises from other energy-saving solutions within buildings. For instance, advancements in building insulation or more efficient heating, ventilation, and air conditioning (HVAC) systems can vie for the same capital expenditure budgets that might otherwise be allocated to lighting upgrades. However, the compelling energy savings offered by LED lighting, often exceeding 50% compared to traditional incandescent or fluorescent options, makes it a highly attractive and competitive investment in many scenarios.

Emerging Technologies with Overlapping Capabilities

New technologies could offer capabilities currently met by lighting systems, posing a threat of substitution. For instance, advancements in sensors and IoT devices might provide sophisticated data collection and environmental monitoring without relying on light-based infrastructure. Similarly, alternative security systems or building management platforms could offer ambiance control and monitoring features, diminishing the unique value proposition of smart lighting solutions. In 2023, the global IoT market was valued at over $1.5 trillion, demonstrating significant investment and growth in connected technologies that could encroach on traditional lighting domains.

Signify's own exploration into LiFi, a technology that uses light for data transmission, illustrates this dynamic. While LiFi can enhance connectivity, it also signals a broader trend where light itself can be repurposed for communication, potentially substituting conventional data networks. This strategic move by Signify highlights awareness of evolving technological landscapes where core functionalities might be delivered through novel, non-traditional means. The potential for these emerging technologies to offer integrated solutions could fragment the market for standalone lighting products.

- Emerging IoT devices: Sensors for environmental monitoring, security cameras, and smart home hubs offer data collection and control functions that could overlap with smart lighting capabilities.

- LiFi as a dual-purpose technology: Signify's own development in LiFi demonstrates how light can become a platform for data transmission, potentially substituting traditional Wi-Fi or wired networks.

- Integrated building management systems: Advanced platforms can control HVAC, security, and ambiance, reducing reliance on lighting systems for these functions.

- Market disruption potential: Technologies offering combined data, security, and ambiance control could present a compelling alternative to segmented smart lighting solutions.

DIY and Low-Cost Generic Solutions

The threat of substitutes for Signify is amplified by the rise of do-it-yourself (DIY) and low-cost generic lighting solutions. For basic illumination needs, consumers can readily opt for affordable, unbranded LED bulbs. These directly compete with Signify's more premium offerings. The market for smart home technology has also seen an influx of DIY kits and less integrated systems that provide similar functionalities at a lower price point.

Significant price erosion in the LED lamp market, observed throughout 2024, further strengthens this threat. Energy-efficient lighting is no longer a niche product, making it accessible to a broader consumer base. This accessibility means consumers have more choices outside of established brands like Signify, potentially impacting market share and pricing power.

- Availability of Low-Cost Generic LEDs: Basic LED bulbs are widely available from numerous manufacturers, often at a fraction of the cost of Signify's branded products.

- DIY Smart Home Solutions: The proliferation of DIY smart home kits, such as affordable smart plugs and basic smart bulbs, offers alternative ways to achieve smart lighting without investing in fully integrated systems.

- Price Competition: The general decline in LED pricing means that even basic Signify products face competition from cheaper, functionally similar alternatives. For instance, by late 2024, reports indicated average prices for standard LED bulbs had fallen by over 15% year-over-year in many regions.

- Accessibility of Energy Efficiency: The widespread availability and affordability of energy-efficient lighting, regardless of brand, reduces the perceived value of premium features for some consumer segments.

Natural Light & IoT: The Rising Tide of Lighting Substitutes

The threat of substitutes for Signify is significant, encompassing architectural designs that maximize natural light and alternative technologies that fulfill similar roles. For example, advanced building insulation and HVAC systems compete for capital expenditure, even as LED lighting offers substantial energy savings, often over 50% compared to older technologies. The growing IoT market, valued over $1.5 trillion in 2023, also presents a substitute threat as sensors and connected devices can offer environmental monitoring and ambiance control without relying on traditional lighting infrastructure.

Entrants Threaten

High Capital Investment

Entering the global lighting market, particularly in areas like LED component manufacturing and smart lighting systems, demands significant upfront capital. Companies need to invest heavily in research and development to innovate, build state-of-the-art production facilities, and establish robust supply chains. For instance, setting up a modern LED manufacturing plant can easily run into tens of millions of dollars, creating a substantial hurdle for newcomers.

Research and Development Intensity

The lighting industry, especially in smart and connected solutions, demands substantial and ongoing investment in research and development. Signify, for instance, consistently allocates resources to innovation, as evidenced by its significant R&D expenditure. For example, in 2023, Signify reported R&D expenses of €421 million, highlighting the capital intensity required to stay competitive.

Newcomers face a considerable hurdle in matching Signify's established innovation capabilities and its robust patent portfolio, which protects its technological advancements and market position. This R&D intensity acts as a significant barrier, making it difficult for new players to develop comparable product offerings and intellectual property.

Established Distribution Channels and Brand Loyalty

Signify's established global distribution channels present a significant hurdle for potential new entrants. For instance, their extensive network reaches across numerous countries, making it challenging for newcomers to secure comparable market access and shelf space. This deep penetration means that even with a superior product, a new company would struggle to get its offerings in front of consumers effectively.

Brand loyalty, particularly with brands like Philips and Philips Hue, further solidifies Signify's position. Years of marketing and product quality have cultivated trust and preference among consumers. Acquiring this level of customer allegiance requires substantial investment in marketing and consistent product performance, resources that are often beyond the reach of nascent competitors.

In 2023, Signify reported sales of €7.5 billion, demonstrating the scale of their existing market presence. This financial strength underpins their ability to maintain and expand their distribution and marketing efforts, creating a formidable barrier to entry for any new player aiming to compete in the lighting industry.

Regulatory Hurdles and Standards

The lighting industry faces significant barriers to entry due to stringent regulatory hurdles and evolving standards. Companies looking to enter the market must grapple with a complex web of energy efficiency mandates, safety certifications, and interoperability requirements, such as the Matter standard for smart lighting systems. For example, in 2024, many regions continued to update their energy performance standards for lighting products, requiring substantial investment in research and development to meet these new benchmarks. Compliance with these regulations can be a substantial cost and time burden for new players, potentially delaying product launches and increasing initial capital expenditure.

Navigating these requirements is not a minor undertaking. It often necessitates specialized expertise and dedicated resources to ensure all products meet the necessary legal and technical specifications. Failure to comply can result in product recalls, fines, and reputational damage, effectively deterring many potential new entrants. The ongoing development and adoption of smart home and IoT standards further complicate this landscape, demanding that new products seamlessly integrate with existing ecosystems.

- Energy Efficiency Regulations: Many countries have implemented or are strengthening regulations like the US Department of Energy's (DOE) energy conservation standards for lighting products, impacting luminaire efficiency requirements.

- Safety Standards: Compliance with safety certifications such as UL (Underwriters Laboratories) or CE (Conformité Européenne) marks is mandatory for market access in many regions.

- Interoperability Standards: The growing adoption of standards like Matter for smart lighting necessitates backward compatibility and adherence to specific protocols, adding complexity for new entrants.

- Testing and Certification Costs: The process of testing and obtaining certifications for new lighting products can range from thousands to tens of thousands of dollars per product line, a significant upfront cost.

Intellectual Property and Patents

Signify's robust portfolio of intellectual property and patents presents a significant barrier to new entrants in the lighting industry. These patents, covering areas like advanced LED chip design, energy-efficient lighting technologies, and sophisticated smart lighting control systems, create a strong competitive moat.

For instance, in 2023, Signify continued to invest heavily in R&D, securing new patents that further solidify its technological leadership, especially in connected lighting solutions and sustainable illumination. This extensive IP library means newcomers would either need to develop entirely novel, non-infringing technologies or face substantial costs for licensing Signify's existing innovations.

- Extensive Patent Portfolio: Signify holds thousands of patents globally, safeguarding its technological advancements in LED, smart lighting, and IoT integration.

- R&D Investment: Signify's commitment to research and development, with significant annual expenditures, consistently generates new IP, reinforcing its market position.

- Licensing Costs: Potential new entrants face high costs associated with licensing Signify's patented technologies, deterring market entry.

- Innovation Challenges: Developing comparable or superior lighting technology without infringing on Signify's IP requires substantial innovation and investment from new players.

High Barriers Secure Lighting Market from New Entrants

The threat of new entrants into the lighting market, including segments Signify operates in, is moderately low. High capital requirements for manufacturing and R&D, coupled with established brand loyalty and extensive distribution networks, create significant barriers. For example, Signify reported sales of €7.5 billion in 2023, illustrating the scale of established players. This financial muscle allows them to invest heavily in innovation and market penetration, making it challenging for newcomers to compete effectively.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built on a robust foundation of data, including proprietary market research, industry-specific trade publications, and comprehensive company financial statements. This multi-faceted approach ensures a thorough understanding of competitive intensity and strategic positioning.