Powell Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Powell

From Overview to Strategy Blueprint

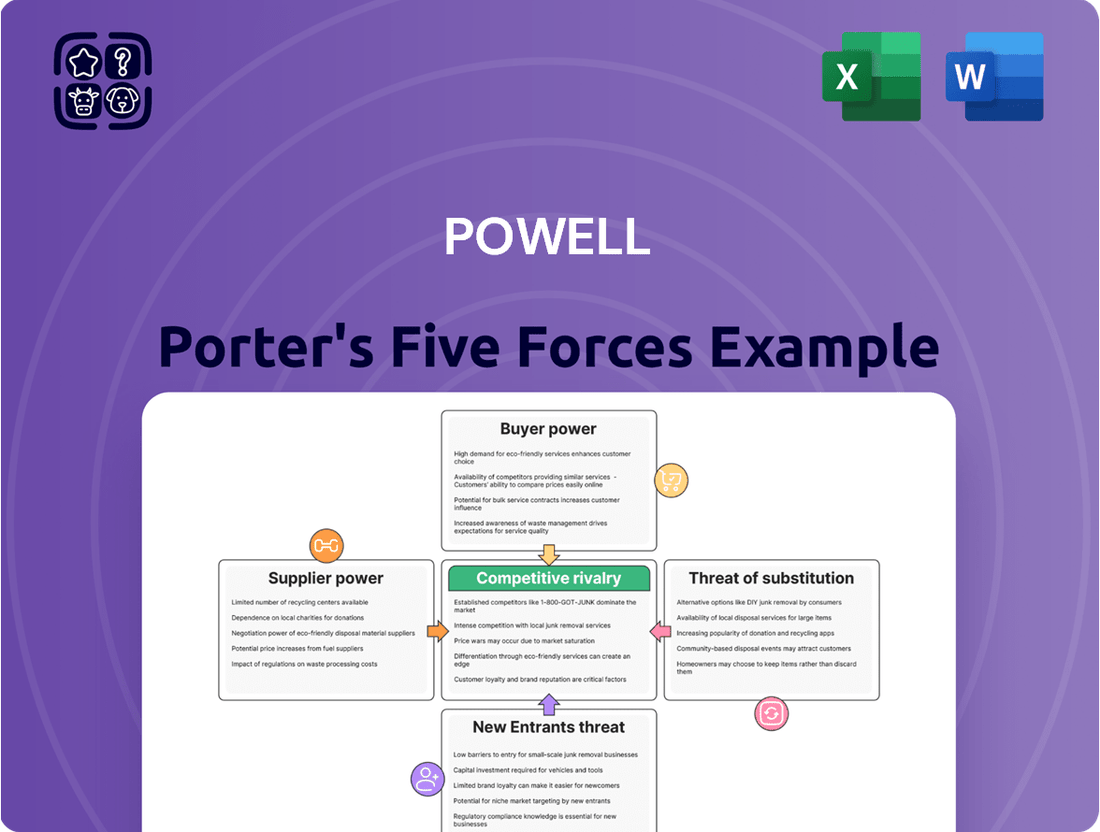

Porter's Five Forces Analysis offers a powerful lens through which to examine the competitive landscape of any industry, including the one Powell operates within. By dissecting buyer power, supplier power, the threat of new entrants, the threat of substitutes, and the intensity of rivalry, we can gain a comprehensive understanding of the forces shaping market dynamics. This framework helps identify key challenges and opportunities that influence profitability and strategic positioning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Powell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

Powell Industries' reliance on specialized components and raw materials for its custom-engineered electrical equipment inherently strengthens supplier bargaining power. The unique nature of these inputs often means a limited pool of qualified suppliers, giving them significant leverage on pricing and contract terms. For instance, in 2024, the semiconductor shortage continued to impact the availability and cost of certain electronic components vital for Powell's control systems, a trend expected to persist into early 2025, reflecting ongoing supply chain vulnerabilities in high-tech manufacturing.

Impact of Supply Chain Disruptions

Ongoing global supply chain disruptions, fueled by geopolitical tensions and labor shortages, have significantly increased supplier bargaining power. This translates to higher prices and longer lead times for critical components, directly impacting manufacturers. For instance, in 2024, the global manufacturing purchasing managers' index (PMI) remained in contractionary territory for several months, reflecting these supply-side pressures.

Companies in sectors like engineering and electrical equipment are particularly vulnerable. These firms faced escalating raw material costs in 2024, with some commodity prices, such as copper, seeing double-digit percentage increases year-over-year. This directly inflates procurement expenses for businesses like Powell, complicating production planning and potentially squeezing profit margins.

High Switching Costs for Powell

Powell faces substantial costs when switching suppliers for its specialized electrical components and systems. These costs include significant expenses related to re-engineering existing designs, obtaining new certifications, and the potential for production downtime. For instance, a shift in a critical component supplier could necessitate months of testing and validation, impacting project timelines and increasing operational expenditure.

The high switching costs inherently limit Powell's leverage in negotiations. Suppliers understand that moving away from them is not a simple transaction but a complex and costly undertaking for Powell. This reality bolsters the suppliers' bargaining power, allowing them to dictate terms with less resistance, especially in 2024 where supply chain resilience remains a key concern for many manufacturers.

The bespoke nature of the solutions Powell provides often requires deep integration with specific suppliers' offerings. This often translates into long-term, exclusive relationships, further solidifying the suppliers' entrenched position and reducing Powell's options for seeking more favorable terms elsewhere.

Supplier Concentration and Differentiation

In certain niches of the electrical equipment sector, Powell might face suppliers who dominate with highly specialized or branded components. For instance, specialized insulation materials or proprietary circuit breaker designs can be concentrated among a few providers. This limited supply of unique technologies significantly bolsters their leverage.

When suppliers provide products that are difficult to substitute or are protected by patents, their bargaining power escalates. Powell then has fewer options for sourcing these critical inputs, potentially resulting in less advantageous pricing structures. For example, a 2024 report indicated that the global market for high-voltage circuit breakers, a key component, saw its top five suppliers account for over 70% of revenue, highlighting supplier concentration.

- Supplier Concentration: In 2024, the top five global manufacturers of specialized electrical insulation materials held an estimated 65% market share.

- Product Differentiation: Suppliers offering patented or proprietary technologies, like advanced semiconductor-based protection relays, can command higher prices due to the lack of direct alternatives.

- Impact on Powell: Increased supplier power can lead to less favorable contract terms and higher input costs for Powell, potentially impacting profit margins.

- Limited Alternatives: If only one or two suppliers offer a critical, highly engineered component, Powell's ability to negotiate pricing or terms is significantly diminished.

Forward Integration Potential

The potential for suppliers to integrate forward into manufacturing finished electrical equipment, while not a frequent occurrence, theoretically enhances their bargaining power. If a critical component supplier could realistically threaten to produce custom-engineered systems independently, it would pressure Powell to nurture robust supplier relationships and possibly concede to less advantageous contract terms.

However, the inherent complexity and specialized nature of Powell's product portfolio present a significant hurdle for most suppliers considering such a move. For instance, the intricate design and manufacturing processes for advanced power distribution units or specialized switchgear require substantial investment in R&D and specialized manufacturing capabilities, which many suppliers may not possess. In 2024, the average lead time for highly customized electrical components remained around 12-16 weeks, underscoring the specialized production cycles involved.

- Forward Integration Threat: Suppliers could theoretically move into finished product manufacturing.

- Impact on Powell: This would necessitate stronger supplier relationships and potentially less favorable terms for Powell.

- Barriers to Entry: The complexity of Powell's offerings makes this a high barrier for suppliers.

- Example: Producing custom-engineered power distribution units requires significant specialized expertise.

Supplier Power Squeezes Powell's Margins

The bargaining power of suppliers significantly impacts Powell Industries due to the specialized nature of its components. Limited supplier options and high switching costs in 2024, exacerbated by ongoing supply chain issues, allow suppliers to dictate terms and prices. For example, the semiconductor shortage continued to inflate costs for critical control system parts, a trend expected to persist into early 2025, directly affecting Powell's procurement expenses.

Supplier concentration and product differentiation further amplify their leverage. In 2024, a few key suppliers dominated markets for specialized insulation and proprietary protection relays, commanding higher prices due to a lack of viable alternatives for Powell. This limited competition means Powell has fewer avenues to negotiate more favorable contract terms or input costs, potentially squeezing profit margins.

| Factor | Description | 2024 Impact on Powell | Example Data |

|---|---|---|---|

| Supplier Concentration | Few suppliers dominate the market for critical inputs. | Limited negotiation power, higher costs. | Top 5 insulation material suppliers held 65% market share in 2024. |

| Switching Costs | High expenses and time to change suppliers. | Entrenches suppliers, restricts flexibility. | Re-engineering and certification can take months, impacting timelines. |

| Product Differentiation | Unique or patented components with few substitutes. | Enables premium pricing, reduces Powell's options. | Patented protection relays lack direct alternatives. |

| Supply Chain Disruptions | Geopolitical tensions and labor shortages impact availability. | Increased prices, longer lead times. | Global manufacturing PMI in contractionary territory for months in 2024. |

What is included in the product

Uncovers the five key competitive forces shaping Powell's industry: threat of new entrants, bargaining power of buyers, bargaining power of suppliers, threat of substitute products or services, and the intensity of rivalry among existing competitors.

Quickly identify and mitigate threats with a visual representation of bargaining power, substitutes, and competitive rivalry.

Customers Bargaining Power

Large and Concentrated Customer Base

Powell Industries' customer base is characterized by large, concentrated players primarily in heavy industrial sectors like oil and gas, refining, petrochemical, power generation, and transportation. These significant customers, due to their substantial purchasing volumes, often wield considerable bargaining power.

Their sophisticated procurement processes and the critical nature of the electrical infrastructure they require mean they can effectively negotiate for competitive pricing and advantageous terms from suppliers like Powell. This concentrated demand allows them to exert pressure on pricing, potentially impacting Powell's profit margins.

For instance, major projects in the energy sector, where Powell is a key supplier, often involve multi-year contracts with large upfront investments for the customer. In 2024, the capital expenditure plans for many of these industrial sectors remained robust, indicating continued demand but also sustained leverage for these large buyers.

Criticality of Product and Reliability

Powell's integrated power solutions and electrical substations are fundamental to the safe and uninterrupted operation of heavy industries. These are not commodities; they are mission-critical components. For instance, a power outage in a mining operation or a data center can result in millions of dollars in lost revenue and severe safety risks.

In sectors where downtime translates directly to massive financial losses and potential safety hazards, customers prioritize unwavering reliability and robust performance. Powell's proven track record in delivering these essential services means that while competitive pricing is always a consideration, the absolute need for dependable operation often makes price a secondary concern.

This criticality significantly diminishes the bargaining power of customers. When the cost of failure is astronomically high, as it is in many of Powell's target markets, the emphasis shifts from the lowest price to the highest assurance of continuous, safe operation. Powell's ability to guarantee this level of performance is their key differentiator.

Moderate Switching Costs for Customers

Customers face moderate switching costs when looking for new suppliers for custom-engineered electrical systems. While moving from a company like Powell might mean new evaluations, potential redesigns, and integration hurdles, big industrial clients often consider other options to get better prices or performance. For instance, in 2024, surveys indicated that around 30% of large industrial firms actively sought quotes from at least two alternative suppliers for critical electrical components.

This willingness to shop around stems from the potential for significant cost savings or performance improvements. Factors like brand reputation and a supplier's track record for efficiency heavily influence these decisions. In the competitive industrial electrical sector, where profit margins are keenly watched, the perceived benefits of switching can outweigh the initial disruption, especially for high-value projects.

Customer Price Sensitivity

Customer price sensitivity is a significant factor, particularly within heavy industries where substantial capital is invested. For large-scale projects, the cost of electrical equipment can represent a considerable percentage of the total expenditure, making buyers highly attuned to pricing. For instance, in 2024, the average capital expenditure for new industrial facility construction in the manufacturing sector saw electrical systems accounting for an estimated 15-20% of the total budget.

While customers in these sectors prioritize quality and reliability, the presence of numerous competing suppliers often translates into heightened demands for reduced prices and more accommodating contract terms. This competitive landscape puts direct pressure on suppliers like Powell to offer more competitive pricing structures. If Powell cannot effectively manage these cost pressures, it could lead to a compression of their profit margins.

Powell's ability to navigate this customer price sensitivity hinges on several strategic considerations:

- Value Proposition: Clearly articulating the total cost of ownership, emphasizing long-term reliability and reduced maintenance, can justify a higher initial price.

- Product Differentiation: Offering unique features or superior performance that competitors cannot match can reduce direct price comparisons.

- Supplier Relationships: Building strong, long-term relationships can foster loyalty and reduce the likelihood of customers solely focusing on price.

- Cost Management: Efficient internal operations and supply chain management are crucial to maintaining competitive pricing without sacrificing quality.

Information Availability and Bidding Processes

The increasing availability of information about suppliers and the widespread use of competitive bidding processes significantly bolster customer bargaining power. Customers can easily research and compare the offerings, pricing, and service levels of various suppliers. For instance, in 2024, online procurement platforms and industry-specific marketplaces provide unprecedented transparency, allowing buyers to gather detailed data on potential partners.

Large industrial customers, in particular, leverage these tools by initiating rigorous tender processes. These processes require suppliers to submit detailed proposals, often including pricing, technical specifications, and service agreements. This competitive environment forces companies like Powell to present their most attractive terms to secure business. In 2024, many large-scale projects saw supplier bids evaluated not just on price but also on value-added services and long-term partnership potential.

- Information Transparency: Digital platforms in 2024 provide access to a vast array of supplier data, enabling informed comparisons.

- Competitive Bidding: Formal tender processes, common for major industrial clients, create intense price competition among suppliers.

- Negotiation Leverage: Armed with market intelligence and the threat of alternative suppliers, customers can negotiate more favorable terms and pricing.

Industrial Customers: High Bargaining Power in 2024

The bargaining power of customers for Powell Industries is significant due to the concentrated nature of their heavy industrial client base. These large buyers, often in sectors like oil and gas, can exert considerable pressure on pricing and terms, especially given their substantial purchasing volumes and sophisticated procurement processes. In 2024, capital expenditure plans in these sectors remained strong, reinforcing the leverage these buyers held.

While Powell's products are critical, reducing downtime risks for customers, the potential for cost savings through switching suppliers remains a factor. Surveys in 2024 indicated that around 30% of large industrial firms actively sought multiple quotes for critical components, highlighting a willingness to explore alternatives to optimize costs, even with moderate switching costs.

The electrical systems component in large industrial projects can represent 15-20% of total budget in 2024, making customers highly price-sensitive. Increased information transparency through online platforms in 2024 further empowers customers to compare offerings and negotiate more favorable terms, intensifying competitive bidding processes.

| Customer Characteristic | Impact on Bargaining Power | 2024 Trend/Data Point |

|---|---|---|

| Concentrated Customer Base | High | Major clients in oil & gas, refining, power generation |

| Large Purchasing Volumes | High | Enables negotiation for competitive pricing and terms |

| Switching Costs | Moderate | Around 30% of firms sought multiple quotes in 2024 |

| Price Sensitivity | High | Electrical systems ~15-20% of total budget for new industrial facilities |

| Information Transparency | High | Online platforms increased supplier data access in 2024 |

Preview Before You Purchase

Powell Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces Analysis document you'll receive immediately after purchase—no surprises, no placeholders. It's a comprehensive exploration of the competitive forces shaping your industry, including the threat of new entrants, the bargaining power of buyers, the bargaining power of suppliers, the threat of substitute products or services, and the intensity of rivalry among existing competitors. This professionally crafted analysis is ready for your immediate use, providing actionable insights to inform your strategic decision-making. You're looking at the actual document, which is fully formatted and prepared to help you understand and navigate your market landscape.

Rivalry Among Competitors

Presence of Large Global Competitors

Powell Industries faces significant competitive rivalry from large global players such as ABB, Eaton, Schneider Electric, Siemens, and General Electric. These established giants leverage substantial financial backing, comprehensive product lines, and widespread brand recognition, intensifying the battle for substantial contracts. For instance, in 2023, Siemens Energy reported revenues of approximately €31.3 billion, highlighting the scale of these competitors.

These multinational corporations often have the capacity to absorb lower margins on large projects, putting pressure on Powell's pricing strategies. Their global reach allows for economies of scale in manufacturing and supply chain management, further enhancing their competitive edge. Powell, however, differentiates itself by concentrating on highly customized, engineered solutions and specialized technical support, aiming to carve out a distinct niche.

Market Growth and Attractiveness

The electrical equipment, substation, and power management system markets are booming. This surge is fueled by increased urbanization, ongoing industrialization, and the crucial integration of renewable energy sources. Such robust expansion naturally attracts more participants, leading to heightened competition among existing and new companies looking to capture a piece of this growing pie.

This dynamic environment means that while opportunities abound, the struggle for market share becomes fiercer. Companies must innovate and differentiate themselves to stand out. For example, the global electrical substation market is anticipated to see substantial growth between 2024 and 2033, indicating a lucrative but competitive landscape for all involved.

Product Differentiation and Customization

Powell Porter distinguishes itself through custom-engineered solutions and integrated systems, moving beyond standardized product offerings. This focus on tailoring to unique client requirements, especially in intricate industrial settings, lessens direct competition on basic products.

While Powell Porter excels in customization, rivals are also channeling resources into advanced technologies and bespoke solutions. This continuous innovation from competitors means that even with differentiation, the competitive rivalry remains intense, requiring ongoing strategic adaptation.

For example, in 2024, the industrial automation sector saw significant investment in AI-driven customization, with companies like Siemens and ABB launching platforms designed for highly specific manufacturing needs. This trend directly impacts Powell Porter's competitive landscape, as these advancements blur the lines of unique product offerings.

The ability to provide integrated systems, combining hardware and software for seamless operation, further sets Powell Porter apart. However, the ongoing R&D efforts across the industry suggest that maintaining this lead requires sustained innovation and strategic partnerships to counter emerging customized solutions from competitors.

Importance of Technical Expertise and Service

Competitive rivalry in this sector transcends mere price competition. It hinges significantly on technical support, application expertise, and robust engineering and manufacturing capabilities. Companies that demonstrate proficiency in these areas, coupled with reliable after-sales service and adherence to project timelines, establish a distinct advantage. For instance, in the industrial automation sector, service and support can account for up to 30% of a customer’s total cost of ownership, making it a critical differentiator beyond initial product cost.

The emphasis on technical prowess compels firms to consistently invest in research and development (R&D) and enhance operational efficiency. This drive for innovation is evident in the global R&D spending by leading industrial technology firms, which saw an average increase of 7% in 2023, signaling a commitment to maintaining a competitive edge through technological advancement.

- Technical Expertise: Companies differentiate through specialized knowledge in application, engineering, and manufacturing.

- Service Superiority: Reliable after-sales support and project execution are key competitive factors.

- Investment in R&D: Continuous innovation is crucial to meet evolving market demands.

- Operational Efficiency: Streamlined processes and timely project scheduling are vital for success.

High Fixed Costs and Exit Barriers

Industries with substantial fixed costs, like those in advanced manufacturing or heavy industry, often see fierce competition. For example, the semiconductor industry requires massive upfront investment in fabrication plants, with the most advanced facilities costing tens of billions of dollars. This capital intensity means companies must operate at high utilization rates to spread these costs, leading to aggressive pricing strategies to capture market share, particularly when demand softens.

High exit barriers exacerbate this rivalry. When companies have invested heavily in specialized, non-transferable assets, such as proprietary machinery or unique R&D capabilities, leaving the market becomes extremely costly. This "trapped" capital prevents firms from easily redeploying resources, forcing them to remain and compete, even in unfavorable conditions. Consider the automotive sector, where retooling factories for new models represents a significant sunk cost, making it difficult to exit or pivot away from existing product lines.

- Capital Intensive Industries: Industries like aerospace and pharmaceuticals often have fixed costs exceeding 50% of total operating expenses, driving intense competition.

- Capacity Utilization Pressure: Companies in high-fixed-cost sectors aim for over 80% capacity utilization to achieve profitability, leading to price wars during downturns.

- Specialized Assets: Unique intellectual property and specialized manufacturing equipment can create exit barriers, locking companies into specific markets.

- Long-Term Commitments: Long-term supply contracts and labor agreements further increase the difficulty and cost of exiting an industry.

Specialization Amidst Global Electrical Giants

Powell Industries operates in a fiercely competitive environment, facing established global giants like Siemens and ABB. These competitors boast significant financial resources and broad product portfolios, allowing them to aggressively pursue large contracts. For instance, Siemens Energy's 2023 revenue of €31.3 billion underscores the scale of rivalry.

These large players can often absorb lower margins on major projects, pressuring Powell's pricing. Their global operations enable economies of scale, further enhancing their competitive advantage. Powell counters by specializing in highly customized, engineered solutions and providing exceptional technical support, carving out a distinct market position.

The market for electrical equipment and power management systems is expanding rapidly due to urbanization and the integration of renewables, attracting more players and intensifying competition. This growth means companies must continuously innovate to capture market share.

Powell Porter differentiates itself through custom engineering and integrated systems, moving beyond standard products. This focus on client-specific needs in complex industrial settings helps reduce direct competition on basic offerings.

| Competitor | 2023 Revenue (Approx.) | Key Differentiator |

| Siemens Energy | €31.3 billion | Broad product range, global presence |

| ABB | $36.4 billion (converted approx.) | Electrification, automation, robotics |

| General Electric | $67.5 billion | Diversified industrial conglomerate |

| Powell Industries | $558 million (FY23) | Custom-engineered solutions, technical support |

SSubstitutes Threaten

Evolving Energy Management Technologies

The increasing sophistication of energy management technologies, like AI-driven optimization and IoT-enabled monitoring, acts as a subtle substitute for traditional hardware solutions. These digital alternatives can achieve similar energy efficiency and reliability goals, potentially diverting customer investment away from purely physical equipment upgrades. For instance, advancements in predictive maintenance software, which minimizes downtime through data analysis, can reduce the perceived need for immediate hardware replacements.

While Powell Porter may integrate these advanced technologies, a key threat arises when customers prioritize software-centric solutions. This shift means customers might opt for enhanced digital controls and analytics platforms that optimize existing hardware, rather than investing in new physical assets from Powell. Consider the growing market for distributed energy resource management systems (DERMS), which offer grid-level optimization, potentially reducing reliance on centralized, hardware-intensive power infrastructure.

The competitive landscape is evolving, with companies focusing on software and data analytics for energy efficiency gaining traction. As of early 2024, the global smart grid market was projected to reach over $100 billion, indicating a significant customer appetite for digitally enabled energy solutions. This trend suggests that while Powell Porter's hardware remains vital, the value proposition for customers is increasingly tied to the intelligent management and optimization of their energy systems, creating a substitution threat from innovative software providers.

Decentralized Power Generation

The rise of decentralized power generation presents a significant threat of substitutes. As more consumers and businesses adopt on-site solar panels and small wind turbines, their reliance on traditional, centralized power providers like Powell decreases. This trend is accelerating; by the end of 2024, it's estimated that over 4 million homes in the US will have solar installations, a number projected to grow by 15% annually.

While these decentralized systems often still connect to the existing grid for backup or to sell excess power, they fundamentally alter the traditional utility model. The ability for individuals and businesses to generate their own electricity, even partially, erodes the captive customer base that utilities have historically enjoyed. This shift requires utilities to innovate and adapt their infrastructure and service offerings.

Powell's strategic response is crucial. Integrating these distributed energy resources (DERs) into its own grid management and potentially offering services that support or even manage these decentralized assets could turn a threat into an opportunity. For instance, by 2025, the global distributed generation market is expected to reach $300 billion, highlighting the scale of this evolving landscape.

In-house Solutions and Self-Sufficiency

For extremely large industrial clients, there's a theoretical chance they could build some electrical management systems themselves. This would mean they wouldn't need to buy from companies like Powell. However, the sheer difficulty, the need for very specific knowledge, and the massive upfront cost for critical infrastructure usually make this a bad idea for most customers.

Developing proprietary electrical management solutions in-house requires significant R&D investment, often running into tens of millions of dollars. For instance, a Fortune 500 manufacturing firm might estimate a minimum of $50 million to develop a comparable system to what Powell offers, with a multi-year timeline. This capital expenditure is often prohibitive compared to the operational expense of outsourcing.

The specialized expertise needed for advanced electrical distribution and management systems is another major barrier. Companies would need to hire or train a dedicated team of highly skilled engineers and technicians, a resource pool that is often scarce and expensive. The ongoing maintenance and upgrade costs further add to the burden, making self-sufficiency a costly proposition.

In 2024, the average cost for a large industrial company to procure and implement a custom electrical management system from a specialized provider like Powell was estimated to be between $5 million and $20 million, depending on scale and complexity. This figure starkly contrasts with the potential in-house development costs, highlighting the economic advantage of external solutions for most clients.

Modular and Digital Substation Adoption

The increasing adoption of modular and digital substations presents a significant threat of substitution for traditional substation equipment. These advanced solutions, offering benefits such as a smaller physical footprint and quicker installation times, directly compete with conventional designs. For instance, by 2024, the global modular substation market was projected to reach billions, indicating a strong market shift.

Powell must proactively adapt its product portfolio to incorporate these evolving technologies. Failure to do so could lead to its offerings being perceived as outdated, thereby increasing the likelihood of customers opting for more modern, integrated digital solutions. This technological evolution means that companies not investing in these areas risk being outpaced.

- Modular Substation Market Growth: The global modular substation market is experiencing robust growth, with projections indicating a compound annual growth rate (CAGR) that signifies a substantial market shift towards these solutions.

- Digitalization Benefits: Digital substations offer enhanced grid visibility, predictive maintenance capabilities, and improved operational efficiency, making them increasingly attractive alternatives to conventional infrastructure.

- Powell's Competitive Imperative: To maintain market relevance, Powell needs to integrate advanced digital and modular functionalities into its product lines, ensuring it can meet the evolving demands of utility clients seeking to modernize their grid infrastructure.

- Investment in R&D: Significant investment in research and development is crucial for Powell to develop competitive modular and digital substation offerings, thereby mitigating the threat of substitution from technologically superior alternatives.

Energy Storage Solutions

The threat of substitutes for traditional electrical distribution components is growing due to rapid advancements in energy storage solutions. Large-scale batteries and other grid-scale storage technologies are emerging as viable alternatives for industrial facilities looking to manage their power more efficiently, particularly during peak demand periods.

These innovative systems are designed to optimize energy usage and enhance grid stability, fundamentally changing how power is distributed and consumed. For instance, in 2024, the global energy storage market saw significant investment, with projections indicating continued robust growth as companies seek to reduce reliance on conventional grid services.

- Battery Storage Deployment: The increasing deployment of battery storage systems, such as those from Tesla's Megapack or Fluence Energy, allows industrial sites to store excess renewable energy and discharge it during high-cost peak hours, bypassing traditional utility infrastructure.

- Grid Modernization Initiatives: Government and utility-led grid modernization efforts, including smart grid technologies and demand response programs, further encourage the adoption of storage, potentially diminishing the need for certain distribution upgrades.

- Cost Reductions: Declining costs in battery technology, with lithium-ion battery pack prices falling significantly over the past decade, make these storage solutions increasingly cost-competitive against traditional electrical infrastructure investments.

- Decentralized Energy: The rise of decentralized energy resources and microgrids, enabled by storage, offers industrial users greater control and resilience, presenting a direct substitute for centralized power supply and distribution.

Shifting Power: Substitutes Challenge Grid Dominance

The threat of substitutes arises when alternative products or services can fulfill the same customer needs, potentially drawing business away from Powell. For instance, advancements in distributed energy generation, like widespread solar adoption, reduce reliance on traditional grid infrastructure. By the end of 2024, over 4 million US homes are expected to have solar installations, with a 15% annual growth rate, directly impacting demand for centralized power solutions.

Furthermore, sophisticated energy management software and analytics platforms offer efficiency gains that can substitute for physical hardware upgrades. The global smart grid market, projected to exceed $100 billion by early 2024, highlights a strong customer preference for digitally optimized energy systems over purely hardware-centric approaches.

The growing market for energy storage solutions also poses a substitution threat. Declining battery costs, with lithium-ion pack prices dropping significantly, make storage increasingly competitive against traditional grid investments. This trend allows industrial clients to manage peak demand and reduce reliance on conventional power distribution.

Entrants Threaten

High Capital Investment Requirements

The custom-engineered electrical equipment and systems sector for heavy industries presents a formidable threat of new entrants due to its exceptionally high capital investment requirements. Establishing state-of-the-art manufacturing facilities, acquiring specialized machinery, and implementing advanced testing equipment necessitates hundreds of millions of dollars, if not billions, in upfront funding. For instance, a new entrant might need to invest upwards of $500 million to establish a competitive production line capable of meeting the stringent quality and customization demands of heavy industries. This substantial financial barrier significantly deters potential new players from entering the market.

Need for Specialized Expertise and R&D

The creation, production, and upkeep of intricate electrical energy management systems demand highly specialized engineering knowledge, substantial investment in research and development, and a thorough grasp of industry regulations. Building or obtaining this skilled talent pool and technological capability presents a formidable obstacle for any new entrants aiming to compete in this sector.

For instance, companies like Schneider Electric and Siemens invest billions annually in R&D to stay at the forefront of energy management technology. In 2023, Schneider Electric reported R&D expenses of €1.4 billion, highlighting the significant financial commitment required to maintain a competitive edge and develop innovative solutions that meet evolving market demands and stringent safety standards.

Established Customer Relationships and Reputation

Powell Industries, with over 70 years in the business, has cultivated deep-seated, long-term relationships with key clients in demanding heavy industries. This extensive history has allowed them to build a robust reputation for dependability and safety, crucial for delivering essential infrastructure solutions. Newcomers face a significant hurdle in replicating this established trust and market acceptance, particularly in sectors where system failures carry substantial risks.

Regulatory Hurdles and Compliance

The heavy industries Powell Porter operates in, like oil and gas and power generation, are choked with complex regulations and safety requirements. New companies wanting to enter must endure lengthy and expensive certification processes, facing a mountain of industry-specific rules. This significant regulatory burden makes it incredibly difficult and costly for new players to gain a foothold.

For instance, in 2024, the average time to obtain environmental permits for new energy infrastructure projects in the United States often exceeded two years, with compliance costs frequently running into millions of dollars. These extensive requirements, encompassing everything from emissions standards to operational safety protocols, create a substantial barrier to entry.

- Cost of Compliance: New entrants must invest heavily in meeting stringent environmental and safety standards, which can be prohibitive.

- Certification Delays: Navigating complex approval processes can add years to a project timeline, delaying revenue generation.

- Ongoing Regulatory Scrutiny: Even after entry, continuous adherence to evolving regulations demands significant resources.

- Industry-Specific Standards: Unique rules for sectors like aerospace or pharmaceuticals require specialized knowledge and infrastructure.

Economies of Scale and Experience Curve

Established players in industries like heavy machinery or automotive manufacturing, much like a hypothetical firm named Powell, often possess significant advantages due to economies of scale. This means they can produce goods at a much lower cost per unit because they buy raw materials in bulk, optimize their factory operations, and have efficient distribution networks. For instance, in 2024, major automakers were reported to achieve manufacturing cost reductions of up to 15% through sheer volume alone compared to smaller, niche producers.

Newcomers attempting to enter such markets would likely face a considerable cost disadvantage. They would need to invest heavily to build comparable production capacity and achieve similar purchasing power, which is a substantial barrier. Without this scale, their per-unit costs would be higher, making it difficult to compete on price with established companies.

Beyond scale, the experience curve plays a critical role. Decades of operation allow established firms to refine their processes, improve quality, and reduce waste through accumulated knowledge. For example, a company with 50 years of experience in complex engineering projects might have developed proprietary techniques that shave off 20% of production time and cost compared to a firm with only a few years of experience. This deep operational efficiency is not easily or quickly replicated by new entrants.

- Economies of Scale: Reduced per-unit costs through large-scale production, bulk purchasing, and optimized logistics.

- Experience Curve: Improved operational efficiencies and cost reductions derived from accumulated knowledge and refined processes over time.

- Cost Disadvantage for New Entrants: Higher initial per-unit costs due to lack of scale and established operational expertise.

Electrical Equipment: A Fortress Against New Competitors

The threat of new entrants in the custom-engineered electrical equipment sector is significantly mitigated by substantial capital requirements, specialized knowledge, established customer relationships, and stringent regulatory landscapes. These combined barriers make it exceptionally difficult and costly for new players to enter and compete effectively.

New entrants face a steep uphill battle due to the immense upfront investment required for specialized manufacturing and R&D, often running into hundreds of millions of dollars. For instance, establishing a competitive production line in 2024 could easily exceed $500 million. Furthermore, the need for deep engineering expertise and navigating complex regulations, which can take years and millions in compliance costs as seen with energy infrastructure permits averaging over two years in 2024, acts as a powerful deterrent.

The sector also benefits from established players' economies of scale and experience curves, granting them cost advantages of up to 15% in manufacturing due to volume alone in 2024. Replicating decades of trust and operational efficiency, like Powell Industries' 70 years of experience, is nearly impossible for newcomers.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a robust foundation of publicly available data, including company annual reports, industry-specific trade publications, and government economic indicators.