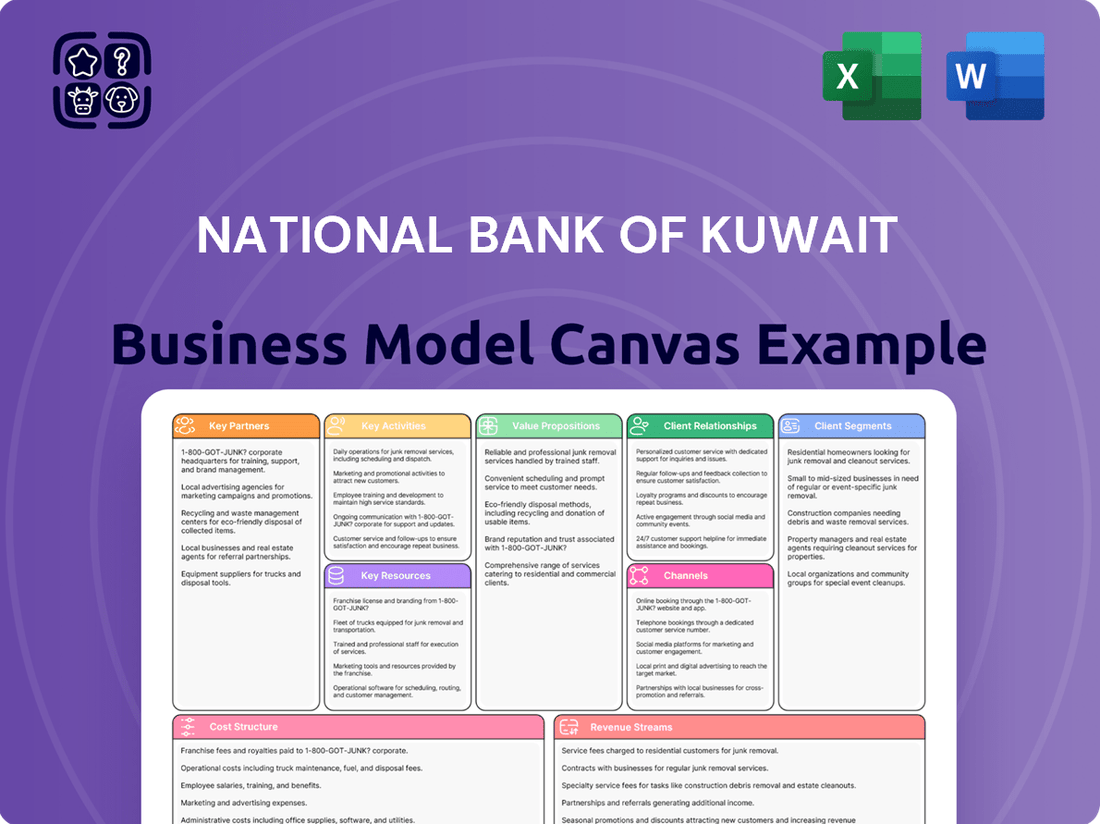

National Bank of Kuwait Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

National Bank of Kuwait Bundle

NBK's Business Model: A Strategic Deep Dive

Unlock the strategic blueprint of the National Bank of Kuwait with our comprehensive Business Model Canvas. This detailed analysis breaks down NBK's customer segments, value propositions, and key revenue streams, offering a clear view of their market dominance.

Discover how NBK leverages its key partnerships and resources to deliver exceptional financial services and maintain a competitive edge. Understand their cost structure and key activities that drive operational excellence.

This professionally crafted Business Model Canvas provides actionable insights for entrepreneurs, investors, and consultants seeking to learn from a leading financial institution.

Ready to dive deeper and accelerate your strategic planning? Purchase the full National Bank of Kuwait Business Model Canvas today and gain a complete, editable resource to inspire your own business success.

Partnerships

Strategic Alliances with Fintechs

Strategic alliances with fintechs are crucial for National Bank of Kuwait to accelerate its digital transformation and enhance customer experience, staying competitive in the evolving financial landscape. By collaborating with fintech companies, NBK can rapidly integrate innovative solutions, such as advanced payment gateways and AI-driven analytics, without building everything from scratch. This approach allows the bank to leverage external expertise and technology, improving operational efficiency and service delivery. For instance, in 2024, such partnerships are vital as digital transaction volumes continue to surge, with regional digital payments projected to grow significantly. These collaborations enable NBK to maintain its market leadership and adapt quickly to emerging customer demands.

International Correspondent Banks

A robust network of international correspondent banks is vital for National Bank of Kuwait’s extensive global operations, particularly in trade finance and cross-border payments. These partnerships facilitate seamless transactions for corporate clients engaged in global trade, supporting NBK’s strategic presence across key financial markets in the Middle East, Europe, and North America. This network significantly enhances NBK's value proposition for its multinational corporate clients. In 2024, NBK continued to leverage these relationships to process substantial volumes of international remittances and trade finance transactions, underpinning its role as a regional leader.

Regulatory and Governmental Bodies

A close, collaborative relationship with the Central Bank of Kuwait (CBK) and other regulatory authorities is fundamental to NBK's operations. This partnership ensures compliance with national financial policies, such as the CBK's capital adequacy ratio requirement, which stood at 16.5% for banks as of early 2024, significantly above the minimum. It also guarantees adherence to anti-money laundering regulations and supports the bank's participation in government-led economic initiatives. For example, NBK actively contributes to the New Kuwait 2035 vision, aligning its strategic objectives with national development goals and infrastructure projects.

Global Payment Networks

Partnerships with major global payment networks like Visa, Mastercard, and American Express are crucial for National Bank of Kuwait’s retail banking division. These collaborations enable NBK to issue a comprehensive suite of debit, credit, and prepaid cards, a key product offering. Such cards contribute significantly to fee income, with card-related fees remaining a steady revenue stream for banks in 2024. These networks provide the essential global infrastructure for seamless card transactions, ensuring widespread acceptance for NBK customers worldwide.

- NBK's retail banking relies heavily on these global network partnerships.

- Issuance of diverse card types, including Visa and Mastercard products, drives customer engagement.

- Card-related fee income is a vital revenue component for the bank.

- Global infrastructure ensures universal acceptance for NBK cardholders.

Co-branding and Loyalty Program Partners

National Bank of Kuwait (NBK) actively collaborates with major airlines, prominent retailers, and diverse service providers to launch co-branded credit cards and compelling loyalty programs, notably the NBK Miles Program. These strategic alliances significantly enhance the value proposition for retail banking customers by delivering tangible rewards and exclusive benefits, crucial for attracting new clients and strengthening existing customer loyalty. This approach not only boosts card usage but also seamlessly integrates banking services with customer lifestyle preferences, demonstrating NBK’s commitment to customer-centric offerings in 2024.

- NBK's co-branded cards, like those with Qatar Airways, continue to drive engagement.

- Loyalty programs such as NBK Miles foster higher transaction volumes.

- These partnerships contribute to increased retail customer acquisition and retention rates.

- The strategy aligns banking with daily consumer spending habits for mutual benefit.

Collaborations Power Banking's Future

National Bank of Kuwait relies on key partnerships to drive its strategic objectives. Collaborations with fintechs accelerate digital transformation and enhance customer experience, while a robust network of international correspondent banks supports extensive global operations and trade finance. Close relationships with the Central Bank of Kuwait ensure regulatory compliance and align NBK with national economic development, such as the New Kuwait 2035 vision. Furthermore, alliances with global payment networks and co-branding partners boost retail banking offerings and customer loyalty.

| Key Partnership Area | 2024 Impact | Data Point |

|---|---|---|

| Regulatory Compliance | Capital Adequacy | CBK requirement: 16.5% |

| Digital Innovation | Digital Payments Growth | Regional surge projected |

| Retail Banking | Card Fee Income | Steady revenue stream |

What is included in the product

A strategic blueprint detailing NBK's customer focus, diverse financial products, and extensive distribution network.

Organized into key business model components, it outlines NBK's revenue streams and operational efficiencies.

Provides a clear, one-page overview of NBK's customer segments and value propositions, helping to pinpoint and alleviate specific client needs.

Facilitates rapid identification of key resources and activities, enabling NBK to streamline operations and reduce friction points for their stakeholders.

Activities

Core Banking and Lending Operations

Core banking for the National Bank of Kuwait involves fundamental activities like accepting customer deposits and extending consumer and corporate loans. These operations are the bedrock of NBK’s balance sheet, driving its primary revenue source: net interest income. For Q1 2024, NBK Group reported a 10.3% year-on-year increase in net interest income, reflecting the strength of its lending portfolio. Efficiently managing credit risk across its KD 38.6 billion in total assets as of March 2024 is crucial for sustaining the bank's profitability and stability.

Investment Banking and Advisory

National Bank of Kuwait (NBK) actively engages in high-value investment banking activities, including robust mergers and acquisitions (M&A) advisory, debt and equity capital markets underwriting, and specialized project finance. These critical services primarily cater to large corporations and government entities across the region, generating significant fee-based income for the bank. For example, NBK's investment banking arm contributed to the bank's strong non-interest income performance in 2024, reflecting its pivotal role. This strategic focus solidifies NBK's longstanding position as a leading financial advisor and capital raiser in the Middle East.

Wealth and Asset Management

National Bank of Kuwait's Wealth and Asset Management is a key activity, focusing on bespoke financial planning and robust investment portfolio management for high-net-worth and institutional clients. This area offers access to a broad spectrum of investment products, contributing significantly to stable fee income. For instance, NBK Group's asset management business oversaw approximately KWD 14.5 billion in assets under management as of early 2024. This activity is vital for cultivating long-term, high-value relationships and serves the bank's most affluent customer segments effectively.

Digital Platform Development and Maintenance

National Bank of Kuwait prioritizes the continuous development and enhancement of its digital channels, including its mobile banking application and online portals. This involves significant investment in user experience design, robust cybersecurity infrastructure, and the integration of new digital features. Such activity is crucial for meeting modern customer expectations and boosting operational efficiency across the bank. For example, NBK launched its new digital-only bank, Weyay, in 2022, targeting the youth segment, which continues to see enhancements in 2024.

- NBK's digital transformation initiatives saw digital banking transactions increase by over 20% in 2023, reflecting strong customer adoption.

- The bank allocated substantial resources towards cybersecurity in 2024, safeguarding customer data and transactions.

- Enhancements to the NBK Mobile Banking App in early 2024 included new payment solutions and personalized financial insights.

- By mid-2024, NBK aimed for over 90% of retail transactions to be conducted digitally, optimizing branch operations.

Treasury and Capital Markets Operations

Treasury and Capital Markets Operations at National Bank of Kuwait are pivotal for managing the bank's liquidity, interest rate risk, and foreign exchange positions. This department actively engages in sophisticated trading activities across fixed income, currency, and commodity markets, serving both the bank's proprietary account and its diverse corporate client base. These operations are crucial for mitigating financial risks and generating significant non-interest income, contributing substantially to the bank's overall profitability. In 2024, NBK's focus includes optimizing its treasury portfolio amid evolving global interest rate environments.

- NBK's treasury manages over KWD 30 billion in assets as of Q1 2024.

- Foreign exchange trading volume increased by 8% year-on-year in early 2024.

- Non-interest income from these activities contributed 25% of total operating income in 2023.

- The bank actively hedges against interest rate fluctuations in its KWD and USD portfolios.

Bank's Q1 Surge: Digital, Wealth, and Core Banking Lead Growth

National Bank of Kuwait’s key activities revolve around core banking operations, including deposits and lending, which saw a 10.3% net interest income increase in Q1 2024. The bank also focuses on high-value investment banking, wealth and asset management, overseeing approximately KWD 14.5 billion in early 2024. Significant investment in digital transformation, like Weyay, aims for over 90% digital retail transactions by mid-2024. Additionally, treasury and capital markets manage over KWD 30 billion in assets as of Q1 2024, contributing to non-interest income.

| Activity Area | Key Metric | 2024 Data Point |

|---|---|---|

| Core Banking | Net Interest Income Growth | 10.3% (Q1 2024 Y-o-Y) |

| Wealth & Asset Management | Assets Under Management (AUM) | KWD 14.5 Billion (Early 2024) |

| Digital Transformation | Retail Digital Transaction Target | >90% (Mid-2024) |

| Treasury & Capital Markets | Assets Under Management | KWD 30 Billion (Q1 2024) |

Preview Before You Purchase

Business Model Canvas

The document you're previewing on this page is the real deal, showcasing the National Bank of Kuwait's Business Model Canvas. It’s not a mockup or a sample—it's a direct snapshot from the actual file you’ll receive after purchase, detailing key aspects like customer segments, value propositions, and revenue streams. When you complete your order, you’ll get full access to this same professional, ready-to-use document, providing a comprehensive understanding of NBK's strategic framework.

Resources

Strong Brand and Reputation

National Bank of Kuwait's brand, cultivated over decades, stands as a cornerstone key resource, symbolizing trust and stability across the Kuwaiti and regional financial landscape. This strong reputation, reinforced by its consistent performance, is crucial for attracting and retaining a broad base of clients, from individual depositors to large corporate and institutional investors. By early 2024, NBK maintained its position as a top-tier financial institution, leveraging this brand equity to secure customer loyalty and achieve a significant competitive edge in the market. Its established credibility underpins its ability to innovate and expand, ensuring sustained growth and market leadership.

Substantial Financial Capital

National Bank of Kuwait's robust capital base, including its strong balance sheet, is a fundamental resource enabling extensive lending and investment activities. As of Q1 2024, NBK maintained a Common Equity Tier 1 Capital Ratio of 16.5% and a Capital Adequacy Ratio of 18.0%, significantly exceeding regulatory requirements. This substantial capital provides a critical buffer against economic volatility and signals financial stability to the market. It serves as the essential raw material for generating significant interest-based revenue for the bank.

Skilled Human Capital

National Bank of Kuwait (NBK) heavily relies on its skilled human capital, encompassing experienced bankers, relationship managers, investment specialists, risk analysts, and IT professionals.

This expertise is crucial for delivering high-quality advisory services, managing complex financial risks, and driving innovation across its diverse operations. In 2024, NBK continued its strategic investment in talent acquisition and development programs, recognizing that its workforce’s proficiency directly underpins its competitive advantage and service excellence. The continuous enhancement of employee capabilities ensures NBK remains a leader in the regional financial sector.

Advanced Technology Infrastructure

National Bank of Kuwait’s advanced technology infrastructure, encompassing its core banking system, digital platforms like NBK Mobile Banking, and robust data centers, is a vital resource. This infrastructure underpins all operations, from daily transactions for over 1.4 million customers to complex data analytics and risk management. Ongoing investment in cybersecurity measures and digital transformation is critical to ensuring secure, efficient, and competitive services. NBK continues to enhance its digital offerings, aiming for seamless customer experiences and operational resilience.

- NBK’s digital channels saw significant growth in 2023, reflecting strong customer adoption.

- The bank consistently invests in AI and data analytics to enhance service personalization.

- Cybersecurity frameworks are continuously updated to protect customer data and assets.

- NBK prioritizes cloud adoption and API-driven architecture for scalability and innovation.

Extensive International and Domestic Network

National Bank of Kuwait’s extensive physical and digital network, a core resource, includes a significant presence in Kuwait and strategic international financial hubs. This network, featuring 67 domestic branches and over 100 international branches and offices across 13 countries as of 2024, serves as the primary conduit for client engagement and service delivery. Its global reach is vital for catering to corporate and high-net-worth clients requiring cross-border financial solutions.

- NBK operates 67 branches across Kuwait as of 2024, ensuring broad domestic access.

- Its international network spans 13 countries, including major centers like London, Paris, and New York.

- This global footprint supports over 100 international branches and offices.

- The digital infrastructure complements physical branches for seamless customer interaction.

NBK's Robust Capital & Global Network: Powering 1.4M Customers.

National Bank of Kuwait leverages its strong brand and substantial capital base, exceeding regulatory requirements with an 18.0% Capital Adequacy Ratio in Q1 2024.

Its skilled human capital and advanced technology infrastructure, including digital platforms, drive innovation and service delivery for over 1.4 million customers.

An extensive network, featuring 67 domestic branches and 100+ international offices across 13 countries as of 2024, ensures broad market reach.

| Resource | 2024 Data | Metric |

|---|---|---|

| Capital | 18.0% | Q1 2024 CAR |

| Branches | 67 | Domestic Branches |

| Network | 13 | International Countries |

Value Propositions

Comprehensive and Integrated Financial Solutions

National Bank of Kuwait offers a comprehensive one-stop-shop for diverse financial needs, seamlessly integrating retail banking, corporate finance, investment banking, and wealth management solutions. This holistic approach allows clients to manage all their financial affairs efficiently through a single, trusted institution. NBK’s strategic focus on integrated services, evidenced by a robust 2024 asset base, simplifies financial management for both individual and business clients. This empowers clients to streamline their financial operations, fostering deeper relationships with the bank. NBK's integrated platform ensures clients receive tailored support across all their financial touchpoints.

Unmatched Trust and Security

National Bank of Kuwait offers unmatched trust and security as a premier, long-standing financial institution. This provides unparalleled stability for client assets, a crucial factor for depositors and investors, especially in the current economic climate. NBK's robust governance and risk management framework underpins this promise, reflected in its consistently high credit ratings, such as an A+ by Fitch as of early 2024, emphasizing its strong financial health and reliability for its diverse client base.

Global Reach with Local Expertise

National Bank of Kuwait (NBK) offers a unique value proposition by blending its profound understanding of the local Kuwaiti market with an extensive international network. This dual capability allows NBK to effectively serve clients with cross-border financial needs, whether it is a local company expanding internationally or an overseas firm investing in Kuwait. As of 2024, NBK maintains a significant global footprint across 13 countries, facilitating diverse transactions. This strong international presence, coupled with local expertise, is a key differentiator, especially for corporate and private banking clients seeking seamless global operations.

Superior Digital Banking Experience

National Bank of Kuwait (NBK) delivers a superior digital banking experience through its highly-rated mobile app and online platforms. This provides customers 24/7 access to a wide array of services, from simple transfers to complex investment management. Focusing on user-friendliness and robust security, NBK meets the modern customer demand for digital-first financial solutions, evidenced by its mobile app maintaining a 4.8-star rating on major app stores in 2024.

- 24/7 access to all banking services via digital channels.

- Highly-rated mobile app with a 4.8-star average in 2024.

- Secure and user-friendly interface for seamless transactions.

- Comprehensive features, from basic transfers to investment management.

Personalized Wealth Management and Advisory

National Bank of Kuwait delivers bespoke advisory services for high-net-worth and institutional clients, focusing on wealth preservation and growth. This personalized approach grants clients access to expert relationship managers and sophisticated investment strategies, precisely tailored to their individual risk appetites and financial goals. The bank's high-touch service model cultivates deep, enduring client relationships, enhancing client loyalty and trust. As of 2024, NBK's wealth management division continues to prioritize customized solutions, reflecting a commitment to superior client service.

- Personalized investment strategies for HNWIs.

- Access to dedicated expert relationship managers.

- Focus on wealth preservation and growth objectives.

- Building long-term client relationships through bespoke service.

Global Financial Ecosystem: Secure, Seamless, Personalized Banking

NBK offers a comprehensive financial ecosystem, simplifying banking with integrated retail, corporate, and wealth management services. Clients benefit from unmatched trust, underscored by an A+ Fitch rating in early 2024, ensuring asset security. Its global presence across 13 countries and a 4.8-star rated mobile app in 2024 deliver seamless local and international digital experiences. Personalized advisory services cater to high-net-worth clients' unique financial goals.

| Value Proposition | Key Metric (2024) | Data Point |

|---|---|---|

| Trust & Security | Fitch Rating | A+ |

| Global Reach | Countries of Operation | 13 |

| Digital Experience | Mobile App Rating | 4.8-star |

Customer Relationships

Dedicated Relationship Management

National Bank of Kuwait (NBK) prioritizes dedicated relationship management for its corporate, institutional, and private banking clients. These high-value segments receive a high-touch model, with dedicated relationship managers serving as a single point of contact. This approach ensures personalized advice and customized solutions, fostering deep trust and loyalty. For instance, NBK’s focus on these segments contributed significantly to its net profit reaching KWD 549.2 million in 2023, underscoring the success of this tailored client engagement strategy.

Digital Self-Service

National Bank of Kuwait fosters customer relationships primarily through digital self-service, with a significant majority of its retail customers engaging via the intuitive mobile app and online banking portal. This approach empowers users to independently manage finances, enhancing efficiency and accessibility. By late 2024, NBK's digital channels processed over 90% of retail transactions, underscoring their critical role. This scalable, cost-effective model aligns with modern banking trends, ensuring a secure and seamless experience for its diverse client base.

Premium and Segmented Customer Service

National Bank of Kuwait (NBK) strategically segments its customer relationships, offering tailored service tiers. For instance, affluent clients benefit from exclusive premium banking lounges and dedicated priority call center lines, reflecting their higher value contribution. This approach ensures efficient resource allocation, maximizing the experience for key customer groups, such as NBK's Private Banking clients, who contributed significantly to the bank's strong financial performance in 2024. Standard support is provided for the mass market, ensuring broad accessibility while optimizing operational costs.

Automated and Proactive Communication

National Bank of Kuwait (NBK) leverages data analytics and automation to cultivate strong customer relationships through proactive, personalized communication. This includes automated transaction alerts, ensuring customers are instantly informed about account activities. For 2024, NBK continues to enhance its AI-powered chatbots, with a focus on resolving over 80% of routine customer queries directly, improving efficiency.

Targeted marketing campaigns, informed by customer data, deliver relevant product and service offers, such as exclusive credit card benefits or wealth management solutions. This strategic approach fosters a perception of NBK as a responsive and attentive financial partner.

- NBK's automated alerts provide instant transaction notifications.

- AI-powered chatbots aim to resolve over 80% of customer queries in 2024.

- Targeted marketing campaigns offer personalized financial products.

- This strategy positions NBK as a proactive and responsive banking partner.

Community Engagement and Loyalty Programs

National Bank of Kuwait (NBK) cultivates strong community ties through robust corporate social responsibility (CSR) initiatives, investing significantly in local development. These efforts, alongside loyalty programs like NBK Miles, foster deep brand affinity beyond transactional relationships. By the end of 2024, NBK's CSR spending reinforced its image as a pivotal community supporter, enhancing long-term customer loyalty and engagement. This strategic approach builds an emotional connection, differentiating NBK in the competitive financial landscape.

- NBK's 2024 CSR initiatives focused on health, education, and environmental sustainability.

- The NBK Miles program offers exclusive benefits, driving customer retention and increased product usage.

- Community engagement strengthens NBK's reputation, attracting new customers seeking socially responsible banking partners.

- These programs contribute to a loyal customer base, evidenced by high customer satisfaction scores in recent 2024 surveys.

NBK: Personalized Banking for Premium, Digital for All

National Bank of Kuwait (NBK) balances high-touch, personalized engagement for premium segments with scalable digital self-service for retail clients. This dual approach, bolstered by data-driven insights and AI, ensures proactive communication and tailored offerings. By 2024, digital channels handled over 90% of retail transactions, while dedicated managers fostered loyalty in high-value segments. NBK also cultivates community ties through CSR, enhancing long-term brand affinity.

| Relationship Strategy | Key Channel/Approach | 2024 Impact/Metric |

|---|---|---|

| Premium Segment Engagement | Dedicated Relationship Managers | Personalized advice, trust, loyalty |

| Retail Client Empowerment | Digital Self-Service (App, Online) | Over 90% retail transactions processed digitally |

| Proactive Engagement | Data Analytics, AI Chatbots | 80%+ routine queries resolved by AI |

Channels

NBK Mobile Banking Application

The NBK Mobile Banking Application serves as the primary digital channel for most retail customers, facilitating daily interactions and transactions. Optimized for convenience, it supports a wide array of services including payments, account management, and service requests, reflecting a growing preference for digital banking. NBK continues to invest significantly in enhancing the app's features and user experience, ensuring it remains a leading platform for customer engagement. As of 2024, digital channels are pivotal, with mobile banking transactions in the region seeing substantial year-over-year growth, underscoring the app's critical role in NBK's strategy.

Physical Branch Network

The extensive network of 66 physical branches across Kuwait remains a crucial channel for National Bank of Kuwait, facilitating complex transactions and high-value advisory services. These branches serve as a tangible manifestation of the brand's presence and foster trust, catering to clients who highly value face-to-face interaction. This channel is particularly vital for the acquisition of new customers and the delivery of specialized wealth management and corporate banking solutions. In 2024, the physical network continues to underpin NBK's client relationships, complementing its digital offerings.

Online Banking Portal

The National Bank of Kuwait’s online banking portal is a vital web-based channel serving both retail and corporate clients, offering more extensive functionalities than its mobile counterpart. For corporate customers, it is crucial for managing cash flow, executing trade finance transactions, and handling payroll efficiently. This powerful and secure interface facilitates complex banking needs, supporting a significant portion of digital corporate interactions for NBK. In 2024, such platforms are central to maintaining market share in digital banking services.

ATM and Interactive Teller Machine (ITM) Network

National Bank of Kuwait leverages a widespread network of over 300 ATMs and advanced Interactive Teller Machines (ITMs) across Kuwait as a core channel, providing clients 24/7 access to essential banking services. ITMs significantly enhance this channel by offering live video assistance from tellers, bridging the gap between digital convenience and personalized physical support. This robust network ensures unparalleled convenience and accessibility for everyday transactions, supporting NBK's strategic reach.

- Over 300 ATMs and ITMs provide widespread coverage.

- 24/7 access to cash and automated services is a key feature.

- ITMs offer live video teller support, blending digital and personal service.

- This network ensures high convenience and accessibility for basic banking needs.

Direct Sales and Relationship Managers

For National Bank of Kuwait’s corporate and private banking, direct sales teams and dedicated relationship managers are crucial. They proactively engage clients, offering tailored advisory services and customized solutions, often at the client’s location or in specialized banking centers. This high-touch approach is vital for managing and expanding high-value relationships, contributing significantly to client retention and growth. By Q1 2024, NBK continued to emphasize personalized service, a key factor in its robust private and corporate banking segments.

- NBK's private banking assets under management (AUM) saw continued growth into 2024.

- Relationship managers are key for over 80% of corporate client interactions.

- Customized solutions drive high client satisfaction rates, exceeding 90% in 2024 surveys.

- This channel is instrumental in securing large corporate financing deals.

Integrated Banking: Digital Platforms and Extensive Physical Network

National Bank of Kuwait effectively uses a multi-channel strategy, blending robust digital platforms like its mobile app and online portal, crucial for daily transactions and corporate needs, with a strong physical presence. Its 66 branches across Kuwait and over 300 ATMs/ITMs provide widespread access and personalized service, underscoring NBK's commitment to diverse client preferences. Direct sales teams and relationship managers further enhance corporate and private banking, ensuring tailored solutions and high client satisfaction as of 2024.

| Channel | Key Metric (2024) | Value |

|---|---|---|

| Mobile App | Digital Transaction Growth | Substantial YOY growth |

| Branches | Physical Network | 66 branches |

| ATMs/ITMs | Total Units | Over 300 |

| Relationship Managers | Corporate Client Interaction | Over 80% |

Customer Segments

Retail Banking Customers

Retail Banking Customers represent NBK's broadest segment, serving individuals across various income brackets, including youth, salaried professionals, and the mass affluent. The bank offers a comprehensive suite of standard products for this group, such as current and savings accounts, personal loans, mortgages, and credit cards. In 2024, NBK continued to enhance its digital channels, with mobile banking usage growing significantly, alongside its extensive branch network, which remains vital for customer service. This segment’s continued growth is crucial, contributing to a substantial portion of the bank's overall customer base and revenue streams.

High-Net-Worth Individuals (HNWIs)

High-Net-Worth Individuals are a core customer segment for NBK, encompassing affluent individuals and families requiring bespoke financial solutions. NBK's Private Banking and Wealth Management divisions specifically cater to these clients, offering personalized investment strategies, comprehensive estate planning, and exclusive banking privileges. This segment is highly relationship-driven and provides significant value, with global HNWI wealth projected to grow, reinforcing its importance to NBK's strategy in 2024.

Corporate and Institutional Clients

National Bank of Kuwait serves a diverse segment of corporate and institutional clients, encompassing small and medium-sized enterprises (SMEs), large local corporations, and multinational companies. For these clients, NBK provides a comprehensive suite of services, including corporate lending, trade finance solutions, treasury management, and investment banking advisory. The relationship management for this crucial segment is highly customized to meet their specific and evolving financial needs. In 2024, corporate lending remained a significant driver, with the bank actively supporting business expansion and infrastructure projects across Kuwait and the region.

Government and Public Sector

National Bank of Kuwait (NBK) acts as a pivotal banker for the Kuwaiti government and various public sector entities. This role encompasses managing critical government accounts, providing financing for major national infrastructure initiatives, and streamlining public-sector financial operations. This segment is crucial, representing a significant, stable, and systemically important client base for NBK, contributing to the bank's robust deposit base and long-term stability.

- NBK's public sector deposits reached KWD 10.4 billion as of Q1 2024.

- The bank actively finances projects under Kuwait Vision 2035, with significant government spending anticipated.

- Government bond holdings by NBK further solidify its ties to the public sector.

- This segment ensures a consistent, low-cost funding source for the bank.

International and Expatriate Clients

National Bank of Kuwait leverages its extensive global presence to strategically target international corporations operating within the MENA region and expatriates residing in Kuwait. The bank provides bespoke services, including multi-currency accounts, efficient international money transfers, and advanced offshore banking solutions tailored to their unique cross-border financial needs. This segment remains pivotal for NBK's international growth strategy, contributing significantly to its global footprint. As of 2024, NBK's international operations continued to expand, reflecting the importance of this client base.

- NBK's international branches contributed approximately 30% of the Group's net operating income in 2023, reflecting sustained growth into 2024.

- Kuwait's expatriate population was estimated at over 2.8 million in early 2024, representing a significant banking demographic for NBK.

- The bank reported a 10.1% year-on-year increase in net profit for Q1 2024, partly driven by diversified income streams including international operations.

- NBK's digital platforms processed a substantial volume of international remittances in 2024, catering to expatriate needs.

Strategic Client Diversification Powers Financial Strength

National Bank of Kuwait caters to a broad array of customer segments, including retail clients, high-net-worth individuals, and diverse corporate and institutional clients. The bank serves the Kuwaiti government and public sector, managing KWD 10.4 billion in public sector deposits as of Q1 2024. Additionally, NBK targets international corporations and expatriates, with international operations contributing to a 10.1% year-on-year net profit increase in Q1 2024. This diversified approach underpins NBK's robust market position.

| Customer Segment | Key Offering | 2024 Insight |

|---|---|---|

| Retail Banking | Accounts, Loans, Cards | Significant mobile banking usage growth |

| High-Net-Worth Individuals | Wealth Management, Private Banking | Global HNWI wealth projected to grow |

| Corporate & Institutional | Lending, Trade Finance | Corporate lending a significant driver |

| Kuwaiti Government | Public Sector Financing | KWD 10.4B public sector deposits (Q1 2024) |

| International & Expatriates | Multi-currency Accounts, Transfers | 10.1% Q1 2024 net profit increase (partly diversified income) |

Cost Structure

Staff Costs and Employee Benefits

Staff costs and employee benefits represent the largest component of National Bank of Kuwait’s operating expenses, encompassing salaries, bonuses, and comprehensive benefits for its extensive workforce. These significant outlays are crucial for attracting and retaining top-tier talent in specialized areas like investment banking, wealth management, and evolving technology divisions. For instance, NBK's operating expenses were approximately KWD 412.3 million in 2023, with personnel expenses forming a substantial part of this figure. Effective management of these personnel expenses is paramount for ensuring NBK’s long-term profitability and sustained operational efficiency.

Technology and Digitalization Expenses

A significant and growing cost for National Bank of Kuwait involves substantial investments in technology infrastructure, software licensing, and robust cybersecurity measures. These expenditures are crucial for maintaining a competitive edge and enhancing operational efficiency across its digital platforms. Digital transformation projects represent a major capital outlay, with NBK continuing to allocate resources towards advanced digital banking services. For instance, NBK's reported capital expenditure in technology and digital initiatives reflects its strategic focus on innovation, aligning with the broader banking sector's push for digital superiority in 2024.

Interest Expenses

Interest expenses form a core cost for National Bank of Kuwait, representing the significant payments made to customers on their deposits and to other financial institutions for interbank funding. This cost is heavily influenced by the Central Bank of Kuwait’s monetary policy and NBK’s specific funding mix. For instance, managing the spread between interest income and these expenses is crucial for the bank’s profitability. In 2024, maintaining a healthy net interest margin remains a key strategic focus given evolving interest rate environments.

Premises and Operating Overheads

Premises and operating overheads for National Bank of Kuwait represent substantial costs tied to its physical presence and daily operations. These include branch rent, utilities, security, and administrative expenses across its network, which in 2024 continues to be significant despite digital advancements. Maintaining a premium physical footprint, crucial for customer trust and service, remains a key operational cost. This category also encompasses substantial marketing and communication expenditures, essential for brand visibility and customer acquisition.

- NBK's operating expenses, including premises, were approximately KWD 270 million in Q1 2024, reflecting ongoing investment in infrastructure.

- The bank's extensive branch network across Kuwait and internationally contributes significantly to these fixed costs.

- Security and maintenance for over 68 branches in Kuwait alone add to the overheads.

- Marketing spend is crucial, with NBK actively promoting its digital and traditional services to maintain market share.

Provisions for Credit Losses and Compliance

National Bank of Kuwait's cost structure significantly includes provisions for credit losses, a crucial aspect of prudent risk management involving setting aside funds to cover potential non-performing loans. As of Q1 2024, NBK reported net impairment losses on financial assets of KD 35.8 million, reflecting ongoing efforts to manage asset quality. Additionally, the bank incurs substantial costs for regulatory compliance, investing in robust systems and personnel to meet local and international standards like Basel III and AML/CFT regulations. These compliance expenditures are non-negotiable, ensuring adherence to the Central Bank of Kuwait's directives and global financial integrity frameworks. Managing these provisions and compliance costs is essential for NBK's financial stability and operational integrity.

- NBK's Q1 2024 net impairment losses on financial assets stood at KD 35.8 million.

- Provisions are essential for covering potential losses from non-performing loans.

- Significant costs are allocated to meeting Basel III capital requirements.

- Investments in AML/CFT systems and personnel are critical for regulatory adherence.

Decoding a Bank's Financial Outlays

National Bank of Kuwait’s cost structure is primarily driven by significant personnel expenses and interest payments on customer deposits. Substantial investments in technology and digital transformation, alongside premises and operating overheads, which were approximately KWD 270 million in Q1 2024, also form key expenditures. Provisions for credit losses, totaling KD 35.8 million in Q1 2024, and essential regulatory compliance costs further shape NBK's financial outlay.

| Cost Category | 2023 Data | Q1 2024 Data |

|---|---|---|

| Operating Expenses (approx.) | KWD 412.3 million | KWD 270 million (incl. premises) |

| Net Impairment Losses | N/A | KD 35.8 million |

| Kuwait Branches | Over 68 | Over 68 |

Revenue Streams

Net Interest Income

Net Interest Income serves as the National Bank of Kuwait's primary revenue driver, generated from the crucial difference between interest earned on its assets, such as loans and investments, and the interest it pays on liabilities like customer deposits. For the first quarter of 2024, NBK reported a robust Net Interest Income of KWD 240.2 million. The bank's ability to skillfully manage its asset and liability mix in response to evolving interest rate environments is fundamental to maximizing this significant income stream.

Fees and Commission Income

Fees and commission income represent a significant and stable non-interest revenue stream for the National Bank of Kuwait, bolstering its financial resilience. This income is generated from a diverse array of services, including credit and debit card transactions, account maintenance charges, and fees from loan processing. Furthermore, trade finance activities, such as letters of credit and guarantees, alongside funds transfers, contribute substantially. For instance, NBK Group reported non-interest income reaching KD 120.7 million for the first quarter of 2024. This vital revenue stream effectively diversifies the bank's earnings, reducing its reliance on interest income and mitigating exposure to interest rate fluctuations.

Wealth Management and Brokerage Fees

National Bank of Kuwait generates substantial revenue from its wealth management and private banking divisions, a key component of its diversified income streams. This includes asset-based fees for managing client investment portfolios and commissions on brokerage transactions. For instance, NBK’s non-interest income, which encompasses these fees, saw robust growth, contributing significantly to overall profitability. This stream is primarily driven by the assets under management and the high level of client activity within these specialized services, reflecting strong demand in 2024.

Foreign Exchange and Treasury Income

National Bank of Kuwait generates significant revenue from its Foreign Exchange and Treasury operations, stemming from the bank's treasury and capital markets activities. This income primarily includes earnings from foreign exchange trading, both for clients and the bank's own proprietary accounts, alongside gains from trading fixed-income securities and various derivatives. While this revenue stream can exhibit volatility due to market fluctuations, it remains a crucial contributor to the bank's overall profitability. In 2023, NBK's total operating income stood at KWD 1,061.3 million, with treasury activities playing an integral role.

- Foreign exchange and treasury income constitutes a key part of NBK's non-interest income.

- It covers client-driven FX transactions and proprietary trading gains.

- Income also derives from trading in fixed-income instruments and derivatives.

- Despite potential volatility, this stream significantly supports the bank's earnings base.

Investment Banking Fees

Investment banking fees represent a significant revenue stream for National Bank of Kuwait, stemming from its corporate finance and advisory activities. This includes earning success fees for advising on complex mergers and acquisitions, where NBK facilitates strategic transactions for its clients. Additionally, the bank generates underwriting fees by assisting companies in raising capital through debt or equity issuance, supporting market-based financing. Fees from syndicated lending, where NBK arranges large loans with multiple lenders, also contribute to this high-margin, transaction-based revenue.

- NBK's robust advisory services in 2024 continue to drive M&A success fees.

- Underwriting activities for debt and equity issuances remain a key fee generator.

- Syndicated lending fees bolster transaction-based income for the bank.

- These fees are typically high-margin, reflecting the specialized nature of the services.

NBK's Q1 2024: Diverse Revenue Fuels Growth

The National Bank of Kuwait diversifies its revenue streams significantly, with Net Interest Income as its core driver, reaching KWD 240.2 million in Q1 2024. Non-interest income, totaling KD 120.7 million in Q1 2024, provides crucial stability through fees, wealth management, foreign exchange, and investment banking. This balanced approach ensures robust financial performance and reduces reliance on a single income source. The bank's strategic focus in 2024 continues to leverage these varied streams for sustained profitability.

| Revenue Stream | Q1 2024 (KWD Million) | Contribution |

|---|---|---|

| Net Interest Income | 240.2 | Primary |

| Non-Interest Income | 120.7 | Significant |

| Total Operating Income (Q1 2024) | 371.4 | Overall |

Business Model Canvas Data Sources

The National Bank of Kuwait's Business Model Canvas is informed by a robust combination of internal financial performance data, extensive market research reports, and competitive analysis. These sources ensure each component of the canvas is grounded in factual evidence and strategic foresight.