Heijmans Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Heijmans Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Heijmans's competitive landscape is shaped by several powerful forces, from the bargaining power of their buyers to the intensity of rivalry within the construction sector. Understanding these dynamics is crucial for strategic planning and identifying potential threats and opportunities. This brief snapshot only scratches the surface.

Unlock the full Porter's Five Forces Analysis to explore Heijmans’s competitive dynamics, market pressures, and strategic advantages in detail. Gain a comprehensive view of supplier power, the threat of new entrants, and the impact of substitute products on their business. Don't miss out on the actionable insights needed to navigate and thrive in their industry.

Suppliers Bargaining Power

Suppliers of Raw Materials and Commodities

Suppliers of essential raw materials like steel, cement, and timber generally hold moderate bargaining power. This power stems from the inherent volatility of global commodity prices and the fundamental need for these inputs in any construction endeavor. For instance, in 2024, steel prices experienced significant fluctuations, impacting project budgets across the sector.

While a large entity like Heijmans can use its considerable purchasing volume to negotiate better terms, persistent market volatility can still exert upward pressure on costs. The availability and pricing of these core materials represent critical cost drivers that directly influence profitability.

Specialized Subcontractors and Labor

Specialized subcontractors, especially those with unique skills in complex engineering or cutting-edge sustainable technologies, hold considerable sway. Their limited availability means they can command higher prices and dictate terms, directly impacting Heijmans' project costs and timelines. For example, in 2024, the demand for certified installers of advanced solar panel systems outstripped supply in many regions, leading to a reported 15% increase in installation costs for such projects.

The availability of skilled labor is another critical factor. A tight labor market, as experienced in many European construction sectors through 2024, can significantly drive up wages and make it challenging to secure the necessary workforce. This scarcity can lead to project delays and increased operational expenses for Heijmans if not managed proactively. Reports from industry associations in late 2024 indicated a 7% average increase in construction labor wages year-over-year due to these pressures.

To counter this supplier power, Heijmans must cultivate robust relationships with a diverse range of specialized subcontractors and labor pools. Diversifying sourcing not only provides leverage in negotiations but also ensures continuity of operations even when specific suppliers face capacity constraints or price hikes. Maintaining a strong network of pre-qualified vendors and investing in long-term partnerships are key strategies to mitigate these risks.

Technology and Equipment Providers

Technology and equipment providers hold significant bargaining power, particularly those offering proprietary advanced construction technologies, specialized software, or complex heavy machinery. For Heijmans, the high cost and intricate integration required for these solutions, coupled with the need for extensive staff training, create substantial switching costs, limiting flexibility.

This is particularly true for providers of cutting-edge sustainable building technologies, where innovation is rapid and specialized expertise is paramount. For instance, the adoption of Building Information Modeling (BIM) software, a common tool in modern construction, can involve significant upfront investment and ongoing licensing fees, giving software developers leverage. In 2024, the global construction technology market was projected to reach over $10 billion, highlighting the economic importance and influence of these suppliers.

Energy and Fuel Providers

Energy and fuel providers hold substantial bargaining power over construction firms like Heijmans. The construction sector is inherently energy-intensive, requiring significant fuel for heavy machinery and power for operational sites and administrative offices. In 2024, the volatility of global energy markets, influenced by geopolitical tensions and supply chain disruptions, directly translates into unpredictable operational costs for Heijmans. For instance, average Brent crude oil prices experienced significant fluctuations throughout 2024, impacting diesel fuel costs, a primary expense for construction equipment. Furthermore, the ongoing shift towards more sustainable energy solutions, while beneficial long-term, often necessitates higher upfront capital expenditures and can create dependence on a limited number of specialized providers for new technologies and infrastructure.

- Dependence on Fuel: Construction operations heavily rely on fossil fuels for machinery, making them vulnerable to price hikes.

- Price Volatility: Geopolitical events and supply constraints in 2024 led to significant fluctuations in energy prices, directly impacting Heijmans' cost of operations.

- Transition Costs: The move to sustainable energy sources may increase initial investment and reliance on niche suppliers.

Logistics and Transportation Services

The bargaining power of suppliers in the logistics and transportation sector significantly impacts Heijmans' operations. Efficient movement of materials and equipment to various project sites, often in challenging terrains, is paramount. Suppliers can leverage their position through factors like route availability, fluctuating fuel costs, and the specialized requirements for transporting oversized or hazardous goods.

The reliability and cost of logistics directly influence project timelines and overall expenses. For instance, in 2024, global shipping costs saw considerable volatility due to geopolitical events and capacity constraints, directly affecting companies like Heijmans. Specialized transport, such as for large construction machinery or specific building materials, often involves a limited number of providers, amplifying their bargaining leverage.

- Route Availability: Limited direct routes to remote or developing project sites can give logistics providers more power.

- Fuel Costs: Fluctuations in global fuel prices, a major component of transportation expenses, directly impact the cost of services. For example, Brent crude oil prices in early 2024 averaged around $83 per barrel, a key indicator for transportation costs.

- Specialized Transport: The need for specialized vehicles or handling for large, heavy, or hazardous materials narrows the supplier pool, increasing their influence.

- Supply Chain Disruptions: Events causing delays, such as port congestion or labor shortages, can lead to increased costs and project delays for Heijmans, highlighting supplier dependency.

Rising Supplier Power Impacts 2024 Construction Costs

Suppliers of critical and specialized materials, such as advanced insulation or unique facade systems, can exert significant bargaining power. This is amplified when these materials are patented, have limited alternatives, or are essential for meeting specific sustainability certifications that clients demand. The reliance on these suppliers for project differentiation and compliance means Heijmans has less leverage in price negotiations. In 2024, the demand for high-performance, low-carbon concrete formulations, for instance, saw a notable increase, giving specialized producers more pricing power.

The bargaining power of suppliers in the construction sector, including those providing raw materials, specialized components, and labor, presents a tangible challenge for companies like Heijmans. Fluctuations in commodity prices, the limited availability of skilled labor and specialized subcontractors, and the increasing demand for sustainable technologies all contribute to suppliers' ability to influence costs and terms. For example, in 2024, a shortage of skilled electricians specialized in smart building systems led to increased rates for these services, impacting project budgets.

| Supplier Type | Bargaining Power Factors | 2024 Impact Example |

|---|---|---|

| Raw Material Suppliers (Steel, Cement) | Global commodity price volatility, essential inputs | Steel prices saw significant fluctuations, impacting project budgets. |

| Specialized Subcontractors | Unique skills, limited availability, demand for new technologies | 15% increase in costs for certified solar panel installers due to supply/demand imbalance. |

| Labor Providers | Tight labor market, wage increases | 7% average increase in construction labor wages year-over-year. |

| Technology Providers (BIM Software) | Proprietary technology, high switching costs, integration complexity | Global construction tech market projected over $10 billion, indicating supplier influence. |

| Energy & Fuel Providers | Sector's energy intensity, price volatility | Brent crude oil price fluctuations directly impacted diesel costs. |

| Logistics & Transportation | Route availability, fuel costs, specialized transport needs | Global shipping cost volatility affected project timelines and expenses. |

What is included in the product

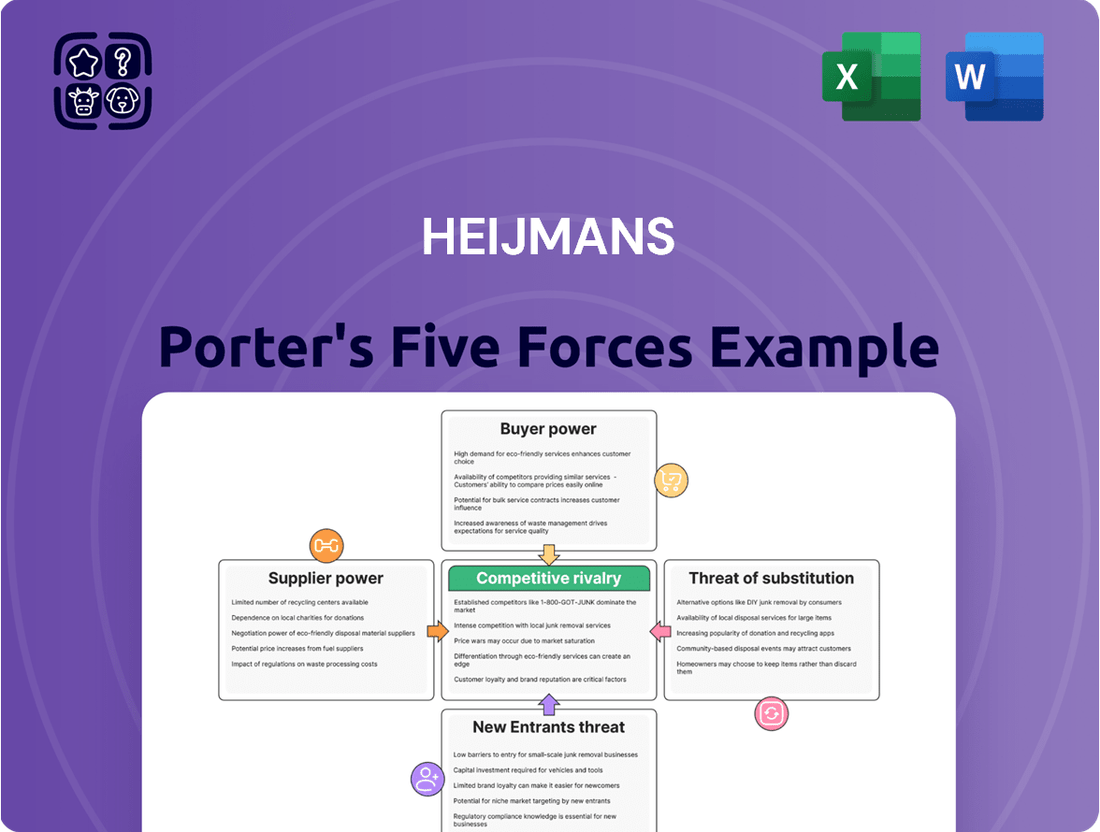

A comprehensive assessment of the competitive landscape for Heijmans, detailing the intensity of rivalry, buyer and supplier power, threat of new entrants and substitutes.

Quickly identify and address competitive threats with a clear, actionable overview of all five forces.

Customers Bargaining Power

Public Sector Clients (Government and Municipalities)

Public sector clients, like national and local governments, hold significant bargaining power. This is largely due to the immense scale of infrastructure projects they commission and the stringent, competitive tendering processes they employ. For instance, in 2023, infrastructure spending by governments globally continued to be a major driver for construction firms.

These government entities often set the precise project specifications, project timelines, and payment schedules, giving them considerable leverage. They can further amplify this power by fostering competitive bidding, encouraging multiple construction companies to vie for contracts, which naturally drives down prices. Heijmans, therefore, needs to present compelling value propositions that extend beyond mere cost-effectiveness.

Large-Scale Property Developers

Large-scale property developers wield considerable bargaining power due to their capacity to initiate multiple significant residential and commercial ventures. These sophisticated buyers can effectively solicit competitive bids from a range of construction companies, enabling them to negotiate assertively on pricing and contractual conditions. Furthermore, their ability to dictate stringent quality benchmarks and adherence to project timelines places additional leverage in their hands. For instance, in 2024, major Dutch developers like AM Real Estate Development and VolkerWessels proceeded with substantial urban renewal projects, seeking multiple construction partners to ensure competitive pricing and efficient project execution.

Individual Home Buyers (Indirect Influence)

Individual home buyers, while seemingly small players, wield significant indirect influence on Heijmans. Their collective demand, willingness to pay, and the availability of alternative housing choices like resale properties or homes from competing builders shape the overall market sentiment. For instance, in 2024, rising interest rates and economic uncertainty led to a noticeable cooling in the Dutch housing market, giving buyers more leverage to negotiate prices, impacting Heijmans' property development segment.

Project-Specific Nature of Demand

The project-specific nature of demand in the construction sector significantly empowers Heijmans' customers. Each construction contract, often a substantial investment for the client, grants them considerable bargaining power. This leverage is evident in contract negotiations, where clients can dictate terms and specifications, and throughout the project's execution, influencing change orders and demanding strict adherence to quality standards.

Customers can also impose penalty clauses for delays or deviations from agreed-upon quality, further amplifying their influence. For instance, in 2024, construction projects across Europe faced scrutiny for cost overruns and timeline adherence, leading clients to demand tighter contractual controls and performance guarantees from contractors like Heijmans. This environment means customers wield substantial sway over project outcomes and profitability.

- Significant Contract Value: Individual projects represent a large portion of a client's capital expenditure, making them highly invested in project success and thus influential.

- Control over Specifications and Changes: Clients often have the final say on design modifications and scope adjustments, directly impacting project costs and timelines.

- Enforcement of Penalties: Contractual clauses for delays or quality defects allow customers to impose financial penalties, incentivizing contractors to meet stringent requirements.

- Risk Transfer: By specifying detailed requirements and performance metrics, customers can transfer project-specific risks to the contractor.

Ability to Switch Contractors

Before Heijmans is even awarded a contract, potential clients hold significant power. They can easily opt for a different bidder if Heijmans' proposal or pricing isn't competitive. This pre-contractual phase is where customer bargaining power is at its peak.

Heijmans actively works to reduce this power by building a strong reputation and demonstrating a proven track record. Highlighting specialized expertise, particularly in sustainable building solutions, and consistently delivering complex projects on time and within budget are crucial. These factors lower the perceived switching costs for customers once a relationship is established.

- Reputation and Track Record: Heijmans aims to build a strong brand image through successful project completion, influencing customer perception and reducing the inclination to switch.

- Specialized Expertise: A focus on sustainable solutions can differentiate Heijmans, making it a more attractive choice and potentially locking in customers who prioritize these offerings.

- Project Delivery Excellence: Consistently meeting deadlines and budget constraints for complex projects directly combats the customer's ability to easily seek alternatives, as reliability becomes a key factor.

Customer Bargaining Power: A Force in Construction

Customers, particularly large institutional buyers like governments and major developers, exert substantial bargaining power over Heijmans. This stems from the significant value of their contracts and their ability to solicit competitive bids, driving down prices and dictating terms. In 2024, factors like economic uncertainty and a focus on cost efficiency amplified this customer leverage, especially in large infrastructure and residential projects across the Netherlands.

The ability for clients to impose penalties for delays or quality issues further strengthens their position, forcing contractors like Heijmans to maintain high standards and efficient project management. For example, in 2024, many European construction projects faced increased client scrutiny regarding budget adherence and timely delivery, leading to tighter contractual controls being demanded.

Heijmans counters this by building a strong reputation and emphasizing specialized expertise, such as in sustainable building, to reduce perceived switching costs for clients. This focus on reliability and unique value propositions is key to mitigating the inherent bargaining power of its customer base.

| Customer Segment | Bargaining Power Drivers | Impact on Heijmans (2024 Context) |

| Public Sector (Governments) | Large contract values, stringent tendering, fixed specifications | High power, drives competitive pricing, strict project management needs |

| Large Developers | Multiple project initiations, competitive bidding, quality control | Significant power, influences pricing and contractual terms |

| Individual Home Buyers | Collective demand, market sentiment, alternative housing options | Indirect but notable influence, impacts pricing in residential segments |

Full Version Awaits

Heijmans Porter's Five Forces Analysis

The document you see here is the complete Heijmans Porter's Five Forces Analysis, ready for immediate use upon purchase. This preview accurately reflects the professionally formatted and detailed report you will receive, ensuring no surprises. You're looking at the actual, finished analysis, providing you with the strategic insights you need without any placeholders or missing sections. This is your deliverable – the exact file you'll download, offering a comprehensive understanding of Heijmans' competitive landscape.

Rivalry Among Competitors

Fragmented and Mature Market

The Dutch construction market where Heijmans operates is indeed a mature and fragmented landscape. This means there are many companies, both local and international, vying for projects. Think of it like a large pie with many slices being cut, and everyone wants the biggest piece they can get. This sheer number of competitors, including other significant construction firms, naturally fuels a strong rivalry.

This intense competition often translates into fierce price wars, particularly when bidding on straightforward or less specialized construction projects. Companies feel compelled to offer lower prices to secure contracts. For instance, in 2023, the average bid-to-award ratio for public infrastructure projects in the Netherlands indicated significant competitive pressure, with some sectors seeing ratios exceeding 3:1, suggesting many more bids than successful awards.

Heijmans, therefore, must actively seek ways to stand out from the crowd. This differentiation isn't just about being the cheapest; it's about offering superior value. Key areas where Heijmans aims to differentiate include embracing innovation in building techniques, leading the charge in sustainable construction practices, and relentlessly pursuing operational efficiency to manage costs effectively.

The maturity of the market also means that growth opportunities might be slower compared to emerging markets. This forces companies like Heijmans to be highly strategic in their approach, focusing on niche markets, value-added services, and long-term partnerships to maintain a competitive edge and secure profitable projects amidst the crowded field.

Diverse Competitor Landscape

Heijmans faces a multifaceted competitive environment. This includes large, integrated construction companies offering a broad spectrum of services, alongside smaller, specialized firms excelling in areas like property development, advanced building technologies, and specific infrastructure segments.

Competition extends beyond mere cost considerations. Factors such as deep technical expertise, a strong track record and reputation, the demonstrable quality of delivered projects, and rigorous compliance with evolving regulatory frameworks and stringent environmental standards are critical differentiators for Heijmans and its rivals.

For instance, in the Dutch construction market, which is a key operational area for Heijmans, the sector is characterized by a significant number of SMEs alongside larger players. The Dutch construction sector's turnover was projected to reach approximately €70 billion in 2024, indicating a robust yet highly contested market where specialization and innovation are paramount.

Focus on Sustainability and Innovation

Competitive rivalry in the construction sector is intensifying, particularly around sustainability and innovation. Companies are increasingly judged on their ability to deliver environmentally friendly building practices, energy-efficient designs, and smart infrastructure. This focus means that firms like Heijmans, which invest in advanced, green, and tech-integrated solutions, can differentiate themselves.

However, this also attracts significant competition, as rivals are also channeling substantial resources into these very areas. For instance, the Netherlands, Heijmans' primary market, saw a significant push towards circular construction in 2024, with governmental incentives driving innovation in material reuse and reduced environmental impact. This competitive dynamic requires continuous investment in R&D to maintain a leading edge.

Cyclical Industry Dynamics

The construction sector, where Heijmans operates, is inherently cyclical. Its performance is closely tied to broader economic health, government infrastructure spending, and prevailing interest rates. When the economy slows, fewer new projects get initiated, and this scarcity directly amplifies competitive rivalry.

During these downturns, companies like Heijmans often experience intensified competition. With a shrinking pool of available work, bidding becomes more aggressive as firms vie for limited contracts, inevitably squeezing profit margins. For instance, in 2023, the Netherlands construction sector saw a notable decline in new orders, particularly in residential building, leading to increased price sensitivity among clients.

Heijmans' strategy of diversifying its operations across various segments, such as residential, non-residential, and infrastructure, serves as a crucial buffer against these sharp cyclical swings. This diversification helps to smooth out revenue streams, as weakness in one sector might be offset by strength in another, reducing the overall impact of economic downturns on its competitive positioning.

- Cyclicality Impact: The construction industry's reliance on economic cycles means that periods of high demand can be followed by sharp contractions.

- Downturn Competition: Fewer projects during economic slowdowns lead to heightened rivalry and pressure on profitability for firms like Heijmans.

- Heijmans' Mitigation: Diversification across residential, non-residential, and infrastructure sectors helps to reduce vulnerability to sector-specific downturns.

- 2023 Data Point: The Dutch construction sector experienced a contraction in new orders in 2023, highlighting the cyclical pressures faced by industry players.

Reputation and Track Record

In the project-based construction industry, a company's reputation acts as a powerful competitive weapon. Heijmans, with its extensive history, has cultivated a strong track record in delivering complex projects reliably, with high quality, and on schedule. This established credibility serves as a significant barrier to entry for newer or less experienced competitors, making it harder for them to secure lucrative contracts.

Heijmans’ commitment to safety, quality, and timely project completion is a key differentiator. For example, in 2024, the company continued to emphasize these core values across its diverse portfolio. This focus on dependable execution directly translates into client trust and repeat business.

- Reputation as a Barrier: Heijmans' long-standing reputation for reliability and quality makes it difficult for new entrants to gain traction in securing large, complex projects.

- Track Record Advantage: Proven success in past projects, a hallmark of Heijmans' operations, provides a competitive edge when bidding for new contracts.

- Client Trust: A history of on-time and high-quality delivery fosters strong client relationships, leading to preferential consideration for future work.

- Safety Emphasis: Heijmans' consistent focus on safety in 2024 reinforces its image as a responsible and dependable partner, further strengthening its competitive position.

Dutch Construction: Intense Rivalry & Strategic Shifts

The competitive rivalry within Heijmans' operating environment is intense due to the fragmented nature of the Dutch construction market, characterized by numerous local and international players. This leads to aggressive bidding, especially on standard projects, as companies strive to secure market share. Heijmans differentiates itself through innovation, sustainability, and operational efficiency, aiming to provide superior value beyond just price. The sector's cyclicality further amplifies competition during economic downturns, making diversification and a strong reputation critical for navigating market pressures.

| Metric | 2023 (Estimated/Actual) | 2024 (Projected/Target) | Impact on Rivalry |

|---|---|---|---|

| Dutch Construction Market Turnover | €68.5 billion | €70 billion | Indicates a large, attractive market, thus intensifying competition for projects. |

| Bid-to-Award Ratio (Public Infrastructure) | Exceeded 3:1 in some segments | Expected to remain high | Signifies a high volume of bids per awarded contract, demonstrating fierce competition. |

| Investment in Sustainable Construction | Significant increase | Continued growth with government incentives | Rivals are investing heavily in green technologies, raising the bar and increasing competitive pressure on innovation. |

| New Orders Growth (Residential) | Negative growth | Slight recovery expected | A contracting segment intensifies rivalry for remaining projects, impacting profitability. |

SSubstitutes Threaten

Modular and Prefabricated Construction

Modular and prefabricated construction present a substantial threat as alternatives to conventional building. These approaches can deliver quicker project completion, more reliable cost estimations, and enhanced quality assurance, particularly for uniform residential and commercial projects.

For instance, the global modular construction market was valued at approximately USD 150 billion in 2023 and is projected to grow significantly in the coming years. This growth is driven by the demand for efficiency and cost savings, directly challenging traditional construction models where Heijmans operates.

Heijmans needs to either adopt these industrialized methods by integrating them into its operations or develop strategies to compete directly with companies specializing in off-site construction. Failure to address this threat could lead to a loss of market share and reduced competitiveness in the housing and construction sectors.

Renovation and Repurposing of Existing Structures

The renovation, refurbishment, and adaptive reuse of existing structures present a significant threat of substitution for new construction projects. In many urban centers, the cost-effectiveness and environmental benefits of revitalizing older buildings make them a compelling alternative to ground-up development. This trend directly impacts demand for new builds, especially as cities increasingly prioritize sustainability and heritage preservation. For instance, the global building renovation market was valued at approximately $1.1 trillion in 2023 and is projected to grow, indicating a strong preference for upgrading rather than replacing existing stock.

Advanced Digitalization and Virtual Solutions

The rise of advanced digitalization, including Building Information Modeling (BIM) and digital twins, presents a significant threat of substitutes for traditional construction processes. These technologies can streamline design and planning, potentially reducing the need for certain physical prototyping and on-site validation steps. For instance, by 2024, the global construction BIM market was projected to reach over $13 billion, indicating a substantial shift towards digital solutions that can replicate or enhance aspects of physical work.

These digital substitutes can fundamentally alter the demand for traditional construction services. While they don't replace the physical act of building, they can substitute for elements of the design, pre-construction, and even some testing phases. This means companies that heavily rely on older, less digitized methods may find their services less competitive as clients increasingly opt for more efficient, digitally-driven project delivery.

Infrastructure Alternatives and Optimization

The threat of substitutes for Heijmans in infrastructure is significant. Instead of constructing entirely new roads or tunnels, existing networks can be optimized through smart traffic management systems or enhanced public transportation. For example, the Dutch government's investment in high-speed rail and improved local public transport options offers alternatives to new road construction for commuter travel.

Policy changes can also redirect demand. A shift towards demand management strategies, like congestion pricing or promoting remote work, could lessen the need for large-scale infrastructure projects. Furthermore, the increasing focus on smaller, localized infrastructure solutions, such as neighborhood-level renewable energy grids or localized water management systems, presents alternatives to traditional, large-scale public works.

- Optimization of existing infrastructure: Smart traffic management and public transport upgrades can reduce the need for new road and tunnel construction.

- Policy shifts: Government initiatives promoting demand management or localized solutions can decrease reliance on large-scale infrastructure.

- Technological advancements: Innovations in areas like autonomous vehicles could alter future infrastructure needs, potentially reducing the demand for traditional road expansion.

Do-It-Yourself (DIY) or Informal Construction

For smaller renovation or extension projects, clients might consider DIY approaches or hire uncertified, informal labor. This trend acts as a substitute, particularly for the lower end of the construction market, potentially impacting demand for Heijmans' professional services. For instance, in 2024, the UK's DIY market continued to show resilience, with many homeowners undertaking smaller projects themselves to save costs.

This diffuse threat is more pronounced in segments where project complexity is lower. While Heijmans focuses on larger infrastructure and residential developments, the availability of affordable, albeit less professional, alternatives for smaller jobs can still influence overall market dynamics. The informal construction sector, often characterized by lower overheads and flexible pricing, presents a persistent challenge, especially in price-sensitive markets.

- DIY impact: Homeowners undertaking minor renovations themselves to reduce labor costs.

- Informal labor: Use of uncertified contractors for smaller, less complex construction tasks.

- Market segmentation: Threat is more significant in the lower-end, smaller-scale renovation market.

- Cost sensitivity: DIY and informal options appeal to clients prioritizing budget over professional certification.

Disrupting Construction: Emerging Alternatives to Traditional Building

Modular and prefabricated construction represent a significant substitute for traditional building methods, offering faster completion times and more predictable costs, especially for standardized projects. The global modular construction market was valued at approximately USD 150 billion in 2023 and is expected to see robust growth, directly challenging Heijmans' conventional operations.

The renovation and adaptive reuse of existing buildings are also powerful substitutes for new construction, driven by cost-effectiveness and sustainability goals in urban areas. This trend is supported by the global building renovation market, valued at roughly $1.1 trillion in 2023, highlighting a growing preference for upgrading existing structures over new developments.

Digitalization, including Building Information Modeling (BIM), offers substitutes for certain traditional design and planning phases. The global construction BIM market was projected to exceed $13 billion by 2024, indicating a clear industry shift towards digital solutions that can streamline processes and potentially reduce reliance on certain physical construction elements.

In infrastructure, alternatives like smart traffic management and enhanced public transportation can substitute for new road construction, as exemplified by Dutch investments in high-speed rail. Policy shifts promoting demand management, such as congestion pricing, can also reduce the need for large-scale infrastructure projects.

Entrants Threaten

High Capital Requirements

Entering the large-scale construction and infrastructure sector, where Heijmans operates, demands immense financial resources. New companies need significant capital for heavy machinery, specialized equipment, and advanced technology. For instance, acquiring a fleet of excavators, cranes, and other essential construction vehicles can easily run into millions of euros, creating a formidable barrier.

Beyond equipment, substantial working capital is crucial for managing the long project cycles and cash flow demands inherent in infrastructure development. Heijmans, like its peers, must finance materials, labor, and operational costs for projects that may span several years. This need for deep pockets effectively discourages many potential new entrants who lack the necessary financial backing to compete.

Established Relationships and Reputation

The construction sector thrives on deep-seated connections with clients, suppliers, and a skilled web of subcontractors. Newcomers struggle to replicate the trust and proven history that established players like Heijmans have cultivated over many years, hindering their ability to win significant contracts.

Complex Regulatory and Permitting Environment

The Dutch construction sector is heavily regulated, with strict building codes, environmental standards, and complex permitting processes. For example, in 2024, the average time to obtain a building permit in the Netherlands could extend for several months, depending on the project's complexity and local municipality. This intricate legal and administrative framework demands considerable expertise and financial resources, acting as a significant deterrent for potential new entrants aiming to establish themselves in the market.

Access to Skilled Labor and Specialized Expertise

The competition for skilled labor presents a significant barrier to entry. New companies find it challenging to attract and retain talent, especially in specialized areas like sustainable building and advanced engineering. Established firms, such as Heijmans, often have a strong reputation and existing relationships that make it difficult for newcomers to source experienced professionals.

This difficulty in acquiring specialized expertise directly impacts a new entrant's ability to operate efficiently and effectively. For instance, the demand for construction workers skilled in green building techniques has surged. In 2024, the Dutch construction sector reported a shortage of over 70,000 skilled workers, a figure that heavily impacts new players trying to establish a foothold.

- Talent Acquisition Difficulty: New entrants face an uphill battle in recruiting experienced engineers and tradespeople.

- Retention Challenges: Retaining skilled workers is equally tough, as established companies offer competitive packages and career progression.

- Specialized Skills Gap: Expertise in emerging areas like modular construction and digital building technologies is particularly scarce.

- Impact on Operational Capacity: A lack of skilled labor directly hinders a new entrant's ability to scale operations and deliver projects.

Economies of Scale and Experience Curve

Existing major construction and infrastructure companies, such as Heijmans, leverage significant economies of scale. This scale translates into preferential pricing on materials and equipment through bulk purchasing, as well as optimized project management and operational efficiencies. For instance, in 2024, large-scale infrastructure projects often involve billions of euros in capital, where even a small percentage saving on procurement due to scale can represent millions.

Furthermore, Heijmans and similar established firms benefit from an experience curve. Decades of managing diverse and complex projects, from residential developments to large public works, have honed their execution capabilities and risk assessment. This accumulated knowledge allows them to bid more competitively and deliver projects with greater certainty and lower costs than newer entrants who lack this historical data and proven track record.

- Economies of Scale: Bulk purchasing power for materials and equipment, leading to cost advantages.

- Operational Efficiency: Streamlined processes in project management and execution due to size.

- Experience Curve Advantage: Accumulated knowledge from past projects improves bidding and delivery efficiency.

- Competitive Bidding: Lower cost structures enable more aggressive pricing compared to new firms.

Construction Sector: High Barriers Deter New Competitors

The threat of new entrants in Heijmans' sector is moderate. The substantial capital requirements for machinery and skilled labor create significant barriers. For example, a single large crane can cost upwards of €500,000, and the Dutch construction sector faced a shortage of over 70,000 skilled workers in 2024, making talent acquisition difficult and expensive for newcomers.

Regulatory hurdles and the need for established client relationships further deter new players. Navigating complex permitting processes, which can take months in 2024, demands specialized knowledge and resources. Furthermore, winning large infrastructure contracts often relies on a proven track record, which new entrants lack.

| Barrier Type | Description | 2024 Data/Example |

|---|---|---|

| Capital Requirements | High cost of heavy machinery and equipment. | A single excavator can cost €100,000 - €500,000. |

| Skilled Labor Shortage | Difficulty attracting and retaining experienced personnel. | Over 70,000 skilled worker shortage in Dutch construction in 2024. |

| Regulatory Compliance | Complex building codes, environmental standards, and permits. | Building permit acquisition can take several months in 2024. |

| Established Relationships | Need for trust and proven history with clients and suppliers. | New entrants struggle to displace long-standing supplier contracts. |

Porter's Five Forces Analysis Data Sources

Our Heijmans Porter's Five Forces analysis is built upon a robust foundation of data, integrating information from company annual reports, industry expert interviews, and publicly available market research databases to provide a comprehensive view of competitive dynamics.