Svenska Handelsbanken Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Svenska Handelsbanken Bundle

Go Beyond the Preview—Access the Full Strategic Report

Svenska Handelsbanken operates in a banking landscape shaped by moderate rivalry and significant buyer power, as customers can readily switch between institutions. The threat of new entrants is somewhat mitigated by high capital requirements and regulatory hurdles, but digital disruptors pose an evolving challenge.

The complete report reveals the real forces shaping Svenska Handelsbanken’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Access to Capital and Funding Sources

Svenska Handelsbanken's access to capital is a critical component of its operations, and the bargaining power of its suppliers in this area is generally constrained. The bank draws funds from a variety of sources, including customer deposits, borrowing from other financial institutions, and issuing debt in capital markets. This diversification inherently limits the power of any single supplier or group of suppliers.

The highly regulated nature of the financial sector also plays a significant role in mitigating supplier power. Regulatory frameworks often ensure a degree of liquidity and stability within the banking system, making it more challenging for capital providers to exert undue influence. For instance, in 2023, Handelsbanken reported total deposits of SEK 3,400 billion, highlighting the substantial base of customer funding.

However, external economic factors can shift this dynamic. Significant increases in central bank interest rates, as seen in many economies during 2023 and continuing into 2024, can increase the cost of borrowing for banks. Similarly, a decline in overall investor confidence in financial markets can make it more expensive for banks to raise capital through debt issuance, thereby amplifying the bargaining power of these capital providers.

Technology and Infrastructure Providers

Technology and infrastructure providers hold a moderate level of bargaining power in the banking sector. Banks like Svenska Handelsbanken are heavily dependent on specialized software, cloud computing, and robust cybersecurity solutions to maintain operations and offer digital services. For instance, in 2024, the global cloud computing market, a key area for banks, was projected to reach over $600 billion, highlighting the significant role of these providers.

However, this power is somewhat constrained. The banking industry often sees a diverse ecosystem of technology vendors, offering alternatives for essential services. Furthermore, large institutions like Handelsbanken possess the resources to develop some in-house capabilities or to switch between providers, which acts as a counterbalance to excessive supplier demands. The ability to negotiate and diversify technological partnerships remains a critical strategy for managing this relationship.

Human Capital and Specialized Talent

Highly skilled employees, particularly in IT, data analytics, cybersecurity, and specialized financial advisory roles, are vital suppliers for Svenska Handelsbanken. The intense competition for this talent means these individuals hold considerable bargaining power, which can translate into increased wage demands and recruitment hurdles for the bank.

Regulatory Bodies and Compliance Services

Regulatory bodies, though not traditional suppliers, wield significant power by dictating the operational landscape and compliance mandates for Svenska Handelsbanken. Increased regulatory scrutiny, exemplified by directives from Finansinspektionen and broader EU regulations, necessitates substantial investment in compliance services and legal expertise.

These requirements directly impact the bank's cost structure and strategic flexibility, effectively acting as a powerful external force. For instance, the ongoing implementation of Basel III and IV standards, which were actively being discussed and refined throughout 2024, demands continuous adaptation and investment in risk management systems, adding to operational overhead.

- Increased Compliance Costs: Banks face rising expenses for legal counsel, technology solutions, and personnel dedicated to meeting evolving regulatory demands.

- Operational Constraints: Strict capital adequacy ratios and liquidity requirements imposed by regulators can limit lending capacity and product innovation.

- Strategic Influence: Regulatory changes can force banks to divest certain business lines or alter their market focus to remain compliant.

- Need for Specialized Services: The complexity of financial regulations drives demand for external compliance consultants and audit firms, who benefit from this power.

Information and Data Providers

Information and data providers can exert some bargaining power on Svenska Handelsbanken, especially those offering unique or proprietary financial data, market intelligence, and credit ratings. Access to reliable data is fundamental for the bank's risk assessment, strategic decisions, and overall operational efficiency. For instance, specialized financial data terminals, like Bloomberg or Refinitiv, which aggregate vast amounts of real-time market information, can command significant subscription fees due to the critical nature and comprehensiveness of their services.

However, this supplier power is often tempered by several factors. The increasing availability of multiple data sources and the bank's own robust internal data generation capabilities and analytics platforms serve as a counterbalance. Svenska Handelsbanken, like other major financial institutions, invests heavily in its own data infrastructure and research teams. This reduces its sole reliance on external providers. In 2024, the financial data market is competitive, with many vendors offering similar services, further diluting the power of any single supplier.

- Critical Data Dependence: Banks rely heavily on accurate financial data for trading, risk management, and compliance, making specialized data providers essential.

- Proprietary Information Value: Suppliers with unique datasets or analytical tools that offer a competitive edge can negotiate stronger terms.

- Counterbalancing Factors: The presence of numerous data vendors and a bank's internal data capabilities limit the bargaining power of individual suppliers.

- Market Competition: The competitive landscape among financial information providers in 2024 generally keeps pricing in check, reducing supplier leverage.

Supplier Power Dynamics in Banking: Funding, Tech, Talent

The bargaining power of Svenska Handelsbanken's suppliers is generally moderate, with capital providers and technology vendors having the most influence. Customer deposits form a substantial funding base, limiting the power of other capital sources. In 2023, Handelsbanken's total deposits were SEK 3,400 billion, demonstrating this strength.

However, rising interest rates in 2023 and 2024 increased the cost of wholesale funding, giving these suppliers more leverage. Similarly, the bank's reliance on specialized technology, such as cloud services projected to exceed $600 billion globally in 2024, grants significant power to key IT vendors, though diversification of providers offers some mitigation.

| Supplier Type | Bargaining Power Level | Key Factors |

| Capital Providers (Wholesale) | Moderate to High | Interest rate environment (e.g., 2023-2024 rate hikes), investor confidence, market liquidity. |

| Technology & Infrastructure Providers | Moderate | Dependence on specialized software/cloud, cybersecurity needs. Vendor competition and bank's internal capabilities are counterbalances. |

| Skilled Employees | High | Competition for talent in IT, data analytics, and specialized finance roles. |

| Information & Data Providers | Moderate | Criticality of data for risk management and decision-making. Value of proprietary data. Bank's internal data capabilities and vendor competition limit power. |

What is included in the product

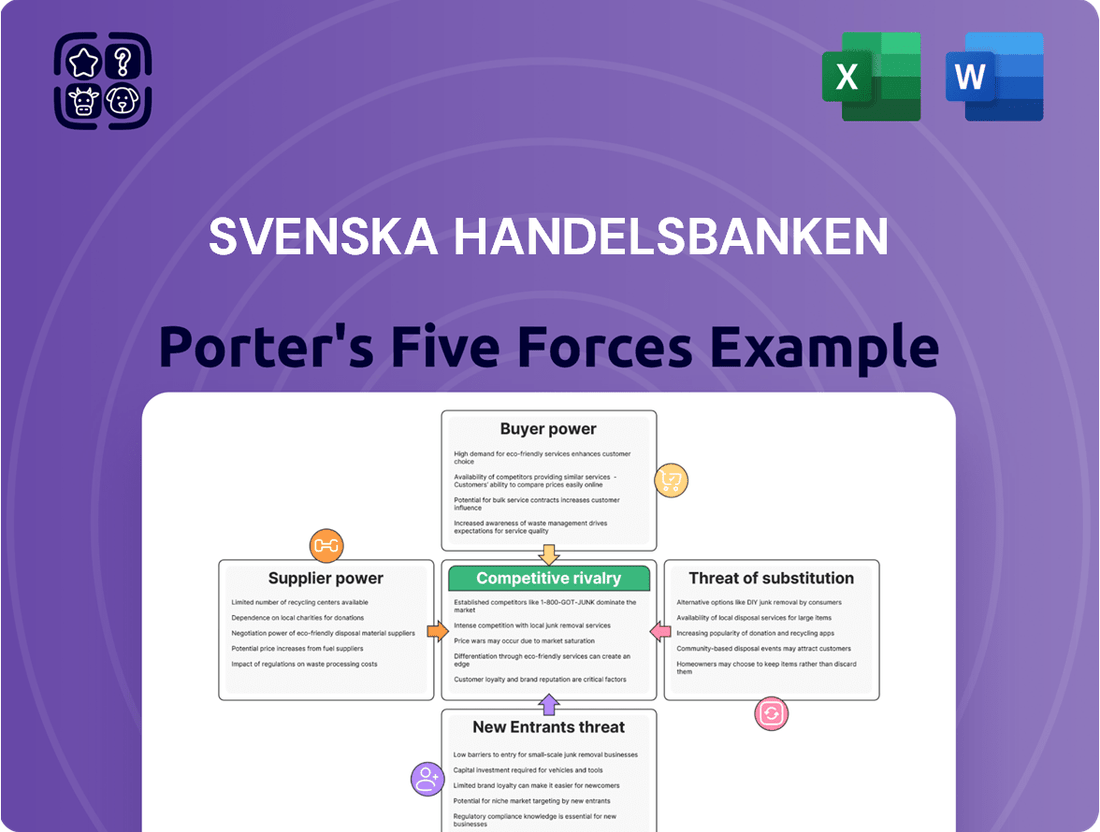

This analysis unpacks the competitive forces impacting Svenska Handelsbanken, detailing the intensity of rivalry, the power of buyers and suppliers, the threat of new entrants, and the availability of substitutes.

Effortlessly gauge Svenska Handelsbanken's competitive landscape with a visual breakdown of each force, simplifying complex strategic analysis.

Customers Bargaining Power

Diverse Customer Segments

Svenska Handelsbanken caters to a wide array of customers, from individuals managing personal finances to large corporations and institutional investors. This diversity means the bargaining power of customers isn't uniform across the board.

For retail customers, individual bargaining power is typically limited. Products are often standardized, and the effort and potential costs associated with switching banks, even for a few basis points on a loan or deposit, can be substantial. This inertia contributes to lower price sensitivity for many individual clients.

Conversely, large corporate and institutional clients hold more sway. These entities often manage significant volumes of business, including substantial deposits, complex loan portfolios, and investment banking services. Handelsbanken's willingness to negotiate terms, fees, and pricing is often directly correlated with the overall value and potential future business these larger clients represent.

Low Switching Costs for Standard Products

For basic banking products like current accounts and standard loans, customers can switch banks with relative ease, especially as digital banking simplifies the process. This ease of switching means customers have more power, as they can easily move to competitors offering better rates or services. In 2024, Sweden's banking sector continues to see high consumer mobility, indicating that barriers to switching banks remain low.

Access to Information and Price Transparency

Customers today possess unprecedented access to information about financial products and services, allowing them to effortlessly compare offerings from various banking institutions. This ease of comparison significantly amplifies their bargaining power.

Online comparison tools and readily available financial advisory services have dramatically increased price transparency in the banking sector. For instance, in 2024, a significant portion of consumers actively used digital channels to research and compare banking products, leading them to demand more competitive interest rates and favorable terms from providers like Svenska Handelsbanken.

Decentralized Decision-Making and Relationship Banking

Svenska Handelsbanken's decentralized approach, empowering local branches and prioritizing long-term customer relationships, directly counters customer bargaining power. This model fosters deep loyalty and personalized service, making it harder for customers to switch based solely on price. By building these strong, enduring connections, Handelsbanken aims to increase perceived switching costs, a key strategy to mitigate customer leverage.

This focus on relationship banking creates a significant differentiator compared to more transactional banking models. For instance, in 2024, Handelsbanken continued to report high levels of customer satisfaction, a testament to the effectiveness of its localized service model. This loyalty inherently reduces the willingness of customers to exert pressure for better terms, as they value the established relationship.

- Decentralized Autonomy: Local branches have significant decision-making power, enabling tailored customer solutions.

- Relationship Focus: Emphasis on long-term partnerships rather than transactional interactions.

- Reduced Switching Incentives: Strong relationships and personalized service increase perceived switching costs for customers.

- Customer Stickiness: Loyalty fostered by deep engagement makes customers less likely to seek alternative providers.

Availability of Alternative Financial Service Providers

The rise of fintech firms and challenger banks significantly amplifies customer bargaining power. These new entrants, along with other non-traditional financial service providers, offer customers a broader array of choices beyond established institutions like Handelsbanken.

This increased competition compels traditional banks to enhance their offerings and value propositions. For instance, by mid-2024, the global fintech market was projected to reach over $300 billion, indicating substantial growth and a wider competitive landscape.

- Fintech Growth: The fintech sector's rapid expansion provides customers with more diverse and often more accessible financial solutions.

- Challenger Banks: These digital-first banks often offer lower fees and more user-friendly interfaces, directly challenging incumbents.

- Customer Expectations: Increased alternatives raise customer expectations for service quality, pricing, and innovation from all financial providers.

- Handelsbanken's Response: To counter this, Handelsbanken must focus on differentiated services, digital transformation, and customer-centricity to retain its market position.

Customer Bargaining Power: Navigating Bank-Client Dynamics

The bargaining power of Svenska Handelsbanken's customers is a significant factor, particularly for large corporate and institutional clients who manage substantial business volumes. These clients can negotiate terms, fees, and pricing based on the value they bring to the bank, a dynamic evident throughout 2024 as competition intensified. Retail customers, while having more options due to digital banking and comparison tools, often face higher switching costs due to the inertia and established relationships that Handelsbanken cultivates through its decentralized, relationship-focused model. This approach aims to mitigate customer leverage by fostering loyalty and perceived switching costs.

| Customer Segment | Bargaining Power Factors | Handelsbanken's Mitigation Strategy | 2024 Data Insight |

|---|---|---|---|

| Retail Customers | Low individual power, ease of switching for basic products, access to comparison tools. | Relationship banking, personalized service, building loyalty to increase perceived switching costs. | High customer satisfaction reported, indicating effectiveness of localized service model. |

| Corporate/Institutional Clients | High power due to significant business volumes (deposits, loans, investment banking). | Negotiation on terms, fees, and pricing based on client value. | Continued focus on tailored solutions for large clients to maintain market share. |

| Overall Market Influence | Increased by fintech growth and challenger banks offering diverse, often lower-cost alternatives. | Differentiated services, digital transformation, customer-centricity to retain market position. | Global fintech market projected to exceed $300 billion by mid-2024, highlighting competitive landscape. |

Full Version Awaits

Svenska Handelsbanken Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis of Svenska Handelsbanken, detailing the competitive landscape and strategic positioning of the bank. The document you see here is the exact, professionally formatted report you will receive immediately after purchase, providing actionable insights into the industry's dynamics. You're looking at the actual document; once you complete your purchase, you’ll get instant access to this exact file, ready for your strategic planning.

Rivalry Among Competitors

Concentrated Market with Intense Competition

Svenska Handelsbanken operates in a concentrated Swedish banking market where the top four banks, including Handelsbanken, control a substantial portion of the credit market. For instance, as of early 2024, these major banks collectively held over 70% of the total banking assets in Sweden, highlighting the market's consolidation.

Despite this concentration, competition remains fierce. Smaller and challenger banks have been actively gaining market share, particularly in areas like digital services and specialized lending, putting pressure on established players like Handelsbanken. This ongoing challenge from both large incumbents and agile smaller firms signifies a strong competitive rivalry.

Market Share Dynamics and Growth Strategies

Svenska Handelsbanken, a titan in the banking sector, faces a dynamic competitive environment. While it remains a dominant force, its market share in specific areas like mortgages has seen a slight erosion, with nimbler, smaller banks capturing a larger slice of these markets. This shift underscores an intense rivalry where established institutions and emerging players are actively deploying diverse strategies to attract and retain customers.

Focus on Efficiency and Cost Management

Competitive rivalry in the Swedish banking sector is intense, with a strong emphasis on efficiency and cost management. Swedish banks, in general, operate with remarkably low and stable operational costs. This efficiency is a direct result of the competitive landscape, which compels institutions to constantly refine their processes and maintain competitive pricing for their services.

Handelsbanken, for instance, has actively pursued efficiency gains, including strategic staffing adjustments, to uphold its deeply ingrained cost-conscious culture. This focus is crucial for navigating the competitive pressures and maintaining profitability in a mature market.

Product and Service Differentiation

Competitive rivalry at Svenska Handelsbanken is intensified by factors beyond just pricing, with product and service differentiation playing a crucial role. Handelsbanken has carved out a distinct market position through its unique decentralized operating model, which empowers local branches to make decisions tailored to their specific customer needs. This fosters a strong local presence and cultivates long-term customer relationships, a key differentiator in a crowded financial landscape.

The bank's commitment to customer-centricity translates into personalized service and a deep understanding of local market dynamics. This approach contrasts with more centralized banking models and allows Handelsbanken to build trust and loyalty. For instance, in 2023, Handelsbanken's customer satisfaction scores remained high, reflecting the success of its localized strategy.

Furthermore, like many of its peers, Handelsbanken is actively investing in digital transformation and artificial intelligence (AI). These investments are aimed at enhancing the customer experience through more intuitive digital platforms and improving operational efficiency. By leveraging technology, the bank seeks to offer seamless digital services while retaining the personal touch that defines its brand. In 2024, the bank continued to roll out new digital tools designed to streamline banking processes for both individual and corporate clients.

Key differentiators for Handelsbanken include:

- Decentralized Operating Model: Empowers local branches to make independent decisions, fostering agility and customer responsiveness.

- Strong Local Presence: Deep roots in communities allow for tailored financial solutions and relationship building.

- Emphasis on Long-Term Relationships: Focuses on building enduring customer loyalty through personalized service rather than short-term gains.

- Digital and AI Investments: Enhancing customer experience and operational efficiency through technology adoption.

Regulatory Environment and Capital Requirements

The robust regulatory landscape in Sweden, particularly concerning capital requirements, significantly shapes the competitive rivalry within the banking sector. These stringent rules, enforced by bodies like Finansinspektionen, act as substantial barriers to entry for new players, thereby consolidating the market among established institutions. For instance, as of early 2024, Swedish banks are operating under Basel III and its subsequent refinements, which mandate rigorous capital adequacy ratios. This necessitates considerable financial resources and robust risk management frameworks, directly impacting how intensely banks compete on factors beyond just price.

These regulatory demands mean that banks must allocate significant capital towards compliance and risk mitigation. This can influence their strategic choices, potentially limiting aggressive expansion or product innovation if it doesn't align with regulatory prudence. Consequently, competitive battles often revolve around operational efficiency, customer service, and the ability to navigate complex compliance requirements, rather than solely on market share acquisition through aggressive pricing. For example, the ongoing focus on cybersecurity and data protection, driven by regulations like GDPR, adds another layer of operational cost and strategic consideration for all Swedish banks.

- High Capital Adequacy Ratios: Swedish banks must maintain strong Common Equity Tier 1 (CET1) ratios, often exceeding minimum regulatory requirements, as demonstrated by the sector's average CET1 ratio which remained robust through 2023 and into 2024, typically above 18%.

- Compliance Costs: The investment in regulatory compliance, including technology and personnel, represents a significant operational expense, impacting profitability and influencing pricing strategies.

- Barriers to Entry: The substantial capital and expertise required to meet regulatory standards effectively limit the number of new entrants, reducing direct competitive pressure from startups.

- Focus on Stability: Regulations encourage a focus on financial stability and risk management, leading to a more conservative competitive environment where long-term sustainability is prioritized.

Swedish Banking: Intense Rivalry, Digital Drive, and Regulatory Strength

Competitive rivalry is a defining characteristic of Svenska Handelsbanken's operating environment. The Swedish banking sector is dominated by a few large players, with the top four banks holding over 70% of the credit market as of early 2024. Despite this concentration, competition is intense, fueled by both established rivals and agile challenger banks that are actively gaining ground, particularly in digital offerings.

This rivalry forces banks like Handelsbanken to prioritize efficiency and cost management, leading to remarkably low operational costs across the sector. Handelsbanken itself actively pursues efficiency gains, including strategic staffing adjustments, to maintain its cost-conscious culture. Differentiation is also key, with Handelsbanken leveraging its decentralized model and strong local presence to build long-term customer relationships, a strategy that yielded high customer satisfaction scores in 2023.

Furthermore, the competitive landscape is shaped by significant investments in digital transformation and AI, aimed at enhancing customer experience and operational efficiency. For example, in 2024, Handelsbanken continued to introduce new digital tools for both individual and corporate clients, reflecting the ongoing technological race.

The regulatory environment, particularly stringent capital requirements under Basel III and its refinements, acts as a substantial barrier to entry. This necessitates high capital adequacy ratios, with the sector's average Common Equity Tier 1 (CET1) ratio remaining robust, often above 18% through 2023 and into 2024. These regulations steer competition towards operational excellence and customer service rather than solely aggressive pricing.

| Metric | Handelsbanken (Approximate) | Swedish Banking Sector Average (Approximate) | Notes |

|---|---|---|---|

| Market Share (Top 4 Banks) | Significant | >70% of Credit Market (Early 2024) | Indicates market concentration. |

| Operational Costs | Low and Stable | Remarkably Low and Stable | Driven by competitive pressure for efficiency. |

| CET1 Ratio | Strong (e.g., ~19-20%) | >18% (2023-2024) | Exceeds regulatory minimums, demonstrating financial strength. |

| Customer Satisfaction | High (2023) | Generally High | Reflects success in customer-centric strategies. |

SSubstitutes Threaten

Fintech Companies and Digital Payment Solutions

Fintech companies are increasingly challenging traditional banks like Svenska Handelsbanken by offering digital payment solutions and other financial services. For instance, Swish, a popular mobile payment system in Sweden, allows users to transfer money instantly between bank accounts, directly competing with Handelsbanken's own payment services.

These fintech alternatives often boast lower transaction fees and a more streamlined user experience, attracting customers who prioritize convenience and cost savings. The rapid adoption of such digital platforms, with Swish reportedly handling billions of transactions annually in Sweden, signifies a substantial threat to incumbent banks' market share in payment processing.

Neobanks and Challenger Banks

Neobanks and challenger banks, digital-first financial institutions, present a significant threat of substitution to Svenska Handelsbanken's traditional retail banking services. These agile competitors, like Klarna Bank and Revolut, often boast lower operational costs due to their lack of physical branches. This allows them to offer competitive pricing and innovative digital solutions, particularly appealing to younger, tech-savvy demographics.

In the Nordic region, challenger banks are steadily gaining traction. For instance, by the end of 2023, Klarna reported over 150 million global consumers and 2.3 million merchants. This growing adoption signifies a direct substitution of services previously dominated by established players like Handelsbanken, especially in areas like payments, lending, and savings.

Direct Lending and Alternative Financing

The rise of direct lending and other alternative financing avenues presents a significant threat to traditional banks like Svenska Handelsbanken. For corporate clients, especially those seeking specialized or growth-oriented funding, these alternatives can indeed replace conventional bank loans. This trend is particularly noticeable as non-bank financial institutions increasingly offer flexible and tailored financing solutions.

In 2024, the alternative lending market continued its robust expansion, with global private debt fundraising reaching an estimated $1.5 trillion by the end of the year. This growth directly impacts banks by offering businesses more choices, thereby diminishing their exclusive role as primary lenders and potentially fragmenting market share.

In-house Corporate Treasury Functions

Large corporations increasingly leverage sophisticated in-house treasury functions, diminishing their reliance on external banks for critical financial services. This internal capacity directly substitutes for traditional corporate banking offerings, particularly in areas like liquidity management, investment execution, and foreign exchange hedging. For instance, many multinational corporations now manage significant portions of their foreign currency exposure internally rather than solely relying on bank-provided solutions.

The trend towards insourcing treasury operations is driven by a desire for greater control, cost efficiency, and customized risk management. As of 2024, a substantial number of Fortune 500 companies have dedicated treasury teams capable of executing complex financial transactions, effectively acting as a substitute for many services previously exclusive to banks.

- Reduced Dependence: Corporations with robust in-house treasury functions require fewer transactional banking services, particularly for foreign exchange and short-term investments.

- Cost Savings: Managing these functions internally can often be more cost-effective than paying bank fees for similar services, especially for high-volume activities.

- Enhanced Control: In-house teams provide greater direct oversight and flexibility in managing liquidity and investment portfolios according to specific corporate strategies.

- Technological Advancements: Modern treasury management systems (TMS) empower corporations to perform sophisticated analyses and execute transactions that were once the sole domain of financial institutions.

Cryptocurrencies and Blockchain-based Financial Services

Cryptocurrencies and blockchain-based financial services, though still in their early stages for everyday banking, pose a growing threat as substitutes for traditional payment and lending models. Their decentralized architecture offers the potential for reduced transaction fees and faster processing times, which could erode the market share of established financial intermediaries.

While widespread adoption for daily banking remains limited, the underlying blockchain technology is increasingly being explored for various financial applications. For instance, by the end of 2023, global crypto adoption reached an estimated 420 million users, indicating a significant, albeit niche, user base that could bypass traditional banking channels for certain transactions.

The threat is particularly pronounced in areas like cross-border payments and remittances, where traditional systems can be slow and expensive. Blockchain solutions aim to streamline these processes, potentially offering a more efficient alternative. By mid-2024, the global remittance market was projected to reach over $800 billion, a substantial segment where digital alternatives could gain traction.

- Potential disruption in payment systems: Blockchain's ability to facilitate peer-to-peer transactions without intermediaries challenges traditional payment networks.

- Remittance market impact: Lower fees and faster settlement times for cross-border transfers offered by crypto could attract users away from conventional services.

- Lending and borrowing innovation: Decentralized finance (DeFi) platforms built on blockchain offer alternative avenues for lending and borrowing, potentially bypassing traditional banks.

- Growing user adoption: While not yet mainstream for daily banking, the increasing number of cryptocurrency users signifies a growing segment willing to explore alternative financial services.

Substitutes Threaten Traditional Banking Dominance

The threat of substitutes for Svenska Handelsbanken is multifaceted, encompassing fintech innovations, challenger banks, alternative financing, corporate treasury functions, and cryptocurrencies. These substitutes offer convenience, lower costs, and specialized services that challenge traditional banking models. For instance, Swish in Sweden provides instant mobile payments, directly competing with Handelsbanken's payment services.

Entrants Threaten

High Regulatory Barriers to Entry

The banking sector, including Svenska Handelsbanken, faces substantial regulatory hurdles. Finansinspektionen, Sweden's financial supervisory authority, along with EU-level directives, mandates rigorous licensing, capital adequacy, and compliance procedures. For instance, the Common Equity Tier 1 (CET1) ratio, a key measure of a bank's financial strength, must be maintained at specific levels, requiring significant upfront capital investment.

Significant Capital Requirements

Establishing a bank, even a digital-first one, demands immense capital. Regulatory bodies mandate significant minimum capital reserves, and building the required technological infrastructure, cybersecurity measures, and operational frameworks necessitates substantial upfront investment. For instance, in 2024, new challenger banks often require hundreds of millions of dollars to secure licenses and launch competitive services.

Brand Loyalty and Customer Relationships

Established banks like Handelsbanken leverage significant brand loyalty and deep customer relationships, making it difficult for new entrants to gain traction. In 2024, Handelsbanken continued to emphasize its relationship-based banking model, which fosters strong customer retention. This inherent loyalty, built over decades, acts as a substantial barrier, as new players struggle to replicate the trust and personalized service that existing customers value.

Economies of Scale and Scope

Svenska Handelsbanken, like other established banks, benefits significantly from economies of scale. Its vast customer base and extensive branch network, operating across multiple countries, allow for significant cost efficiencies in areas like IT infrastructure, marketing, and regulatory compliance. For instance, in 2023, Handelsbanken reported a cost-to-income ratio of 42%, a testament to its operational efficiency driven by scale.

New entrants face a substantial hurdle in matching these economies of scale. Building a comparable infrastructure and customer base requires immense capital investment and time, making it difficult to compete on cost. This cost disadvantage can deter potential new players from entering the market or force them to operate with thinner margins initially.

Furthermore, Handelsbanken leverages economies of scope by offering a comprehensive suite of financial products and services, from retail banking and mortgages to corporate finance and wealth management. This integrated offering creates cross-selling opportunities and strengthens customer loyalty. New entrants typically start with a narrower product range, limiting their ability to achieve similar synergistic benefits.

- Economies of Scale: Established banks like Handelsbanken benefit from lower per-unit costs due to their large operational size, impacting everything from technology investments to risk management systems.

- Economies of Scope: Offering a wide array of financial products allows incumbent banks to spread costs across different services and create bundled value for customers.

- Cost Disadvantage for New Entrants: Start-ups must invest heavily to build scale and scope, putting them at an immediate cost disadvantage compared to established players.

- Barriers to Entry: The significant capital and time required to achieve comparable efficiencies act as a substantial barrier, limiting the threat of new entrants.

Technological Advancements by Incumbents and Fintech Competition

Technological advancements by incumbents like Handelsbanken, which is investing heavily in digital transformation and AI, can indeed create new barriers for potential entrants. For instance, Handelsbanken's focus on enhancing customer experience through digital channels aims to raise the bar for technological sophistication. However, the persistent rise of challenger banks and specialized fintechs, often targeting niche markets or specific services, demonstrates that new, agile business models are continuously finding pathways to enter the financial services landscape, despite these incumbent efforts.

The threat of new entrants for Svenska Handelsbanken is nuanced by the dual nature of technological advancements. While incumbent banks can leverage technology to build stronger competitive moats, the very same innovations can lower barriers for nimble fintechs. For example, in 2024, the European fintech sector continued to see significant investment, with over €20 billion raised across various segments, indicating a vibrant ecosystem of potential new competitors. These new players often exploit gaps in traditional banking services or offer superior digital user experiences, posing a direct challenge.

- Incumbent Innovation as a Barrier: Handelsbanken's strategic investments in digital transformation and AI are designed to enhance its own service offerings, thereby increasing the technological and operational standards that new entrants must meet.

- Fintech Entry Strategies: Despite incumbent efforts, challenger banks and specialized fintech firms continue to emerge, often by focusing on underserved market segments or by offering highly specialized, user-friendly digital solutions.

- Market Dynamics: The ongoing influx of fintech innovation means that while incumbents can raise the bar, the threat of new entrants remains dynamic, requiring continuous adaptation and investment in technology to maintain competitive advantage.

Moderate Threat: Banking Entry Barriers Persist

The threat of new entrants for Svenska Handelsbanken is moderate, primarily due to significant regulatory capital requirements and the established brand loyalty of incumbent banks. For instance, in 2024, obtaining a banking license in Sweden still necessitates substantial capital reserves and adherence to strict compliance frameworks, making it a high-cost endeavor for startups.

New entrants face considerable challenges in replicating the economies of scale and scope enjoyed by established players like Handelsbanken. The bank's extensive branch network and broad product offering, developed over decades, create cost efficiencies and customer stickiness that are difficult and expensive for newcomers to match. This inherent cost disadvantage for new entrants acts as a significant deterrent.

While technological advancements can lower some barriers, particularly for agile fintechs, incumbents are also investing heavily in digital transformation. Handelsbanken's ongoing commitment to enhancing its digital platforms and customer experience in 2024 aims to further solidify its market position, requiring new entrants to demonstrate a comparable level of technological sophistication and service quality to gain market share.

Porter's Five Forces Analysis Data Sources

Our Svenska Handelsbanken Porter's Five Forces analysis is built upon a foundation of robust data, including Handelsbanken's official annual reports, investor presentations, and regulatory filings. We supplement this with industry-specific research from reputable financial data providers and macroeconomic indicators to capture the broader competitive landscape.