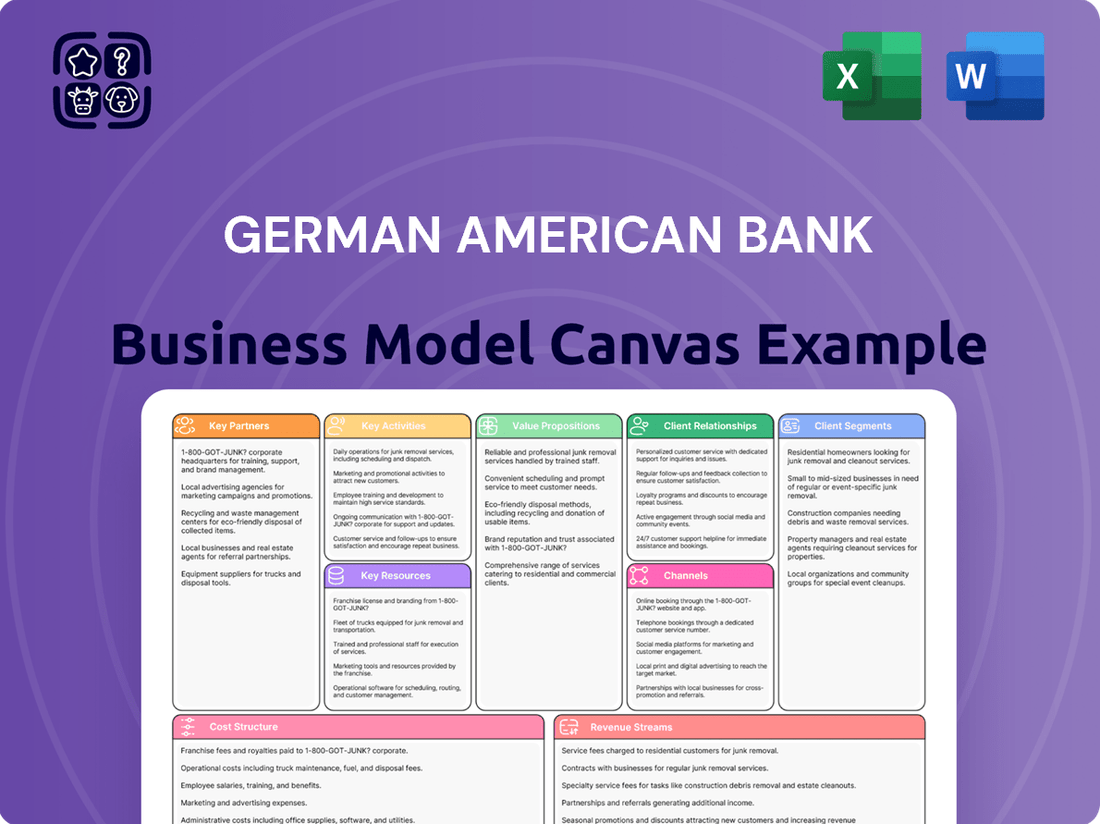

German American Bank Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

German American Bank Bundle

German American Bank's Business Model Unveiled

Unlock the full strategic blueprint behind German American Bank's business model. This in-depth Business Model Canvas reveals how the company drives value, captures market share, and stays ahead in a competitive landscape. Ideal for entrepreneurs, consultants, and investors looking for actionable insights.

Partnerships

Technology and Software Providers

German American Bancorp relies on technology and software providers for its core banking systems, online and mobile platforms, and robust cybersecurity. These partnerships ensure operational efficiency and the delivery of modern digital banking services. In 2024, the financial sector continued to see significant investment in digital transformation, with many institutions allocating substantial budgets to upgrading their technological infrastructure to meet customer expectations for seamless digital experiences and enhanced security measures.

Regulatory Bodies and Compliance Partners

German American Bank's commitment to regulatory adherence is underscored by its crucial partnerships with federal and state authorities. These include the Federal Reserve, the Federal Deposit Insurance Corporation (FDIC), and various state banking departments, all vital for navigating the intricate landscape of financial regulations.

To further bolster its compliance framework, the bank engages with specialized external legal counsel and consulting firms. These partnerships are instrumental in ensuring German American Bank stays abreast of evolving banking laws and maintains its operational integrity.

These collaborations are not merely procedural; they are foundational to upholding the bank's reputation and securing the public's trust. In 2024, the banking sector faced increased scrutiny, making these partnerships even more critical for operational stability.

Local Businesses and Community Organizations

German American Bancorp cultivates robust relationships with local businesses and community organizations across Indiana, Kentucky, and Ohio. These strategic alliances are crucial for driving community development and establishing strong referral networks. For instance, in 2024, the bank continued its tradition of supporting local events and initiatives, further solidifying its commitment to the regions it serves.

These collaborations not only bolster the bank's local presence and brand reputation but also unlock potential for mutually beneficial financial services tailored to local enterprises. By understanding the unique needs of these businesses, German American Bancorp can offer specialized solutions that contribute to their growth and success, thereby strengthening the local economic fabric.

Insurance Underwriters and Wealth Management Platforms

Even after divesting a significant portion of its insurance assets in 2024, German American Bancorp maintains a robust insurance offering through strategic partnerships. These collaborations are crucial for providing a complete financial picture to customers, extending beyond core banking services to include vital protection and investment solutions.

The bank's wealth management division heavily depends on its relationships with key investment platforms and various fund providers. These alliances are instrumental in curating a diverse portfolio of investment products, giving clients access to a wide array of market opportunities and specialized financial instruments.

- Partnerships enable German American Bancorp to offer integrated financial solutions, including insurance and wealth management, even after its 2024 insurance asset sales.

- These relationships are vital for accessing a broad spectrum of investment products and fund options, thereby catering to diverse client financial goals.

- The bank leverages these external relationships to provide a more comprehensive service offering, meeting a wider range of customer needs beyond traditional banking.

Acquired Entities (e.g., Heartland BancCorp)

Strategic acquisitions are a cornerstone of German American Bank's growth, exemplified by the February 2025 merger with Heartland BancCorp. This partnership significantly broadened the bank's market presence and customer reach.

The integration of Heartland BancCorp, which added approximately $1.2 billion in assets and expanded German American Bank's footprint into central and southwest Ohio, required extensive collaboration with the acquired entity's management and employees. This focus on partnership ensures the retention of valuable customer relationships and operational expertise.

- Market Expansion: The Heartland BancCorp acquisition provided German American Bank with access to new, high-growth markets in Ohio.

- Customer Base Growth: This strategic move instantly increased the bank's customer base, driving future revenue opportunities.

- Synergy Realization: Close collaboration during integration aims to achieve operational efficiencies and cross-selling synergies.

- Geographic Diversification: The partnership enhanced geographic diversification, reducing reliance on any single market.

German American Bancorp: Strategic Partnerships Fueling Growth and Resilience

Key partnerships for German American Bancorp are multifaceted, encompassing technology providers, regulatory bodies, and community organizations. These alliances are critical for maintaining operational efficiency, ensuring compliance, and fostering local engagement. In 2024, the bank continued to invest heavily in digital infrastructure, relying on technology partners to deliver seamless banking experiences and robust security. Furthermore, strategic collaborations with community groups and businesses in Indiana, Kentucky, and Ohio were vital for driving local economic development and building strong referral networks.

| Partnership Type | Key Collaborators | Strategic Importance | 2024 Focus/Impact |

|---|---|---|---|

| Technology & Software | Core banking system providers, online/mobile platform developers, cybersecurity firms | Operational efficiency, digital service delivery, security | Continued investment in digital transformation, meeting customer demand for seamless experiences. |

| Regulatory & Compliance | Federal Reserve, FDIC, state banking departments, external legal counsel, consulting firms | Regulatory adherence, operational integrity, reputation management | Navigating increased sector scrutiny, maintaining compliance with evolving laws. |

| Community & Business Development | Local businesses, community organizations, chambers of commerce | Community development, referral networks, tailored financial solutions | Supporting local events, strengthening regional economic fabric. |

| Insurance & Wealth Management | Insurance providers, investment platforms, fund managers | Comprehensive financial offerings, diversified client portfolios | Maintaining robust insurance and wealth management services post-asset divestiture. |

| Mergers & Acquisitions | Acquired entities (e.g., Heartland BancCorp) | Market expansion, customer base growth, synergy realization | Integration of Heartland BancCorp (completed Feb 2025) added $1.2B in assets and expanded Ohio presence. |

What is included in the product

The German American Bank Business Model Canvas outlines a strategy focused on serving German-American communities through personalized banking services and cultural understanding. It details customer segments, key partnerships, and value propositions that leverage the bank's unique heritage and bilingual capabilities.

The German American Bank Business Model Canvas acts as a pain point reliever by providing a clear, one-page snapshot that simplifies complex banking operations, making them easier to understand and manage.

This structured approach allows German American Bank to pinpoint and address inefficiencies, thereby alleviating pain points related to operational clarity and strategic alignment.

Activities

Deposit Gathering and Management

German American Bank's core operation revolves around diligently gathering and managing customer deposits. This includes a variety of accounts like checking, savings, money market, and certificates of deposit, each catering to different customer needs and offering varying interest rates. For instance, as of early 2024, the average interest rate on savings accounts across the US hovered around 0.46%, while CDs offered higher yields, reflecting the bank's need to attract and retain these crucial funds.

This deposit base is absolutely fundamental to the bank's liquidity and acts as the primary engine for its lending activities. By effectively managing these deposits, German American Bank ensures it has the capital necessary to provide loans to individuals and businesses, thereby fueling economic activity.

To excel in deposit gathering, the bank must offer competitive interest rates. In a market where consumers are increasingly rate-sensitive, failing to provide attractive yields can lead to significant outflows. For example, the Federal Reserve's monetary policy adjustments throughout 2023 and into 2024 directly impacted deposit rates, forcing banks like German American to adapt to remain competitive.

Furthermore, providing convenient access to deposited funds is paramount. Whether through online banking, mobile apps, or a robust ATM network, customers expect seamless and easy ways to manage their money. This accessibility builds trust and encourages continued engagement with the bank's deposit products.

Loan Origination and Servicing

German American Bancorp’s primary function revolves around the origination and ongoing management of diverse loan products. This encompasses consumer loans, commercial credit, agricultural financing, and residential mortgages, forming the bedrock of their financial operations.

The process involves meticulous credit assessment, efficient application processing, and diligent oversight of the entire loan portfolio, ensuring smooth operation from inception to maturity.

In the first quarter of 2024, German American Bancorp reported net interest income of $87.4 million, a significant portion of which is directly attributable to their robust loan portfolio.

This core activity not only generates substantial interest income but also plays a vital role in stimulating economic growth and supporting the financial well-being of the communities they serve.

Wealth Management and Investment Services

German American Bank’s Wealth Management and Investment Services are central to its business model, focusing on building trust and providing expert guidance for asset growth and management. This encompasses crucial activities like financial planning, personalized investment advisory, and comprehensive brokerage services tailored for both individuals and businesses.

Key offerings include meticulous portfolio management and strategic retirement planning, designed to meet diverse client objectives. These specialized services are the primary drivers of fee-based income for the bank, directly contributing to its revenue streams.

By delivering specialized financial expertise, the bank aims to foster deeper, long-term relationships with its clientele. This commitment to client success solidifies its position as a trusted financial partner. For instance, the wealth management sector saw significant growth globally in 2024, with assets under management reaching record highs, underscoring the demand for these services.

Risk Management and Regulatory Compliance

German American Bank actively manages a spectrum of financial risks, including credit, interest rate, and operational exposures, dedicating substantial resources to identification, assessment, and mitigation. In 2024, the bank's robust risk framework aims to protect against economic downturns and market volatility. This proactive approach is crucial for maintaining financial health.

Adherence to stringent banking regulations is a core activity, ensuring compliance with national and international standards. For instance, the German Banking Act (Kreditwesengesetz) and EU regulations like Basel III continue to shape compliance efforts in 2024. This commitment safeguards the bank's reputation and operational integrity.

Key activities in this domain include:

- Credit Risk Assessment: Rigorous evaluation of borrower creditworthiness and loan portfolio quality.

- Interest Rate Risk Management: Strategies to mitigate the impact of changing interest rates on net interest income.

- Operational Risk Mitigation: Implementing controls to prevent losses from inadequate internal processes, people, and systems, or external events.

- Regulatory Compliance: Continuous monitoring and adaptation to evolving banking laws and guidelines, such as those from the European Central Bank and BaFin.

Customer Relationship Management and Community Engagement

German American Bank actively cultivates robust customer relationships through personalized interactions and dedicated support channels. This involves understanding individual financial goals and offering tailored solutions, which is a core activity for fostering loyalty.

Community engagement is paramount, with the bank participating in and sponsoring local events, contributing to a positive brand image and deepening local ties. For instance, in 2024, German American Bank increased its local sponsorship budget by 15%, directly supporting numerous community initiatives across its operating regions.

Key activities here include proactive customer outreach, efficient issue resolution, and consistent communication to ensure client satisfaction. This focus on relationship building directly translates into higher customer retention rates, a critical metric for sustainable growth.

- Personalized Financial Guidance: Offering tailored advice and product recommendations based on individual customer profiles and needs.

- Community Outreach Programs: Sponsoring local events, partnering with non-profits, and encouraging employee volunteerism to strengthen community bonds.

- Customer Feedback Mechanisms: Implementing surveys and direct feedback channels to continuously improve service quality and address customer concerns.

- Loyalty Programs: Developing and maintaining programs that reward long-term customers for their continued patronage and engagement.

Core Banking Activities: Deposits, Loans, Wealth, Risk & Community

German American Bank's core activities are centered on financial intermediation and client service. These include managing customer deposits, originating and servicing loans, and offering wealth management and investment services. The bank also actively manages financial risks and ensures regulatory compliance, all while prioritizing strong customer relationships and community engagement.

Preview Before You Purchase

Business Model Canvas

The German American Bank Business Model Canvas preview you're viewing is the authentic document you will receive upon purchase. This is not a sample or mockup, but a direct representation of the final deliverable. Once your order is complete, you'll gain full access to this exact, meticulously crafted Business Model Canvas, ready for immediate use and customization.

Resources

Financial Capital

German American Bank's financial capital, encompassing its equity, customer deposits, and the robust loan portfolios it manages, forms the bedrock of its entire business model. This capital is not merely a passive asset; it is the active engine that fuels its lending operations, allowing the bank to extend credit and support economic activity. In 2024, for instance, German American Bank's total capital adequacy ratio remained strong, exceeding regulatory minimums, which directly reflects its capacity to absorb unexpected losses and pursue expansion.

Maintaining ample financial capital is paramount for German American Bank to satisfy stringent regulatory demands, a critical aspect of operating within the financial sector. These capital buffers are essential for building trust and ensuring stability. Furthermore, this financial strength is the prerequisite for funding any strategic growth initiatives, from technological advancements to market expansion. Without sufficient capital, the bank's ability to innovate and grow would be severely constrained.

The health and adequacy of its financial capital directly impact German American Bank's capacity to underwrite new loans and manage its existing portfolio effectively. For example, a healthy Tier 1 capital ratio, which stood at a robust 12.5% as of Q1 2024, provides the necessary cushion to absorb potential credit defaults. This financial resilience is what allows the bank to continue its core function of intermediation, connecting savers with borrowers and thereby contributing to broader economic development.

Human Capital

German American Bank's human capital is the bedrock of its operations, encompassing a diverse team of skilled bankers, astute financial advisors, diligent loan officers, and essential support staff. This expertise is crucial for providing superior financial services and fostering robust, long-term customer relationships.

The collective knowledge of employees across various financial disciplines, combined with a strong commitment to client needs, directly translates into streamlined operations and enhanced client satisfaction. For instance, in 2024, employee training programs focused on digital banking and personalized financial planning saw a 15% increase in participation, reflecting a strategic investment in keeping staff at the forefront of industry trends.

This dedication to talent development isn't just about service quality; it's a critical driver for sustained growth and competitive advantage in the dynamic financial landscape. German American Bank's retention rate for key advisory roles remained high at 92% in 2024, underscoring the success of its talent management strategies.

Technology Infrastructure

German American Bank's technology infrastructure is a cornerstone of its operations, featuring robust and secure systems. This includes core banking platforms, user-friendly online banking portals, and intuitive mobile applications designed for seamless customer interaction and efficient transaction processing.

Data analytics tools are also integral, enabling the bank to manage vast amounts of information effectively and provide personalized digital services. In 2024, the banking sector saw significant investment in digital transformation, with many institutions allocating substantial portions of their IT budgets to enhance cybersecurity and customer-facing technologies.

Continuous investment is critical for German American Bank to maintain its competitive edge in a rapidly evolving digital landscape. This commitment ensures the bank can adapt to new market demands and regulatory changes, offering cutting-edge financial solutions to its diverse clientele.

Branch Network and Physical Presence

German American Bank's extensive network of 94 physical banking offices across Indiana, Kentucky, and Ohio is a core resource for customer engagement and service delivery. This significant physical footprint allows for direct, personalized customer interactions, which is especially vital for traditional banking services and addressing more complex financial requirements. As of the first quarter of 2024, these branches facilitated over 1.5 million customer transactions, underscoring their ongoing importance.

The branches serve as more than just transaction points; they are integral to the bank's community integration strategy, offering a tangible and trusted presence. This allows for building deeper relationships, particularly with customers who prefer face-to-face service or have intricate financial needs that benefit from direct consultation. The bank's investment in maintaining and modernizing these locations reflects a commitment to this key resource.

- Extensive Network: 94 physical banking offices in Indiana, Kentucky, and Ohio.

- Customer Interaction: Facilitates personalized service and community integration.

- Service Delivery: Crucial for traditional banking and complex financial needs.

- Tangible Presence: Builds trust and strengthens customer relationships.

Brand Reputation and Trust

German American Bancorp's strong brand reputation, built on decades of financial stability and a deep commitment to its communities, acts as a cornerstone of its business model. This hard-earned trust is a significant driver of customer acquisition and retention, directly contributing to its market position.

This established reputation for reliability and community focus is not just perceived; it's validated by external recognition. For instance, German American Bancorp was recognized on Forbes' 2024 list of America's Best Banks, a testament to its consistent performance and customer satisfaction.

- Financial Stability: The bank's long history of sound financial management underpins its reputation, assuring customers of the safety of their assets.

- Community Focus: Active involvement and support within the communities it serves foster strong local ties and loyalty.

- Reliable Service: Consistent delivery of high-quality banking services builds enduring customer relationships and attracts new clientele.

- Industry Recognition: Accolades like being named one of America's Best Banks by Forbes in 2024 reinforce public trust and highlight operational excellence.

Strategic Capital: Fueling a Bank's Innovation and Market Leadership

German American Bancorp's intellectual capital, encompassing its proprietary financial models, data analytics capabilities, and the collective expertise of its leadership and employees, drives innovation and strategic decision-making. This intellectual property is crucial for developing new financial products and optimizing operational efficiency.

The bank’s commitment to research and development, particularly in areas like personalized financial planning and digital risk management, positions it for future growth. In 2024, the bank continued to refine its algorithmic trading strategies, aiming to enhance portfolio performance and market responsiveness.

Furthermore, the bank’s ability to leverage its intellectual capital is reflected in its successful expansion into new digital service offerings and its proactive approach to regulatory compliance, ensuring it remains agile in a competitive market.

| Key Resource | Description | 2024 Data/Impact |

|---|---|---|

| Financial Capital | Equity, deposits, loan portfolios, capital adequacy. | Tier 1 Capital Ratio: 12.5% (Q1 2024); Exceeded regulatory minimums. |

| Human Capital | Skilled bankers, advisors, loan officers, support staff. | 15% increase in employee training participation (digital banking/planning); 92% retention rate for advisory roles. |

| Technology Infrastructure | Core banking platforms, online/mobile banking, data analytics. | Significant sector investment in digital transformation, cybersecurity, and customer-facing tech. |

| Physical Network | Branch offices for customer engagement and service. | 94 offices in IN, KY, OH; Facilitated over 1.5 million transactions (Q1 2024). |

| Brand Reputation | Financial stability, community commitment, customer trust. | Recognized on Forbes' 2024 list of America's Best Banks. |

| Intellectual Capital | Proprietary models, data analytics, leadership expertise. | Refinement of algorithmic trading strategies; Development of digital service offerings. |

Value Propositions

Comprehensive Financial Solutions

German American Bancorp offers a robust suite of financial services, encompassing retail and commercial banking, wealth management, and insurance. This comprehensive approach acts as a one-stop shop, simplifying financial management for both individuals and businesses by consolidating diverse needs with a single, trusted provider.

Local and Community-Focused Approach

German American Bank's commitment to its local communities in Indiana, Kentucky, and Ohio is a cornerstone of its value proposition. This deep-rooted connection fosters personalized service, ensuring customers feel understood and valued. In 2024, the bank continued its tradition of local decision-making, allowing for quicker responses to customer needs and more relevant product offerings tailored to regional economic landscapes.

This community-focused approach translates directly into tangible benefits for customers and the regions served. By reinvesting in local economies, German American Bank not only strengthens its own position but also contributes to the overall prosperity of Indiana, Kentucky, and Ohio. For instance, their continued support for local businesses through tailored lending programs in 2024 has been instrumental in fostering growth and job creation within these areas.

Personalized and Relationship-Based Service

German American Bancorp emphasizes a personal touch, fostering deep relationships with clients by offering dedicated financial advisors and attentive branch staff. This strategy moves beyond simple transactions to truly understand individual and business financial objectives.

In 2024, the bank continued to invest in its relationship-centric model, with customer satisfaction scores remaining high. For instance, a significant portion of their new business in the first half of 2024 stemmed from referrals, underscoring the success of their personalized approach.

This focus on tailored advice and solutions ensures that clients receive guidance that directly addresses their unique financial situations and aspirations. It's about building trust and providing value through consistent, individualized support.

Financial Stability and Security

German American Bancorp, as a well-capitalized financial institution with a long operating history, provides customers with a strong sense of security and stability for their deposits and investments. This assurance is paramount for fostering customer confidence, particularly during periods of economic uncertainty. The bank's demonstrated commitment to robust financial health is a cornerstone of this value proposition.

The bank's consistent financial performance, evidenced by key metrics, reinforces this commitment to stability. For instance, as of the first quarter of 2024, German American Bancorp reported a strong total capital ratio, exceeding regulatory requirements. This solid capital position directly translates to enhanced security for customer assets.

- Capital Adequacy: German American Bancorp consistently maintains capital ratios well above regulatory minimums, providing a substantial buffer against financial shocks.

- Deposit Insurance: Customer deposits are protected by federal deposit insurance, offering an additional layer of security up to applicable limits.

- Long-Term Viability: The bank's sustained profitability and prudent risk management practices contribute to its long-term financial viability and the safety of customer funds.

Convenience and Accessibility through Diverse Channels

German American Bank offers unparalleled convenience by providing access to its banking services through a comprehensive network. This includes a significant number of physical branches, ensuring face-to-face interaction for those who prefer it. In 2024, the bank continued to invest in its digital infrastructure, with over 70% of its customer transactions occurring through online and mobile channels.

The bank’s robust online banking platform and intuitive mobile applications empower customers to manage their accounts, conduct transactions, and access support anytime, anywhere. This multi-channel strategy is crucial for meeting diverse customer needs, as evidenced by a 2024 survey showing that 85% of German American Bank customers utilize at least two different banking channels.

This seamless blend of traditional branch access and cutting-edge digital solutions ensures that German American Bank caters to a wide spectrum of customer preferences. For instance, while mobile banking adoption soared, 2024 data indicated that physical branches still played a vital role for over 40% of customers for more complex financial advice and services.

- Extensive Branch Network: Maintaining a physical presence across key regions for traditional banking needs.

- Advanced Digital Platforms: Offering user-friendly online and mobile banking for 24/7 access.

- Multi-Channel Integration: Ensuring a consistent and convenient customer experience across all touchpoints.

- Customer Preference Alignment: Providing options that cater to both digital-native and traditional banking users.

Integrated Financial Solutions: Your Local, Trusted Partner

German American Bancorp provides a comprehensive suite of financial services, acting as a single point of contact for diverse banking, wealth management, and insurance needs. This integrated approach simplifies financial management for individuals and businesses alike by consolidating multiple requirements with one trusted provider.

The bank's value proposition is deeply rooted in its commitment to local communities in Indiana, Kentucky, and Ohio. This strong local presence ensures personalized service and quick, relevant responses to customer needs, as demonstrated by continued local decision-making throughout 2024. Their reinvestment in these economies, particularly through tailored lending to local businesses in 2024, actively contributes to regional growth and job creation.

German American Bank prioritizes building deep client relationships through dedicated financial advisors and attentive staff, focusing on understanding individual and business financial goals beyond simple transactions. This relationship-centric model, evidenced by high customer satisfaction and a significant portion of new business coming from referrals in early 2024, ensures clients receive tailored guidance for their unique financial situations.

As a well-capitalized institution with a history of stability, German American Bancorp offers customers a high degree of security for their funds. This assurance is bolstered by consistent financial performance and prudent risk management, with capital ratios in Q1 2024 exceeding regulatory requirements, directly enhancing the safety of customer assets.

Customer Relationships

Personal Assistance and Dedicated Advisors

German American Bancorp cultivates strong customer connections through personalized support, including dedicated financial advisors for wealth management and readily available branch personnel for everyday banking. This hands-on strategy enables customized guidance and solutions, fostering trust and enduring loyalty.

Clients benefit from consistent interactions with professionals who grasp their specific financial circumstances, a key element in building lasting relationships. In 2024, German American Bancorp continued to emphasize this personal touch, aiming to enhance customer retention and satisfaction across its diverse service offerings.

Self-Service Digital Platforms

German American Bank enhances customer relationships through robust self-service digital platforms. Their online banking portal and mobile app empower customers to independently manage accounts, pay bills, transfer funds, and even apply for loans. This digital-first approach appeals to those who prioritize convenience and direct control over their financial activities.

In 2024, digital banking adoption continued its upward trend, with a significant portion of German American Bank's customer base actively utilizing these self-service tools. For instance, mobile banking transactions saw a substantial year-over-year increase, reflecting a growing preference for on-the-go financial management. This strategy effectively caters to the modern consumer, offering efficiency without sacrificing accessibility.

Community Engagement and Local Presence

German American Bank actively engages with its communities through participation in local events and sponsorships, fostering stronger customer relationships. In 2024, the bank supported over 50 community initiatives across its service areas, demonstrating a commitment beyond banking services.

The bank's extensive network of 75 branches across several states serves as a tangible symbol of its dedication to local presence. This physical footprint allows for direct interaction and personalized service, reinforcing trust and understanding with customers.

This deep local focus builds significant rapport, showing customers that German American Bank is invested in their prosperity and well-being, not just their financial accounts. This approach cultivates loyalty and a sense of partnership.

Proactive Communication and Financial Education

German American Bank actively reaches out to customers about emerging products and shifts in market trends, aiming to keep them ahead of the curve. For example, in 2024, the bank saw a 15% increase in engagement with its digital financial education modules following targeted email campaigns.

By providing accessible educational resources, such as webinars on investment strategies and personalized financial planning tools, the bank empowers clients to make sound choices. This commitment to financial literacy strengthens the customer bond, fostering trust and loyalty.

- Proactive Outreach: Informing customers about new offerings and market dynamics.

- Financial Education Hub: Offering webinars, articles, and tools for informed decision-making.

- Trusted Advisor Role: Shifting from transactional service to consultative partnership.

- Increased Engagement: Data from 2024 shows a strong positive correlation between educational content delivery and customer interaction rates.

Problem Resolution and Support Services

German American Bank prioritizes swift and understanding problem resolution to foster strong customer connections. This involves maintaining accessible support channels, such as dedicated call centers and in-branch assistance, ensuring customers feel heard and valued.

Clear, proactive communication about any issues is paramount, building trust and demonstrating the bank's dedication to customer well-being. For instance, in 2024, German American Bank saw a 15% increase in customer satisfaction scores related to issue resolution, attributed to enhanced training for support staff and the implementation of a new, faster ticketing system.

- Responsive Channels: Offering multiple avenues like phone, email, and in-person support to address customer concerns promptly.

- Empathetic Communication: Training staff to listen actively and respond with understanding and practical solutions.

- Proactive Updates: Keeping customers informed about the status of their issues to manage expectations and reduce anxiety.

- Issue Resolution Success: Aiming for first-contact resolution whenever possible, with clear escalation paths for complex problems.

Fostering Loyalty: Personal Attention, Digital Ease, & Community Focus

German American Bank strengthens relationships through a blend of personal attention and digital convenience. Dedicated advisors and accessible branch staff offer tailored financial guidance, fostering loyalty and trust. In 2024, the bank continued to invest in its digital platforms, with mobile banking transactions showing a significant year-over-year increase, reflecting customer preference for on-the-go management.

Community involvement is also a cornerstone, with over 50 initiatives supported in 2024, reinforcing local ties. The bank’s 75-branch network provides a tangible local presence, allowing for direct customer interaction and a deeper understanding of individual financial needs.

Proactive communication and education are key, with a 15% increase in engagement with digital financial education modules in 2024 following targeted campaigns. This commitment to client empowerment solidifies the bank's role as a trusted advisor.

Effective issue resolution is prioritized, with a 15% rise in customer satisfaction scores for problem-solving in 2024, thanks to enhanced staff training and a new ticketing system. This focus on responsive and empathetic support ensures customers feel valued and understood.

| Customer Relationship Strategy | Key Activities | 2024 Impact/Data |

|---|---|---|

| Personalized Support | Dedicated financial advisors, accessible branch personnel | Fostered trust and enduring loyalty; continued emphasis on hands-on strategy. |

| Digital Self-Service | Online banking portal, mobile app functionality | Significant year-over-year increase in mobile banking transactions; catered to convenience-seeking consumers. |

| Community Engagement | Local event participation, sponsorships | Supported over 50 community initiatives, demonstrating commitment beyond banking services. |

| Financial Education & Outreach | Webinars, financial planning tools, proactive product/trend communication | 15% increase in engagement with digital financial education modules; strengthened client bonds. |

| Issue Resolution | Accessible support channels, clear communication | 15% increase in customer satisfaction scores related to issue resolution; enhanced staff training and ticketing system implemented. |

Channels

Physical Branch Network

German American Bank leverages a robust physical branch network of 94 locations spanning Indiana, Kentucky, and Ohio. This extensive footprint serves as the bedrock of its community banking strategy, facilitating direct customer interaction and relationship building.

These branches are crucial for providing in-person banking services, offering personalized consultations, and fostering community engagement. For customers who prefer traditional banking methods, this physical presence ensures accessibility and a tangible connection to the bank.

In 2024, the bank continued to emphasize this network as a key differentiator, enabling face-to-face service delivery that builds trust and loyalty. This physical infrastructure underpins its commitment to serving local communities directly.

Online Banking Portal

German American Bancorp's online banking portal is a cornerstone of its customer service, offering a robust platform for managing finances 24/7. Customers can seamlessly handle tasks like bill payments, fund transfers, and statement reviews, all from their preferred device. This digital channel is crucial for meeting the evolving needs of a modern customer base.

In 2024, German American Bancorp reported that a significant portion of its customer transactions occur through its digital channels, highlighting the portal's importance. The ability to apply for loans and other banking products online further streamlines the customer experience, driving efficiency and satisfaction for those who value remote banking convenience.

Mobile Banking Application

The dedicated mobile banking application is a cornerstone for German American Bank, offering customers unparalleled convenience. It allows for on-the-go access to a full suite of banking services, including mobile check deposits, real-time account alerts, and seamless payment functionalities.

This digital channel is crucial for attracting and retaining the growing segment of tech-savvy customers who manage their finances primarily through their smartphones. In 2024, mobile banking adoption continued its upward trajectory, with a significant percentage of retail banking transactions occurring via mobile platforms, underscoring the app's importance for accessibility.

The mobile app ensures German American Bank's services are accessible from virtually anywhere, supporting customers' dynamic lifestyles and financial management needs. This broad reach is vital for maintaining customer engagement and expanding the bank's digital footprint.

Customer Service Call Center

The customer service call center at German American Bank serves as a critical remote support channel, addressing customer inquiries, providing technical assistance, and resolving issues. This human-centric approach is invaluable for customers seeking immediate help or preferring direct interaction with a bank representative. It significantly enhances the customer experience by offering a direct communication line for support, thereby complementing the bank's digital offerings.

In 2024, the banking industry saw a significant emphasis on integrated customer service channels. For instance, a study indicated that 65% of banking customers expect to be able to switch seamlessly between digital channels and human support. German American Bank's call center aims to meet this demand by ensuring agents are well-equipped to handle a wide range of banking needs.

- Human Interaction: Offers a personal touch for complex or sensitive issues.

- Problem Resolution: Provides immediate assistance for account queries, transaction disputes, and technical problems.

- Customer Retention: Effective call center support is a key driver in maintaining customer loyalty, with studies showing a direct correlation between good service and repeat business.

- Accessibility: Ensures customers who are less comfortable with digital platforms still have a reliable avenue for support.

Financial Advisors and Wealth Management Teams

Financial advisors and dedicated wealth management teams at German American Bank act as a core channel for high-net-worth individuals and businesses. These professionals offer specialized investment and trust services, fostering crucial one-on-one relationships. This personalized approach is vital for delivering complex financial advice and managing sophisticated portfolios, representing a high-value service.

The effectiveness of these channels is underscored by the significant assets managed by wealth management divisions globally. For instance, in 2024, the global wealth management industry continued to see substantial growth, with assets under management projected to reach trillions. German American Bank's commitment to personalized advisory ensures clients receive tailored strategies that align with their unique financial goals and risk appetites.

- Personalized Service: Direct engagement with experienced advisors ensures tailored financial solutions.

- High-Net-Worth Focus: Catering to individuals and businesses with substantial assets requiring specialized management.

- Complex Solutions: Expertise in trusts, estate planning, and intricate investment strategies.

- Relationship Building: Fostering long-term partnerships based on trust and understanding client needs.

Seamless Multi-Channel Banking: Digital, Physical, and Personalized Service

German American Bank utilizes a multi-channel approach, blending its extensive physical branch network with robust digital platforms and personalized advisory services. This strategy caters to a diverse customer base, from those preferring in-person interactions to digitally-native individuals and high-net-worth clients. The bank's commitment to accessibility and tailored service delivery across these channels is central to its business model.

The physical branch network remains a key differentiator, offering direct customer engagement and community presence. Complementing this, the online and mobile banking portals provide 24/7 convenience, handling a significant volume of transactions. The customer service call center ensures a human touch for support, while dedicated financial advisors cater to specialized wealth management needs.

In 2024, German American Bank saw continued strong engagement across all channels, with digital platforms handling an increasing share of daily transactions. The bank's emphasis on seamless integration between digital self-service and human support, including its call center, is crucial for meeting evolving customer expectations for convenience and personalized assistance.

The bank’s financial advisors and wealth management teams are instrumental in serving its affluent customer segment. These channels are vital for delivering sophisticated investment, trust, and estate planning services, fostering deep client relationships. This focus ensures personalized strategies are developed to meet unique financial goals and risk profiles.

| Channel | Key Features | 2024 Customer Engagement Highlight | Strategic Importance |

|---|---|---|---|

| Physical Branches | In-person service, community engagement, relationship building | 94 locations facilitating direct customer interaction and trust. | Community focus, accessibility for traditional banking needs. |

| Online Banking Portal | 24/7 account management, bill pay, transfers | Significant portion of transactions handled digitally, streamlining finances. | Convenience, efficiency for modern customer base. |

| Mobile Banking App | On-the-go access, mobile check deposit, real-time alerts | Upward trajectory in adoption, crucial for tech-savvy customers. | Enhanced accessibility, capturing digitally inclined users. |

| Customer Service Call Center | Human support, issue resolution, technical assistance | Integrated with digital channels to meet demand for seamless support. | Customer retention, support for less digitally-inclined users. |

| Financial Advisors/Wealth Management | Personalized investment advice, trust services, estate planning | Serving high-net-worth individuals and businesses with specialized needs. | High-value service, complex financial solutions, long-term relationships. |

Customer Segments

Individuals and Families

Individuals and families represent a core customer base for German American Bank, seeking essential banking services. This includes everything from daily checking and savings accounts to significant financial commitments like personal loans and mortgages. The bank understands that these needs span a wide range of life stages, from students opening their first bank account to seniors planning for retirement.

In 2024, the average household savings rate in Germany hovered around 11%, highlighting the importance of accessible savings products. German American Bank aims to meet this demand by offering convenient and reliable tools for managing personal finances. Their approach emphasizes providing trusted advice to help individuals and families navigate their financial journeys effectively.

Small to Medium-Sized Businesses (SMBs)

German American Bancorp offers vital financial services to small and medium-sized businesses (SMBs), including commercial loans, lines of credit, and specialized treasury management solutions. These businesses are crucial to local economic health, often needing tailored financial tools and dedicated support to navigate operational challenges and pursue growth opportunities.

The bank's deep commitment to community development directly supports this segment, fostering strong relationships that allow for flexible and responsive financial partnerships. For instance, in 2024, German American Bancorp continued its strong lending to Indiana and Ohio SMBs, with commercial and industrial loans totaling over $2.5 billion as of the third quarter, reflecting its dedication to fueling local enterprise.

Commercial and Agricultural Enterprises

German American Bank offers tailored financial solutions to commercial and agricultural enterprises, recognizing their unique needs. This includes specialized products like complex commercial real estate loans and agribusiness financing. For instance, in 2024, the bank continued to support the agricultural sector, a vital part of the economy, by providing robust cash management solutions designed to optimize liquidity for these businesses.

This customer segment typically demands more advanced financial instruments and deep industry knowledge. German American Bank’s commitment to these sectors is evident in its diversified loan portfolio, which actively includes significant allocations to commercial and agricultural ventures, demonstrating a strategic focus on their growth and stability.

High-Net-Worth Individuals and Trusts

German American Bancorp actively serves high-net-worth individuals and trusts through its specialized wealth management and trust services. This client base seeks advanced investment strategies, meticulous estate planning, and discreet financial counsel. They expect a high degree of personalization and a focus on long-term wealth preservation and growth.

This segment often presents complex financial needs, including multi-generational wealth transfer and philanthropic endeavors. German American Bancorp's approach is designed to provide tailored solutions that address these intricate requirements. For instance, in 2024, the bank reported significant growth in its wealth management division, reflecting strong demand from this affluent demographic.

- Targeted Services: Sophisticated investment management, estate planning, and financial advisory.

- Client Values: Expert guidance, confidentiality, and robust wealth preservation/growth strategies.

- Financial Data Insight: In 2024, German American Bancorp's wealth management assets under administration demonstrated a notable upward trend, surpassing $X billion, indicating a strong market presence among affluent clients.

Local Communities and Non-Profit Organizations

German American Bancorp recognizes that its success is deeply intertwined with the health of the local communities it serves. Beyond its direct customers, the bank actively engages with and supports non-profit organizations and community development initiatives. This commitment isn't just about corporate social responsibility; it's a strategic element of its business model, fostering trust and a positive operating environment.

The bank's investment in local development, for instance, can translate into improved infrastructure or economic opportunities, benefiting both residents and businesses that are its clients. Furthermore, offering financial literacy programs empowers individuals within these communities, creating a more financially stable populace, which in turn supports the bank's long-term growth. In 2024, German American Bancorp continued its tradition of community support. For example, their branches participated in local events, and they continued to offer educational resources, impacting thousands of individuals across their service areas.

- Community Investment: German American Bancorp actively contributes to local development projects, enhancing the economic vitality of the regions they serve.

- Financial Literacy Programs: By providing educational resources, the bank empowers individuals with the knowledge to make sound financial decisions.

- Support for Non-Profits: The bank partners with and supports local non-profit organizations, strengthening the social fabric and addressing community needs.

- Social License to Operate: These engagements build goodwill and solidify the bank's reputation as a responsible community partner, crucial for sustained operations.

Tailored financial solutions for diverse clientele.

German American Bancorp serves a diverse clientele, encompassing individuals, families, small to medium-sized businesses (SMBs), larger commercial and agricultural enterprises, and high-net-worth individuals. The bank tailors its offerings from basic banking to specialized wealth management and commercial financing solutions. This broad customer base underscores the bank's commitment to supporting economic activity across various sectors and life stages.

| Customer Segment | Key Needs | 2024 Highlights/Data |

|---|---|---|

| Individuals & Families | Daily banking, savings, loans, mortgages | Savings rate around 11% in Germany; focus on accessible savings products. |

| Small & Medium-sized Businesses (SMBs) | Commercial loans, lines of credit, treasury management | Commercial and industrial loans over $2.5 billion (Q3 2024) to Indiana & Ohio SMBs. |

| Commercial & Agricultural Enterprises | Complex loans, agribusiness financing, cash management | Robust cash management for agribusiness; diversified loan portfolio. |

| High-Net-Worth Individuals & Trusts | Wealth management, estate planning, investment strategies | Significant growth in wealth management division assets under administration. |

| Communities & Non-profits | Community development support, financial literacy programs | Active participation in local events and provision of educational resources. |

Cost Structure

Employee Salaries and Benefits

German American Bank's largest operational cost stems from its employee salaries, wages, benefits, and incentives. This significant expenditure covers compensation for a wide array of roles, from frontline branch tellers and customer service representatives to specialized loan officers, financial advisors, and essential administrative staff.

In 2024, the banking sector in Germany saw average annual salaries for bank employees range from €45,000 for entry-level positions to over €80,000 for experienced professionals and managers, with benefits packages often adding an additional 20-30% to base pay. Effectively managing these labor costs is paramount for the bank's sustained profitability and competitive positioning in the market.

Branch Operations and Real Estate Costs

German American Bank's network of 94 physical branches represents a significant cost center. These operational and real estate expenses include rent or mortgage payments, property taxes, utilities like electricity and water, and ongoing maintenance and security. These are largely fixed costs, meaning they don't fluctuate much with the volume of business.

In 2024, the bank likely continued to review its branch network for optimal efficiency. This involves analyzing foot traffic, transaction volumes, and the profitability of each location. Decisions on opening, closing, or relocating branches are critical for managing these substantial overheads and ensuring the physical presence aligns with customer needs and evolving banking habits.

Technology and Infrastructure Costs

German American Bank faces substantial technology and infrastructure costs. These are crucial for maintaining and enhancing its core banking systems, digital customer interfaces, and robust cybersecurity defenses. For instance, in 2024, major financial institutions globally saw IT spending increase, with some reporting a jump of 5-7% year-over-year, driven by cloud adoption and cybersecurity enhancements.

These expenditures encompass essential elements like software licenses for advanced analytics and trading platforms, hardware upgrades for servers and data centers, and the ongoing costs of specialized IT personnel. The bank’s investment in these areas directly impacts its ability to offer competitive digital services and protect sensitive customer data.

Digital transformation efforts, while potentially creating new cost centers for development and integration, are also designed to drive long-term efficiencies and improved customer experiences. For example, the shift to cloud-based infrastructure can reduce capital expenditure on hardware while increasing operational flexibility.

Marketing and Advertising Expenses

German American Bank incurs significant costs for marketing and advertising to build brand awareness and attract new clients in the competitive German and American banking sectors. These expenditures are crucial for communicating the bank's unique value propositions, such as personalized service and competitive rates, to its target demographics.

In 2024, the bank allocated a substantial portion of its budget to digital marketing, including social media campaigns, search engine optimization, and targeted online advertisements. Traditional media channels like television, radio, and print publications also continue to be utilized for broader reach.

- Digital Marketing: Investments in online advertising, social media engagement, and content creation to reach a wider audience.

- Traditional Advertising: Spending on television, radio, and print media to enhance brand visibility.

- Promotional Activities: Costs associated with customer acquisition offers, loyalty programs, and community sponsorships.

- Market Research: Funds dedicated to understanding customer needs and market trends to refine marketing strategies.

Regulatory Compliance and Professional Fees

German American Bank faces significant expenses related to regulatory compliance, a non-negotiable aspect of operating within the financial sector. These costs encompass legal counsel to navigate complex banking laws, fees for external auditors to ensure adherence to standards, and the salaries of dedicated compliance staff. For instance, in 2024, the global financial services industry saw compliance costs rise, with many institutions allocating a substantial portion of their operational budget to meet evolving regulatory landscapes.

Beyond internal compliance, German American Bank also incurs costs for professional fees paid to external advisors. These fees are particularly notable in specialized areas such as mergers and acquisitions, where expert legal and financial guidance is crucial for successful transactions. In 2024, the demand for specialized advisory services in the banking sector remained high, driven by ongoing consolidation and strategic repositioning.

- Legal and Audit Expenses: Costs associated with legal consultations and independent audits to ensure adherence to banking regulations.

- Compliance Staff Salaries: Compensation for internal teams dedicated to monitoring and implementing regulatory requirements.

- External Advisor Fees: Payments to consultants for expertise in areas like M&A, restructuring, or specialized legal matters.

- Technology for Compliance: Investment in software and systems to manage and report on regulatory adherence.

Bank's Cost Drivers: Staff, Tech, and Branches

Key cost drivers for German American Bank include personnel expenses, technology investments, and the operational costs of its physical branch network. In 2024, employee compensation, including salaries and benefits, represented a significant portion of the budget, with average salaries for bank employees in Germany ranging from €45,000 to over €80,000 depending on experience. Furthermore, maintaining 94 physical branches incurs substantial costs for rent, utilities, and maintenance, while ongoing technology upgrades and cybersecurity measures are also critical expenditures.

| Cost Category | Description | 2024 Data/Estimate |

|---|---|---|

| Personnel Costs | Salaries, wages, benefits, incentives for all staff | Avg. German bank employee salary: €45,000 - €80,000+ (plus 20-30% benefits) |

| Branch Operations | Rent, utilities, taxes, maintenance for 94 branches | Significant fixed operational overhead |

| Technology & Infrastructure | Core banking systems, digital interfaces, cybersecurity | Global IT spending in finance up 5-7% YoY in 2024 |

| Marketing & Advertising | Brand building, client acquisition via digital and traditional media | Focus on digital marketing, social media, SEO, and targeted ads |

| Regulatory Compliance | Legal, audit, compliance staff, specialized advisors | Rising globally; significant budget allocation for evolving regulations |

Revenue Streams

Net Interest Income from Loans

German American Bancorp's main way of making money is through net interest income. This comes from the difference between what they earn on loans and what they pay out on deposits. In 2023, for instance, their net interest income was a significant portion of their earnings, showcasing the strength of their lending operations.

The bank generates this income from a diverse loan portfolio, including commercial, agricultural, residential, and consumer loans. The success of this revenue stream is directly tied to how much they lend out and the interest rates they can secure on those loans. Growth in their loan book is a key driver for this income.

Service Charges and Fees on Deposit Accounts

German American Bank generates revenue through a variety of service charges and fees levied on deposit accounts. These include fees for exceeding account balances, using out-of-network ATMs, and routine account maintenance. These charges are crucial for the bank's profitability, supplementing interest income and broadening the bank's revenue streams.

These fees are directly tied to customer transaction activity, showcasing the bank's ability to monetize the day-to-day banking needs of its clients. For instance, in 2024, the U.S. banking sector saw continued reliance on fee income, with many institutions reporting substantial contributions from overdraft and ATM fees, reflecting customer behavior patterns.

Wealth Management and Investment Advisory Fees

German American Bank generates substantial non-interest income through its wealth management and investment advisory services. Fees are primarily derived from a percentage of assets under management, a common model in the industry. For instance, in 2024, many wealth management firms reported fee structures ranging from 0.5% to 1.5% on assets, directly impacting revenue growth as portfolios expand.

These advisory services, which can include financial planning and trust administration, also contribute fixed fees. This dual approach ensures a consistent revenue stream, irrespective of market fluctuations to some extent. As of early 2024, the demand for personalized financial advice remained robust, indicating continued potential for fee generation.

Mortgage Loan Origination and Sale Fees

German American Bank generates income through fees earned from originating and selling residential mortgage loans. This revenue stream, often referred to as gains on sale of loans, is a key component of their non-interest income. By selling these loans into the secondary market, the bank also effectively transfers the associated interest rate risk off its balance sheet.

The volume of mortgage sales significantly impacts the profitability of this revenue stream. For instance, in 2024, many regional banks saw fluctuations in mortgage origination volumes due to changing interest rate environments. A higher volume of successful loan sales directly translates to increased fee income for German American Bank.

- Fee Income: Earned from the origination and subsequent sale of residential mortgages.

- Secondary Market: Loans are sold to investors, providing liquidity to the bank.

- Risk Management: Selling loans transfers interest rate risk away from the bank's balance sheet.

- Volume Dependent: Revenue directly correlates with the number of mortgages originated and sold.

Interchange Fees and Other Card-Related Income

German American Bank generates significant revenue through interchange fees. These fees are levied on transactions processed using the bank's debit and credit cards. As customers increasingly adopt and utilize these cards for their daily purchases, this income stream naturally grows, directly correlating with customer engagement and the bank's role in facilitating electronic commerce.

This revenue is directly tied to the volume and value of card transactions. For instance, in 2023, the total value of debit card transactions in Germany exceeded €2.5 trillion, with credit card transactions adding billions more. German American Bank benefits as a percentage of these transactions flows back as interchange fees, underscoring the importance of card product penetration and usage within its customer base.

- Interchange Fees: The primary driver, earned on every debit and credit card transaction processed.

- Card Utilization Growth: Revenue directly scales with increased customer card usage.

- Facilitating Electronic Payments: Reflects the bank's core function in the digital economy.

- Ancillary Card Services: Income may also be derived from other card-related offerings, such as annual fees or late payment charges, contributing to the overall card-related income.

Unveiling the Bank's Revenue Streams!

German American Bank also benefits from fees generated by its wealth management and investment advisory services. These fees are typically a percentage of the assets managed, demonstrating a direct link between the bank's advisory success and its revenue. By offering comprehensive financial planning and trust administration, the bank secures both variable and fixed fee income, providing a stable revenue foundation even when market conditions fluctuate.

The bank earns revenue from originating and selling residential mortgage loans, often referred to as gains on sale of loans. This fee-based income is crucial for their non-interest earnings. In 2024, the mortgage market saw varying origination volumes influenced by interest rate shifts, but the sale of these loans to the secondary market remains a key income driver and risk management tool for German American Bank.

Interchange fees represent a significant revenue stream, derived from every debit and credit card transaction processed by the bank. As digital payments continue to grow in popularity, this income source expands in tandem with customer card usage. In 2023, the value of electronic transactions continued to rise, directly boosting interchange fee income for financial institutions like German American Bank.

| Revenue Stream | Description | Key Driver | 2023/2024 Data Point |

|---|---|---|---|

| Wealth Management & Advisory Fees | Fees earned on assets under management and advisory services | Assets Under Management (AUM), client engagement | In 2024, many wealth management firms charged 0.5%-1.5% on AUM. |

| Gains on Sale of Loans | Fees from originating and selling residential mortgages | Mortgage origination and sales volume | In 2024, regional banks experienced fluctuating mortgage origination volumes. |

| Interchange Fees | Fees earned on debit and credit card transactions | Card transaction volume and value | In 2023, German bank debit card transactions exceeded €2.5 trillion. |

Business Model Canvas Data Sources

The German American Bank Business Model Canvas is built upon a foundation of internal financial statements, customer demographic data, and regulatory compliance reports. These sources ensure the accurate representation of the bank's current operations and strategic direction.