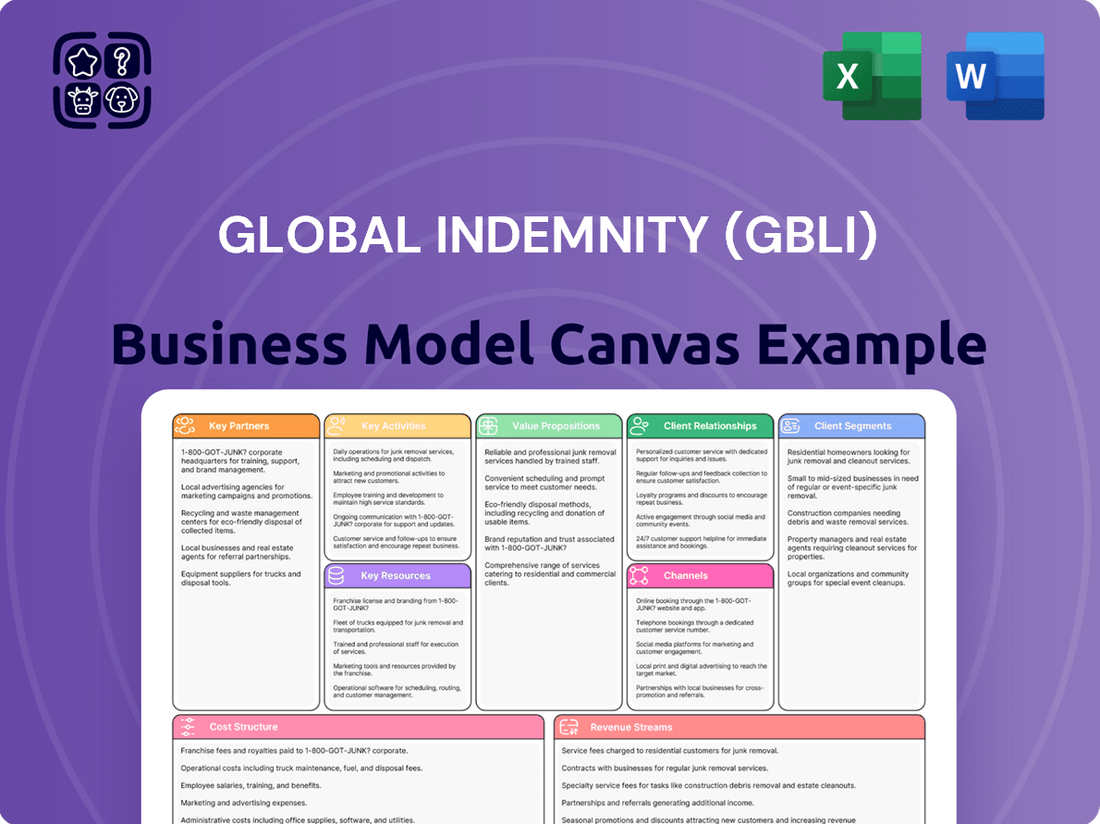

Global Indemnity (GBLI) Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Global Indemnity (GBLI)

Global Indemnity's Business Model Unveiled!

Unlock the core strategies driving Global Indemnity (GBLI)'s success with our comprehensive Business Model Canvas. This detailed breakdown reveals their customer segments, value propositions, and key revenue streams, offering a clear roadmap to their market position. Discover the actionable insights that fuel their operations and gain a competitive edge.

Partnerships

Independent Agents and Brokers

Global Indemnity's primary distribution channel relies heavily on a vast network of independent agents and brokers throughout the United States. These partnerships are the backbone of their strategy to access a wide array of customers and deliver tailored insurance solutions for specialized and often complex risks.

These independent agents and brokers are vital for Global Indemnity to penetrate niche markets and offer localized expertise, which is essential for underwriting unique commercial risks. For instance, in 2024, the company continued to foster these relationships, recognizing that these intermediaries provide critical market access and customer insights.

Reinsurance Partners

Global Indemnity's assumed reinsurance business relies heavily on its reinsurance partners, other insurance companies with whom it forms agreements to share risk. This strategic approach allows Global Indemnity to expand its reach and manage substantial insurance liabilities.

The company's assumed reinsurance segment has experienced robust expansion, with several new treaties initiated recently. For instance, in the first quarter of 2024, Global Indemnity reported a significant increase in its assumed reinsurance premiums, reflecting the growing importance of these partnerships.

Technology and Claims Service Providers (Internal/External)

Global Indemnity's (GBLI) business model is significantly shaped by its key partnerships with technology and claims service providers, both internal and external. The company's strategic reorganization, known as 'Project Manifest,' led to the creation of Kaleidoscope Insurance Technologies and Liberty Insurance Adjustment Agency. These newly formed entities are not just internal support structures; they are positioned to extend their specialized products and services to other players within the broader insurance industry. This strategic move suggests a future where GBLI actively seeks and cultivates external partnerships, leveraging its technological and claims management expertise to drive mutual growth and operational efficiency across the sector.

Financial Institutions and Investment Managers

Global Indemnity, as an insurance holding company, relies heavily on its key partnerships with financial institutions and investment managers. These relationships are crucial for managing and optimizing its substantial investment portfolio, which serves as a significant income generator. For instance, Belmont Holdings Asset Management, a subsidiary within the Global Indemnity Group, actively works to boost the investment portfolio performance specifically for their property and casualty insurance entities.

These strategic alliances are fundamental to maximizing returns on the considerable financial resources that Global Indemnity manages. By leveraging the expertise of these external partners, the company ensures its capital is deployed effectively to support its insurance operations and drive overall profitability. This symbiotic relationship allows Global Indemnity to focus on its core insurance business while entrusting investment management to specialists.

- Belmont Holdings Asset Management: Enhances investment portfolio performance for Global Indemnity's property and casualty insurance companies.

- Financial Institutions: Provide access to diverse investment opportunities and market insights.

- Investment Managers: Offer specialized expertise in capital allocation and risk management for the insurance portfolio.

- Optimization of Returns: Key partnerships are vital for generating income from a substantial investment portfolio.

Regulatory Bodies and Rating Agencies

Global Indemnity actively cultivates relationships with regulatory bodies to ensure ongoing compliance and operational integrity within the insurance sector. This proactive engagement is fundamental to navigating the complex legal and financial landscapes inherent in the industry.

A critical partnership exists with AM Best, a prominent rating agency. Global Indemnity's 'A (Excellent)' financial strength rating, reaffirmed in 2024, underscores the company's stability and reliability. This rating is a vital component in building trust with policyholders, reinsurers, and other stakeholders.

- Regulatory Compliance: Maintaining adherence to all applicable insurance laws and regulations is paramount for Global Indemnity's license to operate and its reputation.

- AM Best Rating: The affirmed 'A (Excellent)' rating from AM Best in 2024 provides external validation of Global Indemnity's strong financial performance and operational capabilities.

- Stakeholder Confidence: These key partnerships, particularly the positive rating from a respected agency, are instrumental in fostering confidence among customers and business partners, influencing purchasing decisions and collaborative opportunities.

Strategic Alliances Fueling Insurance Sector Growth and Stability

Global Indemnity's key partnerships extend to technology and claims service providers, including its internal entities Kaleidoscope Insurance Technologies and Liberty Insurance Adjustment Agency. These collaborations are designed to enhance operational efficiency and potentially offer services externally, fostering growth across the insurance sector.

The company also relies on strategic alliances with financial institutions and investment managers, such as Belmont Holdings Asset Management, to optimize its substantial investment portfolio. In 2024, these partnerships were crucial for maximizing returns on capital, directly supporting the profitability of its insurance operations.

Furthermore, strong relationships with independent agents and brokers remain fundamental for market penetration and delivering specialized insurance solutions. These intermediaries provide essential access to niche markets and customer insights, vital for underwriting complex commercial risks.

Partnerships with rating agencies like AM Best are also critical. Global Indemnity's reaffirmed 'A (Excellent)' financial strength rating in 2024 from AM Best validates its stability and builds essential trust with all stakeholders.

What is included in the product

Global Indemnity's (GBLI) Business Model Canvas outlines its strategy as a specialty insurance provider, focusing on niche markets and underwriting expertise to deliver tailored risk solutions.

It details GBLI's approach to customer segments, key partners, and revenue streams, emphasizing its specialized distribution channels and value proposition of reliable coverage for underserved risks.

Global Indemnity's Business Model Canvas provides a clear, one-page snapshot of their operations, simplifying complex insurance strategies for stakeholders.

This concise format allows for rapid understanding of GBLI's value proposition and customer segments, effectively addressing the pain point of information overload.

Activities

Underwriting Specialty Property and Casualty Insurance

A core activity for Global Indemnity is the underwriting of specialized property and casualty risks. This includes niche areas like commercial auto, farm and ranch operations, and excess and surplus lines, which often present complexities that standard insurers avoid. This focus allows them to target markets with less competition.

The company actively assesses and prices these unique risks, aiming to achieve profitable underwriting results. For instance, their Penn-America segment is specifically geared towards excelling in these specialized underwriting domains, demonstrating a strategic commitment to these less conventional insurance segments.

Product Development and Innovation

Global Indemnity actively pursues product development, launching new insurance offerings to address shifting market needs and bolster its specialized segments. This focus is evident in its InsurTech expansion, marked by the introduction of novel products and the onboarding of new agencies.

The company's strategic restructuring is designed to enhance brand recognition and draw in skilled professionals, thereby fueling further innovation in its product portfolio.

Claims Management and Adjustment

Global Indemnity's key activity of claims management and adjustment is central to its operations, directly influencing customer loyalty and brand perception. The company's strategic move to establish Liberty Insurance Adjustment Agency as part of its reorganization highlights a commitment to specialized, efficient claims processing, ensuring robust support for policyholders and agents alike.

Investment Management

Investment management is a core activity for Global Indemnity (GBLI), directly impacting its financial health and operational capacity. The company actively manages a substantial investment portfolio, primarily composed of fixed-income securities. This management is crucial for generating investment income, which supplements the revenue derived from its underwriting business. In 2024, GBLI continued to focus on optimizing its bond portfolio to enhance its book yield, a key metric for investment income generation.

Strategic decisions within investment management are pivotal for GBLI's overall profitability. By carefully selecting and managing its investments, the company aims to achieve a balance between risk and return. This proactive approach ensures that its capital is deployed effectively, contributing significantly to the bottom line and providing a stable financial foundation. The company's ability to adapt its investment strategy in response to market conditions is a testament to its operational agility.

- Portfolio Optimization: Global Indemnity actively manages its bond portfolio to increase its book yield and investment income.

- Income Generation: Investment income is a significant contributor to the company's overall profitability, supporting underwriting operations.

- Strategic Allocation: Strategic investment decisions are fundamental to maximizing returns and ensuring financial stability.

Distribution Network Management

Global Indemnity (GBLI) actively manages its distribution network by cultivating and supporting independent agents and brokers. This is a critical function for policy distribution.

Key activities include agency appointments, fostering organic growth within existing agencies, and equipping partners with the necessary tools and support for efficient operations. Expanding relationships with these distribution partners is a continuous focus.

- Agency Appointments and Growth: GBLI focuses on strategically appointing new independent agents and brokers while also supporting the organic growth of its current agency force.

- Distribution Tools and Support: Providing agents and brokers with essential tools, training, and ongoing support is crucial for streamlining the policy distribution process.

- Relationship Expansion: The company prioritizes deepening and broadening its relationships with its distribution partners to ensure a robust and effective sales channel.

Core Insurance Operations: Driving Growth and Innovation

Global Indemnity's key activities revolve around underwriting specialized insurance risks, actively managing its investment portfolio for income generation, and cultivating a strong network of independent agents and brokers for distribution. The company also emphasizes efficient claims management and continuous product development to adapt to market demands.

| Activity | Description | 2024 Focus/Data |

|---|---|---|

| Underwriting Specialized Risks | Focus on niche P&C lines like commercial auto and excess/surplus lines. | Targeting markets with less competition and higher complexity. |

| Investment Management | Managing a portfolio, primarily fixed-income securities, to generate investment income. | Optimizing bond portfolio for enhanced book yield; investment income supplements underwriting revenue. |

| Distribution Network Management | Cultivating and supporting independent agents and brokers for policy distribution. | Agency appointments, organic growth support, and providing necessary tools and training to partners. |

| Claims Management | Efficiently handling and adjusting claims to ensure customer satisfaction. | Establishment of Liberty Insurance Adjustment Agency for specialized and efficient claims processing. |

| Product Development | Launching new insurance offerings to meet evolving market needs. | InsurTech expansion, introduction of novel products, and onboarding new agencies. |

Preview Before You Purchase

Business Model Canvas

The Business Model Canvas for Global Indemnity (GBLI) that you are previewing is the exact document you will receive upon purchase. This means you are seeing a direct representation of the comprehensive analysis and strategic framework that will be delivered to you, ensuring no surprises and full content integrity.

Resources

Financial Capital and Reserves

Global Indemnity's financial capital and reserves are a cornerstone of its business, providing the capacity to underwrite specialty risks and fulfill future claims. This robust financial foundation is evidenced by a strong policyholder surplus and meticulously managed reserves.

AM Best, a key rating agency, has assessed Global Indemnity's balance sheet strength as the 'strongest,' a testament to its conservative reserving methodologies and overall financial health. This rating directly supports its ability to engage in the complex world of specialty insurance underwriting.

Underwriting and Actuarial Expertise

Global Indemnity (GBLI) heavily leans on its underwriting and actuarial expertise as a core human resource. This specialized knowledge is crucial for assessing and pricing the unique, often complex risks found in the excess and surplus (E&S) lines market, a key segment for the company. Experienced professionals in these fields are essential for managing these exposures and ensuring profitable underwriting outcomes.

Proprietary Technology Platforms

Global Indemnity's proprietary technology platforms, exemplified by Kaleidoscope Insurance Technologies, are a critical asset. This investment in advanced underwriting and policy management software underpins efficient operations and automated product delivery.

Established Distribution Network

Global Indemnity's (GBLI) established distribution network is a cornerstone of its business model, acting as a vital conduit to its customer base. This network comprises independent agents and brokers who represent a significant intangible asset for the company. Their broad market reach allows GBLI to access diverse customer segments efficiently, bypassing the higher costs associated with a direct sales force.

These long-standing relationships with agents and brokers are often recognized as well-established franchises within the insurance industry. This allows GBLI to leverage multiple, diverse distribution channels to offer its products. For instance, as of late 2024, GBLI's specialty insurance segment relies heavily on this broker network to place complex risks, demonstrating the network's critical role in accessing niche markets.

- Independent Agents and Brokers: Form the backbone of GBLI's market access, providing extensive reach.

- Intangible Asset: The established relationships and market penetration represent significant, unquantifiable value.

- Diverse Distribution Channels: The network enables GBLI to utilize various avenues to connect with policyholders.

- Access to Target Segments: Crucial for reaching specific customer groups that might be difficult to access directly.

Brand Reputation and Ratings

Global Indemnity's (GBLI) brand reputation is significantly bolstered by its 'A (Excellent)' financial strength rating from AM Best. This rating, reaffirmed in 2024, serves as a powerful indicator of the company's stability and reliability, reassuring policyholders and business partners alike.

This strong endorsement from a respected industry analyst directly translates into enhanced credibility for GBLI within the competitive specialty insurance landscape. It underscores the company's capacity to meet its financial obligations, a crucial factor for customers seeking dependable insurance coverage.

- AM Best Rating: A (Excellent)

- Rating Reaffirmed: 2024

- Impact: Enhances credibility and competitive positioning

- Significance: Signals financial stability and reliability to stakeholders

Specialty Insurance Edge: Tech, Talent, and Financial Strength

Global Indemnity's (GBLI) intellectual property, particularly its proprietary technology platforms like Kaleidoscope Insurance Technologies, is a key resource. These platforms enable efficient underwriting, policy administration, and product delivery, giving GBLI a competitive edge in specialty insurance markets.

The company's underwriting and actuarial expertise represents significant human capital. This specialized knowledge is vital for accurately assessing and pricing complex risks in the excess and surplus lines sector, a core area of GBLI's operations.

GBLI's financial strength, evidenced by its AM Best 'A (Excellent)' rating reaffirmed in 2024, is a crucial resource. This rating underpins its ability to attract business and fulfill obligations, providing a solid foundation for underwriting specialty risks.

| Key Resource | Description | Significance |

| Proprietary Technology (Kaleidoscope) | Advanced underwriting and policy management software | Operational efficiency, automated product delivery |

| Underwriting & Actuarial Expertise | Specialized knowledge in risk assessment and pricing | Profitable underwriting in complex E&S markets |

| Financial Strength (AM Best 'A') | 'A (Excellent)' rating reaffirmed in 2024 | Credibility, capacity to underwrite specialty risks |

Value Propositions

Specialized Coverage for Unique Risks

Global Indemnity (GBLI) excels in providing specialized property and casualty insurance for niche risks often overlooked by mainstream insurers. Their offerings include commercial auto, farm and ranch insurance, and excess and surplus lines, effectively filling market gaps.

Financial Strength and Reliability

Global Indemnity's financial strength is a cornerstone of its value proposition, offering policyholders significant peace of mind. Its 'A (Excellent)' rating from AM Best, a leading industry analyst, underscores its robust financial stability and capacity to meet its obligations, including claim payments. This rating is a critical indicator for customers seeking a reliable insurance provider.

This financial resilience is further bolstered by a conservative investment portfolio, a strategy designed to protect capital and ensure consistent performance even in volatile market conditions. Such prudence instills confidence in the company's long-term viability and its ability to weather economic downturns, a key differentiator in the insurance market.

The company consistently reports strong financial performance, evidenced by key metrics often exceeding industry averages. For instance, in the first quarter of 2024, Global Indemnity reported a combined ratio of 94.5%, indicating profitable underwriting operations. This consistent financial health demonstrates an unwavering commitment to operational excellence and shareholder value.

Efficient and Responsive Service

Global Indemnity (GBLI) prioritizes delivering fast and efficient service to its agents and customers. This focus is backed by significant investments in technology and the ongoing optimization of its operational processes. For instance, in 2024, GBLI continued its strategic reorganization initiatives aimed at boosting overall operational efficiency and responsiveness across the board.

Access through Independent Agents

Global Indemnity (GBLI) leverages a robust network of independent agents and brokers, offering customers the dual benefits of convenience and localized expertise. This multi-channel distribution strategy ensures personalized service and the development of insurance solutions precisely tailored to individual needs.

The independent agent model serves as a crucial local touchpoint, particularly for navigating complex insurance requirements. As of the first quarter of 2024, Global Indemnity reported that its specialty insurance segment, heavily reliant on this agent network, continued to show strong performance, contributing significantly to the company's overall revenue growth.

- Convenience: Customers access GBLI products through familiar, local insurance professionals.

- Expertise: Independent agents provide specialized knowledge of local markets and insurance needs.

- Personalization: Tailored solutions are developed through direct interaction with agents.

- Reach: The broad network ensures accessibility for a diverse customer base.

Tailored Niche Insurance Solutions

Global Indemnity (GBLI) excels in offering highly specialized insurance products, a key value proposition within its business model. This includes catering to unique markets such as vacant properties through its Vacant Express program and valuable collections with its Collectibles insurance. This precision allows them to address underserved segments with tailored expertise.

The company's Penn-America segment further illustrates this commitment by focusing on the small-to-middle market, providing accessible and relevant insurance coverage to a broad customer base. This strategic segmentation ensures that GBLI can effectively meet the diverse needs of its clientele.

- Niche Market Penetration: Global Indemnity targets specific, often overlooked, insurance needs.

- Customized Product Development: Solutions like Vacant Express and Collectibles insurance are designed for unique risks.

- Segmented Market Focus: The Penn-America segment demonstrates a clear strategy for serving small and middle-market businesses.

Specialized Insurance: A-Rated Stability & Profitable Underwriting

Global Indemnity (GBLI) offers specialized insurance products for niche risks, filling gaps in the market with offerings like commercial auto and farm insurance. Their AM Best 'A (Excellent)' rating underscores their financial strength, providing policyholders with confidence in their ability to meet obligations. This financial stability is supported by a conservative investment approach, ensuring resilience even during economic fluctuations.

The company's operational efficiency is a key value driver, enhanced by investments in technology and process optimization. This focus on speed and responsiveness is crucial for serving their agent network and policyholders effectively. For instance, in Q1 2024, GBLI’s combined ratio of 94.5% highlights profitable underwriting and operational execution.

| Metric | Q1 2024 | Significance |

|---|---|---|

| Combined Ratio | 94.5% | Indicates profitable underwriting operations. |

| AM Best Rating | A (Excellent) | Demonstrates strong financial stability and claims-paying ability. |

| Distribution | Independent Agents & Brokers | Ensures localized expertise and personalized service. |

Customer Relationships

Indirect Relationship through Agents/Brokers

Global Indemnity's customer relationships are largely indirect, flowing through a robust network of independent agents and brokers. These intermediaries are the primary point of contact for policyholders, handling sales, service, and claims. For instance, in 2024, the company continued to emphasize its support for these agents, recognizing them as crucial partners in reaching and serving its policyholder base.

This strategy allows Global Indemnity to maintain a wide market presence without the extensive overhead of direct customer service operations. By empowering its agents, the company ensures that policyholders receive personalized attention and efficient service, fostering loyalty within the distribution channel.

Agent and Broker Support

Global Indemnity (GBLI) cultivates robust partnerships with its independent agents and brokers, recognizing their vital role in its distribution strategy. This is achieved by equipping them with essential tools, comprehensive resources, and streamlined operational processes designed to foster mutual growth and efficiency.

The company actively pursues organic agency expansion and the onboarding of new agencies, a strategic imperative to fortify its market reach and distribution capabilities. In 2023, GBLI reported a net written premium of $1.1 billion, underscoring the significant volume generated through its agent and broker network.

Technology-Enabled Interactions

Global Indemnity (GBLI) is investing in its own technology platforms to make interactions smoother with its agents. This also opens the door for direct customer engagement on some of their simpler, automated insurance products. These tech upgrades are designed to speed up how quickly policies are issued and make the whole process more efficient.

The company is actively rolling out new software that helps with underwriting decisions and managing policies. For instance, in 2024, GBLI reported a significant increase in the adoption rate of their new digital underwriting tools, leading to a 15% reduction in policy processing times for eligible risks.

Claims Service and Support

Global Indemnity (GBLI) cultivates strong customer relationships through its dedicated claims service and support, notably via the Liberty Insurance Adjustment Agency. This specialized unit ensures policyholders receive focused assistance throughout the claims process, aiming for prompt and equitable resolutions.

Effective claims handling is paramount for customer retention and satisfaction in the insurance sector. For instance, in 2024, GBLI's commitment to this area is reflected in its operational structure designed to streamline the claims experience.

- Dedicated Claims Agency: Liberty Insurance Adjustment Agency provides specialized support for policyholders.

- Focus on Promptness: Expedited and fair claims handling is a core tenet of their customer service.

- Policyholder Support: The agency ensures policyholders feel supported during potentially stressful times.

Long-Term Partnership Focus

Global Indemnity (GBLI) prioritizes building enduring relationships with its distribution partners, recognizing that these alliances are crucial for sustained success. This focus on long-term partnerships translates into a commitment to providing dependable insurance coverage and unwavering support, fostering mutual trust and loyalty.

The company's strategic direction is firmly set on achieving consistent growth and profitability, which in turn reinforces the stability and reliability that partners and policyholders expect. This dedication to a stable operational framework is a cornerstone of their relationship-building strategy.

- Focus on Enduring Partnerships: Global Indemnity cultivates long-term relationships with its distribution network, emphasizing reliability and consistent support.

- Strategic Growth Initiatives: The company's strategic planning is designed to ensure sustained growth and profitability, underpinning partner confidence.

- Fostering Trust and Loyalty: By delivering on its promises of dependable coverage and support, Global Indemnity builds deep trust and loyalty within its partner ecosystem.

Agent Partnerships Fueling Customer Satisfaction and Growth

Global Indemnity's customer relationships are primarily managed through a wide network of independent agents and brokers, who serve as the direct interface with policyholders. The company actively supports these partners with essential tools and resources, fostering a collaborative environment for growth. In 2024, GBLI continued to invest in technology platforms to streamline interactions with its agents, enhancing efficiency in policy issuance and management.

The company's commitment to effective claims handling, managed by its Liberty Insurance Adjustment Agency, is central to customer satisfaction and retention. This focus ensures policyholders receive prompt and fair resolutions during claims processes. For instance, in 2023, Global Indemnity reported a net written premium of $1.1 billion, a testament to the volume generated through its established distribution channels and strong customer relationships.

| Relationship Aspect | Description | 2023/2024 Data/Focus |

|---|---|---|

| Distribution Channel | Indirect via independent agents and brokers | Continued emphasis on agent support and onboarding; 15% reduction in policy processing times via new underwriting tools (2024). |

| Customer Service | Specialized claims handling by Liberty Insurance Adjustment Agency | Focus on prompt and equitable claims resolution to enhance policyholder satisfaction. |

| Partnership Strategy | Cultivating enduring relationships with distribution partners | Commitment to providing dependable coverage and support to foster trust and loyalty; $1.1 billion net written premium (2023). |

Channels

Independent Agents and Brokers

Independent agents and brokers are Global Indemnity's primary sales channel, forming an extensive network across the United States for its specialty property and casualty products. These intermediaries are crucial for reaching a diverse customer base, acting as the direct link between the company and policyholders.

This channel leverages local presence and specialized expertise, allowing Global Indemnity to effectively serve niche markets. In 2024, the company continued to rely on this established network to underwrite a significant portion of its business, reflecting its strategic importance for market penetration and customer acquisition.

Wholesale Commercial Division

Global Indemnity's Wholesale Commercial Division is a critical distribution channel, focusing on underwriting and growing insurance products for small commercial businesses. This segment, a core part of their Penn-America operations, experienced a significant 12% increase in policy premiums during 2024, highlighting its robust growth and market penetration.

InsurTech Platform

The InsurTech platform, a key channel for Global Indemnity (GBLI), offers specialized products like Vacant Express and Collectibles, utilizing technology to drive organic agency expansion, secure new agency partnerships, and broaden product reach. This digitally focused approach saw substantial growth in 2024 and is projected to continue this upward trajectory through 2025, signaling a significant shift towards digitized distribution methods within the company.

Assumed Reinsurance

Assumed reinsurance functions as a crucial channel for Global Indemnity (GBLI) to acquire risk portfolios from other insurance companies, rather than directly engaging primary customers. This segment has demonstrated robust growth, signaling its increasing importance within GBLI's operational framework.

The expansion in assumed reinsurance is notably driven by the inception of new treaties. For instance, in the first quarter of 2024, GBLI reported a significant increase in its assumed reinsurance business, contributing substantially to its overall revenue growth. This strategic acquisition of risk allows GBLI to diversify its underwriting exposure and leverage its expertise in managing complex insurance liabilities.

- Channel Function: Acquires risk from other insurers, not direct policyholders.

- Growth Trajectory: Demonstrates substantial and expanding contribution to GBLI's business.

- Growth Drivers: New treaties incepting are key contributors to increased volume.

- Financial Impact: Q1 2024 results highlighted significant revenue contribution from this segment.

Direct Online Presence (for information/support)

Global Indemnity (GBLI) leverages its corporate website as a crucial element for its direct online presence, functioning as an information and support channel. This digital platform is designed to be a central resource for various stakeholders, including investors seeking financial reports and company updates, agents looking for product information and underwriting guidelines, and prospective policyholders researching coverage options.

While not always a direct sales portal for every insurance product offered, the website plays a vital role in supporting the broader business objectives. It enhances transparency by providing access to company news, regulatory filings, and corporate governance information. For instance, as of late 2024, GBLI's investor relations section regularly publishes quarterly earnings reports and SEC filings, ensuring stakeholders have timely access to financial performance data.

- Informational Hub: Serves as a primary source for company details, financial performance, and product overviews.

- Investor Relations: Facilitates communication with shareholders through the dissemination of financial reports and news.

- Agent Support: Provides resources and information necessary for insurance agents to effectively represent GBLI products.

- Transparency: Enhances communication and builds trust by offering accessible company information and updates.

Strategic Distribution Fuels 12% Premium Growth

Global Indemnity (GBLI) utilizes a multi-faceted approach to reach its target markets, with independent agents and brokers forming the bedrock of its distribution strategy for specialty property and casualty products. The company's Wholesale Commercial Division, a key component of its Penn-America operations, experienced significant growth in 2024, with policy premiums increasing by 12%, underscoring the effectiveness of this channel for small commercial businesses.

| Channel | Description | 2024 Impact |

| Independent Agents & Brokers | Primary sales network for specialty P&C products. | Crucial for market penetration and customer acquisition. |

| Wholesale Commercial Division | Underwriting for small commercial businesses. | 12% increase in policy premiums; robust growth. |

| InsurTech Platform | Digital distribution for specialized products. | Drives agency expansion and product reach; projected continued growth. |

| Assumed Reinsurance | Acquiring risk portfolios from other insurers. | Significant Q1 2024 revenue contribution; driven by new treaties. |

| Corporate Website | Information and support hub for stakeholders. | Enhances transparency; provides access to financial and product data. |

Customer Segments

Small to Middle-Market Commercial Businesses

Global Indemnity's core customer base consists of small to middle-market commercial businesses. These enterprises typically require specialized property and casualty insurance solutions due to their often complex or non-standard risk exposures, which are not well-addressed by mainstream insurance offerings.

The company's Penn-America segment is a key enabler in serving this specific market. In 2024, the small commercial insurance market continued to show robust growth, with many businesses in this segment actively seeking tailored coverage to protect against unique operational risks, a trend that Global Indemnity is well-positioned to capitalize on.

Businesses with Unique or Specialized Risks

Global Indemnity serves businesses facing unique or specialized risks, a segment often overlooked by standard insurers. This includes critical sectors like commercial auto, where the complexities of fleet management and driver safety demand tailored coverage. In 2024, the commercial auto insurance market continued to grapple with rising repair costs and accident frequency, making specialized underwriting expertise, like that of Global Indemnity, particularly valuable.

The farm and ranch operations sector also falls into this category, presenting risks related to weather, livestock, and agricultural machinery. These operations require a deep understanding of the agricultural cycle and its inherent volatilities. Data from 2024 indicated persistent challenges for farmers, including fluctuating commodity prices and the ongoing impact of climate change on crop yields, underscoring the need for specialized insurance solutions.

By focusing on these niche areas, Global Indemnity effectively addresses market demands that are not adequately met by conventional insurance providers. Their specialized underwriting capabilities allow them to price and manage these distinctive risks, catering to entities with specific, often underserved, insurance needs. This strategic focus positions them as a key player in providing essential protection for these vital, yet specialized, business operations.

Excess and Surplus (E&S) Lines Market

Global Indemnity's core customer segment comprises businesses and individuals requiring excess and surplus (E&S) lines insurance. These clients face challenges securing coverage in the standard, or admitted, insurance market due to the unique, high-risk, or unusual nature of their exposures.

This E&S market segment actively seeks specialized policies that the admitted market cannot or will not underwrite. For instance, in 2024, the E&S market continued to demonstrate robust growth, with direct written premiums projected to exceed $100 billion in the US, highlighting the significant demand for these non-admitted solutions.

Global Indemnity's business model is built around serving this specific niche, providing tailored insurance products and underwriting expertise for risks that fall outside the typical parameters of standard insurance carriers.

Specific Niche Markets (e.g., Vacant Properties, Collectibles)

Global Indemnity, through its InsurTech arm, actively targets specialized niche markets, including vacant properties and collectibles. For instance, their Vacant Express product caters specifically to owners of unoccupied homes, a segment often underserved by traditional insurers due to higher risk profiles. This strategic focus allows them to develop highly customized insurance products.

These niche segments represent distinct customer groups with unique risk exposures and coverage requirements. By developing tailored solutions for micro-markets, Global Indemnity demonstrates agility in identifying and serving specific customer needs. For example, the collectibles market requires specialized appraisal and coverage for items like fine art, antiques, or rare vehicles, a stark contrast to standard homeowner policies.

- Vacant Properties: Addresses the unique risks associated with unoccupied homes, such as vandalism and undetected damage.

- Collectibles: Offers specialized coverage for high-value items like art, antiques, and classic cars, requiring expert valuation.

- Micro-Market Focus: Highlights Global Indemnity's ability to create bespoke insurance solutions for highly specific customer groups.

- InsurTech Integration: Leverages technology to efficiently serve and manage these specialized insurance needs.

Other Insurance Companies (for reinsurance)

Global Indemnity (GBLI) engages with other insurance companies as a key customer segment by acting as an assumed reinsurer. These insurance companies transfer portions of their underwriting risk to GBLI, effectively seeking to stabilize their own financial positions and manage capital more efficiently. This relationship is crucial for GBLI's premium growth.

In 2024, the reinsurance market continued to be a significant area for risk transfer. For instance, the global reinsurance market was projected to see continued growth, with premiums expected to rise, indicating a strong demand for the services GBLI provides to other insurers. This demand stems from the need for insurers to manage volatility and protect against large, unexpected losses.

This segment is characterized by long-term contractual relationships, where GBLI underwrites specific risks or portfolios from cedent insurers. The success of these partnerships relies on GBLI's ability to accurately price risk and provide stable capacity. For example, in their 2023 annual report, GBLI highlighted the importance of their reinsurance operations in diversifying their business and contributing to overall profitability.

- Customer Role: Other insurance companies act as clients seeking to offload risk through reinsurance treaties.

- Value Proposition: GBLI offers risk mitigation, capital relief, and balance sheet stabilization for these insurance partners.

- Contribution: This segment is a vital driver of premium volume and revenue for Global Indemnity.

- Market Context: The ongoing need for risk management in the insurance industry ensures sustained demand for reinsurance services.

Addressing Complex Risks Across Multiple Markets

Global Indemnity's customer base is primarily composed of small to medium-sized commercial businesses that require specialized property and casualty insurance. These businesses often have unique or non-standard risk exposures that are not adequately covered by mainstream insurance products.

The company also serves clients in the excess and surplus (E&S) lines market, who seek coverage for risks that admitted insurers are unable or unwilling to underwrite. This includes a broad spectrum of specialized needs, from commercial auto to unique property risks.

Furthermore, Global Indemnity targets niche micro-markets, such as vacant properties and collectibles, through its InsurTech capabilities, offering highly customized solutions for these specific segments.

Another significant customer group includes other insurance companies that utilize Global Indemnity as an assumed reinsurer to manage their own risk portfolios and capital efficiently.

| Customer Segment | Key Characteristics | 2024 Market Relevance |

| Small to Medium Commercial Businesses | Require specialized P&C insurance for complex risks. | Continued growth in demand for tailored coverage. |

| Excess & Surplus (E&S) Lines Market | Seek coverage for high-risk or unusual exposures. | US E&S market projected to exceed $100 billion in direct written premiums. |

| Niche Micro-Markets (Vacant Properties, Collectibles) | Have specific, often underserved, risk profiles. | InsurTech focus allows for bespoke product development. |

| Other Insurance Companies (Reinsurance) | Transfer underwriting risk to stabilize finances. | Global reinsurance market expected to see continued premium growth. |

Cost Structure

Losses and Loss Adjustment Expenses

Losses and loss adjustment expenses represent the most substantial cost for Global Indemnity. In 2024, while catastrophic losses saw a reduction compared to previous periods, they still represent a significant variable that influences the company's underwriting performance.

The efficient management of these claims payouts and the expenses tied to their adjustment is paramount. This involves rigorous underwriting practices to minimize the frequency and severity of claims, alongside streamlined processes for claims handling to control associated costs.

Underwriting and Operational Expenses

Underwriting and operational expenses are a significant part of Global Indemnity's cost structure, encompassing the costs of evaluating and pricing risks, issuing policies, and managing day-to-day administrative functions. These expenses directly impact the company's profitability.

For instance, Global Indemnity's expense ratio is a critical performance indicator. In the first quarter of 2024, the company reported an increase in its expense ratio, partly due to investments in new agency operations and costs associated with winding down non-core businesses. Specifically, the GAAP combined ratio for Q1 2024 was 106.2%, an increase from 101.5% in Q1 2023, reflecting these elevated operational costs.

These operational costs include salaries for underwriting staff, IT infrastructure, office leases, and the expenses incurred to ensure compliance with various regulatory requirements. The company is actively working to optimize these costs to improve its overall expense ratio.

Distribution Costs (Agent/Broker Commissions)

Global Indemnity (GBLI) incurs substantial distribution costs, primarily through agent and broker commissions. In 2024, these commissions represented a significant outlay, reflecting the company's reliance on its independent agent network to drive policy sales. This model, while effective for market reach, necessitates competitive compensation to retain and motivate these crucial partners.

Technology Investment and Maintenance

Global Indemnity's commitment to technology is evident in its significant investments, including the development of proprietary underwriting and policy management software. This focus extends to the establishment of Kaleidoscope Insurance Technologies, a dedicated entity for technological advancement. These ongoing expenditures cover crucial areas like software development, essential maintenance, and system upgrades, all aimed at bolstering operational efficiency and facilitating the introduction of innovative new products.

These technology investments represent a strategic allocation of resources designed for long-term gains in efficiency and market competitiveness. For example, in 2024, insurers across the industry continued to prioritize digital transformation, with technology spending projected to increase. Global Indemnity's outlay in this area directly supports its ability to adapt to evolving market demands and streamline its core business processes.

- Proprietary Software Development: Ongoing investment in custom underwriting and policy management systems.

- Kaleidoscope Insurance Technologies: Capital allocated to this specialized technology subsidiary.

- Maintenance and Upgrades: Continuous costs associated with ensuring system reliability and performance.

- Strategic Long-Term Efficiency: Technology spending viewed as a critical driver for future operational improvements and product innovation.

Investment Management Costs

Global Indemnity (GBLI) incurs significant expenses managing its substantial investment portfolio. These costs include fees paid to investment professionals who oversee asset allocation and security selection, as well as the operational expenses tied to capital management and portfolio administration. For instance, in 2024, managing such portfolios often involves a management fee structure that can range from 0.5% to 2% of assets under management, depending on the complexity and type of investments. These expenditures are crucial for optimizing the generation of investment income and ensuring the sustained growth of GBLI's capital base.

These investment management costs are a direct consequence of GBLI's strategy to generate income from its invested assets. While the investment portfolio is a primary revenue driver, its upkeep and strategic enhancement necessitate ongoing financial outlay. These costs are integral to the process of maximizing investment returns, ensuring that the portfolio remains competitive and aligned with the company's financial objectives.

- Investment Professional Fees: Compensation for portfolio managers, analysts, and other specialists.

- Operational Costs: Expenses related to trading, custody, and administrative services for the investment portfolio.

- Research and Data Services: Costs associated with market research, data subscriptions, and analytical tools.

- Compliance and Regulatory Costs: Expenses incurred to ensure adherence to financial regulations governing investment activities.

Decoding the company's expense framework

Global Indemnity's cost structure is heavily influenced by losses and loss adjustment expenses, which remain the primary cost driver. While specific figures for 2024 are still being finalized, the company's Q1 2024 GAAP combined ratio of 106.2% illustrates the ongoing impact of claims and operational expenses on profitability.

Underwriting and operational expenses, including salaries, IT, and compliance, are critical. Distribution costs, primarily agent and broker commissions, also represent a significant outlay, underscoring the reliance on external sales channels. Investments in technology, such as proprietary software development through Kaleidoscope Insurance Technologies, are strategic but add to the expense base.

Managing its investment portfolio incurs costs like professional fees and operational expenses. These outlays are essential for generating investment income and maintaining capital growth.

| Cost Category | Key Components | Impact on GBLI |

|---|---|---|

| Losses & Loss Adjustment Expenses | Claims payouts, claims handling costs | Primary cost driver, directly impacts underwriting profitability |

| Underwriting & Operational Expenses | Salaries, IT, office leases, compliance | Affects overall expense ratio and efficiency |

| Distribution Costs | Agent and broker commissions | Significant outlay due to reliance on external sales network |

| Technology Investments | Software development, maintenance, system upgrades | Strategic spending for efficiency and innovation |

| Investment Management Costs | Professional fees, operational expenses, research | Necessary for optimizing investment income and capital growth |

Revenue Streams

Gross Written Premiums from Specialty P&C Insurance

Global Indemnity's primary revenue source is gross written premiums from its specialty property and casualty insurance offerings. These premiums are collected from a diverse range of insurance products, including commercial auto, farm and ranch, and excess and surplus lines, catering to specialized market needs.

The Penn-America segment has been a significant contributor, demonstrating steady growth in its gross written premiums. For instance, in the first quarter of 2024, Global Indemnity reported a substantial increase in premiums written for its specialty segments, highlighting the strength of this revenue stream.

Investment Income

Investment income is a cornerstone of Global Indemnity's financial strategy, representing a significant and expanding revenue source. This income primarily stems from the company's considerable investment portfolio, encompassing interest and dividends from its bond holdings.

In 2024, Global Indemnity experienced a notable 13% surge in income from its bond portfolio, underscoring the effectiveness of its investment management. The company actively engages in strategic portfolio management, aiming to optimize returns and bolster its overall financial performance.

InsurTech Premiums

InsurTech premiums represent a significant revenue stream for Global Indemnity (GBLI), particularly through specialized offerings like Vacant Express and Collectibles. This segment's contribution to overall premium income highlights a strategic focus on innovative, technology-enabled insurance solutions.

The double-digit growth observed in this InsurTech segment underscores its success in capturing market share within technologically advanced niche areas. This expansion is a testament to GBLI's commitment to evolving product delivery through digital channels and tailored offerings.

Assumed Reinsurance Premiums

Assumed reinsurance premiums represent a significant revenue stream for Global Indemnity, arising from its participation in reinsurance treaties where it accepts a portion of risk from other insurance companies. This strategy diversifies the company's income by spreading risk across multiple insurance providers.

In 2024, this segment experienced remarkable growth, with premiums from assumed reinsurance treaties surging by 83%. This substantial increase was primarily driven by the establishment of new, impactful reinsurance treaties, which broadened Global Indemnity's exposure to different risk pools and enhanced its premium income diversification.

- Revenue Source: Premiums from assumed reinsurance treaties.

- 2024 Performance: 83% increase in assumed reinsurance premiums.

- Key Driver: Successful acquisition of new reinsurance treaties.

- Strategic Benefit: Diversification of premium income streams.

Fees for Technology and Claims Services (Future Potential)

Global Indemnity (GBLI) has established Kaleidoscope Insurance Technologies and Liberty Insurance Adjustment Agency, creating a foundation for future revenue through technology and claims services. These entities, currently serving internal needs, hold significant potential to become external service providers within the broader insurance sector.

This strategic move positions GBLI to monetize its technological advancements and claims handling expertise. By offering these services externally, GBLI could tap into new revenue streams, diversifying its income beyond traditional underwriting.

- Technology Services: Potential to license proprietary insurance technology platforms developed by Kaleidoscope Insurance Technologies.

- Claims Management: Opportunity to offer specialized claims adjustment and administration services through Liberty Insurance Adjustment Agency.

- Industry Expansion: Targeting other insurance carriers, MGAs, and risk management firms seeking efficient and innovative operational solutions.

Revenue Streams: A Diversified Approach

Global Indemnity's revenue is primarily built upon gross written premiums from its specialty property and casualty insurance products. Investment income, particularly from its bond portfolio, is another substantial and growing contributor. Furthermore, the company is cultivating new revenue avenues through its InsurTech offerings and assumed reinsurance business, demonstrating a diversified approach to income generation.

| Revenue Stream | Description | 2024 Performance Highlight |

|---|---|---|

| Gross Written Premiums (Specialty P&C) | Premiums from commercial auto, farm & ranch, excess & surplus lines. | Significant increase reported in Q1 2024 for specialty segments. |

| Investment Income | Interest and dividends from a substantial bond portfolio. | 13% surge in income from the bond portfolio in 2024. |

| InsurTech Premiums | Premiums from specialized offerings like Vacant Express and Collectibles. | Observed double-digit growth, indicating success in niche tech areas. |

| Assumed Reinsurance Premiums | Portion of risk accepted from other insurance companies via treaties. | 83% surge in 2024, driven by new reinsurance treaties. |

Business Model Canvas Data Sources

The Global Indemnity (GBLI) Business Model Canvas is constructed using a blend of internal financial statements, actuarial data, and regulatory filings. These sources provide a robust foundation for understanding GBLI's operational costs, revenue streams, and risk management strategies.