Fulton Bank SWOT Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Fulton Bank Bundle

Make Insightful Decisions Backed by Expert Research

Fulton Bank's market position is shaped by a blend of strong regional presence and a commitment to community banking, but understanding the nuances of its operational efficiencies and potential digital disruption is key. Our comprehensive SWOT analysis dives deep into these factors, providing you with the critical intelligence needed to navigate the competitive financial landscape.

Want the full story behind Fulton Bank's strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

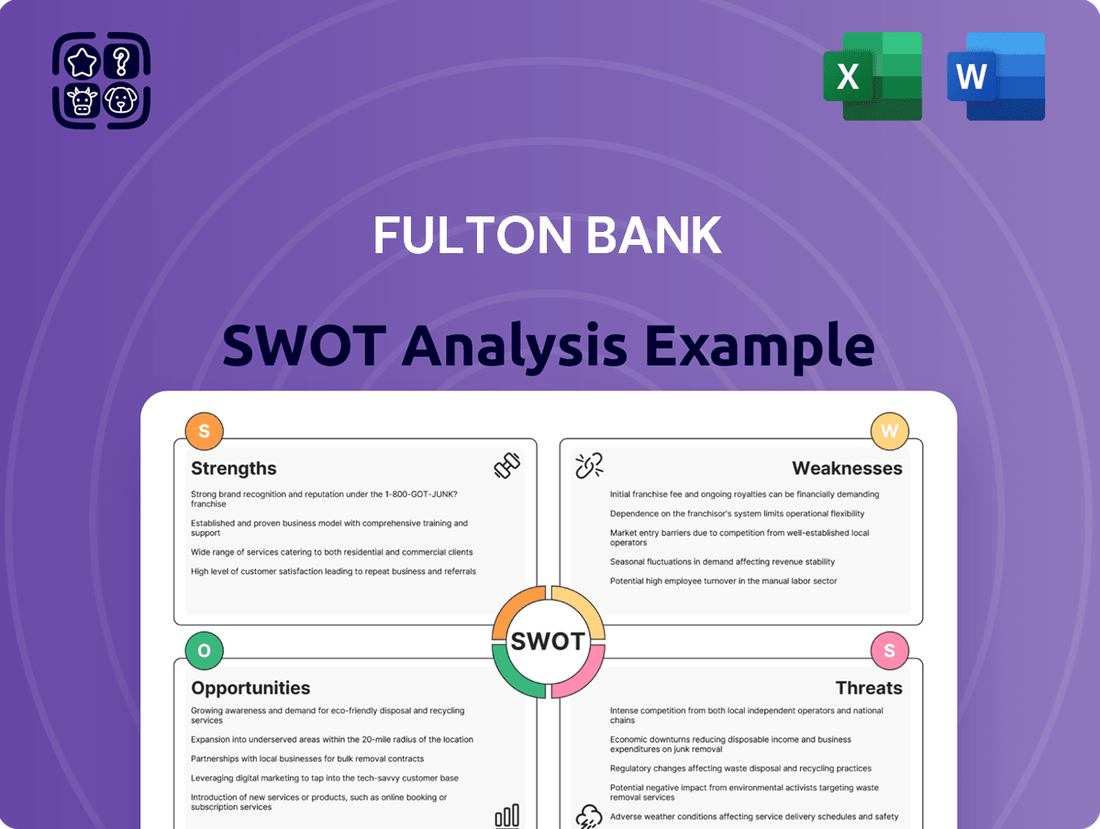

Strengths

Diverse Financial Service Portfolio

Fulton Bank, under Fulton Financial Corporation, boasts a diverse financial service portfolio that includes community banking, investment management, and insurance. This broad offering creates multiple revenue streams, reducing dependence on any single area and allowing them to serve a wider customer base. For instance, as of the first quarter of 2024, Fulton Financial Corporation reported total assets of $27.6 billion, showcasing the scale of their diversified operations.

Strong Regional Market Presence

Fulton Bank boasts a significant and focused presence across key Mid-Atlantic states, including Pennsylvania, Maryland, Delaware, New Jersey, and Virginia. This regional concentration is more than just a footprint; it's a strategic advantage, enabling the bank to cultivate deep local relationships and acquire intimate knowledge of these markets. For instance, as of Q1 2024, Fulton Bank held approximately $27 billion in total assets, with a substantial portion of its loan and deposit base concentrated within these core states, underscoring its established regional strength.

Established Brand and Customer Trust

Fulton Bank's established brand and deep-rooted customer trust are significant strengths. As a financial institution with a long history, it has cultivated a reputation that translates into loyalty and a reduced cost of acquiring new customers. This trust is a vital asset in the banking industry, often leading to organic growth through positive referrals.

Stable Financial Holding Company Structure

Fulton Financial Corporation (Fulton Bank's parent) operates as a stable financial holding company, providing a regulated structure for its diverse banking and non-banking subsidiaries. This allows for efficient capital allocation and strategic integration of acquired businesses, fostering operational synergies across its footprint.

This holding company model is a key strength, supporting Fulton's capacity for strategic growth and financial stability. For instance, as of Q1 2024, Fulton Financial Corporation reported total assets of $28.2 billion, showcasing the scale and breadth of its operations managed under this structure.

- Robust Regulatory Framework: The holding company structure subjects Fulton to stringent regulatory oversight, enhancing trust and confidence among stakeholders.

- Strategic Agility: It facilitates the acquisition and integration of new financial services or geographic markets, as seen in past expansion efforts.

- Operational Synergies: Centralized management and shared resources across subsidiaries can lead to cost efficiencies and improved service delivery.

- Long-Term Stability: The diversified nature of a holding company can buffer against sector-specific downturns, promoting sustained financial health.

Community-Centric Banking Approach

Fulton Bank's dedication to a community-centric banking model is a significant strength, fostering deep relationships with local businesses and individuals. This localized focus translates into robust customer loyalty and a dependable deposit base, as evidenced by its strong presence in its operating regions.

This community-first strategy allows Fulton Bank to keenly understand and respond to the unique economic conditions and needs of its service areas. For instance, in 2024, the bank continued to prioritize small business lending, contributing to local economic growth and solidifying its position as a trusted financial partner. This tailored approach differentiates Fulton Bank from larger, national institutions by offering more personalized financial solutions.

- Deep Community Ties: Fulton Bank's emphasis on local engagement strengthens customer relationships.

- Stable Deposit Base: Community focus leads to higher customer retention and a more reliable deposit foundation.

- Tailored Financial Products: Understanding local economic nuances enables customized service offerings.

- Competitive Differentiation: This approach sets Fulton Bank apart from larger, less personalized national competitors.

Diversified Strategy Fuels Bank's Growth and Stability

Fulton Bank's diverse service portfolio, encompassing community banking, investment management, and insurance, creates multiple revenue streams. This diversification, as shown by Fulton Financial Corporation's $28.2 billion in total assets in Q1 2024, reduces reliance on any single area and broadens its customer reach.

The bank's strong regional presence in Mid-Atlantic states like Pennsylvania and Maryland is a key advantage, fostering deep local relationships and market knowledge. This concentration, with approximately $27 billion in assets as of Q1 2024, allows for tailored services and a stable customer base.

Fulton Bank benefits from significant brand recognition and established customer trust, a result of its long history. This trust translates into customer loyalty and organic growth through positive referrals, a critical asset in the competitive banking sector.

The holding company structure of Fulton Financial Corporation provides a stable, regulated framework for its subsidiaries. This structure facilitates efficient capital allocation and integration of acquisitions, enhancing operational synergies and long-term financial health.

What is included in the product

Analyzes Fulton Bank’s competitive position through key internal and external factors, highlighting its strengths, weaknesses, opportunities, and threats.

Offers a clear, actionable framework to identify and address Fulton Bank's competitive challenges and capitalize on opportunities.

Weaknesses

Geographic Concentration Risk

Fulton Bank's significant geographic concentration in a few Mid-Atlantic states, particularly Pennsylvania, creates a notable weakness. This focus means the bank is more susceptible to regional economic downturns or industry-specific challenges within these concentrated areas. For instance, a slowdown in Pennsylvania's key industries could disproportionately affect Fulton's loan portfolio and overall financial performance.

Competition from Larger Institutions and Fintechs

Fulton Bank operates in a fiercely competitive banking landscape. It contends with larger national banks that possess considerably more financial resources and a wider customer base, making it harder for Fulton to expand its market share. For instance, as of Q1 2024, the top five U.S. banks by assets held over $10 trillion in total assets, dwarfing regional banks like Fulton.

The increasing influence of fintech companies presents another significant challenge. These agile innovators frequently introduce cutting-edge digital banking solutions, often targeting younger, tech-savvy consumers who may be less inclined to use traditional banking services. This trend puts pressure on Fulton to continually invest in and upgrade its own digital offerings to remain relevant and competitive.

This intense competitive environment can compress Fulton Bank's profit margins and create hurdles in attracting and retaining customers. Staying ahead of rapid technological advancements in the financial sector demands substantial and ongoing investment, which can strain resources for institutions of Fulton's size.

Potential for Slower Digital Transformation

Fulton Bank, like many regional institutions, might experience a slower digital transformation compared to nimble fintechs or larger banks with vast IT resources. This lag could translate into less intuitive customer experiences, potentially deterring digitally inclined customers. For instance, in 2024, the banking sector saw significant investment in AI and cloud-based solutions, areas where smaller banks may struggle to keep pace without substantial capital allocation.

Reliance on Net Interest Margin

Fulton Bank, like many traditional financial institutions, faces a significant weakness in its heavy reliance on net interest margin (NIM). This metric, representing the difference between interest income from loans and investments and interest paid on deposits and borrowings, forms a substantial part of its revenue. For instance, in the first quarter of 2024, net interest income was a primary driver of profitability for many regional banks, but this also highlights their vulnerability to interest rate shifts.

This dependence makes Fulton Bank susceptible to the volatility of interest rates. A prolonged period of low interest rates, as seen in recent years, can compress NIM and stifle profitability. Conversely, rapid increases in rates, while potentially boosting NIM, can also lead to higher funding costs and increased competition for deposits, creating a delicate balancing act. This sensitivity to monetary policy decisions is a key challenge.

- NIM Sensitivity: Fulton Bank's profitability is directly tied to interest rate movements, impacting its core revenue stream.

- Monetary Policy Impact: Changes in Federal Reserve policy can significantly compress or expand the bank's NIM.

- Competitive Pressure: Rising rates can intensify competition for deposits, potentially increasing Fulton's cost of funds.

Branch Network Overhead Costs

Fulton Bank's extensive physical branch network, while fostering customer relationships, presents a significant weakness due to high overhead costs. These costs encompass rent, utilities, and staffing for each location, contributing to a less efficient operational model compared to purely digital banking channels. In 2023, for instance, regional banks often saw their non-interest expenses rise, with a portion directly attributable to branch maintenance.

The ongoing shift towards digital banking further exacerbates this weakness. As more customers opt for online and mobile services, the foot traffic in physical branches may decline, making the substantial investment in maintaining these locations less justifiable. This trend puts pressure on profitability, as these fixed costs continue to accrue even with reduced in-person activity.

- Branch Network Overhead: Significant costs associated with rent, utilities, and staffing for physical locations.

- Efficiency Gap: Branches are generally less cost-efficient than digital channels for many banking transactions.

- Impact of Digital Adoption: Declining branch traffic due to increased digital usage can strain profitability.

- Optimization Challenge: Balancing the need for physical presence with the drive for digital efficiency is a persistent hurdle.

Regional Banking's Hurdles: Concentration, Costs, and Competition

Fulton Bank's geographic concentration in a few Mid-Atlantic states, particularly Pennsylvania, makes it vulnerable to regional economic downturns. This limited reach also hinders its ability to diversify its customer base and revenue streams effectively, unlike larger national competitors. For instance, as of Q1 2024, the bank's primary market performance heavily influences its overall financial health.

The bank faces intense competition from larger national banks and agile fintech companies. These competitors often have greater financial resources, wider customer bases, and more advanced digital offerings, creating a challenging environment for Fulton to expand market share and attract new customers. In 2024, the banking sector saw significant investment in digital transformation, an area where regional banks like Fulton may lag.

Fulton Bank's reliance on its Net Interest Margin (NIM) makes it susceptible to interest rate fluctuations. While a higher NIM can boost profits, it also means the bank is highly sensitive to changes in monetary policy, which can compress margins or increase funding costs. This sensitivity was evident in Q1 2024, where interest rate movements significantly impacted regional bank profitability.

Maintaining an extensive physical branch network, while beneficial for customer relationships, results in high overhead costs. These costs, including rent, utilities, and staffing, can make Fulton Bank less efficient than digital-first competitors. As customer preferences shift towards digital banking, the profitability of these physical locations faces increasing pressure.

Full Version Awaits

Fulton Bank SWOT Analysis

This is the actual Fulton Bank SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and actionable insights.

The preview below is taken directly from the full SWOT report you'll get, showcasing the comprehensive evaluation of Fulton Bank's strategic position. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete Fulton Bank SWOT analysis. Once purchased, you’ll receive the full, editable version, ready for your strategic planning.

Opportunities

Expansion of Digital Banking Services

Fulton Bank can capitalize on the growing demand for digital financial solutions by investing in its online and mobile banking platforms. This includes enhancing features like mobile check deposit, peer-to-peer payments, and personalized financial management tools. By offering a seamless and intuitive digital experience, Fulton can attract and retain a younger, tech-savvy demographic, which is crucial for long-term growth. For instance, as of Q1 2024, the global digital banking market was valued at over $25 trillion, with mobile banking transactions alone projected to reach $10 trillion annually by 2025, indicating a substantial opportunity for banks to expand their digital reach.

Strategic Acquisitions and Partnerships

Fulton Bank can pursue strategic acquisitions of smaller community banks or fintech firms to broaden its market presence and service capabilities. For instance, in 2024, the banking sector saw significant consolidation activity, with many regional banks looking to scale. Integrating new technologies through acquisition or partnership can significantly boost Fulton's competitive edge.

Partnering with fintech innovators offers a pathway to rapid technological advancement, potentially integrating advanced digital banking solutions or AI-driven customer service tools. This approach allows Fulton to leverage external expertise and innovation, accelerating its digital transformation efforts without the substantial capital outlay of full in-house development. Such collaborations are increasingly vital in the rapidly evolving financial services landscape.

Growth in Wealth Management and Insurance Segments

Fulton Bank can capitalize on the growing demand for wealth management and insurance services, leveraging its established customer relationships to cross-sell these offerings. The bank's existing client base presents a significant opportunity to expand its investment management and insurance segments, thereby increasing non-interest income.

As individuals and families navigate increasingly complex financial landscapes, offering comprehensive wealth planning and protection solutions can foster deeper client loyalty and create new revenue streams. These segments typically boast higher profit margins, contributing to a more robust and diversified income structure for Fulton Bank.

By developing tailored wealth management and insurance products, Fulton Bank can attract and retain high-net-worth individuals, further solidifying its position in these lucrative markets. For instance, the U.S. wealth management industry is projected to reach $73.7 trillion in assets under management by 2027, according to industry reports.

Targeting Niche Lending Markets

Fulton Bank can capitalize on opportunities by strategically targeting niche lending markets. By focusing on specialized areas like commercial real estate for specific industries, healthcare facilities, or renewable energy projects, the bank could potentially achieve higher yields due to less competition. This approach requires developing deep expertise to gain a competitive edge and diversify its loan book effectively.

Expanding into these specialized segments can unlock new revenue streams for Fulton Bank. For instance, the U.S. market for green bonds and sustainable finance is projected to continue its robust growth through 2025, offering significant lending opportunities. Similarly, healthcare real estate financing has seen consistent demand, with the sector's financing needs expected to remain strong.

- Focus on High-Yield Segments: Identifying and serving niche lending markets can lead to better risk-adjusted returns compared to broader, more commoditized lending.

- Competitive Differentiation: Developing specialized knowledge in areas like healthcare or sustainable energy financing can set Fulton Bank apart from competitors.

- Portfolio Diversification: Entering niche markets helps spread risk across different economic sectors, making the bank more resilient.

- Market Growth Potential: Sectors like renewable energy financing are experiencing significant growth, presenting substantial opportunities for expansion.

Leveraging Data Analytics for Personalized Services

Leveraging advanced data analytics presents a significant opportunity for Fulton Bank to deepen its understanding of customer behavior and financial needs. This allows for the creation of highly personalized product offerings and tailored financial advice, directly boosting customer satisfaction and fostering stronger loyalty. For instance, by analyzing transaction data, Fulton Bank can anticipate upcoming needs, such as offering a mortgage pre-approval to a customer showing increased savings, a strategy that aligns with the broader industry trend of hyper-personalization in financial services.

Data-driven insights also offer a powerful avenue for optimizing risk management protocols and refining marketing strategies. By identifying patterns in customer data, the bank can more accurately assess creditworthiness and tailor marketing campaigns to specific customer segments, increasing conversion rates and reducing wasted expenditure. In 2024, many financial institutions reported improved ROI on marketing campaigns after implementing advanced analytics, with some seeing a 15-20% uplift in engagement metrics.

Furthermore, this enhanced analytical capability can unlock new market opportunities and drive product innovation. Understanding emerging trends and unmet customer needs through data analysis allows Fulton Bank to proactively develop and launch relevant financial products and services. The bank's investment in a robust data infrastructure is crucial to realizing these benefits, ensuring the secure and efficient processing of vast amounts of customer information.

Key opportunities include:

- Enhanced Customer Segmentation: Deeper insights into customer demographics, transaction history, and life events for hyper-targeted product development.

- Proactive Financial Guidance: Utilizing predictive analytics to offer timely advice on investments, savings, and loan products based on individual financial trajectories.

- Optimized Risk Assessment: Improving credit scoring models and fraud detection through sophisticated data analysis, leading to reduced losses.

- Personalized Marketing Campaigns: Delivering tailored promotions and communications that resonate with individual customer preferences, increasing engagement and conversion.

Unlocking Growth: Digital, Strategic, and Niche Opportunities for Banks

Fulton Bank can significantly expand its market reach and customer base by embracing digital transformation and enhancing its online and mobile banking capabilities. This strategic focus on digital solutions aligns with a global trend, as the digital banking market was valued at over $25 trillion in Q1 2024, with mobile banking transactions projected to hit $10 trillion annually by 2025.

The bank can also pursue growth through strategic acquisitions of smaller financial institutions or fintech companies, a strategy that saw considerable activity in the 2024 banking sector as regional players sought to scale. Additionally, forming partnerships with fintech innovators can accelerate the adoption of advanced technologies, such as AI-driven customer service, allowing Fulton to leverage external expertise for rapid digital transformation.

Expanding into wealth management and insurance services offers a substantial opportunity to increase non-interest income by cross-selling to its existing customer base. The U.S. wealth management industry is on track to reach $73.7 trillion in assets under management by 2027, highlighting the lucrative potential of this segment.

Fulton Bank has an opportunity to capitalize on niche lending markets, such as commercial real estate for specific industries or renewable energy projects, which can yield higher returns due to reduced competition. The market for sustainable finance, including green bonds, is experiencing robust growth through 2025, presenting significant lending avenues.

Leveraging advanced data analytics is key to understanding customer behavior for personalized product offerings and improved financial advice, fostering loyalty. This data-driven approach also optimizes risk management and marketing strategies, with financial institutions reporting up to a 20% increase in engagement metrics from advanced analytics in 2024.

| Opportunity Area | Key Drivers | Market Data/Projections |

|---|---|---|

| Digital Banking Enhancement | Growing demand for online/mobile services | Global digital banking market > $25T (Q1 2024); Mobile transactions to reach $10T by 2025 |

| Strategic Acquisitions/Partnerships | Industry consolidation, fintech integration | Significant M&A activity in regional banking (2024) |

| Wealth Management & Insurance | Cross-selling to existing base, higher profit margins | U.S. Wealth Management AUM to reach $73.7T by 2027 |

| Niche Lending Markets | Higher yields, diversification | Strong growth in sustainable finance markets through 2025 |

| Data Analytics & Personalization | Customer insights, improved risk/marketing | 15-20% uplift in engagement metrics reported by users of advanced analytics (2024) |

Threats

Economic Downturn and Credit Quality Deterioration

A significant economic downturn in Fulton Bank's core markets, particularly Pennsylvania and New Jersey, poses a substantial threat. Projections for 2024 indicate a potential slowdown, with some economists forecasting GDP growth below 2% for the US. This could translate to increased loan defaults and a rise in non-performing assets for Fulton Bank, directly impacting its asset quality and profitability.

Should a recession materialize, demand for banking services like loans and mortgages might also decrease, further squeezing revenue streams. For instance, a 1% increase in unemployment in Fulton's operating regions could lead to a noticeable uptick in delinquency rates across its loan portfolio, necessitating higher loan loss provisions and consequently eroding earnings per share.

Interest Rate Volatility and Net Interest Margin Compression

Interest rate volatility poses a significant threat to Fulton Bank's profitability by compressing its net interest margin. For instance, if interest rates were to remain low throughout 2024, the bank's ability to earn income on its loan portfolio would be constrained. Conversely, a rapid rise in rates in 2025 could increase Fulton Bank's cost of funds more quickly than it can adjust the yields on its existing assets, squeezing margins.

This dynamic directly impacts the bank's core revenue stream. For example, if Fulton Bank's net interest margin, which stood at approximately 3.15% in Q1 2024, were to decline by 20 basis points due to rate changes, it could translate to millions in lost earnings. Effectively managing the bank's assets and liabilities is therefore paramount to navigating these unpredictable market conditions.

Increased Regulatory Burden and Compliance Costs

Fulton Bank, like all financial institutions, faces an increasing regulatory burden. In 2024, the financial sector continued to grapple with evolving rules around capital requirements, consumer data privacy, and anti-money laundering efforts. These regulations demand significant investment in compliance technology and skilled personnel, impacting operational efficiency.

The cost of adhering to these complex frameworks can be substantial. For instance, investments in enhanced cybersecurity and data governance to meet new privacy standards are ongoing necessities. Failure to comply can lead to severe penalties, with fines in the millions of dollars being common across the industry for breaches, alongside significant damage to a bank's reputation.

Intensified Competition from Non-Bank Lenders and Fintechs

Fulton Bank confronts intensified competition not only from traditional banks but also from a surge of non-bank lenders and agile fintech companies. These new players, often unburdened by legacy systems and regulatory overheads, are rapidly capturing market share by offering streamlined, specialized services in areas like digital payments, peer-to-peer lending, and investment platforms. For instance, the global fintech market was projected to reach approximately $1.5 trillion in 2024, highlighting the significant scale of this disruption.

These fintechs and non-bank lenders can innovate at a pace that traditional institutions often struggle to match, directly impacting Fulton's ability to retain customers in key product segments. This dynamic necessitates a strategic response to maintain market relevance and profitability.

- Fintech lending growth: The U.S. fintech lending market has seen substantial growth, with some estimates suggesting it could reach hundreds of billions of dollars annually by 2025, directly challenging incumbent banks.

- Specialized offerings: Fintechs excel at targeting niche customer needs, offering faster loan approvals or more user-friendly investment tools, which can draw away valuable customer relationships.

- Lower operational costs: Many fintechs operate with significantly lower overheads compared to traditional banks, allowing them to offer more competitive pricing.

Cybersecurity Risks and Data Breaches

As a financial institution, Fulton Bank faces significant cybersecurity risks, including the potential for data breaches, ransomware attacks, and various forms of fraud. These threats are amplified given the sensitive nature of customer financial information. For instance, the financial services sector consistently ranks among the most targeted industries for cyberattacks. In 2023, reports indicated a substantial increase in the average cost of a data breach, reaching millions of dollars, a figure that continues to be a concern for institutions like Fulton Bank.

A successful cyberattack could result in substantial financial losses for Fulton Bank, not only from direct theft or operational disruption but also from regulatory fines and legal liabilities. Beyond monetary damages, the reputational impact and the erosion of customer trust can be even more detrimental, potentially leading to customer attrition. The banking industry experienced a notable rise in phishing and malware attacks in late 2024, highlighting the persistent and evolving nature of these threats.

To mitigate these risks, Fulton Bank must prioritize continuous investment in robust cybersecurity measures and comprehensive disaster recovery plans. This includes advanced threat detection systems, regular security audits, employee training, and secure data storage solutions. The financial sector is increasingly adopting AI-powered security tools to proactively identify and neutralize threats before they can impact operations. For example, many banks are allocating upwards of 10-15% of their IT budgets specifically to cybersecurity initiatives to stay ahead of sophisticated cybercriminal tactics.

- Data Breach Impact: The average cost of a data breach in the financial sector in 2023 was estimated to be over $5 million, underscoring the financial exposure.

- Targeted Attacks: Financial institutions are prime targets due to the high value of the data they hold.

- Reputational Damage: A breach can severely damage customer trust, leading to long-term business consequences.

- Investment in Security: Proactive and continuous investment in cybersecurity is crucial for operational integrity and customer data protection.

Navigating Financial Headwinds: Fintech, Economy, and Cyber Threats

Intensified competition from fintech firms and non-bank lenders presents a significant threat, as these entities often operate with lower overheads and greater agility. The global fintech market was projected to reach approximately $1.5 trillion in 2024, indicating the scale of this challenge. These competitors can innovate rapidly, potentially eroding Fulton Bank's market share in key product areas like lending and payments.

Fulton Bank must also contend with a challenging macroeconomic environment, including potential economic slowdowns in its core markets of Pennsylvania and New Jersey. Projections for 2024 suggested GDP growth below 2% for the US, which could lead to higher loan defaults. Furthermore, interest rate volatility can compress the bank's net interest margin; for example, a 20 basis point decline in the margin, which was around 3.15% in Q1 2024, could mean millions in lost earnings.

Increasing regulatory requirements demand substantial investment in compliance technology and personnel, impacting operational efficiency and potentially leading to significant fines for non-compliance. Cybersecurity risks, including data breaches and ransomware attacks, are also a major concern, with the financial sector being a prime target. The average cost of a data breach in finance exceeded $5 million in 2023, underscoring the financial and reputational exposure.

SWOT Analysis Data Sources

This SWOT analysis is built upon a robust foundation of data, drawing from Fulton Bank's official financial statements, comprehensive market research reports, and expert analyses of the banking industry to provide a well-rounded perspective.