EL AL Isreal Airline Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

EL AL Isreal Airline

From Overview to Strategy Blueprint

EL AL Israel Airline faces a complex competitive landscape, with significant pressure from rivals and powerful buyers influencing pricing. Understanding the strength of these forces is crucial for strategic planning.

The complete report reveals the real forces shaping EL AL Isreal Airline’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Aircraft Manufacturers Duopoly

The bargaining power of suppliers in the aircraft manufacturing sector is exceptionally high for airlines like EL AL, primarily due to the industry's duopoly structure dominated by Boeing and Airbus. These two giants control the vast majority of the global commercial aircraft market, leaving airlines with very few alternatives for their fleet needs.

The immense capital investment required for aircraft acquisition, coupled with lengthy manufacturing and delivery timelines, significantly amplifies the suppliers' leverage. For instance, a new wide-body aircraft can cost upwards of $300 million, and lead times for custom orders can extend for years, making it difficult for EL AL to switch suppliers quickly if faced with unfavorable terms.

EL AL's dependence on these manufacturers for new aircraft, spare parts, and maintenance services further solidifies Boeing and Airbus's strong position. The specialized nature of their products and the high costs associated with transitioning to a different manufacturer's ecosystem create substantial switching costs, limiting EL AL's ability to negotiate favorable pricing or contract conditions.

Fuel Price Volatility and Suppliers

Fuel is a significant expense for EL AL, directly impacting its bottom line. In 2024, jet fuel prices experienced considerable volatility, influenced by global supply concerns and geopolitical tensions. This volatility means suppliers hold substantial leverage, as the price of the underlying commodity is largely outside EL AL's control.

While EL AL sources fuel from various providers, the global market price for oil and refined jet fuel dictates terms. For instance, during periods of high crude oil prices, such as those seen in early 2024 due to increased demand and supply chain disruptions, suppliers are in a stronger position to pass on these costs.

EL AL's profitability is therefore highly sensitive to these fuel price fluctuations. Suppliers can leverage market conditions to dictate pricing and payment terms, potentially squeezing EL AL's margins if the airline cannot adequately pass these costs onto passengers through higher ticket prices.

Specialized MRO and Technology Providers

EL AL relies on specialized Maintenance, Repair, and Overhaul (MRO) providers and technology vendors for critical operational software. These suppliers often possess unique expertise or proprietary systems, making it costly and disruptive for EL AL to switch to alternatives.

The concentration of these specialized services means that a limited number of providers can exert significant bargaining power. For instance, in 2024, the global MRO market was valued at approximately $100 billion, with a significant portion driven by highly specialized technical services, indicating the potential leverage of key players.

Airport Services and Infrastructure

Airports frequently function as monopolies or duopolies, especially in smaller or more remote locations. This concentrated market power allows them to exert significant influence over airlines by controlling access to vital services such as landing slots, baggage handling, and air traffic control. For EL AL, this means a reliance on airport authorities for operational continuity, enabling airports to dictate terms and fees.

The bargaining power of airport suppliers is considerable, as airlines like EL AL often have limited alternatives for essential ground operations. For instance, in 2024, airport landing and handling fees can represent a substantial portion of an airline's operating costs, sometimes ranging from 5% to 15% depending on the airport's location and service level. This dependence translates into a strong position for airports to negotiate pricing and service agreements.

- Monopolistic Control: Airports often hold exclusive rights to provide critical services at specific locations.

- Essential Services: Airlines depend on airports for landing, takeoff, ground handling, and passenger services.

- Cost Impact: Airport fees can be a significant operational expense for airlines, impacting profitability.

- Limited Alternatives: Airlines have few substitutes for airport infrastructure, strengthening supplier power.

Labor Unions and Skilled Personnel

EL AL, like many airlines, operates in a sector heavily reliant on skilled labor. The bargaining power of suppliers, particularly in the form of labor unions and specialized personnel, is a critical factor. Unions representing pilots, cabin crew, and maintenance engineers can wield considerable influence due to the specialized training and certifications required for these roles.

The aviation industry is inherently labor-intensive, and shortages of highly skilled professionals, such as certified aircraft mechanics or experienced pilots, can amplify the bargaining power of these workers. This dynamic can translate into increased labor costs for EL AL, impacting operational efficiency and profitability. For instance, in 2023, global pilot shortages contributed to increased recruitment and retention costs for airlines worldwide.

- Skilled Workforce Dependence: Aviation requires specialized skills, making personnel a significant supplier group.

- Union Influence: Strong unions representing key employee groups can negotiate favorable terms, impacting labor costs.

- Personnel Shortages: Scarcity of pilots or mechanics can empower unions and increase wage demands.

- Operational Risk: Labor disputes or strikes stemming from bargaining power can lead to flight cancellations and disruptions for EL AL.

EL AL's Supplier Power Challenges: Costs, Control, and Constraints

The bargaining power of suppliers for EL AL is significant across several key areas, including aircraft manufacturers, fuel providers, specialized maintenance services, and labor. The concentrated nature of aircraft manufacturing, dominated by Boeing and Airbus, grants them immense leverage due to the high capital costs and long lead times associated with fleet acquisition, making switching suppliers extremely difficult and expensive for EL AL.

Fuel costs represent a substantial operational expense for EL AL, and suppliers in this sector hold considerable power due to global market price volatility. In 2024, fluctuations in jet fuel prices, influenced by geopolitical events and supply concerns, directly impacted EL AL's profitability, as suppliers could pass on increased costs, limiting the airline's ability to control this critical expense.

EL AL also faces strong supplier power from specialized MRO providers and technology vendors. The unique expertise and proprietary systems offered by these entities create high switching costs, reinforcing the suppliers' ability to dictate terms. Furthermore, the bargaining power of labor, particularly represented by unions for pilots and engineers, is amplified by the specialized skills required and potential personnel shortages, as seen in the global pilot shortages contributing to increased labor costs in 2023.

| Supplier Category | Key Factors Amplifying Power | Impact on EL AL | 2024/Recent Data Point |

|---|---|---|---|

| Aircraft Manufacturers (Boeing, Airbus) | Industry duopoly, high capital investment, long lead times, specialized technology | Limited alternatives, high switching costs, significant influence on fleet acquisition costs | New wide-body aircraft can exceed $300 million, with multi-year delivery backlogs. |

| Fuel Suppliers | Global commodity price volatility, geopolitical influences, supply chain disruptions | Direct impact on operating costs, potential margin squeeze if costs cannot be passed on | Jet fuel prices in 2024 showed significant volatility due to increased demand and supply concerns. |

| Specialized MRO & Technology Providers | Unique expertise, proprietary systems, high integration costs | Dependence on specific providers for critical maintenance and software, limiting flexibility | The global MRO market, valued around $100 billion in 2024, includes highly specialized technical services. |

| Labor (Pilots, Engineers, Crew) | Specialized skills, certifications, unionization, potential labor shortages | Increased labor costs, potential for operational disruptions due to negotiations or disputes | Global pilot shortages in 2023 led to higher recruitment and retention expenses for airlines. |

What is included in the product

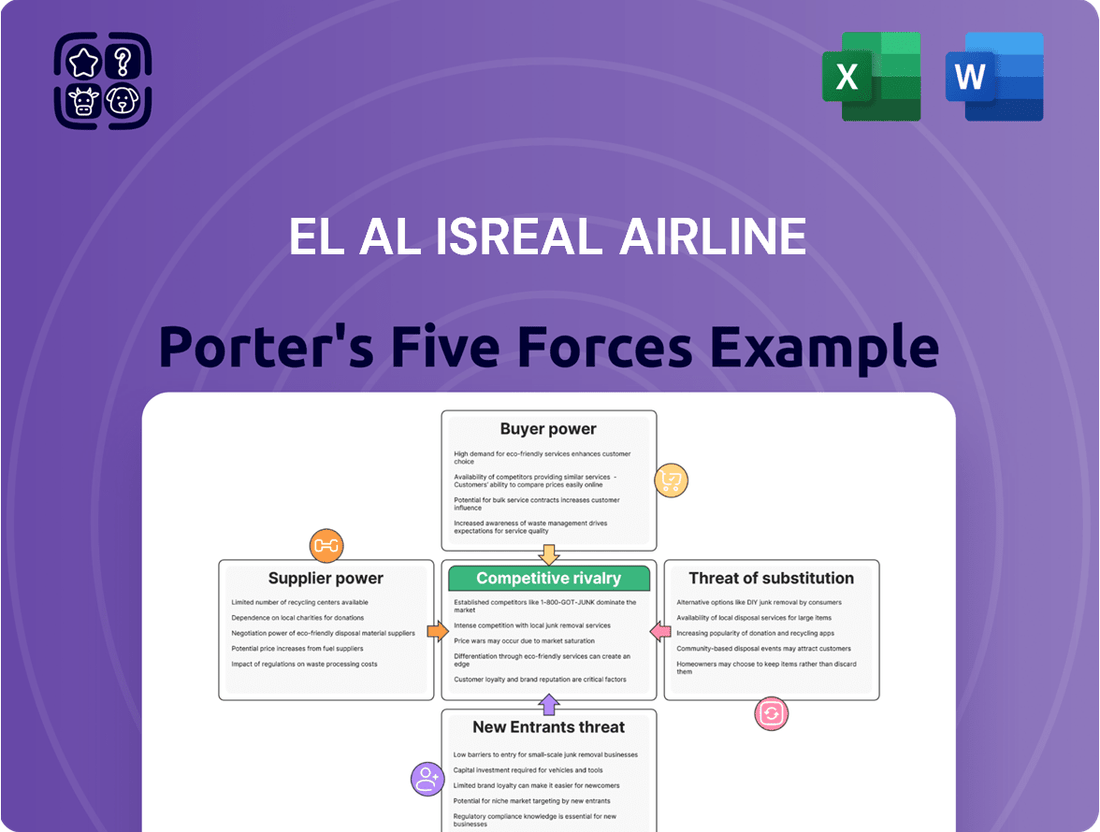

Tailored exclusively for EL AL Isreal Airline, analyzing its position within its competitive landscape by examining buyer and supplier power, the threat of new entrants and substitutes, and existing rivalry.

Gain a dynamic understanding of competitive pressures by visualizing EL AL's Porter's Five Forces with interactive sliders for bargaining power and threat levels.

Effortlessly identify strategic vulnerabilities and opportunities within EL AL's competitive landscape through a visually intuitive, customizable five forces matrix.

Customers Bargaining Power

Price-Sensitive Leisure Travelers

Price-sensitive leisure travelers wield significant bargaining power. They readily compare fares across numerous airlines using online travel agencies and flight comparison sites, a trend that intensified in 2024 with increased digital adoption. This ease of comparison, coupled with the availability of many competing carriers flying to and from Israel, compels EL AL to maintain competitive pricing and offer frequent promotions to attract this segment.

Corporate and Business Travel Demand

While business travelers are often less concerned with price, major corporations wield significant bargaining power. They can negotiate better deals and service packages with airlines like EL AL. For instance, in 2024, corporate travel spending globally was projected to reach over $1.4 trillion, highlighting the immense value of this segment.

EL AL needs to meet the specific needs of these corporate clients. This includes offering flexible booking options, premium services, and attractive loyalty programs. Failing to cater to these demands could mean losing out on substantial revenue streams from large business accounts.

Cargo Clients' Negotiation Leverage

Cargo clients, particularly those with substantial or ongoing shipping demands, possess significant negotiation power when it comes to air freight rates. For instance, in 2024, major logistics providers often secure bulk discounts due to the sheer volume of shipments they consolidate, directly impacting EL AL's pricing flexibility.

This leverage is amplified by the availability of multiple cargo carriers and alternative shipping methods, allowing clients to easily switch providers if EL AL's offerings are not competitive. The global air cargo market in 2024 saw capacity fluctuate, giving larger shippers more options and thus more bargaining power.

Consequently, EL AL's cargo division is compelled to consistently deliver efficient, reliable, and cost-effective air freight solutions to maintain the loyalty of these high-value clients. Failure to do so could result in a loss of significant revenue streams, as clients can readily explore more attractive alternatives.

Impact of Online Travel Agencies (OTAs)

Online Travel Agencies (OTAs) and aggregators significantly amplify customer bargaining power by consolidating demand. This concentration gives them considerable leverage over pricing and distribution, forcing airlines like EL AL to negotiate terms that often include substantial commissions. For instance, in 2024, commission rates from major OTAs typically ranged from 15% to 30%, directly impacting EL AL's net revenue per ticket.

EL AL's reliance on these platforms for broad customer reach means they must balance the benefits of visibility against the cost of these commissions. This dynamic effectively transforms the collective customer base, channeled through OTAs, into a powerful negotiating bloc. The ability of OTAs to compare prices across multiple airlines also intensifies price competition, further empowering consumers and pressuring EL AL's margins.

- Consolidation of Demand: OTAs aggregate traveler searches, creating a unified front for customer price sensitivity.

- Commission Pressure: In 2024, typical OTA commissions for airlines ranged between 15% and 30%, directly reducing EL AL's revenue.

- Distribution Channel Control: OTAs dictate terms for visibility and booking, influencing how EL AL reaches its customers.

- Price Transparency: Aggregators enable easy comparison, increasing pressure on EL AL to offer competitive pricing.

Availability of Competing Routes and Airlines

The availability of numerous competing airlines on EL AL's international routes significantly amplifies customer bargaining power. For instance, when flying from Tel Aviv to London, passengers can choose from carriers like British Airways, Virgin Atlantic, or even budget options, forcing EL AL to remain competitive on pricing and service. This wide selection allows customers to easily switch to a more attractive offer, putting pressure on EL AL to meet or beat competitor deals.

In 2024, the global airline industry saw continued passenger growth, with approximately 4.7 billion travelers expected. This high volume of air travel, coupled with the presence of many carriers on popular international corridors, gives consumers substantial leverage. For example, on routes like Tel Aviv to New York, customers can compare options from EL AL, United, Delta, and others, readily switching for better fares or flight times.

- Customer Choice: Multiple airlines on international routes provide passengers with a broad spectrum of choices.

- Price Sensitivity: The ease of comparison makes customers highly sensitive to price differences between carriers.

- Service Differentiation: Beyond price, customers can select airlines based on flight schedules, onboard services, and loyalty programs.

Customer Power Shapes EL AL's Market Strategy

The bargaining power of customers for EL AL Israel Airlines is substantial, driven by price-sensitive leisure travelers and powerful corporate clients. Online Travel Agencies (OTAs) and route competition further amplify this influence, compelling EL AL to offer competitive pricing and tailored services.

| Customer Segment | Bargaining Power Drivers | Impact on EL AL |

|---|---|---|

| Leisure Travelers | Price comparison sites, numerous airline options | Pressure on fares, need for promotions |

| Corporate Clients | Volume purchasing, negotiation of service packages | Need for customized deals, premium services |

| OTAs & Aggregators | Consolidation of demand, distribution control | Commission costs, reduced pricing flexibility |

| International Route Competition | Availability of multiple carriers, ease of switching | Intensified price competition, service differentiation imperative |

Preview the Actual Deliverable

EL AL Isreal Airline Porter's Five Forces Analysis

This preview shows the exact EL AL Israel Airline Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. You'll gain a comprehensive understanding of the competitive landscape, including the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the airline industry, all presented in a professionally formatted document.

Rivalry Among Competitors

Intense Competition on Key Routes

EL AL Israel Airlines navigates a highly competitive landscape, particularly on its lucrative routes connecting Israel with Europe, North America, and Asia. Major international carriers, alongside a growing number of budget airlines, vie for market share, often triggering price wars and aggressive promotional campaigns.

This intense rivalry forces EL AL to continuously innovate its service offerings and customer experience to stand out. For instance, in 2024, the airline continued to invest in cabin upgrades and digital services to enhance passenger satisfaction amidst the pressure from competitors like Turkish Airlines and Ryanair, who have significant presence on many of EL AL's key international corridors.

Rise of Low-Cost Carriers (LCCs)

The rise of Low-Cost Carriers (LCCs) like Wizz Air and Ryanair has dramatically reshaped the Israeli airline market. These carriers often target price-sensitive travelers, offering significantly lower base fares than full-service carriers such as EL AL. For instance, in 2024, LCCs continued to expand their routes and capacity into and out of Ben Gurion Airport, directly challenging EL AL on popular European destinations.

This intensified competition forces EL AL to be more strategic with its pricing, especially on routes where LCCs have a strong foothold. While EL AL maintains a focus on premium services and long-haul routes, the aggressive pricing by LCCs directly impacts its ability to capture market share on shorter, more competitive segments, potentially pressuring yields.

Capacity Management and Pricing Strategies

EL AL Israel Airlines operates in a fiercely competitive landscape where airlines constantly adjust their flight schedules and ticket prices to fill seats and maximize earnings. This dynamic approach means EL AL must vigilantly track rivals' capacity expansions and pricing shifts to stay competitive.

For instance, in 2023, the global airline industry saw a significant rebound in passenger traffic, with IATA reporting a 37.6% increase in revenue passenger kilometers compared to 2022. This surge in demand intensifies the need for effective capacity management and aggressive pricing by all carriers, including EL AL.

Such intense rivalry, particularly concerning capacity and pricing, often leads to compressed profit margins and reduced yields for all players. Airlines might engage in price wars or over-capacity deployment to capture market share, directly impacting profitability.

Brand Loyalty vs. Price Sensitivity

EL AL Israel Airlines enjoys a certain level of brand loyalty, partly due to its national carrier status and its renowned security measures. However, this loyalty faces a significant challenge from a highly price-sensitive customer base, particularly in the leisure travel market. Balancing its unique offerings, such as kosher meals and its strong safety perception, with the necessity of competitive pricing against numerous rivals is a constant strategic hurdle.

The airline must navigate this tension effectively. For instance, while EL AL might attract passengers willing to pay a premium for perceived security and specific services, the broader market often prioritizes cost. This dynamic is evident in the competitive landscape where budget carriers frequently undercut established airlines on price, forcing EL AL to make difficult decisions regarding its fare structures and service packages to remain relevant.

- Brand Loyalty Drivers: National carrier status, perceived superior security, and unique service offerings like kosher meals contribute to a dedicated customer base for EL AL.

- Price Sensitivity Impact: A significant portion of travelers, especially in leisure segments, are highly influenced by price, leading to intense competition on fares.

- Competitive Pricing Challenge: EL AL must balance its brand equity and service differentiators against the need to offer competitive prices to attract a broader market share.

- Rivalry Dynamics: The presence of numerous airlines, including low-cost carriers, intensifies rivalry, putting pressure on EL AL to optimize its pricing strategies without alienating its loyal customer segment.

Global Airline Alliances and Partnerships

EL AL faces intense competition from airlines deeply integrated into global alliances like Star Alliance, SkyTeam, and Oneworld. These alliances provide passengers with vast route networks and integrated services, a significant advantage. For instance, in 2024, these major alliances collectively served over 1,000 destinations worldwide, offering a seamless travel experience that EL AL, as an independent carrier, must counter through strategic partnerships and distinct offerings.

EL AL's independent status necessitates a focus on bilateral agreements and unique selling propositions to compete. While alliances offer economies of scale and broader market reach, EL AL must leverage its strengths, such as its strong brand recognition in specific markets and potentially more flexible service offerings, to attract and retain customers. The airline's strategy in 2024 likely involves strengthening these individual relationships to bridge the gap created by the consolidated power of alliance members.

- Global Alliance Reach: Major alliances like Star Alliance, SkyTeam, and Oneworld connect over 1,000 destinations globally, providing extensive network benefits.

- EL AL's Strategy: The airline relies on bilateral agreements and unique selling propositions to compete against the integrated networks of alliance members.

- Competitive Pressure: Independent status requires EL AL to offer compelling value propositions to offset the network advantages enjoyed by alliance participants.

EL AL's Competitive Skies: Navigating Rivalry

Competitive rivalry is a significant force for EL AL Israel Airlines, with numerous international and low-cost carriers vying for passengers on key routes. This intense competition, particularly from airlines like Turkish Airlines and Ryanair, often leads to price wars and necessitates continuous service innovation from EL AL. For instance, the airline's investments in cabin upgrades in 2024 were a direct response to the pressure from these rivals.

The aggressive pricing strategies of Low-Cost Carriers (LCCs) such as Wizz Air and Ryanair continue to challenge EL AL, especially on popular European routes. These LCCs expanded their operations into and out of Ben Gurion Airport in 2024, directly impacting EL AL's ability to compete on price-sensitive segments and potentially reducing yields.

EL AL's independent status also means it must contend with the vast network advantages of global airline alliances like Star Alliance, SkyTeam, and Oneworld. These alliances collectively served over 1,000 destinations globally in 2024, offering seamless travel experiences that EL AL counters through bilateral agreements and unique service offerings to remain competitive.

| Key Competitor Type | Examples | Impact on EL AL | 2024 Trend Example |

| Major International Carriers | Turkish Airlines, Lufthansa | Price competition, network matching | Continued route expansion and service enhancements |

| Low-Cost Carriers (LCCs) | Ryanair, Wizz Air | Aggressive pricing, market share capture on leisure routes | Increased capacity on routes from Israel to Europe |

| Alliance Members | United Airlines (Star Alliance), Air France-KLM (SkyTeam) | Network reach, integrated loyalty programs | Global alliance networks serving over 1,000 destinations |

SSubstitutes Threaten

Virtual Communication and Remote Work

Advancements in virtual communication, such as high-definition video conferencing and immersive collaboration platforms, present a significant threat of substitution for traditional business travel. Companies are increasingly leveraging these technologies to conduct meetings, reducing the need for physical presence and thus impacting airline demand. For instance, by 2024, many businesses reported a substantial decrease in non-essential business travel, with virtual meetings becoming the norm for internal discussions and many client interactions.

Alternative Travel Modes for Shorter Distances (Conceptual)

While EL AL primarily focuses on long-haul international routes where direct substitutes are limited, the threat of alternative travel modes becomes more pronounced in shorter regional markets. For instance, globally, advancements in high-speed rail networks, like Japan's Shinkansen or Europe's TGV, offer competitive travel times and convenience for distances up to around 500-800 kilometers, directly challenging short-haul airline routes. In 2023, European rail passenger numbers saw a significant rebound, nearing pre-pandemic levels, indicating a strong consumer preference for rail where viable.

Although Israel's geographical constraints make extensive high-speed rail a less direct international substitute for EL AL, the broader airline industry faces this conceptual threat. For example, the expansion of efficient bus services and improved road infrastructure can also divert passengers on shorter domestic or near-international segments. The increasing focus on sustainable travel also fuels interest in these alternatives, potentially impacting overall air travel demand in specific segments.

Cruise Lines and Tour Packages

For leisure travelers, cruise lines and all-inclusive tour packages present a significant threat of substitutes to traditional air travel vacations. These options compete directly for a traveler's vacation budget and desired experience, potentially diverting customers who might otherwise book flights. For instance, the global cruise industry revenue was projected to reach $47.2 billion in 2024, showcasing its substantial appeal as an alternative holiday.

Economic Downturns Limiting Discretionary Travel

Economic downturns present a significant threat of substitutes for EL AL Israel Airlines by reducing overall demand for air travel. During periods of financial strain, both leisure and business travelers tend to cut back on non-essential trips, opting to save money instead of flying. This means the primary substitute isn't another airline, but rather the decision to forgo travel altogether.

For instance, a global economic slowdown, like the one experienced in 2023 and projected to continue with varying intensity into 2024, can severely impact discretionary spending. This directly affects EL AL's passenger volume and revenue potential as consumers prioritize essential expenses over vacations or non-critical business meetings. The airline must contend with a market where the choice to stay home becomes a powerful alternative to booking a flight.

- Reduced Consumer Spending: In 2023, global inflation and rising interest rates led to a noticeable tightening of household budgets, impacting discretionary spending on travel.

- Business Travel Cutbacks: Many companies implemented stricter travel policies in 2023 to control costs, leading to fewer business-related flights.

- Shift in Priorities: Consumers facing economic uncertainty may choose to allocate funds to savings or essential goods rather than leisure travel in 2024.

- Impact on Load Factors: A sustained economic downturn would likely lead to lower load factors for EL AL, as fewer passengers opt for flights.

Security Concerns and Travel Restrictions

Geopolitical instability and health crises represent significant threats to EL AL, acting as potent substitutes for traditional air travel. For instance, the heightened security concerns following events in the Middle East can lead passengers to seek alternative transportation or even cancel travel plans altogether. This was evident in 2023, where various global events impacted travel sentiment, pushing some consumers towards domestic or virtual alternatives.

When security concerns escalate, travelers may pivot to other forms of engagement that bypass international flights. This could include opting for domestic travel, utilizing video conferencing for business meetings, or choosing virtual entertainment over physical journeys. The perceived risk associated with air travel during such periods can make these substitutes more appealing, impacting demand for EL AL's services.

- Increased Security Scrutiny: Passengers may opt for destinations with less stringent security measures or choose alternative modes of transport if available.

- Health Crises Impact: Pandemics or localized health outbreaks can lead to border closures and travel advisories, pushing travelers to domestic or virtual alternatives.

- Economic Uncertainty: During periods of global economic slowdown, often exacerbated by geopolitical events, discretionary spending on travel may decrease, favoring less costly substitutes.

- Shift in Business Practices: The widespread adoption of remote work and virtual collaboration tools provides a viable substitute for business travel, reducing demand for airline services.

The Multifaceted Threat of Substitutes to Air Travel Demand

The threat of substitutes for EL AL Israel Airlines is multifaceted, encompassing technological advancements, alternative transportation modes, and even the decision to forgo travel altogether. High-definition virtual communication platforms offer a compelling substitute for business travel, a trend solidified by many companies in 2024 reporting reduced non-essential trips. While EL AL's long-haul focus limits direct substitutes like high-speed rail, shorter regional markets face competition from these networks, which saw a strong rebound in European passenger numbers in 2023. Leisure travelers also have substitutes like cruise lines, with the global cruise industry's revenue projected to reach $47.2 billion in 2024, directly vying for vacation budgets.

Economic downturns significantly amplify the threat of substitutes, as consumers and businesses alike curtail discretionary spending. During periods of financial strain, the primary substitute becomes the decision to not travel at all, a choice made more appealing by inflation and rising interest rates impacting household budgets in 2023. This economic pressure, projected to continue into 2024, forces airlines like EL AL to contend with reduced demand, lower load factors, and a market where staying home is a powerful alternative.

Geopolitical instability and health crises also act as potent substitutes by fostering caution and encouraging alternative engagement methods. Heightened security concerns can lead passengers to seek less risky travel options or opt for virtual communication, a trend observed in 2023 as global events influenced travel sentiment. Pandemics or localized health outbreaks can result in border closures and advisories, further pushing travelers towards domestic travel or virtual alternatives.

| Substitute Type | Description | Impact on EL AL | 2023/2024 Data Point |

|---|---|---|---|

| Virtual Communication | High-definition video conferencing, immersive collaboration platforms | Reduces demand for business travel | Many businesses reported reduced non-essential travel in 2024 |

| Alternative Transport | High-speed rail, efficient bus services, improved road infrastructure | Competes on shorter regional and domestic routes | European rail passenger numbers neared pre-pandemic levels in 2023 |

| Leisure Alternatives | Cruise lines, all-inclusive tour packages | Diverts vacation budgets and demand from air travel | Global cruise industry revenue projected at $47.2 billion in 2024 |

| Economic Factors | Decision to forgo travel due to reduced spending capacity | Decreases overall passenger volume and revenue | Global inflation and rising interest rates impacted discretionary spending in 2023 |

| Geopolitical/Health Crises | Increased security concerns, health advisories, border closures | Deters travel, encourages domestic or virtual alternatives | Global events in 2023 influenced travel sentiment towards alternatives |

Entrants Threaten

High Capital Investment Requirements

The threat of new entrants for EL AL Israel Airlines is significantly mitigated by the exceptionally high capital investment requirements inherent in the airline industry. Launching an airline demands a massive upfront financial commitment, encompassing the purchase or lease of a fleet of aircraft, establishing extensive maintenance facilities, and building the necessary operational infrastructure, including ground handling and IT systems. For instance, a new wide-body aircraft can cost upwards of $300 million, and even leasing requires substantial initial payments and long-term commitments.

This considerable financial barrier effectively deters most potential new competitors from entering the market. The sheer scale of investment needed to acquire aircraft, secure necessary certifications, and build a competitive network means only well-capitalized entities can even consider challenging established players like EL AL. This high barrier protects incumbent airlines by limiting the pool of potential new rivals who can realistically enter and compete on a similar scale.

Stringent Regulatory and Security Hurdles

The aviation sector is inherently challenging for newcomers due to extensive regulatory frameworks. Airlines must secure numerous licenses and certifications, all while adhering to stringent safety and security protocols. This complex web of requirements acts as a significant deterrent to potential new entrants.

For EL AL Israel Airlines, these barriers are amplified. Operating within a unique geopolitical context, the airline faces particularly demanding security standards. These rigorous requirements create a substantial entry barrier, making it exceptionally difficult for new airlines to establish a foothold and compete effectively.

Limited Access to Airport Slots and Infrastructure

Securing desirable landing and take-off slots at major international airports, particularly at busy hubs, presents a significant hurdle for new airlines. For instance, London Heathrow (LHR) consistently operates near full capacity, with slot availability being a critical factor for any airline aiming to establish a presence. This scarcity of prime slots directly limits the ability of new entrants to build competitive route networks, thereby acting as a protective barrier for established carriers like EL AL.

Brand Loyalty and Established Networks

EL AL Israel Airlines, like other established carriers, benefits from significant brand loyalty and extensive networks. This makes it difficult for new airlines to enter the market and gain traction. For instance, EL AL's King David program has cultivated a dedicated customer base over many years, fostering repeat business and a strong sense of trust. New entrants must invest heavily to build similar brand recognition and customer relationships.

The challenge extends to replicating existing infrastructure and operational capabilities. EL AL's decades of experience have allowed it to establish robust partnerships and an efficient global network, including crucial interline agreements and codeshares. New entrants would need to overcome the immense cost and complexity of building a comparable network from scratch, which is a substantial barrier.

Consider the financial commitment. In 2023, the global airline industry saw recovery, but profitability remained a challenge for many. For example, while EL AL reported a net profit for 2023, new entrants face the daunting task of achieving profitability while simultaneously investing in brand building and network development. This financial hurdle is a critical aspect of the threat of new entrants.

- Brand Recognition: EL AL's established reputation and long-standing presence create a significant advantage over newcomers.

- Customer Loyalty Programs: Programs like King David foster repeat business and make it harder for new airlines to attract customers.

- Network Effects: EL AL's extensive global network and partnerships are difficult and costly for new entrants to replicate.

- Capital Investment: The substantial financial resources required to build a comparable brand and network act as a major deterrent.

Potential for Retaliation from Incumbents

Existing airlines, including EL AL, command substantial resources and significant market leverage. This allows them to react forcefully to new competitors through tactics such as aggressive pricing, expanding flight schedules, or bolstering customer loyalty initiatives. For instance, in 2023, major carriers often engaged in competitive fare adjustments to retain market share, a common strategy that can significantly impact profitability for newcomers.

The anticipation of such strong pushback from established players can act as a powerful deterrent for potential new entrants. This threat of retaliation helps protect EL AL's existing market position and profitability by making the entry barriers more formidable. The airline industry's capital-intensive nature, coupled with the established brand loyalty and operational efficiencies of incumbents like EL AL, further solidifies this barrier.

- Incumbent Resources: EL AL, like other legacy carriers, benefits from extensive fleets, established routes, and strong brand recognition, providing a robust defense against new entrants.

- Aggressive Competitive Tactics: Potential new airlines must consider the likelihood of price wars, increased flight frequencies, and enhanced loyalty programs as responses from existing airlines.

- Deterrent Effect: The credible threat of retaliation discourages new companies from entering the market, thereby safeguarding the competitive standing of established airlines.

- Market Share Protection: By making entry costly and risky, incumbent airlines like EL AL can effectively preserve their market share and profitability.

EL AL's Fortress: High Barriers Deter New Airline Entrants

The threat of new entrants for EL AL Israel Airlines is considerably low due to the industry's high capital intensity and stringent regulatory environment. Acquiring and maintaining an aircraft fleet, coupled with securing necessary operating licenses and certifications, demands substantial financial investment and adherence to rigorous safety standards, making entry extremely challenging for potential newcomers.

Established brands like EL AL benefit from strong customer loyalty, cultivated through programs like King David, and extensive, hard-to-replicate global networks. These factors, combined with the financial muscle of incumbents to engage in competitive pricing and service enhancements, create significant barriers that deter new airlines from entering the market and competing effectively.

| Factor | Impact on EL AL | Example/Data (2024) |

|---|---|---|

| Capital Investment | High Barrier | New wide-body aircraft can cost over $300 million; leasing also requires significant upfront capital. |

| Regulatory Hurdles | High Barrier | Extensive safety, security, and operational certifications are complex and costly to obtain. |

| Brand Loyalty & Networks | Strong Advantage | EL AL's King David program and established global partnerships are difficult for new entrants to match. |

| Incumbent Retaliation | Significant Deterrent | Established airlines can initiate price wars or increase service offerings, impacting new entrants' profitability. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for EL AL Israel Airlines is built upon a foundation of publicly available financial statements, annual reports, and industry-specific market research from reputable sources. We also incorporate data from aviation regulatory bodies and news archives to capture competitive dynamics and market trends.