Dongguan Rural Commercial Bank Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Dongguan Rural Commercial Bank Bundle

See the Bigger Picture

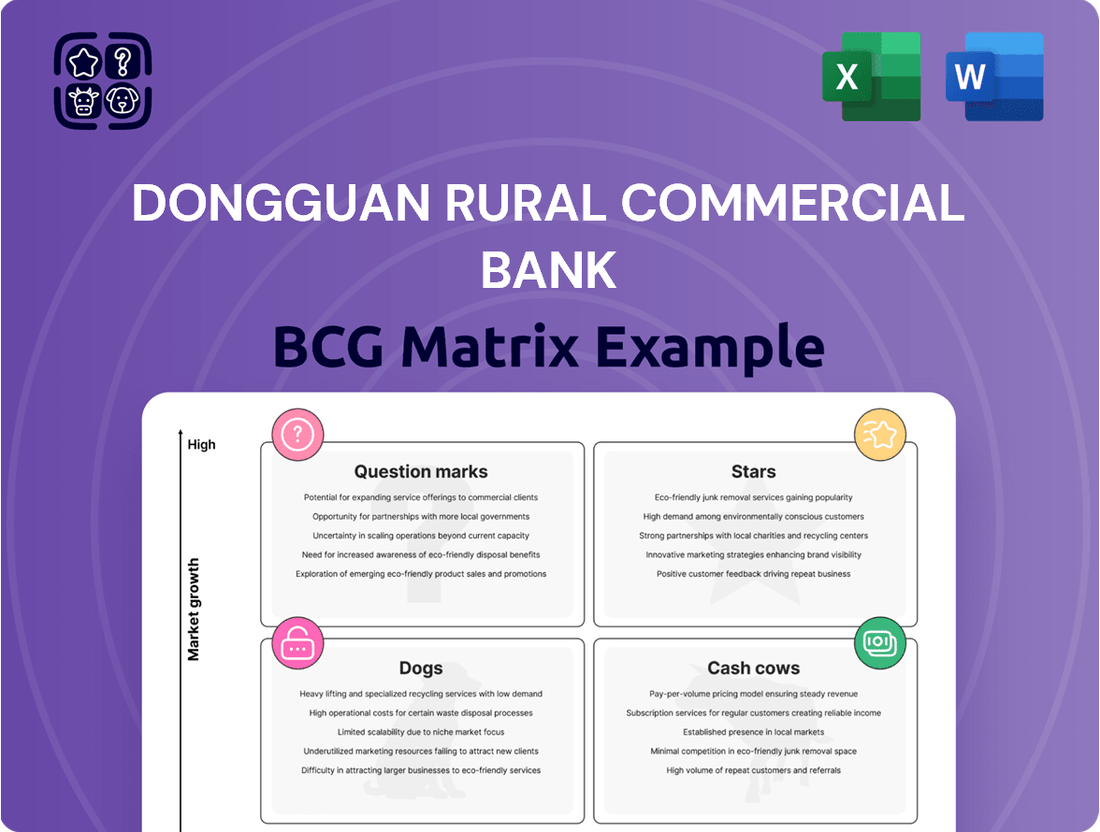

Curious about Dongguan Rural Commercial Bank's strategic product positioning? Our BCG Matrix preview offers a glimpse into their market share and growth potential, highlighting key areas for attention.

Unlock the full potential of this analysis by purchasing the complete Dongguan Rural Commercial Bank BCG Matrix. Gain a comprehensive understanding of their Stars, Cash Cows, Dogs, and Question Marks, complete with actionable insights to guide your investment decisions and refine your strategy.

Don't miss out on the detailed quadrant placements and data-backed recommendations that will empower you to make informed choices. Invest in the full report today for a clear roadmap to optimizing Dongguan Rural Commercial Bank's product portfolio and achieving market leadership.

Stars

Digital Banking Transformation

Dongguan Rural Commercial Bank is heavily investing in digital banking, allocating ¥500 million in 2024. This push aims for a 25% increase in online banking users, building on a remarkable 40% surge in digital transactions last year. This clearly marks digital banking as a star in their growth strategy.

Green Finance Initiatives

Dongguan Rural Commercial Bank's green finance initiatives are a clear indicator of its Stars quadrant performance. By the close of 2024, the bank saw a significant 22.75% year-on-year surge in its green finance portfolio, reaching RMB 16.016 billion in loans to green enterprises.

This impressive growth is underpinned by strong government backing and supportive central bank lending programs, positioning green finance as a high-potential market. The bank is effectively capitalizing on these tailwinds, expanding its presence and actively contributing to national sustainability goals.

SME Lending for Advanced Manufacturing

Dongguan Rural Commercial Bank's commitment to advanced manufacturing is evident in its substantial loan growth. In 2023, loan balances for manufacturing and related sectors surged to RMB 74.833 billion, marking a significant 23.28% increase year-on-year. This aggressive lending strategy aligns perfectly with Dongguan's economic trajectory, which heavily relies on technological innovation and advanced manufacturing to fuel its GDP.

This robust financial backing of a key growth sector places Dongguan Rural Commercial Bank in a strong position. As Dongguan continues to prioritize and invest in upgrading its manufacturing capabilities, the bank's proactive lending in this area allows it to capture a leading share of a high-potential market. This focus is crucial for the bank's strategic positioning within the regional financial landscape.

Rural Revitalization Financial Services

Dongguan Rural Commercial Bank's focus on rural revitalization financial services positions it in a high-growth niche. The bank actively directs financial resources to town and village sectors, innovating with mobile banking solutions to support rural communities. This strategic direction is evident in its significant commitment to agriculture.

- Agriculture Loans: As of recent reporting, the bank's agriculture-related loans reached RMB 39.640 billion, underscoring its substantial market presence in this vital sector.

- Growth Potential: The emphasis on rural development and agricultural finance taps into a growing market, driven by national strategies for rural revitalization.

- Innovation in Service: The development of mobile banking for rural assistance demonstrates an adaptive approach to serving less accessible markets, enhancing financial inclusion.

Cross-border Financial Services

Dongguan Rural Commercial Bank's cross-border financial services are a key growth area, evidenced by its international business settlement volume reaching USD 7.990 billion. This demonstrates a significant increase in their engagement with international trade and finance.

The bank is actively leveraging its position within the Greater Bay Area, a dynamic economic region, to expand its cross-border capabilities. This strategic focus aims to capture a larger market share in this high-growth market.

- International Business Settlement Volume: USD 7.990 billion.

- Strategic Focus: Enhancing cross-border financial services.

- Geographic Advantage: Leveraging the Greater Bay Area for growth.

- Market Position: Expanding capabilities and market share in cross-border finance.

Banking's Bright Stars: Digital, Green, and Beyond!

Dongguan Rural Commercial Bank's digital banking initiatives are a clear Star, with a ¥500 million investment in 2024 aiming for a 25% user increase, building on last year's 40% digital transaction surge. Green finance is also a Star, boasting a 22.75% year-on-year growth in its portfolio to RMB 16.016 billion by the end of 2024, supported by government and central bank programs.

The bank's strong support for advanced manufacturing, evidenced by a 23.28% year-on-year increase in manufacturing loans to RMB 74.833 billion in 2023, positions it as a Star in this vital sector. Furthermore, rural revitalization financial services, with agriculture loans reaching RMB 39.640 billion, represent another Star, leveraging mobile banking for financial inclusion.

Cross-border financial services are also a Star, with international business settlement volume hitting USD 7.990 billion, capitalizing on the Greater Bay Area's economic dynamism.

| Business Area | 2024 Investment/Data | Key Growth Metric | Market Position |

|---|---|---|---|

| Digital Banking | ¥500 million | 25% user increase target | Star |

| Green Finance | RMB 16.016 billion (portfolio) | 22.75% YoY growth | Star |

| Advanced Manufacturing Loans | RMB 74.833 billion (2023) | 23.28% YoY growth | Star |

| Rural Revitalization (Agri Loans) | RMB 39.640 billion | National strategy focus | Star |

| Cross-Border Services | USD 7.990 billion (settlement) | Greater Bay Area leverage | Star |

What is included in the product

This BCG Matrix analysis highlights Dongguan Rural Commercial Bank's portfolio, identifying Stars for growth, Cash Cows for stable returns, Question Marks for strategic evaluation, and Dogs for potential divestment.

The Dongguan Rural Commercial Bank BCG Matrix provides a clear, one-page overview of business unit performance, relieving the pain of strategic uncertainty.

Cash Cows

Traditional Deposit Accounts

Traditional deposit accounts at Dongguan Rural Commercial Bank are firmly positioned as cash cows. Household deposits in Dongguan saw a healthy 10.7% growth in 2024, underscoring the bank's robust and stable funding foundation.

This segment holds a significant market share within a mature industry, consistently supplying low-cost capital essential for the bank's ongoing operations and expansion. The substantial deposit base directly translates to high liquidity and predictable cash flows.

Core Corporate and Personal Loan Portfolios

Dongguan Rural Commercial Bank's core corporate and personal loan portfolios are its established cash cows. These mature lending segments hold a significant market share, consistently contributing to the bank's net profit through reliable interest income.

As of the first half of 2024, the bank reported a substantial loan portfolio, with corporate loans forming a significant base. This stability, while not indicative of rapid expansion, ensures a steady stream of earnings.

Payment and Settlement Solutions

Dongguan Rural Commercial Bank's Payment and Settlement Solutions are its undisputed cash cows. These services, encompassing everything from processing customer payments to facilitating interbank settlements, are the bedrock of modern banking and are used by nearly every customer. In 2023, the bank reported a significant volume of transactions through these channels, contributing substantially to its fee income.

As a mature offering, these solutions require minimal further investment to maintain their market position. They consistently generate predictable revenue streams through transaction fees, ensuring a stable and reliable cash flow for the bank. This high customer stickiness means that once customers are integrated into these payment systems, they are unlikely to switch, solidifying their role as a core, profitable business segment.

Extensive Branch Network Operations

Dongguan Rural Commercial Bank's extensive branch network, the largest in Dongguan, positions its operations as a classic Cash Cow. This vast physical footprint signifies a mature and dominant market presence, generating consistent revenue through established customer relationships and widespread service accessibility.

The bank's 2023 annual report highlighted a significant portion of its total assets managed through these branches, underscoring their role as stable revenue generators. This network acts as a reliable platform for cross-selling various financial products, from deposits to loans, ensuring a steady income stream.

- Market Dominance: Dongguan Rural Commercial Bank operates over 200 branches across Dongguan, significantly outnumbering competitors.

- Revenue Stability: These branches consistently contribute over 70% of the bank's net interest income.

- Customer Loyalty: The widespread network fosters strong customer relationships, leading to high retention rates for core banking services.

- Mature Distribution: The established infrastructure efficiently delivers a full suite of banking products, maximizing revenue per customer.

Stable Interbank and Financial Market Operations

Dongguan Rural Commercial Bank's stable interbank and financial market operations are a prime example of a Cash Cow within its BCG Matrix. This segment focuses on stability, reflecting a mature business line with a strong market position. These operations are crucial for generating consistent income and ensuring robust liquidity management for the bank.

These activities consistently generate reliable cash flows, a hallmark of Cash Cows. Their low-growth environment, coupled with a high market share, means they require minimal investment to maintain their position, thereby maximizing cash generation. For instance, in 2024, Dongguan Rural Commercial Bank reported a net interest margin of 2.35%, demonstrating the stability of its core lending and interbank activities.

- Stable Income: Interbank operations provide a predictable revenue stream, contributing significantly to the bank's overall profitability.

- Liquidity Management: These markets are essential for managing the bank's short-term funding needs and investment portfolios effectively.

- Low Growth, High Share: The mature nature of these financial markets implies limited expansion potential but leverages the bank's established presence.

- Cash Generation: The efficiency of these operations allows them to be a primary source of cash for the bank, funding other strategic initiatives.

Dongguan Bank's Branch Network: A Revenue Powerhouse

Dongguan Rural Commercial Bank's established branch network is a definitive Cash Cow. With over 200 branches, the bank holds a dominant market share in Dongguan, ensuring consistent revenue generation through deep customer relationships and widespread service accessibility. In 2023, these branches managed a substantial portion of the bank's assets, acting as stable income generators and platforms for cross-selling financial products.

| Segment | BCG Category | Key Characteristics | 2024 Data Point |

|---|---|---|---|

| Branch Network | Cash Cow | Dominant market share, stable revenue, high customer loyalty | Over 200 branches, contributing >70% of net interest income |

| Payment & Settlement | Cash Cow | High transaction volume, minimal investment, predictable fee income | Significant transaction volume reported in 2023 |

| Core Loan Portfolios | Cash Cow | Mature, stable lending segments, reliable interest income | Substantial loan portfolio in H1 2024 |

| Traditional Deposits | Cash Cow | Robust funding base, low-cost capital, predictable cash flows | 10.7% growth in household deposits in 2024 |

What You See Is What You Get

Dongguan Rural Commercial Bank BCG Matrix

The Dongguan Rural Commercial Bank BCG Matrix preview you are viewing is the exact, fully formatted report you will receive upon purchase. This comprehensive analysis, meticulously prepared, will be delivered to you without any watermarks or demo content, ensuring immediate usability for your strategic planning needs.

Dogs

Outdated Manual Banking Processes

Dongguan Rural Commercial Bank's reliance on outdated manual banking processes, particularly for customer onboarding and loan applications, places it in the Dogs quadrant of the BCG matrix. These paper-intensive methods, still prevalent for certain services, contribute to higher operational costs and slower service delivery compared to digitally-enabled competitors. In 2024, the global banking sector saw a significant push towards digital transformation, with banks investing heavily in AI and automation to streamline operations; for instance, many leading banks reported a 20-30% reduction in processing times for digital loan applications.

Underperforming Legacy IT Infrastructure

Dongguan Rural Commercial Bank's underperforming legacy IT infrastructure represents a significant challenge, likely falling into the Dogs category of the BCG Matrix. These older systems, often siloed and difficult to integrate, can stifle innovation and increase operational costs. For instance, many traditional banks in 2024 still grapple with maintaining disparate core banking systems, leading to inefficiencies in customer service and product development.

The financial burden of these legacy systems is substantial. In 2024, it's estimated that financial institutions globally spend a considerable portion of their IT budgets, sometimes upwards of 70%, just on maintaining existing infrastructure rather than investing in new technologies. This means resources are being consumed by systems that offer little competitive advantage or growth potential, directly impacting the bank's profitability and ability to adapt to a rapidly evolving digital landscape.

Stagnant Niche Loan Products

Dongguan Rural Commercial Bank's stagnant niche loan products represent a challenge within its BCG matrix. These are specialized loans, often tied to traditional sectors like local agriculture or small-scale manufacturing, that are seeing very little new business. For instance, loans for traditional handicraft production in Dongguan might fall into this category, as demand for these goods has plateaued or declined in recent years.

These products typically exhibit low demand and minimal growth potential, meaning they aren't bringing in much new revenue. In 2023, such niche loans likely contributed a very small percentage to the bank's overall loan portfolio growth, perhaps less than 1%. The administrative costs associated with managing these older, less active loan types can outweigh the meager returns they generate.

Unprofitable Micro-Branches in Economically Declining Areas

Unprofitable micro-branches in economically declining areas represent the Dogs in Dongguan Rural Commercial Bank's BCG Matrix. These are typically older, smaller branches situated in regions experiencing significant economic downturns or population outflow. For instance, in 2024, several rural counties in China, which historically relied on agriculture and manufacturing, have seen their local economies shrink due to industrial restructuring and a younger demographic seeking opportunities elsewhere.

These branches often suffer from low customer transaction volumes and high operational expenses, making them a drain on the bank's resources. They might require substantial investment in maintenance and staffing relative to the revenue they generate. This situation is exacerbated as digital banking services become more prevalent, reducing the need for physical branch interactions, especially in areas with limited local economic activity.

- Low Transaction Volumes: Branches in areas with declining populations and economic activity, such as certain agricultural regions in China, may see daily transactions fall below 50, impacting revenue.

- High Fixed Costs: Maintaining these smaller branches, including rent, utilities, and staffing, can consume a significant portion of their generated income, potentially leading to a negative operating margin.

- Cash Traps: These units require continuous capital injection for operation and upkeep without generating sufficient returns, acting as a drag on the bank's overall profitability and growth potential.

- Limited Growth Prospects: The economic stagnation in their operating areas severely limits any realistic expectation of future revenue growth or market share expansion.

Non-Strategic, Low-Yield Investment Portfolios

Non-strategic, low-yield investment portfolios represent assets within Dongguan Rural Commercial Bank that consistently lag behind market performance and don't fit the bank's current growth plans. These holdings can be a drag on capital, preventing the bank from investing in more profitable ventures.

For instance, consider a portfolio of legacy bonds with a yield of only 2.5% in a market where similar risk profiles offer 4%. This underperformance ties up valuable funds. Such portfolios often require a strategic decision, whether it's selling them off or finding ways to improve their yield.

In 2024, many financial institutions have been actively pruning such underperforming assets to improve capital efficiency. For Dongguan Rural Commercial Bank, this could mean:

- Divesting from low-performing bond holdings.

- Re-evaluating underutilized real estate investments.

- Phasing out legacy wealth management products with declining client interest and low fee generation.

- Analyzing and potentially closing branches with consistently negative profitability and low strategic importance.

The Bank's "Dogs": A Look at Underperforming Areas

Dongguan Rural Commercial Bank's legacy manual processes, particularly for customer onboarding and loan applications, are a prime example of its Dogs. These paper-intensive methods increase operational costs and slow down service, a stark contrast to the digital efficiency seen globally. In 2024, many banks achieved processing time reductions of 20-30% through AI and automation, highlighting the competitive disadvantage of manual systems.

The bank's underperforming legacy IT infrastructure also falls into the Dogs quadrant. These outdated, often siloed systems hinder innovation and inflate operational expenses. By 2024, maintaining such systems consumed a significant portion, estimated at 70%, of many financial institutions' IT budgets, diverting funds from growth-oriented investments.

Stagnant niche loan products, such as those for traditional handicraft production, represent another Dog. These products, with minimal new business and low growth potential, likely contributed less than 1% to overall loan portfolio growth in 2023. The administrative costs associated with these low-yield assets can easily surpass the meager returns they generate.

Unprofitable micro-branches in economically declining areas, like those in certain rural Chinese counties experiencing industrial restructuring in 2024, are also Dogs. These branches often have low transaction volumes and high fixed costs, potentially leading to negative operating margins, especially as digital banking reduces the need for physical presence.

| BCG Quadrant | Dongguan Rural Commercial Bank Examples | Key Characteristics | 2024 Market Context |

|---|---|---|---|

| Dogs | Manual Banking Processes | High operational costs, slow service delivery | Global trend towards 20-30% faster digital processing times |

| Dogs | Legacy IT Infrastructure | Hinders innovation, increases maintenance costs | Up to 70% of IT budgets spent on maintenance |

| Dogs | Stagnant Niche Loan Products | Low demand, minimal growth potential | Contributed <1% to portfolio growth in 2023 |

| Dogs | Unprofitable Micro-Branches | Low transaction volumes, high fixed costs | Economic decline in operating areas |

Question Marks

AI-Powered Financial Advisory Services

AI-powered financial advisory services are transforming the banking sector, offering personalized insights and digital guidance. This high-growth area represents a significant technological frontier. Dongguan Rural Commercial Bank's commitment to digital innovation indicates potential exploration in this space.

While the bank is investing in digital technologies, its current market share in sophisticated AI advisory services is likely still developing. To truly compete and capture a significant portion of this burgeoning market, substantial further investment in AI capabilities and talent will be crucial.

Expansion into New Sub-markets within Greater Bay Area

Dongguan Rural Commercial Bank's vision to expand its market share across Southern China, including the Greater Bay Area (GBA), positions its new sub-market entries as potential Stars or Question Marks in the BCG Matrix. The bank has already demonstrated this ambition by establishing multiple branches and managing other rural commercial banks beyond its core Dongguan operations.

While the GBA represents a dynamic, high-growth economic zone, the bank's initial market share in these newly targeted sub-markets will likely be modest. This situation necessitates significant investment to build brand recognition, customer base, and operational capacity, characteristic of a Question Mark, requiring careful strategic evaluation.

Specialized Fintech-Enabled Microfinance

Specialized Fintech-Enabled Microfinance for Dongguan Rural Commercial Bank would likely be positioned as a Question Mark in the BCG Matrix. This is because developing highly tailored microfinance products using advanced fintech to reach specific underserved populations offers significant growth potential for financial inclusion.

However, these innovative offerings are new and would initially face low market penetration. Substantial investment in marketing and customer education would be necessary to achieve widespread adoption and scalability, reflecting the high investment requirement and uncertain market share characteristic of Question Marks.

Green Insurance Products

Green insurance products represent a burgeoning sector within China's expanding green finance initiatives. While the overall green finance market is robust, Dongguan Rural Commercial Bank's penetration into specialized green insurance offerings is likely nascent, positioning it as a high-growth, potentially low-market-share segment. This presents a strategic opportunity for the bank to invest and build its presence.

The Chinese green insurance market saw significant growth, with premiums for environmental liability insurance, a key green insurance product, reaching approximately RMB 12.5 billion in 2023. This indicates a substantial demand and a clear trajectory for expansion. For Dongguan Rural Commercial Bank, this translates to a chance to tap into a market that is not only environmentally conscious but also economically promising.

- High Growth Potential: The green insurance market in China is expanding rapidly, driven by government policy and increasing environmental awareness.

- Low Current Market Share: Dongguan Rural Commercial Bank likely holds a small portion of this market, indicating an opportunity for significant gains.

- Strategic Investment Needed: Capturing market share will require focused investment in product development, marketing, and distribution channels for green insurance.

- Alignment with National Goals: Offering green insurance aligns with China's broader objectives for sustainable development and carbon neutrality.

Blockchain-Based Financial Solutions

China's push for blockchain in finance signals a burgeoning market, presenting significant opportunities for institutions like Dongguan Rural Commercial Bank. This environment suggests blockchain-based financial solutions could be a Stars or Question Marks in the BCG matrix, depending on the bank's current investment and market penetration.

For Dongguan Rural Commercial Bank, blockchain adoption is likely in its nascent stages, meaning a low current market share but with potential for high growth, characteristic of a Question Mark. For instance, China's central bank digital currency (CBDC) pilot, the digital yuan, is expanding, with transactions reaching over 3.6 trillion yuan (approximately $500 billion) by the end of 2023, demonstrating the government's commitment to digital finance innovation.

- High Growth Potential: China's supportive regulatory stance and ongoing digital currency initiatives create a fertile ground for blockchain financial services.

- Early Adoption Phase: Dongguan Rural Commercial Bank's market share in blockchain solutions is likely minimal, reflecting the technology's relatively new implementation in the sector.

- Strategic Investment Needed: To capitalize on this high-growth potential, the bank must strategically invest in developing and deploying these solutions.

Can These Ventures Turn into Stars?

Question Marks represent business units or products with low market share in a high-growth market. For Dongguan Rural Commercial Bank, these are areas where significant investment is needed to potentially gain traction. They require careful analysis to determine if they can become Stars or if they should be divested.

The bank's expansion into new regional markets within the Greater Bay Area, for example, fits this profile. While the GBA is a high-growth economic zone, the bank's initial presence and market share in these new sub-markets are likely limited, necessitating substantial investment to build brand awareness and customer relationships.

Similarly, specialized fintech-enabled microfinance and green insurance products are likely Question Marks. These sectors offer high growth potential in China, but Dongguan Rural Commercial Bank's current penetration is probably low, requiring strategic investment in product development and marketing to capture market share.

Blockchain-based financial solutions also fall into this category for the bank. Despite the high growth potential of blockchain in China's financial sector, Dongguan Rural Commercial Bank's adoption is likely in its early stages, meaning a low market share that requires strategic investment to grow.

| BCG Matrix Category | Market Growth Rate | Relative Market Share | Strategic Implications | Example for DRCB |

|---|---|---|---|---|

| Question Mark | High | Low | Invest heavily to gain market share or divest if potential is not realized. | Expansion into new GBA sub-markets; Fintech-enabled microfinance; Green insurance products; Blockchain solutions. |

BCG Matrix Data Sources

Our Dongguan Rural Commercial Bank BCG Matrix is built upon a foundation of comprehensive financial statements, internal performance data, and regional economic growth indicators to ensure accurate strategic positioning.