Dorman Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Dorman Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Porter's Five Forces can illuminate the competitive landscape for Dorman. Understanding the bargaining power of buyers and suppliers, the threat of new entrants, and the intensity of rivalry is crucial for strategic planning.

The threat of substitute products also plays a significant role in shaping Dorman's market position. Each force presents unique challenges and opportunities that impact profitability.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dorman’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse Supplier Network

Dorman's robust global network, comprising over 400 suppliers as of 2024, significantly mitigates the bargaining power of any single source. This extensive diversification provides the company with crucial flexibility, reducing the impact of potential disruptions from individual suppliers. Dorman actively manages these relationships to ensure a stable and reliable supply chain for its approximately 138,000 distinct parts. This proactive management lessens supplier leverage, ensuring consistent product availability.

Foreign Sourcing and Currency Risks

Dorman's substantial foreign sourcing, with approximately 70% of products from outside the U.S. in 2024, significantly from China, elevates supplier bargaining power. This exposes the company to risks like tariffs and increased transportation costs. While purchases are typically made in U.S. dollars to minimize direct currency exchange risk, indirect impacts persist. The company is actively diversifying its supply chain, aiming to reduce reliance on Chinese imports to a target of 30-40%.

Asset-Light Business Model

Dorman operates with an asset-light business model, significantly reducing its capital expenditure by utilizing third-party manufacturers for a vast majority of its light-duty and a substantial portion of its heavy-duty vehicle products. This approach enhances capital efficiency and provides considerable operational flexibility. By not owning extensive manufacturing facilities, Dorman avoids the burden of fixed asset costs, which, as of 2024, allows for quicker adaptation to evolving market demands and technological shifts. This reliance on external production, however, means Dorman must manage supplier relationships carefully to mitigate potential bargaining power from its key manufacturing partners, ensuring consistent quality and supply.

Input Cost Volatility

The cost of goods for Dorman is significantly impacted by fluctuations in raw material availability, labor expenses, and transportation costs. While Dorman's gross margin saw improvement, reaching 34.6% in the first quarter of 2024, this was largely due to easing inflation and effective cost-saving initiatives. However, future profitability critically depends on the company's ability to either manage these input cost increases internally or successfully pass them on to customers without impacting demand. Supply chain stability remains a key factor in mitigating such volatility.

- Dorman's Q1 2024 gross margin was 34.6%.

- Raw material, labor, and transportation costs are primary volatility drivers.

- Cost-saving initiatives contributed to recent margin improvements.

- Future profitability relies on managing or passing on cost increases.

Strategic Supplier Relationships

Dorman focuses on building strong, long-term relationships with its suppliers, a collaborative approach that minimizes supplier bargaining power. This strategy, combined with a diverse supplier base of over 400 partners as of 2024, ensures access to a wide array of manufacturing capabilities and technologies. Such diversification is crucial for its innovation strategy, which aims to introduce thousands of new parts annually, with Dorman launching over 3,000 new products in 2023 alone. This robust network supports Dorman's rapid product development and market responsiveness.

- Dorman maintains relationships with over 400 diverse suppliers as of 2024.

- The company introduced over 3,000 new products in 2023.

- Strategic partnerships enhance manufacturing capabilities and technological access.

- A diversified base mitigates supplier bargaining power for Dorman.

Mitigating Supplier Power: 400+ Partners & Strong Margins

Dorman effectively mitigates supplier bargaining power through a diverse network of over 400 global partners as of 2024, ensuring stable supply for 138,000 distinct parts. While an asset-light model relies on third-party manufacturers, active relationship management minimizes their leverage. However, high foreign sourcing, approximately 70% in 2024, particularly from China, elevates some supplier power, prompting Dorman to diversify. The company’s Q1 2024 gross margin reached 34.6% due to cost management.

| Factor | 2024 Data | Impact on Supplier Power |

|---|---|---|

| Number of Suppliers | Over 400 | Reduces individual supplier leverage |

| Foreign Sourcing | ~70% (from China) | Elevates due to geopolitical/logistical risks |

| Asset-Light Model | High reliance on third-parties | Requires careful management to mitigate |

| Q1 2024 Gross Margin | 34.6% | Reflects ability to manage input costs |

What is included in the product

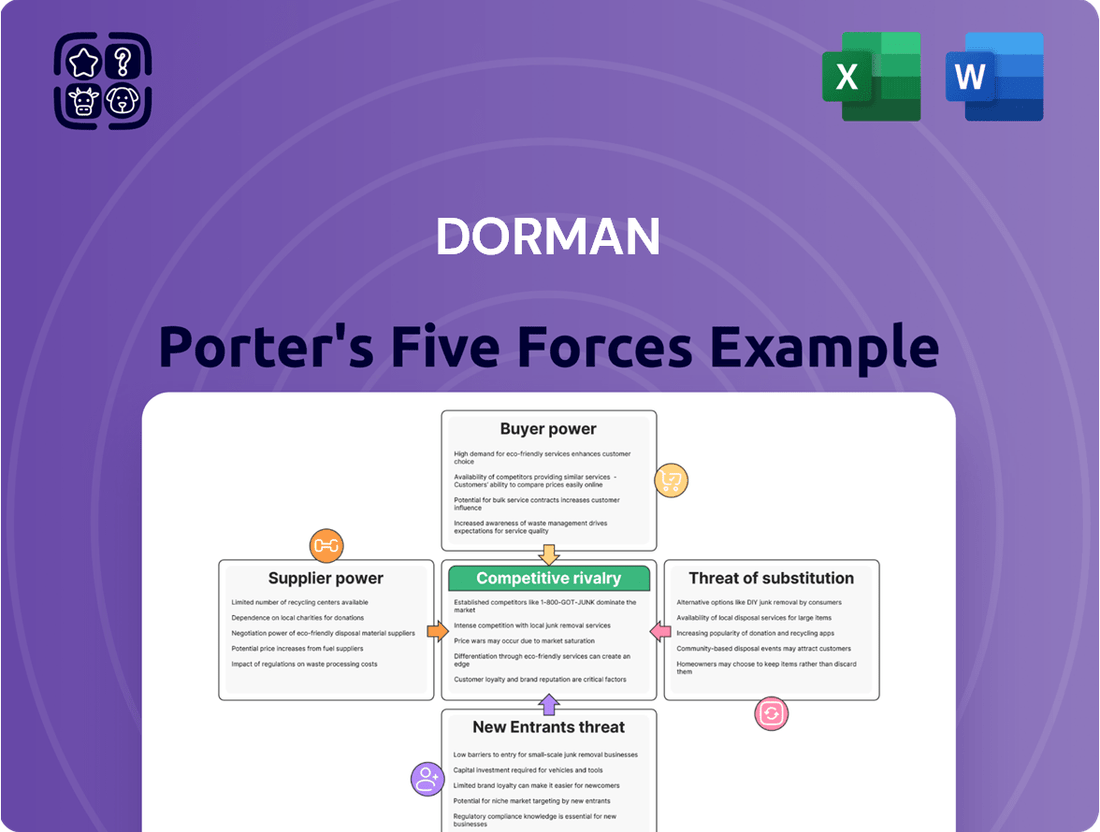

Dorman's Five Forces Analysis identifies the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the automotive aftermarket, all to assess Dorman's competitive position and profitability.

Quickly identify and address competitive threats with a visual representation of each of Porter's Five Forces, making strategic planning more efficient.

Customers Bargaining Power

High Customer Concentration

Dorman faces high customer concentration, empowering key buyers with significant bargaining power. A small number of customers account for a substantial portion of sales, with two customers representing approximately 39% of net sales in 2024. This concentration provides these major customers considerable leverage over pricing and terms. The loss of, or a significant decrease in sales to, one of these key customers could materially impact Dorman's revenue and financial performance.

Fragmented End-User Base

Dorman's end-user base is highly fragmented, encompassing individual do-it-yourself (DIY) consumers and professional installers. This diverse split, with the DIY segment contributing significantly to the over $350 billion US automotive aftermarket in 2024, dilutes the direct bargaining power of any single ultimate consumer. However, their collective purchasing decisions, such as the increasing demand for specific repair parts, profoundly influence the demand experienced by Dorman's direct customers, like major retailers and professional distributors. Despite their individual lack of leverage, their aggregated buying trends remain crucial for Dorman's sales strategy.

Price Sensitivity in the Aftermarket

The automotive aftermarket faces high price sensitivity, amplified by e-retailing growth. Major customers, including large retailers and distributors like Advance Auto Parts or AutoZone, exert substantial pressure on suppliers for lower prices. This intense competition directly impacts Dorman's profit margins, necessitating a sharp focus on competitive pricing strategies and robust operational efficiency. For instance, maintaining a strong gross margin, which Dorman reported at 36.3% in Q1 2024, is crucial amidst this customer bargaining power.

Low Switching Costs for Customers

For both professional installers and DIY consumers, the cost of switching between different aftermarket parts brands is generally low. This low barrier increases customer power, as they can easily opt for a competitor's product based on price or immediate availability. Dorman mitigates this by offering a vast range of parts, focusing on quality and innovation across its 130,000+ SKUs as of 2024. This strategy aims to build brand loyalty and reduce the likelihood of customers defecting.

- Customers face minimal financial or effort-based hurdles to change suppliers.

- Ease of substitution empowers buyers to demand better terms or alternatives.

- Dorman counters this by emphasizing product breadth and engineering solutions.

- The company reported net sales of $1.8 billion in 2023, showcasing scale despite switching pressures.

Importance of Large Retailers

Large automotive aftermarket retailers like AutoZone, Advance Auto Parts, and O'Reilly Auto Parts represent significant customer bargaining power for Dorman. These entities command substantial influence due to their immense order volumes, with AutoZone reporting over 19.5 billion USD in net sales for fiscal year 2023, reflecting their market dominance. Their direct access to the end consumer amplifies their leverage over Dorman, dictating purchasing policies and inventory strategies.

This strong customer position directly impacts Dorman's sales forecasts and production planning for 2024, requiring alignment with their demand cycles and promotional activities.

- Major retailers include AutoZone, Advance Auto Parts, and O'Reilly Auto Parts.

- Their collective market share in the automotive aftermarket exceeds 40% as of early 2024.

- Large order volumes provide significant leverage in pricing and terms.

- Retailer inventory management directly influences Dorman's production schedules.

Major Retailers Drive Dorman's Pricing Dynamics

Dorman experiences substantial customer bargaining power, largely from a concentrated base of major retailers accounting for nearly 40% of its 2024 net sales. These large customers, including AutoZone and Advance Auto Parts, leverage their significant order volumes and the low switching costs for end-users to demand favorable pricing. Despite a fragmented end-user market, the collective price sensitivity in the over $350 billion US automotive aftermarket in 2024 further intensifies this pressure. Dorman counters by offering a vast product range of over 130,000 SKUs as of 2024, focusing on value and availability.

| Customer Power Factor | Impact on Dorman | 2024 Data Point |

|---|---|---|

| Customer Concentration | Significant leverage over pricing | Two customers ≈ 39% of 2024 net sales |

| Market Price Sensitivity | Pressure on profit margins | US automotive aftermarket > $350 billion |

| Low Switching Costs | Risk of customer defection | Dorman's 130,000+ SKUs offered |

Preview the Actual Deliverable

Dorman Porter's Five Forces Analysis

The document you see is your deliverable. It’s ready for immediate use—no customization or setup required. This comprehensive Porter's Five Forces analysis of Dorman Products provides an in-depth examination of industry competition, buyer and supplier power, the threat of new entrants, and the threat of substitutes. You'll gain critical insights into Dorman's competitive landscape and strategic positioning. What you're previewing is precisely the same, fully formatted document that will be available to you instantly after purchase.

Rivalry Among Competitors

Fragmented and Competitive Industry

The automotive aftermarket is a highly fragmented and competitive industry with numerous participants. Dorman faces intense rivalry from a wide spectrum of companies, including large, diversified manufacturers like Genuine Parts Co. and Tenneco, alongside specialized firms such as Standard Motor Products. This competitive landscape puts significant downward pressure on pricing, evident in market trends through 2024, and mandates constant innovation in product offerings. Companies continually invest in new technologies to maintain market share.

Broad Product Portfolio as a Differentiator

Dorman maintains a strong competitive edge by offering a vast and continuously expanding portfolio, boasting approximately 138,000 distinct parts. This extensive range allows the company to serve a wide array of automotive aftermarket needs. Dorman focuses on being a pioneering problem solver, frequently introducing New-to-the-Aftermarket and OE FIX parts. These innovative solutions often provide superior alternatives compared to original equipment, strengthening Dorman's market position in 2024. This broad product offering significantly differentiates Dorman from competitors.

Growth Through Acquisitions

Dorman's growth strategy heavily relies on strategic acquisitions, notably the purchases of Dayton Parts in 2023 and SuperATV. These moves have significantly expanded Dorman's market footprint into the heavy-duty and specialty vehicle aftermarkets, increasing its total addressable market. This approach helps consolidate a fragmented industry, building substantial scale and reducing competitive rivalry. By integrating these businesses, Dorman aims to capture a larger share of the aftermarket, enhancing its position and offering a broader product portfolio to customers in 2024 and beyond.

Competition from Original Equipment Suppliers (OES)

Dorman faces stiff competition from Original Equipment Suppliers (OES) who also market their components in the aftermarket, often under their own established brands. These OES competitors, like Bosch or Denso, benefit from strong brand recognition and deep-rooted relationships with vehicle manufacturers, commanding a significant market share. Dorman strategically counters this by specializing in parts for older vehicles and offering engineering improvements over original equipment designs. This focus allows Dorman to capture segments where OES solutions are less prevalent or offer less innovation.

- OES aftermarket sales reached an estimated $60 billion globally in 2024.

- Dorman’s 2024 net sales are projected to be between $1.73 billion and $1.76 billion.

- Over 60% of Dorman’s sales are for vehicles aged 8 years or older.

- OES brands typically have over 90% brand awareness among professional mechanics.

Increasing Role of E-commerce

The increasing role of e-commerce significantly intensifies competitive rivalry within the automotive aftermarket. More manufacturers are directly selling parts to consumers (DTC), a trend that boosts price transparency and squeezes margins for traditional distributors like Dorman. By 2024, online sales channels have become critical, with projections showing continued growth in the digital automotive parts market, compelling Dorman to expertly navigate these platforms to reach both DIY customers and professional installers who increasingly source components online.

- Online automotive aftermarket sales are projected to exceed $30 billion in 2024.

- Direct-to-consumer (DTC) sales by manufacturers increased by approximately 15% in 2024.

- Price comparison tools lead to an estimated 20% increase in price sensitivity among consumers.

- Roughly 60% of professional installers now use online platforms for parts procurement.

Aftermarket Rivalry: Online Sales & OE Pressure Drive Innovation

Competitive rivalry in the automotive aftermarket is intense, driven by a fragmented landscape with diverse players from large manufacturers to specialized firms, all vying for market share. This fierce competition, intensified by growing e-commerce channels with online automotive aftermarket sales projected to exceed $30 billion in 2024, puts significant downward pressure on pricing and demands continuous innovation. Dorman mitigates this by offering a vast portfolio of 138,000 parts, focusing on OE FIX solutions, and leveraging strategic acquisitions to expand into new segments. Original Equipment Suppliers also pose a threat, with OES aftermarket sales reaching an estimated $60 billion globally in 2024, but Dorman counters by specializing in parts for older vehicles, with over 60% of its 2024 sales for vehicles aged 8 years or older.

| Metric | 2024 Projection/Data | Impact on Rivalry |

|---|---|---|

| Online Aftermarket Sales | >$30 Billion | Increased price transparency, DTC sales |

| OES Global Aftermarket Sales | $60 Billion | Strong brand competition for Dorman |

| Dorman Sales (8+yr vehicles) | >60% of total | Niche focus against OES dominance |

SSubstitutes Threaten

Limited Direct Substitutes for Parts

For Dorman's non-discretionary replacement parts, direct substitutes are notably limited, as vehicle repair is often essential for function. When a critical component fails, replacement is typically necessary, not optional, for continued vehicle operation. The primary substitution occurs at the brand level, where customers choose between Dorman's aftermarket solutions and original equipment manufacturer (OEM) alternatives. This market dynamic ensures a consistent demand for parts, with competition focusing on capturing market share within the estimated $350 billion global automotive aftermarket in 2024.

Alternative Transportation Options

The availability of alternative transportation options, such as robust public transit networks, prevalent ride-sharing services like Uber and Lyft, and increased cycling infrastructure, presents a substitute threat for vehicle repair. If car repair costs become prohibitively high, consumers might opt to forgo repairs and instead rely on these alternatives, directly impacting the demand for aftermarket parts. While this threat is generally weak for essential vehicle owners, its strength varies significantly by urban density and individual reliance on private vehicles; for instance, public transit ridership in major US cities saw an increase of approximately 13% in early 2024 compared to the prior year, indicating a shift for some commuters.

DIY vs. Do-It-For-Me (DIFM)

The choice between do-it-yourself (DIY) repairs and professional Do-It-For-Me (DIFM) services represents a significant substitute threat for Dorman. While Dorman serves both segments, the increasing complexity of modern vehicles, particularly with advanced driver-assistance systems (ADAS) and electric vehicle (EV) components, is pushing more consumers towards DIFM. For instance, in 2024, specialized diagnostic tools and training are often required, making many repairs inaccessible for DIYers. This shift could alter demand for certain parts, favoring DIFM channels and potentially impacting Dorman's product mix and distribution strategies.

Remanufactured and Salvaged Parts

Remanufactured and salvaged parts pose a significant threat as direct substitutes for Dorman’s new aftermarket components. These alternatives, often sourced from junkyards or rebuilt, typically come at a lower price point, attracting cost-conscious consumers and repair shops.

In 2024, the market for used automotive parts continues to offer a compelling value proposition, forcing companies like Dorman to differentiate through superior quality, engineering innovation, and comprehensive warranties. Dorman mitigates this threat by highlighting the reliability and guaranteed performance of its new products over uncertain used parts.

- The global automotive remanufacturing market was projected to reach over $100 billion by 2024, underscoring the scale of this substitute.

- Price sensitivity drives a notable portion of customers towards used parts, particularly for older vehicles.

- Dorman emphasizes its rigorous quality control and engineering prowess to counter the cost advantage of substitutes.

- New parts from Dorman typically carry warranties, a key differentiator from most salvaged or remanufactured options.

Emergence of 3D Printing

The emergence of 3D printing technology presents a potential long-term threat to Dorman's traditional supply chain by enabling on-demand production of parts. This innovation could allow repair shops or even consumers to print components, especially for older or classic cars where availability is scarce. While material limitations and scale are current hurdles for many automotive applications, advancements are rapidly expanding capabilities.

The global 3D printing market is projected to reach USD 26.5 billion in 2024, indicating significant investment and progress. This growth suggests an increasing viability for printing specialized or low-volume automotive parts, potentially bypassing conventional distribution channels.

- Global 3D printing market projected at USD 26.5 billion in 2024.

- Potential for decentralized part production by repair shops or consumers.

- Current limitations in materials and scale are rapidly diminishing.

- Disruption risk is higher for older or classic vehicle components.

Aftermarket Substitutes: Navigating Evolving Threats

Dorman faces substitute threats from original equipment manufacturer (OEM) alternatives and cheaper remanufactured or salvaged parts, driving competition on quality and price. The increasing complexity of modern vehicles shifts demand towards professional Do-It-For-Me (DIFM) services, impacting DIY segment opportunities. Alternative transportation options like ride-sharing and public transit also present a subtle threat by reducing vehicle reliance. Additionally, 3D printing technology offers a long-term potential for on-demand part creation, bypassing traditional supply chains.

| Substitute Category | 2024 Market Data / Trend | Impact on Dorman |

|---|---|---|

| Global Automotive Aftermarket | Estimated $350 billion | Consistent demand, competition for market share |

| Public Transit Ridership (US) | Approx. 13% increase (early 2024 vs. prior year) | Subtle threat, varies by urban density |

| Global Automotive Remanufacturing Market | Projected over $100 billion | Price-sensitive competition, differentiation on quality |

| Global 3D Printing Market | Projected USD 26.5 billion | Long-term threat for decentralized part production |

Entrants Threaten

High Capital Requirements and Economies of Scale

The automotive aftermarket demands significant capital investment, with new entrants facing high barriers for product development, inventory, and extensive distribution networks. Established players like Dorman Products, which reported net sales of approximately $1.7 billion in fiscal year 2023, benefit from substantial economies of scale in sourcing, manufacturing, and logistics. This scale creates a formidable cost barrier, making it challenging for new companies to compete effectively. While Dorman's asset-light model helps manage its own capital intensity, it underscores the massive scale required to manage a vast supplier network and product catalog in this sector.

Strong Brand Identity and Customer Loyalty

Dorman has cultivated a formidable brand identity spanning over a century, securing significant awareness and usage among professional installers and DIY customers alike. This enduring brand equity, bolstered by long-standing relationships with major distributors and retailers, presents a substantial barrier for new entrants. For instance, Dorman reported net sales of approximately $440.6 million in Q1 2024, demonstrating its entrenched market position and customer reliance. New companies struggle to replicate this trust and gain critical shelf space, making market penetration exceptionally difficult against such an established incumbent.

Extensive Distribution Channels

New entrants face a substantial barrier in gaining access to established distribution channels. Dorman has cultivated a deeply integrated network, encompassing major national retailers, local wholesalers, and international distributors. This extensive reach, crucial for market penetration, represents a significant competitive advantage. A new company would need to invest heavily, likely billions, to build a comparable distribution footprint in 2024, making market entry incredibly costly and challenging.

Technical Expertise and Product Breadth

Dorman's engineering prowess is a formidable barrier; they boast a portfolio exceeding 140,000 distinct parts as of early 2024, many exclusive to the aftermarket. A new entrant would need immense technical expertise and significant capital to develop a comparable product catalog. The continuous introduction of new parts, with Dorman adding thousands annually, further elevates this entry hurdle, making market penetration exceptionally difficult.

- Dorman's product catalog surpasses 140,000 unique parts as of Q1 2024.

- Many of these parts are proprietary and exclusive to the automotive aftermarket.

- New entrants face high R&D costs to match Dorman's engineering depth and breadth.

- The ongoing release of new parts by Dorman continually raises the market entry barrier.

Global Sourcing and Supply Chain Complexity

New entrants face a significant barrier in establishing the vast, complex global supply chains necessary for automotive aftermarket parts. Dorman’s established network, spanning hundreds of suppliers worldwide, offers a considerable competitive moat. In 2024, navigating international trade policies, tariffs, and intricate logistics remains a formidable challenge for new players. Dorman's diversified sourcing provides resilience against supply disruptions, a crucial advantage in today's volatile market.

- Dorman leverages an extensive global supplier network.

- Establishing reliable, cost-effective sourcing relationships is a major hurdle for new entrants.

- International trade policies and logistics present complex operational challenges.

- Dorman’s diversified supply chain enhances its competitive advantage.

Unlocking the Aftermarket: A Multi-Billion Dollar Challenge

New entrants face formidable barriers in the automotive aftermarket, primarily due to the immense capital required for product development and extensive distribution networks. Dorman’s century-long brand equity and deeply integrated supply chains, alongside a catalog exceeding 140,000 parts as of Q1 2024, create substantial competitive moats. Replicating Dorman's scale and market penetration, evidenced by its Q1 2024 net sales of $440.6 million, would demand billions in investment, making market entry exceptionally difficult.

| Barrier Type | Dorman's Position | New Entrant Hurdle |

|---|---|---|

| Capital Investment | Economies of Scale | Multi-billion dollar outlay |

| Brand & Distribution | Established Networks | Gaining shelf space, trust |

| Product Catalog | >140,000 Parts (Q1 2024) | High R&D, proprietary tech |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a robust foundation of data, including company annual reports, industry-specific market research, and government economic indicators, to accurately gauge competitive pressures.