Digital Realty Trust Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Digital Realty Trust Bundle

From Overview to Strategy Blueprint

Digital Realty Trust operates in a dynamic data center market, facing moderate threats from new entrants and intense rivalry among established players. Supplier power is somewhat limited due to the commoditized nature of many inputs, while buyer power can be significant for large enterprise clients. The threat of substitutes, though evolving, remains a key consideration.

The complete report reveals the real forces shaping Digital Realty Trust’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

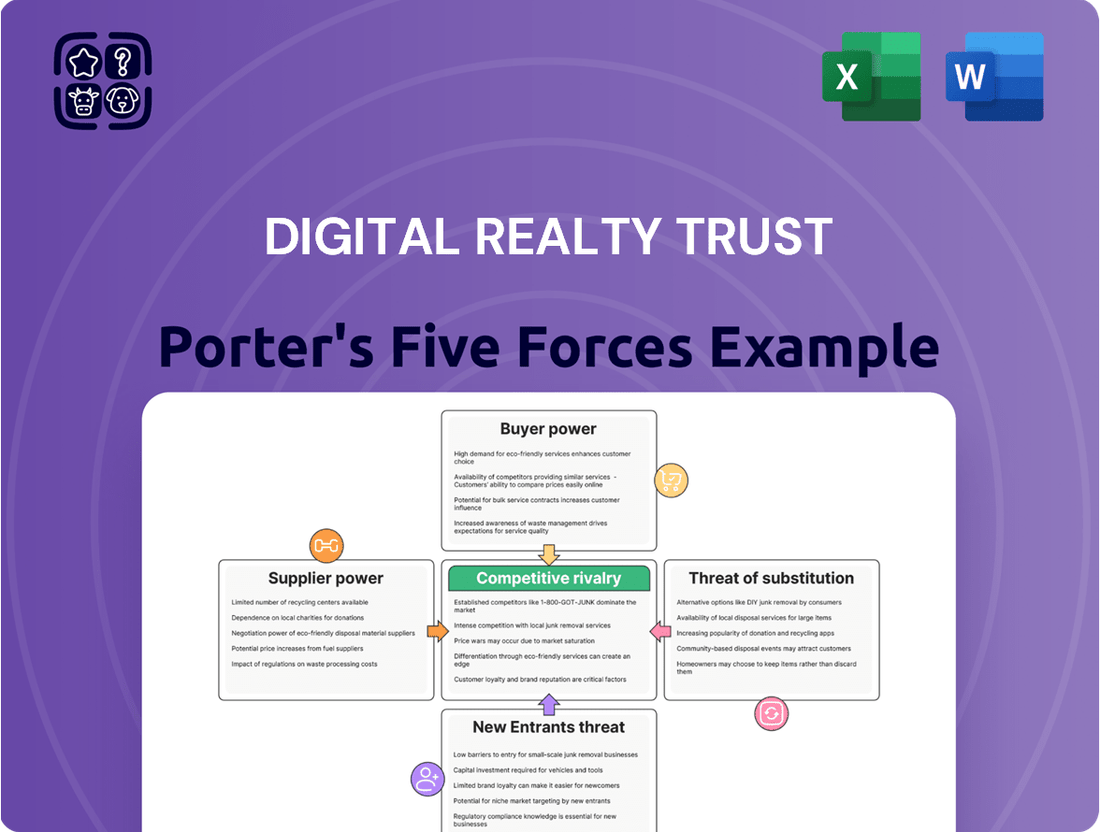

Suppliers Bargaining Power

Concentrated Suppliers for Key Components

The data center sector, including Digital Realty Trust, depends heavily on a select group of specialized suppliers for essential components. These include sophisticated power infrastructure, advanced cooling systems crucial for high-density AI workloads, and high-performance networking gear. The limited number of providers for these critical technologies can translate into significant bargaining power for the suppliers.

This concentration of suppliers means they can influence pricing and contract terms, potentially impacting Digital Realty Trust's operational costs and flexibility. For instance, the burgeoning demand for innovative cooling solutions, such as liquid cooling, driven by the AI revolution, further consolidates market power in the hands of a few specialized manufacturers.

Rising Costs of Land and Energy

Suppliers of prime real estate, especially in sought-after, well-connected urban areas, exert significant bargaining power over Digital Realty Trust. The company's core operations depend on securing suitable land for data center development, meaning the cost and availability of these plots directly impact its expansion capabilities and profitability. For instance, in 2024, prime industrial land prices in key tech hubs continued their upward trajectory, with some markets seeing year-over-year increases exceeding 15%.

Energy providers also hold considerable sway. Electricity is a fundamental and substantial operating cost for data centers, and the increasing global focus on sustainability and renewable energy sources further amplifies this power. As Digital Realty Trust invests in green energy solutions, the cost and accessibility of these power sources become critical negotiation points, with renewable energy credits and power purchase agreements representing key areas of supplier influence.

Labor Shortages for Skilled Workforce

The data center sector, including companies like Digital Realty Trust, grapples with a significant shortage of skilled labor across construction, operations, and technical roles. This scarcity directly impacts the bargaining power of employees and the training programs that supply them, potentially driving up wages and complicating hiring efforts.

For instance, in 2024, reports indicated a widening gap between the demand for cybersecurity professionals and the available talent pool, a critical area for data center security and operations. This talent deficit empowers skilled workers, allowing them to negotiate for better compensation and benefits, which can increase Digital Realty Trust's operating expenses.

Technology and Equipment Vendors

Suppliers of advanced IT and network equipment, particularly those providing high-density GPUs and specialized networking gear essential for AI workloads, wield considerable bargaining power. Digital Realty Trust's commitment to offering state-of-the-art infrastructure means it depends on these few dominant vendors for critical components. This reliance can lead to increased costs and a greater degree of influence for these technology providers.

For instance, the demand for AI-ready infrastructure has driven significant growth in the semiconductor market. In 2024, the global AI chip market was projected to reach hundreds of billions of dollars, with companies like NVIDIA dominating the GPU supply. This concentration of power among a limited number of suppliers means Digital Realty Trust must carefully manage its relationships and procurement strategies to mitigate potential cost escalations and supply chain disruptions.

- High Dependency on Key Vendors: Digital Realty Trust's need for specialized, high-performance hardware for AI and high-density computing creates a dependency on a few leading technology and equipment vendors.

- Cost Implications: The specialized nature of these components, coupled with vendor market dominance, can result in higher procurement costs for Digital Realty Trust.

- Strategic Sourcing: To counter this, Digital Realty Trust likely engages in strategic sourcing, long-term contracts, and potentially multi-vendor strategies to secure supply and manage costs effectively.

Financing and Capital Providers

Digital Realty Trust, as a Real Estate Investment Trust (REIT), fundamentally depends on consistent access to capital for its growth initiatives, including property acquisitions, new development projects, and ongoing expansion efforts. The availability and cost of this capital directly influence its strategic execution and profitability.

The primary suppliers of this essential capital are a diverse group including commercial banks, large institutional investors like pension funds and insurance companies, and the broader bond markets. These entities provide the financial fuel that powers Digital Realty's operations and expansion plans.

The bargaining power of these capital providers is significantly shaped by prevailing economic conditions. Factors such as prevailing interest rates, the overall liquidity within financial markets, and the general level of investor confidence play a crucial role. For instance, during periods of high interest rates or market uncertainty, capital providers can demand higher returns, thereby increasing Digital Realty's cost of financing and potentially impacting its investment capacity.

- Capital Dependency: Digital Realty's business model as a REIT necessitates continuous access to external capital for growth.

- Supplier Landscape: Key capital suppliers include banks, institutional investors, and bond markets.

- Influencing Factors: Interest rates, market liquidity, and investor confidence directly impact the bargaining power of capital providers.

- Impact on Cost: Higher bargaining power for suppliers translates to increased financing costs for Digital Realty.

Data Center Suppliers Wield Strong Bargaining Power

Suppliers of specialized infrastructure and real estate for data centers hold significant bargaining power. This is due to the limited number of providers for critical components like advanced cooling systems and prime urban land, which are essential for Digital Realty Trust's operations and expansion. For instance, in 2024, prime industrial land prices in key tech hubs saw increases exceeding 15% year-over-year, directly impacting Digital Realty's development costs.

What is included in the product

This analysis examines the competitive forces impacting Digital Realty Trust, including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry within the data center industry.

Instantly identify and mitigate competitive threats in the data center industry with a clear, actionable Digital Realty Trust Porter's Five Forces analysis, streamlining strategic planning.

Customers Bargaining Power

Large Hyperscale Customers

Digital Realty Trust caters to major cloud providers and hyperscalers, who represent a significant portion of their clientele. These large customers possess considerable bargaining power, stemming from the sheer volume of data center space they occupy and their capacity to develop their own facilities if negotiations falter.

Their immense scale enables these hyperscale clients to secure highly favorable lease terms, directly influencing Digital Realty's pricing flexibility and overall profitability. For instance, in 2023, Digital Realty's top 20 customers accounted for approximately 40% of its rental revenue, highlighting the concentrated power of these anchor tenants.

Customer Concentration Risk

Digital Realty Trust faces potential customer concentration risk, where a few large clients could wield significant bargaining power. For instance, in 2023, while Digital Realty serves a broad customer base, a notable portion of its revenue was derived from a limited number of hyperscale providers, suggesting that the loss of even one major tenant could disproportionately affect its financial performance and increase its susceptibility to their pricing demands.

Demand for Flexibility and Scalability

Enterprises are increasingly demanding flexible and scalable data center solutions, often referred to as Data Center as a Service (DCaaS). This shift means customers can readily adjust their capacity and services, giving them significant leverage.

This growing demand for adaptability allows customers to negotiate more favorable terms, pushing for shorter contract durations and more dynamic pricing models. For providers like Digital Realty Trust, this can impact long-term revenue predictability and pricing power.

In 2024, the global edge computing market, a key driver of demand for flexible infrastructure, was projected to reach over $270 billion, highlighting the significant customer appetite for on-demand solutions.

Price Sensitivity in Competitive Markets

In mature and highly competitive data center markets, customers often possess significant bargaining power due to the availability of multiple providers. This can translate into heightened price sensitivity, especially as the demand for AI-driven expansion, while robust, faces potential shifts. For instance, if the pace of AI adoption moderens or if new supply enters the market rapidly, customers could leverage these conditions to negotiate more favorable pricing. Digital Realty Trust, like its peers, must navigate this dynamic where customer options directly influence their pricing strategies.

The bargaining power of customers in the data center sector is a critical factor influencing Digital Realty Trust's profitability. In 2024, the market continues to see substantial investment, but the long-term sustainability of current demand growth is a key consideration. Should growth rates moderate, or if capacity expansions by competitors outpace demand, customers will likely exert greater pressure on pricing.

- Increased Customer Options: In competitive markets, customers can switch providers more easily, increasing their leverage.

- Price Sensitivity: Customers are more likely to seek the lowest possible prices when alternatives are readily available.

- AI Demand Dynamics: While AI is a current driver, any slowdown could empower customers to demand price concessions.

- Supply-Demand Balance: A shift towards oversupply would significantly bolster customer bargaining power.

Ability to Insourced or Migrate Workloads

Large enterprise clients and major cloud providers possess the significant financial and technical capabilities to develop their own data center infrastructure or shift existing workloads to alternative providers. This ability to insource or migrate grants them considerable bargaining power when negotiating terms with colocation providers like Digital Realty Trust.

For instance, a hyperscale cloud provider might choose to build its own facilities rather than lease space, directly reducing the addressable market for Digital Realty. This option forces Digital Realty to present highly competitive pricing and service level agreements to retain such high-value customers. In 2024, the increasing maturity of cloud technologies and the ongoing drive for cost optimization among large enterprises continue to amplify this particular customer leverage.

- Customer Self-Sufficiency: The capacity for major clients to build or manage their own data center facilities directly challenges colocation providers.

- Workload Mobility: Advances in cloud orchestration and hybrid cloud strategies make it easier for customers to migrate data and applications between different infrastructure environments.

- Negotiating Leverage: This inherent capability empowers customers to demand better pricing, more flexible contract terms, and superior service levels from Digital Realty.

- Market Dynamics: The trend is reinforced by the ongoing digital transformation initiatives across industries, pushing more organizations to evaluate all infrastructure options.

Hyperscale Clients Hold Sway Over Data Center Revenue

Digital Realty Trust's major clients, particularly hyperscale cloud providers, hold substantial bargaining power. Their ability to develop their own data centers or easily migrate to competitors gives them significant leverage in negotiations. This is underscored by the fact that in 2023, Digital Realty's top 20 customers represented about 40% of its rental revenue, highlighting the concentration of power among these anchor tenants.

| Customer Segment | Bargaining Power Factor | Impact on Digital Realty | 2023 Revenue Concentration (Top 20 Customers) | 2024 Market Trend |

|---|---|---|---|---|

| Hyperscale Cloud Providers | Ability to self-build or migrate | Forces competitive pricing and favorable terms | Approx. 40% of rental revenue | Continued drive for cost optimization |

| Large Enterprises | Demand for flexible DCaaS | Shorter contracts, dynamic pricing | N/A (part of overall customer base) | Global edge computing market projected over $270 billion |

| All Customers | Availability of alternative providers | Increased price sensitivity | N/A | Potential moderation in AI demand growth |

Preview the Actual Deliverable

Digital Realty Trust Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders, providing a comprehensive Porter's Five Forces analysis of Digital Realty Trust. You'll gain deep insights into the competitive landscape, including the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the data center industry. This detailed analysis is professionally written and formatted, ready for your immediate use.

Rivalry Among Competitors

Presence of Major Global Players

Digital Realty Trust operates in a fiercely competitive data center market, facing significant rivalry from major global players. Companies like Equinix, another prominent data center REIT, directly compete for colocation and interconnection services. Beyond REITs, numerous private data center operators and large hyperscalers, such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, are also expanding their own substantial infrastructure, intensifying the pressure.

This intense competition for market share and crucial customer contracts, particularly from large enterprise and cloud providers, naturally drives down pricing. For instance, in 2024, the average price per megawatt for data center space saw continued pressure due to this competitive landscape. Digital Realty must therefore focus on differentiation through services, geographic reach, and energy efficiency to maintain its competitive edge.

Rapid Market Expansion and Capacity Builds

The digital infrastructure sector is booming, fueled by the insatiable demand for AI and cloud services. This rapid expansion sees major players, including Digital Realty Trust, investing heavily in new data center capacity. For instance, hyperscale cloud providers alone are projected to increase their data center footprint significantly in the coming years, with substantial capital expenditures planned for 2024 and beyond.

However, this aggressive build-out by numerous competitors presents a double-edged sword. While demand is robust, a synchronized surge in new capacity across multiple markets could eventually lead to an oversupply situation. This intensified competition for tenants could pressure rental rates and impact occupancy levels, especially in markets with a high concentration of new builds.

Differentiation and Specialization

Companies in the data center industry, including Digital Realty Trust, differentiate themselves beyond mere price. They compete on critical factors like strategic location for low latency, robust connectivity through interconnection services, and the ability to provide high power density, which is increasingly vital for AI and high-performance computing. Sustainability initiatives are also becoming a key differentiator, appealing to environmentally conscious clients.

Digital Realty's strategic focus on colocation, a foundational offering, coupled with its extensive interconnection services and dark fiber networks, allows it to stand out. This specialization, combined with a significant global footprint, enables Digital Realty to offer unique value propositions that are difficult for competitors to replicate, thereby reducing direct price-based competition.

In 2024, the demand for specialized data center solutions, particularly those supporting AI, is soaring. Digital Realty reported that its AI-ready capacity was a significant driver of its business, with a robust pipeline for these high-density deployments. This focus on specialized, high-demand services allows them to command premium pricing and maintain a competitive edge.

Pricing Power and Renewal Spreads

Digital Realty's ability to raise rental rates on new and renewed leases is a significant measure of its competitive standing. The company has shown robust renewal spreads, especially within its larger operational segments, suggesting a degree of pricing power. This strength, however, is continually challenged by the competitive landscape of the data center market.

In 2024, the demand for data center space remained strong, driven by cloud adoption and AI growth. Digital Realty reported positive leasing spreads on renewals. For instance, in Q1 2024, their renewal rate change was positive, reflecting their ability to maintain or increase rental income from existing tenants. This indicates that while competition exists, Digital Realty's offerings and tenant relationships allow for some leverage in pricing negotiations.

- Digital Realty's renewal spreads in 2024 have generally been positive, indicating an ability to command favorable terms.

- The competitive nature of the data center market means this pricing power is not absolute and is subject to market conditions and competitor offerings.

- Strong tenant relationships and the specialized nature of their facilities can contribute to Digital Realty's ability to achieve higher renewal rates.

Geographic and Segment Competition

Digital Realty's competitive landscape shifts significantly based on geography and the specific market segment it targets. For instance, competition for hyperscale clients in North America might involve different players than those serving enterprise colocation needs in Europe.

This means Digital Realty must craft distinct strategies to contend with rivals like Equinix, CyrusOne, and QTS in various regions and for differing service offerings, such as colocation versus powered shell solutions.

- Hyperscale Competition: In markets with high demand from cloud providers, Digital Realty faces intense competition from companies capable of delivering massive, custom-built data center solutions.

- Enterprise Colocation: For enterprise clients seeking space, power, and connectivity, competition often comes from providers offering flexible, modular solutions and strong interconnection ecosystems.

- Regional Dynamics: Key competitors vary by region; for example, in Europe, companies like Interxion (now part of Digital Realty itself, but historically a competitor) and Telehouse are significant players, while in Asia, NTT and ST Telemedia are major forces.

- Service Specialization: Competition for powered shell offerings, where Digital Realty provides the building and core infrastructure, differs from colocation, which includes more managed services and connectivity.

The Data Center Battleground: Competing for Market Share

Competitive rivalry is a significant force for Digital Realty Trust, with numerous players vying for market share in the booming data center sector. Companies like Equinix, CyrusOne, and QTS are direct competitors, offering similar colocation and interconnection services. Furthermore, hyperscale cloud providers such as Amazon Web Services, Microsoft Azure, and Google Cloud are increasingly building their own infrastructure, intensifying competition for large enterprise clients and driving down pricing, especially evident in 2024's market dynamics.

Digital Realty differentiates itself through strategic locations, robust interconnection capabilities, and a focus on high-density deployments catering to AI workloads, a segment showing strong demand in 2024. While intense competition pressures pricing, Digital Realty's ability to secure positive renewal spreads, as seen in early 2024, suggests some pricing power derived from tenant relationships and specialized offerings.

The competitive landscape varies by region and service type, with different rivals emerging for hyperscale versus enterprise colocation needs. For instance, while Equinix is a global competitor, regional players like NTT in Asia also present significant rivalry, requiring tailored strategies for each market segment.

| Competitor | Primary Service Focus | Key Differentiator |

|---|---|---|

| Equinix | Colocation & Interconnection | Largest global interconnection ecosystem |

| CyrusOne | Hyperscale & Enterprise Data Centers | Large-scale build-to-suit capabilities |

| QTS Realty Trust | Colocation, Cloud & Enterprise | Integrated hybrid cloud solutions |

| Amazon Web Services (AWS) | Cloud Computing Infrastructure | Proprietary hyperscale facilities |

| Microsoft Azure | Cloud Computing Infrastructure | Extensive global cloud network |

SSubstitutes Threaten

Public Cloud Services

Public cloud services represent a significant substitute threat to Digital Realty Trust's core business. Companies can opt to migrate their IT infrastructure and data to hyperscale public cloud providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform. This approach eliminates the need for dedicated physical data center space, a service Digital Realty specializes in. For instance, in 2024, the global public cloud market was projected to exceed $600 billion, showcasing the massive scale and attractiveness of these alternatives.

On-Premise Data Centers

While the migration to third-party data centers is a strong trend, the threat of substitutes for Digital Realty Trust remains. For some enterprises, particularly those with stringent security, regulatory compliance, or unique legacy system needs, maintaining and expanding their own on-premise data centers continues to be a viable alternative. This can limit the addressable market for colocation providers.

Edge Computing Solutions

The rise of edge computing presents a potential threat to traditional centralized data centers like those operated by Digital Realty Trust. As the need for low-latency processing increases, driven by IoT and AI, solutions that process data closer to its origin could offer an alternative to relying solely on large, remote facilities. For instance, the global edge computing market was projected to reach $275 billion by 2027, indicating substantial growth and a potential diversion of investment away from hyperscale data centers.

Software-Defined Infrastructure and Virtualization

The increasing sophistication of software-defined infrastructure (SDI) and virtualization technologies presents a significant threat of substitutes for traditional data center providers like Digital Realty Trust. These advancements allow businesses to abstract and pool IT resources, enabling greater flexibility and efficiency in managing their computing needs. This can reduce the perceived necessity for dedicated physical data center space, as companies can optimize their on-premises or hybrid cloud environments more effectively.

For instance, the global virtualization market was valued at over $60 billion in 2023 and is projected to grow substantially. This growth indicates a strong trend towards virtualizing IT operations, which can lessen the demand for physical colocation services. Companies can achieve higher server utilization and consolidate workloads, thereby delaying or even eliminating the need for expansion into external data center facilities.

- Software-Defined Networking (SDN): SDN allows for centralized control and programmability of network resources, enabling dynamic allocation and optimization that can reduce reliance on physical network infrastructure within a data center.

- Server Virtualization: Technologies like VMware and KVM allow multiple virtual machines to run on a single physical server, significantly increasing hardware utilization and reducing the overall number of physical servers required.

- Hyperconverged Infrastructure (HCI): HCI integrates compute, storage, and networking into a single system, simplifying IT management and offering a more agile alternative to traditional, siloed infrastructure deployments.

- Cloud Computing: Public and private cloud services offer scalable and on-demand IT resources, providing a direct substitute for companies that might otherwise lease space in a colocation facility.

Improved Data Transmission Technologies

The emergence of improved data transmission technologies, such as 5G and advanced fiber optics, presents a significant threat of substitution for traditional data center services. These advancements enable faster and more efficient data movement, potentially diminishing the need for data to be physically housed in highly interconnected, centralized facilities. This could allow workloads to be distributed across a wider range of locations, including edge computing sites or even directly to end-user devices, thereby reducing the perceived value of Digital Realty Trust's core offering if clients can achieve similar performance and connectivity elsewhere.

For instance, the continued rollout of 5G, which offers significantly higher speeds and lower latency compared to previous generations, could empower businesses to run more applications and process more data closer to the source of generation. This trend might lessen reliance on large, centralized data centers for certain functions. By July 2025, the global 5G infrastructure market is projected to reach hundreds of billions of dollars, highlighting the rapid adoption and capability expansion of these alternative transmission methods.

- Reduced Dependence on Physical Data Centers: Enhanced connectivity allows for greater workload distribution, potentially decreasing demand for centralized colocation.

- Rise of Edge Computing: Faster data transmission supports processing at the network's edge, offering an alternative to traditional data center deployment.

- Technological Advancements: Innovations like 5G and improved fiber optics directly compete by offering alternative means of data access and processing.

Public Cloud and Edge Computing: Data Center Disruptors

The threat of substitutes for Digital Realty Trust is substantial, primarily driven by the growth of public cloud services. Companies are increasingly migrating their IT infrastructure to hyperscale providers like AWS, Azure, and Google Cloud, which directly bypass the need for physical data center space. This trend is underscored by the projected global public cloud market exceeding $600 billion in 2024.

Beyond public cloud, the rise of edge computing and advancements in software-defined infrastructure also present viable alternatives. Edge computing allows for data processing closer to its origin, potentially reducing reliance on large, centralized facilities. Furthermore, technologies like server virtualization and hyperconverged infrastructure enhance the efficiency of on-premises IT, lessening the perceived need for external colocation services.

| Substitute Category | Key Technologies/Providers | Impact on Digital Realty Trust | Market Size/Growth Indicator (2024/Projected) |

|---|---|---|---|

| Public Cloud | AWS, Microsoft Azure, Google Cloud | Direct replacement for colocation needs | Global market projected > $600 billion |

| Edge Computing | Various edge providers, IoT platforms | Decentralizes processing, reducing centralized data center demand | Global market projected $275 billion by 2027 |

| On-Premise Virtualization | VMware, KVM, HCI solutions | Increases efficiency of existing infrastructure, delaying colocation needs | Global virtualization market valued > $60 billion (2023) |

Entrants Threaten

High Capital Investment

The digital infrastructure sector, including data centers, demands an enormous upfront capital commitment. Building a modern data center involves significant costs for land, sophisticated cooling and power systems, and robust security. For instance, constructing a hyperscale data center can easily run into hundreds of millions of dollars, making it a daunting prospect for newcomers.

This substantial financial hurdle acts as a powerful deterrent for potential new competitors looking to enter the market. Companies like Digital Realty Trust, which have already invested billions in their global footprint, possess a significant advantage. The sheer scale of investment required means only well-funded entities can realistically consider challenging established players.

Access to Power and Connectivity

New entrants face substantial hurdles in securing the critical, high-density power and robust network connectivity required for modern data centers, particularly those supporting AI workloads. Existing operators, like Digital Realty Trust, benefit from established, long-term relationships with utility providers and network carriers, often securing favorable terms and priority access. For instance, in 2024, the demand for specialized power infrastructure for AI has surged, with some hyperscale cloud providers reportedly seeking power commitments exceeding 100MW per campus, a scale difficult for newcomers to replicate immediately.

Regulatory Hurdles and Permitting

The digital infrastructure sector, including data centers, faces significant regulatory hurdles. New entrants must navigate a complex web of local, state, and federal regulations concerning zoning, environmental impact, and data privacy. For instance, obtaining permits for large-scale data center construction can involve lengthy approval processes and substantial compliance costs, effectively deterring smaller or less capitalized competitors.

Expertise and Experience

The threat of new entrants in the data center industry, particularly for companies like Digital Realty Trust, is significantly influenced by the high barriers to entry related to expertise and experience. Developing, operating, and managing sophisticated data center facilities demands deep technical knowledge, robust operational capabilities, and a highly skilled workforce. New players must either cultivate this specialized expertise internally or acquire it, both of which represent substantial investments and time commitments.

This need for specialized knowledge creates a considerable hurdle. For instance, understanding and implementing advanced cooling systems, ensuring stringent security protocols, and maintaining uninterrupted power supply require years of hands-on experience. Digital Realty Trust, having been in operation for decades, has honed these skills, making it difficult for newcomers to replicate their level of operational efficiency and reliability.

The capital expenditure involved in building a single hyperscale data center can easily run into hundreds of millions of dollars, further deterring new entrants. Beyond the physical infrastructure, the operational expertise to manage these facilities effectively, including cybersecurity and network management, is a critical differentiator.

- High Capital Investment: Building a new, state-of-the-art data center can cost upwards of $500 million to $1 billion, a significant barrier for new entrants.

- Technical Expertise Gap: New companies must recruit and train personnel with specialized skills in areas like electrical engineering, mechanical systems, and network infrastructure.

- Operational Experience: Proven track records in uptime, security, and customer support are crucial for attracting clients, which new entrants lack.

- Regulatory Compliance: Navigating complex zoning laws, environmental regulations, and data privacy standards requires significant legal and operational know-how.

Customer Relationships and Trust

Digital Realty Trust, like other established data center providers, has cultivated deep, long-term relationships with a significant customer base, including major hyperscalers and enterprise clients. This trust is built on a track record of reliability, service quality, and understanding specific client needs. For instance, Digital Realty's focus on global connectivity and its extensive portfolio of interconnected facilities, which served over 4,000 customers as of late 2023, underscores the depth of these relationships.

New entrants face a formidable challenge in replicating this level of customer loyalty and trust. They would need substantial investments in sales infrastructure, marketing campaigns, and a proven history of operational excellence to even begin competing for these established relationships. The cost and time required to build this credibility are significant barriers.

- Established customer loyalty: Digital Realty's extensive client network, including major cloud providers and enterprises, represents a significant hurdle for new entrants.

- High investment requirements: New players must allocate considerable resources to sales, marketing, and building a reputation for reliability to attract and retain customers.

- Competitive market saturation: The data center industry is highly competitive, making it difficult for new entrants to gain market share against established, trusted providers.

- Demonstrated performance: A proven history of operational uptime and service delivery, like Digital Realty's consistent performance metrics, is crucial for building customer trust and is hard for new entrants to quickly establish.

Capital, Expertise, & AI Demand: Data Center Entry Barriers

The threat of new entrants for Digital Realty Trust is significantly mitigated by the immense capital required to establish a data center presence, often exceeding hundreds of millions of dollars per facility. This financial barrier, coupled with the need for specialized technical expertise in areas like power management and cooling, makes it exceptionally difficult for new players to compete. Furthermore, established relationships with utility providers and network carriers, secured by incumbents like Digital Realty, grant them preferential access and terms, a significant advantage newcomers struggle to replicate, especially as demand for high-density power for AI surged in 2024.

Porter's Five Forces Analysis Data Sources

Our Digital Realty Trust Porter's Five Forces analysis is built upon a robust foundation of data, including Digital Realty's SEC filings, annual reports, and investor presentations. We supplement this with industry-specific market research reports from firms like Gartner and IDC, as well as competitive intelligence gathered from news outlets and trade publications.