CSPC Pharmaceutical Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

CSPC Pharmaceutical Group Bundle

Go Beyond the Preview—Access the Full Strategic Report

CSPC Pharmaceutical Group operates in a dynamic industry, heavily influenced by intense rivalry, the bargaining power of buyers, and the constant threat of new entrants. Understanding these forces is crucial for navigating the competitive landscape and identifying strategic opportunities.

The pharmaceutical sector's high R&D costs and stringent regulatory hurdles impact the threat of substitutes and the bargaining power of suppliers for CSPC. These elements collectively shape the profitability and strategic direction of the company.

The complete report reveals the real forces shaping CSPC Pharmaceutical Group’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

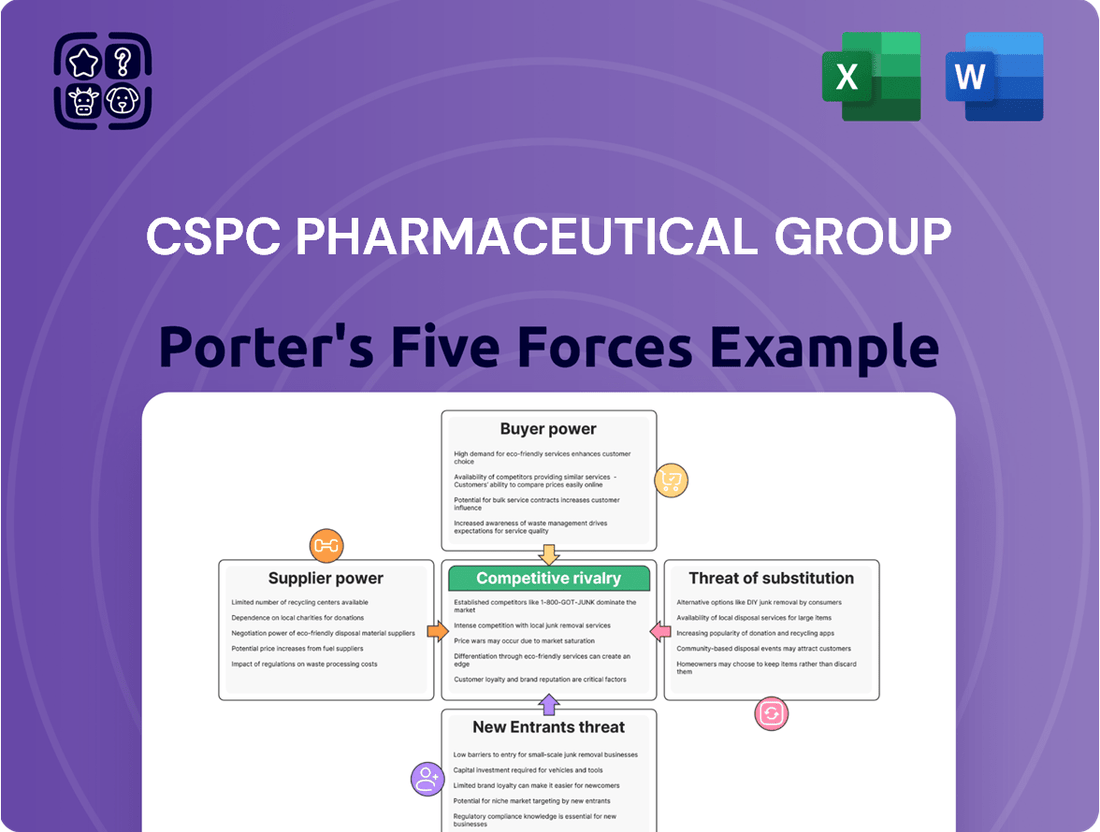

Suppliers Bargaining Power

Concentration of Key Raw Material Suppliers

The pharmaceutical sector, including companies like CSPC Pharmaceutical Group, depends heavily on a consistent supply of Active Pharmaceutical Ingredients (APIs) and essential chemical intermediates. If a limited number of suppliers control the production of critical or highly specialized APIs, their ability to negotiate prices rises, which can translate into increased raw material expenses for CSPC. For instance, a significant portion of global API production originates from China, potentially providing CSPC with a degree of purchasing influence.

Uniqueness and Differentiation of Inputs

Suppliers of highly specialized or patented raw materials, unique excipients, or advanced manufacturing equipment can wield significant bargaining power over CSPC Pharmaceutical Group. This is because the costs and complexities involved in switching to alternative suppliers for these critical inputs would be prohibitively high for CSPC. For instance, if CSPC's innovative drug development relies on a specific patented molecule or a unique delivery system component sourced from a single supplier, that supplier holds considerable leverage.

CSPC's strategic emphasis on developing innovative drugs, as evidenced by its substantial investment in research and development, often means it requires inputs that are not readily available from multiple sources. This reliance on niche suppliers for essential components in their cutting-edge pharmaceutical products directly enhances the suppliers' bargaining power. For example, in 2023, CSPC reported R&D expenses of RMB 3.88 billion, underscoring its commitment to innovation which inherently increases dependence on specialized suppliers.

When these specialized inputs are absolutely critical to CSPC's innovative pipeline and the successful launch of new blockbuster drugs, the influence of these niche suppliers on pricing, supply volumes, and overall contract terms becomes substantial. A delay or disruption in the supply of such a critical component could jeopardize years of R&D and significant financial investment, giving these suppliers considerable sway in negotiations. This is particularly true for active pharmaceutical ingredients (APIs) that are complex to synthesize or require proprietary manufacturing processes.

Threat of Forward Integration by Suppliers

Suppliers of critical pharmaceutical intermediates or specialized components could potentially move into manufacturing finished drugs themselves, directly competing with CSPC Pharmaceutical Group. This capability would significantly increase their bargaining power, as CSPC relies on these suppliers for essential inputs and would prefer to avoid developing new competitors. For instance, if a supplier for a key active pharmaceutical ingredient (API) sees strong demand and high margins in the finished drug market, they might invest in their own production lines.

The increasing global ambitions of Chinese pharmaceutical companies, including a greater focus on exporting finished products, further complicate this dynamic. This shift means suppliers might see a greater opportunity in bypassing intermediaries like CSPC and directly accessing international markets. In 2023, China's pharmaceutical exports reached over $50 billion, indicating a growing trend that could empower suppliers to consider forward integration.

Importance of CSPC to Supplier's Business

The significance of CSPC Pharmaceutical Group to its suppliers plays a crucial role in determining supplier bargaining power. If CSPC constitutes a substantial percentage of a supplier's total sales, that supplier's reliance on CSPC increases, thereby weakening their negotiating position. Conversely, if CSPC is a relatively small client for a large, diversified supplier, CSPC's individual bargaining leverage is diminished.

CSPC's status as a major pharmaceutical entity within China, evidenced by its significant market share and revenue, offers a degree of counter-leverage against suppliers. For instance, in 2023, CSPC's revenue reached RMB 34.06 billion, underscoring its considerable purchasing volume. This scale can give CSPC more influence in negotiations, particularly when dealing with suppliers whose business is heavily concentrated on the pharmaceutical sector.

- Supplier Dependence: When a supplier's revenue is heavily dependent on CSPC, their ability to demand higher prices or less favorable terms is reduced.

- CSPC's Scale: CSPC's large operational scale and market presence in China provide it with greater purchasing power.

- Supplier Diversification: If a supplier serves numerous clients, CSPC's importance to that supplier is diluted, limiting CSPC's direct leverage.

- Strategic Importance: For suppliers of critical raw materials or specialized components, CSPC's bargaining power may be more limited if alternative suppliers are scarce.

Switching Costs for CSPC

Switching costs for CSPC Pharmaceutical Group's suppliers are a significant factor in their bargaining power. These costs encompass not only the financial outlay for qualifying new materials but also the extensive process of re-validating existing manufacturing processes. In 2024, the pharmaceutical industry's stringent regulatory environment means that any change in raw material sourcing can trigger lengthy and expensive re-certification procedures, potentially delaying product launches and impacting revenue streams.

These substantial switching costs grant existing suppliers considerable leverage. CSPC would likely incur millions in direct costs and lost productivity if they were to change suppliers for critical active pharmaceutical ingredients (APIs) or specialized excipients. This reluctance to disrupt established, validated supply chains means suppliers of these specialized or regulated inputs hold a stronger negotiating position, able to command more favorable terms.

- High Switching Costs: Expenses related to qualifying new materials and re-validating manufacturing processes.

- Regulatory Hurdles: The pharmaceutical industry's strict compliance requirements amplify the difficulty and cost of supplier changes.

- Supplier Leverage: Existing suppliers benefit from CSPC's avoidance of disruption and expense, strengthening their negotiation power.

- Specialized Inputs: Sourcing for unique or highly regulated components presents even greater switching challenges.

Supplier Leverage: Shaping CSPC's Costs and Innovation Pathways

The bargaining power of suppliers for CSPC Pharmaceutical Group is influenced by the concentration of suppliers for critical raw materials, particularly Active Pharmaceutical Ingredients (APIs) and specialized intermediates. If only a few entities control the production of essential components, they can command higher prices, directly impacting CSPC's cost structure. For example, while China is a major API producer, specific complex molecules might still be sourced from a limited number of highly specialized manufacturers.

Suppliers of patented or unique inputs vital for CSPC's innovative drug development hold significant leverage due to the high costs and complexities associated with finding alternatives. This dependence on specialized suppliers for cutting-edge products amplifies their negotiation power. CSPC's 2023 R&D expenditure of RMB 3.88 billion highlights its reliance on such specialized inputs.

Switching costs for CSPC are substantial, encompassing not only financial outlays but also the rigorous regulatory re-validation of manufacturing processes, especially critical in 2024. These hurdles deter CSPC from changing suppliers for essential, validated components, thus strengthening the position of existing suppliers.

| Factor | Description | Impact on CSPC |

| Supplier Concentration | Limited number of producers for key APIs/intermediates. | Increased raw material costs if suppliers have high market share. |

| Switching Costs | High expenses for material qualification and process re-validation. | Suppliers retain leverage due to CSPC's avoidance of disruption. |

| Input Uniqueness | Reliance on patented or specialized components for innovation. | Suppliers of these critical inputs gain significant pricing power. |

| CSPC's Scale | Large purchasing volume provides some counter-leverage. | Can mitigate supplier power if CSPC represents a significant portion of supplier revenue. |

What is included in the product

This analysis unpacks the competitive forces impacting CSPC Pharmaceutical Group, examining the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the availability of substitutes.

Effortlessly identify and address competitive threats within the pharmaceutical landscape, alleviating the pain point of navigating complex market dynamics.

Customers Bargaining Power

Price Sensitivity and Volume-Based Procurement

CSPC's customer base, comprising hospitals, distributors, and government procurement entities, exhibits considerable price sensitivity. This is largely influenced by China's national reimbursement drug list (NRDL) and volume-based procurement (VBP) initiatives. These policies are designed to exert downward pressure on drug prices, directly impacting CSPC's revenue streams.

The impact of VBP policies is particularly pronounced. For instance, CSPC has experienced average price reductions exceeding 50% on successful bids within these centralized procurement programs. This demonstrates the substantial bargaining power that customers wield when purchasing in high volumes under these government-mandated frameworks.

Customer Concentration and Government Influence

CSPC Pharmaceutical Group's customer base in China is characterized by significant concentration, with a substantial portion of sales flowing through major distributors or directly to large hospital networks and government entities via tenders. This concentration inherently amplifies the bargaining power of these key customers.

The Chinese government wields considerable influence over the pharmaceutical sector, particularly through its role in drug procurement and reimbursement policies. This governmental power allows it to dictate terms and negotiate prices aggressively, impacting CSPC's revenue and profitability.

While the inclusion of new CSPC drugs in the National Reimbursement Drug List (NRDL) is crucial for market access, it necessitates engaging in rigorous price negotiations with the government. For instance, in 2024, numerous pharmaceutical companies, including those with products on the NRDL, faced intensified price reduction mandates during procurement rounds.

Availability of Alternative Drugs and Generics

Customers wield significant power when a drug has many generic or biosimilar alternatives. This allows them to easily switch to more affordable options, pressuring manufacturers on pricing. For CSPC Pharmaceutical Group, this is particularly relevant as its portfolio includes both innovative treatments and more common generics, exposing it to direct price competition.

The increasing number of Chinese innovative drug developers further amplifies this competitive pressure. As more domestic companies bring novel therapies to market, customers gain more choices, intensifying the need for CSPC to differentiate its offerings and manage its cost structures effectively.

Customer Information and Transparency

Increased transparency in drug pricing and efficacy, often driven by government initiatives and public access to information, significantly bolsters customer bargaining power. This allows informed consumers to compare options and negotiate for better value, putting pressure on CSPC Pharmaceutical Group. For instance, in 2024, several countries continued to implement measures promoting greater price transparency for pharmaceuticals, enabling patients and healthcare providers to make more cost-effective decisions.

This heightened transparency can intensify price competition, potentially limiting CSPC's ability to charge premium prices for its products. Regulatory updates aimed at streamlining drug registration processes also contribute to this market transparency by facilitating the entry of new competitors. In 2024, the Chinese government's ongoing efforts to reform drug procurement and pricing mechanisms, such as volume-based purchasing in the national centralized procurement program, directly impacted the pricing power of pharmaceutical companies, including CSPC.

- Increased Information Access: Customers have greater access to comparative drug pricing and effectiveness data.

- Price Sensitivity: Transparency fuels price sensitivity among buyers, leading to demands for lower costs.

- Competitive Pressure: Enhanced transparency intensifies competition, challenging premium pricing strategies.

- Regulatory Influence: Government policies promoting transparency and streamlined registration empower customers.

Backward Integration by Customers

Backward integration by customers, while a significant threat in many industries, presents a more nuanced challenge for pharmaceutical companies like CSPC Pharmaceutical Group. While direct customers such as hospitals typically lack the capital and expertise for drug manufacturing, large distributor networks or integrated healthcare systems could theoretically explore this avenue. For instance, a major hospital chain might consider investing in specialized manufacturing for high-demand generic drugs, although the regulatory hurdles and R&D investment required are substantial. This potential, even if remote, grants these larger entities a degree of bargaining power in price negotiations.

The ability of these large customers to consolidate their purchasing power further amplifies their leverage. For example, if a national healthcare provider procures a significant percentage of its annual drug needs from CSPC, they can exert considerable pressure on pricing. In 2024, major healthcare systems continued to consolidate, leading to increased purchasing volumes and a stronger collective voice in supplier negotiations.

- High Barriers to Entry: The pharmaceutical manufacturing sector demands significant capital investment, specialized technology, and strict regulatory compliance, making it difficult for most customers to integrate backward.

- Consolidated Demand: Large hospital groups or national pharmacy chains can leverage their combined purchasing power to negotiate more favorable terms with manufacturers like CSPC.

- Potential for Niche Manufacturing: While unlikely for complex biologics, customers might explore backward integration for simpler, high-volume generic drugs where the manufacturing process is more standardized.

- Regulatory Complexity: Navigating the stringent regulatory landscape for drug production, including Good Manufacturing Practices (GMP), is a substantial deterrent to backward integration for most customer entities.

Customer Power Reshapes Drug Pricing in China

CSPC's customers, particularly government procurement entities and large hospital networks, wield substantial bargaining power. This is driven by China's volume-based procurement (VBP) policies, which have led to significant price reductions, often exceeding 50% on successful bids in 2024. The concentration of CSPC's sales through major distributors and government tenders further consolidates customer influence.

Increased transparency in drug pricing and the growing number of domestic innovative drug developers also empower customers. In 2024, regulatory efforts promoting price transparency allowed buyers to compare options more effectively, intensifying price competition. This environment challenges CSPC's ability to maintain premium pricing, especially for products with available generic or biosimilar alternatives.

| Factor | Impact on CSPC | Data/Example (2024) |

| Volume-Based Procurement (VBP) | Significant price reduction pressure | Average price cuts >50% on successful bids |

| Customer Concentration | Amplified customer leverage | Sales through major distributors/government tenders |

| Price Transparency & Competition | Weakened premium pricing power | Increased buyer ability to compare and negotiate |

| Government Policies (NRDL, VBP) | Direct price negotiation mandates | Intensified price reduction demands during procurement |

Preview Before You Purchase

CSPC Pharmaceutical Group Porter's Five Forces Analysis

The document you see is your deliverable. It’s ready for immediate use—no customization or setup required. This comprehensive Porter's Five Forces analysis of CSPC Pharmaceutical Group details the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the threat of substitute products within the pharmaceutical industry. Understanding these forces is crucial for strategic decision-making and navigating the competitive landscape effectively.

Rivalry Among Competitors

Number and Diversity of Competitors

The Chinese pharmaceutical market is a battleground, teeming with both domestic powerhouses and global giants. CSPC Pharmaceutical Group navigates this landscape alongside formidable rivals like Sinopharm and Shanghai Pharmaceuticals, who boast extensive distribution networks and established brand recognition.

Multinational corporations such as Pfizer, Novartis, and AstraZeneca also maintain a significant presence, leveraging their innovation pipelines and global marketing expertise to capture market share in China. This diverse competitive set means CSPC must continuously innovate and optimize its offerings.

The market's fragmentation, particularly within the generics and traditional Chinese medicine segments, amplifies the intensity of this rivalry. In 2023, China's pharmaceutical market was valued at over $300 billion, with generics accounting for a substantial portion, creating fierce price competition.

Industry Growth Rate and Innovation Focus

The Chinese pharmaceutical market's growth, especially in innovative drugs and biologics, fuels intense competition across key therapeutic areas such as oncology and cardiovascular treatments. This dynamic environment forces companies to ramp up R&D spending to bring novel, high-margin products to market, igniting a fierce innovation race.

CSPC Pharmaceutical Group is actively participating in this trend, strategically pivoting its focus towards the production of innovative drugs and significantly increasing its research and development expenditures. In 2023, CSPC's R&D investment reached approximately RMB 3.3 billion, marking a substantial commitment to its innovation pipeline.

Product Differentiation and Brand Loyalty

CSPC Pharmaceutical Group operates in a highly competitive landscape where product differentiation is key. Innovative, patented drugs with novel mechanisms of action or proven superior clinical outcomes are the primary drivers of differentiation, allowing companies like CSPC to command premium pricing and foster brand loyalty among prescribers and patients. For instance, the success of innovative oncology drugs often hinges on their ability to target specific pathways or offer better safety profiles than existing treatments.

However, the generic segment of the pharmaceutical market, where CSPC also has a significant presence, experiences minimal product differentiation. This lack of distinctiveness forces intense price competition, as generic manufacturers vie for market share based on cost-effectiveness. In 2024, the global generic drug market continued to see aggressive pricing strategies, with many players focusing on manufacturing efficiency to undercut rivals.

While brand loyalty can be a factor for established finished pharmaceutical products, its impact on CSPC's sales is often tempered by government procurement policies. Many national health systems and tenders prioritize the lowest bid, effectively neutralizing the advantage of a strong brand reputation. This means that even well-regarded brands can face significant price pressure in tenders, as seen in many of China's centralized drug purchasing initiatives throughout 2024, where price reductions of over 50% were not uncommon for successful bidders.

Exit Barriers for Competitors

CSPC Pharmaceutical Group faces intense competition, partly due to high exit barriers. The pharmaceutical industry, especially in China, demands substantial investments in specialized manufacturing facilities and cutting-edge research and development. These sunk costs, often running into hundreds of millions or even billions of dollars, make it economically unviable for companies to simply shut down and exit. For instance, setting up a new pharmaceutical production line in China can easily cost upwards of $50 million, and ongoing R&D into new drug pipelines requires continuous, significant capital outlay. This creates a situation where even struggling competitors are incentivized to remain active, battling for market share rather than cutting their losses.

Furthermore, regulatory shifts in China are actively reinforcing this dynamic. Recent reforms, such as the accelerated drug approval process and the push for innovative therapies, encourage companies to maintain and even expand their presence. This environment means that CSPC Pharmaceutical Group must contend with rivals who are deeply entrenched and motivated to stay competitive. The ongoing commitment to innovation, coupled with the sheer scale of investment required to operate, ensures that the competitive rivalry remains a defining feature of the Chinese pharmaceutical landscape, impacting pricing strategies and market penetration efforts for all players.

- High Capital Investment: Pharmaceutical manufacturing and R&D require substantial, often irreversible, investments in specialized equipment, facilities, and intellectual property, making exit costly.

- R&D Commitment: Continuous investment in drug discovery and development is essential for competitiveness, creating significant ongoing costs that deter exiting.

- Specialized Labor: The need for highly skilled scientists, researchers, and technicians adds to fixed costs and makes workforce redeployment difficult upon exit.

- Regulatory Environment: China's evolving regulatory landscape, which favors innovation and market participation, further discourages companies from leaving, thereby intensifying rivalry.

Strategic Alliances and Acquisitions

Strategic alliances and acquisitions significantly influence the competitive rivalry for CSPC Pharmaceutical Group. Collaborations, like the one with AstraZeneca for AI-driven drug discovery and lipid-lowering therapies, bolster CSPC's capabilities and market presence. These partnerships are crucial for navigating a dynamic industry where shared resources and expertise are vital for innovation and global expansion.

The pharmaceutical sector, including players like CSPC, increasingly relies on mergers and acquisitions to consolidate market share and acquire new technologies or product pipelines. For instance, in 2023, the global pharmaceutical M&A deal value saw a notable increase, reflecting a strategic push by companies to strengthen their competitive standing through inorganic growth. This trend suggests that companies forming strong alliances and pursuing strategic acquisitions are better positioned to face intense rivalry.

- CSPC Pharmaceutical Group's alliance with AstraZeneca focuses on AI-powered drug discovery and novel lipid-lowering therapies.

- Such collaborations enhance competitive positioning and facilitate global market expansion.

- Mergers and acquisitions are strategic tools for consolidating market share and acquiring new technologies in the pharmaceutical industry.

- The trend of strategic partnerships is a key indicator of a dynamic and competitive landscape, crucial for sustained growth.

CSPC Navigates Intense Pharma Competition and Price Wars

CSPC Pharmaceutical Group faces intense competition from domestic rivals like Sinopharm and Shanghai Pharmaceuticals, as well as global players such as Pfizer and Novartis. This rivalry is exacerbated by the market's fragmentation, particularly in generics, where price competition is fierce. For example, in 2024, aggressive pricing strategies were common in the global generic drug market.

SSubstitutes Threaten

Availability of Generic and Biosimilar Drugs

The pharmaceutical industry faces a significant threat from generic and biosimilar drugs. Once a patented drug's exclusivity period ends, these lower-cost alternatives enter the market, directly competing and driving down prices for off-patent medications. This dynamic puts pressure on companies like CSPC Pharmaceutical Group, impacting revenue streams from their established products.

China's Volume-Based Purchasing (VBP) program further intensifies this substitution threat. VBP aggressively negotiates prices for drugs, often favoring generics and biosimilars. For instance, in 2023, VBP tenders saw significant price reductions, with some drug categories experiencing drops exceeding 50%, directly impacting the profitability of off-patent products for domestic manufacturers.

Traditional Chinese Medicine (TCM)

Traditional Chinese Medicine (TCM) presents a considerable threat of substitutes for CSPC Pharmaceutical Group's offerings. Many Chinese consumers turn to TCM for various ailments, influenced by deep-rooted cultural preferences, cost-effectiveness, and a perception of gentler treatment compared to Western medicine. This makes TCM a viable alternative, especially for chronic conditions where long-term management is key.

The inclusion of traditional herbal formulations within China's National Reimbursement Drug List (NRDL) further solidifies TCM's position as a competitive substitute. In 2023, approximately 60% of TCM products were covered by the NRDL, indicating strong government support and accessibility for these treatments. This accessibility means patients can often choose TCM options that are financially covered, directly impacting the demand for CSPC's Western-style pharmaceuticals.

Lifestyle Changes and Preventive Healthcare

The growing emphasis on lifestyle changes and preventive healthcare presents a significant threat of substitution for CSPC Pharmaceutical Group. For chronic conditions such as cardiovascular diseases, healthier diets and regular exercise can lessen the reliance on medications, directly impacting demand for related pharmaceutical products.

Increased public health awareness, particularly concerning chronic disease management, fuels this trend. For instance, in 2024, global health organizations continued to highlight the role of lifestyle interventions, with studies showing that adherence to Mediterranean diets can reduce cardiovascular events by up to 30%, potentially curbing the market for certain cholesterol-lowering drugs.

This shift towards proactive health management is a long-term dynamic. As more individuals adopt preventive strategies, the need for pharmaceutical treatments for conditions that could have been mitigated or delayed through lifestyle adjustments may decline, posing a substitution threat to CSPC's product portfolio.

Alternative Therapies and Medical Devices

Alternative therapies and medical devices present a significant threat to pharmaceutical companies like CSPC Pharmaceutical Group. Non-pharmacological treatments such as surgery, physical therapy, and psychotherapy can directly substitute for drug-based therapies across various conditions. For instance, advancements in minimally invasive surgical techniques or sophisticated medical devices designed to manage chronic pain or cardiovascular issues can lessen the demand for specific medications.

The increasing sophistication and adoption of medical technology mean that for certain ailments, a device or procedure might offer a more effective or convenient solution than a pharmaceutical product. This competitive pressure from alternative treatments compels pharmaceutical firms to continually innovate and focus on therapeutic areas with significant unmet medical needs where drugs remain the primary or only viable option.

Consider the market for pain management; while opioids and other pain relievers are prevalent, the rise of non-opioid alternatives like nerve stimulation devices or advanced physical therapy protocols directly challenges the market share of traditional pharmaceuticals. In 2024, the global medical devices market was valued at over $600 billion, indicating a substantial and growing alternative to drug-based treatments.

- Substitution Risk: Non-drug treatments like surgery, physical therapy, and medical devices can reduce reliance on CSPC's pharmaceutical products.

- Technological Advancement Impact: New medical technologies or surgical methods may decrease the necessity for certain drugs, impacting CSPC's market share.

- Focus on Unmet Needs: This threat pushes pharmaceutical companies towards areas where drug therapies are indispensable due to a lack of viable alternatives.

- Market Data Insight: The significant size of the medical devices market underscores the tangible threat posed by these non-pharmacological substitutes.

Emerging Digital Health Solutions and Diagnostics

The increasing prevalence of digital health solutions and advanced diagnostics poses a significant threat of substitution for traditional pharmaceutical products. Platforms offering remote patient monitoring and personalized treatment plans can potentially reduce the reliance on continuous medication for chronic conditions. For instance, by mid-2024, wearable health trackers and continuous glucose monitors are becoming more sophisticated, offering real-time data that allows for more proactive disease management, potentially lessening the need for some prescription drugs.

These evolving digital tools are reshaping healthcare delivery, shifting the focus from purely pharmacological interventions to more integrated, tech-enabled approaches. While still in development stages for many applications, the long-term impact could see these solutions directly competing with certain drug therapies by offering alternative management pathways. The market for digital therapeutics, which are evidence-based interventions delivered via software, is projected to grow substantially, indicating a tangible shift in how health issues are addressed.

Furthermore, advancements in artificial intelligence (AI) within drug discovery, while an opportunity for pharmaceutical companies, also carry a dual nature. AI can accelerate the development of new drugs, but it also has the potential to uncover highly effective non-drug interventions or preventative strategies. For example, AI-driven insights into genetic predispositions or lifestyle factors might lead to personalized wellness programs or medical devices that can substitute for pharmaceutical treatments in certain health areas. As of 2024, AI-powered diagnostic tools are increasingly being used to identify disease earlier and with greater precision, which could influence treatment decisions away from broad-spectrum pharmaceuticals towards more targeted or even non-pharmacological interventions.

- Digital Health Platforms: Growing adoption of remote monitoring, telehealth, and AI-driven health apps.

- Advanced Diagnostics: Increased use of genetic testing and AI-powered imaging for earlier and more precise disease identification.

- Digital Therapeutics: Expansion of software-based interventions for managing chronic diseases, offering alternatives to medication.

- AI in Drug Discovery: Potential for AI to identify non-drug interventions or highly targeted therapies that could reduce the need for existing pharmaceutical products.

Beyond Pills: The Rise of Pharmaceutical Alternatives

The threat of substitutes for CSPC Pharmaceutical Group is multifaceted, encompassing generic and biosimilar competition, Traditional Chinese Medicine (TCM), lifestyle changes, alternative therapies, and digital health solutions. These substitutes directly challenge CSPC's market share and pricing power.

Generic and biosimilar drugs, post-patent expiry, offer significant cost advantages, forcing price reductions on original medications. China's Volume-Based Purchasing (VBP) program further exacerbates this by aggressively negotiating prices, often favoring these lower-cost alternatives. In 2023, some VBP drug categories saw price drops exceeding 50%, directly impacting revenue from off-patent products.

TCM remains a strong substitute due to cultural preference and cost-effectiveness, with about 60% of TCM products covered by China's National Reimbursement Drug List (NRDL) in 2023, enhancing their accessibility and competitive edge against Western pharmaceuticals.

Lifestyle interventions and preventive healthcare are increasingly reducing reliance on medications for chronic conditions. Studies in 2024 highlighted that adherence to diets like the Mediterranean can cut cardiovascular events by up to 30%, potentially impacting the market for related drugs.

The global medical devices market, valued at over $600 billion in 2024, represents a substantial alternative to drug-based treatments, with advancements in areas like pain management offering non-pharmacological solutions.

Digital health platforms and advanced diagnostics, including AI-powered tools and digital therapeutics, are reshaping healthcare by offering personalized management and potentially reducing the need for continuous medication. The market for digital therapeutics is experiencing substantial growth, signaling a shift towards tech-enabled health solutions.

| Substitute Category | Key Drivers | Impact on CSPC | Supporting Data/Trend (as of 2023-2024) |

|---|---|---|---|

| Generic & Biosimilar Drugs | Lower cost, patent expiry | Price erosion, reduced market share for off-patent drugs | VBP price drops >50% in some categories (2023) |

| Traditional Chinese Medicine (TCM) | Cultural preference, cost-effectiveness, government support | Reduced demand for Western pharmaceuticals in certain segments | ~60% of TCM products on NRDL (2023) |

| Lifestyle & Preventive Healthcare | Increased health awareness, focus on wellness | Decreased reliance on medications for chronic conditions | Mediterranean diet can reduce cardiovascular events by ~30% (studies in 2024) |

| Alternative Therapies & Medical Devices | Technological advancements, non-pharmacological efficacy | Direct competition for specific treatment areas | Global medical devices market >$600 billion (2024) |

| Digital Health & Diagnostics | Technological innovation, personalization, remote monitoring | Potential reduction in medication use, shift in treatment paradigms | Growing market for digital therapeutics |

Entrants Threaten

High Capital Requirements for R&D and Manufacturing

Entering the pharmaceutical sector, particularly in areas like innovative drug development, demands substantial financial commitments. Companies need to allocate significant funds towards research and development (R&D), extensive clinical trials, and the construction of state-of-the-art manufacturing facilities that adhere to stringent Good Manufacturing Practice (GMP) standards. These considerable capital requirements act as a formidable barrier, effectively deterring many potential new players from entering the market.

Stringent Regulatory Approval Processes

Stringent regulatory approval processes represent a significant barrier for new entrants in the pharmaceutical sector. Companies like CSPC Pharmaceutical Group must navigate complex requirements from bodies such as China's National Medical Products Administration (NMPA). These processes involve extensive clinical trials and detailed documentation, demanding substantial investment in time and specialized knowledge. For example, in 2024, the NMPA continued to emphasize rigorous standards for drug safety and efficacy, making it challenging for unestablished firms to gain market access.

Intellectual Property and Patent Protection

CSPC Pharmaceutical Group benefits significantly from intellectual property and patent protection for its groundbreaking drugs. This shields its innovative products, often granting them a period of market exclusivity, effectively creating a temporary monopoly. For any potential new entrant, the barrier is substantial: they must either invest heavily in discovering entirely novel molecular entities or meticulously navigate the intricate and costly patent landscape. CSPC's proactive approach to patent filing, with a steady stream of applications to safeguard its research and development, further solidifies this protective moat.

Established Distribution Channels and Brand Reputation

CSPC Pharmaceutical Group benefits from deeply entrenched distribution channels. Pharmaceutical giants like CSPC have nurtured long-standing relationships with major hospitals, retail pharmacies, and wholesale distributors across China and internationally. These established networks are crucial for ensuring widespread product availability and timely delivery, a significant hurdle for any new competitor aiming to gain market access.

Brand reputation acts as another formidable barrier. CSPC, along with other leading players, has cultivated substantial brand recognition and trust among healthcare professionals and patients over years of consistent product quality and efficacy. Building this level of credibility and loyalty requires significant investment in marketing, clinical trials, and patient support, making it exceedingly difficult for newcomers to challenge existing market perceptions.

- Established Networks: CSPC's existing distribution agreements provide preferential access to key market segments, a privilege new entrants would struggle to replicate quickly.

- Brand Equity: Years of investment in R&D and marketing have resulted in strong brand recognition for CSPC, fostering patient and physician preference.

- Regulatory Familiarity: Long-standing players possess a deep understanding of complex pharmaceutical regulations, streamlining market entry and compliance processes.

Need for Specialized Scientific Expertise and Talent

The pharmaceutical industry, including companies like CSPC Pharmaceutical Group, is heavily reliant on a deep well of specialized scientific and medical knowledge. Developing new drugs requires expertise in fields such as molecular biology, pharmacology, and clinical trial management. New entrants often struggle to build this foundational scientific capability from scratch.

Attracting and retaining top-tier talent is a significant hurdle. Highly skilled researchers and scientists in areas like drug discovery, toxicology, and regulatory affairs are in high demand globally. For instance, as of 2024, the competition for experienced pharmacologists in China's rapidly growing biotech sector remains intense, driving up recruitment costs and timeframes for new companies.

The complexity of pharmaceutical R&D means that without established teams and a proven track record, new entrants face a steep learning curve. This need for specialized expertise acts as a significant barrier, as it requires substantial upfront investment in both human capital and research infrastructure, making it challenging for newcomers to compete effectively with established players like CSPC.

- High demand for specialized scientific talent

- Difficulty in attracting and retaining experts in pharmacology, toxicology, and clinical development

- Significant upfront investment required for R&D infrastructure and personnel

- Intense competition for skilled professionals in key markets like China

Pharma Market Entry: High Walls, Low Threat

The threat of new entrants for CSPC Pharmaceutical Group is generally considered moderate to low due to several significant barriers. High capital requirements for R&D and manufacturing, coupled with stringent regulatory approvals from bodies like China's NMPA in 2024, make market entry exceptionally difficult.

Intellectual property protection, established distribution networks, and strong brand reputation cultivated by CSPC further deter new players. The intense competition for specialized scientific talent, a critical factor in drug development, also presents a substantial challenge for aspiring entrants.

For example, in 2024, the cost to bring a new drug to market remained exceptionally high, often exceeding billions of dollars, a figure prohibitive for most new companies. This financial and regulatory landscape, combined with CSPC's entrenched market position, significantly limits the likelihood of new entrants disrupting the market.

| Barrier Type | Description | Impact on New Entrants for CSPC |

|---|---|---|

| Capital Requirements | High R&D, clinical trials, and manufacturing costs. | Significant deterrent; requires substantial funding. |

| Regulatory Approvals | Complex and lengthy processes (e.g., NMPA in 2024). | Time-consuming and costly, demanding specialized expertise. |

| Intellectual Property | Patents and exclusivity periods. | Requires innovation or costly patent navigation. |

| Distribution Channels | Established relationships with hospitals and pharmacies. | Difficult to replicate, impacting market access. |

| Brand Reputation | Trust and recognition built over time. | Challenging to establish credibility against established brands. |

| Talent Acquisition | Competition for skilled researchers and scientists. | Drives up recruitment costs and timeframes. |

Porter's Five Forces Analysis Data Sources

Our CSPC Pharmaceutical Group Porter's Five Forces analysis is built upon a robust foundation of data, drawing from annual financial reports, industry-specific market research from firms like IQVIA, and public company disclosures including SEC filings.

We leverage insights from regulatory bodies, pharmaceutical trade journals, and economic databases to provide a comprehensive understanding of the competitive landscape for CSPC Pharmaceutical Group.