China Resources Beer (Holdings) Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

China Resources Beer (Holdings) Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

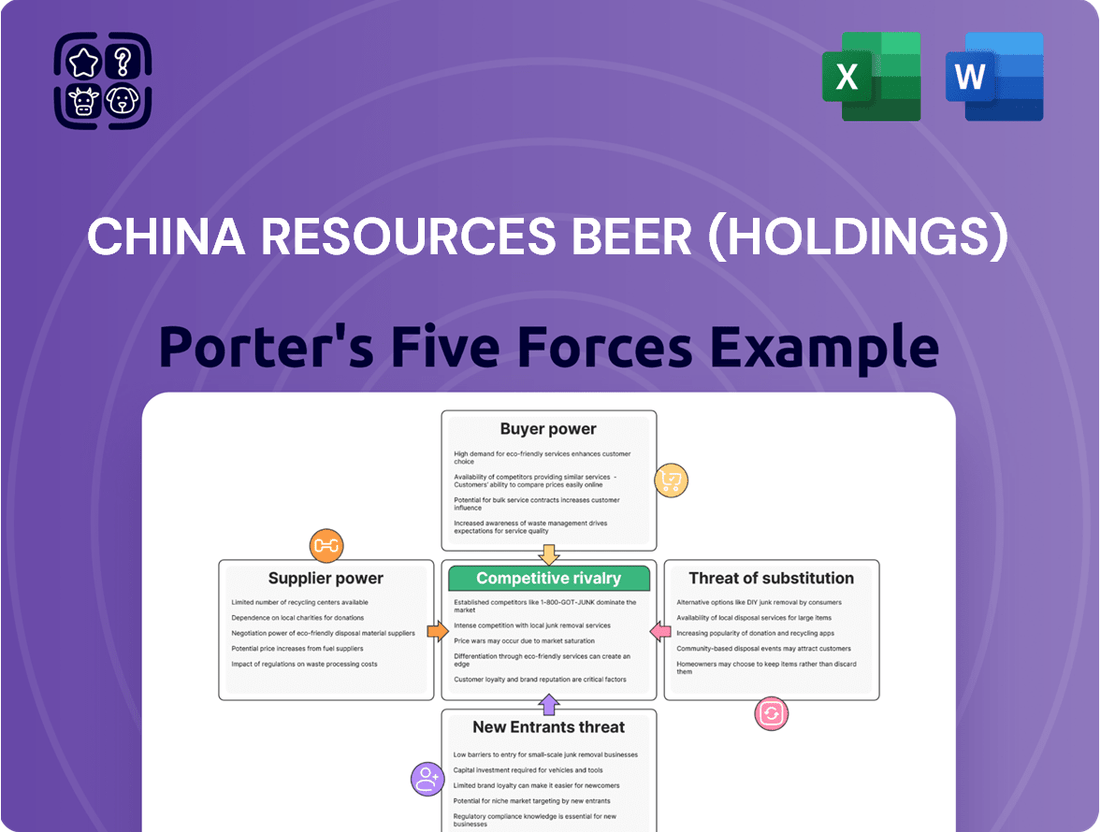

China Resources Beer (Holdings) navigates a competitive landscape shaped by intense rivalry and the looming threat of substitutes. Understanding the power of buyers and the influence of suppliers is crucial for unlocking their strategic positioning.

The complete report reveals the real forces shaping China Resources Beer (Holdings)’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Suppliers

The market for essential brewing inputs like malt, hops, and yeast in China has become more diverse. This growth in both domestic and international suppliers means there are more options for major buyers such as China Resources Beer. This increased competition tends to weaken the bargaining power of individual suppliers.

While the overall supplier landscape is more competitive, specialized or high-quality ingredients, particularly those used in premium beer segments, can still allow certain suppliers to maintain some leverage. For example, in 2024, the import of specialty hops from regions like the Pacific Northwest of the US, known for their unique aroma profiles, continued to be a significant factor for craft beer production, indicating potential residual power for those specific suppliers.

Importance of Raw Materials

Raw materials, such as barley and packaging, represent a substantial cost component for beer manufacturers. In 2023, the cost of key ingredients like barley saw fluctuations, impacting overall production expenses for major players in the Chinese beer market.

The Chinese beer industry, including companies like China Resources Beer, has faced increasing pressure on its profit margins. This is largely attributed to the rising costs of these crucial raw materials, making efficient sourcing paramount.

Consequently, effective procurement strategies and robust supply chain management are vital for China Resources Beer to mitigate the impact of fluctuating raw material prices and maintain healthy profit margins.

Switching Costs

For a major player like China Resources Beer, switching key suppliers, such as those providing malt or hops, isn't a simple flip of a switch. It entails significant logistical hurdles, the need to re-evaluate and potentially adjust quality standards, and the complex process of negotiating entirely new agreements. These embedded switching costs, even if not itemized in public reports, naturally give established suppliers a stronger hand in price discussions.

Supplier Differentiation

Supplier differentiation significantly impacts bargaining power. When suppliers offer unique or highly specialized inputs, especially for premium products, their leverage increases. For China Resources Beer, as it pushes its premiumization strategy, securing consistent, high-quality, and potentially exclusive ingredients for its craft and premium offerings becomes paramount.

This focus on quality and uniqueness can shift power towards specialized ingredient suppliers. For instance, access to specific hop varieties or malts crucial for distinctive flavor profiles in craft beers can give these suppliers more negotiating strength. China Resources Beer's commitment to expanding its premium portfolio, which saw its Snow brand's market share in the premium segment grow, underscores the importance of these specialized inputs.

- Supplier Differentiation: Suppliers providing unique or specialized ingredients, particularly for premium and craft beer production, hold greater bargaining power.

- Premiumization Strategy: China Resources Beer's increasing focus on premium products makes access to consistent, high-quality, and potentially unique ingredients more critical.

- Ingredient Leverage: This critical need for specialized ingredients can enhance the negotiating leverage of suppliers who can consistently deliver on quality and uniqueness.

- Market Impact: The ability to secure these differentiated inputs is vital for China Resources Beer's strategy to capture a larger share of the growing premium beer market.

Threat of Forward Integration

The threat of forward integration by raw material suppliers into beer production for companies like China Resources Beer is generally low. The sheer scale of investment needed for brewing facilities and nationwide distribution makes it a formidable challenge for most suppliers.

Consider the capital required: establishing a brewery comparable to China Resources Beer's operations, which produced 10.1 million kiloliters of beer in 2023, would necessitate billions of dollars. Furthermore, navigating the intricate production processes and building the extensive sales and distribution networks that reach consumers across China represents a significant barrier to entry.

- Low Likelihood of Supplier Forward Integration: Suppliers typically lack the immense capital and operational expertise to compete directly with established brewers.

- High Barriers to Entry: The beer industry demands substantial investment in manufacturing, branding, and distribution, deterring potential entrants.

- Focus on Core Competencies: Suppliers generally concentrate on their primary business, such as grain farming or hop cultivation, rather than venturing into complex beverage manufacturing.

Premium Brews: The Leverage of Specialized Suppliers

While China Resources Beer benefits from a broader supplier base for common brewing ingredients, specialized suppliers of premium inputs like unique hop varieties still wield considerable bargaining power. This is particularly true as CR Beer focuses on premiumization, making consistent access to high-quality, differentiated ingredients crucial for its product strategy.

The ability to secure these specialized inputs directly impacts CR Beer's capacity to compete in the growing premium segment. In 2023, CR Beer's premium beer volume saw a notable increase, highlighting the strategic importance of ingredient sourcing for its market expansion and brand positioning.

The bargaining power of suppliers is moderated by the diversity of the market for essential brewing inputs. However, suppliers offering unique or specialized ingredients, especially those crucial for premium beer production, can still command leverage. This is amplified by China Resources Beer's strategic push into premium segments, where ingredient quality and distinctiveness are paramount for consumer appeal and brand differentiation.

| Supplier Type | Bargaining Power Factor | Impact on CR Beer |

|---|---|---|

| General Malt/Hops Suppliers | Increased competition, diverse sourcing options | Lowered bargaining power for individual suppliers |

| Specialty Hop Suppliers (e.g., US Pacific Northwest) | Unique aroma profiles, critical for craft/premium beer | Higher bargaining power due to ingredient criticality |

| Packaging Suppliers | Essential input, potential for cost fluctuations | Moderate bargaining power, dependent on CR Beer's scale and contracts |

What is included in the product

This analysis delves into the competitive forces shaping China Resources Beer (Holdings), examining supplier and buyer power, the threat of new entrants and substitutes, and the intensity of rivalry within the beer market.

Navigate the intense competition in China's beer market with a clear, one-sheet summary of all five forces, enabling quick, informed strategic decisions for China Resources Beer.

Gain a competitive edge by customizing pressure levels based on new data or evolving market trends, allowing China Resources Beer to proactively adapt its strategies.

Customers Bargaining Power

Customer Price Sensitivity

Customer price sensitivity remains a significant factor in China Resources Beer's market, particularly for its mainstream products. While premiumization is a growing trend, a substantial segment of the Chinese beer market, especially outside major urban centers, still prioritizes affordability. For instance, in 2023, the average disposable income in China was around RMB 39,000, highlighting the importance of value for a large consumer base.

China Resources Beer must navigate this by offering a diverse product portfolio. Balancing their premium Snow Master and other high-end brands with more accessible options is crucial. This strategy allows them to capture value from the premium segment while maintaining market share among price-conscious consumers. The company's ability to manage this pricing dichotomy directly impacts its overall market position and profitability.

Availability of Substitutes

The sheer variety of beverages in China, from traditional baijiu and wine to modern spirits and a rapidly expanding non-alcoholic beer market, gives consumers abundant choices. This wide selection directly translates to increased customer bargaining power.

In 2023, China's beverage market was valued at over $700 billion, with beer holding a significant but not exclusive share. The growth of the non-alcoholic beverage sector, which saw a 7% year-on-year increase in 2023, further amplifies consumer options and their ability to switch away from traditional beer products.

Customers can readily shift to alternatives if they perceive pricing or quality issues with China Resources Beer's offerings. This ease of switching, fueled by a diverse and competitive beverage landscape, means consumers hold considerable sway in the market.

Customer Information

The bargaining power of customers for China Resources Beer is growing as Chinese consumers become more sophisticated, particularly with premium and craft beer. In 2024, a significant portion of the Chinese beer market is seeing demand shift towards higher-quality and more diverse offerings, giving consumers more leverage. This increased discernment means they are less likely to accept standardized products and are actively seeking out brands that align with their evolving preferences for taste, origin, and brand story.

Volume of Purchases (Distributors/Retailers)

For China Resources Beer (Holdings), large distributors and retail chains are crucial customers, commanding significant purchasing volumes. Their substantial orders give them considerable leverage, impacting pricing and promotional strategies. In 2023, China Resources Beer reported revenue of approximately RMB 250 billion, with a substantial portion driven by these large volume buyers.

These powerful intermediaries, controlling vital shelf space and market access, can significantly influence distribution terms and product placement. Their ability to consolidate demand means they can negotiate more favorable pricing and demand specific marketing support. This dynamic places considerable bargaining power in the hands of these key customers.

- High Volume Purchases: Large distributors and retailers buy in bulk, giving them substantial influence.

- Shelf Space Control: Access to prime retail locations is a key bargaining chip.

- Market Access: These intermediaries provide essential reach to consumers.

- Negotiating Power: Their volume allows them to dictate terms on pricing and promotions.

Brand Loyalty

China Resources Beer (Holdings) benefits from significant brand loyalty, particularly with its flagship Snow Beer, which has historically held a dominant market share in China. This strong brand equity acts as a buffer against intense price competition.

However, the landscape is shifting. In 2023, the premiumization trend continued to gain traction, with consumers increasingly seeking out craft and imported beers. This diversification of tastes can erode traditional brand loyalty if companies don't adapt.

To counter this, CR Beer is strategically leveraging its diverse portfolio, including its stake in Heineken. This allows them to cater to a broader range of consumer preferences and maintain loyalty across different market segments. For instance, in 2023, Snow Beer's market share remained robust, but the growth in the premium segment, where Heineken plays a key role, was crucial for overall company performance.

- Snow Beer's historical market dominance fosters strong consumer recognition.

- Consumer shift towards craft and international premium brands presents a challenge to traditional loyalty.

- CR Beer's strategy involves utilizing its broader portfolio, including Heineken, to retain and attract customers.

- The company's ability to adapt to evolving tastes is key to sustaining brand loyalty in a dynamic market.

China's Beer Market: Customer Power Shapes Strategy

The bargaining power of customers in China's beer market is significant and growing, driven by increasing consumer sophistication and a wide array of beverage choices. This forces China Resources Beer (Holdings) to carefully manage pricing and product offerings to cater to diverse preferences.

Consumers can easily switch to alternative beverages if they are dissatisfied with pricing or quality, especially with the expanding non-alcoholic sector and a growing appreciation for craft and imported beers. For instance, the non-alcoholic beverage market saw a 7% year-on-year increase in 2023, indicating a broader competitive landscape.

Large distributors and retailers, acting as key customers, wield considerable influence due to their high-volume purchases and control over shelf space. In 2023, China Resources Beer's revenue of approximately RMB 250 billion was heavily reliant on these powerful intermediaries, allowing them to negotiate favorable terms.

While Snow Beer's strong brand loyalty provides some buffer, the trend towards premiumization and diverse tastes necessitates CR Beer's strategic use of its portfolio, including its stake in Heineken, to maintain customer appeal and market share.

| Factor | Impact on CR Beer | 2023/2024 Data Point |

| Price Sensitivity | High for mainstream products, requiring value-driven offerings. | Average disposable income in China was ~RMB 39,000 in 2023. |

| Beverage Variety | Increases consumer choice and ability to switch. | Non-alcoholic beverage market grew 7% YoY in 2023. |

| Distributor Power | Significant leverage due to volume and market access. | CR Beer's 2023 revenue ~RMB 250 billion, driven by large buyers. |

| Evolving Tastes | Demand for premium and craft beers challenges traditional loyalty. | Continued traction of premiumization trend in 2023. |

Full Version Awaits

China Resources Beer (Holdings) Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis for China Resources Beer (Holdings), detailing the competitive landscape, including threats of new entrants, bargaining power of buyers and suppliers, threat of substitutes, and intensity of rivalry. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. You can trust that this preview accurately reflects the depth and quality of the insights you will receive, providing a thorough strategic overview of the beer industry's dynamics impacting China Resources Beer.

Rivalry Among Competitors

High Market Concentration

The Chinese beer market is a prime example of high concentration. A handful of major players, including China Resources Beer (Snow Beer), Tsingtao Brewery, Budweiser, Yanjing, and Carlsberg, dominate the landscape. These giants collectively command an impressive 92.9% of the market share, leaving very little room for smaller competitors.

This intense consolidation naturally fuels fierce competition. The leading companies are locked in a constant battle for market dominance, vying for increased market share and overall growth. This rivalry shapes pricing strategies, marketing efforts, and product innovation across the sector.

Premiumization as a Key Battleground

The battle for market share in China's beer industry has dramatically shifted. It's no longer just about selling more bottles; the focus is now squarely on profitability through premiumization. Major players like China Resources Beer are heavily investing in their higher-end and craft beer offerings, recognizing the potential for greater margins in these segments.

This strategic pivot has intensified competitive rivalry. Brewers are locked in a fierce race to attract and retain consumers willing to pay more for perceived quality and unique flavors. For instance, China Resources Beer's Snow brand has been actively expanding its premium portfolio, aiming to capture a larger share of this lucrative market, which saw the premium segment grow by approximately 15% in 2023.

Strategic Partnerships and Acquisitions

Strategic partnerships and acquisitions significantly shape competitive rivalry in the beer market. China Resources Beer's notable alliance with Heineken, for instance, grants it access to coveted international premium brands and robust distribution channels, directly impacting its competitive standing.

These strategic moves, including mergers and acquisitions, serve to consolidate market power and enhance product portfolios for major players. This often leads to a more concentrated market, where a few dominant companies leverage these alliances to further differentiate themselves and gain an edge over smaller competitors.

Marketing and Distribution Network

China Resources Beer (Holdings) benefits from an incredibly strong marketing and distribution network, a significant factor in its competitive rivalry. Established players like CR Beer have invested heavily in building out extensive sales channels and brand recognition, making it challenging for newcomers to gain traction. For instance, CR Beer's market share in China reached approximately 23.2% by the end of 2023, underscoring the effectiveness of its established presence.

This robust infrastructure acts as a substantial barrier to entry. Smaller or newer competitors often find it difficult and costly to replicate the reach and brand visibility that CR Beer already commands. The sheer scale of their distribution, reaching even remote areas, coupled with substantial marketing budgets, creates a formidable challenge for any aspiring rival seeking to carve out a significant market share.

- Extensive Distribution: CR Beer's network covers a vast portion of China, ensuring product availability across diverse geographical regions.

- Brand Dominance: Significant marketing investments have cultivated strong brand loyalty and awareness, a key differentiator.

- Barrier to Entry: The cost and complexity of matching CR Beer's distribution and marketing reach deter new entrants.

- Market Share: CR Beer held a leading market share in China's beer industry, estimated at over 23% in 2023, reflecting its competitive strength.

Mature Market Dynamics

The Chinese beer market, while seeing some growth in premium segments, has faced overall volume declines in recent years. This maturity forces competitors like China Resources Beer to concentrate on value growth and capturing market share within specific categories, rather than just increasing total sales volume. For instance, while overall beer sales might be flat or declining, the premium segment continues to expand, offering a battleground for brand loyalty and higher margins.

- Intensified Competition for Value: With overall volume contraction, companies are fiercely competing for existing consumers, driving a focus on premiumization and innovation to capture higher value.

- Innovation as a Differentiator: The need to stand out in a mature market pushes for new product development, unique marketing campaigns, and enhanced distribution strategies.

- Market Share Battles: Competitors are actively vying for dominance in specific segments, leading to aggressive pricing and promotional activities.

- Focus on Profitability: Beyond volume, the emphasis shifts to improving profit margins through cost efficiencies and a stronger product mix.

Fierce Competition Brews in China's Beer Market

Competitive rivalry in China's beer market is intense, with a few dominant players like China Resources Beer (Snow Beer), Tsingtao, and Budweiser controlling over 90% of the market share. This high concentration means companies are constantly fighting for market dominance, focusing on premiumization and innovation to attract consumers willing to pay more. China Resources Beer's market share reached approximately 23.2% by the end of 2023, highlighting its strong position amidst this fierce competition.

| Competitor | Estimated Market Share (End of 2023) | Key Strategy |

|---|---|---|

| China Resources Beer (Snow) | ~23.2% | Premiumization, expanding craft beer portfolio, strategic partnerships (e.g., Heineken) |

| Tsingtao Brewery | ~15.7% | Brand revitalization, international expansion, focus on quality |

| Budweiser Brewing Company APAC | ~16.3% | Leveraging global brands, premium offerings, strong distribution |

| Yanjing Brewery | ~7.1% | Regional strength, cost leadership, expanding product lines |

| Carlsberg Group | ~5.0% | Integration of acquired brands, premiumization, market penetration |

SSubstitutes Threaten

Other Alcoholic Beverages

Traditional Chinese alcoholic beverages, such as baijiu, along with spirits and wine, represent substantial substitutes for beer. These alternatives often cater to formal dining settings or specific social rituals where beer might be perceived as less appropriate. For instance, baijiu, a distilled spirit, holds deep cultural significance and is frequently consumed during banquets and important celebrations.

While beer is a favored choice for casual social events and everyday consumption, the availability of a wide array of alcoholic drinks means consumers aren't limited to just beer. In 2023, the Chinese spirits market, particularly baijiu, continued to demonstrate robust growth, with major players reporting strong revenue increases, indicating a sustained consumer preference for these categories in specific contexts.

Non-Alcoholic Beverages

The increasing health consciousness in China, particularly among younger consumers, is a significant factor driving demand for non-alcoholic beverages. This trend directly impacts the beer market as consumers opt for healthier alternatives like non-alcoholic beers, juices, and other functional drinks.

In 2024, the market for non-alcoholic beverages in China continued its robust growth. For instance, sales of low-alcohol and no-alcohol beer segments saw double-digit percentage increases year-over-year, indicating a clear shift in consumer preference away from traditional alcoholic options.

Emergence of New Categories

The beverage market is dynamic, with new categories like ready-to-drink (RTD) alcoholic beverages and sparkling wines gaining traction. These products cater to consumers looking for novel and often less intense alcoholic options, directly impacting traditional beer consumption.

In 2024, the global RTD market continued its robust expansion, with projections indicating a compound annual growth rate (CAGR) of over 10% through 2028. This growth signifies a significant diversion of consumer spending away from established categories like beer, presenting a clear threat of substitution for companies like China Resources Beer.

Changing Lifestyle Preferences

Younger Chinese consumers are increasingly seeking diverse experiences beyond traditional social drinking. This shift means that while beer remains popular, alternatives like craft spirits, non-alcoholic beverages, and even participation in fitness or cultural events compete for consumer time and disposable income. For China Resources Beer, this evolving lifestyle presents a threat as consumers may allocate less spending to beer.

By 2024, the trend towards experiential consumption is evident. For instance, the growth in the health and wellness sector, including specialized fitness studios and outdoor activities, draws consumer interest and spending away from alcohol. This means that the perceived value of a beer purchase must increasingly compete with the value derived from these alternative leisure pursuits.

- Shifting Beverage Preferences: Younger demographics in China are exploring a wider array of drinks, including craft beers, premium spirits, and sophisticated non-alcoholic options, diversifying their choices beyond mass-market lagers.

- Rise of Experiential Consumption: Consumer spending is increasingly directed towards experiences such as travel, entertainment, and wellness activities, potentially reducing the share of wallet allocated to traditional beverage consumption like beer.

- Health and Wellness Focus: A growing emphasis on health and well-being influences beverage choices, with a segment of consumers actively seeking lower-alcohol or alcohol-free alternatives, posing a direct substitute to traditional beer.

Price-Performance Trade-off

Consumers often weigh a beverage's price against its perceived quality and benefits. This price-performance trade-off is crucial. For instance, China Resources Beer faces competition from a growing array of non-alcoholic beverages.

The market offers increasingly sophisticated premium non-alcoholic beers, alongside more budget-friendly non-alcoholic options. This variety allows consumers to select substitutes that better fit their financial constraints, health aspirations, or specific social settings, potentially influencing overall beer consumption.

- Price Sensitivity: Consumers are increasingly mindful of the price-performance ratio across all beverage categories.

- Non-Alcoholic Alternatives: The rise of premium non-alcoholic beers and affordable non-alcoholic options provides viable substitutes.

- Health and Lifestyle Trends: Growing health consciousness encourages consumers to explore alternatives to traditional alcoholic beverages.

- Substitution Impact: These substitutes can directly impact demand for traditional beer products, especially for price-conscious or health-focused consumers.

Beer's New Rivals: Spirits, RTDs, and Non-Alcoholic Drinks Reshape Market

Traditional alcoholic beverages like baijiu and wine, alongside a growing non-alcoholic segment, present significant substitution threats to beer. These alternatives cater to diverse occasions and evolving consumer preferences, particularly among younger demographics in China.

The robust growth in China's spirits market in 2023, with major players reporting strong revenue increases, highlights the enduring appeal of baijiu in formal settings. Simultaneously, the non-alcoholic beverage market saw double-digit percentage growth in low- and no-alcohol beer segments in 2024, indicating a clear shift for health-conscious consumers.

The global ready-to-drink (RTD) market's projected CAGR of over 10% through 2028 further diversifies beverage choices, drawing spending away from traditional beer. This dynamic market landscape, coupled with a rise in experiential consumption and a focus on wellness, means beer must increasingly compete for consumer attention and disposable income.

| Beverage Category | 2023/2024 Trend | Impact on Beer |

|---|---|---|

| Baijiu & Spirits | Robust growth, strong revenue increases reported by major players in 2023. | Strong substitute for formal occasions and cultural events. |

| Non-Alcoholic Beverages | Double-digit YoY growth in low/no-alcohol beer segments in 2024. | Directly competes with beer for health-conscious consumers. |

| Ready-to-Drink (RTD) | Projected CAGR >10% through 2028 globally. | Offers novel, less intense alcoholic options, diverting consumer spending. |

Entrants Threaten

High Capital Requirements

Establishing a brewing operation that can truly compete with China Resources Beer's massive scale demands significant capital. We're talking about substantial investments in state-of-the-art production facilities, advanced brewing technology, and building out extensive distribution networks across China. For instance, the capital expenditure for a new, large-scale brewery can easily run into hundreds of millions of dollars, making it a formidable barrier.

Established Brand Loyalty and Distribution

China Resources Beer enjoys formidable brand loyalty, particularly with its flagship Snow Beer, which held a significant market share in China. In 2023, Snow Beer's market share remained a dominant force, making it incredibly difficult for newcomers to gain traction.

The company's deeply entrenched distribution network across China presents another substantial barrier. New entrants would struggle to replicate this reach, which ensures Snow Beer products are readily available even in remote areas, a feat that requires massive investment and time to build.

Economies of Scale

China Resources Beer, like other major players, benefits immensely from economies of scale. This means they can produce beer more cheaply per unit because they operate at a massive volume. For instance, their extensive distribution network across China allows for highly efficient logistics, a significant cost advantage that is difficult for newcomers to replicate.

New entrants face a substantial hurdle in matching these cost efficiencies. To achieve similar economies of scale in production and procurement, a new brewer would need to invest heavily upfront, making it challenging to compete on price with established giants like China Resources Beer. This cost disadvantage directly impacts their ability to achieve comparable profit margins from the outset.

Government Regulations

Government regulations in China's beer market present a significant barrier to new entrants. For instance, stringent requirements for filtering and pasteurizing domestically produced bottled beer add complexity and cost for aspiring brewers. In 2024, these types of compliance measures continue to favor established players with existing infrastructure, making it harder for smaller, emerging craft breweries to gain a foothold.

These regulatory hurdles can disproportionately impact smaller, aspiring craft brewers who may lack the capital and scale to meet demanding standards. Additionally, potential high minimum production thresholds for commercial brewing further solidify the advantage of incumbent companies. This regulatory landscape effectively limits the number of new companies that can realistically enter and compete in the market.

Key regulatory considerations include:

- Mandatory Filtering and Pasteurization: Compliance with these processes requires significant investment in equipment and operational expertise.

- Production Thresholds: Minimum production volumes can exclude smaller craft brewers from legally operating at scale.

- Licensing and Permitting: Navigating the complex web of licenses and permits adds another layer of difficulty for new entrants.

Intense Competition from Incumbents

The threat of new entrants for China Resources Beer (Holdings) is significantly mitigated by the intensely competitive landscape already dominated by established players. The Chinese beer market, particularly the premium segment, is characterized by ongoing consolidation, making it difficult for newcomers to gain traction. Incumbents possess substantial resources, strategic agility, and deep market experience, enabling them to effectively defend and expand their existing market shares.

New entrants must contend with significant barriers to entry:

- Established Brand Loyalty: Major players like China Resources Beer have cultivated strong brand recognition and consumer loyalty over years of operation.

- Economies of Scale: Existing large-scale production facilities and distribution networks provide cost advantages that new entrants struggle to match. For instance, in 2023, China Resources Beer reported a sales volume of 12.13 million kiloliters, highlighting their significant operational scale.

- Distribution Network Access: Securing widespread and efficient distribution channels across China is a formidable challenge for any new participant.

- Capital Requirements: The substantial investment needed for manufacturing, marketing, and distribution makes entering the market a capital-intensive endeavor.

China Beer Market: High Barriers Protect Incumbents

The threat of new entrants in China's beer market is relatively low for China Resources Beer due to substantial capital requirements and established brand loyalty. Newcomers face immense hurdles in replicating the scale of production and the extensive distribution networks that giants like China Resources Beer have built over decades. For example, in 2023, China Resources Beer's sales volume reached 12.13 million kiloliters, underscoring their dominant operational scale.

Furthermore, government regulations, such as mandatory filtering and pasteurization, add complexity and cost, favoring incumbents with existing infrastructure. These factors, combined with the cost efficiencies derived from economies of scale, make it exceptionally difficult for new players to compete effectively on price or reach. The market's ongoing consolidation also means that established players are well-positioned to defend their market share against emerging competitors.

| Barrier | Impact on New Entrants | China Resources Beer Advantage (2023/2024 Data) |

|---|---|---|

| Capital Requirements | Extremely High | Operates at massive scale, enabling significant cost efficiencies. |

| Brand Loyalty | High | Snow Beer is a dominant brand with strong consumer recognition. |

| Distribution Network | Challenging to Replicate | Extensive reach across China, ensuring product availability. |

| Economies of Scale | Significant Cost Disadvantage | Lower per-unit production costs due to high volume. |

| Government Regulations | Increased Compliance Costs | Existing infrastructure facilitates compliance with standards. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for China Resources Beer (Holdings) is built upon a foundation of publicly available financial reports, including annual and interim statements. We also incorporate insights from industry-specific market research reports and data from financial news outlets to capture competitive dynamics.